See important disclosures, including any required research certifications, beginning on page 28

Singapore Consumer Discretionary

What's new: Singapore’s public transport landscape is set to undergo

extensive change. In the rail segment, details of regulatory reform and

asset acquisition are scant, and we believe these developments will only

gain traction after rail reliability obligations have been fulfilled, which we do

not expect to occur in the near term. Meanwhile, in the bus segment, the

transition to a new government contracting model (GCM) is imminent, and

we recommend that investors position themselves ahead of the events we

expect to play out in the run-up to, and following, the GCM’s

implementation in September 2016. We expect shares in the sector to be

rerated over the coming months as clarity increases.

What's the impact: Given that we are drawing close to the GCM’s

implementation, we incorporate its full impact into our forecasts despite the

lack of disclosure. Our recent discussions with new entrant Go-Ahead, as

well as our analysis of the London bus market, where a similar model has

been in place since 2000, strengthen our conviction that the transport

service providers under Daiwa’s coverage will be net beneficiaries of the

shift to the GCM, mainly as we foresee: 1) scope for operating-margin

enhancement as revenue risk is transferred to the government, 2) reduced

capex burdens as the government will assume asset ownership, and 3)

capital proceeds from a potential acquisition of existing bus assets.

After fine-tuning our margin assumptions for the bus segment, we estimate

the move to the GCM will account for 5-9% of our operating profit forecasts

for ComfortDelGro (CDG) for 2016-18E, and 4-7% of SMRT’s for FY17-

19E. In terms of asset acquisitions, we believe a direct acquisition remains

the most sensible option for the regulator, and estimate net inflows of

around SGD566m and SGD44.6m for CDG and SMRT respectively.

What we recommend: We have a Positive rating on the sector. We

reaffirm our Buy (1) call on CDG (CD SP, SGD2.97) with a higher DCF-

based 12-month TP of SGD3.59 (from SGD3.38) and Underperform (4)

rating on SMRT (MRT SP, SGD1.58), after raising our DCF-based TP to

SGD1.41 (from SGD1.34). We continue to prefer CDG over SMRT, as we

believe the former is better placed to leverage this operational shift given

the bus segment is CDG’s largest segment (32% of Singapore revenue vs.

SMRT’s 19%). Further, its superior FCF profile, stronger balance sheet (net

cash of SGD229.2m as at end-2015 vs SMRT’s net debt of SGD665.5m as

at end-FY15) and 2016E dividend yield of 3.3% looks attractive, while the

stock is trading at a 2016E PER of 19.7x (vs. SMRT’s 24.7x for FY17E).

How we differ: We believe the attractiveness of the new bus model in the

Singapore market could be under-appreciated by some in the market.

18 March 2016

Singapore Land Transport Sector

What will restructuring mean for the bus market in

2016?

In a pivotal year for the segment, we expect implementation of a new contracting model in September to be positive for existing operators

Government acquisition of CDG and SMRT’s bus assets could take place by 3Q16

We have a Positive sector rating; prefer CDG over SMRT for superior earnings growth and more attractive valuation

Key stock calls

Source: Daiwa forecasts

Jame Osman(65) 6321 3092

New Prev.

ComfortDelGro Corp (CD SP)

Rating Buy Buy

Target 3.590 3.380

Upside p 20.9%

SMRT Corp (MRT SP)

Rating Underperform Underperform

Target 1.410 1.340

Downside q 11%

2

Singapore Land Transport Sector: 18 March 2016

How do we justify our view?

Growth outlook Valuation Earnings revisions

Growth outlook Singapore Land Transport Sector: net profit growth forecasts

(% YoY)

While we expect the transition to a new bus model in

Singapore in September 2016 to drive an expansion in

operating profit margins for CDG and SMRT, we believe

CDG will be the main beneficiary of this move due to its

greater exposure to the bus segment.

Further, our forecast 6.5% YoY decline in SMRT’s FY17E

net profit (2016 forecasts in the chart) incorporates our

expectation of operating losses for its rail operation (MRT

and LRT), due to: 1) increased rail and maintenance

expenses, 2) the impact of the 1.9% fare reduction

implemented in December 2015, and 3) lower government

grants.

Source: Daiwa forecasts Note: SMRT FY17E forecasts shown above as 2016 forecasts due to March year-end

Valuation Singapore Land Transport Sector: 2016E valuations

The valuations of the land transport operators have seen a

rerating, likely driven by a positive shift in the market’s

outlook toward the public transport sector following

favourable policy announcements signalling the

government’s intention to encourage public transport

usage in the long term.

CDG’s valuations look reasonable to us in the context of

its superior free cash flow generation, stronger balance

sheet and 2016E dividend yield of 3.3%, as well as its

stronger earnings growth prospects, relative to SMRT.

(x) PER PBR EV/EBITDA Dividend yield

CDG 19.7 2.6 7.3 3.3%

SMRT 24.7 2.5 9.0 2.2%

Source: Companies, Daiwa forecasts Note: SMRT’s valuations are for FY17E (March year-end)

Earnings revisions Singapore Land Transport Sector: consensus earnings-forecasts revisions

The Bloomberg-consensus EPS forecasts for 2016-17

have seen downward revisions over the past 12 months,

mainly due to the announcement in October 2015 of a

1.9% reduction in fares by the government. SMRT has

seen sharper cuts due to its greater exposure to the

regulated fare environment (around 72% of revenue vs.

24% for CDG), as well as increased expectations of higher

repair and maintenance and staff costs arising from its rail-

enhancement projects.

2016 2017

EPS EBITDA EPS EBITDA

CDG (4) (4) (4) (7)

SMRT (29) (8) (31) (17)

Source: Bloomberg

-7%

-2%

3%

8%

13%

2016 2017 2018

CDG SMRT

3

Singapore Land Transport Sector: 18 March 2016

Sector stocks: key indicators

Source: Bloomberg, Daiwa forecasts

Singapore Land Transport: timeline of GCM-related events

Date Details

May-14 LTA announces plans for new Government Contracting Model

Oct-14 Tender for Bulim package opened

Apr-15 Tender for Loyang package opened

May-15 Winner of Bulim package announced

Aug-15 SBS Transit announces transfer of BSEP buses to LTA

Nov-15 Winner of Loyang package announced

Dec-15 LTA announces it will take over SBST's 2016/17 bus purchase contracts; acquires 50 of its existing buses at NBV

Upcoming

2Q16E Tender for third bus package (Mandai)

3Q16E Purchase of SBST/SMRT bus assets

4Q16E Award of third bus package

Sep-16 GCM takes effect - Tower Transit commences operations

Source: Companies, Land Transport Authority (LTA), Daiwa compiled

CDG: impact of GCM on Singapore bus segment operating forecasts

SMRT: impact of GCM on Singapore bus segment operating forecasts

SGD m 2014 2015E 2016E 2017E 2018E

Current model

Singapore bus revenues 777.4 848.8 883.1 918.7 955.8

YoY revenue growth

9.2% 4.0% 4.0% 4.0%

Operating profit margin 1.6% 1.6% 1.6% 1.6% 1.6%

Segment operating profit 12.4 13.6 14.1 14.7 15.3

Under proposed GCM

Singapore bus revenues 777.4 848.8 794.75 734.98 764.68

YoY revenue growth

9.2% -6.4% -7.5% 4.0%

Operating profit margin 1.6% 1.6% 4.8% 8.0% 8.0%

Segment operating profit 12.4 13.6 38.1 58.8 61.2

Incremental operating profit - - 24.0 44.1 45.9

% increase to overall operating profit forecasts

5.1% 8.8% 9.0%

Assumptions

First 3 GCM packages are not won by either incumbent

20% decline in revenues (according to % of bus routes lost)

SGD m FY15 FY16E FY17E FY18E FY19E

Current model

Bus segment revenues (non-consolidated) 238.6 250.7 260.8 271.3 282.3

YoY revenue growth

5.1% 4.0% 4.0% 4.0%

Operating profit margin -2.7% 4.0% 1.5% 1.5% 1.5%

Segment operating profit (6.5) 10.0 3.9 4.1 4.2

Under proposed GCM

Bus segment revenues 238.6 250.7 234.7 217.0 225.8

YoY revenue growth

5.1% -6.4% -7.5% 4.0%

Operating profit margin -2.7% 4.0% 3.8% 6.0% 6.0%

Segment operating profit (6.5) 10.0 8.9 13.0 13.5

Incremental operating profit - - 5.0 9.0 9.3

% increase to overall operating profit forecasts

4.1% 7.1% 7.0%

Assumptions

First 3 GCM packages are not won by either incumbent

20% decline in revenues (according to % of bus routes lost)

Source: Company, Daiwa estimates Note: CDG stopped disclosing segmental Singapore bus revenue in 4Q15; hence full-year

2015 Singapore bus revenue not available

Source: Company, Daiwa estimates

CDG: proceeds from the potential government acquisition of Singapore bus assets

SMRT: proceeds from the potential government acquisition of bus assets

(SGD m) Amount

SBST segmental bus assets (2014) at NBV 1,095

SBST segmental bus liabilities (2014) 411

Net asset value 684

Less: BSEP buses 118

Total potential net proceeds 566

Per share (SGD) 0.27

SBST accumulated profit (2014) 253

Potential payout at CDG level 0.12

(SGD m) Amount

SMRT segmental bus assets (FY15) 393.1

SMRT segmental bus liabilities (FY15) 348.5

Net asset value 44.6

Potential net proceeds 44.6

Per share (SGD) 0.02

Source: Company, Daiwa estimates

Source: Company, Daiwa estimates

Share

Company Name Stock code Price New Prev. New Prev. % chg New Prev. % chg New Prev. % chg

ComfortDelGro Corp CD SP 2.970 Buy Buy 3.590 3.380 6.2% 0.151 0.153 (1.6%) 0.167 0.171 (2.6%)

SMRT Corp MRT SP 1.585 Underperform Underperform 1.410 1.340 5.2% 0.069 0.069 0.0% 0.064 0.065 (1.8%)

Rating Target price (local curr.) FY1

EPS (local curr.)

FY2

4

Singapore Land Transport Sector: 18 March 2016

Table of contents

Spotlight on the bus segment ................................................................................. 5

A strong push toward greater public transport use .............................................................5

GCM: a recap ....................................................................................................................7

How could the market evolve? ...........................................................................................8

Assessing the impact on financials .................................................................................. 10

Key forecasts ................................................................................................................... 14

Valuations and ratings ..................................................................................................... 16

Key investment risks ........................................................................................................ 18

Company Section

ComfortDelGro Corp ........................................................................................................ 20

SMRT Corp ...................................................................................................................... 23

5

Singapore Land Transport Sector: 18 March 2016

Spotlight on the bus segment

A strong push toward greater public transport use

The public bus segment will see the biggest restructuring

2016 will be a pivotal year for the public transport landscape in Singapore, particularly in

the bus segment, with the transition to a new government contracting model (GCM) in

September 2016. We believe investors should position themselves ahead of the events

that we expect to happen in the lead-up to, and following, the GCM’s implementation.

Despite the likely increase in competition within the bus segment, we believe the transport

service providers under our coverage will still be net beneficiaries of the shift to the new

GCM. This is mainly because revenue and ridership risks will be transferred to the

government under the new system and, as a result, the operators will no longer be

subjected to a regulated fare pricing environment, which has historically been an

impediment to the segment’s profitability.

While there is uncertainty over the level at which margins for the operators could settle

post-GCM, our recent discussions with new entrant Go-Ahead, as well as our analysis of

the London bus market, where a similar bus model is in place, strengthen our conviction

that operating margins of the existing operators will expand significantly from current

levels. After fine-tuning our margin assumptions for the Singapore bus segment for CDG

and SMRT to improve to 6-8% by 2017 (from 8-10% previously), from around 0-2% levels

currently, we estimate the move to the GCM will account for 5-9% of our overall operating

profit forecasts for CDG for 2016-18, and 4-7% of our forecasts for SMRT for FY17-19E.

The other key event investors are waiting on is greater clarity over the potential acquisition

of bus assets of CDG and SMRT by the government. We believe that a direct acquisition

remains the most sensible option to ensure consistency among all operators. And recent

indicators suggest that this could indeed happen in the near term – the government

announced in December 2015 that it will purchase 50 of CDG’s newer buses at net book

value. We expect this to be the benchmark used going forward. Despite the overall lack of

disclosure from both the government and operators, we estimate net inflows of around

SGD566m and SGD44.6m for CDG and SMRT, respectively. We believe that an

acquisition could occur by 3Q16, and we may obtain further clarity as early as 24 March,

the date of the Singapore Budget 2016 announcement.

Singapore Land Transport: timeline of bus GCM-related events

Date Details

May-14 LTA announces plans for new Government Contracting Model

Oct-14 Tender for Bulim package opened

Apr-15 Tender for Loyang package opened

May-15 Winner of Bulim package announced

Aug-15 SBS Transit announces transfer of BSEP buses to LTA

Nov-15 Winner of Loyang package announced

Dec-15 LTA announces it will take over SBST's 2016/17 bus purchase contracts; acquires 50 of its existing buses at NBV

Upcoming

2Q16E Tender for third bus package (Mandai)

3Q16E Purchase of SBST/SMRT bus assets

4Q16E Award of third bus package

Sep-16 GCM takes effect - Tower Transit commences operations

Source: Companies, LTA, Daiwa compiled

Government policies remain strongly supportive of the sector

The new bus model underscores the Singapore government’s push toward greater usage

of public transport services in the land-scarce city state. In addition to the bus segment, the

government has undertaken a range of measures, both in the form of policy

implementation and greater infrastructure development, including: 1) curbing private

vehicle usage by reducing annual vehicle growth to just 0.5%, 2) plans to double the length

of the rail network to 360km by 2030, in addition to introducing new rail reform measures,

2016: a pivotal year for

Singapore public

transport

6

Singapore Land Transport Sector: 18 March 2016

and 3) committing a further SGD36bn to develop the public transport system over the next

5 years after spending SGD14bn in the past 5 years.

Recent news flow suggests to us that public transport ridership will continue to see robust

growth over the longer term. In a recent addendum to the President’s Address in January

2016, the Transport Minister outlined his aim to have 75% of commuters using public

transport as their main mode of travel by 2030. In addition, the General Household Survey

2015 indicated that around 58.7% of Singapore’s resident working population commutes to

work by public transport, up from 54.6% in 2010.

Singapore Land Transport Sector: average daily ridership (ADR) trends

Source: Land Transport Authority (LTA)

No clarity over rail reforms yet

Relative to the bus segment, little is known about the potential reforms in the rail segment,

even though negotiations between SMRT and the Land Transport Authority (LTA) has been

ongoing for 2 years. Comments made by the previous Transport Minister in July 2014

highlighting the “wide gap between SMRT’s expectations and LTA’s position”, as well as

the current minister’s comments in January 2016 flagging an improvement in rail reliability

as a “top priority” in the near term, suggest to us it would be in the best interests of the

government and the public for SMRT to fulfil all of its existing obligations with respect to

network efficiency before addressing asset acquisitions. The upshot: a timeline that could

stretch beyond 2018, in our view.

SMRT: potential impact of transition to new rail model on our current valuation

Operational assumptions Upside to Daiwa’s target price (SGD/share)

Asset sale proceeds Assets are acquired in a lump sum of around SGD463m, based on the existing NAV of the MRT segment

0.30

Capex savings SGD120m in annual capex reduction 0.72

Operating margin Assumption that FY19 margin improves to 5% from current forecasts 0.15

Total valuation impact Assuming no change to gearing levels 1.17

Source: Daiwa estimates

While a shift to an asset-light rail model would clearly be positive for SMRT, the timing,

magnitude and terms of such an event remain unclear to the market. As such, we focus

our attention on the bus segment, given the greater clarity over developments in the

coming months.

Positive sector view; we prefer CDG over SMRT

We have a Positive rating on the Singapore Land Transport Services sector, predicated on

our view that policy reform and government investment in public transport infrastructure

augurs well for operators, both in the near and long terms. Over the near term, we prefer

CDG over SMRT, mainly as the former is more exposed to the bus segment (32% of

Singapore revenue vs. SMRT’s 19%), on which there is greater clarity at this stage. CDG’s

experience in overseas markets such as the UK and Australia, where similar models have

been implemented, should also give it a solid base from which to navigate the new

operational landscape over the next few years, in our view.

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

MRT + LRT Bus Taxi

('000 passenger-trips)

Recent government

comments reinforce our

view

7

Singapore Land Transport Sector: 18 March 2016

We believe that CDG’s record of consistent earnings growth (4.1% net profit CAGR over

2005-15), superior free-cash-flow profile, strong balance sheet (net cash of SGD229.2m as

at end-2015 vs SMRT’s net debt of SGD665.5m as at end-FY15) and 2016E dividend yield

of 3.3% remain attractive attributes, even before considering the stock’s 2016E PER of

19.7x (vs. SMRT’s 24.7x for FY2017E). Further, we expect the company to see greater rail

segment revenue growth over the medium term, driven by the opening of DTL 3 as well as

the progressive ramp-up of both DTL 2 and 1. Last, we see greater potential earnings-

growth catalysts for CDG from overseas acquisitions or expansion with the excess capital

it should have on hand post-GCM.

GCM: a recap

The idea for a new bus model was first floated to the Singapore public in the regulator’s

(Land Transport Authority [LTA]) Land Transport Master Plan 2008, in which it outlined

plans to introduce a competitive tendering process based on packages of bus services.

The LTA later hired an external consultant to study the concept of a bus contracting model

to be applied in Singapore.

In May 2014, the LTA announced formal policy changes which would see a major shake-up

of the public bus system. It proposed a new GCM under which all bus routes in Singapore

would be divided into 12 packages – 3 of the 12 packages (each around 300-500 buses)

are to be tendered out between 2014 and mid-2016, while incumbents CDG and SMRT will

continue to operate the remaining 9 packages until August 2021. The government will use

the results of the initial 3 packages as a basis for negotiating the terms for the remaining 9

(which comprise around 80% of the existing bus fleet) with the 2 incumbents.

Singapore Land Transport Sector: key difference between the current and new bus models

Current bus model

New GCM

Licensing - Bus Service Operating Licences (BSOL) for SBS Transit & SMRT, which expire on 31 August 2016

- competitive tendering process to operate a package of bus routes for a period of 5 years + 2 year extension option

Revenue - fare prices set by the government

- operators keep fare revenue

- fare prices set by the government

- government keeps fare revenue

- operators paid according to contract bid, with additional incentive provisions for meeting operating standards

Costs - operators incur all operating costs

- government provides grants (training grants, BSEP grants etc.) to help defray certain costs

- operators incur all operating costs

Assets - operators own all operating assets (buses, fleet management systems, depots etc.)

- government owns all operating assets (buses, fleet management systems, depots etc.)

- operators lease and maintain these assets from the government

Source: LTA, Daiwa compiled

Under this new GCM, the LTA would pay operators to run bus services through competitive

contract tenders for each package, essentially on a ‘cost-plus’ basis. These contracts

would have a 5-year contract period, with an option for a 2-year extension, and be based

on bus routes and service standards (bus frequency, operating hours, etc) as set by the

LTA. Further incentive or bonus payments would be made (up to 10% of the annual service

fee) or correspondingly deducted to encourage operators to provide quality bus services

and ensure good maintenance of operating assets.

To date, the first (Bulim) and second (Loyang) packages have been awarded to UK-based

bus operators Tower Transit and Go-Ahead, respectively. While the third package (Mandai)

has yet to be put up for tender, we expect this to happen in 2Q16, with the winner to be

announced 6-7 months later (ie, in 4Q16). Our current expectations are for all 3 of the

tendered packages to go to new entrants.

CDG and SMRT will

continue to operate 9 of

12 packages until 2021

Contract-based with

incentives attached

8

Singapore Land Transport Sector: 18 March 2016

Details of the Bulim bus package tender Details of the Loyang bus package tender

Package details

Depot Bulim

Service areas Clementi, Jurong East and Bukit Batok bus interchanges

No. of routes 26

No. of buses 380, to grow progressively to about 500 by 2021

Shortlisted bidders

Company Country Bid amount (SGDm)

Go-Ahead Group UK 693

Woodlands Transport Singapore 684

SBS Transit Singapore 600

Busways Group Australia 568

Keolis SA France 559

Tower Transit Group (Winner) UK / Australia 556

RATP DEV Transdev Asia France 463

SMRT Corporation Singapore 453

Package details

Depot Loyang

Service areas Changi Airport, Changi Village Bus Terminals, Pasir Ris and Punggol Bus Interchanges

No. of routes 25

No. of buses 400, to grow progressively to about 500 by 2021

Shortlisted bidders

Company Country Bid amount (SGDm)

Busways Group Australia 631

RATP Dev Transdev Asia France 604

SMRT buses Singapore 598

Tian San Shipping & Kumho C&E Singapore/Korea 570

SBS Transit Singapore 546

Keolis SA France 535

Woodlands Transport Holdings Singapore 532

Go-Ahead Group (Winner) UK 498

Source: LTA Source: LTA

Why the need for a new bus model?

The new Singapore bus model aims to replicate the success seen in developed markets

such as the UK and Australia, where similar models have been implemented (see our case

study in the next section). Under the current system, bus operators shoulder revenue and

ridership risks. Despite the good ridership growth experienced over the past decade,

regulated fare pricing (governed by the Fare Review Mechanism Committee of the Public

Transport Council [PTC]) has restricted operators from raising fare prices in tandem even

in the face of rising costs.

As a result, both incumbent operators have posted poor operating-profit performances over

the past several years, as they have had to absorb escalations in labour and operating

costs in response to demand for higher bus-service standards. Besides this, operators

have been reluctant to increase fleet capacity and generally improve service standards at

the expense of further erosion in profitability. To tackle this, the Bus Service Enhancement

Program (BSEP) was introduced in March 2012 by the government as a transitionary

measure. This involved a commitment of SGD1.1bn to cover the purchase of an additional

1,000 buses to service 80 new bus routes over a 5-year period.

With the planned implementation of GCM in September 2016, the government’s ultimate

aim is to raise service standards for public transport commuters by being able to transmit

more effectively changes in bus services (frequency, punctuality, route details, etc.) as well

as managing fleet capacity, while balancing the interests of all key stakeholders (regulator,

commuters and operators).

For operators, the removal of revenue risk would mean that cost control and service quality

become 2 important aspects of profitability, given that cost savings accrue to the operator,

while meeting or exceeding operating standards would secure bonus/incentive payments.

How could the market evolve?

Case study: London public bus market

The London scheduled bus market is a useful reference point for how the Singapore bus

market could evolve operationally, as the proposed GCM is in many respects similar to

London’s existing bus model — unsurprising given that the Singapore regulator studied the

London model, which is seen as having efficiently raised service standards and commuter

satisfaction levels.

The evolution of the London bus market

Currently, bus services in London account for around 50% of all the city’s public transport

services, operating across 700 routes with a total fleet size of around 8,600 buses

managed by 21 bus operating companies (7 groups, 2 independent), according to

Transport for London (TfL). However, until 1985, all London bus services operated under a

nationalised model.

A careful balance

between each

stakeholder’s interests

9

Singapore Land Transport Sector: 18 March 2016

Over 1985-1999, the city’s government implemented a ‘gross cost’ model (fare revenue

retained by TfL, full operating cost paid to operator) and tendered out routes, while at the

same time splitting the public operator into smaller companies to compete with private-

market participants.

Subsequently, over the 1995-99 period, the government altered the model toward one

based on ‘net cost’ contracts (fare revenue and ridership risk retained by operators), as the

previous gross cost model did not incentivise operators to meet reliability standards.

However, the net cost model posed its own set of issues, as operators prioritised

profitability over service quality, making transmissions of network changes difficult and

contract negotiations tedious. In response, the quality incentive contract (QIC) model was

proposed in 2000 and is still in effect today.

London’s QIC-based model rewards operators for service outperformance and holds many

similarities with the proposed Singapore GCM – contracts are tendered to bidding

operators for a 5-year period (plus an extension for 2 years). The key differences between

the models: 1) London operators are asset owners for the depot/garages, as well as

buses, whereas the regulator will own all bus assets under the Singapore GCM, and 2)

contracts are individually tendered for 5-6 routes in London (over 700 routes altogether,

with around 20% put up for re-tendering every year), while in Singapore all routes have

been divided into 12 packages of 300-500 buses apiece.

Key comparison of Singapore and London bus models

Singapore London

Model Government Contracting Model (GCM) - gross cost model under an incentive framework based on 5 performance indicators

Quality Incentive Contract (QIC) - gross cost contract with incentive provisions (graduated payment scale)

Asset ownership

- regulator (LTA) owns all bus-related assets - operators own bus depots/garages and buses

Operating structure

- regulator keeps fare revenue and shoulders ridership risks

- operators can receive or be deducted up to 10% of annual service fees for meeting/failing performance indicators

- regulator keeps fare revenue and shoulders ridership risks

- operators are able to earn up to 15% of contract price in bonus payments or deducted up to 10% for poor performance

Tender process

- routes divided into 12 packages of 300-500 buses

- contract period of 5 years + 2-year extension option

- individual tender of tranches of 5-6 routes (around 20% of routes up for re-tender each year)

- contract period of 5 years + 2-year extension option

Source: News reports, LTA, TfL

Currently, there are around 7 key operators vying for bus contracts in London. With the

implementation of a competitive tender-based model, the overall bus market has seen

service reliability standards improve, leading to ridership growth and record commuter

satisfaction levels.

Go-Ahead Group: London bus segment revenue and operating profit trend

Source: Company

8.9%

9.0%

9.1%

9.2%

9.3%

9.4%

9.5%

9.6%

200

250

300

350

400

450

500

FY11 FY12 FY13 FY14 FY15

London bus revenue (LHS) Operating margin (RHS)

(GPP m)

Key comparison

between Singapore and

London models

10

Singapore Land Transport Sector: 18 March 2016

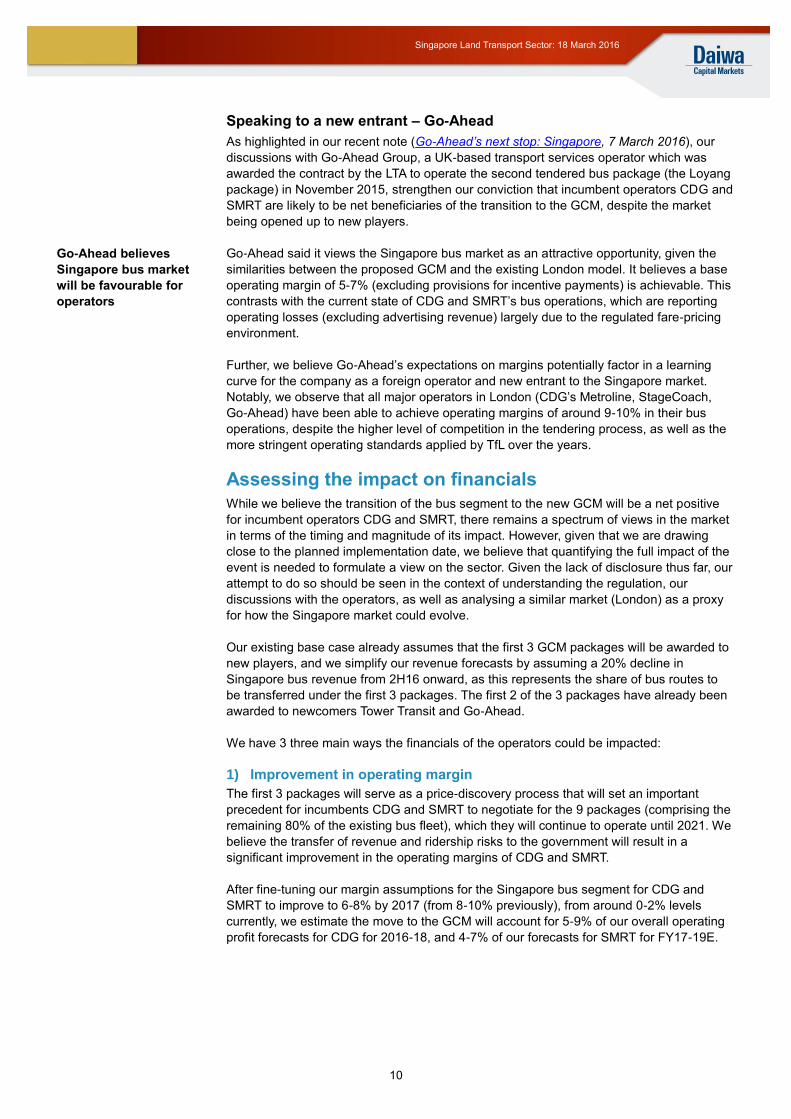

Speaking to a new entrant – Go-Ahead

As highlighted in our recent note (Go-Ahead’s next stop: Singapore, 7 March 2016), our

discussions with Go-Ahead Group, a UK-based transport services operator which was

awarded the contract by the LTA to operate the second tendered bus package (the Loyang

package) in November 2015, strengthen our conviction that incumbent operators CDG and

SMRT are likely to be net beneficiaries of the transition to the GCM, despite the market

being opened up to new players.

Go-Ahead said it views the Singapore bus market as an attractive opportunity, given the

similarities between the proposed GCM and the existing London model. It believes a base

operating margin of 5-7% (excluding provisions for incentive payments) is achievable. This

contrasts with the current state of CDG and SMRT’s bus operations, which are reporting

operating losses (excluding advertising revenue) largely due to the regulated fare-pricing

environment.

Further, we believe Go-Ahead’s expectations on margins potentially factor in a learning

curve for the company as a foreign operator and new entrant to the Singapore market.

Notably, we observe that all major operators in London (CDG’s Metroline, StageCoach,

Go-Ahead) have been able to achieve operating margins of around 9-10% in their bus

operations, despite the higher level of competition in the tendering process, as well as the

more stringent operating standards applied by TfL over the years.

Assessing the impact on financials

While we believe the transition of the bus segment to the new GCM will be a net positive

for incumbent operators CDG and SMRT, there remains a spectrum of views in the market

in terms of the timing and magnitude of its impact. However, given that we are drawing

close to the planned implementation date, we believe that quantifying the full impact of the

event is needed to formulate a view on the sector. Given the lack of disclosure thus far, our

attempt to do so should be seen in the context of understanding the regulation, our

discussions with the operators, as well as analysing a similar market (London) as a proxy

for how the Singapore market could evolve.

Our existing base case already assumes that the first 3 GCM packages will be awarded to

new players, and we simplify our revenue forecasts by assuming a 20% decline in

Singapore bus revenue from 2H16 onward, as this represents the share of bus routes to

be transferred under the first 3 packages. The first 2 of the 3 packages have already been

awarded to newcomers Tower Transit and Go-Ahead.

We have 3 three main ways the financials of the operators could be impacted:

1) Improvement in operating margin

The first 3 packages will serve as a price-discovery process that will set an important

precedent for incumbents CDG and SMRT to negotiate for the 9 packages (comprising the

remaining 80% of the existing bus fleet), which they will continue to operate until 2021. We

believe the transfer of revenue and ridership risks to the government will result in a

significant improvement in the operating margins of CDG and SMRT.

After fine-tuning our margin assumptions for the Singapore bus segment for CDG and

SMRT to improve to 6-8% by 2017 (from 8-10% previously), from around 0-2% levels

currently, we estimate the move to the GCM will account for 5-9% of our overall operating

profit forecasts for CDG for 2016-18, and 4-7% of our forecasts for SMRT for FY17-19E.

Go-Ahead believes

Singapore bus market

will be favourable for

operators

11

Singapore Land Transport Sector: 18 March 2016

CDG: impact of GCM on Singapore bus segment operating forecasts

SGD m 2014 2015E 2016E 2017E 2018E

Current model

Singapore bus revenues 777.4 848.8 883.1 918.7 955.8

YoY revenue growth

9.2% 4.0% 4.0% 4.0%

Operating profit margin 1.6% 1.6% 1.6% 1.6% 1.6%

Segment operating profit 12.4 13.6 14.1 14.7 15.3

Under proposed GCM

Singapore bus revenues 777.4 848.8 794.75 734.98 764.68

YoY revenue growth

9.2% -6.4% -7.5% 4.0%

Operating profit margin 1.6% 1.6% 4.8% 8.0% 8.0%

Segment operating profit 12.4 13.6 38.1 58.8 61.2

Incremental operating profit - - 24.0 44.1 45.9

% increase to overall operating profit forecasts

5.1% 8.8% 9.0%

Assumptions

First 3 GCM packages are not won by either incumbent

20% decline in revenues (according to % of bus routes lost)

Source: Company, Daiwa estimates Note: CDG stopped disclosing segmental Singapore bus revenue in 4Q15; hence full-year 2015 Singapore bus revenue not available

SMRT: impact of GCM on bus segment operating profit forecasts

SGD m FY15 FY16E FY17E FY18E FY19E

Current model

Bus segment revenues (unconsolidated) 238.6 250.7 260.8 271.3 282.3

YoY revenue growth

5.1% 4.0% 4.0% 4.0%

Operating profit margin -2.7% 4.0% 1.5% 1.5% 1.5%

Segment operating profit (6.5) 10.0 3.9 4.1 4.2

Under proposed GCM

Bus segment revenues 238.6 250.7 234.7 217.0 225.8

YoY revenue growth

5.1% -6.4% -7.5% 4.0%

Operating profit margin -2.7% 4.0% 3.8% 6.0% 6.0%

Segment operating profit (6.5) 10.0 8.9 13.0 13.5

Incremental operating profit - - 5.0 9.0 9.3

% increase to overall operating profit forecasts

4.1% 7.1% 7.0%

Assumptions

First 3 GCM packages are not won by either incumbent

20% decline in revenues (according to % of bus routes lost)

Source: Company, Daiwa estimates

Sensitivity analysis to operating margins: A 1.0pp decrease/increase in our operating-

margin assumptions could positively/negatively impact our valuations for CDG by

SGD0.05/share and for SMRT by SGD0.02/share respectively (1.4% of our 12-month

target prices for both stocks).

2) Reduction in capex burden

With the government taking ownership of all bus assets under the GCM, we expect both

CDG and SMRT’s future bus capex commitments to be correspondingly alleviated. Recent

moves by the LTA reaffirm our expectations – in December 2015, the regulator announced

it would be taking over SBS Transit’s contracts for new bus purchases scheduled for

delivery in 2016 and 2017, cumulatively worth SGD164m.

Based on our discussions with the companies, CDG expects its annual capex levels to

decline by around SGD150-180m, while SMRT said around 30-35% of its overall capex

spend is allocated to its bus segment. In 1H FY16, SMRT spent around SGD50.7m in bus-

related capex.

We have factored in around a SGD150m reduction in CDG’s bus segment cash capex (our

2016E overall capex forecast: SGD421.2m), while we estimate SMRT’s bus segment

capex levels will decline by around SGD90m annually as a result of the transition to the

GCM (our overall FY17E capex forecast: SGD286.2m).

Government will take

over the purchase of

new buses post-GCM

12

Singapore Land Transport Sector: 18 March 2016

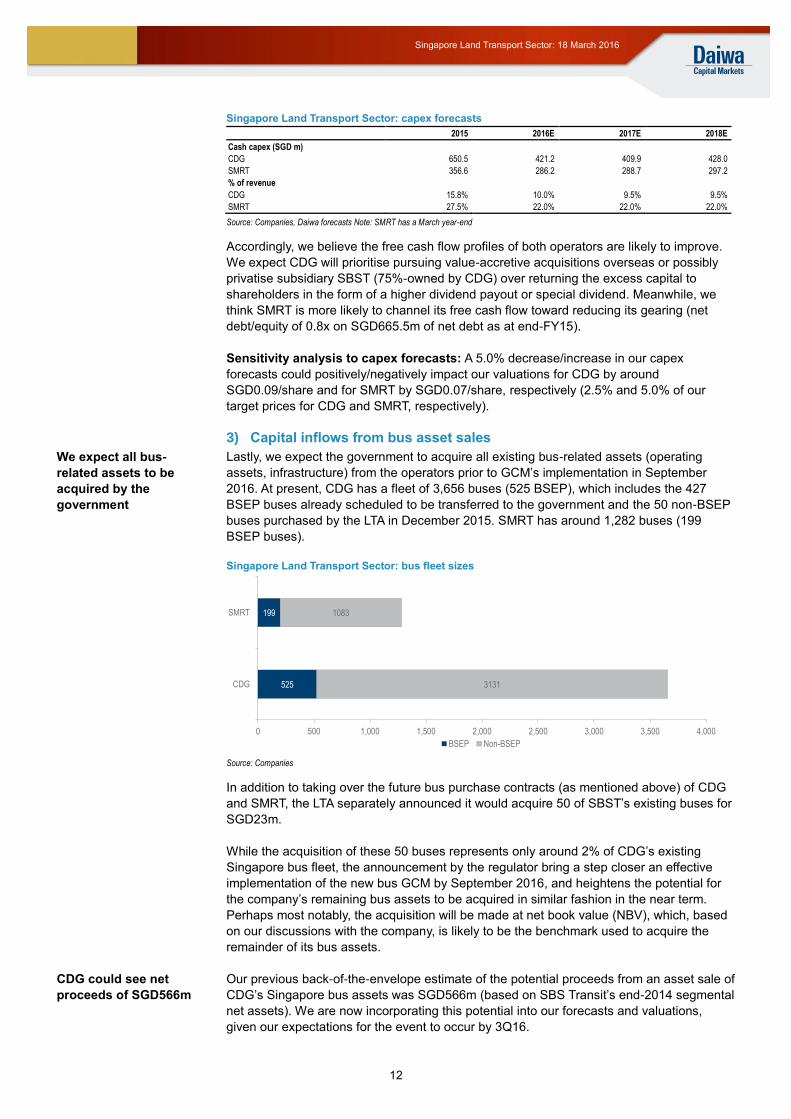

Singapore Land Transport Sector: capex forecasts

2015 2016E 2017E 2018E

Cash capex (SGD m)

CDG 650.5 421.2 409.9 428.0

SMRT 356.6 286.2 288.7 297.2

% of revenue

CDG 15.8% 10.0% 9.5% 9.5%

SMRT 27.5% 22.0% 22.0% 22.0%

Source: Companies, Daiwa forecasts Note: SMRT has a March year-end

Accordingly, we believe the free cash flow profiles of both operators are likely to improve.

We expect CDG will prioritise pursuing value-accretive acquisitions overseas or possibly

privatise subsidiary SBST (75%-owned by CDG) over returning the excess capital to

shareholders in the form of a higher dividend payout or special dividend. Meanwhile, we

think SMRT is more likely to channel its free cash flow toward reducing its gearing (net

debt/equity of 0.8x on SGD665.5m of net debt as at end-FY15).

Sensitivity analysis to capex forecasts: A 5.0% decrease/increase in our capex

forecasts could positively/negatively impact our valuations for CDG by around

SGD0.09/share and for SMRT by SGD0.07/share, respectively (2.5% and 5.0% of our

target prices for CDG and SMRT, respectively).

3) Capital inflows from bus asset sales

Lastly, we expect the government to acquire all existing bus-related assets (operating

assets, infrastructure) from the operators prior to GCM’s implementation in September

2016. At present, CDG has a fleet of 3,656 buses (525 BSEP), which includes the 427

BSEP buses already scheduled to be transferred to the government and the 50 non-BSEP

buses purchased by the LTA in December 2015. SMRT has around 1,282 buses (199

BSEP buses).

Singapore Land Transport Sector: bus fleet sizes

Source: Companies

In addition to taking over the future bus purchase contracts (as mentioned above) of CDG

and SMRT, the LTA separately announced it would acquire 50 of SBST’s existing buses for

SGD23m.

While the acquisition of these 50 buses represents only around 2% of CDG’s existing

Singapore bus fleet, the announcement by the regulator bring a step closer an effective

implementation of the new bus GCM by September 2016, and heightens the potential for

the company’s remaining bus assets to be acquired in similar fashion in the near term.

Perhaps most notably, the acquisition will be made at net book value (NBV), which, based

on our discussions with the company, is likely to be the benchmark used to acquire the

remainder of its bus assets.

Our previous back-of-the-envelope estimate of the potential proceeds from an asset sale of

CDG’s Singapore bus assets was SGD566m (based on SBS Transit’s end-2014 segmental

net assets). We are now incorporating this potential into our forecasts and valuations,

given our expectations for the event to occur by 3Q16.

525

199

3131

1083

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000

CDG

SMRT

BSEP Non-BSEP

We expect all bus-

related assets to be

acquired by the

government

CDG could see net

proceeds of SGD566m

13

Singapore Land Transport Sector: 18 March 2016

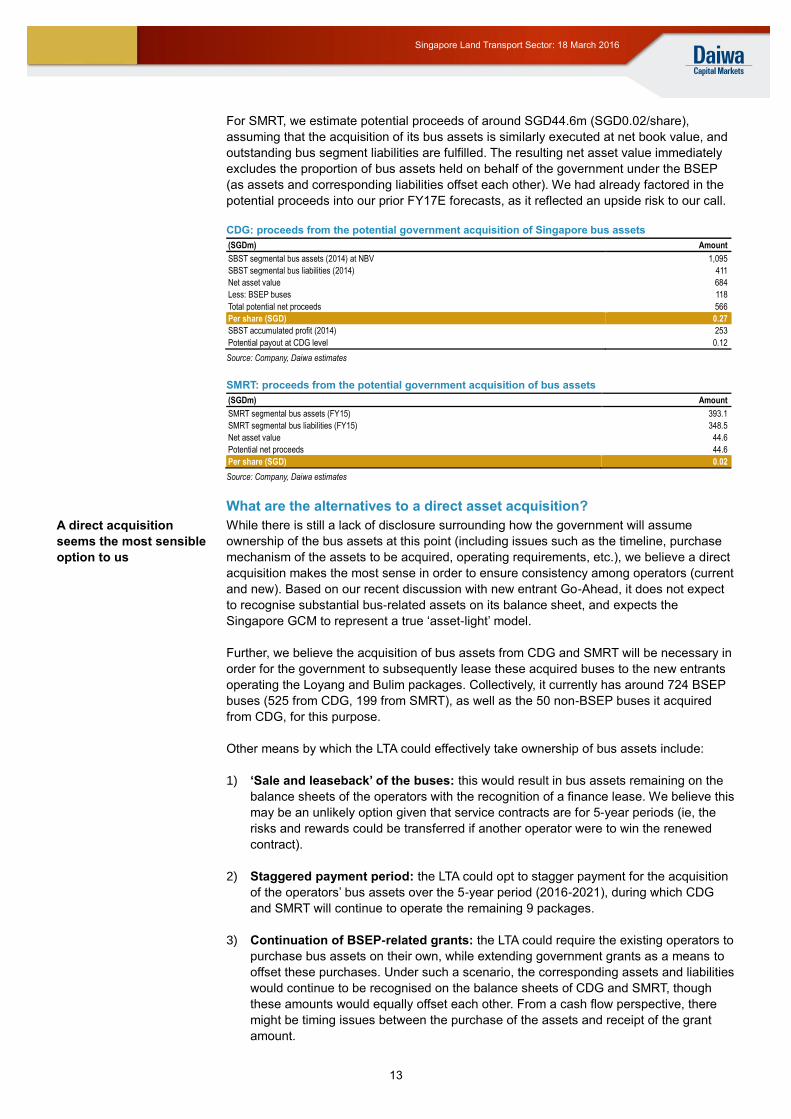

For SMRT, we estimate potential proceeds of around SGD44.6m (SGD0.02/share),

assuming that the acquisition of its bus assets is similarly executed at net book value, and

outstanding bus segment liabilities are fulfilled. The resulting net asset value immediately

excludes the proportion of bus assets held on behalf of the government under the BSEP

(as assets and corresponding liabilities offset each other). We had already factored in the

potential proceeds into our prior FY17E forecasts, as it reflected an upside risk to our call.

CDG: proceeds from the potential government acquisition of Singapore bus assets

(SGDm) Amount

SBST segmental bus assets (2014) at NBV 1,095

SBST segmental bus liabilities (2014) 411

Net asset value 684

Less: BSEP buses 118

Total potential net proceeds 566

Per share (SGD) 0.27

SBST accumulated profit (2014) 253

Potential payout at CDG level 0.12

Source: Company, Daiwa estimates

SMRT: proceeds from the potential government acquisition of bus assets

(SGDm) Amount

SMRT segmental bus assets (FY15) 393.1

SMRT segmental bus liabilities (FY15) 348.5

Net asset value 44.6

Potential net proceeds 44.6

Per share (SGD) 0.02

Source: Company, Daiwa estimates

What are the alternatives to a direct asset acquisition?

While there is still a lack of disclosure surrounding how the government will assume

ownership of the bus assets at this point (including issues such as the timeline, purchase

mechanism of the assets to be acquired, operating requirements, etc.), we believe a direct

acquisition makes the most sense in order to ensure consistency among operators (current

and new). Based on our recent discussion with new entrant Go-Ahead, it does not expect

to recognise substantial bus-related assets on its balance sheet, and expects the

Singapore GCM to represent a true ‘asset-light’ model.

Further, we believe the acquisition of bus assets from CDG and SMRT will be necessary in

order for the government to subsequently lease these acquired buses to the new entrants

operating the Loyang and Bulim packages. Collectively, it currently has around 724 BSEP

buses (525 from CDG, 199 from SMRT), as well as the 50 non-BSEP buses it acquired

from CDG, for this purpose.

Other means by which the LTA could effectively take ownership of bus assets include:

1) ‘Sale and leaseback’ of the buses: this would result in bus assets remaining on the

balance sheets of the operators with the recognition of a finance lease. We believe this

may be an unlikely option given that service contracts are for 5-year periods (ie, the

risks and rewards could be transferred if another operator were to win the renewed

contract).

2) Staggered payment period: the LTA could opt to stagger payment for the acquisition

of the operators’ bus assets over the 5-year period (2016-2021), during which CDG

and SMRT will continue to operate the remaining 9 packages.

3) Continuation of BSEP-related grants: the LTA could require the existing operators to

purchase bus assets on their own, while extending government grants as a means to

offset these purchases. Under such a scenario, the corresponding assets and liabilities

would continue to be recognised on the balance sheets of CDG and SMRT, though

these amounts would equally offset each other. From a cash flow perspective, there

might be timing issues between the purchase of the assets and receipt of the grant

amount.

A direct acquisition

seems the most sensible

option to us

14

Singapore Land Transport Sector: 18 March 2016

Singapore Budget 2016 could provide more clues

Last year (Budget 2015), the government announced that in addition to the SGD14bn

investment in the public transport system over the past 5 years, a further SGD36bn would

be committed for the next 5 years. We expect that the government will provide more details

of its intended allocation for 2016 and shed light on a potential bus asset acquisition during

the Budget 2016 announcement (24 March), given the GCM’s scheduled implementation in

September 2016.

Key forecasts

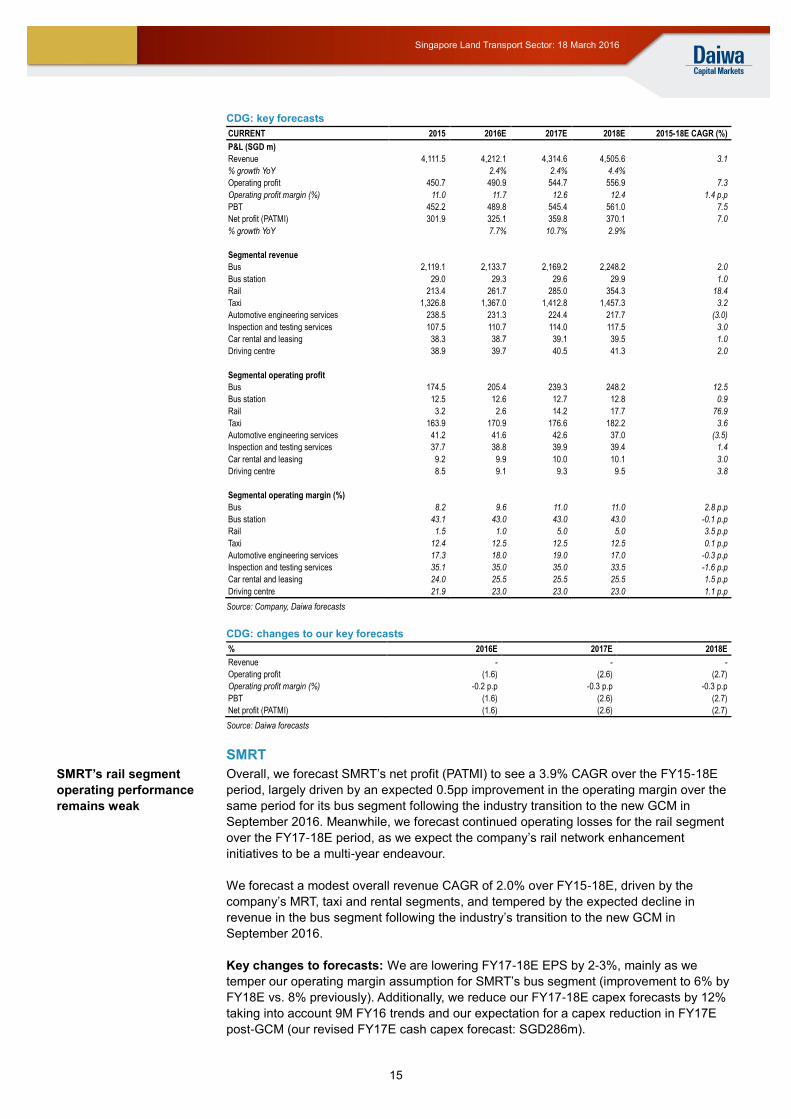

CDG

We forecast CDG’s operating margin to improve by 1.4pp over 2015-18E, and its net profit

to see a 7.0% CAGR over the same period. We expect the improvement in its operating

margin to be driven by the Singapore bus segment, which should benefit from the

implementation of the GCM, as ridership and revenue risks are transferred to the

government.

We forecast CDG’s revenue to record a 3.1% CAGR over 2015-18E, driven mainly by the

18.4% revenue CAGR that we forecast for its rail segment, in which we expect to see

revenue contributions from the opening of its DTL Stages 2 and 3. This is offset by an

expected decline in its Singapore bus revenues, as we anticipate that all 3 tendered GCM

bus packages will go to new entrants.

Key changes to forecasts: We temper our assumptions for CDG’s Singapore bus

segment operating margin to reach 8% by 2017 (from 10% previously) and cut our net

profit forecasts by 2-3% over 2016-18E. Further, we incorporate the potential proceeds

from an asset sale of CDG’s Singapore bus assets of SGD566m into our forecasts and

valuation, given our expectations for the event to occur by 3Q16.

CDG better positioned to

leverage operational

shift from the new GCM

15

Singapore Land Transport Sector: 18 March 2016

CDG: key forecasts

CURRENT 2015 2016E 2017E 2018E 2015-18E CAGR (%)

P&L (SGD m)

Revenue 4,111.5 4,212.1 4,314.6 4,505.6 3.1

% growth YoY

2.4% 2.4% 4.4%

Operating profit 450.7 490.9 544.7 556.9 7.3

Operating profit margin (%) 11.0 11.7 12.6 12.4 1.4 p.p

PBT 452.2 489.8 545.4 561.0 7.5

Net profit (PATMI) 301.9 325.1 359.8 370.1 7.0

% growth YoY

7.7% 10.7% 2.9%

Segmental revenue

Bus 2,119.1 2,133.7 2,169.2 2,248.2 2.0

Bus station 29.0 29.3 29.6 29.9 1.0

Rail 213.4 261.7 285.0 354.3 18.4

Taxi 1,326.8 1,367.0 1,412.8 1,457.3 3.2

Automotive engineering services 238.5 231.3 224.4 217.7 (3.0)

Inspection and testing services 107.5 110.7 114.0 117.5 3.0

Car rental and leasing 38.3 38.7 39.1 39.5 1.0

Driving centre 38.9 39.7 40.5 41.3 2.0

Segmental operating profit

Bus 174.5 205.4 239.3 248.2 12.5

Bus station 12.5 12.6 12.7 12.8 0.9

Rail 3.2 2.6 14.2 17.7 76.9

Taxi 163.9 170.9 176.6 182.2 3.6

Automotive engineering services 41.2 41.6 42.6 37.0 (3.5)

Inspection and testing services 37.7 38.8 39.9 39.4 1.4

Car rental and leasing 9.2 9.9 10.0 10.1 3.0

Driving centre 8.5 9.1 9.3 9.5 3.8

Segmental operating margin (%)

Bus 8.2 9.6 11.0 11.0 2.8 p.p

Bus station 43.1 43.0 43.0 43.0 -0.1 p.p

Rail 1.5 1.0 5.0 5.0 3.5 p.p

Taxi 12.4 12.5 12.5 12.5 0.1 p.p

Automotive engineering services 17.3 18.0 19.0 17.0 -0.3 p.p

Inspection and testing services 35.1 35.0 35.0 33.5 -1.6 p.p

Car rental and leasing 24.0 25.5 25.5 25.5 1.5 p.p

Driving centre 21.9 23.0 23.0 23.0 1.1 p.p

Source: Company, Daiwa forecasts

CDG: changes to our key forecasts

% 2016E 2017E 2018E

Revenue - - -

Operating profit (1.6) (2.6) (2.7)

Operating profit margin (%) -0.2 p.p -0.3 p.p -0.3 p.p

PBT (1.6) (2.6) (2.7)

Net profit (PATMI) (1.6) (2.6) (2.7)

Source: Daiwa forecasts

SMRT

Overall, we forecast SMRT’s net profit (PATMI) to see a 3.9% CAGR over the FY15-18E

period, largely driven by an expected 0.5pp improvement in the operating margin over the

same period for its bus segment following the industry transition to the new GCM in

September 2016. Meanwhile, we forecast continued operating losses for the rail segment

over the FY17-18E period, as we expect the company’s rail network enhancement

initiatives to be a multi-year endeavour.

We forecast a modest overall revenue CAGR of 2.0% over FY15-18E, driven by the

company’s MRT, taxi and rental segments, and tempered by the expected decline in

revenue in the bus segment following the industry’s transition to the new GCM in

September 2016.

Key changes to forecasts: We are lowering FY17-18E EPS by 2-3%, mainly as we

temper our operating margin assumption for SMRT’s bus segment (improvement to 6% by

FY18E vs. 8% previously). Additionally, we reduce our FY17-18E capex forecasts by 12%

taking into account 9M FY16 trends and our expectation for a capex reduction in FY17E

post-GCM (our revised FY17E cash capex forecast: SGD286m).

SMRT’s rail segment

operating performance

remains weak

16

Singapore Land Transport Sector: 18 March 2016

SMRT: key forecasts and assumptions

FY15 FY16E FY17E FY18E FY15-18E CAGR (%)

P&L (SGD m)

Revenue 1,235.5 1,296.7 1,301.0 1,312.4 2.0

% revenue growth YoY

5.0% 0.3% 0.9%

Operating profit 120.8 134.9 128.5 135.1 3.8

Operating profit margin (%) 9.8 10.4 9.9 10.3 0.5 p.p

Net profit (PATMI) 91.0 104.6 97.8 102.2 3.9

EPS (SGD cents) 6.0 6.9 6.4 6.7 3.8

% EPS growth YoY

14.5% -6.5% 4.5%

Segmental revenue

MRT 644.2 670.2 683.6 704.3 3.0

LRT 9.8 10.0 10.0 10.1 1.0

Bus 238.1 250.1 234.2 216.6 (3.1)

Taxi 142.9 150.1 153.1 157.0 3.2

Rental 120.4 134.1 136.3 138.3 4.7

Advertising 36.2 38.0 38.8 39.5 3.0

Engineering services 15.2 13.7 13.0 13.0 (5.1)

Other services 28.7 30.4 31.9 33.5 5.3

Segmental operating profit

MRT 13.4 0.7 (3.4) (3.5) (164.1)

LRT (3.8) (5.5) (5.0) (4.5) 6.2

Bus (6.5) 10.0 8.9 13.0 (225.9)

Taxi 13.7 19.5 15.3 15.7 4.6

Rental 79.6 84.5 84.5 85.8 2.5

Advertising 21.9 23.0 23.5 23.9 3.0

Engineering services (2.4) (0.7) (0.7) (0.7) (33.3)

Other services 2.4 2.5 2.7 2.8 5.3

Investment holding and support services 3.2 3.7 3.4 3.4 2.3

Segmental operating margin (%)

MRT 2.1 0.1 (0.5) (0.5) -2.6 p.p

LRT (38.7) (55.0) (50.0) (45.0) -6.3 p.p

Bus (2.7) 4.0 3.8 6.0 8.7 p.p

Taxi 9.6 13.0 10.0 10.0 0.4 p.p

Rental 66.1 63.0 62.0 62.0 -4.1 p.p

Advertising 60.0 60.0 60.0 60.0 0 p.p

Engineering services (14.4) (5.0) (5.0) (5.0) 9.4 p.p

Other services 8.1 8.1 8.1 8.1 0 p.p

Investment holding and support services 5.6 6.5 6.0 6.0 0.4 p.p

Source: Company, Daiwa forecasts

SMRT: changes to our key forecasts

FY16E FY17E FY18E

P&L (SGD m)

Revenue - - -

Operating profit - (1.7) (3.1)

Operating profit margin (%) 0 p.p -0.2 p.p -0.3 p.p

Net profit (PATMI) - (1.8) (3.4)

Source: Daiwa forecasts

Valuations and ratings

CDG

CDG is trading currently at a 2016E EV/EBITDA of 7.3x, which is more than 1SD above its

past-10-year historical mean of 6.2x. On a PER basis, the stock is trading at 19.7x, about

2SD above its past-10-year historical mean of 14.6x. The last time CDG traded at such

levels was in 2007.

In our view, CDG’s valuations are reasonable, as we believe its business is shifting gears.

Strong potential revenue growth in its rail businesses, a shift toward an asset-light bus-

contracting model in Singapore, and an enhanced balance sheet enabling potential value-

accretive acquisitions overseas all point towards longer-term earnings growth for the

company and a significant improvement in its cash flow, in our opinion.

CDG’s valuations appear

reasonable to us

17

Singapore Land Transport Sector: 18 March 2016

CDG: sensitivity of DCF analysis (2016-25E) CDG: sensitivity of DCF analysis (2016-25E)

WACC

Base

Terminal FCF 5.2% 5.7% 6.2% 6.7% 7.2% 7.7% 8.2% 8.7% 9.2%

0.0% 4.56 4.15 3.81 3.52 3.27 3.06 2.87 2.70 2.55

0.5% 4.90 4.42 4.03 3.70 3.42 3.18 2.97 2.79 2.63

Base 1.0% 5.32 4.75 4.29 3.91 3.59 3.32 3.09 2.89 2.71

1.5% 5.86 5.16 4.60 4.16 3.79 3.49 3.23 3.01 2.81

2.0% 6.56 5.67 4.99 4.46 4.03 3.68 3.39 3.14 2.92

Discount NPV of Enterprise Equity Per Share

Rate FCF Value Value (SGD)

4.7% 3,214.7 12,874.5 12,992.2 6.05

5.2% 3,152.6 11,307.0 11,424.7 5.32

5.7% 3,092.5 10,076.1 10,193.8 4.75

6.2% 3,034.2 9,084.7 9,202.4 4.29

6.7% 2,977.8 8,269.6 8,387.3 3.91

7.2% 2,923.0 7,588.1 7,705.8 3.59

7.7% 2,870.0 7,010.1 7,127.8 3.32

8.2% 2,818.5 6,514.1 6,631.8 3.09

8.7% 2,768.5 6,083.9 6,201.6 2.89

9.2% 2,720.1 5,707.5 5,825.2 2.71

9.7% 2,673.0 5,375.4 5,493.1 2.56

Source: Daiwa estimates Source: Daiwa estimates

CDG: 12-month-forward EV/EBITDA ratio (x) CDG: 12-month-forward PER (x)

Source: Bloomberg, Daiwa forecasts Source: Bloomberg, Daiwa forecasts

SMRT

SMRT is trading currently at a FY17E PER of 24.7x, which is above its past-10-year mean

of 20.6x. Our 12-month target price of SGD1.41 implies a 2017E PER of 21.9x. We believe

valuations are rich given the challenging outlook we see for the company’s key rail

segment.

While the market could possibly be pricing in expectations for a transition of the rail

segment to a new rail model including the acquisition of its operating assets, we believe

negotiations between the government and SMRT will only gain traction once the company

has fulfilled its obligations to return network reliability to satisfactory levels under its

existing licence requirements. In other words, we could be looking at a timeline stretching

beyond 2018.

SMRT: sensitivity of DCF analysis (FY16-25E) SMRT: sensitivity of DCF analysis (FY16-25E)

WACC

Base

Terminal FCF 5.2% 5.7% 6.2% 6.7% 7.2% 7.7% 8.2% 8.7% 9.2%

0.0% 2.02 1.76 1.55 1.37 1.22 1.08 0.97 0.87 0.78

0.5% 2.22 1.92 1.68 1.48 1.30 1.16 1.03 0.92 0.82

Base 1.0% 2.47 2.12 1.83 1.60 1.41 1.24 1.10 0.98 0.87

1.5% 2.79 2.36 2.02 1.75 1.53 1.34 1.18 1.05 0.93

2.0% 3.21 2.67 2.25 1.93 1.67 1.45 1.27 1.12 0.99

Discount NPV of Enterprise Equity Per Share

Rate FCF Value Value (SGD)

4.7% 988.3 5,118.6 4,453.7 2.93 5.2% 959.9 4,430.0 3,765.1 2.47 5.7% 932.6 3,890.4 3,225.6 2.12 6.2% 906.4 3,456.8 2,792.0 1.83 6.7% 881.0 3,101.3 2,436.4 1.60 7.2% 856.6 2,804.8 2,139.9 1.41 7.7% 833.1 2,554.0 1,889.2 1.24 8.2% 810.4 2,339.4 1,674.6 1.10 8.7% 788.5 2,153.9 1,489.1 0.98 9.2% 767.4 1,992.1 1,327.3 0.87 9.7% 747.0 1,849.9 1,185.0 0.78

Source: Daiwa estimates

Source: Daiwa estimates

4

5

6

7

8

9

10

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16+2 stdev

+1 stdev

Mean

12M forward EV/EBITDA (x)

-1 stdev

-2 stdev10

12

14

16

18

20

22

24

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

+2 stdev

+1 stdev

Mean

12M forward PER (x)

-1 stdev

-2 stdev

18

Singapore Land Transport Sector: 18 March 2016

SMRT: 12-month-forward EV/EBITDA ratio (x) SMRT: 12-month-forward PER (x)

Source: Bloomberg, Daiwa forecasts Source: Bloomberg, Daiwa forecasts

Land transport service providers: peer comparison

Bloomberg Share price Market cap PER (x) EV/EBITDA (x) ROE (%) Dividend yield (%)

Company name code (local curr.) (USD m) 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E 2015E 2016E 2017E

Regional peers

17-Mar-16

ComfortDelGro* CD SP 2.97 4,719 21.1 19.7 17.8 9.1 8.7 8.1 13% 14% 14% 3.0% 3.3% 3.7%

SMRT* MRT SP 1.59 1,783 23.1 24.7 23.6 9.2 9.0 8.6 12% 11% 10% 2.4% 2.2% 2.3%

MTR Corp 66 HK 37.95 28,670 24.1 21.6 23.7 14.7 13.4 14.1 6% 7% 6% 6.1% 6.2% 2.9%

Blue Bird BIRD IJ 6,175.00 1,179 18.1 15.4 13.1 8.6 7.5 6.5 23% 23% 23% 2.1% 2.3% 2.8%

Ekspress Transindo Utama TAXI IJ 211.00 35 6.9 4.9 5.0 4.3 4.0 4.3 7% 14% 9% 5.4% 4.4% 4.2%

BTS Group BTS TB 8.60 2,942 40.8 49.7 43.2 44.7 42.0 41.6 4% 5% 5% 7.8% 2.3% 2.2%

Average

22.3 22.7 21.1 15.1 14.1 13.9 11% 12% 11% 4.5% 3.4% 3.0%

Global peers

FirstGroup FGP LN 94.15 1,640 9.8 7.6 6.6 4.6 4.2 4.0 7% 9% 10% 0.6% 2.4% 3.6%

Go-Ahead Group GOG LN 2,641.00 1,642 14.4 12.9 11.6 4.4 3.9 3.7 74% 59% 47% 3.8% 4.2% 4.4%

Average 12.1 10.2 9.1 4.5 4.1 3.9 41% 34% 28% 2.2% 3.3% 4.0%

Source: Bloomberg, *Daiwa forecasts Note: SMRT has a March year-end

We prefer CDG to SMRT

While we expect both operators to be beneficiaries of the new operating landscape for the

transport services sector in Singapore, we recommend that investors switch from SMRT to

CDG, mainly as: 1) CDG is less exposed to Singapore’s regulated fare-pricing environment

(around 24% of revenue vs. 72% for SMRT), 2) CDG is more exposed to the bus

segment, for which we expect a rise in operating margin from a transition to a new asset-

light model, 3) CDG’s stronger balance-sheet position (net cash of SGD229.2m as at end-

2015 vs SMRT’s net debt of SGD665.5m as at end-FY15), 4) we see greater potential

earnings-growth catalysts from overseas acquisitions or expansion, and 5) we think CDG

has greater potential for a higher dividend payout or special dividend in the near term.

Key investment risks

We identify the following key risks to our Positive call on the sector:

Regulatory risks

The public transportation sector is closely regulated by the government. Unfavourable

shifts in the regulatory landscape could result in policies that have an adverse impact on

the businesses of the operators and pose downside risks to our earnings forecasts. This is

the primary risk to our call.

Manpower risks

Staff costs account for around 38% and 41% of CDG and SMRT’s operating expenses,

respectively, representing the biggest cost component to the land transport operators. The

tightening of government restrictions on foreign labour/foreign worker levies in Singapore

or an inability to retain trained and experienced drivers and engineers, could mean that the

operators have to raise wages in order to train or retain skilled staff for their operations,

posing downside risks to our earnings forecasts.

6

7

8

9

10

11

12

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

+2 stdev

+1 stdev

Mean

-1 stdev

-2 stdev

12M forward EV/EBITDA (x)

8

13

18

23

28

33

38

43

Jan-

05

Jul-0

5

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

+2 stdev

+1 stdev

Mean

-1 stdev

-2 stdev

12M forward PER (x)

19

Singapore Land Transport Sector: 18 March 2016

Energy-related costs

Fuel costs (electricity and diesel) represent around 16% and 13% of CDG and SMRT’s

operating expenses, respectively. While operators tend to hedge both their fuel and

electricity requirements, typically on a one-year forward basis, not all their requirements

can be effectively covered. Hence, they remain exposed to price fluctuations in energy

costs and a sharp increase in fuel prices could have a negative impact on our earnings

forecasts.

See important disclosures, including any required research certifications, beginning on page 28

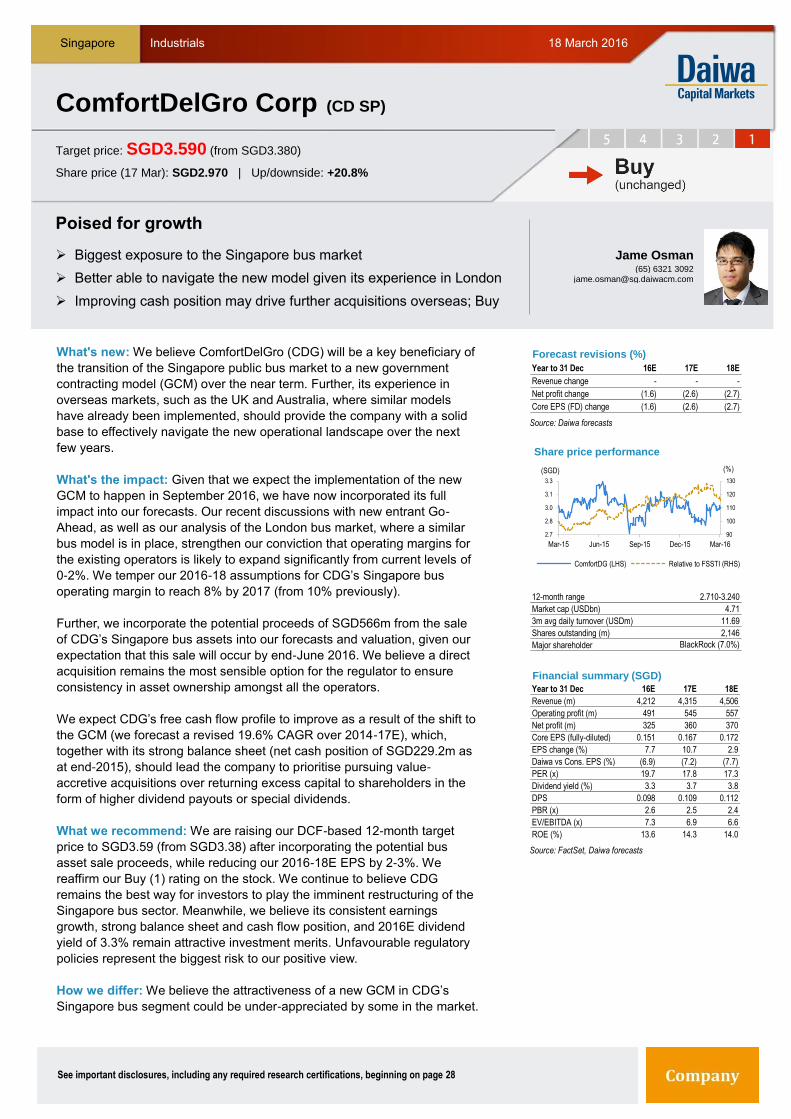

Singapore Industrials

What's new: We believe ComfortDelGro (CDG) will be a key beneficiary of

the transition of the Singapore public bus market to a new government

contracting model (GCM) over the near term. Further, its experience in

overseas markets, such as the UK and Australia, where similar models

have already been implemented, should provide the company with a solid

base to effectively navigate the new operational landscape over the next

few years.

What's the impact: Given that we expect the implementation of the new

GCM to happen in September 2016, we have now incorporated its full

impact into our forecasts. Our recent discussions with new entrant Go-

Ahead, as well as our analysis of the London bus market, where a similar

bus model is in place, strengthen our conviction that operating margins for

the existing operators is likely to expand significantly from current levels of

0-2%. We temper our 2016-18 assumptions for CDG’s Singapore bus

operating margin to reach 8% by 2017 (from 10% previously).

Further, we incorporate the potential proceeds of SGD566m from the sale

of CDG’s Singapore bus assets into our forecasts and valuation, given our

expectation that this sale will occur by end-June 2016. We believe a direct

acquisition remains the most sensible option for the regulator to ensure

consistency in asset ownership amongst all the operators.

We expect CDG’s free cash flow profile to improve as a result of the shift to

the GCM (we forecast a revised 19.6% CAGR over 2014-17E), which,

together with its strong balance sheet (net cash position of SGD229.2m as

at end-2015), should lead the company to prioritise pursuing value-

accretive acquisitions over returning excess capital to shareholders in the

form of higher dividend payouts or special dividends.

What we recommend: We are raising our DCF-based 12-month target

price to SGD3.59 (from SGD3.38) after incorporating the potential bus

asset sale proceeds, while reducing our 2016-18E EPS by 2-3%. We

reaffirm our Buy (1) rating on the stock. We continue to believe CDG

remains the best way for investors to play the imminent restructuring of the

Singapore bus sector. Meanwhile, we believe its consistent earnings

growth, strong balance sheet and cash flow position, and 2016E dividend

yield of 3.3% remain attractive investment merits. Unfavourable regulatory

policies represent the biggest risk to our positive view.

How we differ: We believe the attractiveness of a new GCM in CDG’s

Singapore bus segment could be under-appreciated by some in the market.

18 March 2016

ComfortDel Gro C orp

Poised for growth

Biggest exposure to the Singapore bus market

Better able to navigate the new model given its experience in London

Improving cash position may drive further acquisitions overseas; Buy

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

ComfortDelGro Corp (CD SP)

Target price: SGD3.590 (from SGD3.380)

Share price (17 Mar): SGD2.970 | Up/downside: +20.8%

Jame Osman(65) 6321 3092

Forecast revisions (%)

Year to 31 Dec 16E 17E 18E

Revenue change - - -

Net profit change (1.6) (2.6) (2.7)

Core EPS (FD) change (1.6) (2.6) (2.7)

90

100

110

120

130

2.7

2.8

3.0

3.1

3.3

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Share price performance

ComfortDG (LHS) Relative to FSSTI (RHS)

(SGD) (%)

12-month range 2.710-3.240

Market cap (USDbn) 4.71

3m avg daily turnover (USDm) 11.69

Shares outstanding (m) 2,146

Major shareholder BlackRock (7.0%)

Financial summary (SGD)

Year to 31 Dec 16E 17E 18E

Revenue (m) 4,212 4,315 4,506

Operating profit (m) 491 545 557

Net profit (m) 325 360 370

Core EPS (fully-diluted) 0.151 0.167 0.172

EPS change (%) 7.7 10.7 2.9

Daiwa vs Cons. EPS (%) (6.9) (7.2) (7.7)

PER (x) 19.7 17.8 17.3

Dividend yield (%) 3.3 3.7 3.8

DPS 0.098 0.109 0.112

PBR (x) 2.6 2.5 2.4

EV/EBITDA (x) 7.3 6.9 6.6

ROE (%) 13.6 14.3 14.0

21

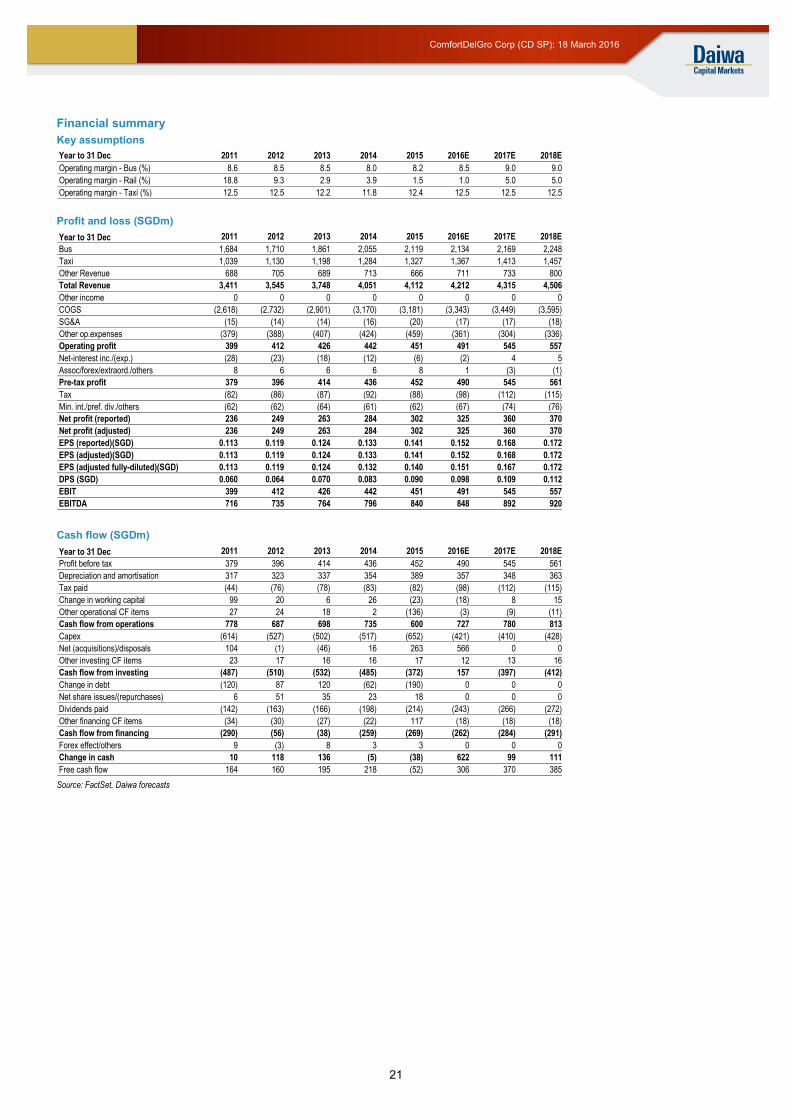

ComfortDelGro Corp (CD SP): 18 March 2016

Financial summary

Key assumptions

Profit and loss (SGDm)

Cash flow (SGDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Operating margin - Bus (%) 8.6 8.5 8.5 8.0 8.2 8.5 9.0 9.0

Operating margin - Rail (%) 18.8 9.3 2.9 3.9 1.5 1.0 5.0 5.0

Operating margin - Taxi (%) 12.5 12.5 12.2 11.8 12.4 12.5 12.5 12.5

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Bus 1,684 1,710 1,861 2,055 2,119 2,134 2,169 2,248

Taxi 1,039 1,130 1,198 1,284 1,327 1,367 1,413 1,457

Other Revenue 688 705 689 713 666 711 733 800

Total Revenue 3,411 3,545 3,748 4,051 4,112 4,212 4,315 4,506

Other income 0 0 0 0 0 0 0 0

COGS (2,618) (2,732) (2,901) (3,170) (3,181) (3,343) (3,449) (3,595)

SG&A (15) (14) (14) (16) (20) (17) (17) (18)

Other op.expenses (379) (388) (407) (424) (459) (361) (304) (336)

Operating profit 399 412 426 442 451 491 545 557

Net-interest inc./(exp.) (28) (23) (18) (12) (6) (2) 4 5

Assoc/forex/extraord./others 8 6 6 6 8 1 (3) (1)

Pre-tax profit 379 396 414 436 452 490 545 561

Tax (82) (86) (87) (92) (88) (98) (112) (115)

Min. int./pref. div./others (62) (62) (64) (61) (62) (67) (74) (76)

Net profit (reported) 236 249 263 284 302 325 360 370

Net profit (adjusted) 236 249 263 284 302 325 360 370

EPS (reported)(SGD) 0.113 0.119 0.124 0.133 0.141 0.152 0.168 0.172

EPS (adjusted)(SGD) 0.113 0.119 0.124 0.133 0.141 0.152 0.168 0.172

EPS (adjusted fully-diluted)(SGD) 0.113 0.119 0.124 0.132 0.140 0.151 0.167 0.172

DPS (SGD) 0.060 0.064 0.070 0.083 0.090 0.098 0.109 0.112

EBIT 399 412 426 442 451 491 545 557

EBITDA 716 735 764 796 840 848 892 920

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Profit before tax 379 396 414 436 452 490 545 561

Depreciation and amortisation 317 323 337 354 389 357 348 363

Tax paid (44) (76) (78) (83) (82) (98) (112) (115)

Change in working capital 99 20 6 26 (23) (18) 8 15

Other operational CF items 27 24 18 2 (136) (3) (9) (11)

Cash flow from operations 778 687 698 735 600 727 780 813

Capex (614) (527) (502) (517) (652) (421) (410) (428)

Net (acquisitions)/disposals 104 (1) (46) 16 263 566 0 0

Other investing CF items 23 17 16 16 17 12 13 16

Cash flow from investing (487) (510) (532) (485) (372) 157 (397) (412)

Change in debt (120) 87 120 (62) (190) 0 0 0

Net share issues/(repurchases) 6 51 35 23 18 0 0 0

Dividends paid (142) (163) (166) (198) (214) (243) (266) (272)

Other financing CF items (34) (30) (27) (22) 117 (18) (18) (18)

Cash flow from financing (290) (56) (38) (259) (269) (262) (284) (291)

Forex effect/others 9 (3) 8 3 3 0 0 0

Change in cash 10 118 136 (5) (38) 622 99 111

Free cash flow 164 160 195 218 (52) 306 370 385

22

ComfortDelGro Corp (CD SP): 18 March 2016

Financial summary continued …

Balance sheet (SGDm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

As at 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Cash & short-term investment 577 695 836 826 788 1,415 1,523 1,641

Inventory 57 58 71 72 75 75 77 80

Accounts receivable 133 129 111 117 139 122 125 130

Other current assets 213 213 222 224 278 246 211 220

Total current assets 979 1,094 1,240 1,239 1,280 1,857 1,936 2,072

Fixed assets 2,604 2,707 2,777 2,895 2,909 2,382 2,511 2,636

Goodwill & intangibles 553 569 687 686 673 664 658 652

Other non-current assets 453 476 381 411 355 355 355 355

Total assets 4,589 4,846 5,085 5,231 5,216 5,258 5,459 5,714

Short-term debt 198 96 218 243 126 126 126 126

Accounts payable 621 634 665 837 844 737 755 788

Other current liabilities 182 187 179 178 166 166 181 230

Total current liabilities 1,002 917 1,063 1,258 1,137 1,030 1,063 1,144

Long-term debt 434 608 590 494 432 432 432 432

Other non-current liabilities 680 684 638 640 635 635 635 635

Total liabilities 2,115 2,209 2,290 2,392 2,204 2,097 2,129 2,211

Share capital 569 585 623 646 666 666 666 666

Reserves/R.E./others 1,323 1,423 1,532 1,544 1,670 1,783 1,909 2,039

Shareholders' equity 1,892 2,008 2,155 2,190 2,335 2,449 2,575 2,704

Minority interests 582 629 640 649 678 712 754 798

Total equity & liabilities 4,589 4,846 5,085 5,231 5,216 5,258 5,459 5,714

EV 7,005 7,005 6,979 6,925 6,811 6,219 6,153 6,079

Net debt/(cash) 55 9 (28) (89) (229) (856) (964) (1,082)

BVPS (SGD) 0.905 0.955 1.014 1.024 1.086 1.141 1.200 1.260

Year to 31 Dec 2011 2012 2013 2014 2015 2016E 2017E 2018E

Sales (YoY) 6.4 3.9 5.7 8.1 1.5 2.4 2.4 4.4

EBITDA (YoY) 5.4 2.7 3.9 4.2 5.6 1.0 5.2 3.1

Operating profit (YoY) 2.8 3.3 3.4 3.7 1.9 8.9 11.0 2.2

Net profit (YoY) 3.1 5.6 5.7 7.7 6.5 7.7 10.7 2.9

Core EPS (fully-diluted) (YoY) 3.0 5.3 4.4 6.9 5.9 7.7 10.7 2.9

Gross-profit margin 23.2 22.9 22.6 21.8 22.6 20.6 20.1 20.2

EBITDA margin 21.0 20.7 20.4 19.6 20.4 20.1 20.7 20.4

Operating-profit margin 11.7 11.6 11.4 10.9 11.0 11.7 12.6 12.4

Net profit margin 6.9 7.0 7.0 7.0 7.3 7.7 8.3 8.2

ROAE 12.8 12.8 12.6 13.1 13.3 13.6 14.3 14.0

ROAA 5.3 5.3 5.3 5.5 5.8 6.2 6.7 6.6

ROCE 13.0 12.8 12.3 12.3 12.6 13.5 14.3 14.0

ROIC 12.5 12.5 12.4 12.6 13.1 15.4 18.5 18.5

Net debt to equity 2.9 0.4 n.a. n.a. n.a. n.a. n.a. n.a.

Effective tax rate 21.5 21.6 21.0 21.2 19.5 20.0 20.5 20.5

Accounts receivable (days) 12.7 13.5 11.7 10.3 11.4 11.3 10.4 10.3

Current ratio (x) 1.0 1.2 1.2 1.0 1.1 1.8 1.8 1.8

Net interest cover (x) 14.5 18.2 23.9 37.8 72.0 260.2 n.a. n.a.

Net dividend payout 53.2 53.8 56.3 62.1 64.0 65.0 65.0 65.0

Free cash flow yield 2.6 2.5 3.1 3.4 n.a. 4.8 5.8 6.0

Company profile

ComfortDelGro is a multi-modal land transport services provider, operating a fleet of over 46,000

vehicles across several countries, including Singapore, UK, Australia and China. The company was

formed following the merger of Comfort Group and DelGro Corporation in 2003.

See important disclosures, including any required research certifications, beginning on page 28

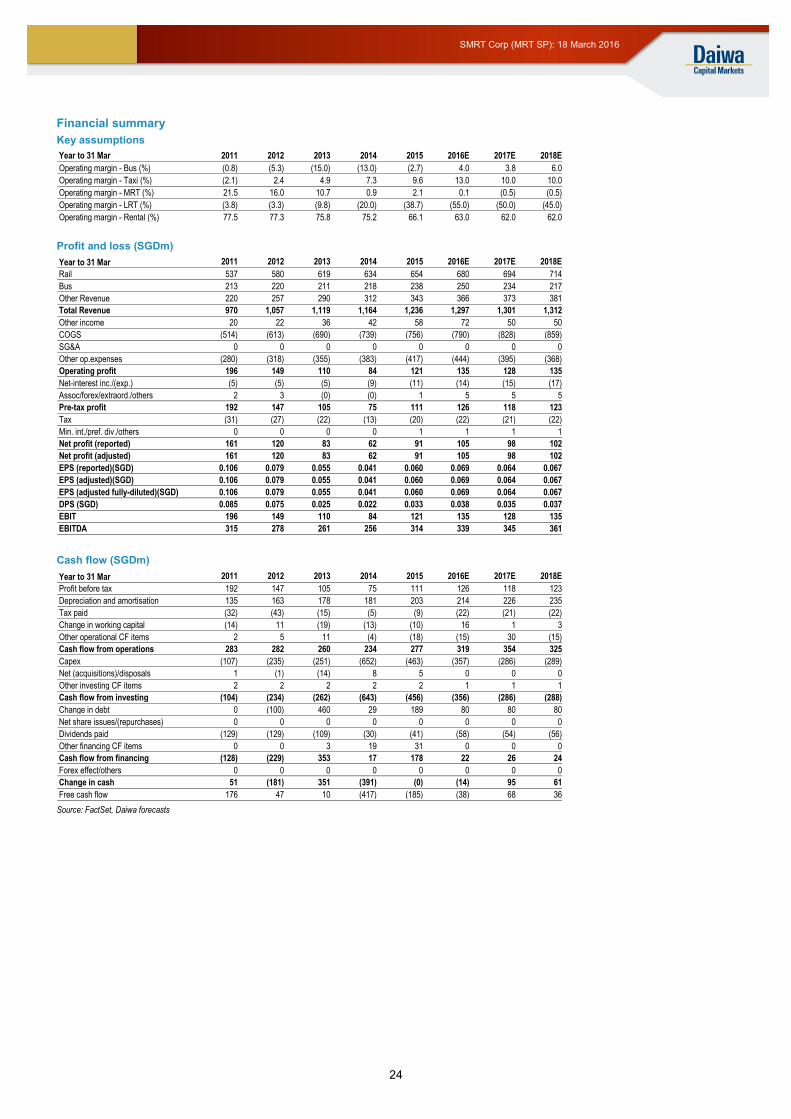

Singapore Industrials

What's new: In our view, SMRT’s recent share-price strength (up 18%

since its low in January 2016) more than adequately reflects the positives

from: 1) its better-than-expected 3Q FY16 results, 2) the transition to the

new bus government contracting model (GCM), and 3) the potential sale of

its rail operating assets. Meanwhile, we remain cautious, mainly as we see

several near-term risk factors weighing on its business.

What's the impact: While we expect SMRT to benefit from the transition of

its bus operations to the new GCM, its exposure to the segment is smaller

than ComfortDelGro’s (CDG) (19% of Singapore-derived revenue vs. 32%

for CDG). Our previous forecasts already factor in the positives we see

from the new bus model. We are lowering our FY17-18E EPS by 2-3%,

mainly after tempering our operating margin assumptions for SMRT’s bus

segment (to an improvement to 6% by FY18E from 8% previously).

Additionally, we reduce our FY17-18E capex by 12% taking into account

9M FY16 trends and our expectation for a capex reduction in FY17E post-

GCM (our revised FY17E cash capex forecast: SGD286m).

Further, although we believe rail reforms would almost certainly be positive

for SMRT’s operations, the timing, magnitude and terms of such a deal

remain unclear to us. In the near term, we expect the focus to remain on

ensuring SMRT fulfils its obligations to return rail network reliability to

satisfactory levels under its existing licence requirements. We remain

cautious on its operating prospects, due chiefly to: 1) its elevated rail

maintenance costs, which management still expects to increase to close to

50% of rail-segment revenue by 4Q FY16 (3Q FY16: 43%), 2) the opening

of Downtown Line 2 (DTL2) (operated by SBS Transit) in December 2015,

which we had previously highlighted could result in a shift of ridership

market share away from SMRT’s North-South East-West lines, and 3) the

impact of a 1.9% cut in fares in December 2015.

What we recommend: We raise our DCF-based 12-month TP to SGD1.41

(from SGD1.34) due mainly to our revised capex forecasts. We reaffirm our

Underperform (4) rating on the stock, as we think near-term visibility on

SMRT’s rail segment operating performance remains poor, while we expect

its FY16E free cash flow to remain in negative territory amid elevated

gearing levels (3Q FY16: net debt position of SGD683m vs. FY12: net cash

of SGD45m). The main upside risk: a near-term announcement on positive

rail reforms.

How we differ: Our FY17-18 EPS forecasts are 1-14% below consensus,

possibly as we believe the market could be expecting a sharper turnaround

in SMRT’s rail segment.

18 March 2016

SMRT C orp

Positives look priced in, but risks remain

Smaller exposure to the Singapore bus segment than ComfortDelGro

Outlook for key rail segment remains uncertain

Reaffirm Underperform (4) rating; raising target price to SGD1.41

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

SMRT Corp (MRT SP)

Target price: SGD1.410 (from SGD1.340)

Share price (17 Mar): SGD1.585 | Up/downside: -11.0%

Jame Osman(65) 6321 3092

Forecast revisions (%)

Year to 31 Mar 16E 17E 18E

Revenue change - - -

Net profit change - (1.8) (3.4)

Core EPS (FD) change - (1.8) (3.4)

80

94

108

121

135

1.1

1.3

1.4

1.6

1.7

Mar-15 Jun-15 Sep-15 Dec-15 Mar-16

Share price performance

SMRT (LHS) Relative to FSSTI (RHS)

(SGD) (%)

12-month range 1.140-1.685

Market cap (USDbn) 1.78

3m avg daily turnover (USDm) 3.22

Shares outstanding (m) 1,522

Major shareholder Temasek Holdings (54.2%)

Financial summary (SGD)

Year to 31 Mar 16E 17E 18E

Revenue (m) 1,297 1,301 1,312

Operating profit (m) 135 128 135

Net profit (m) 105 98 102

Core EPS (fully-diluted) 0.069 0.064 0.067

EPS change (%) 14.9 (6.5) 4.5

Daiwa vs Cons. EPS (%) 5.5 (1.3) (14.1)

PER (x) 23.1 24.7 23.7

Dividend yield (%) 2.4 2.2 2.3

DPS 0.038 0.035 0.037

PBR (x) 2.7 2.5 2.4