company confidential

Regulations for the Digital Economy

Session 8: Digital Services, E-Governance and the Digital Economy

Commonwealth Broadband Asia Forum 2016

21st – 23rd Sept 2016

2company confidential

3company confidential

With The Increase Of OTT Players, The Digital Economy And Value Chain

Have Become Very Complex And Global

Source: GSMA, AT Kearney

4company confidential

Mobile Operators Are Now A Small Part Of The Overall Ecosystem

The bigger pie of the industry

Source: GSMA, AT Kearney

5company confidential

The Fourth Industrial Revolution: The digital economy has potential to

add up to USD 1TRILLION to ASEAN GDP over the next 10 years

Source: AT Kearney Digital Revolution

6company confidential Source: News Articles, Axiata, GSMA, Analysys Mason

WhatsApp voice launched binq early 2015, others

like Viber, WeChat etc. available by end of 2013

MY: TOTAL SMS INDUSTRY REVENUES & ARPU(only Celcom, DiGi, Maxis)

MY: TOTAL VOICE INDUSTRY REVENUES & ARPU

(only Celcom, DiGi, Maxis)

Total Net Revenues in bn. US$, Monthly SMS ARPU per

Sub in US$

Total Net Revenues in bn. US$, Monthly Voice ARPU per

Sub in US$

2.4 2.2 1.9 1.60

2

4

0,5

1,0

-12,3%

0,9150,9240,743

0,5460,839

1,2

RevenuesAvg. ARPU

7.47.88.08.29.40

10

204

2

‘12‘11

3,6243,5053,677

‘10

-1,3%

‘14

3,634 3,483

‘13

RevenuesAvg. ARPU

WhatsApp messaging launched in late 2009 in the US

Challenges to the sector are considerable: Revenue from traditional

voice and SMS services is static / falling. OTT substitution will affect

future ability reinvest into network and innovative services

WhatsApp free voice calls: “The new service, could help wipe hundreds of

billions of dollars from the revenues of mobile carriers in the next five years,

say analysts”. - The Financial Times, February 2014

“Declining growth in operator voice and SMS revenues will accelerate to -6%

annually in the five years to 2025 reflecting continuation of the current

migration of comms to IP messaging platforms, and will become more

substitutive as smartphone penetration rises”. – GSMA, February 2016

“Global annual SMS revenues will fall to around US$97 Bn in 2018,

down from US$120 Bn in 2013... annual Asia Pacific SMS revenues

to drop from US$45.8 Bn in 2013, to US$38 Bn in 2018” –

Telecoms.com, November 2013

7company confidential

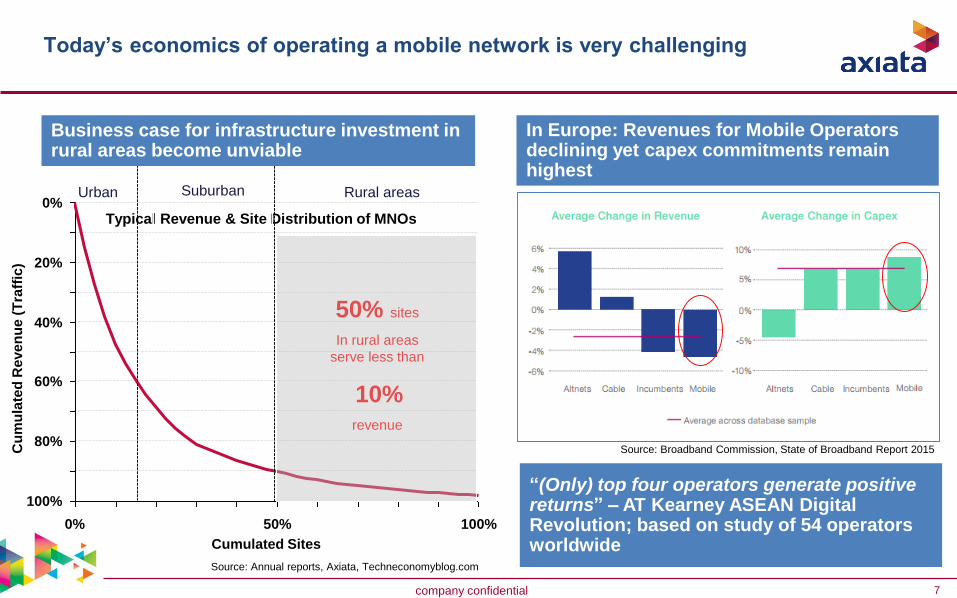

Today’s economics of operating a mobile network is very challenging

Source: Annual reports, Axiata, Techneconomyblog.com

Typical Revenue & Site Distribution of MNOs

Urban Rural areasSuburban

0% 100%

20%

0%

60%

40%

80%

50%

100%

Cu

mu

late

d R

eve

nu

e (

Tra

ffic

)

Cumulated Sites

50% sites

In rural areas

serve less than

10%revenue

In Europe: Revenues for Mobile Operators declining yet capex commitments remain highest

Business case for infrastructure investment in rural areas become unviable

Source: Broadband Commission, State of Broadband Report 2015

“(Only) top four operators generate positive returns” – AT Kearney ASEAN Digital Revolution; based on study of 54 operators worldwide

8company confidential

Meet High Quality Regulatory

Principles?

1. Long-term interest of consumers

allows regulators to balance a range of

competing aims e.g. affordability, service

quality, service choice and safety

2. Non-discrimination and technology neutral

ensures rival services compete on the merits

of the value that they offer consumers, rather

than on the basis of some unfair advantage

3. Innovation

ensure competitive incentives remain to

promote genuine innovation that creates

additional value for consumers.

4. Proportionality

ensure that regulation is intended to address

identifiable specific risk of harm.

5. Responsiveness

ensure regulatory frameworks evolves to

reflect technological, economic etc. changes

Business model

MNOs OTTs

• Regulated, licenced, high-

CAPEX, long-term and

nationally-based

• Focus on connectivity / services,

• Customer data for user

enrichment

• Unregulated, global and

“seasonal”

• Mostly centred around use of

consumer data (service not

‘free’)

• Applicable in line with domestic

laws

• Multiple licenses with >200

including obligations on rollout,

interconnection and CSR

• Usually no license needed;

maybe in home country

jurisdiction only

• Exposed to minimal

obligations

• Sector-specific fees e.g.

spectrum, USO, licence and

general corporate taxes

• Horizontal laws; sector obligations

• Rules on data localisation,

retention, disaster recovery and LI

• Uncertain enforcement

• Minimal restrictions on data

location, retention and LI

Licensing

Taxation

Privacy &

Security

Consumer

Protection

• Customer-centric obligations e.g.

transparency, contract info, QoS,

SMP, emergency services

• No specific enforcement

outside major countries

Current debate on Level-Playing-Field: Same Rules regardless of

difference in technology or business model adopted, for services that are

functionally or economically substitutable

Source: GSMA, Web Henderson, News articles

• No sector-specific taxes,

freedom to structure business

primarily for tax planning

9company confidential

SSSR measures

adopted

SSSR proposed

or debated

There are increasing trends by policy makers to capture OTTs and non-

traditional providers under revised / new national laws and regulations

Examples of Revised OTT Treatment via SSSR rules*

• EU: Digital Single Market reform (‘16)

• MY, AU: Discussions on regulating Uber

• PH: Regulatory Framework for Uber (‘15)

• MX: Establishing OTT regulations

• ID: Proposed OTT regulations; e-coms law

• IN: Proposed regulation of Internet-based

domestic calling apps

• UK: Diverted Profits Tax (‘14)

• AU: Sharing Economy & Tax Guidance (‘15)

• OECD/G20: BEPS (’15/16)

• KR: To introduce “Google Tax” (‘16)

• IT: To introduce “digital tax” (‘16)

• NZ, AU: GST on online goods (‘16)

• EU: GPDR under market reforms (‘16)

• IN: Draft LI framework; new digital levy (‘16)

• FI: Information Society Code (‘14) incl. OTT

privacy, security & cons. protection

• BE: Claim Skype is a telecoms operator

• DE: Claim Gmail is a telecoms service

• EU, RU, DE: Antitrust claims

Addressing this will:

1. Meet long-term interest of consumers, promote digital innovation and ensure MNOs will be able to reinvest into the network.

2. Ensure international OTTs with relaxed rules will not impair the development of local OTTs

3. Ensure government to a certain extend will continue to have control on content, application services and customer data

Genera

lLic

ensin

gT

axation

Priv.; C

ons.

Pro

t.

Note:*non-exhaustive; Source: GSMA, Web Henderson, News articles

10company confidential

Still early stages but proving to be gaining traction

Most enforcement cases or examples are based on competition and tax

evasion but expect the issue on licensing to further increase

11company confidential

Mobile Financial Services can contribute to the Financial Inclusion agenda;

there are more people having a mobile phone than a bank account

High-level principles and recommendations

Secure top-level support and commitment to

achieve national level financial inclusion goals

Enable open and competitive landscape, allow

banks and non-banks to participate on equal

terms

Regulations to cater to the level of market

maturity and development state of MFS

Regulations to be risk-based and proportionate

to encourage market entry and MFS adoption

Strive for interoperable MFS systems when the

market is ready

Cross-regulatory coordination

Use-case: Digital Government finances for

economies of scaleOTC, Money transfers

Remittance

Disbursements (G2P, salaries), Bill payments

Savings, Insurance

Investment, Credit

1: Basic 2: Emerging 3: Deepening 4: Mature

Mobile Financial Services

Source: TRPC, Axiata

12company confidential

Axiata is ready to support and play our part to grow Digital Economies,

pushing for cashless societies, smart cities, borderless digital services

and financial inclusion

The rapid innovation that characterizes the Internet and Digital Economy is an exciting opportunity for countries to accelerate

their economic development and leapfrog into the Fourth Industrial Revolution. Some topics to contribute to the discussion:

Equivalence

• Basis of regulation could be “Same Service,

Same Rules”, regardless of difference in

technology or business model adopted, for

functionally or economically substitutable

services; including application of taxation.

• Regulations could be rolled back where no

longer required. Sector-specific regulations

(e.g. licensing & authorizations tier

structures/categories) could be in time be

simplified or scaled-back.

• Reduction of sector-specific regulations and

increasing reliance on horizontal legislation

to consistently address issues like

competition, customer data privacy, data

retention, LEA.

Building Trust and Security

• National e-Identity system to authenticate

online transactions (e.g. banking, G2C

services). For simplicity and practical

implementation purposes, ‘sit’ within the

mobile SIM card.

• Regulations which are equivalent across

countries e.g. consumer protection, data

protection and privacy, proportionate KYC.

Larger ‘single market’ with have similar rules

will allow for greater innovation and cross-

border electronic payments and transactions.

• Coordinate national cybersecurity

management and monitoring between

various authorities or setup a regional

cybersecurity centre or agency.

Catalyse and Build

• With Mobile Financial Services, allow both

bank-led and non-bank-led models to work.

In certain markets, mandate interoperability

between service providers and open up

bottlenecks preventing greater adoption e.g.

Point-of-Sale Terminals, ATMs.

• Catalyse adoption with Government

payments and disbursements via m-money,

like G2C e-services which were introduced to

catalyse use of ICT.

• Showcase of smart-cities infrastructure

(enabled by IoT, M2M) possibly via PPP

models.

13company confidential

Thank You