Side 1

BNCC MEMBERSHIP LUNCHEON

Tuesday, February 26th

CFO Anders Kapstad

BNCC MEMBERSHIP LUNCHEON

Tuesday, February 26th

CFO Anders Kapstad

Norse Energy at a glance

Norse’s Vision and Objectives

Bovespa and the “Novo Mercado”

“Novo Mercado” Requirements

Company Preparation

Costs

Learning Lessons

AgendaAgenda

”All this and oil too”The Economist, 17th Nov 2007

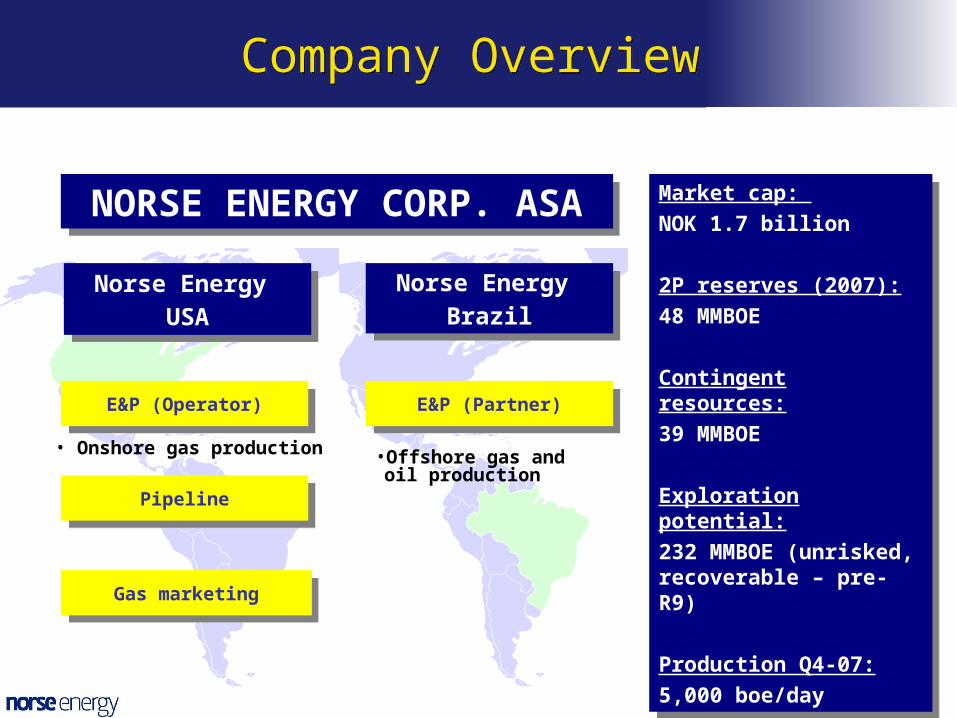

Company OverviewCompany Overview

NORSE ENERGY CORP. ASANORSE ENERGY CORP. ASA

Norse Energy USA

Norse Energy USA

E&P (Operator)E&P (Operator)

PipelinePipeline

Gas marketingGas marketing

• Onshore gas production

Norse Energy Brazil

Norse Energy Brazil

E&P (Partner)E&P (Partner)

•Offshore gas and oil production

Market cap:

NOK 1.7 billion

2P reserves (2007):

48 MMBOE

Contingent resources:

39 MMBOE

Exploration potential:

232 MMBOE (unrisked, recoverable – pre-R9)

Production Q4-07:

5,000 boe/day

Market cap:

NOK 1.7 billion

2P reserves (2007):

48 MMBOE

Contingent resources:

39 MMBOE

Exploration potential:

232 MMBOE (unrisked, recoverable – pre-R9)

Production Q4-07:

5,000 boe/day

Norse Energy do Brasil at a GlanceNorse Energy do Brasil at a Glance

NORSE ENERGY CORP. ASA(Listed in Oslo)

NORSE ENERGY CORP. ASA(Listed in Oslo)

E&P (Partner & Operator)E&P (Partner & Operator)

• Offshore gas and oil production

100%

NORSE ENERGY DO BRASILNORSE ENERGY DO BRASIL

Assets Ownership

(%) Location

Production assets

Manati gas field 10.0 Camamu-Almada Basin (Offshore)

Coral field 35.0 Santos Basin (Offshore)

Development assets

Sardinha field 20.0 Camamu-Almada Basin (Offshore)

Cavalho Marinho field 50.0 Santos Basin (Offshore)

Estrela-do-Mar field 65.0 Santos Basin (Offshore)

Exploration assets

BCAM-40 block 10.0 Camamu-Almada Basin (Offshore)

BM-CAL 5 block 18.3 Camamu-Almada Basin (Offshore)

BM-CAL 6 block 18.3 Camamu-Almada Basin (Offshore)

BT-REC-22 30.0 Reconcavo Basin (Onshore part of Camamu basin)

BT-REC-30 30.0 Reconcavo Basin (Onshore part of Camamu basin)

Round 9 50.0 Santos Basin (Offshore)

Why Brazil?Why Brazil?

• “…there is the potential for many more discoveries on the scale of Tupi—which itself is the world's second-biggest strike in 20 years”.

• “Petrobras announced Nov. 8 it has found between 5 billion and 8 billion barrels of light oil and gas at the Tupi field (..) the largest ever in deep waters. Perhaps more important, Petrobras believes Tupi may be Brazil's first of several new "elephants," an industry term for outsize fields of more than 1 billion barrels”.

BusinessWeek, 19 November 2007

The Economist, 15 November 2007

• Large underexplored area

• Only 22,000 wells drilled to date

• Increasing government focus in Oil & Gas industry

• Infrastructure build-up

• Favorable macro-environment

• Petroleum tax regime, strong currency, increasing GDP growth

• Listing the Brazilian subsidiary rather than follow-on offers in Norway, or BDR* of the Norwegian entity in the Brazilian market

– Offer of pure Brazilian play, only pure E&P publicly listed company on Bovespa

– Brazil as one of the most promising oil frontiers in the world (large potential, under explored basins)

– Improved access to Brazilian and international capital markets

Norse’s Vision and ObjectivesNorse’s Vision and Objectives

*Brazilian Depositary Receipts – international stock values issued in Brazil by international based companies

Bovespa and the Novo MercadoBovespa and the Novo Mercado

• Unique Brazilian stock exchange market

• Largest stock market in Latin America (70% of the region’s traded volume)

• 64 IPOs in 2007

• Novo Mercado (Tag Along) – listing segment where companies voluntarily follows additional corporate governance requirements

– Stock value influenced by shareholders’ additional rights compared to other listings in Bovespa

• Typical investor structure: 70 % international investors (qualified institutional buyers), 20 % Brazilian institutional Investors, 10 % Brazilian retail investors

30 000

40 000

50 000

60 000

70 000

2006 2007 2008

• Only common stocks issued (no preferred stocks)

• Tag along rights to all shareholders of the company

• Board of directors with minimum of five members. At least 20% of the board as independent BOD members

• At least 25% of free float

• Minimum 25 % of of net result dividend distribution

• International standards of financial statements IFRS or US GAAP (requirement from 2009)

• Yearly meetings with analysts and investors

• Public annual calendar – BOD meetings, annual shareholders meeting, quarterly reports

• Acceptance of Câmara de Arbitragem do Mercado to solve shareholders’ conflicts

Novo Mercado RequirementsNovo Mercado Requirements

• Choose financial advisor– Largests investment banks in Brazil:

• UBS Pactual• Credit Suisse• Banco Itau• Unibanco

• Company valuation

• Choose coordinators (sole/ joint bookrunner)

• Choose local and international lawyers

• Audited numbers less than 120 days before filing with CVM (Brazilian SEC)

• Allocate a team responsible for IPO preparation

• Required time : at least 6 months

Company PreparationCompany Preparation

• Costs include:

– Underwriting fees

– Legal fees (US and Brazilian legal team)

– Auditing costs

– Printing

– Travel

– Bovespa related costs

• Plus internal time

Costs: 5-6 % of total deal Costs: 5-6 % of total deal

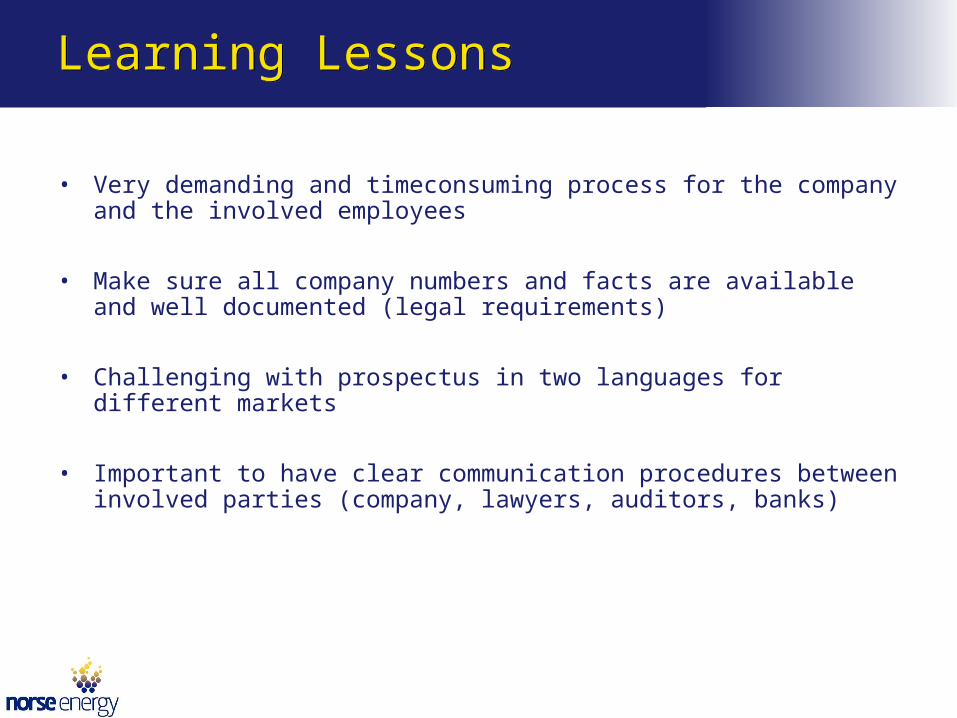

• Very demanding and timeconsuming process for the company and the involved employees

• Make sure all company numbers and facts are available and well documented (legal requirements)

• Challenging with prospectus in two languages for different markets

• Important to have clear communication procedures between involved parties (company, lawyers, auditors, banks)

Learning LessonsLearning Lessons