Professional ethics and the Tax Professional-Module 2

Jan Dijkman

BA LLB LLM H Dip Tax Adv Dip Labour Law Certified Ethics Officer

Agenda

What is ethics?

Why is ethics important for Tax Professionals?

Professions and ethics

The Code of Professional Conduct in Relation to Taxation

Fundamental principles

Disciplinary trends

Solving ethical dilemmas – some guidelines

Final thoughts

Agenda for Module 2

What is ethics?

Why is ethics important for Tax Professionals?

Professions and ethics

The Code of Professional Conduct in Relation to Taxation

Fundamental principles

Disciplinary trends

Solving ethical dilemmas – some guidelines

Final thoughts

What is ethics?

Ethical behaviour is when one does not merely consider what is good for oneself, but also considers what is good for others

Conundrum

Understanding ethics is easy, being ethical isn’t

Why is ethics important for Tax Professionals?

Integrity is the basis of a sound tax system

Integrity means that a person acts on principle

The ‘Golden Rule’ of ethics

Why is ethics important for Tax Professionals?

Professional ethics

The norms and guidelines for moral and ethical behaviour for professionals. Guidelines for professional ethics are usually codified in codes of ethics or codes of professional conduct

Why do we need an ethics code?

Because of diverse make-up of profession, need exists for common understanding of ethics

Hence the Code of Professional Conduct

Characteristic of a profession that there is a commitment to ethical behaviour

The Code of Professional Conduct in Relation to Taxation

What is the purpose of the SAIT Code?

Provides guidance on proper conduct for Tax Professionals

Adherence to the Code assists in protecting the public interest

Assists Tax Professionals to resist pressure to violate the Code

Provides a mechanism by which action can be taken against unethical conduct by Tax Professionals

Helps to achieve the objectives of the Tax Profession

Fundamental principles

Integrity

Objectivity

Professional competence and due care

Confidentiality

Professional behaviour

Professional behaviour

Principle imposes an obligation to comply with relevant laws and regulations and avoid any action that he/she knows or should know may bring discredit to the profession

Professional behaviour – Tax planning and tax avoidance

Tax avoidance is legal, tax evasion is not

Carefully consider and document considerations and advice given to clients

All taxpayers have the right to arrange their affairs under the law to minimise their tax liability

Concealment

Artificial and contrived schemes

Professional behaviour – Files and working papers

Keep proper working papers and files – comply with relevant Tax Standards

Compulsory to perform a critical evaluation of information submitted by the client

Retention of records (liens)

Types of liens

Requirements for the operation of the lien

Extent of the lien

Divisibility of fees

Professional behaviour –Money laundering

Tax Professionals must consider the money laundering statutory reporting requirements

Tax-related offences involve evasion, not avoidance, and proceeds must be treated in accordance with the applicable AML / FT legislation

What are the Tax Professional’s obligations wrt to AML / FT?

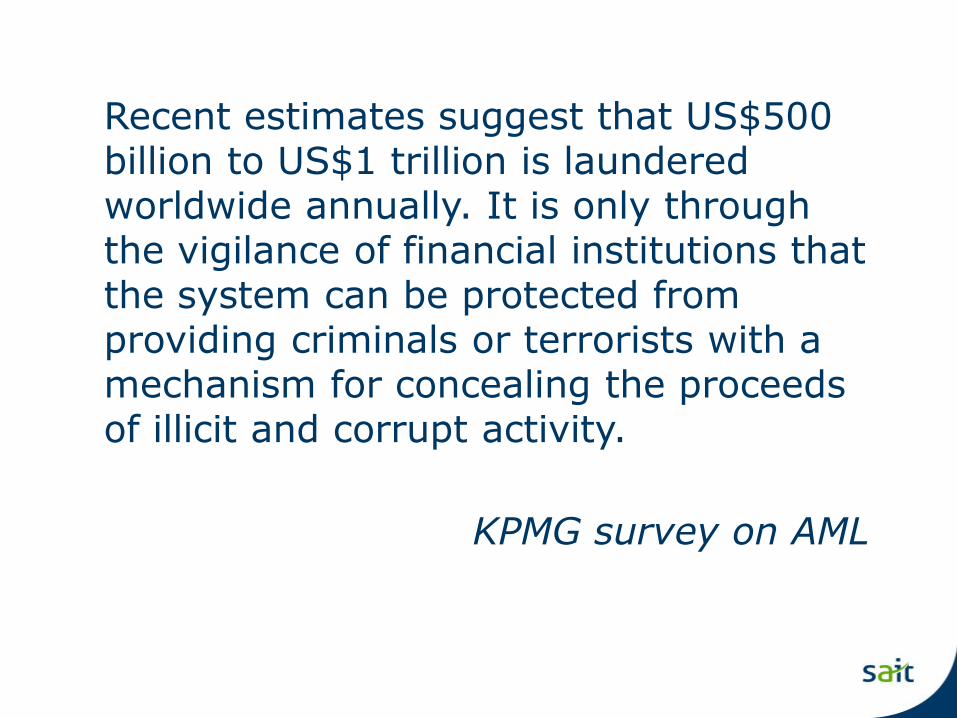

Recent estimates suggest that US$500 billion to US$1 trillion is laundered worldwide annually. It is only through the vigilance of financial institutions that the system can be protected from providing criminals or terrorists with a mechanism for concealing the proceeds of illicit and corrupt activity.

KPMG survey on AML

What is money laundering?

Money laundering is the process by which criminals attempt to hide and disguise the true origin and ownership of the proceeds of their criminal activities, thereby avoiding prosecution, conviction and confiscation of the criminal funds

COMMONLY REFERRED TO AS THE “PROCEEDS OF CRIME” CRIME

The three c’s of money laundering

Convert - illicit cash to another asset

Conceal - the true source or ownership of the criminal proceeds

Create - the perception of legitimacy for the criminal proceeds

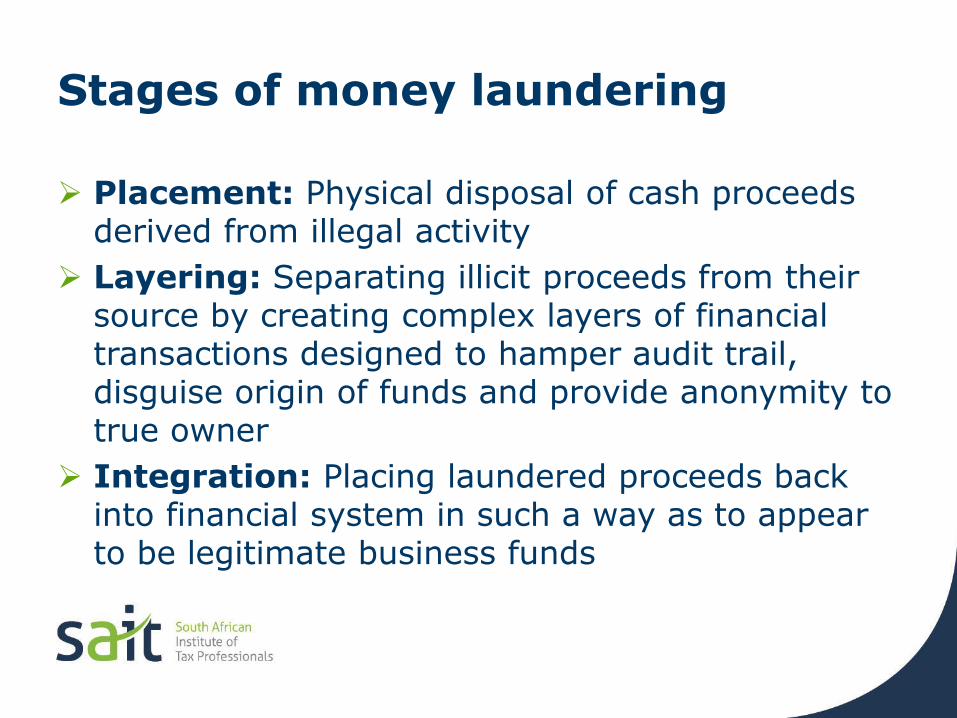

Stages of money laundering

Placement: Physical disposal of cash proceeds derived from illegal activity

Layering: Separating illicit proceeds from their source by creating complex layers of financial transactions designed to hamper audit trail, disguise origin of funds and provide anonymity to true owner

Integration: Placing laundered proceeds back into financial system in such a way as to appear to be legitimate business funds

The expanded crime of money laundering

September 11, 2001 changed the way traditional money laundering (proceeds of crime) was viewed by the international community. Money laundering was expanded to include the use of legal funds for illegal purposes (i.e. terrorist financing and tax evasion)

COMMONLY REFERRED TO AS THE “PROCEEDS FOR CRIME” CRIME

Developing trends in money laundering

General Trends

Becoming more sophisticated

Concealment within business structures

Misuse of legitimate businesses

Use of false identities or documents

Exploiting international jurisdictional issues

Use of anonymous asset types

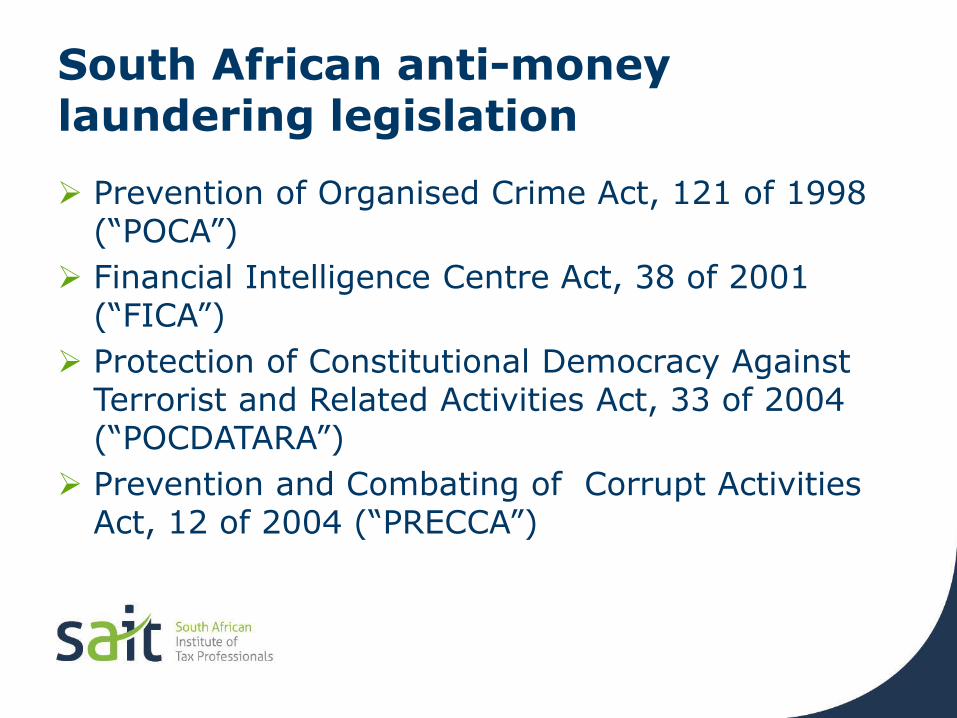

South African anti-money laundering legislation

Prevention of Organised Crime Act, 121 of 1998 (“POCA”)

Financial Intelligence Centre Act, 38 of 2001 (“FICA”)

Protection of Constitutional Democracy Against Terrorist and Related Activities Act, 33 of 2004 (“POCDATARA”)

Prevention and Combating of Corrupt Activities Act, 12 of 2004 (“PRECCA”)

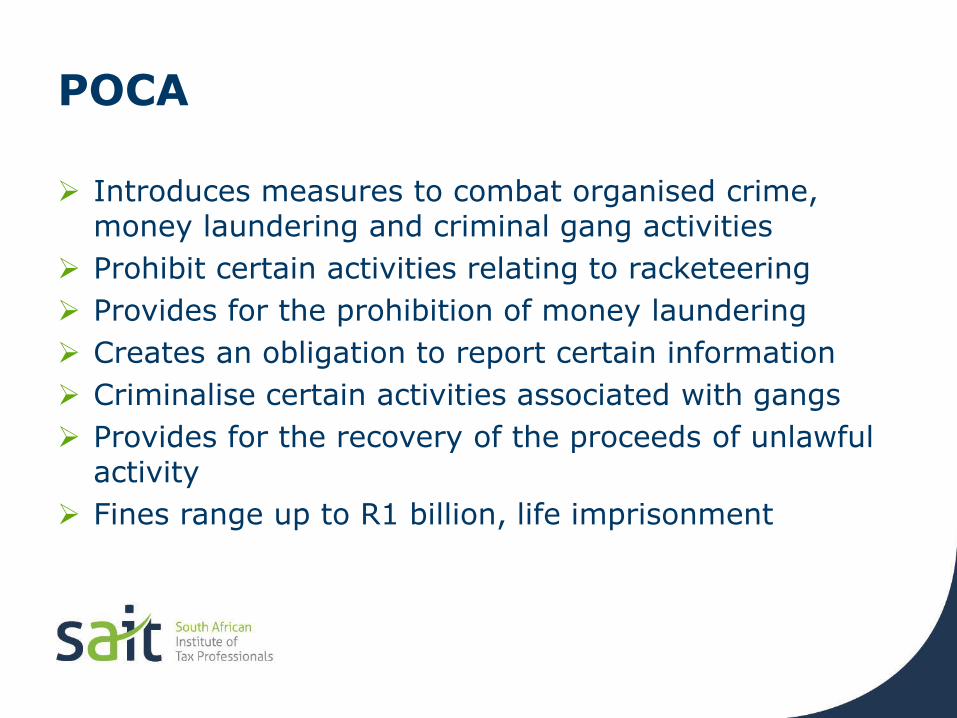

POCA

Introduces measures to combat organised crime, money laundering and criminal gang activities

Prohibit certain activities relating to racketeering

Provides for the prohibition of money laundering

Creates an obligation to report certain information

Criminalise certain activities associated with gangs

Provides for the recovery of the proceeds of unlawful activity

Fines range up to R1 billion, life imprisonment

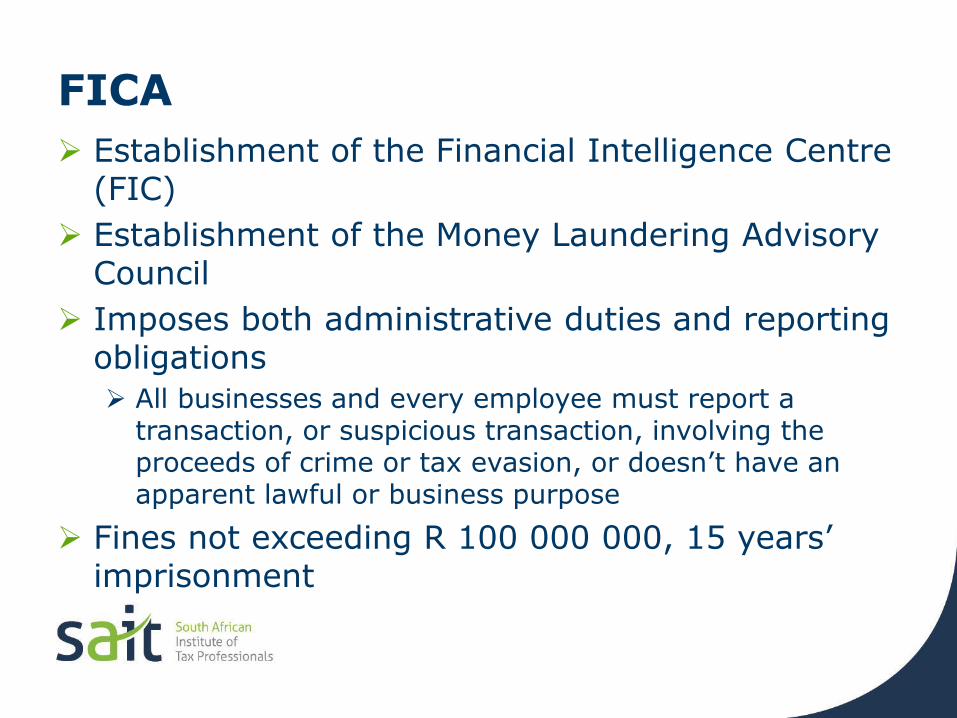

FICA

Establishment of the Financial Intelligence Centre (FIC)

Establishment of the Money Laundering Advisory Council

Imposes both administrative duties and reporting obligations

All businesses and every employee must report a transaction, or suspicious transaction, involving the proceeds of crime or tax evasion, or doesn’t have an apparent lawful or business purpose

Fines not exceeding R 100 000 000, 15 years’ imprisonment

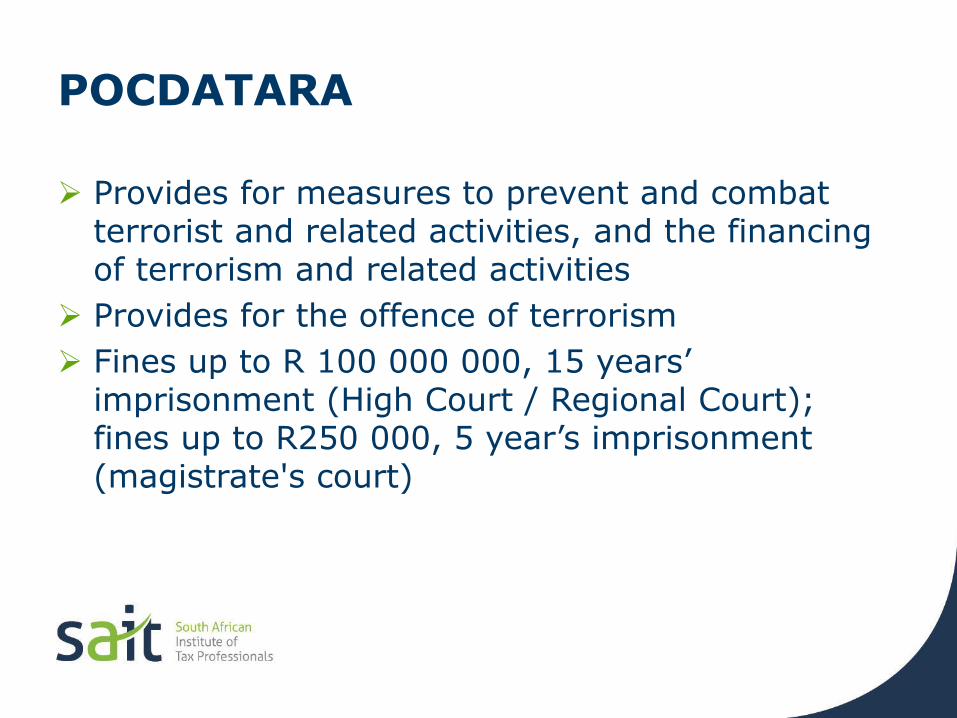

POCDATARA

Provides for measures to prevent and combat terrorist and related activities, and the financing of terrorism and related activities

Provides for the offence of terrorism

Fines up to R 100 000 000, 15 years’ imprisonment (High Court / Regional Court); fines up to R250 000, 5 year’s imprisonment (magistrate's court)

PRECCA

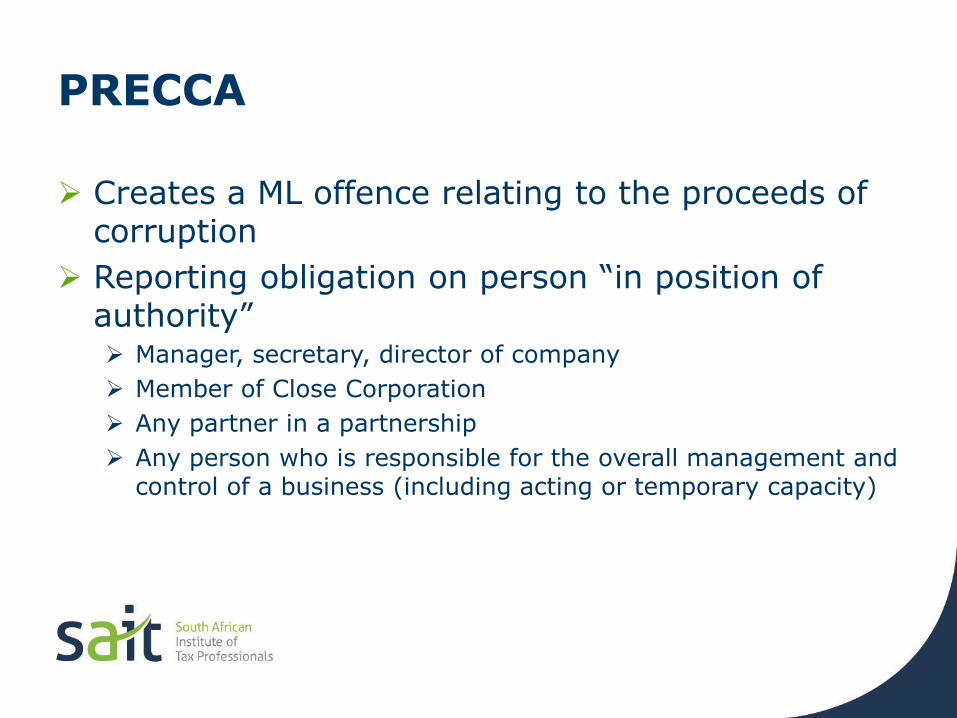

Creates a ML offence relating to the proceeds of corruption

Reporting obligation on person “in position of authority” Manager, secretary, director of company

Member of Close Corporation

Any partner in a partnership

Any person who is responsible for the overall management and control of a business (including acting or temporary capacity)

PRECCA (2)

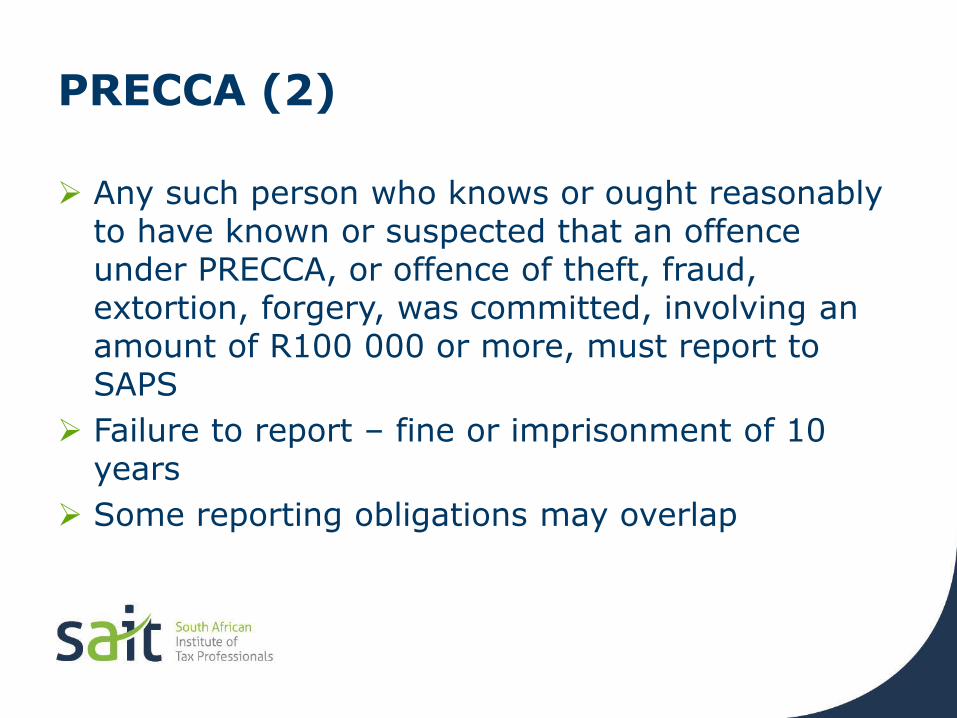

Any such person who knows or ought reasonably to have known or suspected that an offence under PRECCA, or offence of theft, fraud, extortion, forgery, was committed, involving an amount of R100 000 or more, must report to SAPS

Failure to report – fine or imprisonment of 10 years

Some reporting obligations may overlap

AML/FT obligations

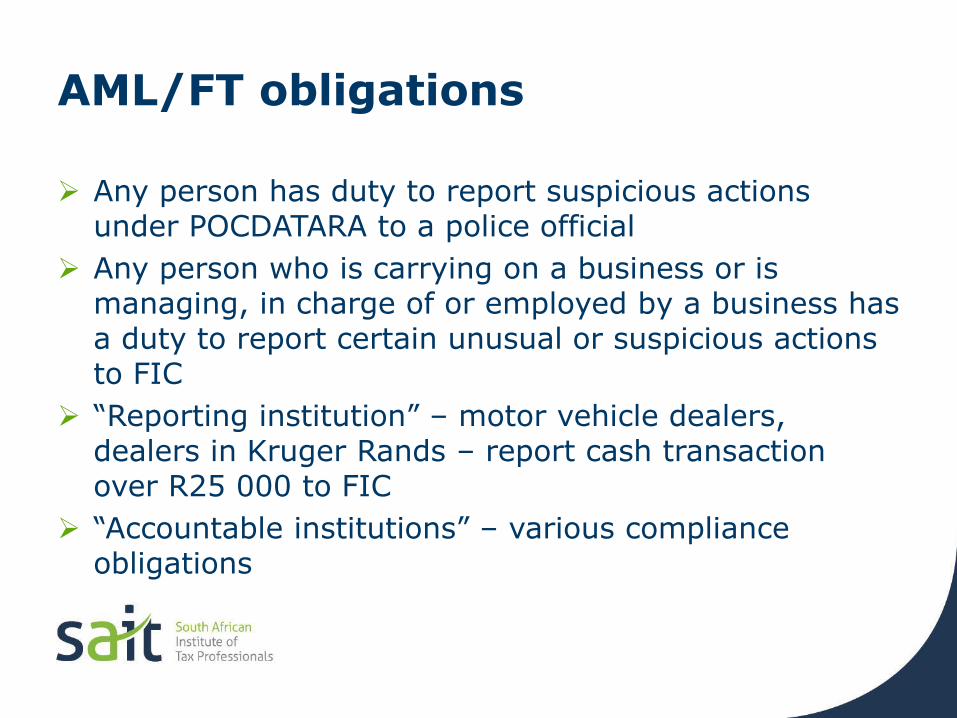

Any person has duty to report suspicious actions under POCDATARA to a police official

Any person who is carrying on a business or is managing, in charge of or employed by a business has a duty to report certain unusual or suspicious actions to FIC

“Reporting institution” – motor vehicle dealers, dealers in Kruger Rands – report cash transaction over R25 000 to FIC

“Accountable institutions” – various compliance obligations

AML/FT obligations – General businesses

Includes practice of Tax Professional

Sec 29 FICA stipulates that any person: Who carries on a business

Who is in charge of or manages a business

Who is employed by a business

Has a duty to report to the FIC if the person knows, suspects or ought reasonably to have suspected that: The business has received or is about to receive the proceeds

of unlawful activities, etc;

AML/FT obligations – General businesses

Has a duty to report to the FIC if the person knows, suspects or ought reasonably to have suspected that: A transaction or series of transactions which the business is

party to:

Facilitated the transfer of proceeds of unlawful activities;

Has no apparent business or lawful purpose;

Is conducted to avoid the FIC reporting threshold;

May be related to the investigation of an evasion or attempted evasion of any SARS tax, duty, or levy

The business has been used or is about to be used for ML or FT purposes

AML/FT obligations – General businesses

The bottom line is that any money, property or interest which was derived from, or can be linked to, an offence committed in South Africa or elsewhere, is tainted property that may require a report to be filed for AML / FT purposes

AML/FT obligations – General businesses – filing a report

May not disclose fact that report has been made to client or any other person

Report must be made as soon as possible but not later than 15 business days after became aware of facts requiring to be reported

Report to be filed electronically direct to FIC

http://www.fic.gov.za

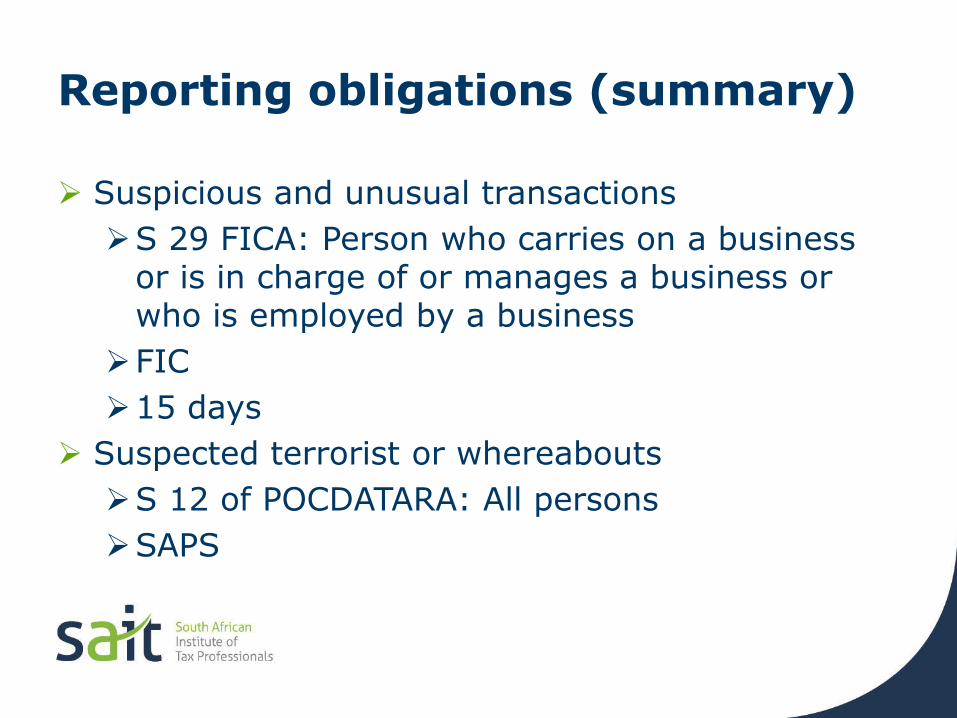

Reporting obligations (summary)

Suspicious and unusual transactions

S 29 FICA: Person who carries on a business or is in charge of or manages a business or who is employed by a business

FIC

15 days

Suspected terrorist or whereabouts

S 12 of POCDATARA: All persons

SAPS

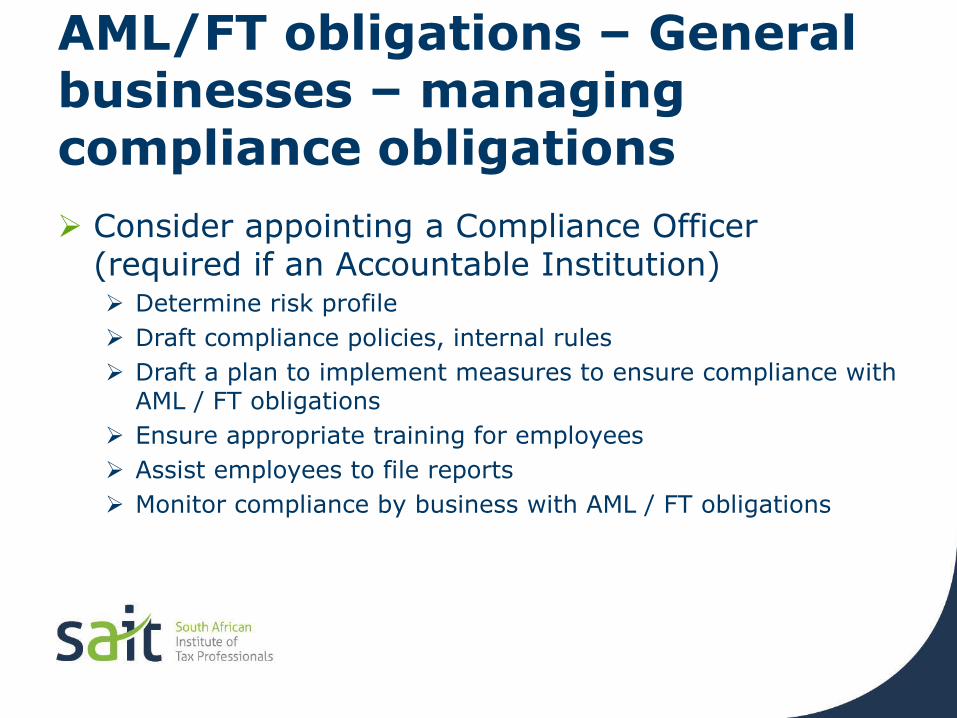

AML/FT obligations – General businesses – managing compliance obligations

Consider appointing a Compliance Officer (required if an Accountable Institution) Determine risk profile

Draft compliance policies, internal rules

Draft a plan to implement measures to ensure compliance with AML / FT obligations

Ensure appropriate training for employees

Assist employees to file reports

Monitor compliance by business with AML / FT obligations

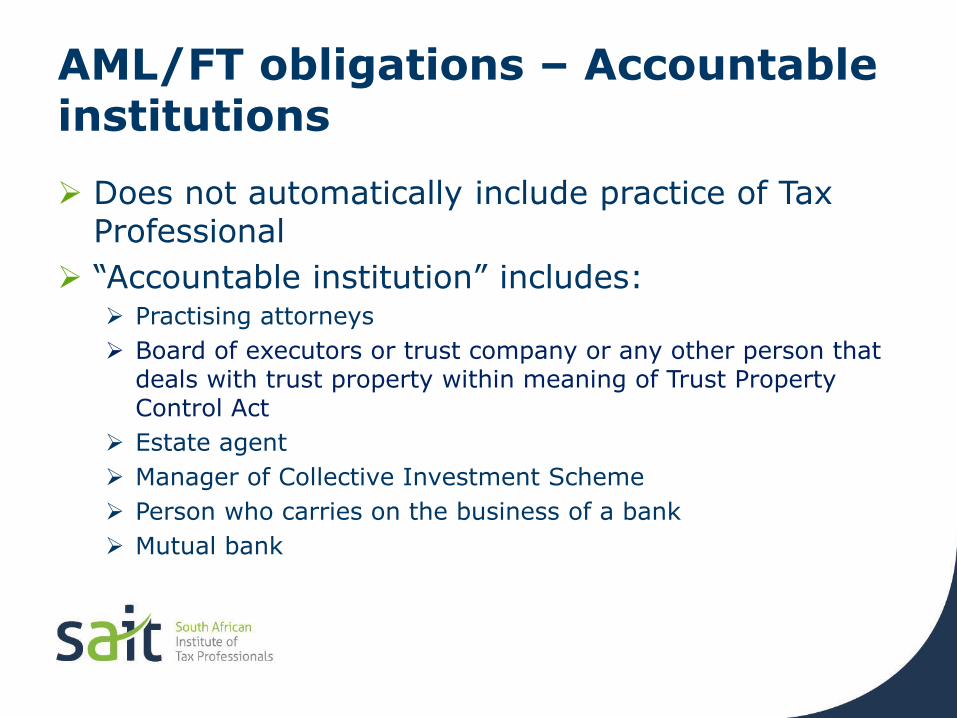

AML/FT obligations – Accountable institutions

Does not automatically include practice of Tax Professional

“Accountable institution” includes: Practising attorneys

Board of executors or trust company or any other person that deals with trust property within meaning of Trust Property Control Act

Estate agent

Manager of Collective Investment Scheme

Person who carries on the business of a bank

Mutual bank

AML/FT obligations – Accountable institutions

“Accountable institution” includes: Person who carries on long-term insurance business

Person who carries on business of making available a gambling activity in respect of which a license is required

Person who carries on business of dealing in foreign exchange

Person who carries on business of lending money against the security of securities

Person who carries on the business of a financial services provider requiring authorisation under FAIS Act

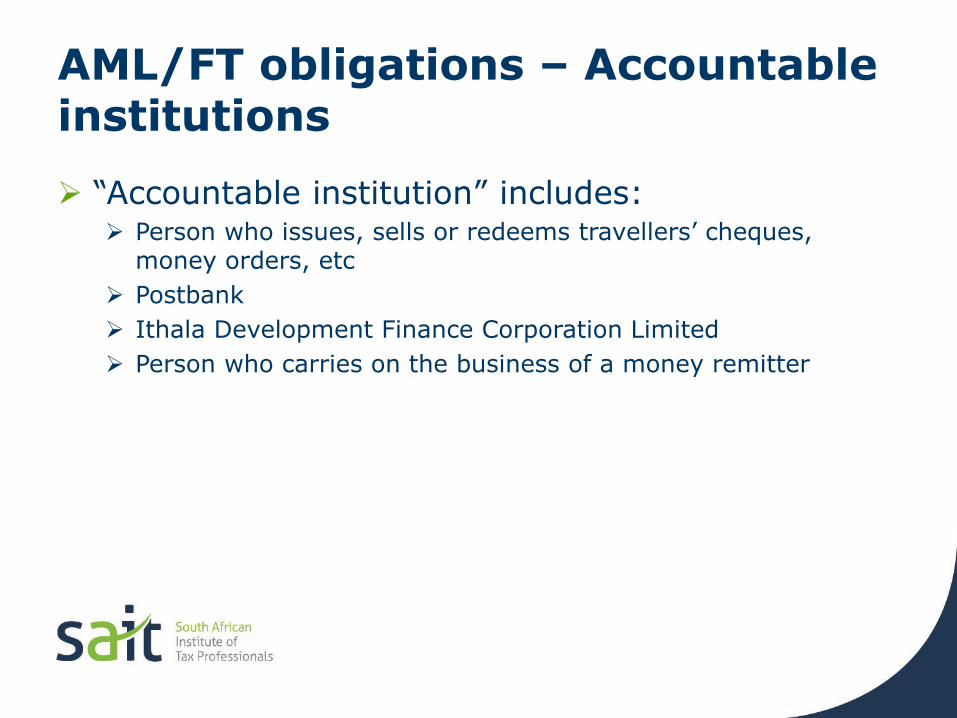

AML/FT obligations – Accountable institutions

“Accountable institution” includes: Person who issues, sells or redeems travellers’ cheques,

money orders, etc

Postbank

Ithala Development Finance Corporation Limited

Person who carries on the business of a money remitter

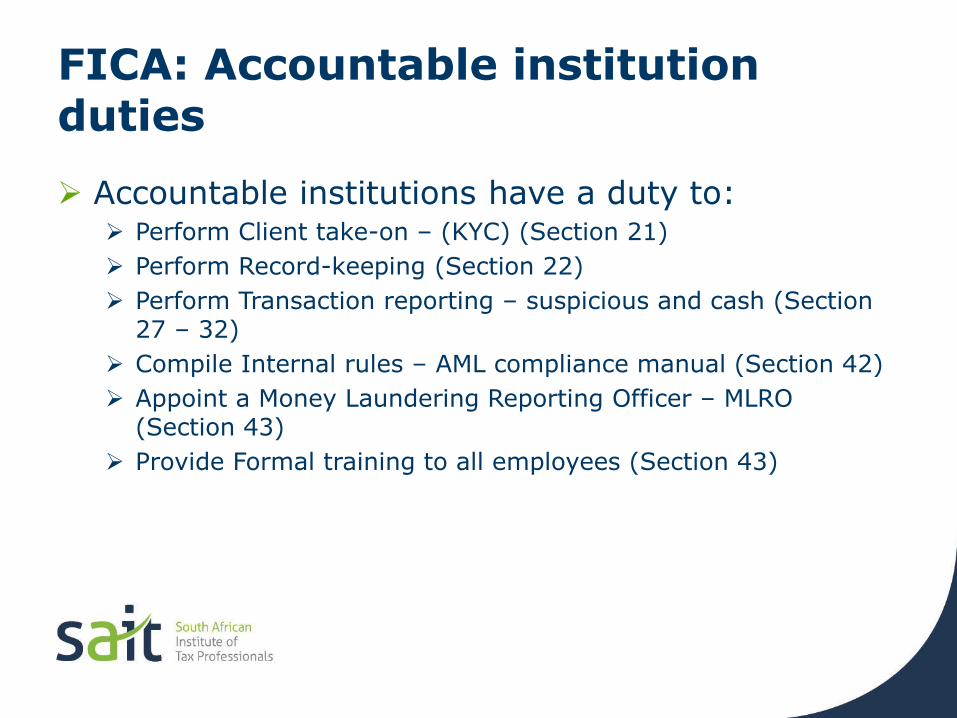

FICA: Accountable institution duties

Accountable institutions have a duty to: Perform Client take-on – (KYC) (Section 21)

Perform Record-keeping (Section 22)

Perform Transaction reporting – suspicious and cash (Section 27 – 32)

Compile Internal rules – AML compliance manual (Section 42)

Appoint a Money Laundering Reporting Officer – MLRO (Section 43)

Provide Formal training to all employees (Section 43)

Factors which may indicate ML (1)

Where client may be involved: Transactions which lack commercial logic

Transactions conducted outside the normal course of business, or where method of payment/receipt is not usual business practice

Transactions where there is a lack of information or explanation or unsatisfactory explanation

Transactions that are undervalued or overvalued, including double billing

Transactions with companies whose identity or ownership is difficult to establish

Factors which may indicate ML (2)

Where client may be involved: Unusually complex group structures where complexity does

not appear to be warranted

Abnormally extensive or unusual related party transactions

Unusual number of cash transactions for substantial amounts or a large number of small transactions

Payment for unspecified services

Formation of companies or trusts with no apparent commercial or other purpose

Long delays in the production of company accounts for no apparent reason

Factors which may indicate ML (3)

Where client may unknowingly be a party to ML: A customer establishing a pattern of small transactions and

then having one or two substantially larger ones

Unusual transactions or a pattern of trading with one customer that is different from the norm

Requests for settlement of sales in cash

Taking out of single premium life assurance policies, with subsequent early cancellation and encashment

Customer setting up a transaction that appears to be of no commercial advantage or logic

Factors which may indicate ML (4)

Where client may unknowingly be a party to ML: Customer requesting special arrangements for vague purposes

Unusual transactions with companies registered overseas

Requests for settlement in bank accounts or jurisdictions, which would be unusual for a normal commercial transaction

Excessive overpayment of accounts, subsequently requesting a refund

Professional behaviour – Publicity, advertising and solicitation

Publicity and advertising i.e. Marketing of all services and products by the Tax Professional is permitted

Material should be prepared with a due sense of responsibility to the tax profession and the public

Must conform to accepted norms of legality, decency, honesty and truthfulness

Should not bring profession into disrepute

Must be truthful and honest

No exaggerated claims

No disparaging references or comparisons

Direct mailing permitted, but must cease if requested to do so

Professional behaviour –Responsibilities to colleagues

Conduct must promote co-operation and good relations between fellow Tax Professionals, and broader accountancy, legal and tax professions

Exercise professional courtesy – remember ethics ‘Golden Rule’

Not allowed to criticise another professional

Take care in manner in which other professionals’ clients are taken over

Professional behaviour – Tax compliance

Tax Professionals must be compliant in their personal tax affairs before attempting to advise or assist the public

Need to submit annual tax clearance certificate to SAIT by 31 January

Professional behaviour - Fees

Fees must be commensurate with the nature and complexity of the task at hand

Charging of a contingency fee for the completion of tax returns is not an acceptable form of remuneration

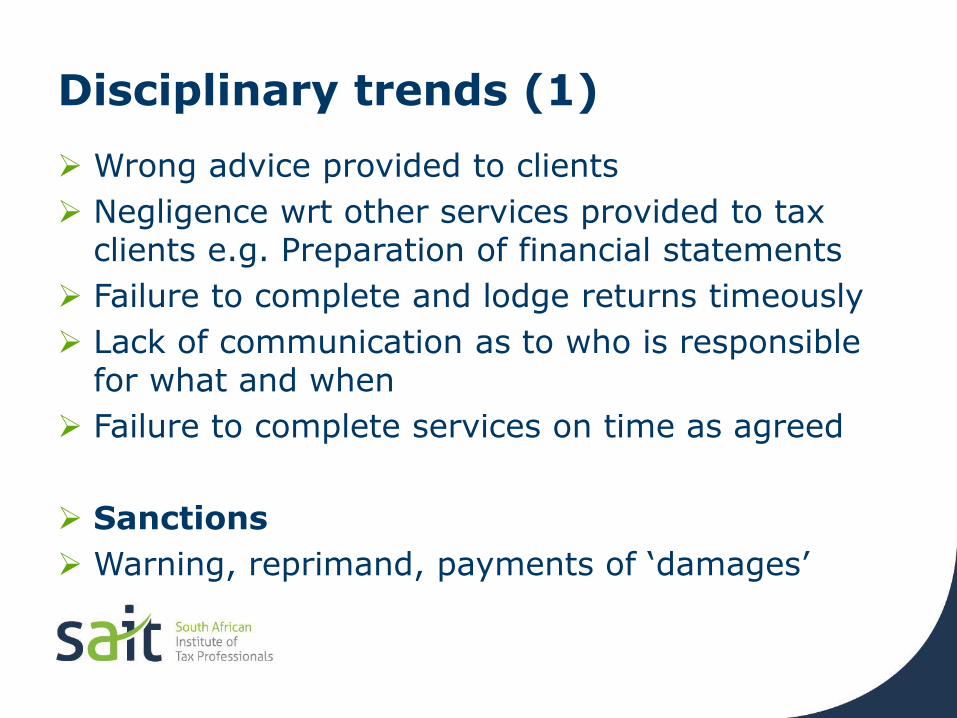

Disciplinary trends (1)

Wrong advice provided to clients

Negligence wrt other services provided to tax clients e.g. Preparation of financial statements

Failure to complete and lodge returns timeously

Lack of communication as to who is responsible for what and when

Failure to complete services on time as agreed

Sanctions

Warning, reprimand, payments of ‘damages’

Disciplinary trends (2)

General disagreement, escalating to fee dispute

Improper retention of documents and e-filing profile

Sanctions

Suspension of membership

Charging of contingency fees / percentage of refund

Possible sanctions

Reprimand, fine, suspension or termination of membership

Disciplinary trends (3)

Allegations of forging / falsifying documents

Misappropriation of money paid to Tax Professional for specific purpose

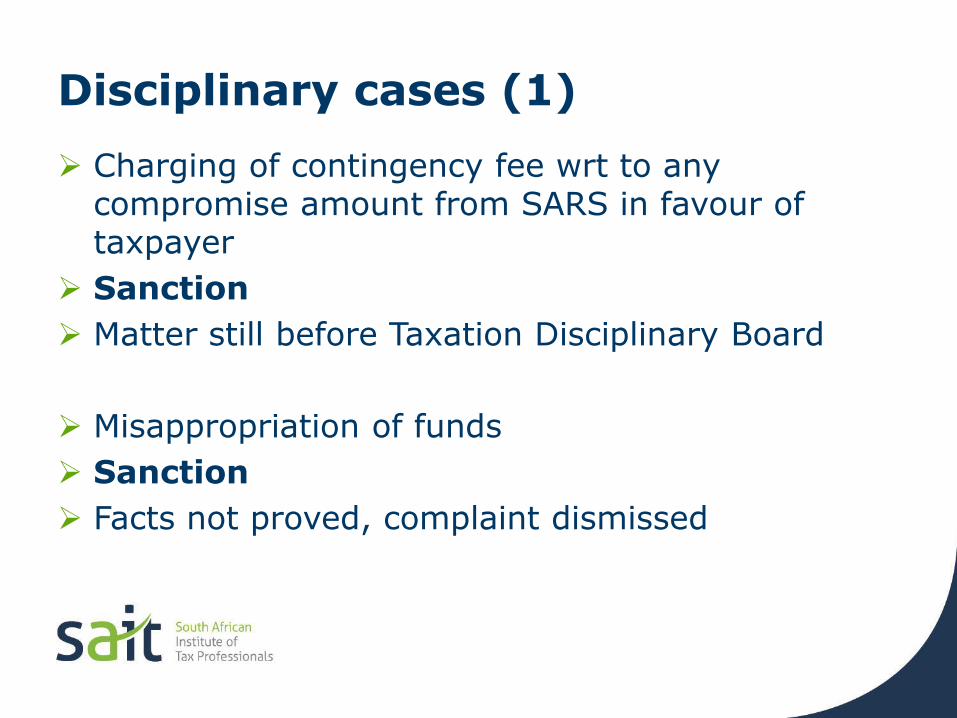

Disciplinary cases (1)

Charging of contingency fee wrt to any compromise amount from SARS in favour of taxpayer

Sanction

Matter still before Taxation Disciplinary Board

Misappropriation of funds

Sanction

Facts not proved, complaint dismissed

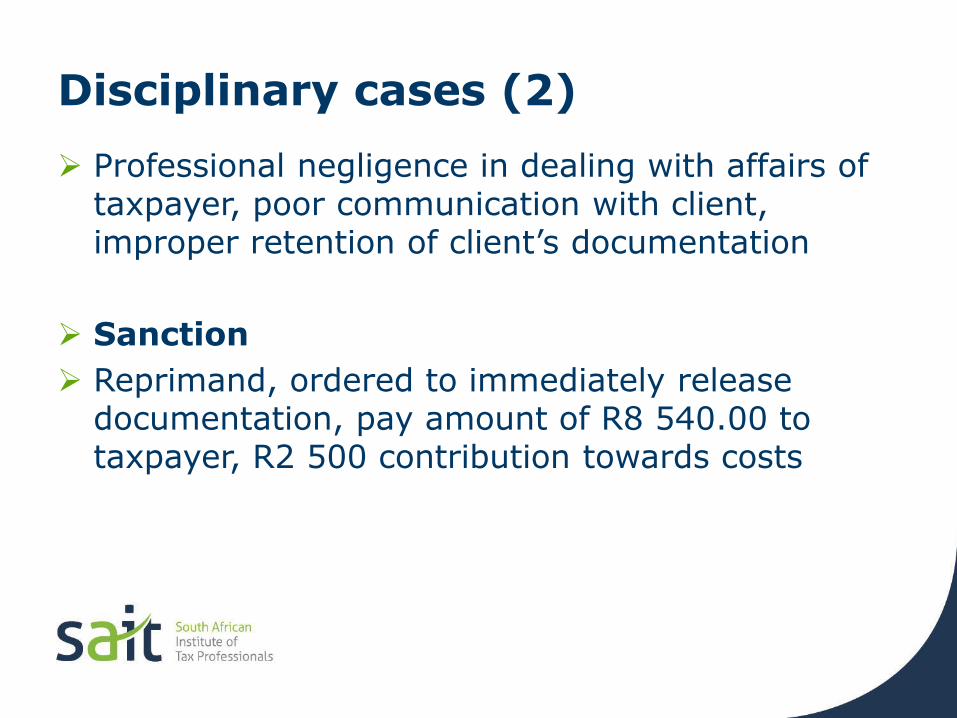

Disciplinary cases (2)

Professional negligence in dealing with affairs of taxpayer, poor communication with client, improper retention of client’s documentation

Sanction

Reprimand, ordered to immediately release documentation, pay amount of R8 540.00 to taxpayer, R2 500 contribution towards costs

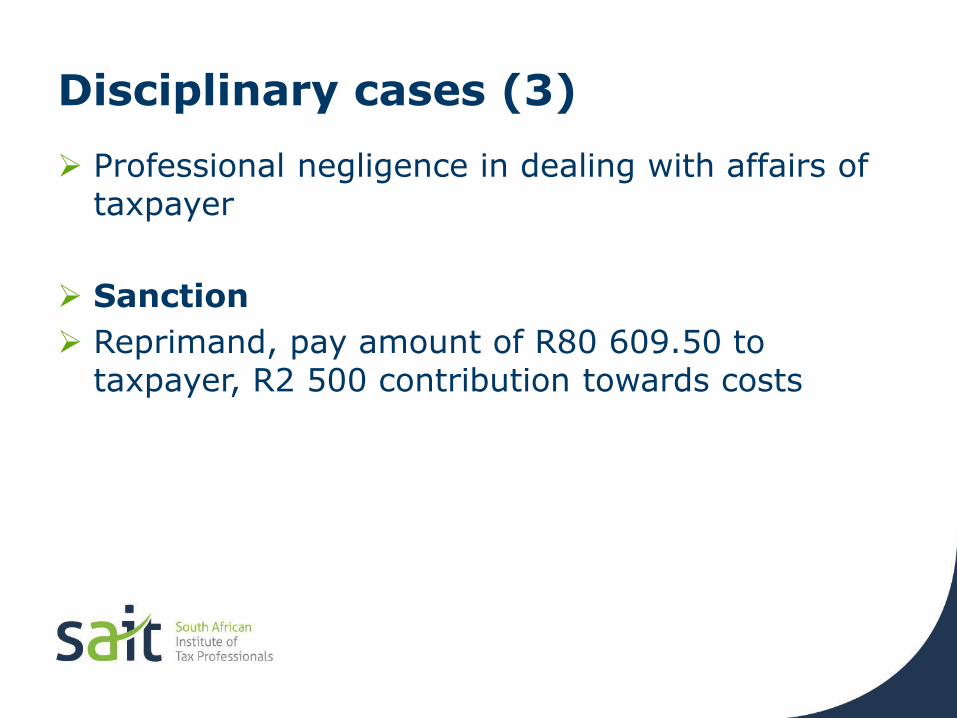

Disciplinary cases (3)

Professional negligence in dealing with affairs of taxpayer

Sanction

Reprimand, pay amount of R80 609.50 to taxpayer, R2 500 contribution towards costs

Disciplinary cases (4)

Professional negligence in dealing with affairs of taxpayer, failed to exercise due care wrtemployees and work done under supervision and control

Sanction

Reprimand, pay amount of R52 036.12 to taxpayer, R2 500 contribution towards costs

Lessons to be learned

• Need to maintain competence and keep up-to-date – only take on work that you are competent to perform

• Act in accordance with fundamental principles –be honest, act professionally, treat others with consideration, communicate regularly with your clients

• Protect your reputation – don’t compromise your ethical principles to ‘help’ your clients, whatever their circumstances may be

• Take more care in ensuring the quality of work performed by your staff

56

Solving ethical dilemmas – some guidelines

James Rest – Four-Component Model of Moral Development

Moral sensitivity

Moral judgement

Moral motivation

Moral character

Solving ethical dilemmas – some guidelines

James Rest – Four-Component Model of Moral Development

Moral sensitivity

In order to make an ethical decision and act ethically, the first step is to identify that an ethical issue exists

Rule of thumb: an ethical issue exists whenever your actions affect others

Solving ethical dilemmas – some guidelines

James Rest – Four-Component Model of Moral Development

Moral judgement

Once ethical issue identified, apply moral judgement to reason out what is most ethical action to take

Use different methods to consider how our actions affect others e.g. Ethics Quick Test

Solving ethical dilemmas – some guidelines

Ethics quick test:

1. Is it legal?

2. How will it look in the newspaper?

3. Is it consistent with my own and/or the organisation’s values?

4. Is it fair to all?

5. If I do it, how will I feel?

Solving ethical dilemmas – some guidelines

James Rest – Four-Component Model of Moral Development

Moral motivation

Ethical intention must follow moral judgment (ethical reasoning) to turn decisions into action

Do you want to be an ethical person? Do you want to do the right thing?

Solving ethical dilemmas – some guidelines

James Rest – Four-Component Model of Moral Development

Moral character

Even the desire to do the right thing is not enough – different pressures can prevent us executing our plans

The key is integrity – the ethical value that summons up the courage to take an ethical action despite pressures to do otherwise

Solving ethical dilemmas – some guidelines

Taking ethical action means we have the courage to act in accordance with our principles to:

Treat others the way we want to be treated (the Golden Rule)

Respect the rights of others

Never take an action that does more harm than good

Conclusion

Being ethical is not easy, it takes moral strength.

“Have the courage to say no. Have the courage to face

the truth. Do the right thing because it is right. These are the magic keys to living your life with integrity.”

W. Clement Stone

Questions?

67

Final thoughts

And if all else fails, remember these words of Marcus Aurelius:

If it is not right, do not do it; if it is not true, do

not say it.