March 27, 2012

Shree Cement Ltd.

Cementing India…

CMP INR 2,923.8 Target INR 3,319.8 Initiating Coverage - ACCUMULATE

SKP Securities Ltd www.skpmoneywise.com Page 1 of 17

Key Share Data

Face Value (INR) 10.0

Equity Capital (INR Mn) 34.8

52 Week High/Low (INR) 3,048/1,520

6 months Avg. Daily Volume (NSE) 10,966

BSE Code 500387

NSE Code SHREECEM

Reuters Code SHCM.BO

Bloomberg Code SRCM IN

Shareholding Pattern (as on 31st Dec. 2011)

Promoter 64.78%

FII's, 8.25%

Others, 22.0%

DII's, 4.97%

Source: BSE

Particulars FY11 FY12E FY13E FY14E

Net Sales 35,118.7 42,383.5 51,200.0 58,485.2

Growth (%) -3.3% 20.7% 20.8% 14.2%

EBITDA 8,856.4 10,659.0 12,970.2 15,178.5

PAT 2,097.0 2,472.9 4,506.7 6,988.4

Growth (%) -69.0% 17.9% 82.2% 55.1%

EPS (INR) 60.2 71.0 129.4 200.6

BVPS (INR) 570.1 622.4 730.7 907.9

Key Financials (INR Million)

Particulars FY11 FY12E FY13E FY14E

P/E (x) 34.4 41.2 22.6 14.6

P/BVPS (x) 3.6 4.7 4.0 3.2

Mcap/Sales (x) 2.1 2.4 2.0 1.7

EV/EBITDA (x) 9.9 10.7 8.3 6.8

ROCE (%) 5.3% 7.0% 14.2% 19.3%

ROE (%) 11.0% 11.9% 19.1% 24.5%

EBITDA Mar (%) 25.2% 25.1% 25.3% 26.0%

PAT Mar (%) 6.0% 5.8% 8.8% 11.9%

Debt - Equity (x) 1.0 0.8 0.7 0.5

Key Financials Ratios

Source: Company, SKP Research

1 Yr price performance SCL vis-à-vis BSE Mid Cap

-50.00%

-20.00%

10.00%

40.00%

70.00%

Mar-11 Jun-11 Aug-11 Oct-11 Jan-12 Mar-12

SCL BSE Mid Cap

Company Background

Shree Cement Ltd (SCL), established in 1985, is a part of BG Bangur

Group. The company is engaged in the manufacturing of cement and

power generation. SCL has a cement capacity of 13.5 MTPA and power

generating capacity of 560 MW. Its cement plants are located at

Beawar, Ras, Khushkhera, Jobner and Suratgarh in Rajasthan and

Laksar (Roorkee) in Uttarakhand.

Investment Rationale

Buoyancy in cement industry to continue

� SCL is expected to benefit from its strong presence in North

India, as prices are expected to remain firm in these regions

due to slowdown in capacity addition over the next few years.

� Over the next two to three years, besides general election at the

Centre, many of SCL’s key cement consuming states like Madhya

Pradesh, Rajasthan, Delhi, Haryana etc. are scheduled for

elections. These electoral developments will keep demand

buoyant till FY15.

Cost efficiencies to contain margin erosion

� SCL is one of the lowest cost cement producer in India, owing to its

100% captive power usage, lesser power consumption per tonne of

cement (~80 units/tonne vis-à-vis the industry average of ~85-95

units/tonne) and locational proximity to key markets which results in

lower freight costs.

Strong balance sheet to drive growth

� The company is likely to fund most of its expansion through internal

accruals. During FY11-14E, SCL is expected to generate cash

flow from operations of ~INR 36,268.0 million, which would be

utilized as capex and towards repayment of debt.

Valuation

We rate a ACCUMULATE rating on the stock with a price target of

INR 3,319.8 /share, implying an upside potential of 13.5 percent

from current levels. Our target price is based on the average of a

target P/BV multiple of 4.0x FY14E book value of INR 907.9/share and

EV/EBITDA multiple of 7.0x FY14E of INR 15,178.5 million.

A Analyst: Nikhil Saboo

Ph: +91 33 4007 7408, M: +91 9330186643

Email: [email protected]

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 2 of 17

India is among the fastest growing

cement markets in the world with

consumption CAGR of 8.4 percent

(FY01-11)

Even though, India is the second

largest cement producer in the world

after China, its per capita cement

consumption is very low

Industry Overview

Cement Industry

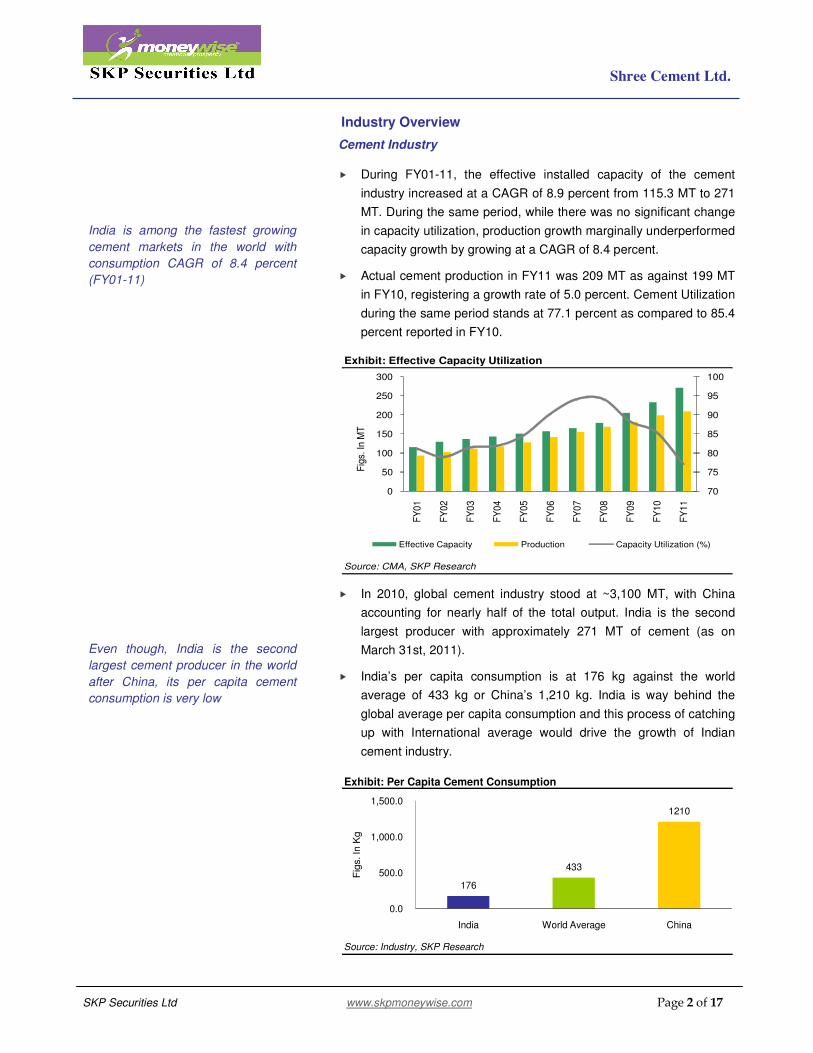

� During FY01-11, the effective installed capacity of the cement

industry increased at a CAGR of 8.9 percent from 115.3 MT to 271

MT. During the same period, while there was no significant change

in capacity utilization, production growth marginally underperformed

capacity growth by growing at a CAGR of 8.4 percent.

� Actual cement production in FY11 was 209 MT as against 199 MT

in FY10, registering a growth rate of 5.0 percent. Cement Utilization

during the same period stands at 77.1 percent as compared to 85.4

percent reported in FY10.

Source: CMA, SKP Research

Exhibit: Effective Capacity Utilization

70

75

80

85

90

95

100

0

50

100

150

200

250

300

FY

01

FY

02

FY

03

FY

04

FY

05

FY

06

FY

07

FY

08

FY

09

FY

10

FY

11

Fig

s. In

MT

Effective Capacity Production Capacity Utilization (%)

� In 2010, global cement industry stood at ~3,100 MT, with China

accounting for nearly half of the total output. India is the second

largest producer with approximately 271 MT of cement (as on

March 31st, 2011).

� India’s per capita consumption is at 176 kg against the world

average of 433 kg or China’s 1,210 kg. India is way behind the

global average per capita consumption and this process of catching

up with International average would drive the growth of Indian

cement industry.

Source: Industry, SKP Research

Exhibit: Per Capita Cement Consumption

176

433

1210

0.0

500.0

1,000.0

1,500.0

India World Average China

Fig

s. In

Kg

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 3 of 17

Recent growth in the global cement

consumption is primarily driven by

the emerging markets, generating

~70 percent of the demand

According to CEA, the total installed

capacity in the country as on

February 2012, stood at 190,592.5

MW

� In India, demand from infrastructure has increased but supply has

remained the same. Moreover, in the 12th five year plan,

Government has planned the spending of ~INR 40,992 billion on

infrastructure against INR 20,542 billion in 11th five year plan.

Hence, massive investment in infrastructure would provide boost to

the Indian cement industry. Exhibit: Infrastructure Spending

Source: Planning Commission, SKP Research

5.0

6.0

7.0

8.0

9.0

10.0

11.0

0

2,000

4,000

6,000

8,000

10,000

12,000

FY

11B

E

FY

12E

FY

13E

FY

14E

FY

15E

FY

16E

FY

17E

Fig

s. in

IN

R B

illio

n

Infrastructure Spending As a %age of GDP

Power Industry

� The power sector in India was understandably underdeveloped in

the era of 1947, both in terms of available capacity and per capita

consumption. But gradually, India was able to stand on its own feet

and now has the fifth largest generation capacity in the world.

� According to CEA, the total installed capacity in the country as on

February 2012, stood at 190,592.5 MW with state sector having

share of 44.1 percent, followed by central sector with 30.5 percent

share and balance contributed by private sector entities (excluding

captive generating capacity of 19,509 MW).

Coal Gas Diesel Total

Northern 27,817.5 4,171.3 13.0 32,001.8 1,620.0 15,022.8 3,830.3 52,474.8

Western 35,204.5 8,254.8 17.5 43,476.8 1,840.0 7,447.5 6,810.3 59,574.6

Southern 21,232.5 4,690.8 939.2 26,862.5 1,320.0 11,338.0 10,976.5 50,497.0

Eastern 21,122.9 190.0 17.2 21,330.1 0.0 3,882.1 381.7 25,593.9

N. Eastern 60.0 787.0 142.7 989.7 0.0 1,158.0 228.3 2,376.1

Islands 0.0 0.0 70.0 70.0 0.0 0.0 6.1 76.1

All India 105,437.4 18,093.9 1,199.7 124,730.9 4,780.0 38,848.4 22,233.2 190,592.5

Total

Note: # R.E.S includes Small Hydro Project, Biomass Gas, Biomass Pow er, Urban & Industrial w aste Pow er and Wind Energy

Source: Central Electricity Authority (CEA), SKP Research

Exhibit: Installed capacity as on February 2012 (Figures in MW)

RegionThermal

Nuclear Hydro R.E.S #

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 4 of 17

Per capita consumption of electricity

in India is one of the lowest in the

world

12th Five-Year Plan (2012-17) has

laid out a draft to add over 100,000

MW of power

Availability of domestic coal is a

challenge on account of various

bottlenecks

� Per capita consumption of electricity in India is one of the lowest in

the world. An increase in per capita consumption of electricity

requires an increase in accessibility of electricity in rural India. The

per capita consumption of power increased from 592 kWh/year in

FY04 to 779 kWh/year in FY10, at a CAGR of 4.7% from FY04-10.

Exhibit: Per Capita Consumption of Electricity (kWh/Year)

Source: CEA, SKP Research Note: * Provisional592

612.5

631.5

671.9

717.1

734.5

779

450

500

550

600

650

700

750

800

FY04 FY05 FY06 FY07 FY08 FY09 FY10*

in K

wh/Y

ear

� The 11th plan (2007-12) called for the addition of 78,700 MW of

power from all sources. Though, it is unlikely that this target will be

realised, the 12th Five-Year Plan (2012-17) is even more

ambitious, calling for the addition of over 100,000 MW of power.

Source: CEA, SKP Research

Exhibit: All India capacity addition Target & Achievement

Note: * Till February 2012

13

.0

35

.0

70

.4

92

.6

12

5.0

19

6.7

22

2.5

30

5.4

40

2.5

41

1.1

78

7.0

11

.0

22

.5

45

.2

45

.8 10

2.0

14

2.3

21

4.0

16

4.2

19

1.2

21

1.8

47

8.0

0%

20%

40%

60%

80%

100%

0

200

400

600

800

1000

1st

2nd

3rd

4th

5th

6th

7th

8th

9th

10th

11th

*

Fig

s. in

'00 M

W

Target Achievement %achievement

� The total thermal capacity, including gas stations and diesel

generation accounts for 65.4 percent of installed capacity of the

country. With 105,437.4 MW of the installed capacity based on coal

which is 55.3 percent of nation capacity, coal remains the key fuel

for power generation.

� However, availability of domestic coal is a challenge on account of

various bottlenecks such as capacity expansion of Coal India

Limited, coal block allocation, tribal land acquisition, environmental

and forest clearances, etc. This is further compounded by issues

around land acquisition for the power plant, water availability and

ash disposal for domestic coal-based plants.

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 5 of 17

SCL is currently having a capacity of

13.5 MTPA cement plant along with

560 MW of power plant

Primarily caters to the markets of

Rajasthan, Haryana, Punjab, Delhi

and Uttar Pradesh, among others

Company Profile

� Shree Cement Ltd (SCL), established in 1985, is a part of BG

Bangur Group. The company is engaged in the manufacturing of

cement and power generation. It is the largest cement

manufacturer in Northern India and among the top five cement

manufacturing groups in the country.

� SCL has more than quadrupled its cement capacity over the past

five years and currently has a capacity of 13.5 million tonnes per

annum (MTPA). Its cement plants are located at Beawar, Ras,

Khushkhera, Jobner and Suratgarh in Rajasthan and Laksar

(Roorkee) in Uttarakhand.

� The company has a power generation capacity of 560 MW with

plants located at Beawar and Ras in Rajasthan, including waste

heat recovery power plants of 46 MW capacity.

Location Cement Capacity Power Capacity

Beawar 3.0 MTPA 342 MW (TP)

Ras 3.0 MTPA 172 MW (TP)

Khushkhera 3.0 MTPA -

Jobner 1.5 MTPA -

Suratgarh 1.2 MTPA -

Roorkee 1.8 MTPA -

Total 560 MW

Note: TP = Thermal Power, GP = Green Power

Source: Company, SKP Research

Exhibit: Plant Overview

+ 46 MW (GP)

� SCL follows a multi brand strategy and sells cement under the

highly recognized brands of Shree Ultra, Bangur and Rockstrong

which together enjoy the largest market share in high value

markets of Rajasthan, Delhi and Haryana.

Source: Company, SKP Research

Exhibit: Installed Capacity & Sales Volume

9.3 1

2.8

13

.5

13

.5

13

.5

10.3

10.4

11

.2

11

.8

12.9

101%

74%76% 82%

90%

60%

70%

80%

90%

100%

110%

0.0

5.0

10.0

15.0

FY

10

FY

11

FY

12E

FY

13E

FY

14E

Fig

s. in

MT

PA

Effective Capacity Sales Volume Capacity Utilization (%)

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 6 of 17

Name Designation Profile

B. G. BangurExecutive

Chairman

He is also the Director in The Didwana Investment Company Ltd., NBI Industrial Finance Co. Ltd.,

Shree Capital Services Ltd., Khemka Properties Pvt. Ltd., Digvijay FinleaseLtd. and Marwar Textile

(Agency) Pvt. Ltd and also been actively associated with various philanthropic and charitable

institutions and trusts.

H. M. BangurManaging

Director

A chemical engineer from IIT, Mumbai, and is driving force of the technical excellence achieved by

the company. He is also a president of Rajasthan Foundation Kolkata Chapter and an Executive

Member of FICCI. During 2007-2009, he was the president of the Cement Manufacturing

Association (CMA).

R. L. Gaggar Director

He is practicing as a solicitor and an advocate in the Hon’ble Calcutta High Court for more than

past 50 years. He is also on the board of Somany Ceramics Ltd., Sarda Plywood Industries Ltd.,

TIL Ltd., Paharpur Cooling Towers Ltd., International Combustion India Ltd., Sumedha Fiscal

Service Ltd. and various other companies.

O. P. Setia DirectorHe is an M.Com from Delhi University and an eminent banker. He was the former Managing

Director of State Bank of India and has held many key position in its associate companies.

Shreekant

SomanyDirector

He is an industrialist and hold a BSc degree from Kolkata University. He is also on the Board of

Somany Ceramics Ltd., S.R. Continental Ltd, Somany Global Ltd., Cosmo Ferrites Ltd., Sarvottam

Vanijya Ltd. and Scope Vinimoy Pvt. Ltd.

Dr. Abid

HussianDirector

He is a retired IAS Officer and former Ambassador of India to United States. He was also a

member of the Planning Commission and Secretary, Ministry of Industries, Government of India

and was honoured with PADMA BHUSHAN for meritorious services in 1988. He is also on the

Board of other reputed companies.

Dr. Y. K. Alagh Director

He holds a Doctoral Degree and Master Degree in Economics from University of Pennsylvania

and is the Chancellor of Nagaland University, Chairman of Institute of Rural Management, Anand,

Gujarat and Vice Chairman of Sardar Patel Institute of Economic and Social Research,

Ahmedabad. He is on the Board of Tata Chemicals Ltd., Somany Ceramics Ltd. & Rallis India Ltd.

Nitin Desai Director

Mr. Desai is the Member of Prime Minister's Council on Climate Change and is connected with

the governing bodies of several NGOs and research institutions and chairs the Governing Body of

the Institute of Economic Growth. He is also a Trustee of Worldwide Fund for Nature (WWF)

International and has worked at the senior levels in the Planning Commission from 1973 to 1987.

Exhibit: Management Team

Source: Company

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 7 of 17

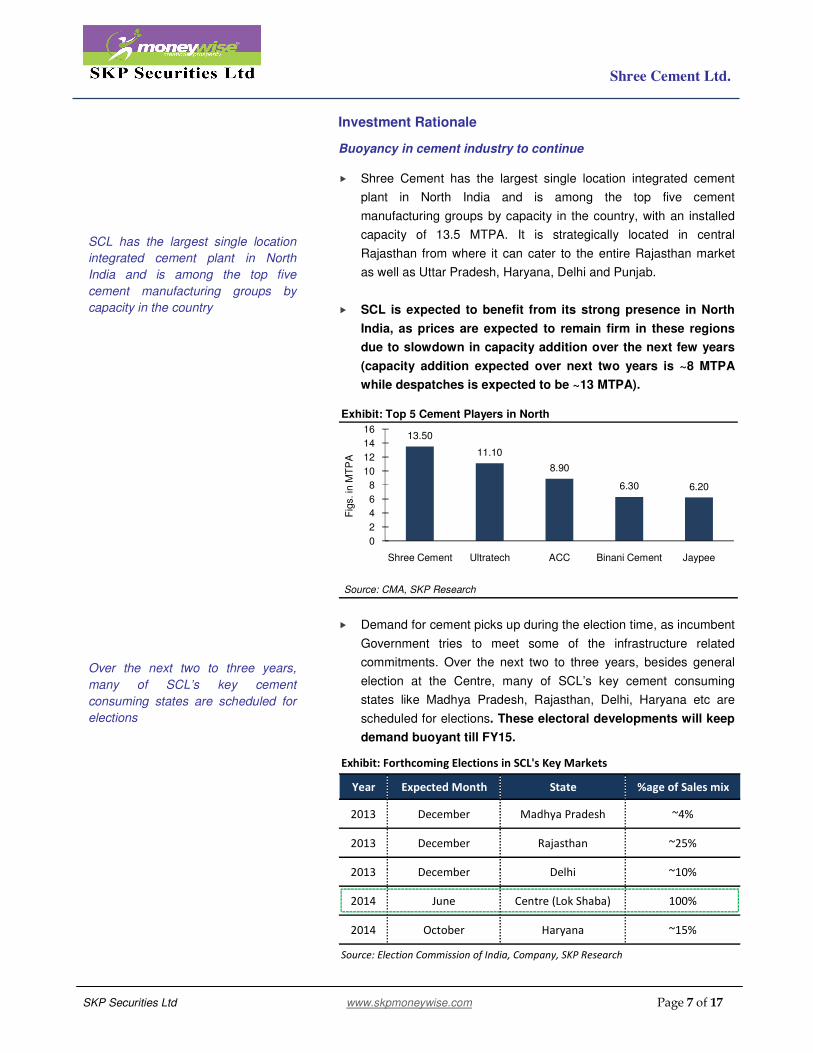

SCL has the largest single location

integrated cement plant in North

India and is among the top five

cement manufacturing groups by

capacity in the country

Over the next two to three years,

many of SCL’s key cement

consuming states are scheduled for

elections

Investment Rationale

Buoyancy in cement industry to continue

� Shree Cement has the largest single location integrated cement

plant in North India and is among the top five cement

manufacturing groups by capacity in the country, with an installed

capacity of 13.5 MTPA. It is strategically located in central

Rajasthan from where it can cater to the entire Rajasthan market

as well as Uttar Pradesh, Haryana, Delhi and Punjab.

� SCL is expected to benefit from its strong presence in North

India, as prices are expected to remain firm in these regions

due to slowdown in capacity addition over the next few years

(capacity addition expected over next two years is ~8 MTPA

while despatches is expected to be ~13 MTPA). Exhibit: Top 5 Cement Players in North

Source: CMA, SKP Research

13.50

11.10

8.90

6.30 6.20

0

2

4

6

8

10

12

14

16

Shree Cement Ultratech ACC Binani Cement Jaypee

Fig

s. in

MT

PA

� Demand for cement picks up during the election time, as incumbent

Government tries to meet some of the infrastructure related

commitments. Over the next two to three years, besides general

election at the Centre, many of SCL’s key cement consuming

states like Madhya Pradesh, Rajasthan, Delhi, Haryana etc are

scheduled for elections. These electoral developments will keep

demand buoyant till FY15.

Year Expected Month State %age of Sales mix

2013 December Madhya Pradesh ~4%

2013 December Rajasthan ~25%

2013 December Delhi ~10%

2014 June Centre (Lok Shaba) 100%

2014 October Haryana ~15%

Exhibit: Forthcoming Elections in SCL's Key Markets

Source: Election Commission of India, Company, SKP Research

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 8 of 17

SCL meets its 100 percent power

requirement from ~120-150 MW of

power plant while surplus power is

available for merchant sale

Its power consumption per tonne of

cement is ~80 units/tonne vis-à-vis

the industry average of ~85-95

units/tonne

Cost efficiencies to contain margin erosion

� SCL is one of the lowest cost cement producer in India, owing to its

captive power plant, lesser power consumption per tonne of

cement and locational proximity to key markets which results in

lower freight costs.

� SCL’s installed power capacity stands at 560 MW, which is self

sufficient to meet its power requirement. SCL meets its 100 percent

power requirement from ~120-150 MW of power plant while surplus

power is available for merchant sale. The company has also

entered into a contract for sale of 225 MW of power with various

SEBs till June 2012, at an average price of INR 4.3/unit.

Installed Capacity Captive Power

380 MW ~ 71%

410.4 MW ~ 70%

192 MW ~ 17%

560 MW 100%

540 MW ~ 80%

Source: Company, SKP Research

India Cement

Shree Cement

Ultratech Cement

Exhibit: Captive Power Availability

Company

ACC*

Ambuja Cement*

Note: * Year ending December 2011

� SCL’s power consumption per tonne of cement is among the lowest

in the industry owing to is continuous operational initiatives. Its

power consumption per tonne of cement is ~80 units/tonne vis-à-

vis the industry average of ~85-95 units/tonne.

Source: Company, SKP Research

Exhibit: Power Consumption

Note: * Year ending December 2011

Company

Ultratech Cement

Shree Cement

India Cement

Ambuja Cement*

ACC*

82.0 units/tonne

79.3 units/tonne

93.2 units/tonne

85.2 units/tonne

84.0 units/tonne

Consumption (unit/tonne)

� SCL’s continues to use petcoke for kiln operations owing to its

lower ash content. The company meets its petcoke requirement

through imports (direct agreement from a refinery in USA) and is

also sourcing from local players (IOC, HPCL Mittal, Essar oil etc.).

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 9 of 17

Looking at the current

macroeconomic environment, we do

not expect the petcoke prices to

surge significantly from current levels

We expect cement EBITDA/tonne of

INR 1,104.9/tonne in FY13E and INR

1,179.6/tonne in FY14E

Due to the ongoing European problems (major user of petcoke),

the prices have declined significantly from its peak levels. Looking

at the current macroeconomic environment, we do not expect

the petcoke prices to surge significantly from current levels.

Source: Bloomberg, SKP Research

Exhibit: Trend in International Petcoke price

40

50

60

70

80

90

100

110

120

130

140

Ap

r-1

0

Ju

n-1

0

Aug

-10

Oct-

10

De

c-1

0

Fe

b-1

1

Ap

r-1

1

Ju

n-1

1

Aug

-11

Oct-

11

De

c-1

1

Fe

b-1

2

Fig

s. In

US

D/t

onn

e

� We expect an improvement in EBITDA/tonne, from INR

862.8/tonne in FY11 to INR 1,179.6/tonne in FY14. EBITDA

margins are likely to improve by 73 bps over FY11-14E to 26.0

percent.

Particulars FY11 FY12E FY13E FY14E

Sales Volume (mtpa) 10.3 11.1 11.7 12.9

Total Expenditure/tonne 2,558.5 2,845.5 3,256.8 3,365.6

Material Consumed 362.7 374.5 400.6 413.5

Power & Fuel Cost 888.8 969.4 1,050.8 1,086.3

Employee Cost 193.4 224.3 249.7 260.7

Packing & Distribution 210.5 228.1 239.3 239.0

Freight & Selling Exp. 598.2 646.3 928.9 960.6

Admin & Other Exp. 304.9 403.0 387.5 405.5

EBIDTA/tonne 862.8 956.0 1,104.9 1,179.6

Exhibit: Per Tonne Analysis

Source: Company, SKP Research

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 10 of 17

During FY11-14E, SCL is expected

to generate cash flow from

operations of ~INR 36,268.0 million,

which would be utilized as capex and

towards repayment of debt

The company has plans to attain

cement capacity of 20 MTPA by

FY17

Exhibit: EBITDA & EBITDA Margins

Source: Company, SKP Research

15%

20%

25%

30%

35%

40%

45%

0

2000

4000

6000

8000

10000

12000

14000

16000

FY

08

FY

09

FY

10

FY

11

FY

12E

FY

13E

FY

14E

Fig

s. in

IN

R M

illio

n

EBITDA EBIDTA Margins (%)

Strong balance sheet to drive growth

� SCL has reported a strong financial performance over the last four

years. The sales for the period FY07-11 has reported a

compounded annual growth rate (CAGR) of 26.6 percent from INR

13,679.8 million to INR 35,118.7 million. The net profit for the same

period has grown at a CAGR of 4.3 percent from INR 1,770.0

million in FY07 to INR 2,097.0 million.

� Going forward, we expect the sales to grow at CAGR of 18.5

percent over FY11-FY14E to INR 58,485.2 million while net

profit is expected to grow at CAGR of 49.4 percent to INR

6,988.4 million during the same period.

� The company is likely to fund most of its expansion through internal

accruals. During FY11-14E, SCL is expected to generate cash flow

from operations of ~INR 36,268.0 million, which would be utilized

as capex and towards repayment of debt.

� The company has plans to attain cement capacity of 20 MTPA by

FY17. For the same, it has acquired mining lease for limestone in

the states of Chhattisgarh and Karnataka and is in the process of

completing land acquisition at both the locations. Given the low

leverage balance sheet, SCL should be able to capitalize its future

capex from internal accruals and raise debt, if necessary

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 11 of 17

Increased cost-based headwinds

across the cost structure (i.e. raw

material & fuel prices) are likely to

reduce profitability particularly in a

scenario where pricing power is likely

to be modest

On valuation front, SCL is relatively

trading at premium compared to its

peers

Key Concerns

Capacity augmentation a concern for cement players

� The cement industry of the country is currently facing a serious

threat from the heavy augmentation of capacities which has been

added during the last three years coupled with subdued demand

resulting in over supply situation.

Soaring raw material prices

� Prices of key raw materials viz. limestone and gypsum are on the

increasing trends over the past few quarters. While prices of

limestone have increased due to increase in royalty payments to

Government of India, its impact is limited as SCL has captive

limestone reserves.

Comparative Valuation

Particulars Ultra Tech ACC * Shree Cement

Total Income 175,917.5 102,374.4 42,222.9

EBITDA 40,102.5 19,212.3 10,927.8

EBITDA Margin (%) 22.80% 18.8% 25.9%

PAT 23,056.4 13,008.0 2,184.3

PAT Margin (%) 13.11% 12.7% 5.2%

Diluted EPS 84.13 68.70 62.7

Book Value Per Share 424.3 371.7 597.0

CMP (26-Mar-12) 1491 1330.3 2923.9

P/E (x) 17.7 19.4 46.6

P/BV (x) 3.5 3.6 4.9

Debt/Equity (x) 0.35 0.07 0.84

ROE (%) 19.8% 18.5% 10.5%

EV/EBITDA (x) 11.2 12.4 10.5

EV/Total Income (x) 2.5 2.3 2.7

FY12E Capacity (mtpa) 52.0 28.7 13.5

EV/tonne (In USD) 172.1 166.1 170.2

Exhibit: Comparative Valuation Figs in INR Million

Source: Company, SKP Research

Note: Total Income, EBITDA, PAT are on TTM Basis ended December 2011, while

Debt/Equity & ROE (%) as on September 2011, * ACC financials are for the calender year

2011.

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 12 of 17

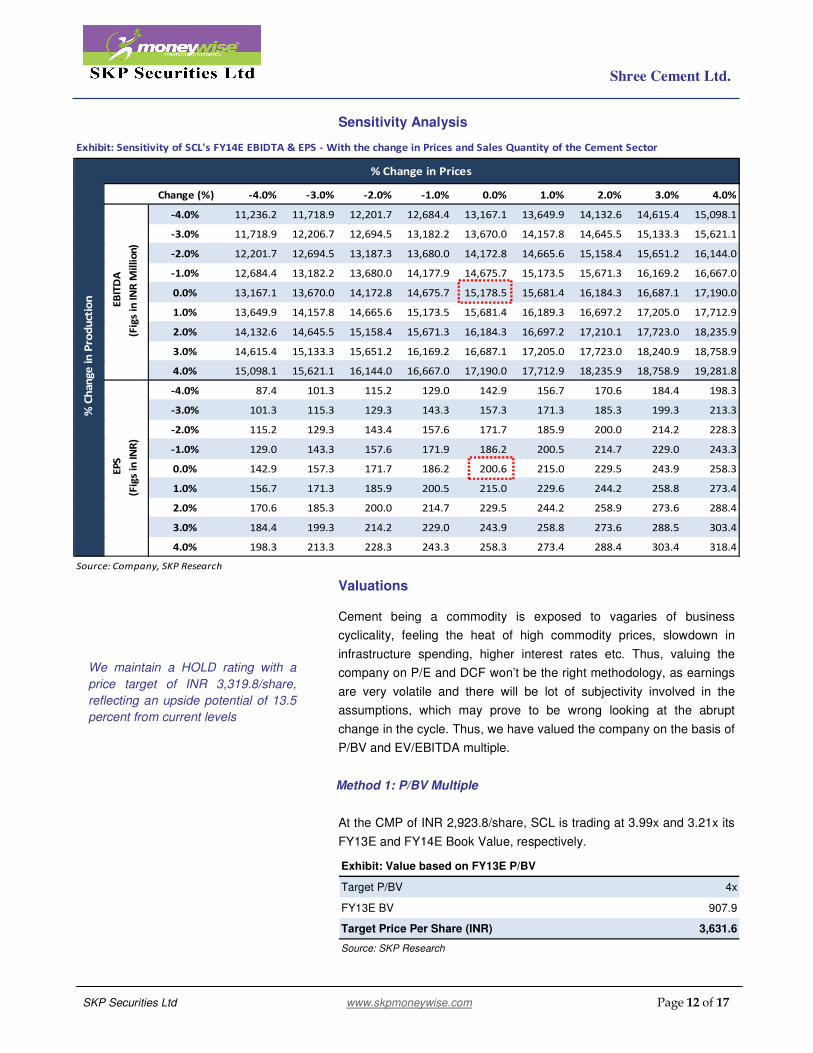

We maintain a HOLD rating with a

price target of INR 3,319.8/share,

reflecting an upside potential of 13.5

percent from current levels

Sensitivity Analysis

Valuations

Cement being a commodity is exposed to vagaries of business

cyclicality, feeling the heat of high commodity prices, slowdown in

infrastructure spending, higher interest rates etc. Thus, valuing the

company on P/E and DCF won’t be the right methodology, as earnings

are very volatile and there will be lot of subjectivity involved in the

assumptions, which may prove to be wrong looking at the abrupt

change in the cycle. Thus, we have valued the company on the basis of

P/BV and EV/EBITDA multiple.

Method 1: P/BV Multiple

At the CMP of INR 2,923.8/share, SCL is trading at 3.99x and 3.21x its

FY13E and FY14E Book Value, respectively.

Target P/BV 4x

FY13E BV 907.9

Target Price Per Share (INR) 3,631.6

Exhibit: Value based on FY13E P/BV

Source: SKP Research

Change (%) -4.0% -3.0% -2.0% -1.0% 0.0% 1.0% 2.0% 3.0% 4.0%

-4.0% 11,236.2 11,718.9 12,201.7 12,684.4 13,167.1 13,649.9 14,132.6 14,615.4 15,098.1

-3.0% 11,718.9 12,206.7 12,694.5 13,182.2 13,670.0 14,157.8 14,645.5 15,133.3 15,621.1

-2.0% 12,201.7 12,694.5 13,187.3 13,680.0 14,172.8 14,665.6 15,158.4 15,651.2 16,144.0

-1.0% 12,684.4 13,182.2 13,680.0 14,177.9 14,675.7 15,173.5 15,671.3 16,169.2 16,667.0

0.0% 13,167.1 13,670.0 14,172.8 14,675.7 15,178.5 15,681.4 16,184.3 16,687.1 17,190.0

1.0% 13,649.9 14,157.8 14,665.6 15,173.5 15,681.4 16,189.3 16,697.2 17,205.0 17,712.9

2.0% 14,132.6 14,645.5 15,158.4 15,671.3 16,184.3 16,697.2 17,210.1 17,723.0 18,235.9

3.0% 14,615.4 15,133.3 15,651.2 16,169.2 16,687.1 17,205.0 17,723.0 18,240.9 18,758.9

4.0% 15,098.1 15,621.1 16,144.0 16,667.0 17,190.0 17,712.9 18,235.9 18,758.9 19,281.8

-4.0% 87.4 101.3 115.2 129.0 142.9 156.7 170.6 184.4 198.3

-3.0% 101.3 115.3 129.3 143.3 157.3 171.3 185.3 199.3 213.3

-2.0% 115.2 129.3 143.4 157.6 171.7 185.9 200.0 214.2 228.3

-1.0% 129.0 143.3 157.6 171.9 186.2 200.5 214.7 229.0 243.3

0.0% 142.9 157.3 171.7 186.2 200.6 215.0 229.5 243.9 258.3

1.0% 156.7 171.3 185.9 200.5 215.0 229.6 244.2 258.8 273.4

2.0% 170.6 185.3 200.0 214.7 229.5 244.2 258.9 273.6 288.4

3.0% 184.4 199.3 214.2 229.0 243.9 258.8 273.6 288.5 303.4

4.0% 198.3 213.3 228.3 243.3 258.3 273.4 288.4 303.4 318.4

% Change in Prices

% C

han

ge

in

Pro

du

ctio

n

Exhibit: Sensitivity of SCL's FY14E EBIDTA & EPS - With the change in Prices and Sales Quantity of the Cement Sector

Source: Company, SKP Research

EB

ITD

A

(Fig

s in

IN

R M

illi

on

)

EP

S

(Fig

s in

IN

R)

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 13 of 17

SCL historically traded in a wide

band of 2x to 10x on the one year

forward EV/EBITDA basis, mainly

due to high volatility in earnings on

account of cyclical nature of cement

industry

Exhibit: One Year Forward P/BV Band

Source: Company, SKP Research

0

500

1000

1500

2000

2500

3000

3500

Mar-

07

Sep-0

7

Mar-

08

Sep-0

8

Mar-

09

Sep-0

9

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

4x 3.5x 3x 2.5x 2x

Method 2: EV/EBITDA Multiple

SCL is trading at an EV/EBITDA of 8.32x and 6.79x FY13E and FY14E

EBITDA respectively.

Target EV/EBITDA Multiple 7x

FY14E EBITDA (INR Million) 15,178.5

Target EV (INR Million) 106,249.8

Less: FY14E Debt (INR Million) (15,070.3)

Add: FY14E Cash (INR Million) 13,612.2

Target Market Cap (INR Million) 104,791.8

No of Shares (in Million) 34.8

Target Price Per Share (INR) 3,008.0

Exhibit: Value based on FY13E EV/EBITDA

Source: SKP Research

Exhibit: One Year Forward EV/EBITDA Band

Source: Company, SKP Research

0

20

40

60

80

100

120

140

160

Mar-

07

Sep-0

7

Mar-

08

Sep-0

8

Mar-

09

Sep-0

9

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

Fig

s. In

IN

R B

illio

n

10x 8x 6x 4x 2x

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 14 of 17

On an EV/tonne basis, SCL is trading

at USD160.4 and USD153.1 its

FY13E and FY14E capacities of 13.5

MTPA

At CMP, the stock is trading at 22.6x

and 14.6x its FY13E and FY14E

earnings, respectively

Thus, assigning equal weightage to P/BV and EV/EBITDA

methodology, we arrived at a price target of INR 3,319.8/share,

implying an upside potential of 13.5 percent. We initiate coverage

on the company with ACCUMULATE rating.

One Year Forward EV/tonne Band

Exhibit: One Year Forward EV/tonne Band

Source: Company, SKP Research

30

50

70

90

110

130

150

170

190

210

Mar-

08

Aug-0

8

Jan-0

9

Jul-09

Dec-0

9

May-1

0

Oct-

10

Mar-

11

Aug-1

1

Jan-1

2

Fig

s. In

US

D/T

onne

One Year Forward P/E Band

Exhibit: One Year Forward P/E Band

Source: Company, SKP Research

0

500

1000

1500

2000

2500

3000

3500

4000

4500

Mar-

07

Sep-0

7

Mar-

08

Sep-0

8

Mar-

09

Sep-0

9

Mar-

10

Sep-1

0

Mar-

11

Sep-1

1

Mar-

12

20x 16x 12x 8x 4x

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 15 of 17

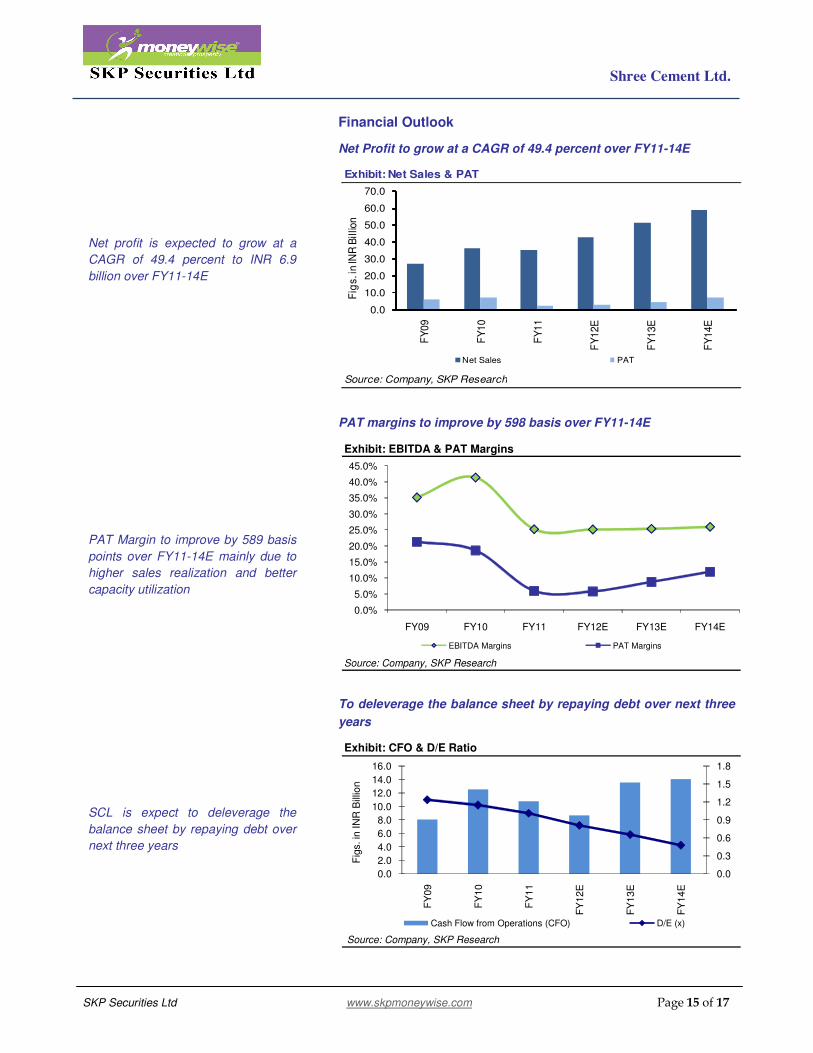

Net profit is expected to grow at a

CAGR of 49.4 percent to INR 6.9

billion over FY11-14E

PAT Margin to improve by 589 basis

points over FY11-14E mainly due to

higher sales realization and better

capacity utilization

SCL is expect to deleverage the

balance sheet by repaying debt over

next three years

Financial Outlook

Net Profit to grow at a CAGR of 49.4 percent over FY11-14E

Source: Company, SKP Research

Exhibit: Net Sales & PAT

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

FY

09

FY

10

FY

11

FY

12E

FY

13E

FY

14E

Fig

s. i

n IN

R B

illio

nNet Sales PAT

PAT margins to improve by 598 basis over FY11-14E

Exhibit: EBITDA & PAT Margins

Source: Company, SKP Research

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

45.0%

FY09 FY10 FY11 FY12E FY13E FY14E

EBITDA Margins PAT Margins

To deleverage the balance sheet by repaying debt over next three

years

Exhibit: CFO & D/E Ratio

Source: Company, SKP Research

0.0

0.3

0.6

0.9

1.2

1.5

1.8

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

FY

09

FY

10

FY

11

FY

12E

FY

13E

FY

14E

Fig

s. in

IN

R B

illio

n

Cash Flow from Operations (CFO) D/E (x)

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 16 of 17

Exhibit: Balance Sheet

Particulars FY11 FY12E FY13E FY14E Particulars FY11 FY12E FY13E FY14E

Net Sales 35,118.7 42,383.5 51,200.0 58,485.2 Share Capital 348.4 348.4 348.4 348.4

Growth (%) -3.3% 20.7% 20.8% 14.2% Reserve & Surplus 19,513.4 21,334.2 25,107.3 31,280.6

Expenditure 26,262.4 31,724.5 38,229.8 43,306.7 Shareholders Funds 19,861.8 21,682.5 25,455.7 31,629.0

Material Consumed 3,723.4 4,175.2 4,701.9 5,320.4 Secured Loan 17,804.9 15,275.9 14,394.4 12,796.2

Power & Fuel Cost 9,123.2 10,807.8 12,335.2 13,977.9 Unsecured Loan 2,274.1 2,274.1 2,274.1 2,274.1

Employee Cost 1,985.4 2,500.6 2,931.1 3,354.7 Total Debt 20,079.0 17,550.0 16,668.5 15,070.3

Packing & Distribution 2,160.6 2,543.0 2,809.0 3,075.1 Total Liabilities 39,940.8 39,232.5 42,124.2 46,699.2

Freight & Selling Exp. 6,140.6 7,205.2 10,904.4 12,360.5

Admin & Other Exp. 3,129.2 4,492.6 4,548.2 5,218.0 Net Block inc Capital WIP 21,948.9 15,540.5 13,363.9 11,744.7

EBITDA 8,856.4 10,659.0 12,970.2 15,178.5 Investments 11,964.6 13,403.0 14,072.7 16,058.3

Depreciation 6,757.6 7,869.4 7,176.6 6,619.2 Deferred Tax Asset 722.572 814.893 814.893 814.893

EBIT 2,098.8 2,789.6 5,793.6 8,559.3 Current Assets 14,388.5 17,160.5 24,306.8 29,048.6

Other Income 1,242.9 1,340.3 1,336.9 1,485.4 Inventories 4,042.3 5,113.3 6,206.2 6,506.3

Interest Expense 1,753.5 1,693.3 1,497.1 1,309.2 Sundry Debtors 1,082.1 1,240.2 1,425.0 1,619.5

Profit Before Tax (PBT) 1,588.2 2,436.6 5,633.4 8,735.5 Cash & Bank Balance 4,608.1 5,509.1 10,275.6 13,612.2

Exceptional Items 634.3 484.7 94.4 0.0 Other Current Asset 224.5 211.9 256.0 292.4

Income Tax -993.5 -130.7 1,126.7 1,747.1 Loans & Advances 4,431.5 5,086.0 6,144.0 7,018.2

Effective Tax Rate (%) -62.6 -5.4 20.0 20.0 Current Liabilities & Prov 9,083.9 7,686.4 10,434.0 10,967.3

Profit After Tax (PAT) 2,097.0 2,472.9 4,506.7 6,988.4 Current Liabilities 6,264.2 6,626.8 7,874.0 8,043.0

Growth (%) -69.0 17.9 82.2 55.1 Provisions 2,819.7 1,059.6 2,560.0 2,924.3

Diluted EPS 60.2 71.0 129.4 200.6 Total Assets 39,940.8 39,232.5 42,124.2 46,699.2

Particulars FY11 FY12E FY13E FY14E Particulars FY11 FY12E FY13E FY14E

PBT 1,588.2 2,436.6 5,633.4 8,735.5 Earning Ratios (%)

Depreciation 6,757.6 7,869.4 7,176.6 6,619.2 EBITDA Margin (%) 25.2% 25.1% 25.3% 26.0%

Interest Provided 1,753.5 1,693.3 1,497.1 1,309.2 PAT Margins (%) 6.0% 5.8% 8.8% 11.9%

Chg. in Working Capital 1,634.9 (3,360.8) 367.9 (872.0) ROCE (%) 5.3% 7.0% 14.2% 19.3%

Direct Taxes Paid 708.8 130.7 (1,126.7) (1,747.1) ROE (%) 11.0% 11.9% 19.1% 24.5%

Other Charges (1,698.6) (94.4) - - Per Share Data (INR)

Operating Cash Flows 10,744.3 8,674.8 13,548.3 14,044.9 Diluted EPS 60.2 71.0 129.4 200.6

Capital Expenditure (11,518.0) (1,461.0) (5,000.0) (5,000.0) Cash EPS (CEPS) 254.2 296.9 335.4 390.6

Investments 4,491.6 (1,438.4) (669.7) (1,985.7) BVPS 570.1 622.4 730.7 907.9

Others 665.7 - - - Valuation Ratios (x)

Investing Cash Flows (6,360.7) (2,899.3) (5,669.7) (6,985.7) P/E 34.39 41.19 22.60 14.58

Equity Capital Raised - - - - Price/BVPS 3.63 4.70 4.00 3.22

Inc / (Dec) in Debt (1,629.6) (2,529.0) (881.5) (1,598.3) EV/Sales 2.49 2.69 2.11 1.77

Dividend Paid (inc tax) (568.7) (652.1) (733.6) (815.1) EV/EBITDA 9.89 10.69 8.35 6.81

Interest Paid (1,741.0) (1,693.3) (1,497.1) (1,309.2) Dividend Yield (%) 0.7% 0.5% 0.6% 0.7%

Financing Cash Flows (3,939.3) (4,874.4) (3,112.2) (3,722.6) Balance Sheet Ratios

Chg. in Cash & Cash Eqv 444.3 901.0 4,766.5 3,336.6 Debt - Equity 1.0 0.8 0.7 0.5

Opening Cash Balance 4,163.7 4,608.1 5,509.1 10,275.6 Current Ratio 1.6 2.2 2.3 2.6

Closing Cash Balance 4,608.1 5,509.1 10,275.6 13,612.2 Fixed Asset Turn. Ratios 3.7 3.1 4.0 7.3

Source: Company Data, SKP Research

Exhibit: Income Statement Figures in INR Million Figures in INR Million

Exhibit: Cash Flow Statement Figures in INR Million Exhibit: Ratio Analysis

Shree Cement Ltd.

SKP Securities Ltd www.skpmoneywise.com Page 17 of 17

The above analysis and data are based on last available prices and not official closing rates. SKP Research is also available on Bloomberg, Thomson

First Call & Investext Myiris, Moneycontrol, Ticker plant and ISI Securities

DISCLAIMER: This document has been issued by SKP Securities Ltd (SKP), a stock broker registered with and regulated by Securities & Exchange Board of India, for the information of its clients/potential clients and business associates/affiliates only and is for private circulation only, disseminated and available

electronically and in printed form. Additional information on recommended securities may be made available on request. This document is supplied to you solely

for your information and no matter contained herein may be reproduced, reprinted, sold, copied in whole or in part, redistributed or passed on, directly or indirectly, to any other person for any purpose, in India or into any other country without prior written consent of SKP. The distribution of this document in other

jurisdictions may be strictly restricted and/ or prohibited by law, and persons into whose possession this document comes should inform themselves about such

restriction and/ or prohibition, and observe any such restrictions and/ or prohibition. If you are dissatisfied with the contents of this complimentary document or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using the document and SKP shall not be responsible and/ or liable in any manner.

Neither this document nor the information or any opinion expressed therein should be construed as an investment advice or offer to anybody to acquire, subscribe,

purchase, sell, dispose of, retain any securities or derivatives related to such securities or an offer to sell or the solicitation of an offer to purchase or subscribe for

any investment or as an official endorsement of any investment. Any recommendation or view or opinion expressed on investments in this document is not

intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any professional advice. The views expressed in this document are those of the analyst which are subject to change and do not represent to be an authority on the subject. SKP may or may not

subscribe to any and/ or all the views expressed herein. It is the endeavor of SKP to ensure that the analyst(s) use current, reliable, comprehensive information and

obtain such information from sources, which the analyst(s) believes to be reliable. However, such information may not have been independently verified by SKP

or the analyst(s). The information, opinions and views contained within this document are based upon publicly available information, considered reliable at the

time of publication, which are subject to change from time to time without any prior notice. The Document may be updated anytime without any prior notice to

anybody. SKP makes no guarantee, representation or warranty, express or implied; and accepts no responsibility or liability as to the accuracy or completeness or

correctness of the information in this Report. SKP, its Directors, affiliates and employees do not accept any liability whatsoever, direct or indirect, that may arise

from the use of the information or recommendations herein. Please note that past performance is not necessarily a guide to evaluate future performance. SKP or its

affiliates, may, from time to time render advisory and other services to companies being referred to in this document and receive compensation for the same. SKP and/or its affiliates, directors and employees may trade for their own account or may also perform or seek to perform investment banking or underwriting services

for or relating to those companies and may also be represented in the supervisory board or on any other committee of those companies or may sell or buy any

securities or make any investment, which may be contrary to or inconsistent with this document. This document should be read and relied upon at the sole discretion and risk of the reader. The value of any investment made at your discretion based on this document or income there from may be affected by changes in

economic, financial and/ or political factors and may go down as well as up and you may not get back the full or the expected amount invested. Some securities

and/ or investments involve substantial risk and are not suitable for all investors. Neither SKP nor its affiliates or their directors, employees, agents or representatives/associates, shall be responsible or liable in any manner, directly or indirectly, for information, views or opinions expressed in this document or the

contents or any errors or discrepancies herein or for any decisions or actions taken in reliance on the document or inability to use or access our service or this

document or for any loss or damages whether direct or indirect, incidental, special or consequential including without limitation loss of revenue or profits or any

loss or damage that may arise from or in connection with the use of or reliance on this document or inability to use or access our service or this document.

SKP Securities Ltd

Contacts Research Sales

Mumbai Kolkata Mumbai Kolkata

Phone 022 2281 9012 033 4007 7000 022 2281 1015 033 4007 7400

Fax 022 2283 0932 033 4007 7007 022 2283 0932 033 4007 7007

E-mail [email protected] [email protected] [email protected]

Member: NSE BSE NSDL CDSL NCDEX* MCX* MCX-SX FPSB *Group Entities

INB/INF: 230707532, BSE INB: 010707538, CDSL IN-DP-CDSL-132-2000, DPID: 021800, NSDL IN-DP-NSDL: 222-2001, DP ID: IN302646, ARN: 0006, NCDEX: 00715, MCX: 31705, MCX-SX: INE 260707532