2014 Momentum Webinar Series:Security and ComplianceIn the Interconnected Age

Alan Akahoshi

June 24, 2014

• Momentum Series

• Polls

• Q/A

Welcome

Introduction

Alan Akahoshi is a lead security product manager at Digital Insight. With 22 years of network communication, applications and security experience, Alan has safeguarded systems for the nation’s leading technology companies. His previous roles include program manager for Microsoft's hosted services group, and product manager for Symantec's consumer business unit.

Agenda• The Internet of Everything (IoE)

– Ecosystem

• FFIEC Guidelines for your customer digital channel

– Coverage

• A security model for protecting your Customer

– Closing the gap

Have you ever received an email fromyour refrigerator or television set?a. Yes

b. No

c. Is that possible?!

Poll Question 1 : Current Events

>750K malicious emails sent by botnet.It’s enough to give you chills.

“In this case, hackers broke into more than 100,000 everyday consumer gadgets, such as home-networking routers, connected multi-media centers, televisions, and at least one refrigerator, Proofpoint says. They then used those objects to send more than 750,000 malicious emails to enterprises and individuals worldwide.”

The Internet of EverythingToday’s Challenge

IoE = User x (Devices x Networks x Services)

The connected state or the “Internet of Everything”

Networks(Places)

Services(Transactions/Interactions)

Devices

Data DataData

DataData

Data

Source: http://www.businessinsider.com/the-internet-of-everything-2014-slide-deck-sai-2014-2?op=1

An explosion of interconnectivity

Cyber Security is the biggest concern

Source: http://www.businessinsider.com/the-internet-of-everything-2014-slide-deck-sai-2014-2?op=1

• “Six degrees or less,” you are connected to a vulnerable element in the IoE ecosystem.

For Financial Institutions, Security must extend beyond

your purview.

youyou

OLB OLB

Gotcha!

• The Heartbleed bug is a vulnerability in the OpenSSL cryptographic software library that existed since 2012 and was not uncovered until early this year.

And the effects may be devastating

Reputation takes years to build, and only moments to lose.

In IoE, controlling borders and layering security isn’t enough.

You need to dramatically change your security strategy.

FFIEC GuidelinesWhat does it address in IoE?

• Federal rules and regulations– Federal Reserve Board

• Regulation E (Electronic Fund Transfers, 12 CFR 205)

– Uniform Commercial Code• Article 4A, Funds Transfer (2012)

– Dodd-Frank Wall Street Reform and Consumer Protection Act

• The FFIEC prescribes recommendations for federal examinations of financial institutions .– E-Banking– Information Security– Supplement in 2011

In a highly regulated industry, how do you respond to IoE?

• 2001: Electronic Banking

• 2005, 2011: Internet Banking

• What does it protect?

– Customer data (privacy)

– Fund movement (anti-fraud)

• How does it protect?

– Periodic risk assessments

– Multi-factor authentication

– Layered security controls• Access controls (limits)

• Monitoring

– Customer awareness

FFIEC Internet Banking Guidelines (2011)

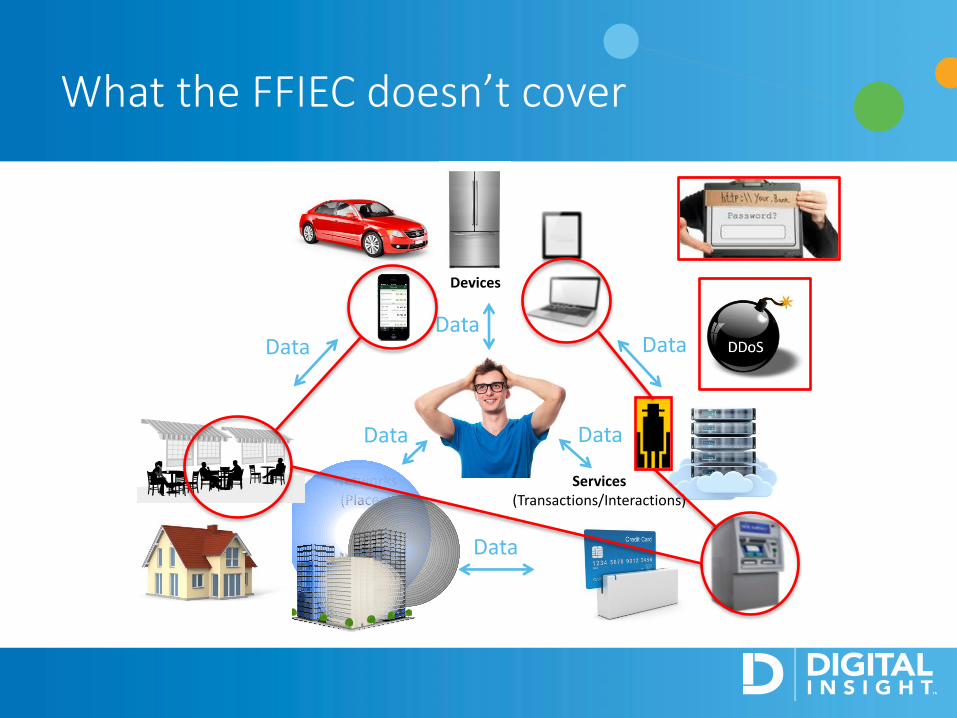

Networks(Places)

Services(Transactions/Interactions)

Devices

Data DataData

DataData

Data

What the FFIEC doesn’t cover

Financial Institution Best PracticesHow do you provide an effective and secure digital banking experience?

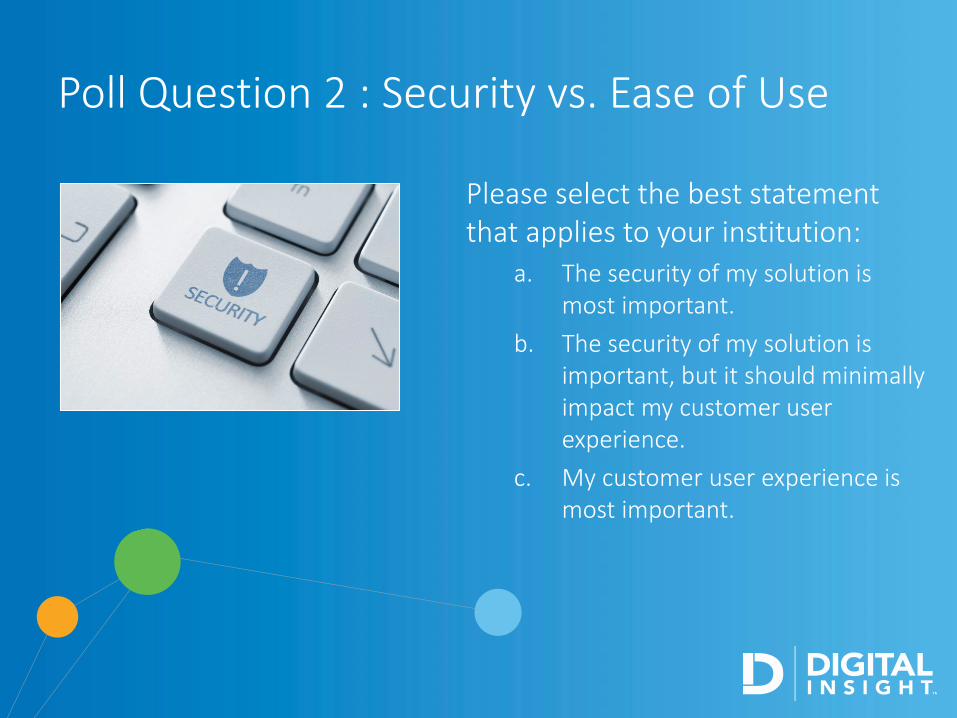

Please select the best statement that applies to your institution:

a. The security of my solution is most important.

b. The security of my solution is important, but it should minimally impact my customer user experience.

c. My customer user experience is most important.

Poll Question 2 : Security vs. Ease of Use

• Includes Prevention

• Includes Monitoring

• Includes Remediation

• Is multi-faceted, multi-layered to provide maximum protection – a system of redundancy

An effective security program framework

Prevention

MonitoringRemediation

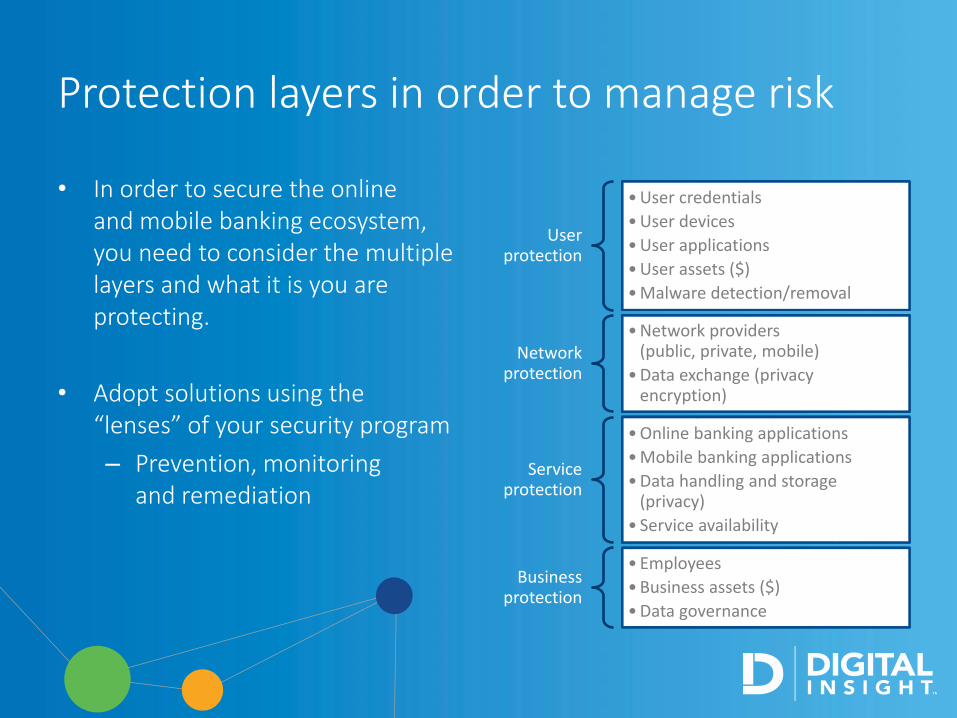

• In order to secure the online and mobile banking ecosystem, you need to consider the multiple layers and what it is you are protecting.

• Adopt solutions using the “lenses” of your security program

– Prevention, monitoring and remediation

User protection

• User credentials

• User devices

• User applications

• User assets ($)

• Malware detection/removal

Network protection

• Network providers(public, private, mobile)

• Data exchange (privacy encryption)

Service protection

• Online banking applications

• Mobile banking applications

• Data handling and storage (privacy)

• Service availability

Business protection

• Employees

• Business assets ($)

• Data governance

Protection layers in order to manage risk

• Identity Verification (Account Origination)– Required by Section 326 of the USA Patriot

Act (FFIEC 2005)– Reduce the risk of

• Identity theft• Fraudulent account applications (international

money laundering and terrorist financing)• Unenforceable account agreements or

transactions

• User Verification (Authentication, Authorization and Access Control)– Layered “what you can see” & “what you can

do”– Reduce the risk of

• Unauthorized account access (privacy; protecting data)

• Account takeover• Fraudulent activity

Prove you are who you say you are

P

MR

User

Network

Service

Business

• User verification methods– Something the user knows

• “Shared secret”, password, PIN

– Something the user has

• ATM card, smart card, scratch card

• Mobile device, FOB token, USB token

– Something the user is

• Biometric hardware (fingerprint, face, voice, retinal/iris, etc.)

– Other factors that complement authentication

• User device identification

• User location / network

• User internet protocol address

Authentication, Authorization and Access Control

P

MR

User

Network

Service

Business

• Layered Security Controls

– Measure the level of risk and match protection methods

• Consumer Banking

– Accessing banking account information

– Accessing personal account information

– Money movement activity

• Bill payment

• Intrabank funds transfers

• Interbank funds/wire transfers

• Business Banking

– Frequent and higher $$$ amounts money movement activity

• ACH file origination

• Frequent interbank wire transfers

Not all online activity or actions are equal

P

MR

User

Network

Service

Business

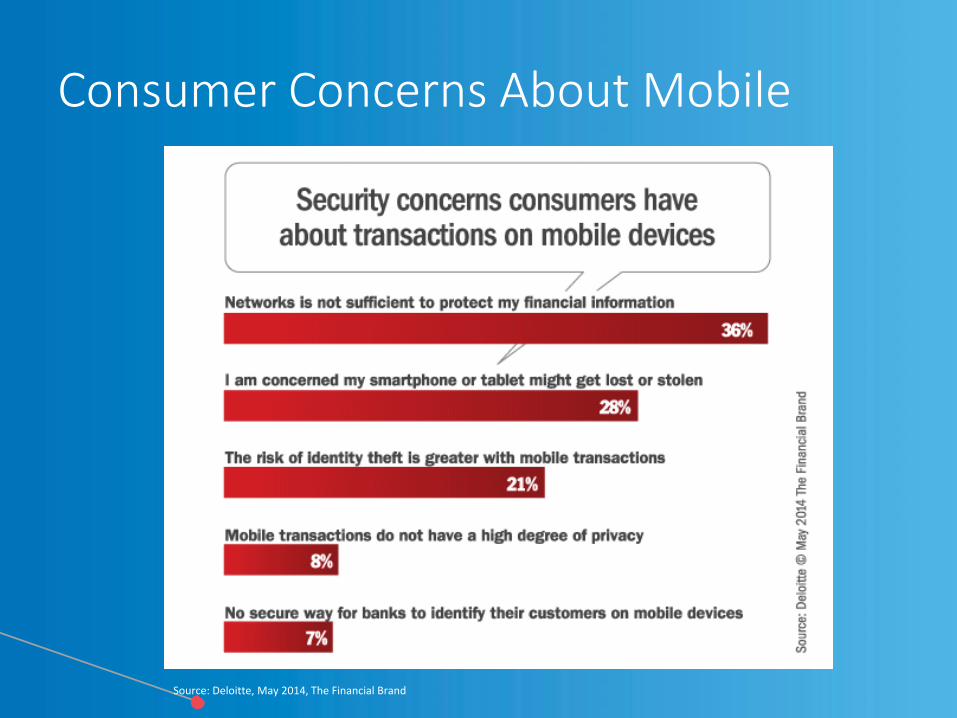

Consumer Concerns About Mobile

Source: Deloitte, May 2014, The Financial Brand

What is your greatest mobile security concern? (Select one) a. Application security

b. Device data leakage

c. Device loss or theft

d. Malware attack

Poll Question 3 : Mobile Risk

• Mobile devices, networks it connects to,services it accesses, and data shared…– 63% of smartphone users access

their bank or credit union institution– 61% of smartphone owners who

don’t use mobile banking cite “security” issues

• Mobile Apps vs Mobile Web• Secure communication channel

(data privacy)• Complex device identification,

geo-location and reputation– Assurance to tie this to a user– Monitoring

Mobile is personal, an extension of You

P

MR

User

Network

Service

Business

Source: Deloitte, May 2014, Mobile Financial Services: Raising The Bar on Customer Engagement

• It’s never a question of ‘if’ I get hacked,but ‘when’ I get hacked…

– Hackers are continuously finding and exploiting the weakest link

• Effective monitoring is key todetecting fraud and preventing attacks

• Complex analytics of user, device and system data, and behavioral modeling provide intelligent detection

• Mitigation processes

Hackers hack and they will continue to hack

P

MR

User

Network

Service

Business

How do you provide customers/members with tools and tips to safeguard their online and/or mobile banking experience? (select all that apply)

a. Online Banking Application

b. Mobile Banking Application

c. Email

d. Text/SMS

e. In-Branch

f. Other

g. We do not provide any tools or tips

Poll Question 4 : Education Programs

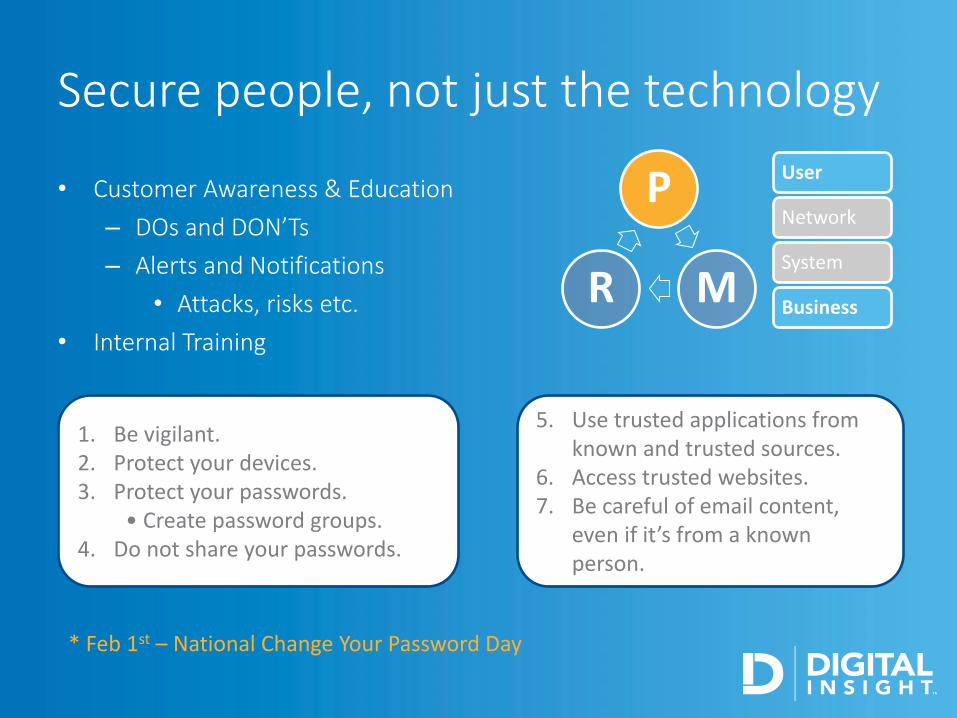

• Customer Awareness & Education

– DOs and DON’Ts

– Alerts and Notifications

• Attacks, risks etc.

• Internal Training

Secure people, not just the technology

P

MR

1. Be vigilant.2. Protect your devices.3. Protect your passwords.

• Create password groups.4. Do not share your passwords.

5. Use trusted applications from known and trusted sources.

6. Access trusted websites.7. Be careful of email content,

even if it’s from a known person.

* Feb 1st – National Change Your Password Day

User

Network

System

Business

What you can do . . .

Effective security strategy – elements forprevention, monitoring and remediation

Multi-factor authentication

Layered security controls

Transaction monitoring

Marketing programs for customerawareness and education

Annual risk assessment

Security and Compliance Checklist

User

Service

Business

Network

Questions?

www.digitalinsight.com

Thank you!

October 2014: Trends in Delivery: Channel

Convergence and Funding Innovation David Potterton, Cornerstone Advisors

Visit Us: