Quick, easy working capital loans for SMEs

1

The $200 Billion ProblemSMEs do not have access to Credit

92.77%

5.18% 2.05%

SME Financing in India

Self Financed/No Finance

Institutional

Non-Institutional

Causes of SME lack of

Credit Access

Lack of access to formal sources

Poor cash flow due to higher cost of credit

Higher risk profile

Lack of hard asset collateral

Lack of creditworthiness for banks

There exists a $200 Billion funding gap for enterprises that the banks and NBFCs do not lend to

Reserve Bank of India’s stance on the Problem

“India has 30 million

enterprises – only 7% have access

to financing – 93% are either self financed or not financed”

Formed committee on Comprehensive Financial Services

for small businesses and low income

households in 2011

“90% of businesses have no links with formal financial institutions.

Exists robust demand for financial services this

demand currently being served by informal

sources.”

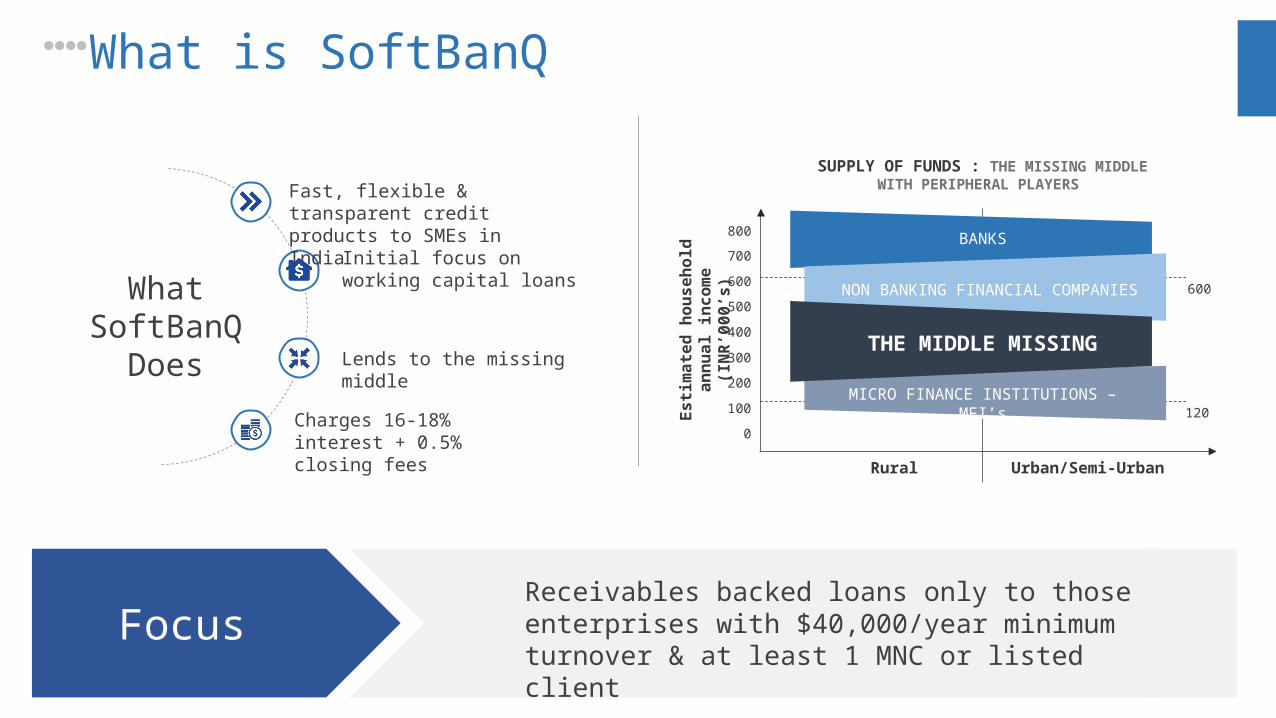

What SoftBanQ

Does

Fast, flexible & transparent credit products to SMEs in India

Initial focus on working capital loans

Lends to the missing middle

Charges 16-18% interest + 0.5% closing fees

Receivables backed loans only to those enterprises with $40,000/year minimum turnover & at least 1 MNC or listed client

Focus

Rural Urban/Semi-Urban

Esti

mate

d h

ou

seh

old

an

nu

al in

com

e

(IN

R’0

00

’s)

0

100

200

300

400

500

600

700

800 BANKS

NON BANKING FINANCIAL COMPANIES

THE MIDDLE MISSING

MICRO FINANCE INSTITUTIONS – MFI’s120

SUPPLY OF FUNDS : THE MISSING MIDDLE WITH PERIPHERAL PLAYERS

600

What is SoftBanQ

Various SME Credit Products

Loan against Invoice

Unsecured Business Loan

Mortgage Loan

Hypothecation Loan

• 1-12 month term/16-18% annualized interest

• Should have positive monthly cash flows

• Set criteria, no discretion required

• 1-5 year loan terms

• Secured by mortgage

• Requires ascertaining value of property

• Discretion on part of loan disbursement team required

• 6 months – 2 years term

• Secured by working assets of the business

• Requires ascertaining value of assets

• Discretion on part of loan disbursement team required

• 30-180 days term

• 16-18% annualized interest

• For companies with established customers

• Set criteria, no discretion required

Why Receivables Backed Financing

• Short term loans, therefore keeps cash churning for SoftBanQ – helping liquidity

• Set lending criteria, no discretion required on part of disbursement team

• No asset valuation required

• Less exposure per transaction – hedging risk for SoftBanQ capital partners

How it Works

CUSTOMER

1. Purchase Order

2. Delivery + Invoice

3. Payment only after 30-180 days

SME SoftBanQ

SoftBanQ Advance up to 80% of invoice value

Repayment after customer pays

SME PROFILE TERMS FOR SOFTBANQ CREDIT PRODUCTS

• Established corporate customers (MNC’s, E-commerce sites, listed companies)

• Long payment terms with above customers (30 days or more)

• Manufacturing, B2B, E-commerce, Distribution businesses

• $5,000 – $50,000 in loan amount (never exceeding 80% of invoice value)

• One time bullet repayment + EMIs

• 1-12 months loan term

Borrower Profiles / Diligence Criteria / Loan Sizes

Borrower Profile

• Fast growing India based SMEs with at least one reputed client (MNCs, large E-commerce players or publicly listed Indian corporates)

• 1+ year in business

• More than INR 25 lacs ($40,000) in annual turnover

• Initially, businesses based in Delhi, Bangalore, Mumbai, Chennai and Pune only

• Company & promoter profile

• Company Financials via Tally

• Bank statements & Income Tax Returns

• Invoice/purchase order information

• $5,000 – 50,000

Diligence Documents

Loan Sizes

Disbursement cycle of 7 days/1-12 month loan term/flexible repayment schedules

SoftBanQ vs Alternate FinancingBenefit to SMEs

SB vs Banks/NBFC’s SB vs Factoring SB vs Money Lenders

SB vs Credit Cards

• No property/machinery required as collateral

• Will lend to businesses under 3-5 years old

• Quick, paperless online application process

• Funds transfer within 7 days

• No pre closure penalties

• Flexible repayment options

• Interest rates at par with effective rates charged

• Available to all business sizes, not just large suppliers

• Ability to selectively finance invoices only as and when funds are required

• Quick empanelment

• 4 weeks typically taken by factoring companies

• No hard collateral requirement

• Significantly lower interest rates (16% vs 40-60%)

• Get funds equally fast

• Free of risks typically associated with informal sector finance

• Less burdensome repayment schedules

• Significantly lower interest rates (credit cards ~40%)

• Dependable source of credit for regular business needs

• Loan sizes set according to business needs, not card limits

Lower interest. Flexible repayment terms. No hard collateral.

Target Market & Acquisition

SoftBanQ

Vendors on E-commerce sites

Tie-ups with Industry Trade Bodies

Tie-ups with lending desks at banks

Business development team

Execution Strategy

0

10

20

30

40

50

60

Indian E-commerce Market Size (in $Bil-lions)

2009 2011 2013 2023

Indian E-commerce growing at 30% CAGR vs 8-10% globally

SMEs sell on these sites

Sites are adding 200,000 SMEs an annum to their marketplaces

SMEs have unmet capital demand, even by existing players such as Capital Float, Wonka, etc.

Sites support startups like SoftBanQ – good ecosystem

E-commerce Companies

Market Size, Revenue Potential & Exit

0.16 1.6 16 1600

50010001500

REVENUE POTENTIAL

Revenues(in $millions)

Pri

nci

pa

l A

mo

un

t

(in

$m

illio

ns)

Market Size

• 30 Million+ SMEs & Micro Enterprises in India

• $200 Billion credit funding gap where banks / NBFCs don’t lend – IFC/McKinsey Report

• India – 3rd largest economy growing at 7.5%

• Online lending at the cusp of booming in India

• Acquisition by bank / NBFC

• Acquisition by Kabbage / Capital Float

• IPO

• Principal amount is for 12 months at 16.5% annualized

• Loan repayment default rate is 1%

• Exclusive of fixed costs

• Exclusive of closing fees of 0.5 – 3%

Exit Revenue Assumptions

Capital Structure

Guarantees repayment

default

Equity Investors in SoftBanQ

HNI Lenders to SoftBanQ

Lends to SoftBanQ at lower interest

rates

Increases capital base

to lend

Receives principal and interest

through Escrow

Uses the interest rate carry/maturity transformation principle of commercial banking

~60% of equity capital is an asset/not a cost

Hedging Risk

~30% of equity capital is liquid

Short duration of capital churn

Used for fixed costs

of the business

Used as principal lending amount

Used to guarantee any

repayment defaults to HNI Capital Base

Hedging of Risk

Industry Ecosystem

In descending order of amounts of funds

managed

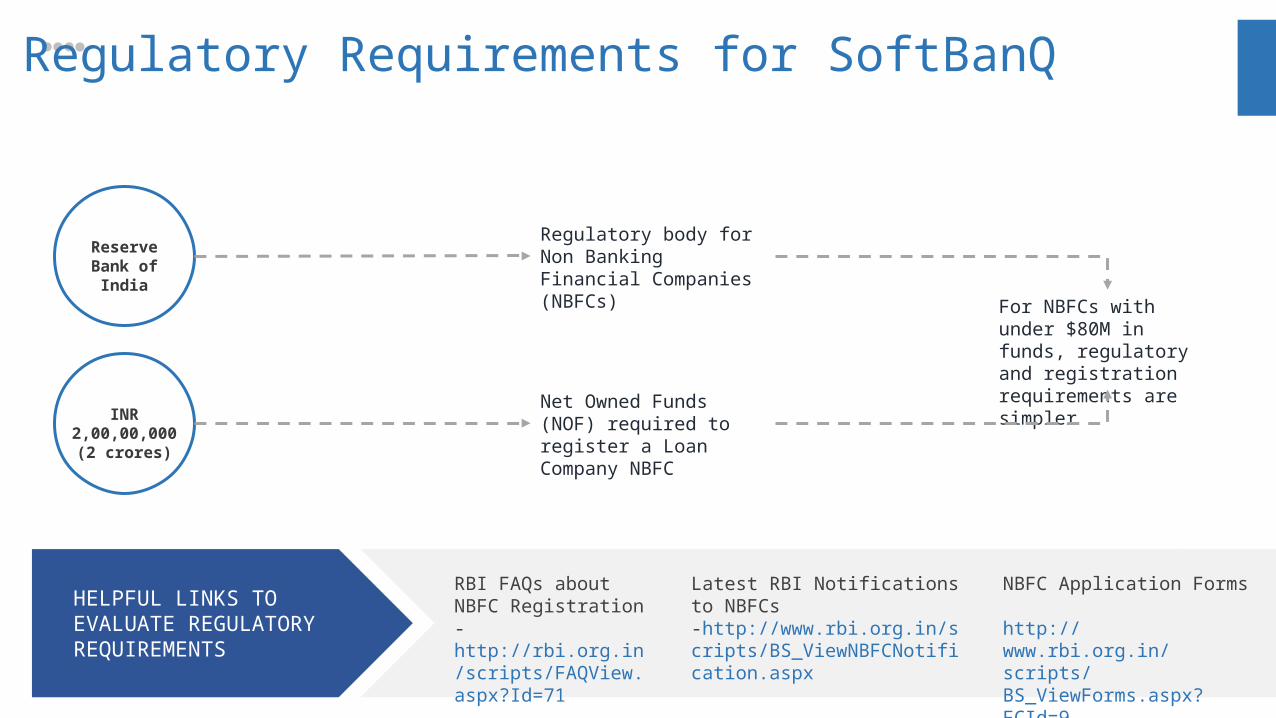

Regulatory Requirements for SoftBanQ

Reserve Bank of

India

INR 2,00,00,000 (2 crores)

Regulatory body for Non Banking Financial Companies (NBFCs)

Net Owned Funds (NOF) required to register a Loan Company NBFC

For NBFCs with under $80M in funds, regulatory and registration requirements are simpler

RBI FAQs about NBFC Registration - http://rbi.org.in/scripts/FAQView.aspx?Id=71

HELPFUL LINKS TO EVALUATE REGULATORY REQUIREMENTS

Latest RBI Notifications to NBFCs -http://www.rbi.org.in/scripts/BS_ViewNBFCNotification.aspx

NBFC Application Forms

http://www.rbi.org.in/scripts/BS_ViewForms.aspx?FCId=9

Founding Team

• Successful Fintech startup entrepreneur

• Ex corporate lawyer with 7 years in finance & investment banking, advising on capital raises

• Founded & led to success, www.BankerBay.com – a leading deal origination platform used by top investment banks and private equity firms – Headquartered in the US, teams in New York, San Francisco, Singapore & Bangalore

• Experience in bootstrapping, product development, enterprise customer acquisition, raising capital, scaling & building & leading a 25 member team

• Experience in working with investors and serving on a BoardAsh Narain / Founder

MENA Based Founding Investor

• CEO of a $1.4 Billion Family Office in the Mid East

• Investing in SoftBanQ with a group of angels

• MBA - Colombia Business School, MIT

Head / Credit & Credit Products

• Professional with 5+ years in underwriting credit for SMEs in India

• Past experience working for a Loan Company NBFC in India

Head – Business Development

• Establishing relationships between SoftBanQ & E-commerce firms

• Establishing relationships between SoftBanQ & banks

• Creating SME funnel