___________________________________________________________________________

2008/SOM3/EC/SEM/004 Agenda Item: 6

Regulation and Port Productivity Overview of Global Port Benchmarking - A Focus on Hong Kong and

South China Region

Submitted by: Hong Kong, China

Seminar on Best Practices in Regulation and Promotion of Efficiency in Transport

Infrastructure Facilities Lima, Peru

15-16 August 2008

2

Regulation and Port Productivity Overview of Global Port Benchmarking (A Focus on Hong Kong and South China Region) John J. Liu and T. L. Yip Department of Logistics and Maritime Studies Faculty of Business The Hong Kong Polytechnic University Hong Kong, China Background Globalization and trade liberalization in the past decades have profound impacts on port industry. Governments are increasingly realizing that, ports have become the most dynamic link in international transport networks and, as a result, inefficient ports can easily wither gains from trade liberalization and export performance. Port authorities have been trying to improve port efficiency through adopting new technologies and deregulation. The disappearance of national boundaries of port hinterlands, the increasing containerization, and the trend of deregulation force container ports to face keen competition, because of the diminishing product differentiation and government power. Competition leads to an increasing pressure on ports to control their costs, offer competitive user charges, and improve quality of services to shipping liners and shippers. A port benchmarking project is conducted to study the port productivity for major container ports in the world. The project addresses one fundamental question: what are the best practices to improve port efficiency (productivity) for a port. By collecting data from ports around the world, empirical models have been developed to compare port performance under different (regulation) scenarios. The results from this benchmarking project will be the foundation for a port to design appropriate regulatory tools. Port Benchmarking of Technical Efficiency The production and cost theories in economics makes it possible to estimate production and cost functions empirically, and thus to investigate the productivity and technology change of a port. The port production function can be written as: Port production = function (Infrastructure, Superstructure, Port characteristics). The quantity to indicate port production may be port throughputs (TEU, tonnage), ship arrivals or other outputs. The superstructure denotes cargo handling equipment, storage facilities etc. The port characteristics covers water depth, port groups, continental region etc. The findings are summarised as follows (Yan, Sun and Liu, 2008):

1. Port facility operators with deeper water terminals and larger numbers of calling liners is more efficient.

2. More terminals in a port reduce the efficiency. 3. Port groups are more efficient. 4. Ports are more efficient in the Far East Asia in general.

Several factors that may impact on the port efficiency are being addressed, e.g. Multiple outputs - the effect of port facility mix (container, bulk and tanker). We further discuss the implication of Port globalisation and Container flows Implication 1: Globalisation on ports From the port benchmarking study, ports groups are found more efficient. One of the main impacts of globalisation has been the integration of transport facilities provided by service organisations around the world. In the port sectors, there exist some of the prominent operators who provide services on a global scale.

3

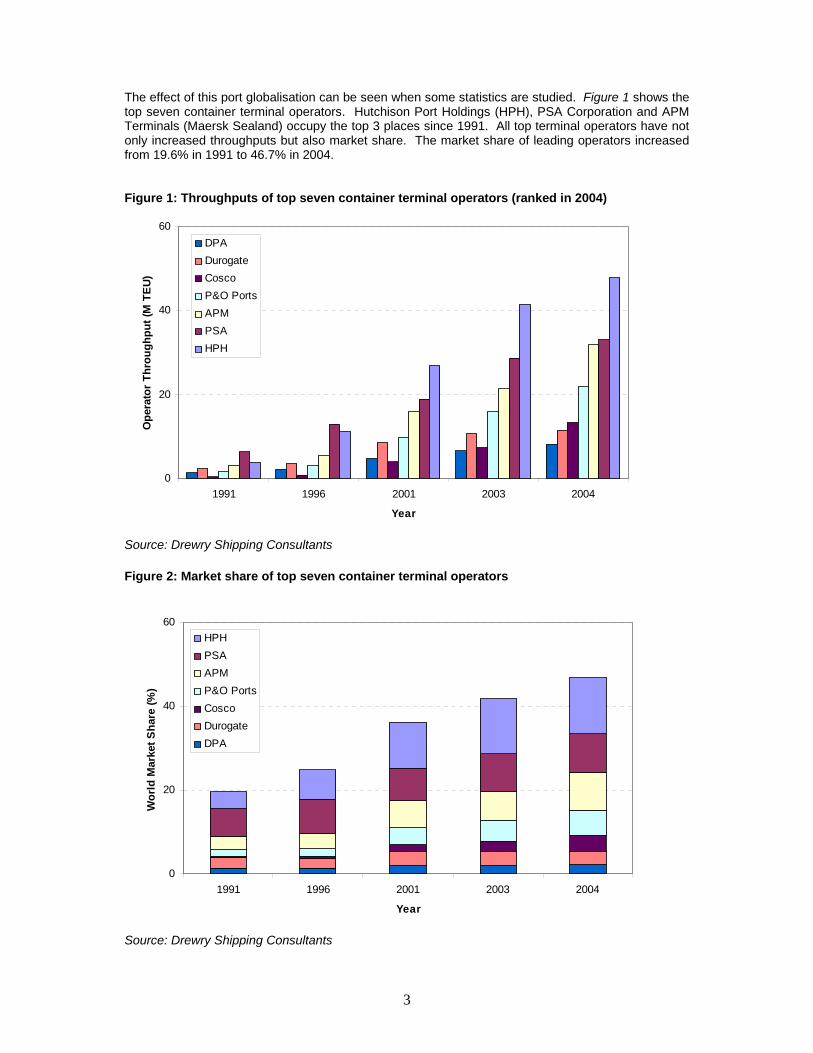

The effect of this port globalisation can be seen when some statistics are studied. Figure 1 shows the top seven container terminal operators. Hutchison Port Holdings (HPH), PSA Corporation and APM Terminals (Maersk Sealand) occupy the top 3 places since 1991. All top terminal operators have not only increased throughputs but also market share. The market share of leading operators increased from 19.6% in 1991 to 46.7% in 2004. Figure 1: Throughputs of top seven container terminal operators (ranked in 2004)

0

20

40

60

1991 1996 2001 2003 2004

Year

Ope

rato

r Th

roug

hput

(M T

EU)

DPADurogateCoscoP&O PortsAPMPSAHPH

Source: Drewry Shipping Consultants Figure 2: Market share of top seven container terminal operators

0

20

40

60

1991 1996 2001 2003 2004

Year

Wor

ld M

arke

t Sha

re (%

)

HPHPSAAPMP&O PortsCoscoDurogateDPA

Source: Drewry Shipping Consultants

4

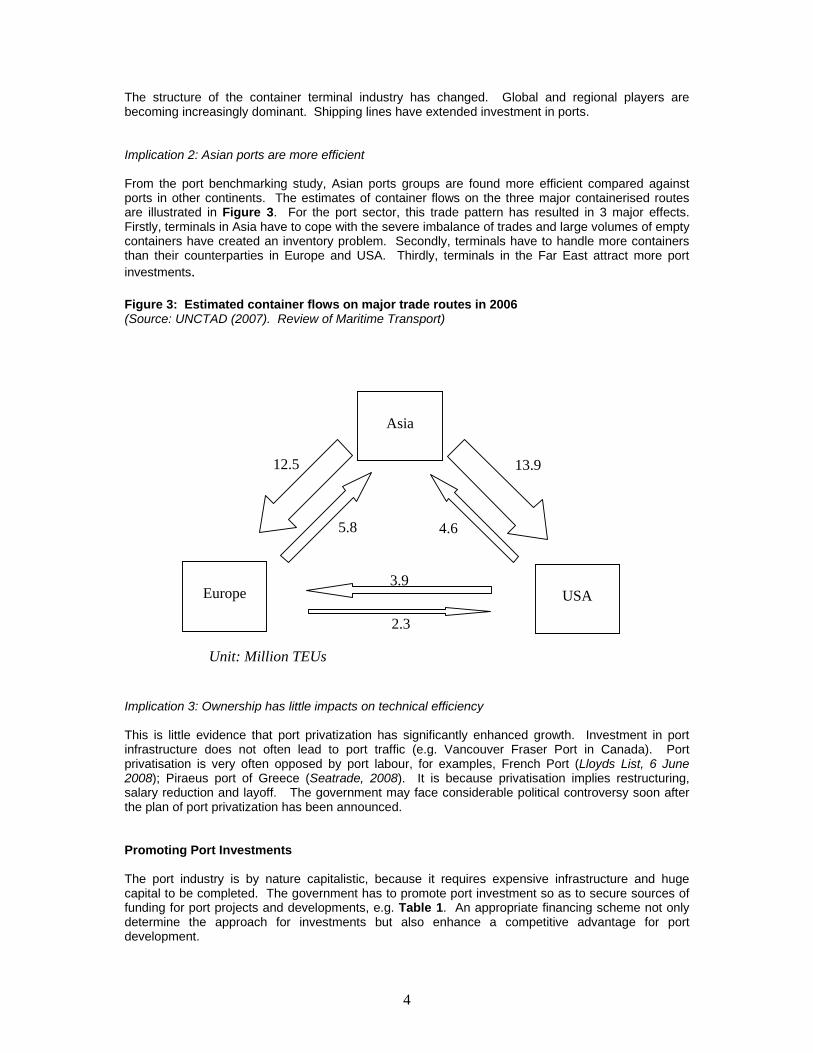

The structure of the container terminal industry has changed. Global and regional players are becoming increasingly dominant. Shipping lines have extended investment in ports. Implication 2: Asian ports are more efficient From the port benchmarking study, Asian ports groups are found more efficient compared against ports in other continents. The estimates of container flows on the three major containerised routes are illustrated in Figure 3. For the port sector, this trade pattern has resulted in 3 major effects. Firstly, terminals in Asia have to cope with the severe imbalance of trades and large volumes of empty containers have created an inventory problem. Secondly, terminals have to handle more containers than their counterparties in Europe and USA. Thirdly, terminals in the Far East attract more port investments. Figure 3: Estimated container flows on major trade routes in 2006 (Source: UNCTAD (2007). Review of Maritime Transport)

Implication 3: Ownership has little impacts on technical efficiency This is little evidence that port privatization has significantly enhanced growth. Investment in port infrastructure does not often lead to port traffic (e.g. Vancouver Fraser Port in Canada). Port privatisation is very often opposed by port labour, for examples, French Port (Lloyds List, 6 June 2008); Piraeus port of Greece (Seatrade, 2008). It is because privatisation implies restructuring, salary reduction and layoff. The government may face considerable political controversy soon after the plan of port privatization has been announced. Promoting Port Investments The port industry is by nature capitalistic, because it requires expensive infrastructure and huge capital to be completed. The government has to promote port investment so as to secure sources of funding for port projects and developments, e.g. Table 1. An appropriate financing scheme not only determine the approach for investments but also enhance a competitive advantage for port development.

Asia

Europe

USA

13.9

4.6

12.5

5.8

3.9

2.3

Unit: Million TEUs

5

One of port privatisation problems is that the port ownerships may be eventually transferred to foreign ownership that the government does not want, e.g. Dubai Ports World (DPW) intended to acquire P&O in 2006. Port privatisation may not create or improve port infrastructure and facilities to benefit the local economy (Baird and Valentine, 2007). In the past, port projects are funded or subsidised by the public sector. Today, the involvement of the private sector in the port industry has increased significantly in both developed and developing countries. However, port infrastructure projects have rarely financed by commercial banks but international lending institutions such as the World Bank, and Asian Development Bank. As the private sector involvement in port projects has increased, the World Bank (2007, p. 98) has enumerated seven elements which are shaping the nature of the private sector involvement in ports:

1. Expected yield 2. Debt / equity financing structure 3. Sponsorship 4. Legality of contracts 5. Transparency 6. Fair and open bidding procedures 7. Feasibility studies (technical, financial, economic and environmental)

The World Bank (2007) further discussed a large variety of funding schemes. The most prominent of these schemes are the various forms of “leasing” and “concession arrangements”.

1. Leasing – is a method by which an agreement is made for the right to use an asset (e.g. land, equipment) over an agreed period of time in return for payment. Payment can be a single one-off transaction or made in a series of instalments. The two dominant forms of leasing agreements are “lease contract” and “leasehold agreement”. The main methods of lease payment are ‘flat rate’, ‘minimum/maximum rate’ and ‘shared revenue’.

2. Concession arrangement – government maintains the ownership of the port land, but grants the concessionaire the right to fiancé, build and operate a facility or some equipment, for public use, for a stated period of time. The concessionaire not only covers the costs of investment but assumes all commercial risks. The major advantage of concession arrangement is to increase private financial participation in the development of the port without changing the structure of the port status.

Other private participation schemes are: management contracts (e.g. dedicated terminals), joint ventures, and BOT (build, operate, transfer) agreements (IAPH 2001; Ernst & Young 1994). An alternative financing scheme is Initial Public Offer (IPO). The liquidity of the stock exchange offer a better debt position and raise equity for future expansions, especially the currency risk (interest rate) are high (e.g. Tianjin port, Dalian port, Santos Brazil). China approach to finance port projects There are several characterise of China port policy:

1. The government (national or province) does not manage the terminals directly. 2. Foreign Direct Investment (FDI) is conducted in the form of joint venture. Foreign companies

were in effect restricted to holding less than 50% share of joint venture. 3. Foreign companies act as both investors and managers. Local authorities act as mainly

landlord of the terminals. The joint venture offers easier access to new technologies (for the benefits of China) and to new markets (in favour of foreign companies).

6

References: ADB (2000). Developing Best Practices for Promoting Private Sector Investment in Infrastructure. Manila, Philippines: Asian Development Bank. Baird, A. J. and Valentine, V.F. (2007). Port privatisation in the United Kingdom. In Devolution, Port Governance and Port Performance, Research in Transportation Economics, 17, 55-84. Ernst & Young (1998). Privatization – Investing in State-owned Enterprises Around the World. John Wiley & Sons, Inc. EU Commission (2004). Proposal for a Directive of the European Parliament and of the Council on Market Access to Port Services. Brussels. IAPH (2001). Guidelines for Port Planning and Design. Tokyo, Japan: International Association of Ports and Harbours. Liu, John J., Yip T. L. (2005) “Assessment and outlook of port competition in Greater China Region”, Asian Ports and Shipping, August 2005, Shanghai. Liu, John J., Yan J., Yip, T. L. (2007) “Competition and productivity of global container ports”. Proceedings of International Conference on Economic Development and Industrial Efficiency of East Asia, Taipei, 17 July, 2007, Section C3, pp. 1-7. Lloyd’s List (2008). Fresh wave of strikes hit French ports (6 June 2008). Seatrade (2008). Privatisation battle – The Greek government’s decision to privatise national ports is being fiercely opposed by determined dock workers. May/June 2008. WB (2007). Port Reform Toolkit, 2nd edition. Washington, DC: The World Bank. Yan, J., Sun X. and John J. Liu (2008). Assessing container operator efficiency with heterogeneous and time-varying production frontiers. Transportation Research Part B. doi: 10.1016/j.trb.2008.06.001 Yan, J., Sun X., Yip, T. L. (2006) “Efficiency analysis of global container ports with time-variant individual production frontiers”. INFORMS Annual Meeting, Pittsburgh.

7

Table 1: Examples of port privatization projects in Europe

Date Year Company Name Country Area SIC Sector

% for Sale

Value of Transaction in US$ million

Method of Sale

Market Area

01/02/1983 1983 Associated British Ports Hldgs

United Kingdom

Old Europe 4491 Transportation

Industry 51.5 33.4 PO Domestic

01/04/1984 1984 Associated British Ports Hldgs

United Kingdom

Old Europe 4491 Transportation

Industry 48.5 74.8 PO Domestic

31/01/1991 1991 Verolme Dockyard Ireland Old

Europe 4493 Transportation Industry 100 1.8 PS ------------

--

31/01/1992 1992 Tees and Hartlepool Port Authority

United Kingdom

Old Europe 4491 Transportation

Industry 100 328.23 PS --------------

11/03/1992 1992 Port of Tilbury United Kingdom

Old Europe 4493 Transportation

Industry 100 55.17 PS --------------

30/06/1992 1992 Medway Ports Authority

United Kingdom

Old Europe 4491 Transportation

Industry 100 51.2 PS --------------

17/11/1995 1995 Dundee Port Authority

United Kingdom

Old Europe 4491 Transportation

Industry 100 28.31 PS --------------

02/03/1998 1998 Mersey Docks & Harbour Co

United Kingdom

Old Europe 4491 Transportation

Industry 13.9 117.8 PO Domestic

01/01/1999 1999 Belfast Port United Kingdom

Old Europe 4491 Transportation

Industry NA 150 PO Domestic

01/08/2001 2001 Thessaloniki Port Authority Greece Old

Europe 4491 Transportation Industry 25 15 PO Domestic

26/07/2003 2003 Piraeus Port Authority Greece Old

Europe 4491 Transportation Industry 25.5 61.5 PO Domestic

Key: PO = Public offer, PS = Private sale Source: Privatization Barometer

Regulation and Port ProductivityOverview of Global Port Benchmarking

(A Focus on Hong Kong and South China Region)

John J. Liu and T.L. Yip(Hong Kong PolyU)

16 August 2008APEC Lima (Peru) 2008

APEC Seminar: Best Practices in Regulation of Ports

Key Factors in Port Productivity

Port technology: Output, Growth, and Innovation Input factors: Tangible (capital, labor), Intangible (usable knowledge, IT factors)Efficiency: Total factor productivity (TFP) heterogeneity (technical, political, and market) Regulation: Ownership, Legal system, Government quality, Governance system

The puzzling IT-revolution: lagging and stepwise

Robert Solow (1987):``you see the computer revolution everywhere except in the productivity data''

Alan Greenspan (1996): Negative trends in measured productivity observed in many services industries seemed inconsistent with the fact that they ranked among the top computer-using industries

Practices in Port Regulation: Best, or Not?

Privatization: Really the best for ports? Then something else must be missing in Hong Kong, as the records in recent years showed.Either public or private, but not joint (mixed): What about Shanghai?Container ports: Throughput = Efficiency?Income difference: Explainable by technology difference? Regulation/policy difference? Or system heterogeneity?

The pending issues in Port Efficiency:

“Two intrinsic characteristics of the port industry – the individual heterogeneity in production technology and the time-varying nature of technical efficiency, have been generally ignored.” (Yan, Sun and Liu, TRB 2008): Natural conditions and business environment

Drastic difference in income across countries is not due to technical differences and differences in endowments of natural resources. (Prescott, 1997): Income HK = 10 x Shenzhen

大鏟灣Da Chan Port

8/20/2008 LGT/Liu 6

Development of Total-Factor Port Efficiency Assessment Tools at C.Y. Tung ICMS (since 2005;

HK PolyU)Initial grant (HK$1.26 million) on Regional Port Competition: December, 20051st Port Forum on Port Benchmarking: April 27 - 29, 2006; PolyU HK1st Special IAME Session on Port Benchmarking: IAME-Melbourne, July 13 – 15, 2006 Initial meeting on collaboration on N.E.T.S at Institute for Water Resource of US-ACE: November 8 – 9, 2006; Alexandria, VA; by Keith Hofseth (IWR), Wesley Wilson (Oregon), Jia Yan (PolyU), and John Liu (PolyU)Further funding and donation to ICMS (over HK$10 million) from Tung Foundation2nd Port Forum, IFSPA-2007 (International Forum on Shipping, Port, and Airport): May 10 – 12, 2007; PolyU2nd Special Session on Port Benchmarking: IAME-Athens, July 4 – 6, 2007

8/20/2008 LGT/Liu 7

Development of Total-Factor Port Efficiency Assessment Tools at C.Y. Tung ICMS

(Continuing on …)PolyU Niche Area: Consortium of Shipping and Maritime Studies (CSMS) – Services and Management; ($12 M five-year grant, approved 15 November, 2007)Keynote presentation: Conference on Global Maritime and Intermodal Logistics (Singapore), December 17 – 19, 2007Special Session at IAME 2008-Dalian: 2-4 April, 2008 (Dalian, China)

============3rd Port Forum, IFSPA-2008: May 25 – 28, 2008 (www.lgt.polyu.edu.hk/ifspa2008), at which 1st Report of Global Container Ports Performance Benchmarking is to be released.Website for Port Performance Benchmarking, and Port-adapted Logistics Index (PortAL Index): Under construction

8

BACKGROUND AND OUTLOOK

Asymmetric port competition: Port-focal logistics and supply chain management (as opposed to firm-focal logistics and SCM)

Logistics and Port Index: TFP, Mutual risk system; Financial, Economic, Social, Security, and Environmental risks …

CSMS grant ($2.07m): “Port-Adapted Logistics (PortAL) Index - An Interactive Dynamic Efficiency Assessment System (IDEAS)”

Production Frontiers under Inputs

• Frontier:• Maximum possible output by a certain

production technology over a given period time, with minimized input cost over a given set of input possibilities (production possibility set)

Deterministic Frontier Model

Deterministic inefficiency

Expected Performance

frontier

Stochastic Frontier Model

Stochastic Inefficiency

frontier

Actual output

Analysis 1997-2004

• Technical Efficiency of Container Operators from 1997 to 2004

• An Econometric Analysis to the World’s Major Ports

Objectives

• To study the production efficiency of container port industry

• To develop corresponding econometric tools

Features should be incorporated in an empirical model

• Controlling for individual heterogeneity: Clustering effects (by port, country, region, and port groups);

• Controlling for the technical change;

• Time varying efficiency and time persistence in efficiency change;

Output Variables

• 1. Container Throughput (TEUs)• 2. Cargo Throughput (tones)• 3. Vessel Arrivals/Departures• 4. Ship Turn Around Time

Input Variables• 1. Cargo handling equipments: Quay crane, Yard

crane, Mobile crane, Forklifts, etc;• 2. Terminal infrastructure: number of container

berths, Length of quay lines, Terminal area, etc;• 3. Labor inputs: Working hours, number of full-time

workers;• 4. Storage facilities: storage area, reefer points

Port characteristics• 1. Depth of Water• 2. Number of ship calls• 3. Ownership structure• 4. Number of Operators• 5. Corporate law system and many social

economic variables

Overview of Data

• The basic unit is operator.

• Time period is between 1997 and 2004.

• We focus on the top 100 container ports in the world (ranked in 2005)

• Data was collected from different sources:– Containerization International Yearbooks, – World Bank, and – a subscribed data base : Containerization International

Intelligence

Fig. 1 Container Throughput from 1999 to 2002

0

20000004000000

6000000

800000010000000

12000000

1400000016000000

18000000

Sin

gapo

re_p

ort

HIT

_Ter

min

alD

ubai

_Por

tM

orde

n_Te

rmin

alFe

lixst

owe

Tanj

ung_

Por

tY

antia

n_P

ort

Med

cent

erC

onta

iner

TB

urch

ardk

aiTe

rmin

alK

eelu

ng_P

ort

Kla

ngM

ultiT

erm

inal

_Sdn

_BhE

urog

ateC

onta

iner

Term

inbE

urog

ateC

onta

iner

Term

inN

orth

Sea

Term

inal

Shi

nsun

daeC

onta

iner

Term

iJa

sung

daeC

onta

iner

Term

iTe

rmin

al3_

Sea

_lan

d_O

rieH

anjin

Shi

ppin

g_C

o_Lt

dS

heko

u_P

ort

Chi

wan

_Chi

wan

Con

tain

erT

Gam

man

Glo

balC

onta

iner

TLo

ngB

each

Con

tain

erT

Gam

man

Hyu

anda

iCon

tain

Van

term

Kor

eaE

xpre

ssG

amm

anC

oN

oord

Nat

ieTe

rmin

alD

elta

port

Tolle

rortT

erm

inal

U_A

M_C

onta

iner

Term

inal

Chi

wan

_Chi

wan

Har

bour

Co

Kob

e_P

C14

&15

7thS

treet

(Ben

EN

utte

r)Con

tA

PLT

erm

inal

Mae

rskT

erm

inal

Cen

tern

T(C

asco

P&

O_P

ort

Ber

th5&

6(N

omcT

)E

stib

ador

_de_

Pon

ent

Cha

rlesP

How

ardT

Mat

son&

SS

AT

oakY

usen

TTr

ansB

ayT

(Mae

rsk)

Sea

land

T

1999

2000

2001

2002

Fig. 2 Cargo handling equipments at quay side from 1999 to 2002

0102030405060708090

Sin

gapo

re_p

ort

HIT

_Ter

min

alFe

lixst

owe

Kee

lung

_Por

tbE

urog

ateC

onta

iner

Term

iB

urch

ardk

aiTe

rmin

alM

orde

n_Te

rmin

alTa

njun

g_P

ort

Dub

ai_P

ort

Yan

tian_

Por

tM

edce

nter

Con

tain

erT

Jasu

ngda

eCon

tain

erTe

rmS

hins

unda

eCon

tain

erTe

rN

oord

Nat

ieTe

rmin

alhE

urog

ateC

onta

iner

Term

iK

lang

Mul

tiTer

min

al_S

dn_

Nor

thS

eaTe

rmin

alA

PLT

erm

inal

Tolle

rortT

erm

inal

7thS

treet

(Ben

EN

utte

r)Con

Kob

e_P

C14

&15

Long

Bea

chC

onta

iner

TV

ante

rmC

hiw

an_C

hiw

anC

onta

iner

Cen

tern

T(C

asco

P&

O_P

orS

heko

u_P

ort

(Mae

rsk)

Sea

land

TC

harle

sPH

owar

dTD

elta

port

Est

ibad

or_d

e_P

onen

tU

_AM

_Con

tain

erTe

rmin

alB

erth

5&6(

Nom

cT)

Gam

man

Glo

balC

onta

iner

Gam

man

Hyu

anda

iCon

tain

Han

jinS

hipp

ing_

Co_

Ltd

Kor

eaE

xpre

ssG

amm

anC

Mae

rskT

erm

inal

Mat

son&

SS

AT

Term

inal

3_S

ea_l

and_

Orie

oakY

usen

TTr

ansB

ayT

Chi

wan

_Chi

wan

Har

bour

C

1999200020012002

Fig. 3 Cargo handling equipments at yard from 1999 to 2002

0

200

400

600

800

1000

1200

Felix

stow

eS

inga

pore

_por

tS

hins

unda

eCon

tain

erTe

rmM

orde

n_Te

rmin

alY

antia

n_P

ort

HIT

_Ter

min

alK

lang

Mul

tiTer

min

al_S

dn_

hEur

ogat

eCon

tain

erTe

rmi

Dub

ai_P

ort

Bur

char

dkai

Term

inal

Long

Bea

chC

onta

iner

TJa

sung

daeC

onta

iner

Term

i7t

hStre

et(B

enE

Nut

ter)C

ont

Med

cent

erC

onta

iner

TK

obe_

PC

14&

15V

ante

rmG

amm

anH

yuan

daiC

onta

inbE

urog

ateC

onta

iner

Term

iN

oord

Nat

ieTe

rmin

alH

anjin

Shi

ppin

g_C

o_Lt

dTe

rmin

al3_

Sea

_lan

d_O

rieM

atso

n&S

SA

TC

ente

rnT(

Cas

coP

&O

_Por

tK

orea

Exp

ress

Gam

man

Co

Gam

man

Glo

balC

onta

iner

TD

elta

port

Kee

lung

_Por

tTa

njun

g_P

ort

She

kou_

Por

tU

_AM

_Con

tain

erTe

rmin

alC

hiw

an_C

hiw

anC

onta

iner

Tolle

rortT

erm

inal

Ber

th5&

6(N

omcT

)A

PLT

erm

inal

oakY

usen

TN

orth

Sea

Term

inal

Tran

sBay

TC

harle

sPH

owar

dTE

stib

ador

_de_

Pon

ent

Chi

wan

_Chi

wan

Har

bour

CM

aers

kTer

min

al(M

aers

k)S

eala

ndT

1999200020012002

Fig. 4 Number of berths from 1999 to 2002

05

1015

2025

3035

40

Sin

gapo

re_p

ort

Felix

stow

eK

eelu

ng_P

ort

Dub

ai_P

ort

HIT

_Ter

min

alY

antia

n_P

ort

Est

ibad

or_d

e_P

onen

tB

urch

ardk

aiTe

rmin

alhE

urog

ateC

onta

iner

Term

ibE

urog

ateC

onta

iner

Term

iC

ente

rnT(

Cas

coP

&O

_Por

tM

orde

n_Te

rmin

alTa

njun

g_P

ort

Jasu

ngda

eCon

tain

erTe

rmi

Kla

ngM

ultiT

erm

inal

_Sdn

_N

oord

Nat

ieTe

rmin

alV

ante

rmA

PLT

erm

inal

Shi

nsun

daeC

onta

iner

Term

Tolle

rortT

erm

inal

(Mae

rsk)

Sea

land

T7t

hStre

et(B

enE

Nut

ter)C

ont

Chi

wan

_Chi

wan

Con

tain

erK

obe_

PC

14&

15Lo

ngB

each

Con

tain

erT

Mat

son&

SS

AT

Nor

thS

eaTe

rmin

alC

harle

sPH

owar

dTB

erth

5&6(

Nom

cT)

Del

tapo

rtM

edce

nter

Con

tain

erT

She

kou_

Por

tTr

ansB

ayT

U_A

M_C

onta

iner

Term

inal

Chi

wan

_Chi

wan

Har

bour

CG

amm

anG

loba

lCon

tain

erT

Gam

man

Hyu

anda

iCon

tain

Han

jinS

hipp

ing_

Co_

Ltd

Kor

eaE

xpre

ssG

amm

anC

oM

aers

kTer

min

aloa

kYus

enT

Term

inal

3_S

ea_l

and_

Orie

1999200020012002

Fig. 5 Quay length (m) from 1999 to 2002

0

1000

2000

3000

4000

5000

6000

7000

Sin

gapo

re_p

ort

Felix

stow

eH

IT_T

erm

inal

Dub

ai_P

ort

Kee

lung

_Por

tM

edce

nter

Con

tain

erT

Bur

char

dkai

Term

inal

Yan

tian_

Por

tTa

njun

g_P

ort

hEur

ogat

eCon

tain

erTe

rmin

alM

orde

n_Te

rmin

albE

urog

ateC

onta

iner

Term

inal

Kla

ngM

ultiT

erm

inal

_Sdn

_Bhd

Cen

tern

T(C

asco

P&

O_P

ortC

aJa

sung

daeC

onta

iner

Term

inal

Shi

nsun

daeC

onta

iner

Term

inal

Est

ibad

or_d

e_P

onen

tV

ante

rmN

oord

Nat

ieTe

rmin

alK

obe_

PC

14&

157t

hStre

et(B

enE

Nut

ter)C

onta

inTo

llero

rtTer

min

alN

orth

Sea

Term

inal

Long

Bea

chC

onta

iner

TC

hiw

an_C

hiw

anC

onta

iner

Ter

AP

LTer

min

al(M

aers

k)S

eala

ndT

Mat

son&

SS

AT

Del

tapo

rtS

heko

u_P

ort

Cha

rlesP

How

ardT

U_A

M_C

onta

iner

Term

inal

Ber

th5&

6(N

omcT

)Tr

ansB

ayT

Gam

man

Glo

balC

onta

iner

Term

Gam

man

Hyu

anda

iCon

tain

erT

Han

jinS

hipp

ing_

Co_

Ltd

Kor

eaE

xpre

ssG

amm

anC

onta

iM

aers

kTer

min

alTe

rmin

al3_

Sea

_lan

d_O

rient

_oa

kYus

enT

Chi

wan

_Chi

wan

Har

bour

Con

ta

1999200020012002

Fig. 6 Terminal area (sqm) from 1999 to 2002

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

Sin

gapo

re_p

ort

Dub

ai_P

ort

Felix

stow

eB

urch

ardk

aiTe

rmin

albE

urog

ateC

onta

iner

Term

inTa

njun

g_P

ort

Yan

tian_

Por

tS

hins

unda

eCon

tain

erTe

rmM

edce

nter

Con

tain

erT

HIT

_Ter

min

alhE

urog

ateC

onta

iner

Term

inC

hiw

an_C

hiw

anC

onta

iner

Noo

rdN

atie

Term

inal

Mor

den_

Term

inal

Jasu

ngda

eCon

tain

erTe

rmi

Nor

thS

eaTe

rmin

alK

lang

Mul

tiTer

min

al_S

dn_B

Long

Bea

chC

onta

iner

TD

elta

port

Kee

lung

_Por

t7t

hStre

et(B

enE

Nut

ter)C

ont

AP

LTer

min

alTo

llero

rtTer

min

alV

ante

rmB

erth

5&6(

Nom

cT)

Mae

rskT

erm

inal

Mat

son&

SS

AT

(Mae

rsk)

Sea

land

TK

obe_

PC

14&

15C

ente

rnT(

Cas

coP

&O

_Por

tS

heko

u_P

ort

Cha

rlesP

How

ardT

oakY

usen

TU

_AM

_Con

tain

erTe

rmin

alTe

rmin

al3_

Sea

_lan

d_O

rieC

hiw

an_C

hiw

anH

arbo

urC

Kor

eaE

xpre

ssG

amm

anC

oG

amm

anH

yuan

daiC

onta

inH

anjin

Shi

ppin

g_C

o_Lt

dG

amm

anG

loba

lCon

tain

erT

Tran

sBay

TE

stib

ador

_de_

Pon

ent

1999200020012002

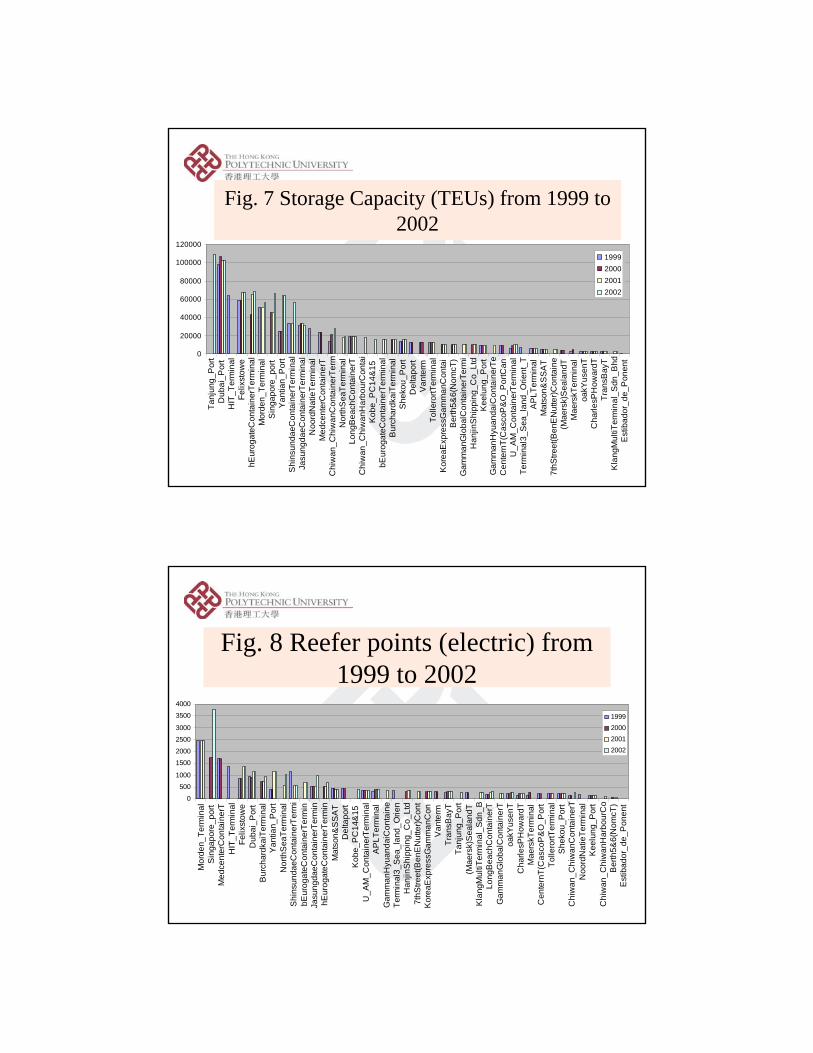

Fig. 7 Storage Capacity (TEUs) from 1999 to 2002

0

20000

40000

60000

80000

100000

120000

Tanj

ung_

Por

tD

ubai

_Por

tH

IT_T

erm

inal

Felix

stow

ehE

urog

ateC

onta

iner

Term

inal

Mor

den_

Term

inal

Sin

gapo

re_p

ort

Yan

tian_

Por

tS

hins

unda

eCon

tain

erTe

rmin

alJa

sung

daeC

onta

iner

Term

inal

Noo

rdN

atie

Term

inal

Med

cent

erC

onta

iner

TC

hiw

an_C

hiw

anC

onta

iner

Term

Nor

thS

eaTe

rmin

alLo

ngB

each

Con

tain

erT

Chi

wan

_Chi

wan

Har

bour

Con

tai

Kob

e_P

C14

&15

bEur

ogat

eCon

tain

erTe

rmin

alB

urch

ardk

aiTe

rmin

alS

heko

u_P

ort

Del

tapo

rtV

ante

rmTo

llero

rtTer

min

alK

orea

Exp

ress

Gam

man

Con

tai

Ber

th5&

6(N

omcT

)G

amm

anG

loba

lCon

tain

erTe

rmi

Han

jinS

hipp

ing_

Co_

Ltd

Kee

lung

_Por

tG

amm

anH

yuan

daiC

onta

iner

TeC

ente

rnT(

Cas

coP

&O

_Por

tCan

U_A

M_C

onta

iner

Term

inal

Term

inal

3_S

ea_l

and_

Orie

nt_T

AP

LTer

min

alM

atso

n&S

SA

T7t

hStre

et(B

enE

Nut

ter)C

onta

ine

(Mae

rsk)

Sea

land

TM

aers

kTer

min

aloa

kYus

enT

Cha

rlesP

How

ardT

Tran

sBay

TK

lang

Mul

tiTer

min

al_S

dn_B

hdE

stib

ador

_de_

Pon

ent

1999200020012002

Fig. 8 Reefer points (electric) from 1999 to 2002

0

500

1000

1500

2000

2500

3000

3500

4000

Mor

den_

Term

inal

Sin

gapo

re_p

ort

Med

cent

erC

onta

iner

TH

IT_T

erm

inal

Felix

stow

eD

ubai

_Por

tB

urch

ardk

aiTe

rmin

alY

antia

n_P

ort

Nor

thS

eaTe

rmin

alS

hins

unda

eCon

tain

erTe

rmi

bEur

ogat

eCon

tain

erTe

rmin

Jasu

ngda

eCon

tain

erTe

rmin

hEur

ogat

eCon

tain

erTe

rmin

Mat

son&

SS

AT

Del

tapo

rtK

obe_

PC

14&

15U

_AM

_Con

tain

erTe

rmin

alA

PLT

erm

inal

Gam

man

Hyu

anda

iCon

tain

eTe

rmin

al3_

Sea

_lan

d_O

rien

Han

jinS

hipp

ing_

Co_

Ltd

7thS

treet

(Ben

EN

utte

r)Con

tK

orea

Exp

ress

Gam

man

Con

Van

term

Tran

sBay

TTa

njun

g_P

ort

(Mae

rsk)

Sea

land

TK

lang

Mul

tiTer

min

al_S

dn_B

Long

Bea

chC

onta

iner

TG

amm

anG

loba

lCon

tain

erT

oakY

usen

TC

harle

sPH

owar

dTM

aers

kTer

min

alC

ente

rnT(

Cas

coP

&O

_Por

tTo

llero

rtTer

min

alS

heko

u_P

ort

Chi

wan

_Chi

wan

Con

tain

erT

Noo

rdN

atie

Term

inal

Kee

lung

_Por

tC

hiw

an_C

hiw

anH

arbo

urC

oB

erth

5&6(

Nom

cT)

Est

ibad

or_d

e_P

onen

t

1999200020012002

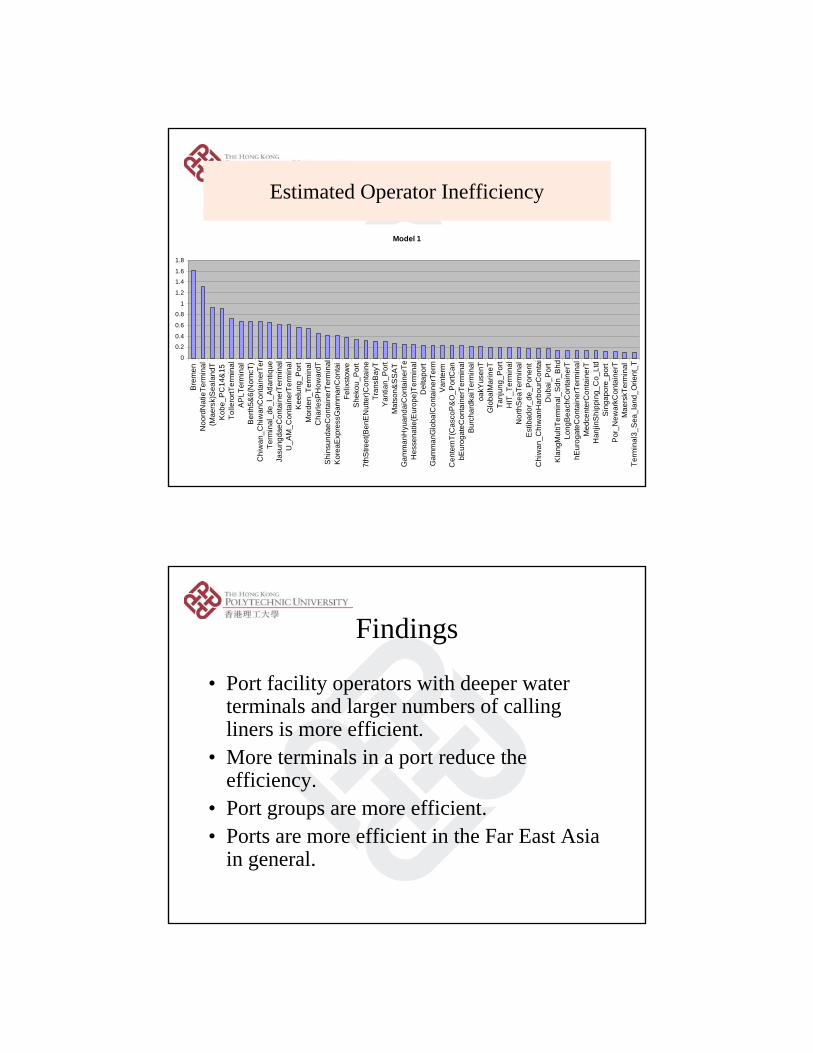

Estimated Operator Inefficiency

Model 1

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Bre

men

Noo

rdN

atie

Term

inal

(Mae

rsk)

Sea

land

TK

obe_

PC

14&

15To

llero

rtTer

min

alA

PLT

erm

inal

Ber

th5&

6(N

omcT

)C

hiw

an_C

hiw

anC

onta

iner

Ter

Term

inal

_de_

l_A

tlant

ique

Jasu

ngda

eCon

tain

erTe

rmin

alU

_AM

_Con

tain

erTe

rmin

alK

eelu

ng_P

ort

Mor

den_

Term

inal

Cha

rlesP

How

ardT

Shi

nsun

daeC

onta

iner

Term

inal

Kor

eaE

xpre

ssG

amm

anC

onta

iFe

lixst

owe

She

kou_

Por

t7t

hStre

et(B

enE

Nut

ter)C

onta

ine

Tran

sBay

TY

antia

n_P

ort

Mat

son&

SS

AT

Gam

man

Hyu

anda

iCon

tain

erTe

Hes

sena

tie(E

urop

e)Te

rmin

alD

elta

port

Gam

man

Glo

balC

onta

iner

Term

Van

term

Cen

tern

T(C

asco

P&

O_P

ortC

anbE

urog

ateC

onta

iner

Term

inal

Bur

char

dkai

Term

inal

oakY

usen

TG

loba

lMar

ineT

Tanj

ung_

Por

tH

IT_T

erm

inal

Nor

thS

eaTe

rmin

alE

stib

ador

_de_

Pon

ent

Chi

wan

_Chi

wan

Har

bour

Con

tai

Dub

ai_P

ort

Kla

ngM

ultiT

erm

inal

_Sdn

_Bhd

Long

Bea

chC

onta

iner

ThE

urog

ateC

onta

iner

Term

inal

Med

cent

erC

onta

iner

TH

anjin

Shi

ppin

g_C

o_Lt

dS

inga

pore

_por

tP

or_N

ewar

kCon

tain

erT

Mae

rskT

erm

inal

Term

inal

3_S

ea_l

and_

Orie

nt_T

Findings

• Port facility operators with deeper water terminals and larger numbers of calling liners is more efficient.

• More terminals in a port reduce the efficiency.

• Port groups are more efficient.• Ports are more efficient in the Far East Asia

in general.

Top Terminal Operators

0

20

40

60

1991 1996 2001 2003 2004

Year

Ope

rato

r Thr

ough

put (

M T

EU)

DPADurogateCoscoP&O PortsAPMPSAHPH

More and more market share

0

20

40

60

1991 1996 2001 2003 2004

Year

Wor

ld M

arke

t Sha

re (%

)

HPHPSAAPMP&O PortsCoscoDurogateDPA

Container Flows

Asia

Europe USA

13.9

4.6

12.5

5.8

3.9

2.3

Unit: Million TEUs

Alternative financing

• IPO– Initial Public Offers

• Real Options

“T” structure

Yangtze River

0

5

10

15

20

25

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Mill

ions

Year

TEU

Hong KongShenzhen

Source: Hong Kong Container Terminal Operators Association

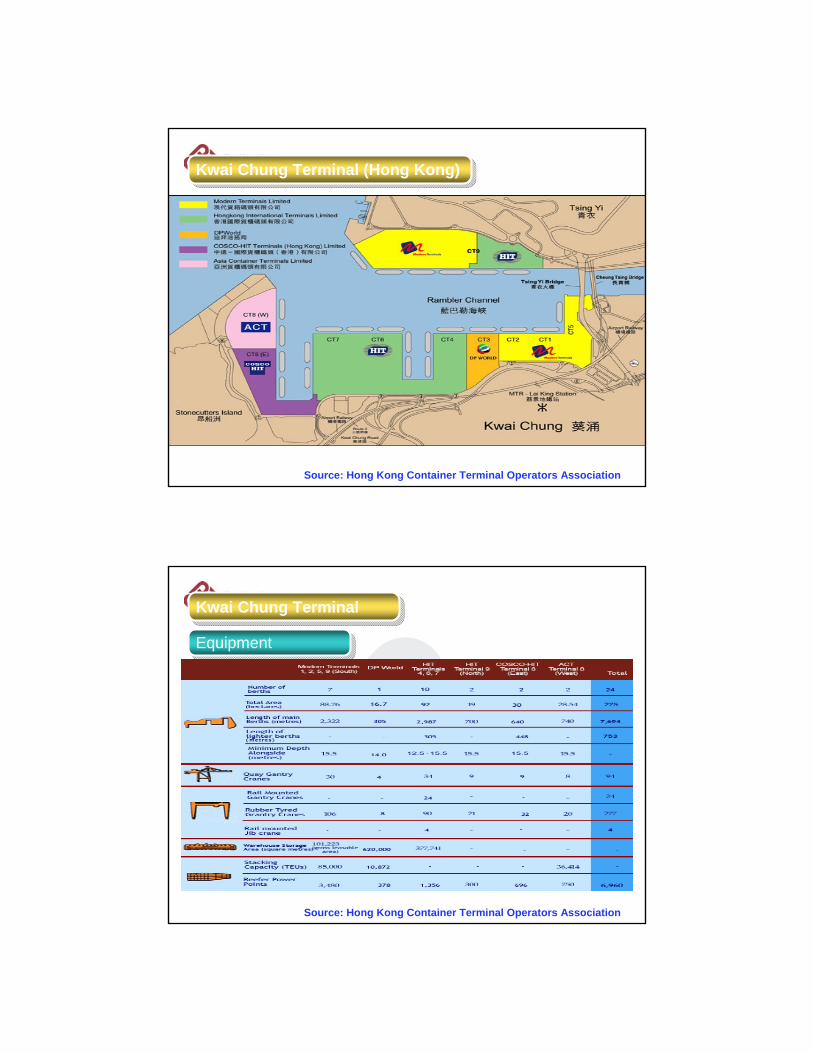

Kwai Chung Terminal (Hong Kong)Kwai Chung Terminal (Hong Kong)

Kwai Chung Terminal Kwai Chung Terminal

EquipmentEquipment

Source: Hong Kong Container Terminal Operators Association

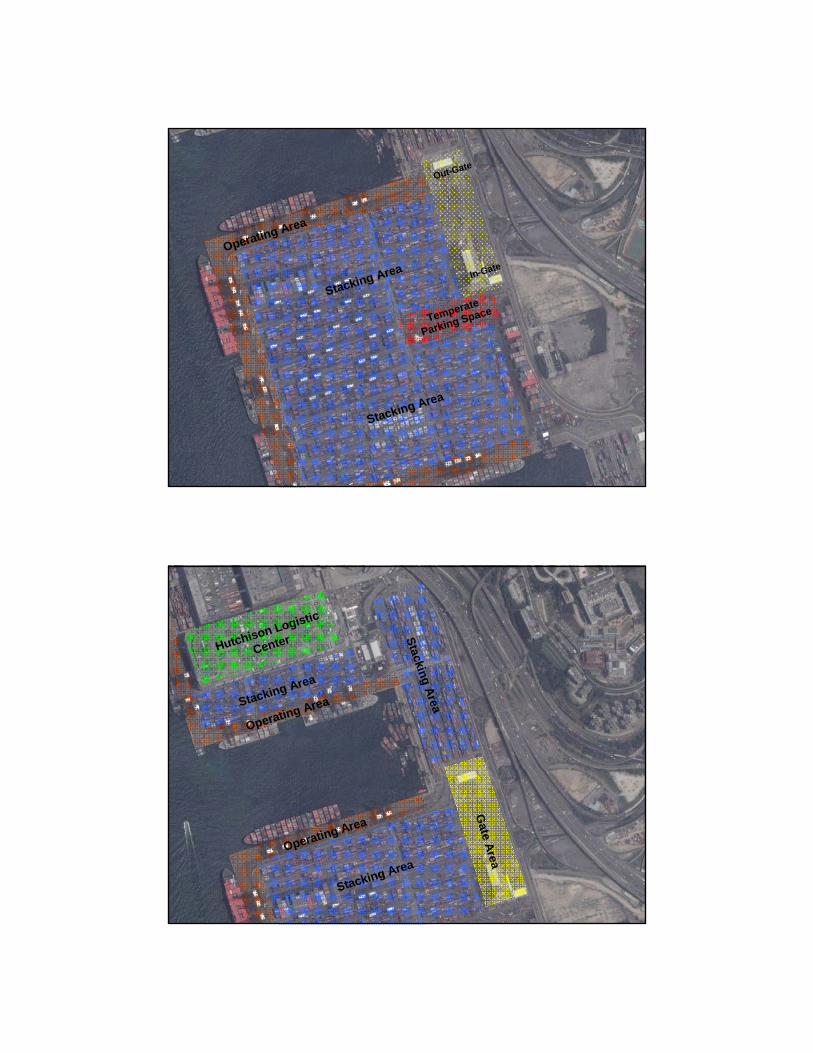

In-Gate

Out-Gate

Stacking Area

Stacking Area

Temperate

Parking Space

Operating Area

Stacking Area

Stacking Area

Hutchison Logistic

Center Stacking Area

Operating Area

Operating Area

Gate Area

Stacking Area

Parking Area

Gate Area

Logistic Center

Operating Area

Port Governance in China

• Definition of “port governance”– “Port” as a corporation– The port governance specifies the distribution of rights

and responsibilities among the different participants in the corporation.

• Port Development in China– Centralization (pre 1984)– Decentralization (1984-2001)– Corporatization (2001-)

Port Governance (2)

• Centralization (pre-1980)– Planned economy

• Provided the basic port service

– High level of centralization• Ministry of Communications (= Transport Bureau)

Port Governance (3)

• Centralization (pre-1980)Ministry of

Communications

Terminals

Port Governance (4)

• Decentralization (1984-2001)– 1978 “Open door policy”

• The limitation on the water transport price was removed in the late of 1990s gradually.

• The market became gradually free competition.

– Dual leadership (or ownership)• Ministry of Communications (= Transport Bureau)• Local authorities

Port Governance (5)

• Decentralization (1984-2001)Ministry of

Communications

Terminals

Local Government

Port Governance (6)

• State-owned enterprises (SOE)

• Foreign participation– 1990s, Hutchison Port Holdings (HPH) started

operations in Shanghai, Yantian, Ningbo and Zhuhai.

Port Governance (7)

• Corporatization (2001-)– China’s entry into WTO– 2004 “Port Law”– Central Government = Regulator– Terminals = Market player

Port Governance (8)

• Corporatization (2001-)Local Government

Terminals

Corporation JV

Port Law of China

• Dated 28th June, 2004• Definition of ports

– Fishing ports– Commercial ports

• First generation port• Traditional role of port (ship/shore interface)

Port Law of China (2)

• Implications– The Chinese central government will no longer

retain any ownership of ports– The public ports will be transferred to local

government.

Ownership

• Hongkong International Terminals (HIT)– Solely owned by

• Hutchison Port Holdings (HPH)

• Yantian Port Holding– Stock No. 0000088– Joint venture of

• Hutchison Port Holdings (HPH)• Shenzhen Yantian Port Group

China Approach

• The government (national or province) does not manage the terminals directly.

• Foreign Direct Investment (FDI) is conducted in the form of joint venture. Foreign companies were in effect restricted to holding less than 50% share of joint venture.

China Approach (2)

• Foreign companies act as both investors and managers. Local authorities act as mainly landlord of the terminals.

• The joint venture offers easier access to new technologies (for the benefits of China) and to new markets (in favour of foreign companies).

Shenzhen Corporation ModelShenzhen Government

Terminal JV

Corporation Port Authority

Ministry of Communications

Overseas Firms

regulation

Port Privatisation

• Port privatization may not create or improve port infrastructure and facilities to benefit the local economy.

• Investment in port infrastructure does not often lead to port traffic.

Summary

• The Port Benchmark Study shows that:– Global terminal operators are more efficient.– Asian ports are more efficient.– Ownership has little impacts on technical

efficiency.