Agenda

Current software in actuarial analysis

What is R?

R as a functional language

Basic Examples

Actuarial pricing

GLM Example

Challenges and opportunities

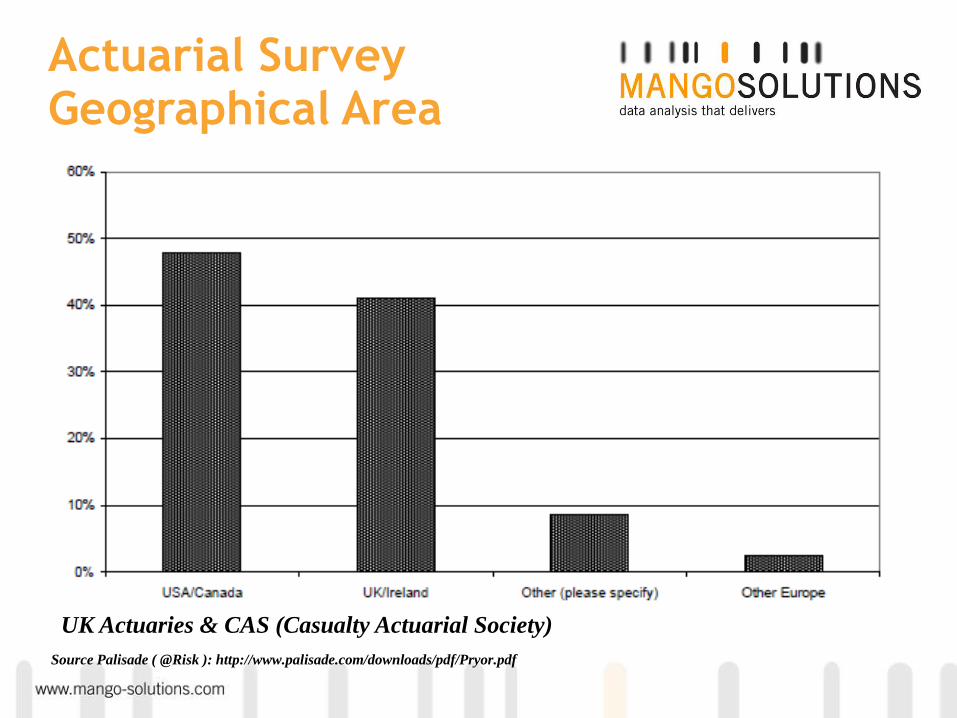

UK Actuaries & CAS (Casualty Actuarial Society)

Source Palisade ( @Risk ): http://www.palisade.com/downloads/pdf/Pryor.pdf

Actuarial Survey Geographical Area

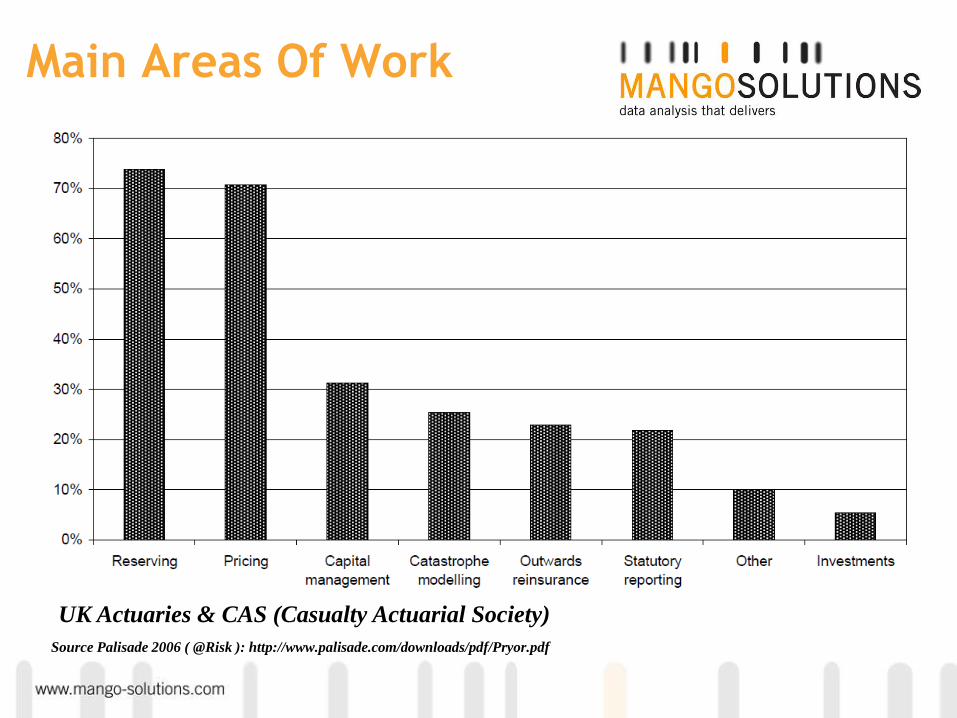

Main Areas Of Work

UK Actuaries & CAS (Casualty Actuarial Society)

Source Palisade 2006 ( @Risk ): http://www.palisade.com/downloads/pdf/Pryor.pdf

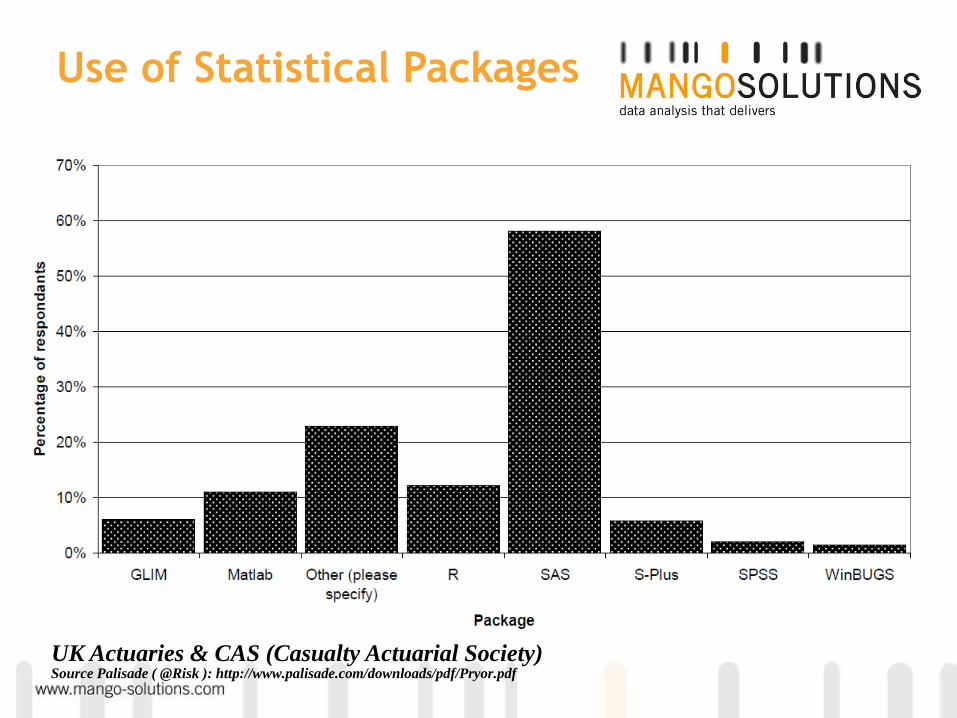

UK Actuaries & CAS (Casualty Actuarial Society)

Source Palisade ( @Risk ): http://www.palisade.com/downloads/pdf/Pryor.pdf

Main area of work in which software is used

Percentage of respondents using each package

UK Actuaries & CAS (Casualty Actuarial Society) Source Palisade ( @Risk ): http://www.palisade.com/downloads/pdf/Pryor.pdf

Percentage of statistical package users using individual packages

UK Actuaries & CAS (Casualty Actuarial Society) Source Palisade ( @Risk ): http://www.palisade.com/downloads/pdf/Pryor.pdf

Use of Statistical Packages

R is the programming language of statistics

Why should it not be the programming language of Actuaries?

Inadequate current incumbents

• VBA: huge versioning issues and inadequate data manipulation and statistical function capabilities

• Excel: Inappropriate for analysis

• Proprietary Actuarial Software: No Granular Access To Processing Outputs

R offers so much in terms of data manipulation, statistical models

Spreadsheets are unstructured computer programs:

The Risks Of Using Spreadsheets for Statistical Analysis (IBM White Paper):

http://public.dhe.ibm.com/common/ssi/ecm/en/imw14297usen/IMW14297USEN.PDF

Excel

Very labour intensive

Excel spreadsheets are unstructured computer programs

Problems with checking calculations and types of errors which can be silent and unknown

Do your spreadsheets start to grind to a halt with rather moderate sets of data?

Versioning excel files could be over 50MB each relative to script versions few KB. Imagine this across your network and the waste of space this encourages

Linking spreadsheets stability issues etc

VBA versioning problems, inadequate for data analysis and most useful purposes – harsh but true?

What is R?

• A big calculator?

• A programming language?

• A rapid prototyping tool?

• A free SAS?

• Statistical Analysis Tool?

People have

described R as:

Useful R Features

Open source object oriented and functional programming language based on S+ designed for manipulating data/objects and carrying out statistical analysis

Easy connections to external programs databases, e.g. RODBC - very stable, dynamic SQL queries etc

Massive library of tools >>3400 packages

GUIs can be created in a straightforward way, gWidgets (GTK+, RGTK) package

Easy output formats, all picture files, data formats, even Excel!

Current Actuarial R Packages

actuar (loss distributions)

ChainLadder

lifecontingencies

LifeTables

http://cran.r-project.org/web/packages/

Reference: http://nsaunders.wordpress.com/2010/08/20/a-brief-introduction-to-apply-in-r/

apply(data, index, function)

lapply(list, function)

aggregate(data, by, FUN)

mapply(function(arg1, arg2), vector(arg1), vector(arg2), ...)

by(data, indices, function)

More “advanced/powerful” {plyr} package extends the apply functionality (Hadley Wickham)

Functional Programming

{plyr} Author: Hadley Wickham

http://www.jstatsoft.org/v40/i01/paper

I/O Array Data Frame List Discarded

Array aaply adply alply a_ply

Data Frame daply ddply dlply d_ply

List laply ldply llply l_ply

a*ply(.data, .margins, .fun, ...)

d*ply(.data, .variables, .fun, ...)

l*ply(.data, .fun, ...)

Example Data

Data Source (Simulated): Modern Actuarial Risk Theory Using R: Kaas, Goovaerts, Dhaene, and Denuit.

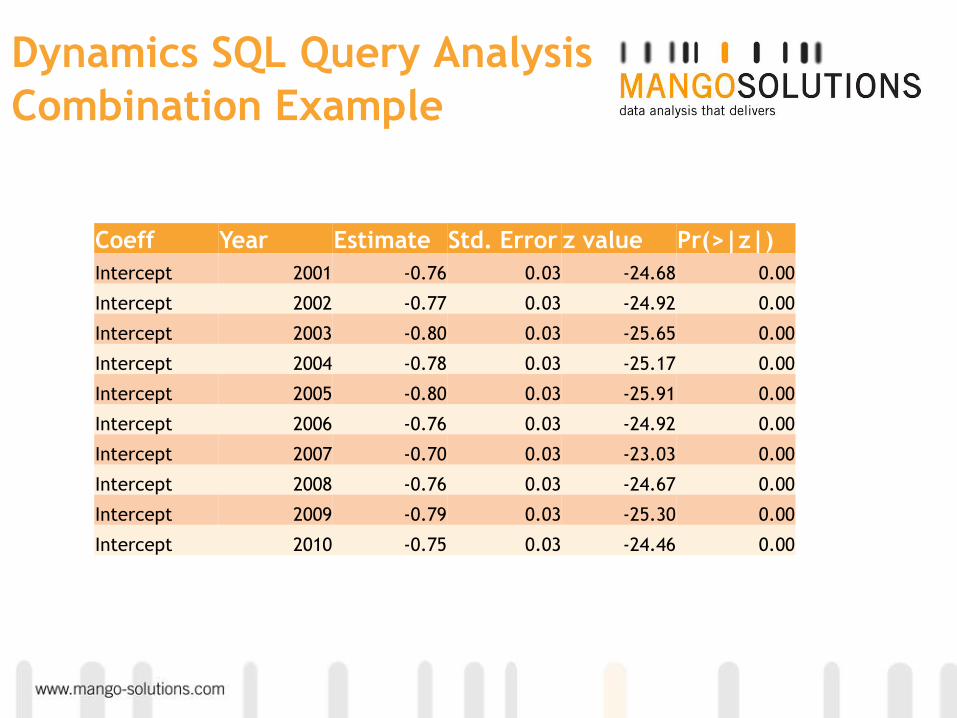

Dynamic SQL

Query Example

require(RODBC)

doMyAnalysis <- function(myYear = 2001){

sqlString <- paste("SELECT * FROM policyClaims WHERE Year='",myYear,"'", sep = "")

myData <- sqlQuery(channel = odbcConnect(dsn = "InsuranceData"), query = sqlString)

odbcCloseAll()

myGlm <- glm(noclaims ~ age + bonusmalus + region + mileage, data = myData, offset =

log(exposure), family = poisson(link = "log"))

myCoeffs <- summary(myGlm)$coeff

theNames <- colnames(myCoeffs)

myCoeffs <- data.frame(myCoeffs)

myCoeffs <- data.frame(rownames(myCoeffs), myYear, myCoeffs)

colnames(myCoeffs) <- c("Coeff", "Year", theNames)

print(myYear)

return(myCoeffs[1,])

}

analysisOutPut <- lapply(2001:2010, doMyAnalysis)

analysisOutPut <- do.call(rbind, analysisOutPut)

rownames(analysisOutPut) <- 1:nrow(analysisOutPut)

Dynamics SQL Query Analysis

Combination Example

Coeff Year Estimate Std. Error z value Pr(>|z|)

Intercept 2001 -0.76 0.03 -24.68 0.00

Intercept 2002 -0.77 0.03 -24.92 0.00

Intercept 2003 -0.80 0.03 -25.65 0.00

Intercept 2004 -0.78 0.03 -25.17 0.00

Intercept 2005 -0.80 0.03 -25.91 0.00

Intercept 2006 -0.76 0.03 -24.92 0.00

Intercept 2007 -0.70 0.03 -23.03 0.00

Intercept 2008 -0.76 0.03 -24.67 0.00

Intercept 2009 -0.79 0.03 -25.30 0.00

Intercept 2010 -0.75 0.03 -24.46 0.00

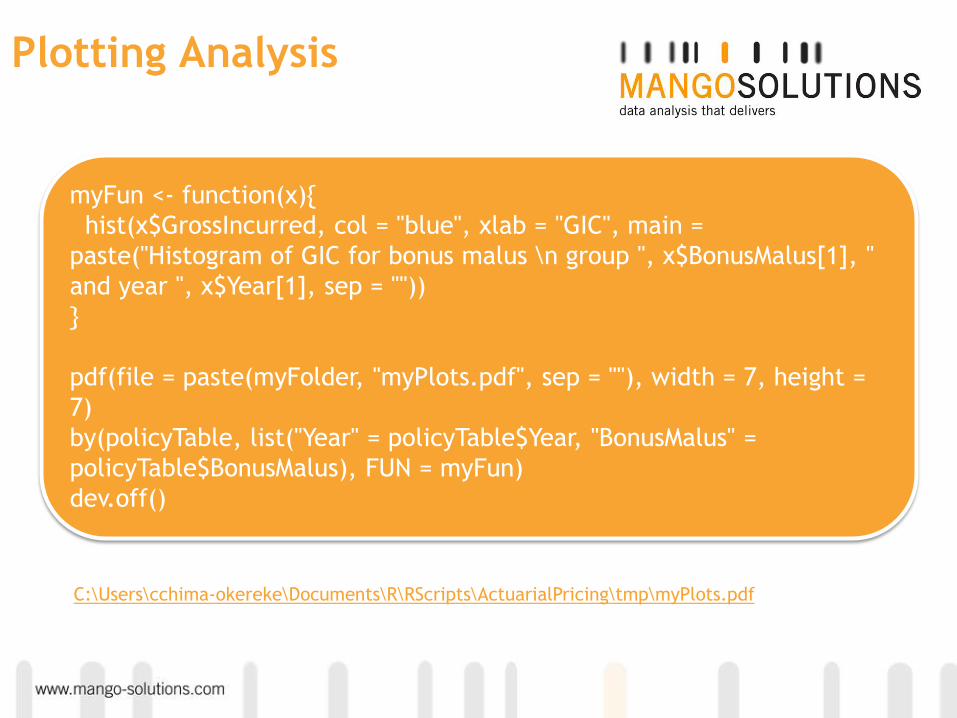

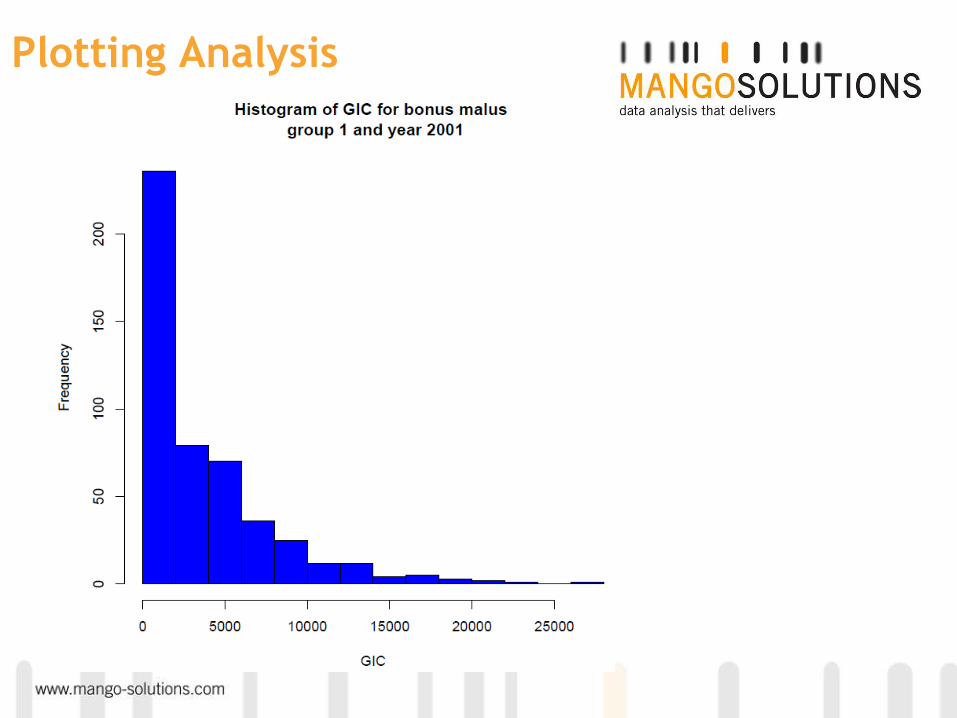

Plotting Analysis

myFun <- function(x){

hist(x$GrossIncurred, col = "blue", xlab = "GIC", main =

paste("Histogram of GIC for bonus malus \n group ", x$BonusMalus[1], "

and year ", x$Year[1], sep = ""))

}

pdf(file = paste(myFolder, "myPlots.pdf", sep = ""), width = 7, height =

7)

by(policyTable, list("Year" = policyTable$Year, "BonusMalus" =

policyTable$BonusMalus), FUN = myFun)

dev.off()

C:\Users\cchima-okereke\Documents\R\RScripts\ActuarialPricing\tmp\myPlots.pdf

Plotting Analysis

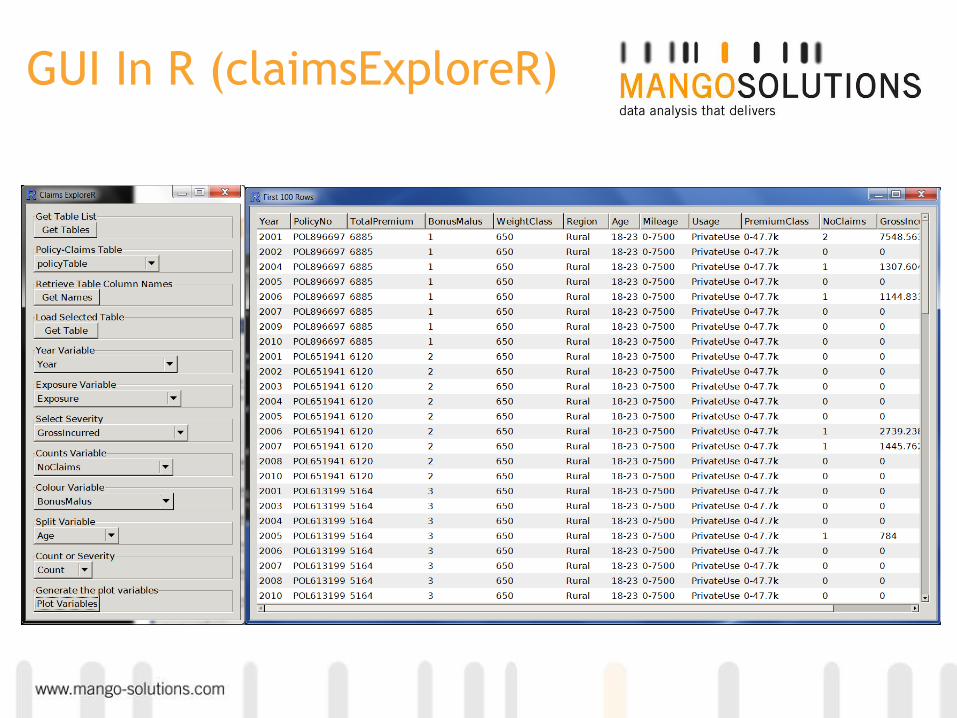

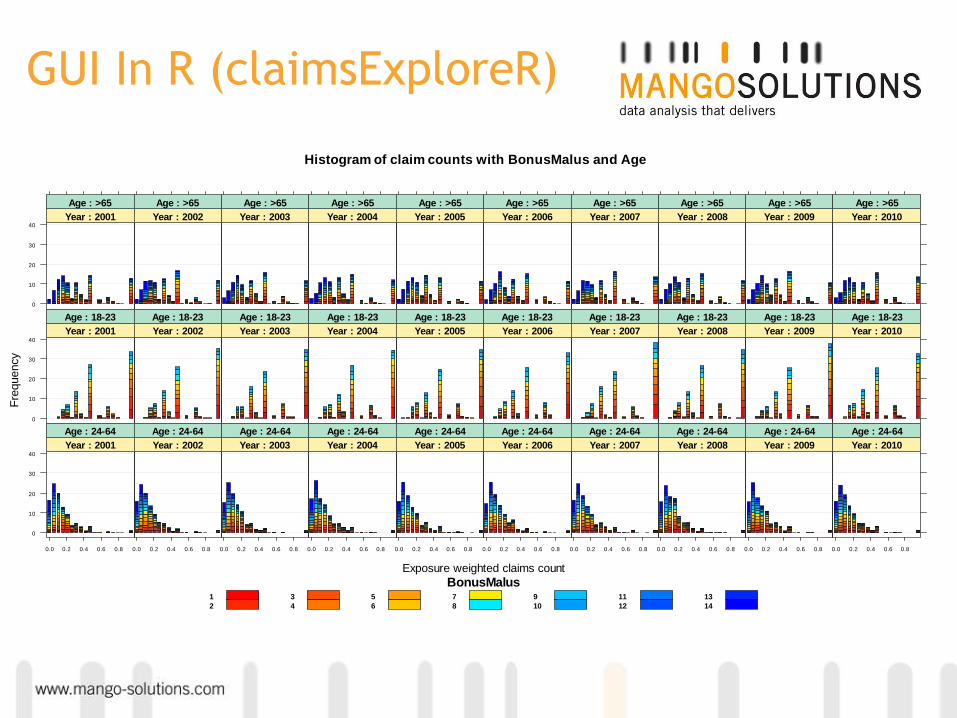

GUI In R (claimsExploreR)

GUI In R (claimsExploreR)

Histogram of claim counts with BonusMalus and Age

Exposure weighted claims count

Fre

quency

0

10

20

30

40

: Year 2001

: Age >65

: Year 2002

: Age >65

: Year 2003

: Age >65

: Year 2004

: Age >65

: Year 2005

: Age >65

: Year 2006

: Age >65

: Year 2007

: Age >65

: Year 2008

: Age >65

: Year 2009

: Age >65

: Year 2010

: Age >65

0

10

20

30

40

: Year 2001

: Age 18-23

: Year 2002

: Age 18-23

: Year 2003

: Age 18-23

: Year 2004

: Age 18-23

: Year 2005

: Age 18-23

: Year 2006

: Age 18-23

: Year 2007

: Age 18-23

: Year 2008

: Age 18-23

: Year 2009

: Age 18-23

: Year 2010

: Age 18-23

0

10

20

30

40

0.0 0.2 0.4 0.6 0.8

: Year 2001

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2002

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2003

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2004

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2005

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2006

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2007

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2008

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2009

: Age 24-64

0.0 0.2 0.4 0.6 0.8

: Year 2010

: Age 24-64

BonusMalus1

2

3

4

5

6

7

8

9

10

11

12

13

14

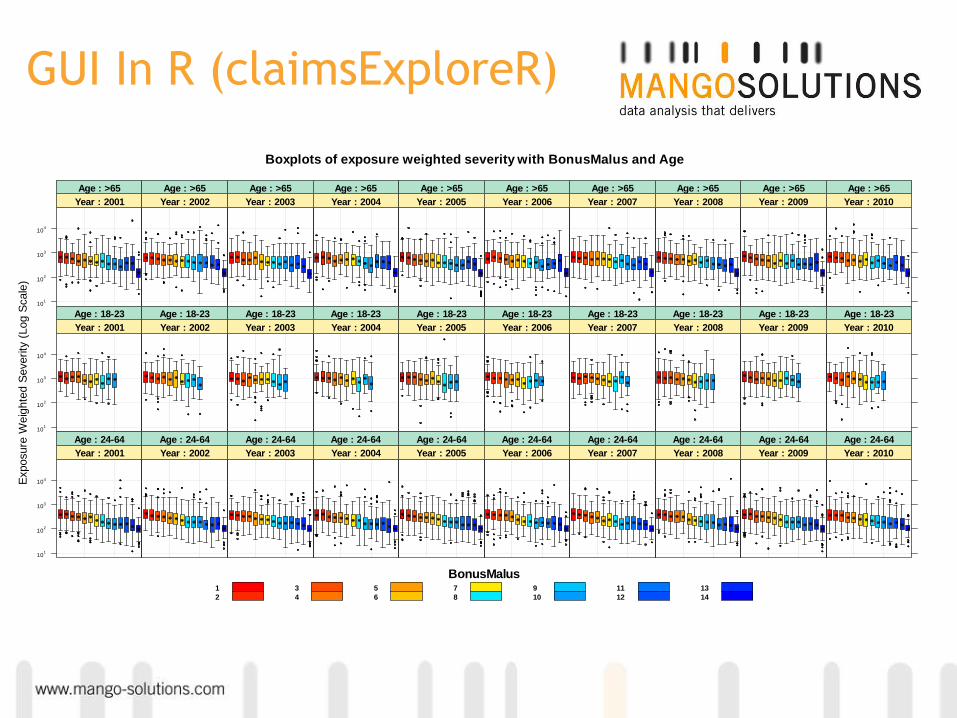

GUI In R (claimsExploreR)

Boxplots of exposure weighted severity with BonusMalus and Age

Exposure

Weig

hte

d S

everity

(Log S

cale

)

101

102

103

104

: Year 2001

: Age >65

: Year 2002

: Age >65

: Year 2003

: Age >65

: Year 2004

: Age >65

: Year 2005

: Age >65

: Year 2006

: Age >65

: Year 2007

: Age >65

: Year 2008

: Age >65

: Year 2009

: Age >65

: Year 2010

: Age >65

101

102

103

104

: Year 2001

: Age 18-23

: Year 2002

: Age 18-23

: Year 2003

: Age 18-23

: Year 2004

: Age 18-23

: Year 2005

: Age 18-23

: Year 2006

: Age 18-23

: Year 2007

: Age 18-23

: Year 2008

: Age 18-23

: Year 2009

: Age 18-23

: Year 2010

: Age 18-23

101

102

103

104

: Year 2001

: Age 24-64

: Year 2002

: Age 24-64

: Year 2003

: Age 24-64

: Year 2004

: Age 24-64

: Year 2005

: Age 24-64

: Year 2006

: Age 24-64

: Year 2007

: Age 24-64

: Year 2008

: Age 24-64

: Year 2009

: Age 24-64

: Year 2010

: Age 24-64

BonusMalus1

2

3

4

5

6

7

8

9

10

11

12

13

14

GLM Models in Pricing

Poisson – Frequency

Gamma – Severity

Negative Binomial for frequency {MASS}

Tweedie combines frequency and severity {statmod}

Variable Selection Criteria

• Information Criteria

• AIC

• BIC (Multiple flavours)

• Significance of variable: Chi-Squared/F-Test

• Consistency measures

• Other Measures

What metrics shall we use to include/exclude

variables?

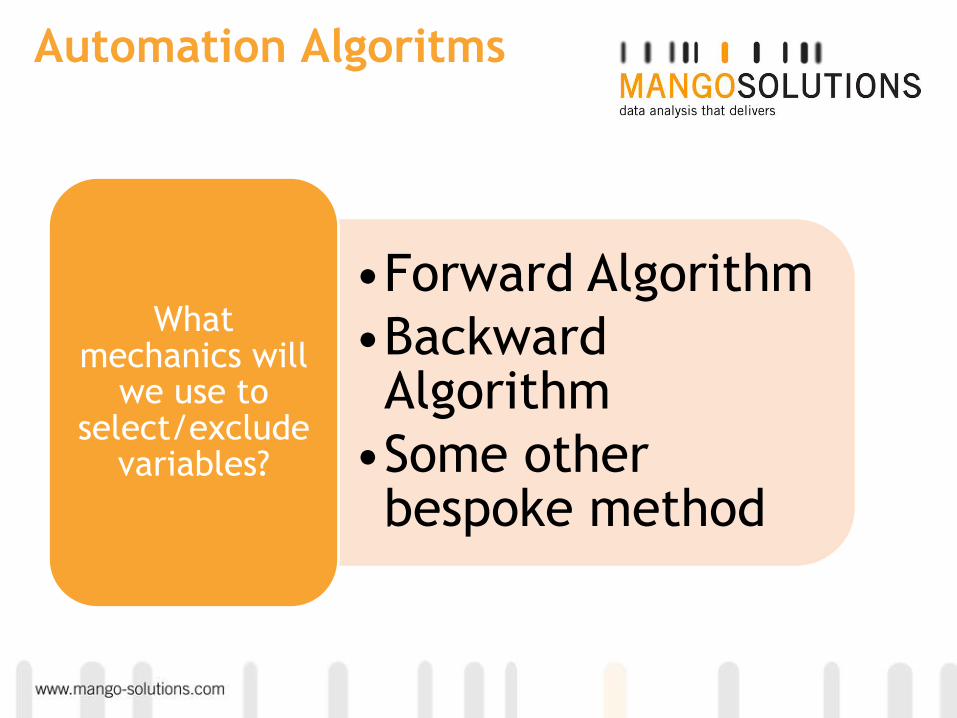

Automation Algoritms

•Forward Algorithm

•Backward Algorithm

•Some other bespoke method

What mechanics will

we use to select/exclude

variables?

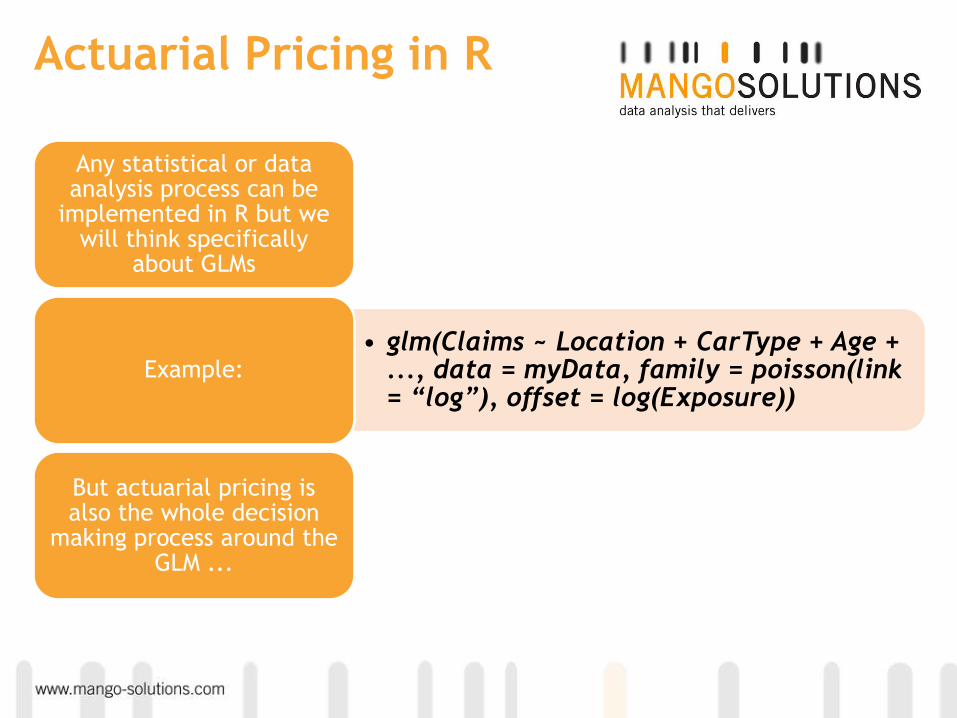

Actuarial Pricing in R

Any statistical or data analysis process can be

implemented in R but we will think specifically

about GLMs

• glm(Claims ~ Location + CarType + Age + ..., data = myData, family = poisson(link = “log”), offset = log(Exposure))

Example:

But actuarial pricing is also the whole decision

making process around the GLM ...

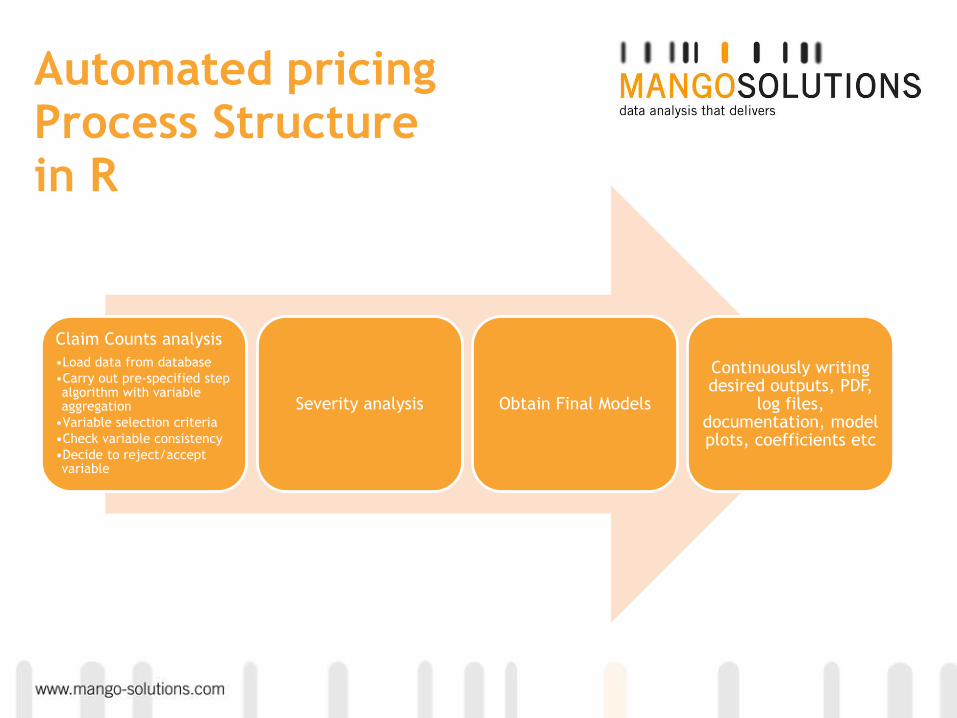

Automated pricing Process Structure in R

Claim Counts analysis

•Load data from database

•Carry out pre-specified step algorithm with variable aggregation

•Variable selection criteria

•Check variable consistency

•Decide to reject/accept variable

Severity analysis Obtain Final Models

Continuously writing desired outputs, PDF,

log files, documentation, model plots, coefficients etc

Automated Actuarial Pricing

We need to defined the consolidation structure for categorical variables e.g.

Location 1 Location 2 Location 3 Location 4

North North North North

N.East North North North

N.West N.West N.West North

S.West S.West S.West South

S.East S.East South South

South South South South

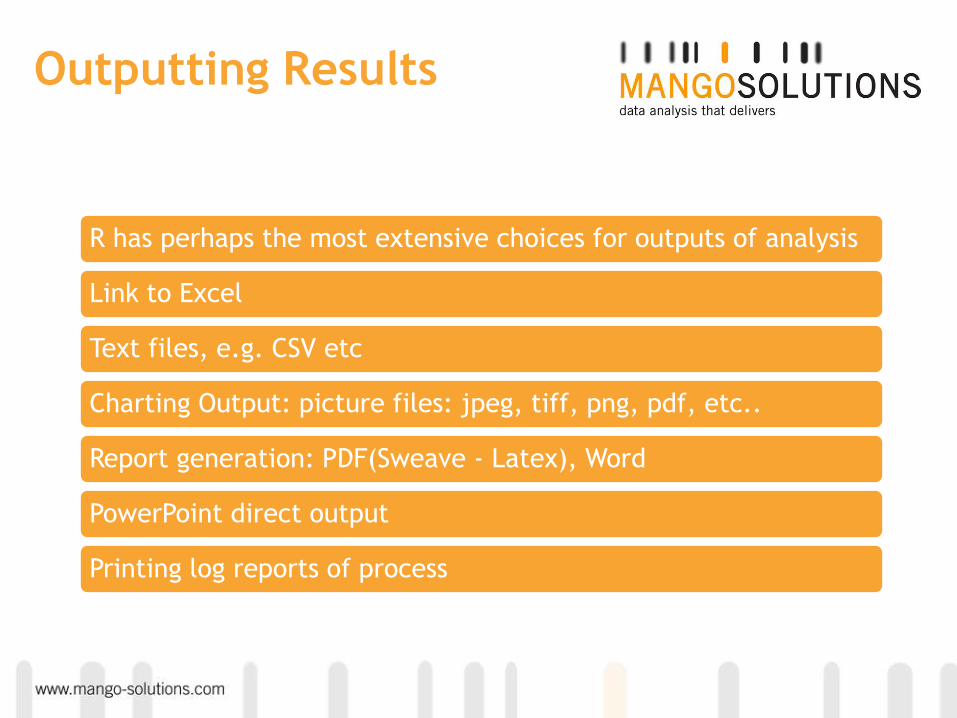

Outputting Results

R has perhaps the most extensive choices for outputs of analysis

Link to Excel

Text files, e.g. CSV etc

Charting Output: picture files: jpeg, tiff, png, pdf, etc..

Report generation: PDF(Sweave - Latex), Word

PowerPoint direct output

Printing log reports of process

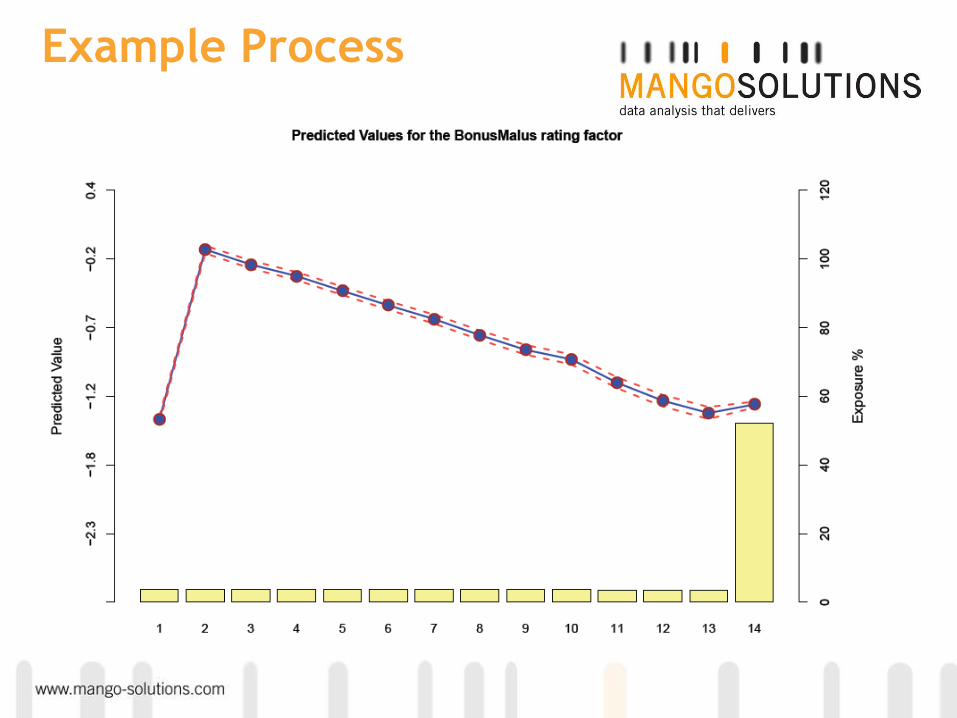

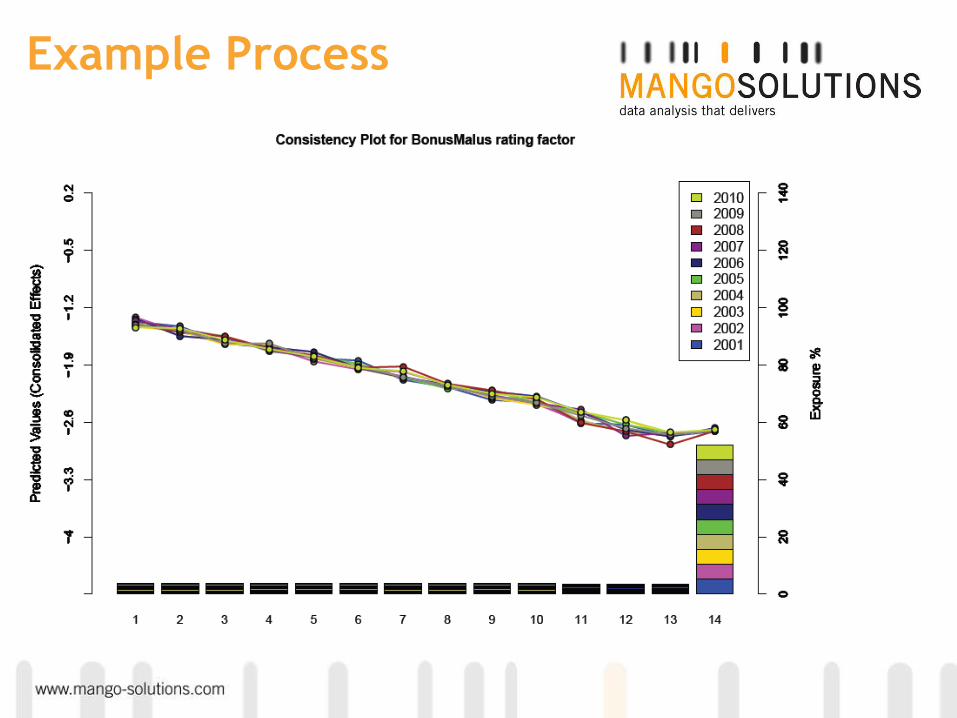

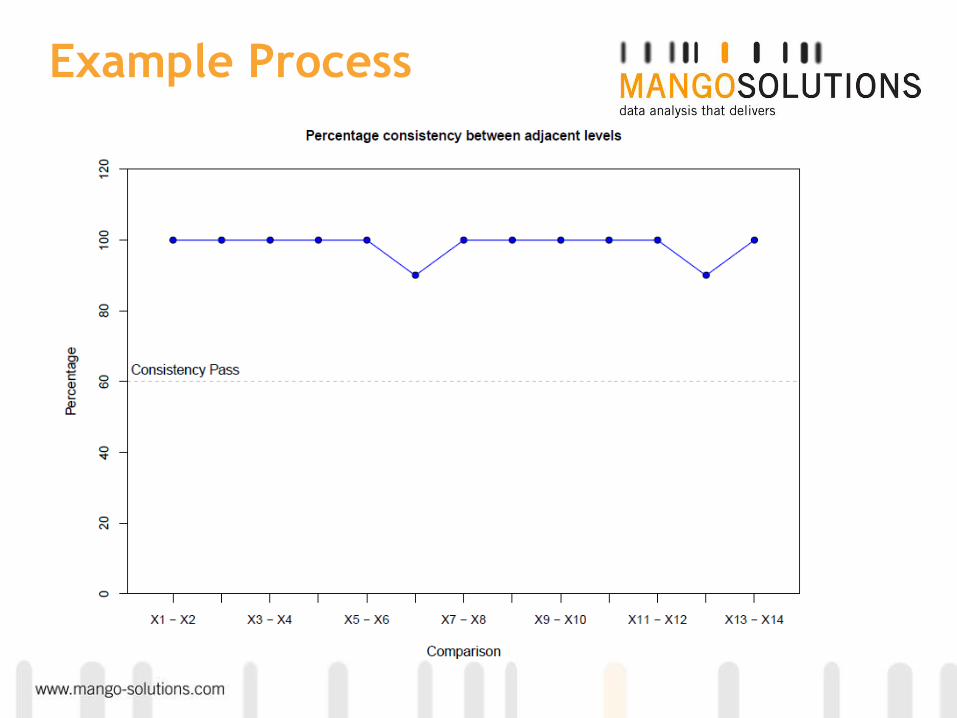

Example Process

Example Process

Example Process

Effects package

Effects plot of Age and Bonus Malus

Bonus Malus

Rela

tivity (

%)

110

120

130

140

150

1 2 3 4 5 6 7 8 9 10 11 12 13 14

: Age 18-23

1 2 3 4 5 6 7 8 9 10 11 12 13 14

: Age 24-64

1 2 3 4 5 6 7 8 9 10 11 12 13 14

: Age >65

effects package from John Fox: http://www.jstatsoft.org/v08/i15/paper

Example Process

Example Process: Final Model

Final Charts

Final Model

Potential Scheme for analytical process

Data residing in some database

Connect to R, RODBC,

RPostgreSQL, RODM etc.

Carry out analysis in R

Write results to PDF, any

picture format, push

to Latex, Excel, CSV, etc

Advantages of R for GLM Analysis

•Standard actuarial GLM techniques are available, e.g. splines, interaction terms etc.

•The best plotting functions of any statistical package

•More advanced techniques are available, GAM, GMM, GNM, GHMM, MCMC methods – too many packages to list here!

•Bespoke methods and new actuarial techniques can be readily implemented in R while they are unavailable in standard actuarial software

•Easy to integrate and fully customisable in any analytical environment

•Complete array of statistical/analysis tools, clustering, neural nets, GRM, tree models, bootstrapping, Bayesian techniques, ODE/PDE, HMMs, contingency tables, survival analysis, copulas, extreme value analysis, geospatial analysis and visualisation

R offers a complete statistical,

data processing, and analysis environment

Challenges & Opportunities

If you are new to R, do something small to begin with test R out

IT support for R

There is great need for training and generation of material to enable actuarial analysts to use R

For mere mortals (like me) the learning curve is tough and the documentation appears ambiguous

R & Hadoop and R & Oracle

See me later for live R demos