SCARCITY

absolute advantage absolute advantage capital capital command economy command economy comparative advantagecomparative advantageconsumer goods consumer goods consumer sovereignty consumer sovereignty economic growth economic growth economic problem economic problem InvestmentInvestmentProductive resourcesProductive resources::natural resourcesnatural resourcescapital resource capital resource human resource human resource (including human capital) (including human capital)

Terms to Know and Apply

Economic decisionsEconomic decisions::ScarcityScarcitychoicechoicecosts and benefits costs and benefits opportunity costopportunity costmarginal (added) costmarginal (added) costtrade-offstrade-offslaissez-faire economylaissez-faire economyopportunity costopportunity costMarketMarketOutputsOutputsPricePriceProductionProductionresources or inputsresources or inputsthree basic questionsthree basic questions

Terms to Know and Apply

Goods and servicesGoods and services::producersproducersconsumersconsumersbuyersbuyerssellerssellersproductionproductiondistributiondistributionconsumptionconsumptionchannels of distributionchannels of distributionmarketingmarketing

The basic economic problem that arises because people have unlimited wants but resources are limited. Because of scarcity, various economic decisions must be made to allocate resources efficiently. Sca

rcity

When we talk of scarcity within an economic context, it refers to limited resources, not a lack of riches. These resources are the inputs of production: land, labor and capital.

People must make choices between different items because the resources necessary to fulfill their wants are limited. These decisions are made by giving up (trading off) one want to satisfy another.

There is only so much wheat grown every year. Some people want bread; some people want cereal; some people want beer, and so on. Only so much of any one product can made because of the scarcity of wheat. How do we decide how much flour should be made for bread?

Because of scarcity people have to make choices, choices have costs and benefits

People are likely to make the choice that has the most benefit to them, with the least cost, or, put another way, the choice that provides more in benefits than it costs.

Scarcity requires choice. People must choose which of their desires they will satisfy and which they will leave unsatisfied.

When we, either as individuals or as a society, choose more of something, scarcity forces us to take less of something else. Economics is sometimes called the study of scarcity because economic activity would not exist if scarcity did not force people to make choices

If not for choice our economic system would not work.

What if we only had one car maker to choose from?What if we only had one company that made bread?, cereal?, soft drinks?

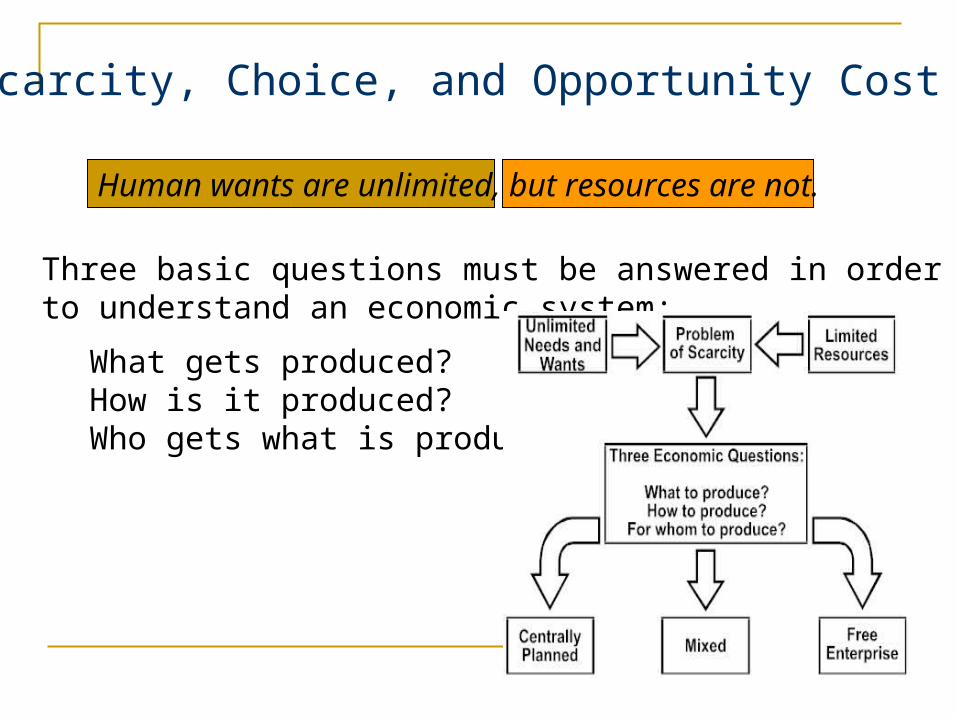

Human wants are unlimited, but resources are not.

Scarcity, Choice, and Opportunity Cost

Three basic questions must be answered in order to understand an economic system:

What gets produced?How is it produced?Who gets what is produced?

•Every society has some system or mechanism that transforms that society’s scarce resources into useful goods and services.

Scarcity, Choice, and Opportunity Cost

The basic resources that are available to a society are factors of production:

LandLaborCapital

Capital refers to the things that are themselves produced and then used to produce other goods and services

Production is the process that transforms scarce resources into useful goods and services.

Resources or factors of production are the inputs into the process of production; goods and services of value to households are the outputs of the process of production.

Nearly all the basic decisions that characterize complex economies must also be made in a single-person economy.

Constrained choice and scarcity are the basic concepts that apply to every society

A producer has an absolute advantage over another in the production of a good or service if it can produce that product using fewer resources.

Scarcity and Choicein an Economy of Two or More

Daily ProductionWood(logs)

Food(bushels)

Colleen 10 10

Bill 4 8

•Colleen has an absolute advantage in the production of both wood and food because she can produce more of both goods using fewer resources than Bill.

Daily ProductionWood(logs)

Food(bushels)

Colleen 10 10

Bill 4 8

In terms of wood: For Bill, the opportunity cost of 8 bushels of food is 4 logs. For Colleen, the opportunity cost of 8 bushels of food is 8 logs.

In terms of food: For Colleen, the opportunity cost of 10 logs is 10 bushels of

food. For Bill, the opportunity cost of 10 logs is 20 bushels of food.

Suppose that Colleen and Bill each wanted equal numbers of logs and bushels of food. In a 30-day month they could produce

Daily Production

Wood(logs)

Food(bushels)

Colleen 10 10

Bill 4 8

Monthly Production with No Trade

Wood(logs)

Food(bushels)

Colleen 150 150

Bill 80 80

Total 230 230

Monthly Production after Specialization

Wood(logs)

Food(bushels)

Colleen 270 30

Bill 0 240

Total 270 270

By specializing on the basis of comparative advantage, Colleen and Bill can produce more of both goods.

To end up with equal amounts of wood and food after trade, Colleen could trade 100 logs for 140 bushels of food. Then:

Monthly Production after Specialization

Wood(logs)

Food(bushels)

Colleen 270 30

Bill 0 240

Total 270 270

Monthly Use After Trade

Wood(logs)

Food(bushels)

Colleen 170 170

Bill 100 100

Total 270 270

The economic problem: Given scarce resources, how, do large, complex societies go about answering the three basic economic questions?

Economic systems are the basic arrangements made by societies to solve the economic problem. They include: Command economies Laissez-faire economies Mixed systems

In a command economy, a central government either

directly or indirectly sets output targets, incomes, and prices.

Economy planned and directed by government, where resources are allocated to factories by the state through central planning. This system is unresponsive to the needs and whims of consumers and to sudden changes in conditions (for example, crop failure or fluctuations in the world price of raw materials).

For example, in the former USSR, state planners decided what was to be produced. They passed orders down to factories, allocating raw materials, workers, and other factors of production to them. Factories were then told how much they should produce with these resources and where they should be sent. If there was a shortage of goods in the shops, then goods would be rationed through queuing.

In a laissez-faire economy, individuals and firms pursue their own self-interests without any central direction or regulation.

The central institution of a laissez-faire economy is the free-market system.A market is the institution through which buyers and sellers interact and engage in exchange.

In a laissez-faire economy, the distribution of output is also determined in a decentralized way. The amount that any one household gets depends on its income and wealth.

Consumer sovereignty is the idea that consumers ultimately dictate what will be produced (or not produced) by choosing what to purchase (and what not to purchase).

The theory of consumer sovereignty says that, while businesses and companies can produce anything they choose, if consumers do not want or need a product, it will not sell. If a product is not sold, it will not continue to be produced. Therefore, buyers ultimately decide what is produced.

Under a free market system, individual producers must figure out how to plan, organize, and coordinate the production of products and services.

Free Enterprise is an economic system where few restrictions are placed on business activities and ownership. In this system, governments generally have minimal ownership of enterprises in the market place. This system aims for limited restrictions on trade and minimal government intervention.

Free Enterprise

The basic coordinating mechanism in a free market system is price. Price is the amount that a product sells for per unit. It reflects what society is willing to pay.

In economics, price is determined by what (1) a buyer is willing to pay, (2) a seller is willing to accept, and (3) the competition is allowing to be charged. With product, promotion, and place of marketing mix, it is one of the business variables over which organizations can exercise some degree of control

Capitalism and Free Enterprise are interchangeable. Capitalism: an economic system in which resources and means of production are privately owned and prices, production, and the distribution of goods are determined mainly by competition in a free market. The United States in a capitalist economy.

Since markets are not perfect, governments intervene and often play a major role in the economy. Some of the goals of government are to: Minimize market inefficiencies Provide public goods Redistribute income Stabilize the macroeconomy:

Promote low levels of unemployment Promote low levels of inflation

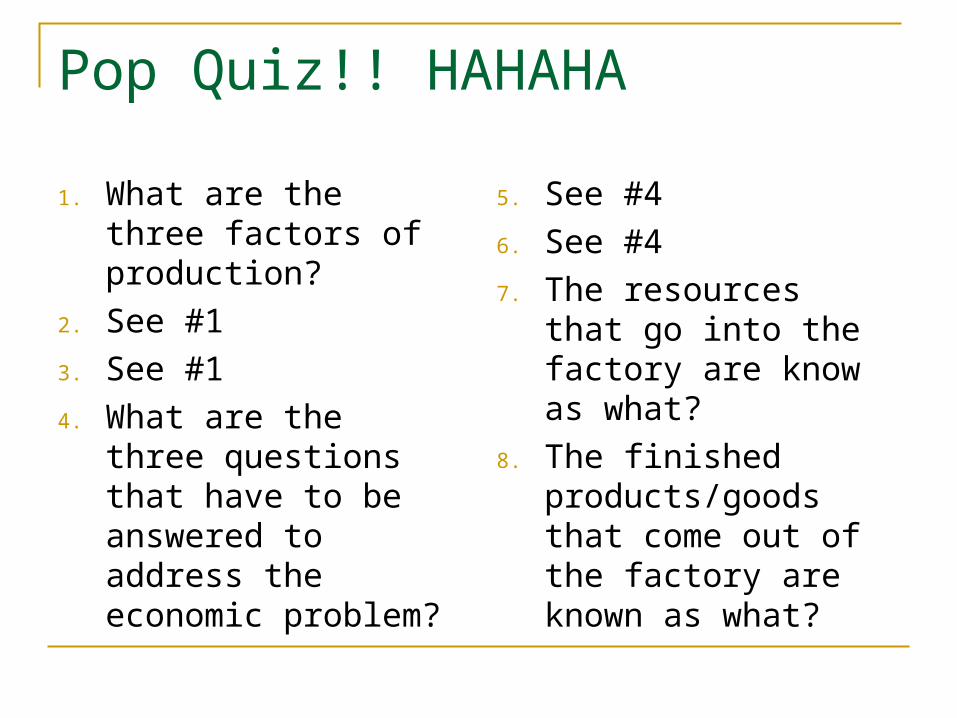

Pop Quiz!! HAHAHA

1. What are the three factors of production?

2. See #1

3. See #1

4. What are the three questions that have to be answered to address the economic problem?

5. See #4

6. See #4

7. The resources that go into the factory are know as what?

8. The finished products/goods that come out of the factory are known as what?

Supply and DemandSupply and Demand Supply- the amount of product that a Supply- the amount of product that a

producerproducer is willing and able to is willing and able to sellsell at a at a specified price.specified price.

Demand- the amount of product that a Demand- the amount of product that a consumerconsumer is willing and able to is willing and able to buybuy at a at a specified pricespecified price

Efficiency- performing with little or no wasteEfficiency- performing with little or no waste

Supply and demand:supply curvedemand curve equilibrium priceElasticinelasticSubstitutescomplementsShortagesurplusFactors affecting supply or demand:price of the productprice of inputscompetition

Terms to Know and Apply

price of related (complementary or substitute) productstechnological changeconsumer tastesPreferencesincome levels Factors of production (i.e., land, labor, capital, and entrepreneurship)Factors affecting production and distribution:IncentiveProfitrisk Pricerelative price capital investment supply and demand consumption vs. saving

Terms to Know and Apply

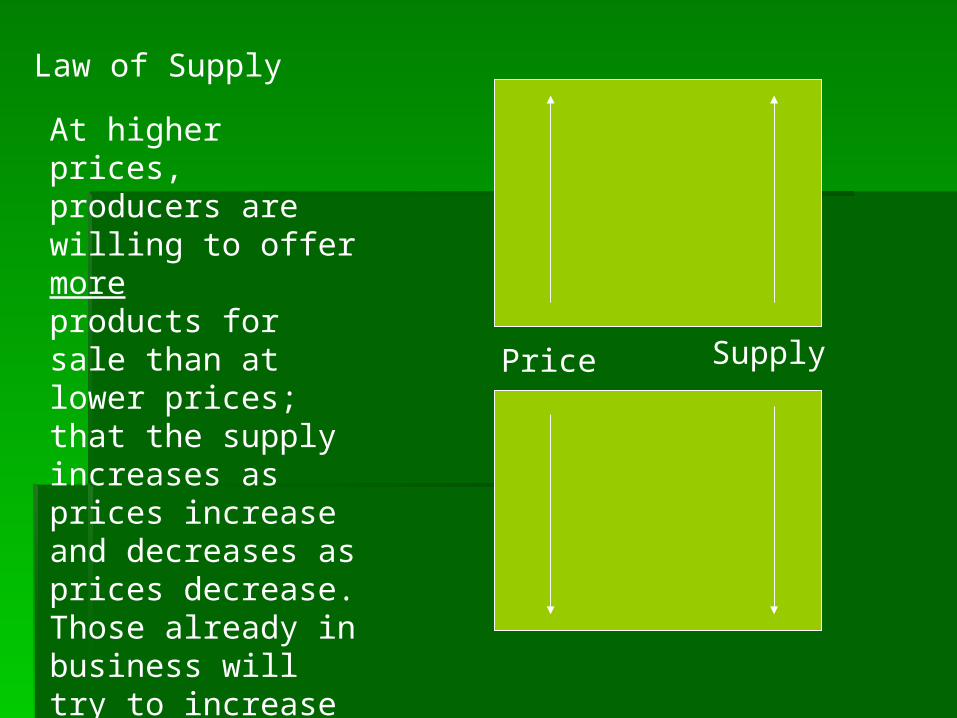

At higher prices, producers are willing to offer more products for sale than at lower prices; that the supply increases as prices increase and decreases as prices decrease. Those already in business will try to increase productions as a way of increasing profits.

Law of Supply

Price Supply

Consumers will buy more of a product at a lower price than at a higher price, if nothing changes. At a lower price, more people can afford to buy more goods and more of an item more frequently, than they can at a higher price. At lower prices, people tend to buy some goods as a substitute for others more expensive

Law of Demand

Price Demand

The law of supply and demand is not an actual law but it is well confirmed and understood realization that if you have a lot of one item, the price for that item should go down. At the same time you need to understand the interaction; even if you have a high supply, if the demand is also high, the price could also be high.

The Law of Supply and Demand

Determinants of Demand

•Consumer tastes

•Consumer income

•Number of buyers

•Prices of complements and substitutes

•Consumer expectations

A product can be considered a complement when it shares a beneficial relationship with another product offering. When the price of a good rises, the demand for its complement will fall because consumers don't want to use the complement alone For example, if the price of hot

dogs rises so much that people stop consuming them, this will also cause a decrease in demand for hot dog buns. Because the price of hot dogs has an inverse relationship to the demand for hot dog buns, we call them complementary products.

Complements

A substitute is something that can be used instead of a particular good or service. For example, beef can be substituted for chicken. If the price of chicken increases relative to the price of beef, people will buy more beef

Substitutes

A substitute can also be an inferior good. A store brand for a name brand.Great Value for Del Monte

Demand ScheduleDemand Schedule

Price of WidgetsPrice of Widgets # of widgets people # of widgets people want to buywant to buy

$1.00$1.00 100100

$2.00$2.00 9090

$3.00$3.00 7070

$4.00$4.00 4040

The demand schedule is a table of the quantity demanded of a good at different price levels. Given the price level, it is easy to determine the expected quantity demanded.

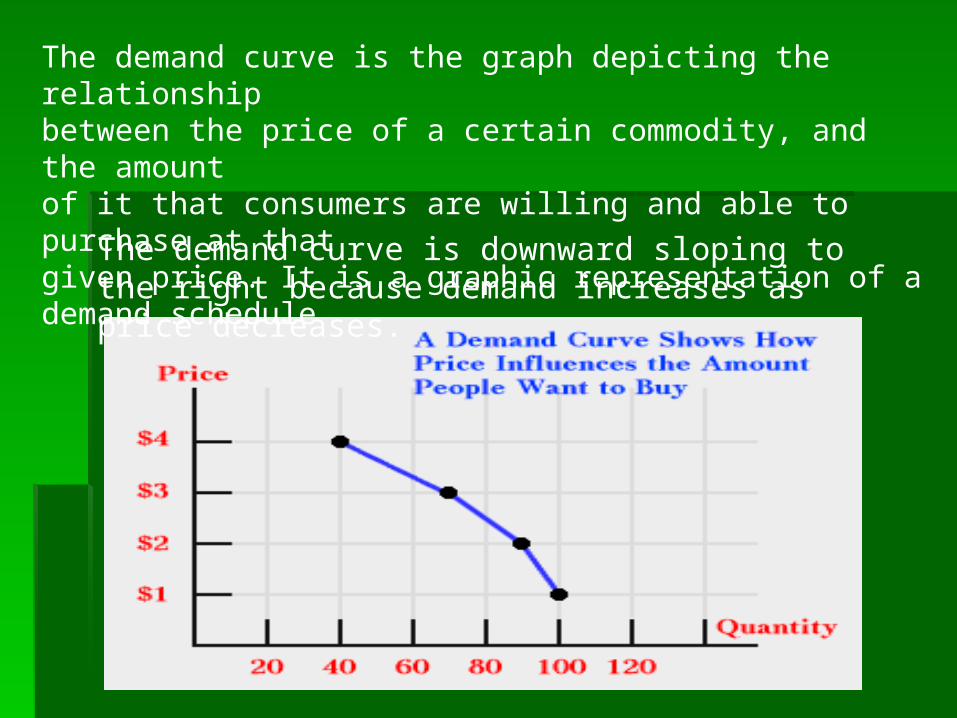

The demand curve is the graph depicting the relationship between the price of a certain commodity, and the amount of it that consumers are willing and able to purchase at that given price. It is a graphic representation of a demand schedule

The demand curve is downward sloping to the right because demand increases as price decreases.

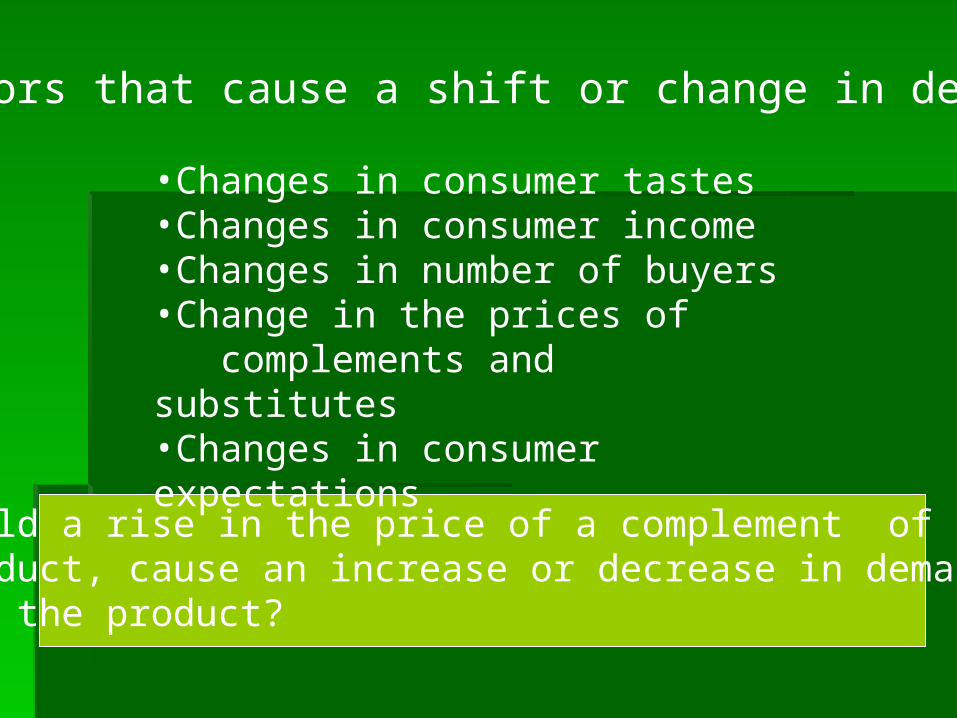

•Changes in consumer tastes•Changes in consumer income•Changes in number of buyers•Change in the prices of complements and substitutes•Changes in consumer expectations

Factors that cause a shift or change in demand

Would a rise in the price of a complement of a product, cause an increase or decrease in demand for the product?

Shift in DemandShift in Demand

Price of Price of WidgetsWidgets

# of # of widgets widgets people people want to want to

buybuy

$1.00$1.00 8080

$2.00$2.00 7070

$3.00$3.00 5050

$4.00$4.00 1010

Price of Price of WidgetsWidgets

# of # of widgets widgets people people want to want to

buybuy

$1.00$1.00 100100

$2.00$2.00 9090

$3.00$3.00 7070

$4.00$4.00 4040

Original New

A decrease in demand will cause a shift to the left on the demand curve as shown below.

Conversely an increase in demand will cause a shift to the right.

Supply ScheduleSupply Schedule

Price of WidgetsPrice of Widgets # of widgets sellers # of widgets sellers want to sellwant to sell

$1.00$1.00 1010

$2.00$2.00 4040

$3.00$3.00 7070

$4.00$4.00 140140

The supply schedule is a table of the quantity supplied of a good at different price levels. Given the price level, it is easy to determine the expected quantity supplied.

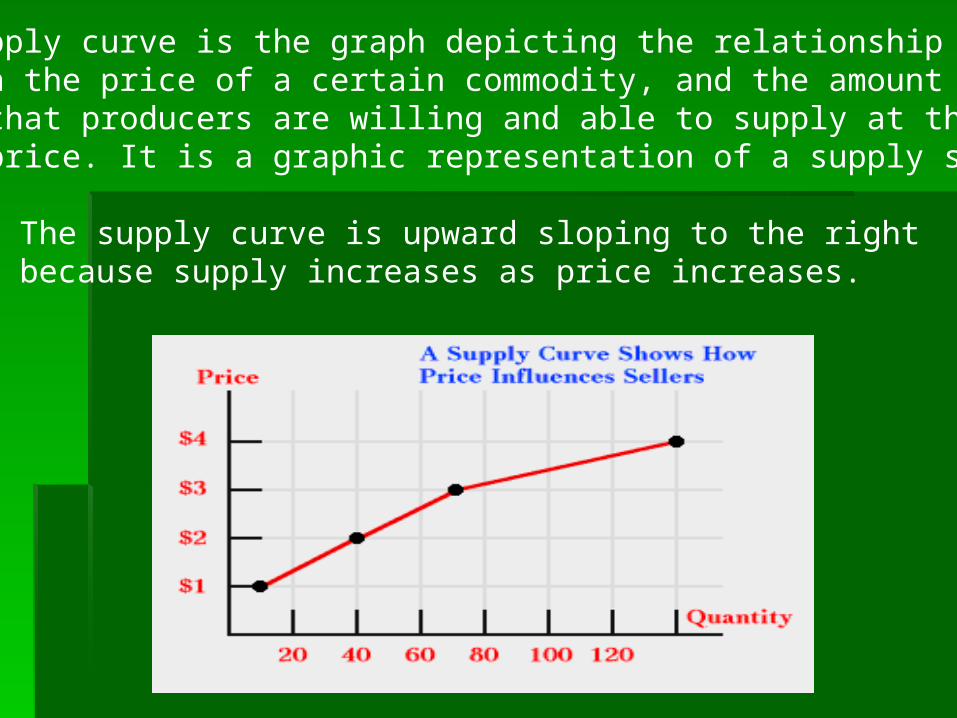

The supply curve is the graph depicting the relationship between the price of a certain commodity, and the amount of it that producers are willing and able to supply at that given price. It is a graphic representation of a supply schedule

The supply curve is upward sloping to the right because supply increases as price increases.

Shift in SupplyShift in Supply

Price of Price of WidgetsWidgets

# of # of widgets widgets

sellers want sellers want to sellto sell

$1.00$1.00 2020

$2.00$2.00 6060

$3.00$3.00 100100

$4.00$4.00 180180

Price of Price of WidgetsWidgets

# of # of widgets widgets

sellers want sellers want to sellto sell

$1.00$1.00 1010

$2.00$2.00 4040

$3.00$3.00 7070

$4.00$4.00 140140

An increase in supply will cause a shift to the right on the supply curve as shown below.

Conversely a decrease in supply will cause a shift to the left.

Ceteris paribus, the market will reach equilibrium where the supply and demand schedules intersect. At this point, the corresponding price will be the equilibrium market price, and the corresponding quantity will be the equilibrium quantity exchanged in the market.

Supply and Demand TogetherSupply and Demand Together

A demand schedule is typically used in conjunction with a supply schedule showing the quantity of a good that would be supplied to the market at given price levels. Then, graphing both schedules on a chart with the axes described above, it is possible to obtain a graphical representation of the supply and demand dynamics of a particular market.

Supply and Demand Supply and Demand TogetherTogetherPrice of WidgetsPrice of Widgets # of widgets # of widgets

people want to buypeople want to buy# of widgets # of widgets

sellers want to sellsellers want to sell

$1.00$1.00 100100 1010

$2.00$2.00 9090 4040

$3.00$3.00 7070 7070

$4.00$4.00 4040 140140

Supply curve for the previous supply schedule

EquilibriumEquilibrium Still another Still another

view of supply view of supply and demand and demand curves, to curves, to view demand view demand as points of as points of buyer buyer equilibrium equilibrium and supply as and supply as points of points of seller seller equilibriumequilibrium

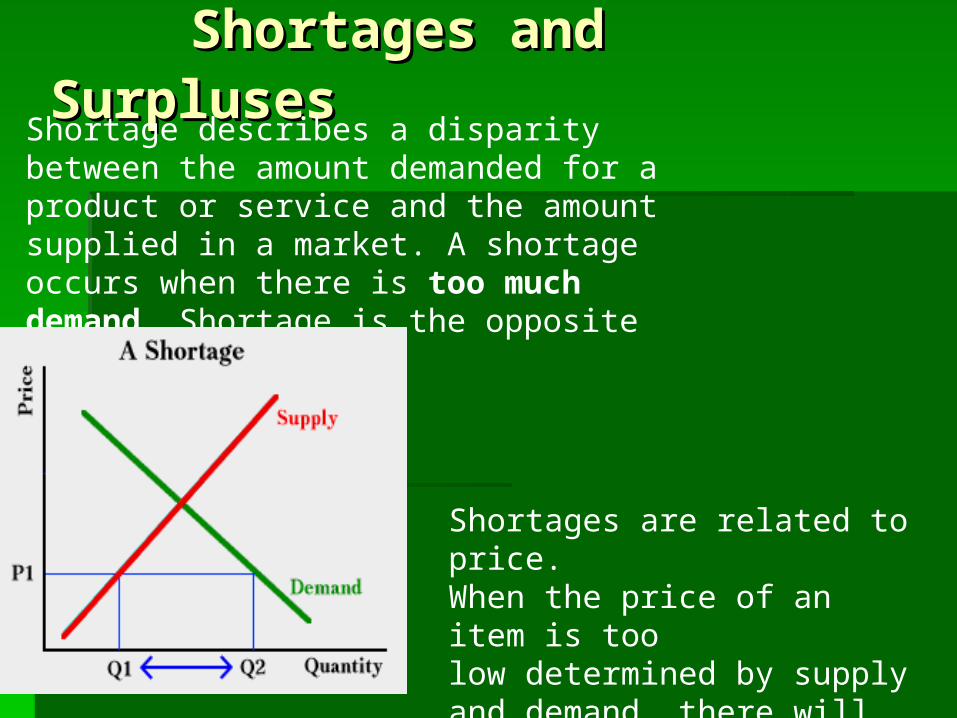

Shortages and SurplusesShortages and Surpluses In other words, at the lowest price the smallest quantity will be sold

If price is originally P1 in the graph, only Q1 will be sold even though buyers would like to buy Q2. The difference Q2 - Q1 represents a shortage. The sellers are in equilibrium in this situation because they can sell everything they want to sell at this price, but buyers are not. Some buyers who cannot obtain the product are willing to offer more, and sellers are always willing to accept a higher price.

Therefore, the actions of the buyers, as they compete with each other to obtain the amount that is available, drive the price upward in this model toward market equilibrium.

Shortages and SurplusesShortages and Surpluses Shortage describes a disparity between the amount demanded for a product or service and the amount supplied in a market. A shortage occurs when there is too much demand. Shortage is the opposite of a surplus.

Shortages are related to price. When the price of an item is too low determined by supply and demand, there will be a shortage

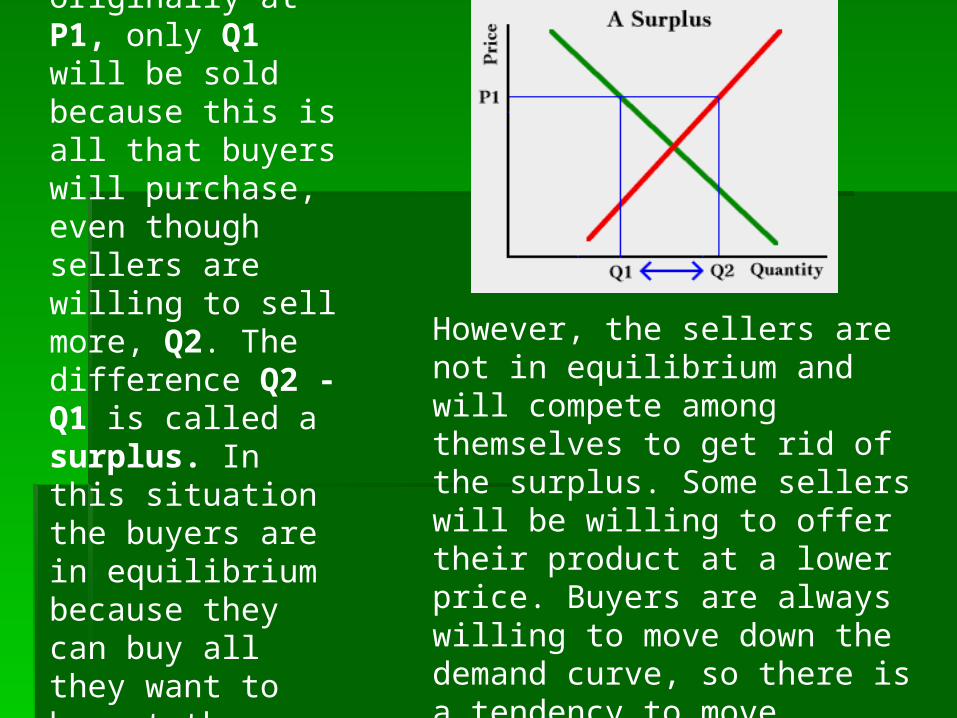

If price is originally at P1, only Q1 will be sold because this is all that buyers will purchase, even though sellers are willing to sell more, Q2. The difference Q2 - Q1 is called a surplus. In this situation the buyers are in equilibrium because they can buy all they want to buy at the going price.

However, the sellers are not in equilibrium and will compete among themselves to get rid of the surplus. Some sellers will be willing to offer their product at a lower price. Buyers are always willing to move down the demand curve, so there is a tendency to move downward toward market equilibrium.

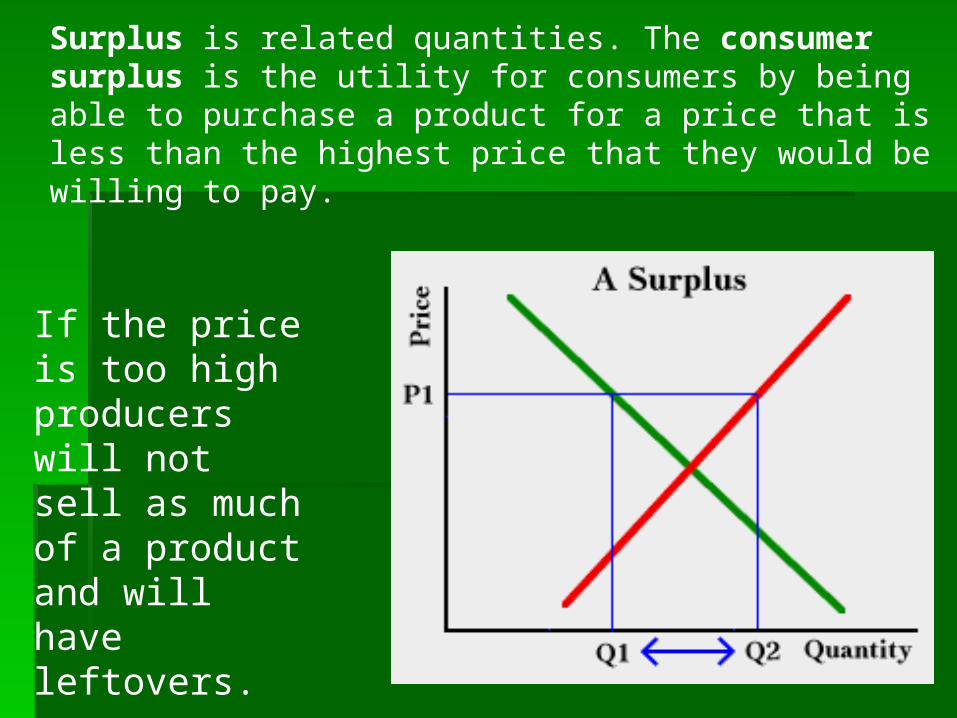

Surplus is related quantities. The consumer surplus is the utility for consumers by being able to purchase a product for a price that is less than the highest price that they would be willing to pay.

If the price is too high producers will not sell as much of a product and willhave leftovers.

At a price of 3 what would be the quantity demanded?

At a price of 3 what would be the quantity supplied?

At a price of 3 what would there be a surplus or shortage?

If the price was shown at 6, estimate what the amount demanded would be?

Why do you think producers supply more at a higher price than they do at a lower price?

If the price is too low and the demand becomes too high for the amount, supplied what economic condition would producers and consumers be in?

The price elasticity of demand measures the rate of response of quantity demanded due to a price change.

Elasticity of Demand

If a small change in price causes a large change in quantity demanded, the product is said to be elastic (or responsive to price changes).

The opposite also applies, a product is inelastic if a large change in price is accompanied by a small amount of change in demand.

Can you think of a product that you will refuse to buy if the price increases drastically?

Can you think of a product that you will continue to buy even if the price increases drastically?

The Price Elasticity of Supply measures the rate of response of quantity demand due to a price change

Price (OLD)=9Price (NEW)=10Q Supply (OLD)=150Q Supply (NEW)=210

The price elasticity of supply is used to see how sensitive the supply of a good is to a price change. The higher the price elasticity, the more sensitive producers and sellers are to price changes. A very high price elasticity suggests that when the price of a good goes up, sellers will supply a great deal less of the good and when the price of that good goes down, sellers will supply a great deal more. A very low price elasticity implies just the opposite, that changes in price have little influence on supply.

Economics

Consumers use goods and services. Producers depend on consumers to use their product

and consumers depend on producers to make the goods/services they need and want.

This dependency on each other for goods/services is called interdependence.

The interdependence that exists between producers and consumers requires that each pay

careful attention to the other. Producers must be aware of consumer likes and dislikes to

know what to produce, how much of it to produce, and when to produce it. Consumers

must understand the difficulties of production and provide good consumer feedback to

the producer.

Think of it this way!!!!!Everything you do hasan opportunity cost.

TINSTAAFL

What does this mean?

1. The best things in life are free.

2. The largest cost of going to college is tuition, room and board.

3. Anything worth doing is worth doing well.

4. The purpose of economic activity is to improve the well-being of some people at the expense of others

Think about these statements Are they true or false

First, hardly anything is free. Resources are scarce and our wants are unlimited, so we constantly have to decide how to use those scarce resources. Things we think of as free, like spending time with our families or enjoying nature, have a cost. In order to do those things, we must give up something else. Economists use the term TINSTAAFL – an acronym for “There is No Such Thing as a Free Lunch.” This means everything in life has a cost. While things may appear to be free, everything has a cost. A good example is the free lunch program. In order for a student to get a free lunch, he or she must come to school. Coming to school is the cost of that free lunch. This statement also points out that economics is the study of human behavior, not merely traditional topics such as taxes, investments, or money.

Statement 1

The second statement is also false. Students who attend college must give up the chance to work and earn money immediately following graduation from high school, and this cost is larger than tuition (room and board are irrelevant, since you must have a place to live and food to eat whether you go to college or to work). The cost of something is not always measured in direct outlays of money, but in opportunities sacrificed. Have students compare the opportunity cost for someone like LeBron James (professional basketball player who went straight from high school to the NBA) to what they might face when they graduate from high school.

Statement 2

Statement 3

The third statement is also false. We are often told this is true, but economists point out that time is a resource that is limited and that we must make choices. We just don’t have enough time to do everything well.

The fourth statement is false as well. This is a common misconception of economic concepts. When people trade with each other, they both anticipate being better off after making a voluntary trade. Trade is a win-win proposition.

Statement 4

http://www.kidseconposters.com/images/hp_op_cost.pdf

In other words, opportunity cost is a trade off

Every purchase is a trade-off. Maybe it’s more obvious with discretionary expenses, such as books and gym memberships and cable television. But you’re making trade-offs even when you buy the things you need. When you buy food for your family, you’re giving up other things you might really want, like new furniture or a car repair. And if you choose to go into debt, you’re trading your future income in order to have the things you want today.

When more units of a good or a service can be produced on a larger scale, yet with (on average) less input costs, economies of scale are said to be achieved.

Economies of Scale

In a simple example explaining the principal, where a manufacturing company saves money as it produces higher quantities of its product, as in all business areas, 'the more you buy, the more you save'

An example is that of a private soft drinks manufacturer. The more orders that the manufacturer receives, the more savings it makes, as it will in turn get cheaper prices for the materials it needs to produce its drinks as it will be buying them in larger quantities and receiving discounts, the manufacturing company in turn would give its customers cheaper prices for the more orders for drinks they make for this very reason, as they will gain the discounts, they can pass a saving onto their customers, making themselves stronger, a more respected company from its suppliers as it is buying in higher volumes and its turnover becomes higher.

1. Oh Scarcity!(Tune: Oh, Christmas Tree)

Oh, Scarcity! Oh, Scarcity!We can’t have all the

things we want.Oh, Scarcity! Oh, Scarcity!

We cannot have it all.We really want a lot of

stuff.But sometimes there’s just

not enough.Oh, Scarcity! Oh, Scarcity!

We cannot have it all.

2. We Are Workers (Tune: Are You Sleeping)

We are workers, We are workers,Yes we are! Yes we are!Brian is a baker. Brian is a baker.He makes bread. He makes bread.We are workers, We are workers,Yes we are! Yes we are!Sarah is a fire fighter. Sarah is a fire fighter.She puts out fires. She puts out fires.

3. Oh Give Me a Choice (Tune: Home on the Range)

Oh give me a choice,Oh, a difficult choice,And I’ll think about what I could use.I’ll have to decide,With my eyes open wide,What I’ll give up and what I will choose.Opportunity cost!It’s the thing you give up when you choose.It’s the price that is paidWhen a choice must be made.It’s the thing that I surely will lose.

4. The Money Goes ‘Round(Tune: Here We Go ‘Round the Mulberry Bush)

Verse 1:

The businesses pay the people who work,The people who work,The people who work.The businesses pay the people who work,The money goes ‘round and ‘round.

Chorus:

The money goes ‘round and ‘round and ‘round.The money goes ‘round and ‘round and ‘round.The money goes ‘round and ‘round and ‘round.The money goes ‘round and ‘round.

Verse 2:

The people buy the businesses’ goods,The businesses’ goods,The businesses’ goods.The people buy the businesses’ goods,The money goes ‘round and ‘round.

(Repeat chorus)

5. Questions (Tune: Oh Where, Oh Where Has My Little Dog Gone)

Oh what, oh what will our country produce?Oh what, oh what will it make?With its natural and capital and human resources,Oh what, oh what will it make?Oh how, oh how will our country produce?Oh how, oh how will it work?With its natural and capital and human resources,Oh how, oh how will it work?For whom, for whom will our country produce?For whom, for whom will it work?With its natural and capital and human resources,For whom, for whom will it work?

6. The Baker Wants a Pair of Shoes (Tune: Old MacDonald)

The baker wants a pair of shoes, E-I-E-I-O!The baker wants the shoe clerk’s help, E-I-E-I-O!With a shoe clerk here, and a shoe clerk there,Here a clerk, there a clerk,Everywhere a clerk, clerk.The baker wants the shoe clerk’s help, E-I-E-I-O!The shoe clerk wants some food to eat, E-I-E-I-O!The shoe clerk wants the grocer’s help, E-I-E-I-O!With a grocer here, and a grocer there,Here a grocer, there a grocer,Everywhere a grocer, grocer.The shoe clerk wants the grocer’s help, E-I-E-I-O!The grocer has a little dog, E-I-E-I-O!The grocer wants the vet to help, E-I-E-I-O!With a vet, vet here, and a vet, vet there,Here a vet, there a vet,Everywhere a vet, vet.The grocer wants the vet to help, E-I-E-I-O!

7. Buying and Selling (Tune: Row, Row, Row, Your Boat)

Goods, goods, goods are thingsThat we make and use.We’re buying and sellingAnd buying and sellingAny goods we choose.Services are things we doThat other people use.We’re buying and sellingAnd buying and sellingServices that we choose.

8. Spending and Saving (Tune: On Top of Old Smoky)

Keep spending your money; get something this way.The value is small but you’ll have it today!Start saving your money; get something this way.The value is great and you’ll get it some day!

12. Consumers (Tune: The Bear Went Over the Mountain)

Consumers go to the market, consumers go to the market,

Consumers go to the market, to see what they can buy.

And all that they can buy, and all that they can buy,

Are lots of goods and services, lots of goods and services,

Lots of goods and services, that’s all that they can buy.

We’ve been working on production,All the livelong day.We’ve been working on production,Just to make some goods this way.We use natural resources,Such as land, and oil, and trees.We use capital resources,Such as tools and factories.Now we will work!Now we will work!When we use our human resource.Now we will work!Now we will work!We use our human resource.

14. We’ve Been Working on Production (Tune: I’ve Been Working on the Railroad)

The Circular Flow of Economic Activity

Transactions: The Circular-Flow Diagram

•Trade takes the form of barter when people directly exchange goods or services that they have for goods or services that they want.

•The circular-flow diagram is a model that represents the transactions in an economy by flows around a circle.

The Circular-Flow Diagram

Circular-Flow of Economic Activities

•A household is a person or a group of people that share their income.

•A firm is an organization that produces goods and services for sale.

•Firms sell goods and services that they produce to households in markets for goods and services.

•Firms buy the resources they need to produce—factors of production—in factor markets.

The Circular Flow

Goods

Other countriesOther countries

Financial marketsFinancial markets

GovernmentGovernmentFirms

(production)HouseholdTaxes

Factor services

SavingsImports

Government

Spending

Wages, rents, interest, profits

Exports

Investment

Personal consumption

McGraw-Hill/Irwin © 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Growth in the U.S. Economy from 1962…

…to 1988

Consumers

• Consumers play 3 roles in the economy– Consumer -- user of goods and services.

Free to choose. Can spend now for immediate wants or save for future consumption.

– Worker -- producer of goods and services. Earner of income.

– Citizen -- join with others to make group decisions. Influence laws, pay taxes, vote. Determine use of public goods and services.

Business and Industry• Provide goods and services in return for

profit.

• 4 components– production– processing– distribution– services

Government• Provides legal framework for

economic activity. Also is a producer and consumer as well as an economic force. Can use its economic power to accomplish socially desirable goals.

International Trade

• Provides better, different, or cheaper goods and services and the resources we need to produce.

The Circular Flow

• The circular flow follows two paths through the economy -- money and goods and services.

• It shows the interaction between the 4 parts of the economy -- consumers, businesses, government, and international trade.

Flow of Goods and Services

• Individuals provide the factors of production (land, labor, capital, management).

• Businesses use the factors to produce goods and services.

The Money Flow

• Businesses pay for the factors of production.

• Individuals buy the goods and services.

Finished Goods and Services

Money Payments for Products

Money Income Payments (Wages, Rent, Interest, Profit)

Productive Services to Business Firms

ResourceOwners

(Consumers)Business

Firms

• By adding the government, you get two new circles.

• One shows interaction between the government and consumers.

Government Services

Taxes

Money Payments

Productive Services

ResourceOwners

(Consumers)Government

• The second shows the interaction between the government and businesses.

Finished Goods and Services

Purchases and Transfers

Taxes

Government Services

Government BusinessFirms

• Putting those together gives you the two inner circles.

Government Services Finished Goods and Services

Taxes Purchases and Transfers

Money Payments Taxes

Productive Services Government Services

ResourceOwners

(Consumers)Government Business

Firms

• Next we put consumers, businesses and the government together.

Finished Goods and Services

Money Payments

Government Services Finished Goods and Services

Taxes Purchases and Transfers

Money Payments Taxes

Productive Services Government Services

Money Payments

Productive Services

ResourceOwners

(Consumers)Government Business

Firms

International Trade

• The last part of the flow chart involves money and goods and services flowing into and out of the country via imports and exports.

Finished Goods and Services

Money Payments

Government Services Finished Goods and Services

Taxes Purchases and Transfers

Money Payments Taxes

Productive Services Government Services

Money Payments

Productive Services

Imports Exports $ to imports $ from exports

ResourceOwners

(Consumers)Government Business

Firms

International Trade

Employment

and

Labor Unions

People may be unemployed for several reasons; fired, laid-off, quit…

Types of unemployment include:

Frictional, Structural, Cyclical, Seasonal, Technological, and Classical

Unemployment

Frictional unemployment describes people who are unemployed for a short period of time.

This is minor unemployment Most of these are people moving into

the work force for the first time.

--- first time workers

Unemployment

Frictional unemployment also includes people who are between jobs.

Sources of frictional unemployment People entering the workforce from school. People re-entering the workforce after raising

children. People changing employers due to quitting or

being fired. People changing careers due to changing

interests. People moving to a new city (for non-structural

reasons) and being unemployed when they arrive.

Unemployment

Structural unemployment Technology changes or changes in

consumer tastes. Skills do match the openings

Structural unemployment

Changes in Technology: As personal computers replaced typewriters, typewriter factories shut down. Workers in typewriter factories because unemployed and had to find other industries to be employed in.

Changes in Tastes: If bagpipes become unpopular, bagpipe companies will go bankrupt and their workers will be unemployed.

Unemployment

Cyclical unemployment describes dips in the business cycle.

Recession layoffs

Cyclical unemployment

Getting laid off due to a recession is the classic case of cyclical unemployment. This is why the unemployment rate is a key economic indicator.

Business Cycle

A predictable long-term pattern of alternating periods of economic growth (recovery) and decline (recession), characterized by changing employment, industrial productivity, and interest rates. also called economic cycle

Expansion ExpansionRecession

The Phases of the Business Cycle

Boom

Secular growth trend

DownturnUptu

rn

Trough

Peak

0Jan.-Mar

Tot

al O

utpu

t

Apr.-June

July-Sept.

Oct.-Dec.

Jan.-Mar

Apr.-June

July-Sept.

Oct.-Dec.

Jan.-Mar

Apr.-June

McGraw-Hill/Irwin © 2004 The McGraw-Hill Companies, Inc., All Rights Reserved.

Seasonal unemployment

Seasonal unemployment is unemployment due to changes in the season - such as a lack of demand for department store Santa Clauses in January. Seasonal unemployment is a form of structural unemployment, as the structure of the economy changes from month to month.

Unemployment

Technology unemployment includes people that do not have the skills to keep up with technology changes or are replaced by machinery.

Unemployment

Unemployed people are people who are available for work and are making an effort to find a job.

Unemployment rate is found by dividing the number of people in the workforce into the number of unemployed people.

Unemployment

Underemployed- highly skilled workers in low wage jobs or jobs beneath their skill level.

For example, someone with a college degree may be tending bar or driving a cab. This may result from the existence of unemployment, which makes workers with bills to pay (and responsibilities) take almost any jobs available, even if they do not use their full talents

Unemployment

Classical unemployment is also known as the real wage unemployment or disequilibrium unemployment. This type of unemployment occurs when trade unions and labor organization bargain for higher wages, which leads to fall in the demand for labor.

Labor Unions

A labor union is an organization of wage earners or salary workers established for the purpose of protecting their collective interests when dealing with employers.

Labor Unions

The earliest unions in the United States were craft unions. Craft unions represent employees in a single occupation or group of closely related occupations. Members of craft unions are generally highly skilled workers. Examples of craft unions include the various skilled trades in the construction industry. Separate unions exist for each major skill (e.g., carpenters, electricians, plumbers).

Labor Unions

Craft unions are most common in occupations in which employees frequently switch employers. A construction worker is usually hired to complete work at a specific job site and then moves on to work elsewhere (often for another employer). In addition to collective bargaining, craft unions often serve as a placement service for members. Employers contact the union's hiring hall and union members currently out of work are referred to the job.

Labor Unions

Closely related to craft unions, are professional unions. A professional is an employee with advanced and highly specialized skills, often requiring some credential, such as a college degree and/or a license. Professional unions are much more recent than craft unions and are most common in the public sector. The American Federation of Teachers is one of the oldest professional unions.

Labor Unions

Most unionized workers in the United States belong to industrial unions. An industrial union represents workers across a wide range of occupations within one or more industries. A good example of a typical industrial union is the United Auto Workers (UAW). It represents skilled craft workers, assembly line workers, and unskilled workers in all of the major American automobile companies.

Labor Unions

General unions organize workers across all occupations and industries. Although some highly diversified unions, such as the

Teamsters, appear to be general unions, this form of organization does not really exist in the United States. Because they are typically politically oriented, general unions are more common in Europe and developing countries.

Labor Unions

1869 – World War I Formation of 3 national labor organizations: – Knights of Labor (KOL) – American Federation of Labor (AFL) – Industrial Workers of the World (IWW)

Labor Unions

Knights of Labor founded by Uriah S. Stephens- Secret society founded in 1869

Goals: – Opposed mass production – Moral betterment for employees & society Terence V. Powderly – Leader & chief

spokesman from 1879 – 1883

Labor Unions

American Federation of Labor (AFL) Formed in 1886 Samuel Gompers: Former member of the

KOL AFL Objectives: – Economic betterment of members – Enhancement of the capitalistic system – Enhancement of society

Labor Unions

American Federation of Labor (AFL ) AFL Tactics:

– Strike

– Political involvement

– Increased status for organized labor &

collective bargaining.

Labor Unions

Industrial Workers of the World (IWW) Formed in 1905 as an alternative to the

AFL Wobblies - “Big Bill” Haywood leader Goal: To Overthrow Capitalism Viewed AFL as an extension of capitalism

Labor Unions

AFL-CIO Largest organizational unit in labor AFL – American Federation of Labor – Founded in 1886- Craft Unions CIO – Congress of Industrial Organizations – Founded in 1938 - Industrial Unions Merged in 1955

Key Union Terms

Collective Bargaining – Negotiating a labor contract with management

Organizing Campaign Strike- Puts financial pressure on a company Strikebreaker – Nonunion employee

– Performs the job of the striking union member. AKA scab

Labor Unions

Boycott- refusal to do business Lockout- firms refusal to allow employees to

enter the workplace Slowdown- workers work at a slower pace to

decrease production.

Labor Unions

Mediation – Neutral third party

-Assists during negotiations Arbitration – Neutral third party

– Formal hearing in contract negotiations

– Final step in grievance procedure

labor unions labor contractnegotiationopen/closed shopslow downstrikeright to strike laws“right to work” lawslockoutinjunctionscab