DPC – Arts Victoria Performing Arts

Audiences

Prepared for:Department of Premier and Cabinet - Arts Victoria

October 2013

Contents

Section PageBackground, objectives and methodology 3

Executive summary and recommendations 10

Detailed findings 13

AustraliaSCAN| The broader social context 13

How often are people attending a performing arts event? 18

How has their attendance changed over time? 30

Which factors impact upon decision to attend a performing art event? 42

What are the motivations and barriers to taking out a subscription? 52

Appendix 60

Additional charts 60

Sample profile 68

Discussion guides (Qual phase) 71

Questionnaire (Quant phase) 79

Page 2

Background, objectivesand methodology

Page 4

Background | The need for research

Feedback from the performing arts sector shows that ticket sales have been in decline since November 2012. Arts Victoria need to better understand what is behind this trend,

the expected lifecycle of it, and what may ultimately slow or even reverse the decline.

Furthermore, an increase in large/high profile events is impacting on broader demand for performing arts in Melbourne. Ticket sales indicate that some shows sell out quickly with limited promotions, while others do not. There is a need to better understand why,

and what is the broader impact of this trend.

How has consumer confidence and attitudes toward the sector impacted upon ticket sales?What is the optimal approach to address this trend for declining ticket sales?

Page 5

Objectives

The primary objective of the research was to better understand what’s driving the trend in ticket sales and attendances across a range of performing arts events. Specifically, the research looked to:

Quantify changes to ticketrevenues since November 2012.

Quantify attitudes towardsconsumer priorities around discretionary spending and how they spend their leisure time.

Understand awareness of artsand culture offerings in general.

Understand what the shiftsare for consumer preferences when it comes to paid leisure activities.

Understand the preferencesfor performing arts events among regular and occasional ticket buyers. Determine the mix on offer – is there an oversupply in product, or an undersupply of preferred events?

Quantify price sensitivitywithin the sector.

Phas

e Ph

ase

Page 6

Research approach

Qualitative phase (in-depth interviews)

n=8

n=8 in-depth interviews with a range of performing arts stakeholders (all senior management level from a range of performing arts organisations and

also venues).Conducted during May 2013 in Melbourne.

Methodology

Qualitative phase (in-depth interviews)

n=14

n=7

in-depth interviews with

n=7

in-depth interviews with

Quantitative phase (Online

survey) n=1583

Online survey (15 minutes) with both occasional attendees (1-2 performances in the last 12 months) and regular attendees (3-4+

performances within the last 12 months).In field from 2nd August to September 24th 2013.

Respondents incentivised with a prize draw.Sample provided by key stakeholders (both venues and also performing

arts organisations).

Regular attendees (n= 1324)(3-4 attendances or more in the past 12 months)

More likely to...•Live in Melbourne•Be 55-64 years old•Be single with no children (left at home)•Work full time•Earn $150,000 per year or more

How the two audiences were recruited and defined

The research defined the two audiences by the number of performing arts events that they had attended within the last 12 months.

The sample was drawn from databases held by key stakeholders within the performing arts sector in Victoria (including venues). Thesurvey was also sent out through the ACMI and Museums Victoria newsletter (via a link) to try and gain a sample of non-attendees.However, the response rate was very low, with only n=25 respondents completing the survey. As such, the base size is too low to

chart any of the results and have therefore been omitted from this report.

The key demographics differences between the two samples are highlighted below.

Fewer financial pressures Greater financial pressures

Page 7

Occ

asional attendees (n=234)(1-2 attendances or more in the past 12 months)

More likely to...•Live in regional Victoria

•Be 25-44 years old

•Have a family with kids

Page 8

A note on reading the report

• The slides all show whether the information is qualitative or quantitative in nature.

• This is denoted using labels on each slide.

• Data has not been shown where the sample size is less than n=25

• Because the sample was derived from lists provided by performing arts organisations, it is skewed towards those who have attended a performing arts event more recently.

• While every effort was made to reach non-attendees by placing survey links in the newsletters of Museum Victoria and also ACMI, this only garnered n=25 respondents (too low a base size to chart on). As such no data has been shown for this audience within the report.

Key takeouts

Overall there seem to be some key factors at play which have impacted upon attendance of performing arts in Victoria:

1. Regular attendees are going to fewer performing arts events than they were five years ago—mainly due to a lackof appealing performances.

2. Those who are occasional attendees were more likely to be feeling pressure both financially, and also when it comes to their time—making it harder to justify spending money on performing arts events.

3. There is also a feeling that there are a larger number of performing arts events to select from in Melbourne—which is spreading the attendee base more thinly.

4. Occasional attendees feel less passionate about the performing arts compared to regular attendees, they are also less knowledgeable—this means that performing arts are less of a priority to this audience. The implication

of this is that attending performing arts events are a nice to have, rather than an essential—which when combined with greater time and monetary pressures makes it harder for them to justify the cost of attending.

5. Regular attendees are more likely to be older and more affluent. This makes it easier for them to attend more performing arts events as they have both more time and money. However, there is a need to ‘future proof’ the industry to ensure that the next generation of regular attendees is brought on board rather than relying on one

that is ageing.

Page 9

Page 10

Executive summary|OverallWhat do they

attend?How passionate

are they?Are performing arts important to them?

How has their attendance changed

over time?

Key reasons for increase or decline in attendance

SWOT

Regular Attendees

Plays, classical music, musicals, opera and ballet were their most

appealing performing arts and were most

popular to attend.

This audience claimed to be passionate about classical music, plays

and ballet in particular, and also felt more

knowledgeable about performing arts overall

compared to the occasional attendees.

The performing arts were

extremely or very important to 78% of this audience.Attending gives

them pleasure—and there was also a desire to support

the industry.

Claimed attendance has remained

relatively stable with the only real

changes in attendance for local bands and singers and major music artists declining over the last five

years.

For those who claimed that their attendance had declined it was

due primarily to a lack of appealing

performances.

This cohort are the ones with more time, money

and who claimed to place more importance on

performing arts. However, they were more likely to

be critical of the programming, and if it

doesn’t hit the mark will result in them dropping their subscription—a key

revenue stream for organisations.

Occasional Attendees

Classical music, musicals, plays,

opera were most appealing to this audience and also most attended—but

much less frequently than

the regular attendees.

Their level of passion for classical music, plays and the ballet was at lower levels compared to regular attendees. However, this cohort felt more

passionate about musicals—and their

passion for the opera was comparable to

that felt among regular attendees.

While attending live performances

was seen as important to this

group it is at much lower levels (39% extremely or very

important). It gives them pleasure but

this can be outweighed by the cost of attending— other activities start

to vie for their money.

Like regular attendees, claimed attendance of local bands and major

music artists looks to have suffered

over time. Encouragingly, there are indications that for some occasional attendees they have been to the opera more frequently compared to five

years ago.

Where it has increased—it was due to having more time and more

well-known productions coming to

Melbourne. The declines in attendance

were largely due to less disposable income

and time (more so than for regular

attendees).

This audience felt less knowledgeable or

passionate about the performing arts. As such there is a greater risk in attending an event— particularly given that

money is more of an issue for them. As such there is a need to make this audience

feel more comfortable in their ticket purchases—so

help them better justify the expense.

While what is appealing in a performing art event is to an extent a personal decision, it would appear that over the past 12 months in particular for the regular attendees this has been a huge issue. For four in ten (40%) regular attendees who claimed their attendance levels had declined, lack of appealing programming was the reason attributed.

Page 11

Overall, any declines in ticket sales for the performing arts look to be largely down to three key factors:too much choice, cost/time pressures, and issues with programming.

Implications for Arts Victoria

1. Too much choice. 2. Time and money pressures. 3. Programming choices.

• Over the past five years there has been an acknowledgement among both consumers and stakeholders that the choice of performing arts events in Melbourne has increased.

• Essentially organisations are now being forced to compete for the same attendees (time and money) and there is only so much that people can justify spending on performing arts.

• In conjunction with more events to choose from, time and money have become critical factors in being able to attend performing arts events.

• While these pressures are felt more keenly among the occasional attendees, they are still felt by regular attendees. However the latter audience’s passion for, and importance of, performing arts means they were better able to justify money being spent on attending events.

In order to drive take up of performing arts and increase ticket sales there are some key issues to be addressed.

Page 12

Recommendations

1. Make the industry feel more

accessible.

• For those who don’t attend performing arts events particularly regularly there is a sense that the industry is somewhat elitist.

• This can act as a barrier for people for whom attending performing arts events isn’t a regular thing.• Events where these occasional attendees have some form of familiarity with the event (music, storyline, performer etc.)

can make it feel more accessible and also makes it more enjoyable when they do attend.• Once people have been to a performance there is more likelihood of them returning because it has been somewhat

de- mystified for them.

2. Make it easierfor people to justify

the expense.

• Those people who attend less regularly are under greater time and monetary pressure.• Therefore the ticket offering needs to feel like it is great value so that they can better justify the expense.• While we recognise the need for stakeholder organisations to meet revenue targets there is also an opportunity to drive

attendance through availability of better value ticketing—if these tickets are available as early bird specials (or something akin to this) it will also help organisations address the trend of tickets being closer to the date of attendance.

• Risk minimisation also comes through the choice of programming, with some element of familiarity with the performance making the less frequent attendees more comfortable with purchasing a ticket.

AustraliaSCAN |The broader context

Due to all of these pressures, life feels complicated and difficult (more so now then compared with the past). There is a sense of disempowerment whereby Australians feel less able to have an impact on their own lives and the lives of others.

Page 14

AustraliaSCAN

Time poor – life is full of commitments and there is the sense that there is not enough time in the day to fit it all in.Choice overwhelmed – with all of the seemingly endless choices available, Australians are feeling fatigued when it comes to making decisions.

Out of control – with so much going on in Australians’ daily lives, there is a sense of unpredictability and uncontrollability.Imbalanced – juggling work, home and life commitments is proving difficult and achieving a balance is appearing harder than it used to be.

Key social tensions

• From AustraliaSCAN, we know that Australians are increasingly feeling:

AustraliaSCANFinancial unrest above all

• Out of all of the daily pressures, Australians are feeling the financial strain more so than anything else and they believe this will worsen with time.

% Total Australians (2013 ‘areas feeling more stress than a year ago’) 1. Money concerns (41%)

2. Planning for the future (30%)

82% of Australians believe the ‘cost of

living’ will worsen with time.

3. Personal health (29%)

4. Work/job (28%)

5. Personal life (28%)

6. Children (25%)

7. Managing your time (20%)

8. Job security (19%)

9. Rent/mortgage (18%)

10. Household tasks (16%)

Page 15

AustraliaSCAN

$$$

Giving up luxuriesActively looking for

discounts

Page 16

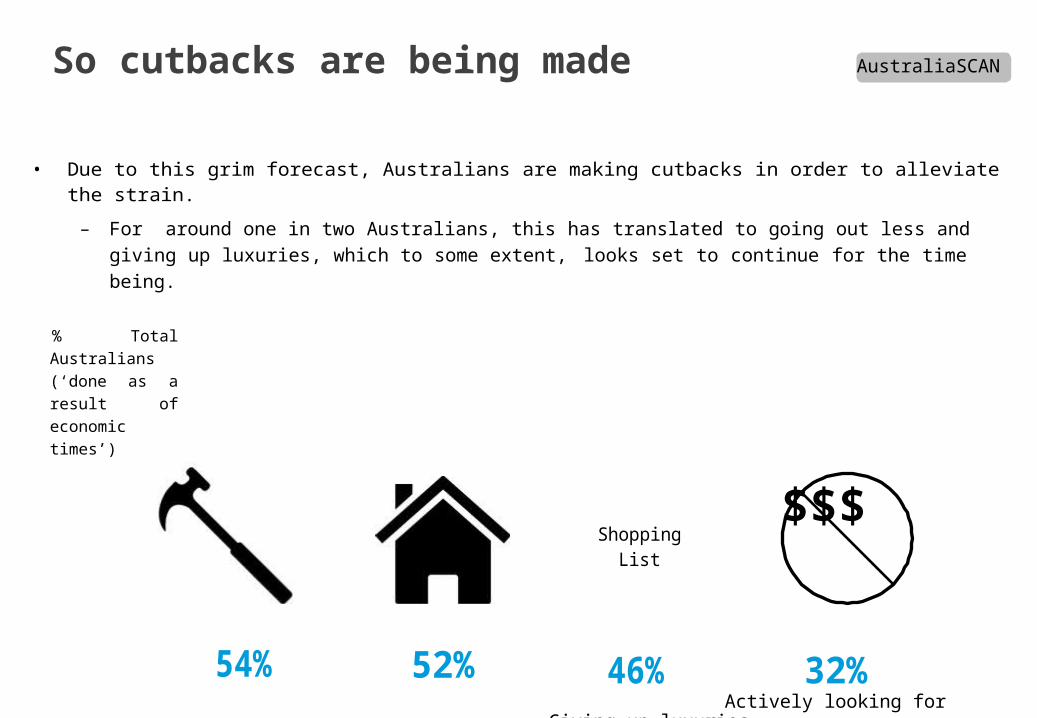

So cutbacks are being made

• Due to this grim forecast, Australians are making cutbacks in order to alleviate the strain.

– For around one in two Australians, this has translated to going out less and giving up luxuries, which to some extent, looks set to continue for the time being.

% Total Australians (‘done as a result of economic times’)

54% 52% 46% 32%

Shopping List

$ ------

DIY rather than paying someone else

Going out less

AustraliaSCANWhat this means for Arts Victoria

Australians are increasingly faced with more pressures than ever.Experiencing a combination of time and choice constraints, there is a general

feeling of ‘uncontrollability’ when it comes to their lives.

Out of all of the stressors experienced, financial hardships are perceived to be the biggest and as a consequence, Australians are making cutbacks in

order to alleviate this.

Such cutbacks include giving up luxuries and limiting their ‘nights out’ – expenses seen to be frivolous and lacking value. This strongly underpins the

broader consumer trend of looking for better ‘value for money’ whether it be purchases or experiential in nature.

What this means for Arts Victoria is that consumers are more selective about their purchase choices (when it comes to buying tickets to

performing arts events) and as such, there is an increasing need to present and communicate a compelling value/quality (in terms of experiential)

proposition to its consumers.

Page 17

How often are peopleattending a

performing arts event?

“I’ve moved around quite a bit. Since I came back to Melbourne I’veappreciated how wonderful the performing arts are here.” Occasional, male, younger

Best in Australia: Melbournians unanimously perceive that their performing arts scene is the bestavailable in Australia.They are proud of their city’s reputation for culture.Regular scheduling of international performances from Russia, China and Europe make Melbourne a world-class destination.

Page 19

Qualitative

Diverse:Something for everyone - an excellent range of performances encompassing all tastes.

Accessible:Well located, good ticket availability, plenty of information available about upcoming performances.

Frequent:Events are scheduled every day.

There’s enough going on to meet demand, no matter your preferences.

Social:Makes a good night out with friends/ family. Can be tied in with drinks or dining out before/after.

Generally affordable:Range of price points to suit different budgets. Relatively expensive compared to other discretionary spending, but acceptable value.

Broadly there’s a very positive perception of Melbourne’sperforming arts scene

Quantitative

Theatre, classical music, musicals and opera are the mostpopular of the performing arts—across both groups

In the last 12 months which of the following types of performances have you attended?

Plays/theatre (not musicals)Regulars are, by their very definition, more likely to have attended more performing

Circus

Family/children's shows

Contemporary dance

80

Cabaret7060

50

40

30

20

10

0

Classical music performance (includes instrumental, choral, chamber music, etc)

Musical theatre (musicals)

Opera/operetta

Major music artists

arts events than the occasional attendees. However, both groups seemed to favour

the more ‘traditional’ performing arts compared to the more contemporary

performing arts such as jazz, cabaret or contemporary dance.

There appear to be some key gender differences by attendance with men

significantly more likely to have attended the opera (53% vs. 45% women ),

classical music performances (65% vs. 53% women),

jazz (26% vs. 18 % women).

Jazz music performance

Stand up comedy

Ballet

Local bands/singers

However, women were significantly more likely to have attended musicals (53% vs. 46% men), the ballet (36% vs. 28% men)and family/children’s shows (18% vs. 9%).

Occasional(n=234) Regular(n=1324)

Q.3NB. Only figures 3% and above shown.

Page 20

Quantitative

Level of appeal (Extremely Appealing and Very Appealing nett score)

Page 21

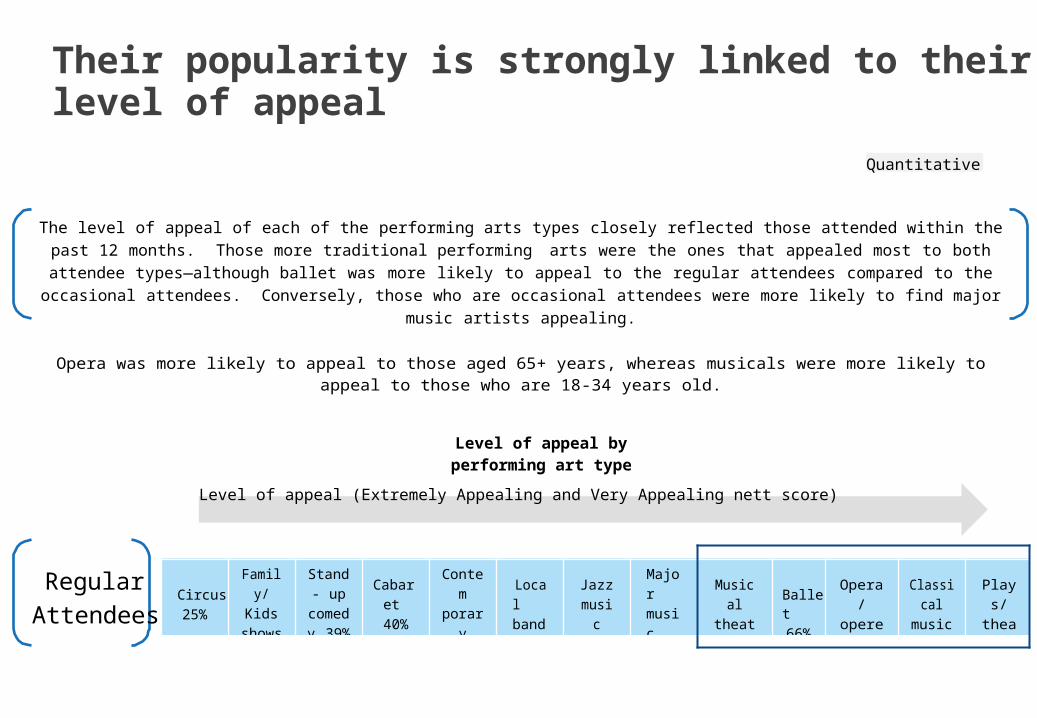

Their popularity is strongly linked to their level of appeal

The level of appeal of each of the performing arts types closely reflected those attended within the past 12 months. Those more traditional performing arts were the ones that appealed most to both attendee types—although ballet was more likely to appeal to the regular attendees compared to the

occasional attendees. Conversely, those who are occasional attendees were more likely to find major music artists appealing.

Opera was more likely to appeal to those aged 65+ years, whereas musicals were more likely to appeal to those who are 18-34 years old.

Level of appeal by performing art type

Regular Attendees

Occasional Attendees

Q.19

Circus25%

Family/ Kids

shows 33%

Stand- up

comedy 39%

Cabaret 40%

Contem porary dance 49%

Local bands 50%

Jazz music 55%

Major music artists 59%

Musical theatre 59%

Ballet66%

Opera/ operetta

67%

Classical music 75%

Plays/ theatre 77%

Cabaret 22%

Circus 27%

Family/ Kids

shows 39%

Local bands 40%

Stand- up

comedy 43%

Contem porary dance 58%

Jazz music 59%

Ballet 59%

Major music artists 61%

Opera/ operetta

64%

Plays/ theatre 68%

Musical theatre 68%

Classical music 72%

QualitativeThis appeal is due to a variety of reasons

• Performing arts are appealing to people because of the experience that they provide. There is a strong sense that they allow attendees to escape their lives for a couple of hours and be transported elsewhere—either through music or through a performance. For some, this experience needs to challenge them, but for others it is simply about it providing a form of escapism.

REASONS PERFORMING ARTS ARE

• The lack of appeal for the performing arts is due to a range of reasons—and is also quite personal in nature (for example someone may love attending classical music concerts but not the opera). However, across the board, cost is a key reason for lack of appeal—particularly if the individual lacks knowledge about the performance as this means that the price can’t then be justified due to the perceived risk involved.

REASONS PERFORMING ARTS CAN BE

“I love going. I love the experience and the

escapism of it all.”Regular, female, older

APPEALING

EscapismSpellbinding

Great night out

Great with family

Cost

Elitist

UNAPPEALING

No one wants to go with you

“I was really surprised by the number of songs I knew—I was pleasantly

surprised. I would

Experience of seeingPerformance is too

‘out there’For older people definitely consider going

to more things now, Igreat performers Lack of familiarity guess it seems a bit less

Educational

Treat

Fulfillingwith

performance

Too ‘highbrow’

‘underground’ and maybe something I would do

again.”Occasional, male,

younger

Page 22

Quantitative

Unsurprisingly the more appealing events are attendedwith greater regularity

Frequency attended type of performance in the last 12 months

Regular Attendees

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Plays/theatre

Classical music performance

Local bands/singers

Opera/operetta

38%

35%

46%

65%

21%

23%

11%

18%

31%

21%

29%

24%

12%

8%

10%

6%

Among the regular attendees the more popular performing arts were plays,

classical music—but also local bands and singers.

Stand-up comedy

Ballet 54%

73%

22%

15% 7% 5%

20% 4%

Those who are older (aged 55 years ormore) were significantly more likely to have attended the theatre seven or more

timesMajor music artists 63% 27% 6%

3%in a year—the same was also true for those

Jazz music performance

Musical theatre

Contemporary dance

63%

72%

73%

25%

21%

22%

9% 3%

4% 2%

3% 2%

who attended classical music performances six to seven times in the

last 12 months. These are likely to be the subscribers (those aged 65+ years are

significantly more likelyCircus

Family/childrens shows

Cabaret70%

81%

97%

27%

16%

21%1%%

3% 1%

2%1%

to have taken out a subscription during 2013)—which explains the higher number

of performances attended.

1-2 times 3-4 times 5-6 times 7 or more times

Q.5

Page 23

Quantitative

“If they halved their prices they would double their audiences.” Occasional, male, older90% 100%

But despite their appeal, the ‘occasionals’ are less likely toattend

Frequency attended type of performance in the last 12 months

Occasional Attendees

0% 10% 20% 30% 0%40% 105%0% 206%0%

307%0%

4800%%

5900%% 16000%%

70% 80%

Stand-up comedy 73% 15% 7% 5%Stand-up comedy 90% 10% Occasional attendees, by their very definition,

Opera/operetta 21% 8% 6%have attended fewer performing arts events.

Opera/operetta Musical theatre 92% 72% 8% 21% 4% 2%

Plays/theatre 21% 11% 29% The two performing arts event types they wereMusical theaCtrleassical music performance

Jazz music performance

86% 35% 23% 14% 18%

25%

24%more likely to attend with greater frequency were classical music and also ballet. Men were sig9n%ific3a%ntly more likely to attend classical music

Plays/theatre

Classical music performance

Local bands/singers

Major music artists69%

84% 46%

63%31%

16% 31%

27%

12% p1e0%rformances (39%), whereas women were mo6%re l3ik%ely to attend ballet

performances morefrequently (3-4 times a year 27%).

Major music artists

Cabaret

Circus 85%97%

15%

16% 2% 1%

T21h%%e1s%e lower attendance rates are likely

Ballet

Ballet

Contemporary dance 77% 73% 23%

22% 20%unde4r%pinned by the financial pressures (largely22% due t3o% l2if%e stage) felt by this cohort—

rather than less of a desire to attend.

Family/childrens shows

1-2 times 3-4 times 5-6 times 7 or more times1-2 times 3-4 times 5-6 times 7 or more

t 27%

3% 1%

Q.5NB. Only those arts with a sample size of n=30 or more shown. Page 24

Regular attendees go to a range events with a variety ofpeople—or even by themselves

Stand-up comedy

0.3

Regular AttendeesQuantitative

0.2

Cabaret

Major music artists

0.1Circus Child(ren)

Friend(s)Jazz music performance

Contemporary dance Local bands/singers

PartnerFamily / childrens shows

0-0.4 -0.2 0 0.2 0.4 0.6 0.8 1 1.2

Plays/theatre

Classical music performance-0.1

Other family member

No one- I go by myself

Opera/operetta

-0.2

Ballet

Musical theatre

-0.3

-0.4

None of theseNot surprisingly, children’s shows were more likely to be attended with children. Regular

attendees were more likely to go and see the less traditional performing arts with their partner and

friends.

-0.5

Parent(s)

-0.6 Q.23

Page 26

Dimension 1 (horizon

comDim

ensio

n 2

Quantitative

Whereas, for the occasional attendees attending a performingarts event is more of a social occasion with a variety of family or friends

Occasional Attendees0.6

No one- I go by myself

0.4

Local bands/singers

Friend(s) 0.2Jazz music performance

Contemporary dance

Major music artists

None of theseCircus

Child(ren)Family / childrens shows

0-0.6 -0.4 -0.2 0 0.2 0.4 0.6 0.8 1 1.2

CabaretStand-up Plays/theatre

Partner

Ballet

Other family member

Classical music performance

Opera/operetta

-0.2

-0.4

Musical theatre

Parent(s)

For occasional attendees, who they go to performing arts with seems to be more varied compared to regular

attendees.Musicals and ballet seem to be more of a family affair,

whereas plays and stand up comedy were more likely to be attended with their partner. Not surprisingly, those events that are more relaxed or social in nature (local bands, jazz,

major music artists) were more likely to be attended by groups of friends than other performance styles.

-0.6

tal)

Q.23

Page 27

Qualitative

PARENTS

For parents there is a range of rolesin attending performing arts events. For younger families they may take kids to see musicals, or performances aimed specifically at children. For the older children (in their thirties) they may ‘treat’ their adult kids to a performance as part of a celebration of some sort (birthday or Christmas for example).

For some of the older parents, they have maintained their subscription and take their adult children with them.

SIBLINGS

Attending an event with siblingsseems to be more likely in the domain of subscribers. Qualitatively there is a sense that parents who are older (65+ years) continue to hold subscriptions which they then choose to take their children too.

“ Mum’s getting on a bit now, so I guess it’s us that physically take her to the ballet. But we have our little routine, a casserole at my sister’s and then go to the ballet.It’s really nice.”

Regular, female, older

FRIENDS

Friends can play a myriad of roles.They can be the ones who make the attendee aware of the event in the first place—i.e. the instigator of attending, or else the performance can form part of a night out.

“I hear about stuff that’s on through my friends, and just agree to go with them. I’ve been to enough with them now that I trust their judgement and I know I’ll like what they choose.”Regular Male, younger

Qualitatively, we know different people offer differentexperiences when attending a performing art event

Sense that this is more popular for those who hold subscriptions—there is almost a

ritual around attending the ballet, or opera with each other.

Friends and partners tend to make attending a performing art event more

of a social outing.

Page 28

By referral from a major showor other performing art:

Spare time / spare cash:“I went to see Mary Poppins a few

years back. There were a bunch of leaflets at the venue about smaller theatre performances which I bought tickets for, plus now I get emails inviting me to other things.” Occasional, male, older“Maybe I’m just growing up abit. When I was a student we just went out drinking. Now I’m older I’m on the lookout for other things I can do socially. Plus, I can afford more tickets now.”

Regular, male, younger

Page 29

Qualitative

As a child:

“My grandmother started by taking me to musicals. As I got older, she began taking me to more sophisticated things – she loves the ballet.” Regular, female, older

Through a new friend / partner:

“My partner has a thing for orchestra; he plays violin. At first I was reluctant because I’m more into *pop / rock+ bands. But when someone shares their passion with you, then you can start to feel enthusiastic about it too!”Occasional, female, older

Friends, partners and family can also play a key role inintroducing people into the performing arts

How has theirattendance changed

over time?

Quantitative

Level of passion (Extremely Passionate and Very Passionate nett score)

Not surprisingly, the regular attendees are more passionateabout performing arts compared to the occasionals

Not surprisingly, those who are regular attendees held stronger levels of passion for their top five performing arts types. This strength of passion is likely underpinning their greater prevalence for attending more performing arts events, and more frequently. In particular the regular attendees were more likely to feel passionate about classical music, theatre and also ballet compared to the occasional attendees.

However, the occasional attendees were more likely to feel passionate about musicals compared to the regular attendees. Qualitatively, this passion amongst the regulars seems to come through their upbringing—i.e. they have been exposed to a love of performing arts through

their parents, or at school. This makes the performing arts more important and intrinsic to their life—and this passion helps them to justify the money spent attending events.

Level of passion by performing art type

Regular Attendees

Occasional Attendees

Q.20

Cabaret 16%

Stand- up

comedy 14%

Circus 13%

Family/ Kids

shows 20%

Local bands 35%

Major music artists 39%

Jazz music 38%

Contem porary dance 36%

Musical theatre 37%

Opera/ operetta

43%

Ballet 51%

Plays/ theatre 54%

Classical music 59%

Cabaret 9%

Stand- up

comedy 12%

Circus 13%

Family/ Kids

shows 23%

Local bands 30%

Major music artists 36%

Jazz music 37%

Contem porary dance 40%

Musical theatre 41%

Opera/ operetta

41%

Ballet 43%

Plays/ theatre 44%

Classical music 50%

Performing arts attendees also commonly participate in otherMelbourne events.They consider performing arts to be a significant part of a broader spectrum of events which make Melbourne vibrant.

However, these other events do not detract from their attendance at performing arts.The majority attend performing arts at threshold – i.e. they attend as many as they want to or aren’t willing to attend more.–This may be due to budget constraints or event enthusiasm.Other events are part of a wider mix of demands on their resources and are considered no more competition than other hobbies / interests.

Page 32

“Yes, I buy AFL tickets and they are expensive. But I spend money on a lot of other things too, like holidays and DVDs. You could say everything is a balance.Going to other events doesn’t affect how often I go to performing arts.” Occasional, male, younger

Qualitative

“Performing arts are so important—they help Melbourne feel alive.” Regular, female, younger

This level of passion means that, for performing arts attendees, otherevents in Melbourne are not seen to be ‘competitors’

Quantitative

Level of knowledge (Extremely Knowledgeable and Very Knowledgeable nett score)

Page 33

This passion is also strongly linked to their broaderknowledge of the performing arts

Like passion, those who are regular attendees were also more likely to claim they felt knowledgeable about performing arts. In particular they were more likely to feel more knowledgeable about classical music, theatre and also ballet. However, claimed knowledge levels were quite low

among both audiences, suggesting that their passion is not necessarily driven by their knowledge of the performing art—bur rather an appreciation for it.

Level of knowledge about each performing art type

Regular Attendees

Occasional Attendees

Q.21

Circus 9%

Cabaret 11%

Stand- up

comedy 13%

Family/ Kids

shows 19%

Local bands 20%

Contem porary dance 21%

Jazz music 22%

Opera/ operetta

30%

Musical theatre 33%

Major music artists 34%

Ballet 36%

Plays/ theatre 37%

Classical music 41%

Cabaret 4%

Circus 7%

Stand- up

comedy 11%

Local bands 11%

Jazz music 13%

Family/ Kids

shows 18%

Major music artists 19%

Plays/ theatre 20%

Opera/ operetta

22%

Ballet 24%

Contemp orary dance 24%

Classical music 28%

Musical theatre 29%

Quantitative

Extremely important 34%

Very important 44%

Somewhat important 21%Not important

1%

I enjoy it/gives me pleasure (41%)

I want to support it/I appreciate it (18%)

Nothing compares to live performances (16%)

This combined knowledge and passion ladders up to a stronger level ofimportance for the performing arts among those who attend regularly

Not surprisingly, those who felt more passionate about the performing arts (the regular attendees) were more likely to claim that attending performing arts is important to them. The key motivating factor for this importance was the pleasure they get from it, coupled with a desire to support the performing arts. Pleasure also motivates the occasional attendees, but for this audience there are other things that they enjoy

doing as well—price comes into play for this audience too.

How important is attending live performances to you?

Regular AttendeesOccasional Attendees

Cost is an issue(25%)

Page 34

Q.12 Q.13

“I can remember my parents taking me to a classical music performance by the MSO (I think) up in Wangaratta when we were kids. It was such a treat for us, we grew up listening to classical music in the house, but to hear it live, wow that was just amazing. It’s an experience that has stayed with me.”Regular, male, olderQualitative

Again, this importance is likely informed by their exposureto performing arts over time

Greater importance seems to be placed on the performing arts if there is more of an attachment to it through personal connection—for example playing an

instrument, having dance lessons as a child, or participating in amateur dramatics. This type of

involvement seems to lead to greater importance being attached to a specific type of performing art, and then exposing children (and grandchildren) to this passion

too.

For those who are less passionate about performing arts, there seems to be more of an air of mystery

about it. There is not necessarily a clear understanding of what it can offer because there is a lack of familiarity with it. This, in combination with

the cost of tickets can provide a huge barrier to attendance. This is where there’s a clear opportunity

for performing arts organisations to provide more accessible events (such as MSO performances in the park) to engage with these audiences. If an event is free (or low cost) then it provides less of a risk for those who are not as au fait with performing arts.

“Performing arts aren’t really a priority in my life, so cost is a bit of an issue. I

need a really good understanding of what I am getting—surety in the product if

you like—before I will commit to seeing something. I rely on close friends

involved in the arts scene to lead the way on what we do, and don’t, go to see.

The free MSO concert in the park was great—there were loads of well known songs, the atmosphere was great, and it was free. Now I’ve been to something like that I would consider going to more performances because I have a better

idea of what they’ll be like.”Occasional, male, younger

Page 35

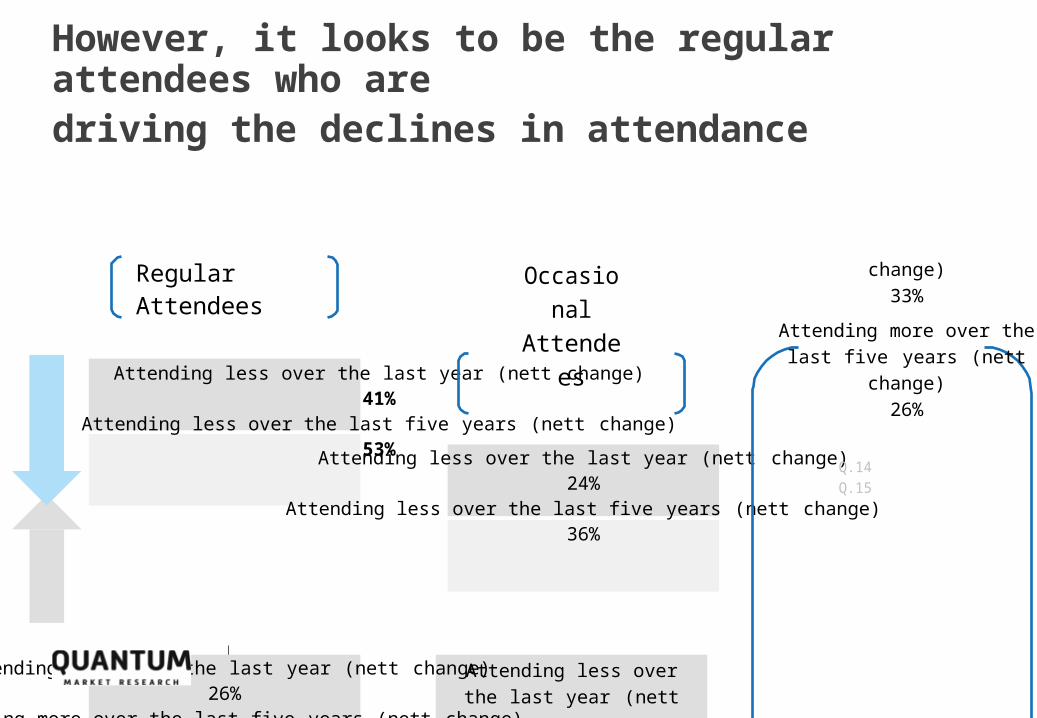

Attending less over the last year (nett change)41%

Attending less over the last five years (nett change)53%

Attending less over the last year (nett change)24%

Attending less over the last five years (nett change)36%

Attending more over the last year (nett change)26%

Attending more over the last five years (nett change)35%

However, it looks to be the regular attendees who aredriving the declines in attendance

Regular Attendees Occasional Attendees

Attending less over the last year (nett change)

33%

Attending more over the last five years (nett change)

26%

Q.14 Q.15

The trend in ticket sales looks to be driven by the regular attendees rather than occasionals. This

decline has been most marked over the past five years—with more than one in two (53%) regular attendees who claimed that their attendance

had declined over this period compared to just one in three

ocassionals (36%).

The primary reason that was cited for their declining attendance was

due to the programming, with fewer performances that appealed

to them. When this factor is combined with greater pressure on finances, there is less of an ability for this audience to be

able to continue their subscription, opting instead to attend performances that held

more appeal.

Page 36

Stakeholder organisations and venues also commented on how late ticket sales have become. Instead of customers purchasing closer to the release date, they are now waiting to see if discounted tickets become available, or making the decision to attend much closer to their attendance.

Page 37

Qualitative

PRICE—DISCOUNTTICKETS

Amongst venues there is a clear sense that customers know that if they wait long enough they will get a discount on their tickets— that they have in fact become ‘trained to do so’.

“Really the practice of discounting tickets last minute has shot the industry in the foot. People know that if they wait long enough they are likely to get a great deal.” Melbourne Venue

VARIETY OF CHOICE

Another stakeholder alsocommented that there is more choice so “the customer can afford to be pickier about what they decide to go and see.” The competitive nature of the market is seen to necessitate working harder to sell the tickets. This is seen to be making for a tougher business environment in general for the industry.

“There’s too much choice in Melbourne, you could go to something every day if you wanted to!” Regular, female, older

APPEAL OF THE PROGRAM

For the production companies there is a strong feeling that the program each season needs to balance out the need to keep current attendees happy, but also attract new audiences. This is particularly true for those organisations for whom subscription sales represent their “bread and butter”.

“We have to balance out keeping our subscribers happy but also attracting new audiences. So we need a few blockbusters in there as the key to subscriptions and also broader sales.”

Qualitatively there are four key factors behind attendancerates declining

From a consumer perspective, there iscertainly a desire to attend more performing arts events but cost is a key barrier.

For those customers who have families, in particular, there are seen to be greater financial pressures on their income and so attending a performing art event (particularly with the whole family) is an expensive undertaking. But conversely for those who are older, the reverse is also true:“Over the last few years money has ceased to be the issue it was, so I go to more events now than I used to. The kids are all out of school, I’m semi-retired so we have more time and money on our hands.” Male, 56 years old

But programming is key—over the past twelve monthsthere have been fewer performances that appeal to bothaudience types

Quantitative

Which of the following reasons best describe why you haven’t been to a performance in the last 12 months?

Regular (%)

Occasional (%)

There have been fewer performances that appeal to me 40 32I have less disposable income available to me now 15 32Doesn't interest me/didn't enjoy it/prefer other things 12 5

I don't have enough time any more 11 11

I don't have anyone to go with/I can no longer go with the person/people I used to attend with 10 10

Too busy/other commitments/family/travel 3 6

Q.18 ANB: responses over 5% shown

Page 38

33

25

1813

16

36

4623

12

Quantitative

The same is true over the past five years

Why has your attendance increased or decreased (over the past five years)?

For both regulars and occasionals, time is a key reason for their

overall attendance increasing. For regulars, the role of direct mail

cannot be underestimated in raising awareness of what’s on.

For regulars, there is also a stronger sense that there’s more to choose from (potentially from becoming more aware through

direct mail rather than an programming).

However, for the regulars the key reason for their claimed decrease in attendance has been due to the

programming. This was particularly true for musicals (49%).

For the occasionals, their declining attendance is largely due to

pressures on their time and also money.

Q.16

IncreasedRegular

%Occasional

%I have more time now 29I have more disposable income available to me 25 23I am on a mail/email list that informs me of what is on 17I have found family/friends who will go with me 24 23There's more to choose from 11I have taken out a subscription 5There are more well known productions coming to Melbourne 12One of my friends/family introduced me and I enjoyed it 12 14

DecreasedRegular Occasional

% %There have been fewer performances that appeal to me 27I have less disposable income available to me now 32I don't have enough time any more 18I don't have anyone to go with/I can no longer go with theperson/people I used to attend with 13 14I decided not to renew a subscription I had 7 6Health problems / declining health 5

NB: responses over 5% shown

Page 39

Which factors impactupon decision to

attend a performing art event?

Qualitatively, the decision making process looks like this...“There are so many ads around for performances. I see things ion the paper, on TV, even outside the arts

centre.” Regular, male, older

• Through word of mouth/recommendations.

Appeal• Can I attend on the dates

available?

Qualitative

• Newspaper (ads and reviews).• Direct mail (from venues and

production companies).• Newspaper reviews (mainly

in The Age).

Become aware ofthe production

•How appealing is the production?• Is it something I’ve seen before?• Who’s performing in it?• Is the music or topic something

that I will like?• Is it traditional? Modern? Will

I like the production?

• How much are the tickets? Can I get good seats for a good price?

• Will anyone want to go with me? Will they be free at the same time as me?

Logistics

“The international productions definitely have more appeal for me. When I grew up in Brisbane there wasn’t a lot of top theatre available there—it was more amateur stuff.

It makes me appreciate the quality of productions that come to Melbourne.”

Regular, female, older

Page 41

On at a time that is convenient for me 74 74Can get great seats 67 65

6767

616565

68

56

69

Quantitative

For both regulars andoccasionals, the availability of good seats, and times that suit were both key factors in making a performance appealing.

For the regular attendees the performance was made more appealing if there was familiarity with some element of the performance, or it is being performed by someone well- known.

For the occasional attendees, a performance was made more appealing if there were discounted tickets available— and it was being held in an accessible venue (probably due to the fact this audience were more likely to live outside of Melbourne).

Page 42

Quantitatively, timing of the performances and availabilityof great seats is key to appeal of a performance

Makes the performance more appealing to meRegular

%Occasional

%

Being performed by a well-known international company/performer 67 61Familiarity with the author/playwright/composer/choreographer 55The performance makes me think 51It’s a performance that’s uplifting 66 68Can get discounted tickets 65Other people I might go with want to see it too 63 64It’s something I've not seen before 54Familiarity with the music 60Storyline is appealing 59Has good reviews 59 59Accessibility of the venue 59Familiarity with the lead performers 58 53Recommended by family/friends 56 58Being performed by a well known Australian company/performer 44

Q.22

Quantitative

Page 43

Very few factors make a performance less appealing

Factors that made very little difference in the level of appeal were those such as familiarity with the producer, whether it’s

a one-performer show, or it coincided with a special

occasion such as an anniversary or birthday. Although the latter is not important for occasional attendees, it was more likely to be of some importance due to

the financial pressures this group are under—i.e. attending is more likely to be perceived

as a ‘treat’.

Q.22

Makes the performance less appealing to me Regular%

Occasional%

It’s a children’s event 29 22It’s something I have seen before 22 25It’s a one-performer show 14 22

Makes no difference to me Regular%

Occasional%

It’s a one-performer show 71 61Familiarity with the producer 70 71Coincides with a special occasion 62 53Familiarity with the storyline 58 53Something I have seen before 56 53

Quantitative

How important is it to be familiar with some element of the performance you are going to see?

Level of importance (Extremely Important and Very Important nett score)

Familiarity with some element of the performance varies byperformance type—for music based events it’s fairly important

For both regular and occasional attendees being familiar with major music artists was deemed to be important if they were going to see them. For other performing art types there was not really a great deal of importance attached to being familiar with some element of the

performance they were going to see. Interestingly, the regular attendees are the audience who were more likely to place some importance on being more familiar with classical music and ballet they were going to see, compared to the occasional attendees.

Regular Attendees

Occasional Attendees

Q.25

Circus 18%

Cabaret 22%

Family/ Kids

shows 28%

Plays/ Theatre

29%

Contem porary dance 30%

Jazz music 30%

Stand- up

comedy 35%

Musical theatre 36%

Opera/ operetta

38%

Ballet 39%

Local bands 41%

Classical music 42%

Major music artists 67%

Circus 8%

Cabaret 15%

Contem porary dance 20%

Family/ Kids

shows 26%

Jazz music 26%

Plays/ Theatre

29%

Ballet 29%

Musical theatre 32%

Classical music 36%

Opera/ operetta

38%

Stand- up

comedy 38%

Local bands 40%

Major music artists 69%

Quantitative

Page 45

Familiarity for occasional attendees is more likely to beimportant than it is for the regular attendees

Which one aspect of a performing arts event production is most important for you to be familiar with?

Regular(n=919)

%

Occasional(n=161)

%The music 27 37The storyline 17 22The performance company 17 12The composer 14 12The performer(s) 14 10The author/playwright 6 3

Q.26 A

However, for those occasional attendees who do need some level of familiarity with the performance, it was about the music or the

storyline. For the regular attendees they were more likely to attach importance to the actual

performers themselves.

For men there was more likely to be greater importance attached to knowing the

composer (20% vs. 11% women), whereas for women the storyline was more

important (21% vs. 11% men)—the same was true for those aged 35-44 years old

(30% vs. 15% 55+ years).

The implication for this is that the occasional attendees will look to minimise the risk of

spending money on attending a performing arts event by going to see something they

have some level of familiarity with.

Page 46

Attendees also look to the communication materials toconvey a sense of what the performance entails Qualitative

For both regular and occasional attendees the communication material for the performing art event is critical because it provides potential attendees with an idea of whether or not it’s something they are

interested in attending.

1. What kind of genre is it?

The images used convey whether it looks

uplifting, depressing, challenging or

humorous.

2. What does the productionvalue look like?

The images can also convey whether the production

looks like it is high value, whether it’s a large cast, one

man show etc.

3. Is there some element I am familiar with?

The communication material also provides the opportunity to establish whether or not there is any familiarity with the music, the author, the performers, the storyline etc.

For occasionals this is critical as familiarity helps to minimise the sense of risk in

For subscribers the brochures produced by each of the organisations are critical in helping them decide whether or not the program is sufficiently appealing for them to renew their subscription.

Quantitative

For the majority of attendees price is part of the decision,but other considerations do exist

How important is price to you in determining whether you go or not? Price was critical for one in

five (21%) occasional attendees, while for those who

attend

RegularAttendees

OccasionalAttendees

more regularly it held lesser importance. Given they are more likely to have a lower levels of engagement and lower household income compared to their regular attendee counterparts this

price sensitivity is predictable.

Interestingly, women were more likely to claim that the price is critical (15% vs. men

9%), while men were significantly more likely to

claim that price is only of minor importance (22% vs. 11%

women). The same was also true of those aged over 55 years (16% vs. 7% 18-34 year olds).

Q.37

The price is critical 11 21

The price is important but other considerations also come into play

68 65

The price is only of minor importance

15 11

The price is irrelevant 5 3

Page 47

Quantitative

Occasional attendees more likely to be sensitive to the costof living

What’s causing you stress in your everyday life?

Regular Attendees

3. Increasing pressure on my time (30%)

4. General cost of living

(29%)

Occasional Attendees

Cost of living was more likely to be a stressor for occasional

attendees, therefore their sensitivity to price is of no real

surprise. But for this group, there is also a feeling that their time is under greater pressure.

When these two factors are combined they present

considerable barriers to attending performing arts events with any degree of

regularity.

Regular attendees felt a greater sense of concern

about what’s happening in a broader social context rather than the more inward focus seen amongst the occasional

attendees.

Q.9a Q.11

Page 48

1. Health of self or family(41%)

2. General cost of living (39%)

3. What’s going on in the world these days

4. Increasing pressure onmy time (32%)

5. My children’s future(20%)

5. My children’s future(24%)

1. What’s going on in the world these days

2. Health of self or family (34%)

Quantitative

However, both attendee types claimed they’re willing to paymore for high calibre performances, or better seats

Can you indicate whether you would be prepared to pay a bit more or would expect to pay less?Total Sample (no significant differences between the two audiences)

Both audiences would be prepared to

pay more for premium seating, but then there is a

steep drop off to the next ‘tier’ of things

they would pay more for.

Attending a production or event at

a venue in the suburbs is expected to

cost less, and to an extent so is a

weeknight performance.

Q.38 NB: top five responses

Pay

Pay

Premium seating (i.e. best seats in the house) 70%

An international performer/performance company 55%

Well-known/high profile performer(s) 55%

Well-known/high profile conductor 47%

An opening night / premiere 35%

A venue in the suburbs 63%

A weeknight performance 51%

A venue that holds a large audience 25%

A one-man/woman show 25%

A production that is designed for families 18%

shown

Page 49

What are the motivations and

barriers to taking out a subscription?

Quantitative

Unsurprisingly, regular attendees are more likely to hold asubscription

Regular attendees were more likely to have held a subscription compared to occasional attendees. For the regular attendees theatre, classical music, ballet and opera were the subscriptions most likely to be held this year. However, the opera has seen the biggest decline in subscriptions this year (-

14%)—likely due to the programming of the Ring Cycle this season. Subscriptions across 2012 look to be relatively low compared to 2013 amongst the regular attendees. For the occasional attendees there looks to be less of a discrepancy between subscriptions last year (2012) and this year—however there has been a noticeable decline from pre –2012; potentially due to the age group of this audience (younger—so either moved from youth/student

concessions or now have families so greater time or monetary pressures).0% Reg10u%lar a2t0t%end3e0e%s

40% 50% 60% 70% 80% 90% 100% Occasional attendees

Plays/theatre Plays3/0th%eatre

15% 30% 38% 15% 42%38%

Classical music peCrlfaosrsmicaanlcme usic per2fo6%rmance

12% 26%29%

12% 512%9%

Ballet20% B

all9e

%t

242%0% 9% 2640%%

Opera/operetta 16% 9% 30%Opera/operetta 16% 9% 30% 57%

Musical theatre 6% 3% 8% 87%Musical theatre

6%3% 8% 87%

Contemporary dance 1%4%

94%

Contemporary dance 1%4%

94%

Plays/theatre

Classical music performance

1% 1% 26% 72%

Musical theatre 0% 1% 1% 98%

Page 51

Jazz music performance 3% 96%Jazz music performance

3%

96%

Subscribed this year (2013) Subscribed last year (2012) Subscribed this year (2013) Subscribed last year (2012)

Subscribed in previous years (prior to 2012) Never subscribedSubscribed in previous years (prior to 2012) Never subscribed

Q.27

Plays/theatre

Classical music performance

1% 1% 26% 72%

Musical theatre 0% 1% 1% 98%

Page 52

As one subscriber put it...

Qualitative

“Being a subscriber is a no brainer for me. It’s important that the arts are supported, but it’s more than that. They provide such great value for money, you book them, forget about them but then you have all

these events throughout the year and you get to look forward to. They’re like a grown up version of a show bag.”

Regular, female, younger

Quantitative

Page 53

But the rational reasons for a subscription are largely focused aroundthe ability to plan in advance, secure seats and save money

For those who chose to take a subscription out this year the ability to plan, saving money

and guaranteeing the ability to see performances they wanted

to were the key motivating factors for doing so.

For those who took out a subscription for musicals this

year it was felt to be particularly good value (67%), whereas for

those who hold a theatre subscription the key benefit was seen to be their ability to plan in advance (75%) as well as good

value (60%).

Q.28

Why did you choose to take out a subscription this year? (n=1089)

It allows me to plan my opera/operetta performances in advance 69%

It works out cheaper than buying individual tickets 56%

It allows me to ensure I get tickets to the performances I want to see 55%

It guarantees that I can get seating in the area that I prefer 49%

It represents good value for money 49%

It is a way of supporting this art form 44%

It means I don't have to worry about buying tickets later in the year 44%

It is a way of supporting a particular production company 37%

The productions offered were really appealing 37%

It is something I have always done 33%

So I can sit with family/friends who also take out subscriptions 27%

A subscription provides me with additional benefits that single ticket buyers don't get 11%

Might not be able to afford it (11%)

Q.29Q.30

Page 54

Quantitative

Despite a strong level of confidence amongst current subscribers that they will renew their subscription, there was a strong sense that it will to an extent depend on the program being offered (in particular for the occasionals). For some there is also a concern that they can’t commit to the dates in advance (more likely to be regulars). Amongst the occasionals there was also a concern that they may not be able to afford it next year.(NB: due to low base size for the occasionals within this sample no figures are given above).

“I sit down and work out which plays appeal, and then fit the subscriptions around that.”Regular, female, older

“It’s a lovely treat, a bit indulgent really, I’d like to have it next year but it depends how appealing the program

Depends on the program being offered (33%)Why/why not

is really.”Regular, female,

younger

Definitely will61%

Probably will 30%

May or may not 8%

The majority of current subscribers claimed they’re likelyto renew their subscription next year

Likelihood of taking out a subscription next year

All current subscribers

n=1089

Enjoy the experience (22%)

Happy to commit to dates each year (13%)

Can’t

commit/prefer to buy tickets as needed

Despite the perceptionof value that the subscriptions offer, the key barrier to renewing a subscription was a lack of ability to justify the expense. Not surprisingly, cost was a bigger barrier to the occasional attendees (42% vs. 22% regular).

Whereas for regulars they were more likely to claim that they didn’t find this year’s productions appealing (16% vs. 8% occasional), or that the people they normally went with stopped subscribing (12% vs. 8% occasional).

Page 55

Quantitative

The key reason underpinning their lapse in subscriptioncomes down to the expense of it

Why did you stop subscribing?All lapsed

subscribers (n=1336)

%

I couldn't afford a subscription/can't justify the expense 24

I preferred not to commit to specific performance dates too early 20

I no longer had the time to go to so many performances 20

I decided to spend the price of a subscription on other activities instead 17

I didn't want to go to the specific performances offered in the subscription series 16

I didn't find this year's productions appealing 16

I didn't want to spend all my money on only one production company/venue 13

I wasn't available to attend performances at the dates/times they were scheduled 12

The price of a subscription went up too much 12

The people I usually go with stopped subscribing 11

I preferred not to commit to specific performances until I had a chance to read the reviews / find out what other people thought of each performance 11

Quantitative

“I looked at renewing my ballet subscription but the dates were just all wrong so I left it—I thought I can always buy them later if things change.” Regular, female, older

Why/why notCan’t commit/prefer to buy tickets as needed (31%)

Definitely will 2%

Probably will 6%

May or may not 29%

Probably will not41%

Definitely will not21%

However, for those whose subscription has lapsed, it’sunlikely to be renewed

Likelihood of taking out a subscription next year

All lapsed subscribers

n=1331

Q.32 Q.33NB: responses over 10% shown Page 56

For those who were lapsed subscribers there was a strong sense that they probably won’t renew it in

the future, preferring instead to buy their tickets as needed. The cost was also a key barrier for this

cohort—in particular the occasional attendees (23% vs. 15% regulars). However, for the regular

attendees their renewal was more likely to depend on the program being offered (21% vs. 12%

occasionals), for this audience there was also a desire for greater variety (8% vs. 3% occasionals).

Depends on the program being offered (20%)

The cost/it’s getting way too expensive (16%)

Not interested in this form of art/like to spend freetime on other activities (15%)

Will purchase a ticket for a particular event (13%)

Might not be able to afford it (11%)

Quantitative

With those who have not subscribed yet, also unlikely todo so in the future

Likelihood of taking out a subscription next year

All non-subscribers n=2688

May or may not 12%

Probably will not 41%

Definitely will not 41%

Q.34All non-subscribers (n=2688)

Why have you never subscribed?

I want to pick and choose what I go to, not be forced to attend whichever performances are part of the subscription series

37%

I've just never considered it 20%

I prefer not to commit to specific performance dates too early 18%

I can't afford a subscription 16%

I don't want to commit to multiple performances by the same company/venue 13%

I was not aware of subscriptions for opera/operetta 12%

I can't afford to pay for several performances all at once 12%

I prefer not to commit to specific performances until I have a chance to read the reviews/find out what other people thought of each performance

12%

I don't have time to go to multiple performances 10%

Definitely will

Probably will

Page 57

Appendix:Sample Profile

Page 59

Sample Profile

Total%

Regular Attendees

%

Occasional Attendees

%

Gender n= 1,583 n= 1,324 n= 234

Male 29 29 30

Female 71 71 70

Location n= 1,583 n= 1,324 n= 234

Melbourne Metro 88 89 81

Other VIC 12 11 19

Age n= 1,583 n= 1,324 n= 234

18-24 2 2 3

25-34 9 9 11

35-44 14 14 17

45-54 21 21 22

55-64 26 27 23

65+ 27 28 24

Total%

Regular Attendees

%

Occasional Attendees

%

Life stage n= 1,583 n= 1,324 n= 234

A single with no/independent/ children 25 26 18

Two or more singles with no/independent children

9 9 7

A couple withno/independent children 40 40 39

A family where most children are under 13 years

11 10 18

A family where most children are 13 years or older

15 14 18

Page 60

Sample Profile (continued)

Total%

Regular Attendees

%

Occasional Attendees

%

Income n= 1,583 n= 1,324 n= 234

Under $50,000 16 14 26

$50,000 - $74,999 13 13 15

$75,000 - $99,999 12 12 13

$100,000 - $149,999 16 15 16

$150,000 - $199,000 7 7 5

$200,000 + 9 10 3

Total%

Regular Attendees

%

Occasional Attendees

%

Work n= 1,583 n= 1,324 n= 234

Full time 34 35 28

Part time / Casual 18 18 18

Self employed 9 9 11

Retired 27 28 26

Unemployed 1 1 2

Home duties 4 3 9

Student 3 3 3

Volunteer 2 2 1