Sovereign Debt ManagementSovereign Debt Management

Emerging Market Trends, Implications for Emerging Market Trends, Implications for Debt Managers, and Country Experiences Debt Managers, and Country Experiences

and Challenges and Challenges

Udaibir S. Das, IMF andGloria M. Grandolini, The World Bank

16th OECD Global Forum on Debt Management and Government Securities MarketsDec 6-7, 2006Amsterdam

OutlineOutline

What do we see as the trends in emerging market debt?How have the debt managers done and possible implications?What are the risk factors for further work in 2007?

Cyclical and Structural Factors Cyclical and Structural Factors Driving Emerging MarketsDriving Emerging Markets

Most of 2005 trends continued during 2006…

Favorable environment for global financial marketsStrengthened financial position of EMCsGrowing demand for EM debt by Institutional InvestorsMarket turbulence in the second quarter of 2006; steps to

attenuate vulnerabilities

24

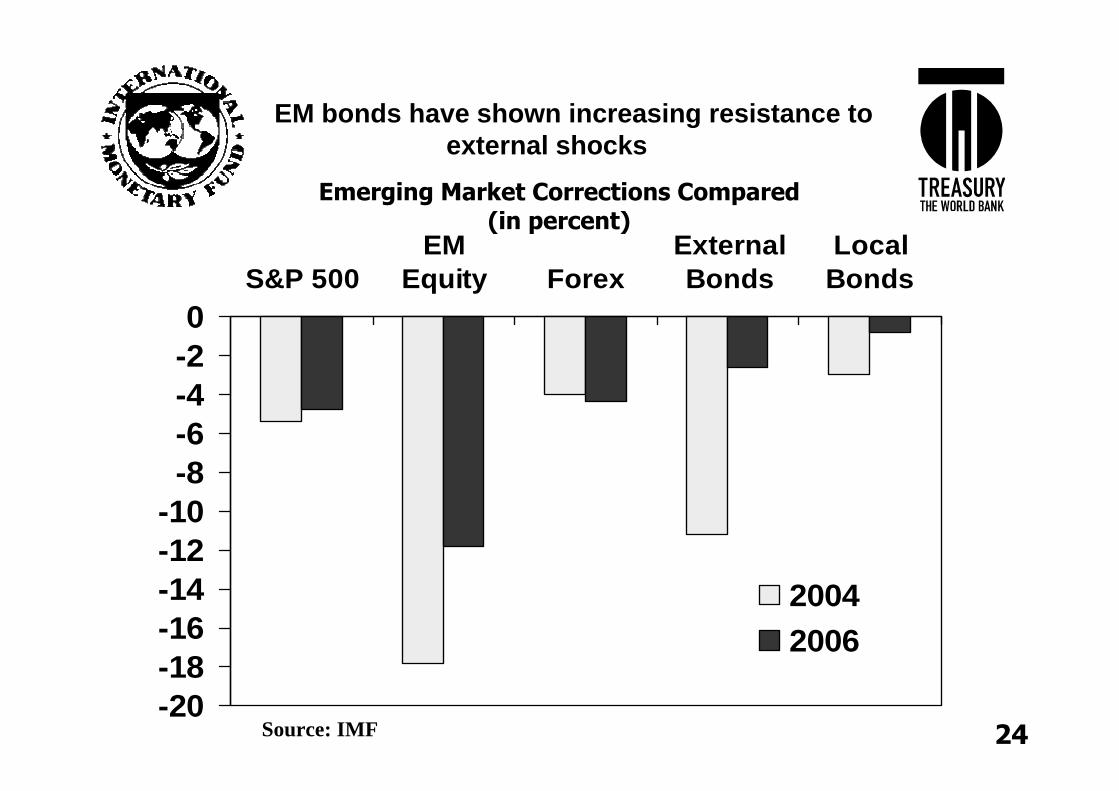

Emerging Market Corrections Compared(in percent)

-20-18-16-14-12-10-8-6-4-20

S&P 500EM

Equity ForexExternalBonds

LocalBonds

20042006

EM bonds have shown increasing resistance to external shocks

Source: IMF

Credit Default Swap Spreads vs. Sovereign Credit Ratings (In basis points)

5/09/06

(R 2 = 0.8772)6/09/06

(R 2 = 0.8913)

0

50

100

150

200

250

300

350

0

50

100

150

200

250

300

350

As of 6/09/06

As of 5/09/06

A BBB BB B

nevertheless, lower rated countries were hit harder by the May 2006 market correction

Source: IMF

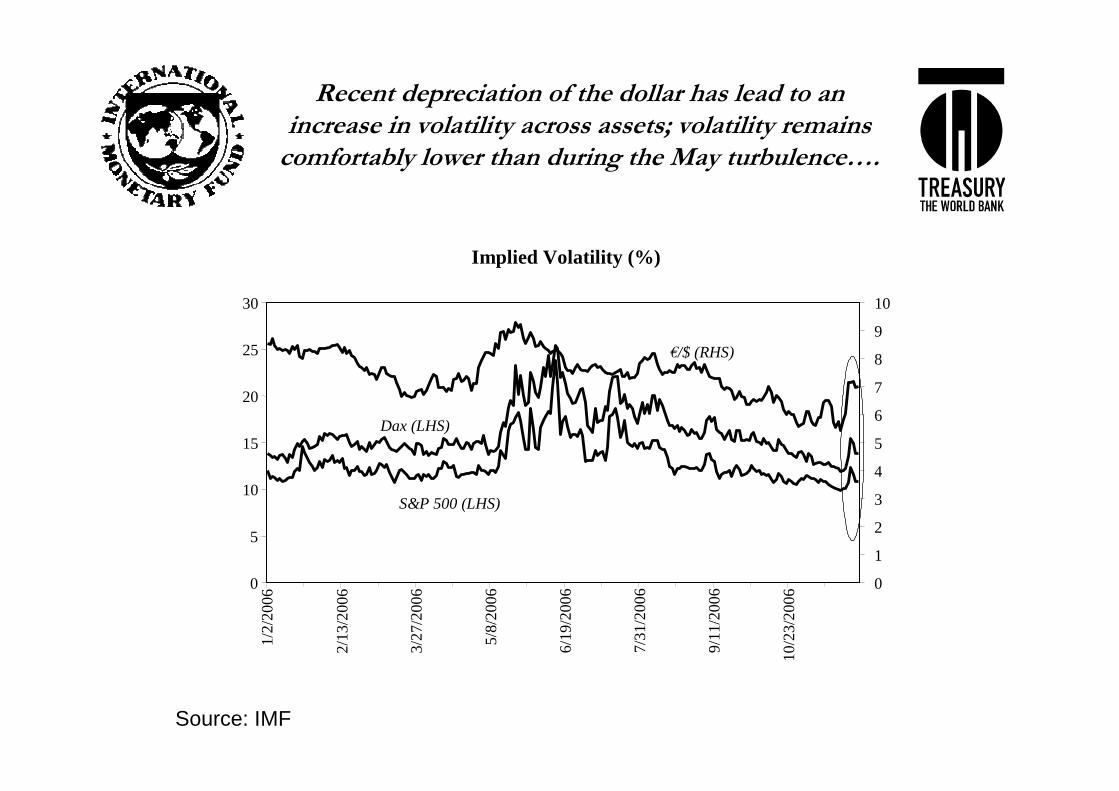

Recent depreciation of the dollar has lead to an Recent depreciation of the dollar has lead to an increase in volatility across assets; volatility remains increase in volatility across assets; volatility remains

comfortably lower than during the May turbulence….comfortably lower than during the May turbulence….

Source: IMF

Implied Volatility (%)

0

5

10

15

20

25

30

1/2/

2006

2/13

/200

6

3/27

/200

6

5/8/

2006

6/19

/200

6

7/31

/200

6

9/11

/200

6

10/2

3/20

06

0

1

2

3

4

5

6

7

8

9

10

S&P 500 (LHS)

Dax (LHS)

€/$ (RHS)

and vulnerabilities remain, particularly in the EMEA and vulnerabilities remain, particularly in the EMEA (Emerging Europe and Africa) region, where (Emerging Europe and Africa) region, where

sovereign debt markets have lagged behind since the sovereign debt markets have lagged behind since the MayMay--June correction….June correction….

Source: IMF

Emerging Market Sovereign Spreads(From Merrill Lynch, bps)

100

200

300

400

500

600

700

Jan-

04

Mar

-04

May

-04

Jul-

04

Sep-

04

Nov

-04

Jan-

05

Mar

-05

May

-05

Jul-

05

Sep-

05

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-

06

Sep-

06

Nov

-06 100

200

300

400

500

600

700

Latin America

Asia

EMEA

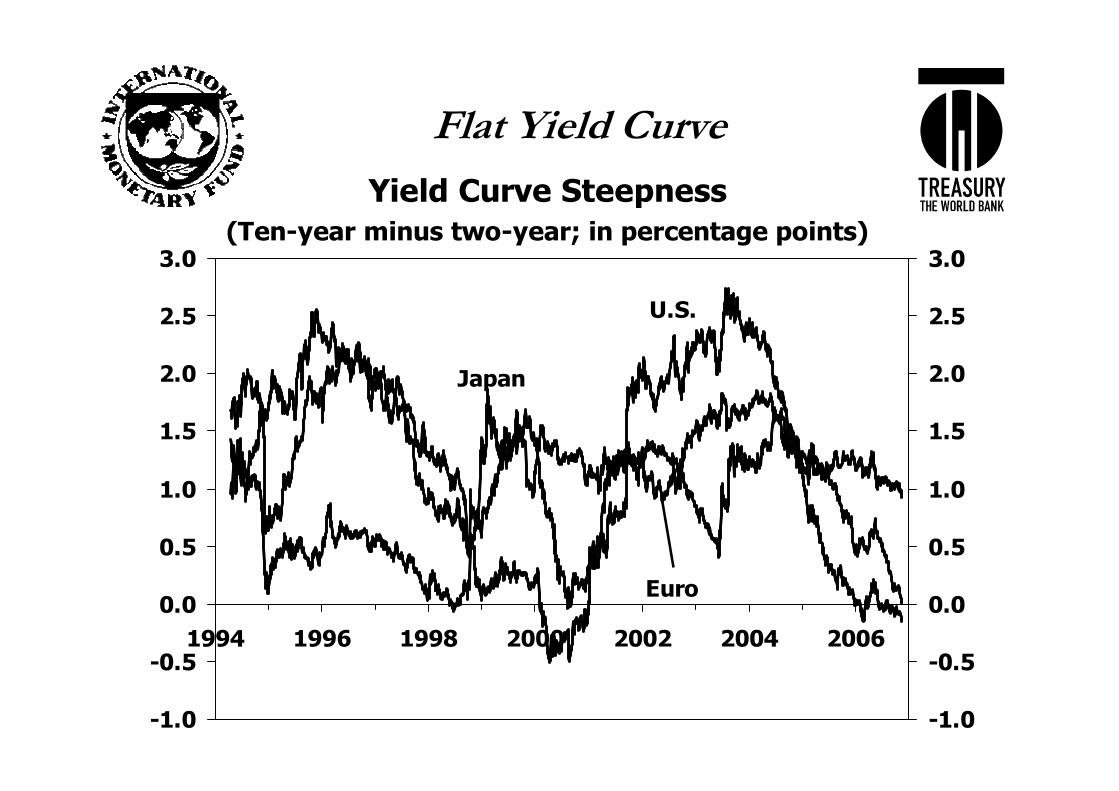

Search for YieldSearch for Yield

Search for yield continues as dominant theme:Stems from historically low long-term bond yields and flat yield curves in mature markets

Despite recent turn in credit cycle

Flat Yield CurveFlat Yield Curve

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1994 1996 1998 2000 2002 2004 2006

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Yield Curve Steepness(Ten-year minus two-year; in percentage points)

Japan

U.S.

Euro

0

40

80

120

160

200

2003 2004 2005 20060

200

400

600

800

1000

1200

1400

1600

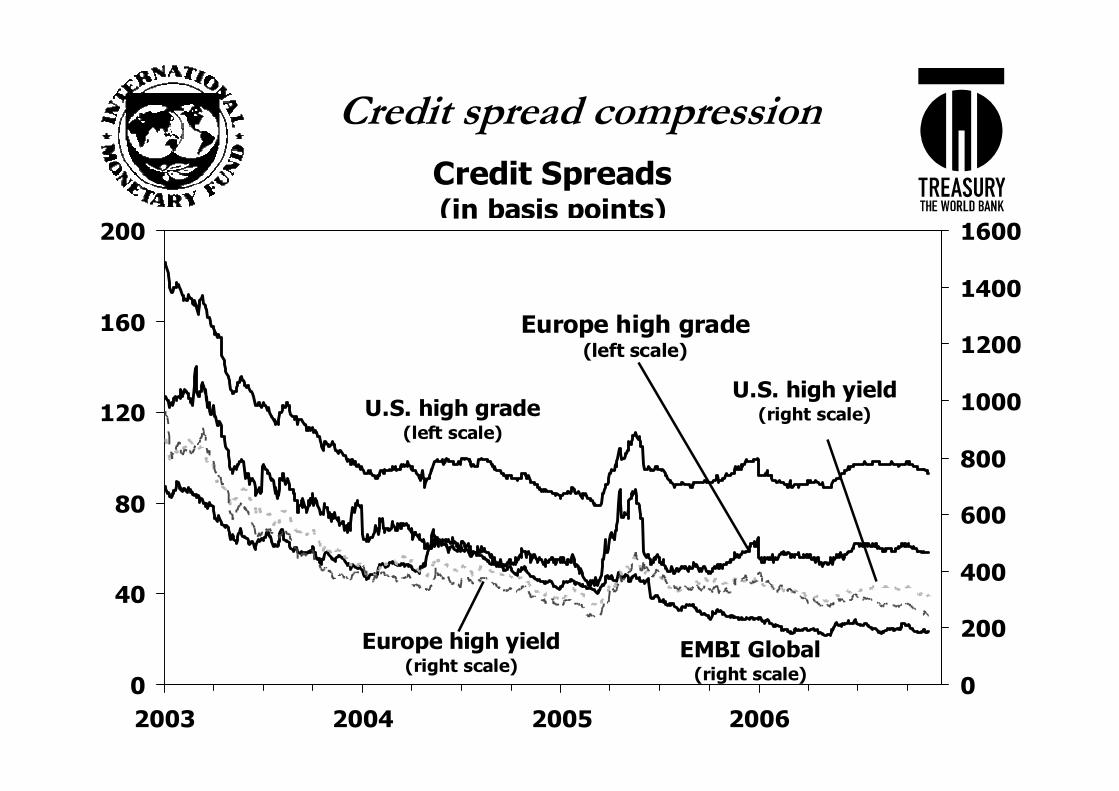

Credit Spreads(in basis points)

Europe high grade(left scale)

U.S. high grade(left scale)

EMBI Global(right scale)

Europe high yield(right scale)

U.S. high yield(right scale)

Credit spread compressionCredit spread compression

0

500

1000

1500

2000

1992 1994 1996 1998 2000 2002 2004 20062

3

4

5

6

7

8

9

Emerging Market Debt Spreads and 10-Year Treasury Yields

10-year Treasury yields(percent, right scale)

EMBI/EMBIG spreads(basis points, left scale)

Sources: Bloomberg L.P.; JPMorgan Chase & Co; and IMF staff estimates.

EM Spreads Continue to DeclineEM Spreads Continue to Decline

Financial Position of EMCsFinancial Position of EMCs

Continues to strengthen• Current account strengthening• Asset accumulation increasing buffers to absorb

shocks• FDI increasing

Fiscal and monetary policies have played an important role in the improvements

EM and Developing Countries: Current EM and Developing Countries: Current Account Balance and External FinancingAccount Balance and External Financing

(In billions of U.S. dollars)(In billions of U.S. dollars)

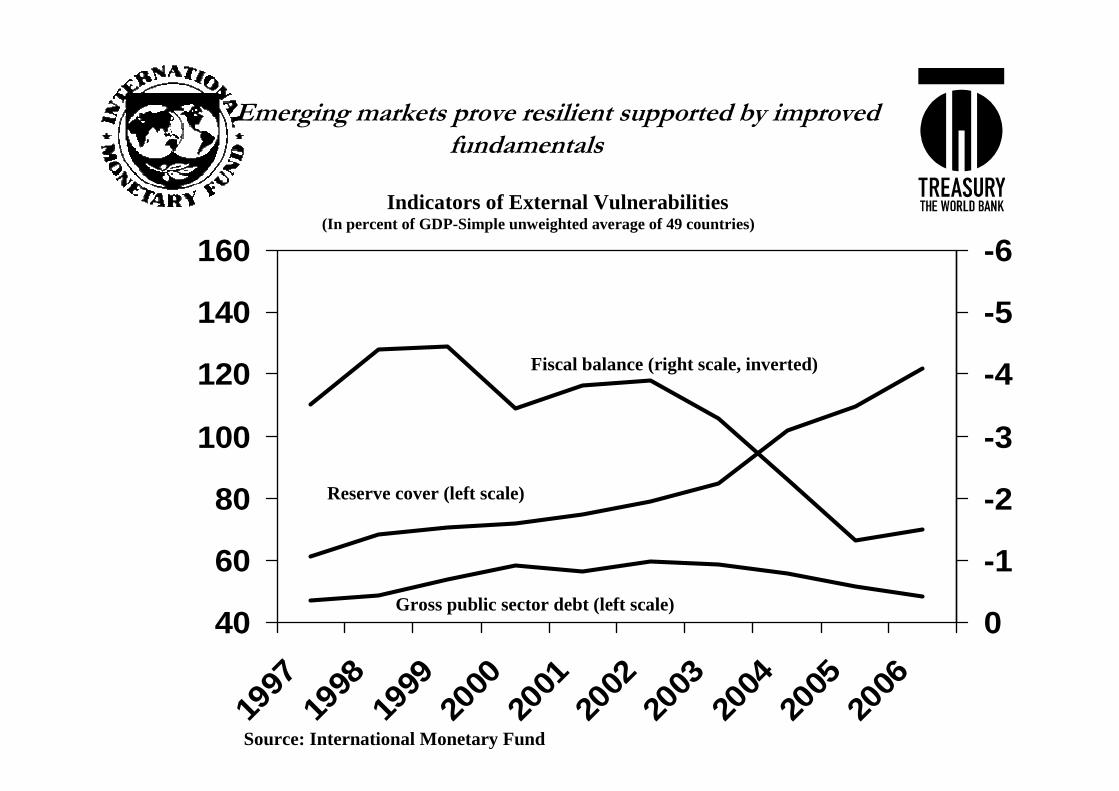

Emerging markets prove resilient supported by improved Emerging markets prove resilient supported by improved fundamentalsfundamentals

40

60

80

100

120

140

160

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

-6

-5

-4

-3

-2

-1

0Gross public sector debt (left scale)

Reserve cover (left scale)

Fiscal balance (right scale, inverted)

Indicators of External Vulnerabilities(In percent of GDP-Simple unweighted average of 49 countries)

Source: International Monetary Fund

Figure A. Public Debt 1/ 2/ (In percent of GDP)

55

60

65

70

75

80

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005P ro j

Indus trial Co untries Emerging Markets

S o urc e : C o untry a utho ritie s a nd s ta ff e s tim a te s .1/ Unwe ighte d a ve ra ge s .2/ 2005 ba s e d o n s ta ff pro je c tio ns .

Public Debt 1,2

(in percent of GDP)

I-19

Falling public debt since 2002Falling public debt since 2002

with domestic debt at increasingly longer maturities

Domestic Sovereign Debt Maturing in Less than One Year(in percent of total sovereign debt)

0

10

20

30

40

50

60

70

80

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

0

10

20

30

40

50

60

70

80

Europe

Latin America

Asia

Source: Global Financial Stability Report, IMF, April 2006

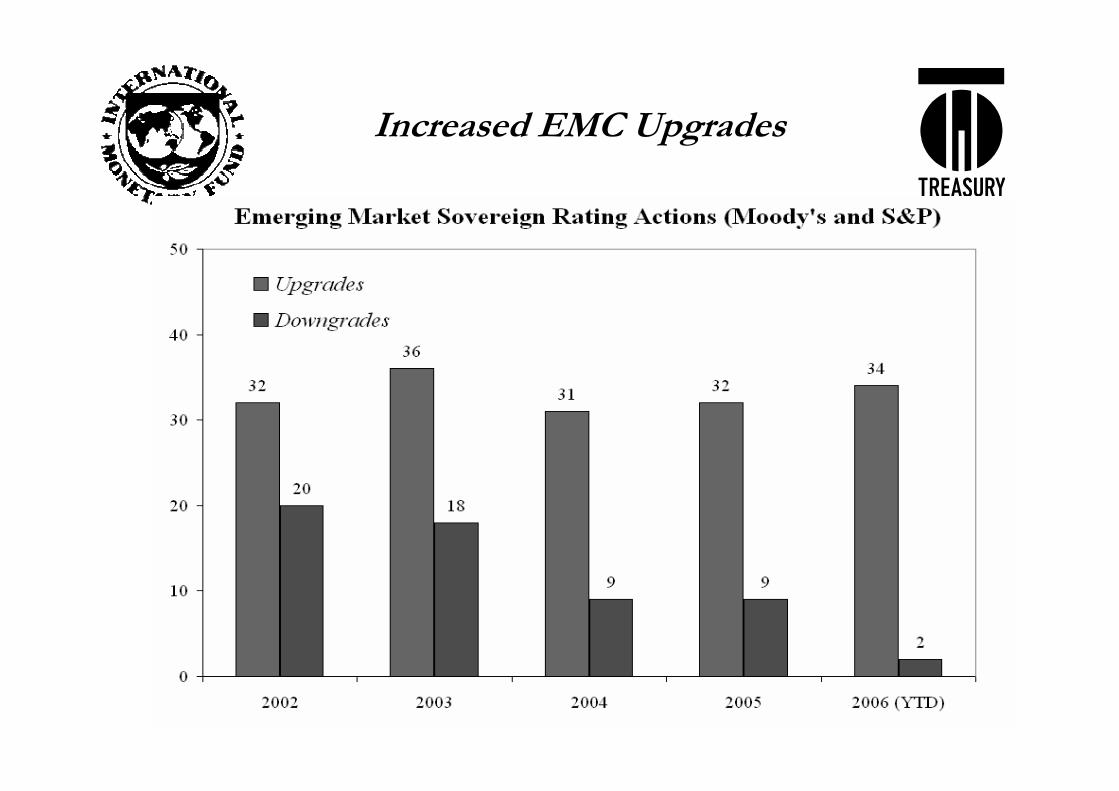

Increased EMC UpgradesIncreased EMC Upgrades

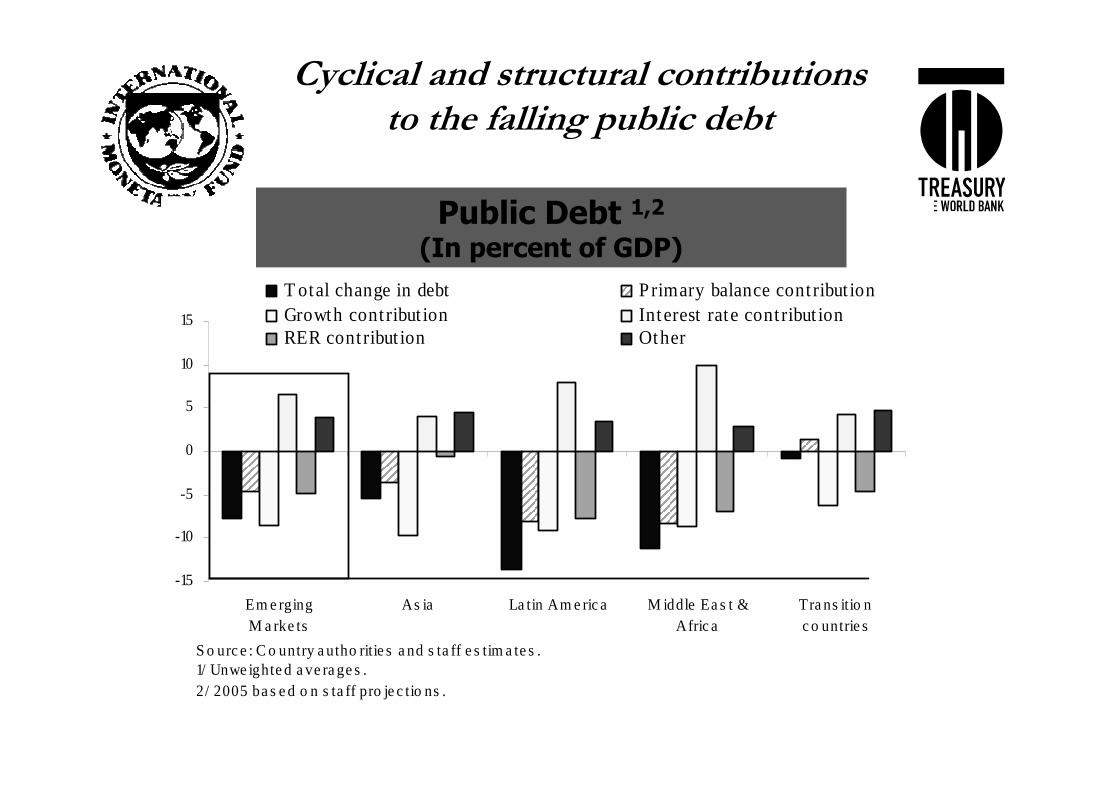

Figure B. Contributions to the Change in Public Debt 2002-05 1/ 2/(In percent of GDP)

-15

-10

-5

0

5

10

15

Em e rgingM a rke ts

As ia La tin Am e ric a M iddle Ea s t &Afric a

Tra ns itio nc o untrie s

T otal change in debt P rimary balance cont ribut ionGrowth cont ribut ion Interest rate cont ribut ionRER cont ribut ion Other

S o urc e : C o untry a utho ritie s a nd s ta ff e s tim a te s .1/ Unwe ighte d a ve ra ge s .2/ 2005 ba s e d o n s ta ff pro je c tio ns .

Cyclical and structural contributions Cyclical and structural contributions to the falling public debtto the falling public debt

Public Debt 1,2

(In percent of GDP)

Implications for EM Debt Implications for EM Debt Managers?Managers?

Opportunities for active debt management and implementation of risk reduction strategies

OpportunitiesOpportunities

Strong demand for new international bond issues• Lower gross issuance• Unsatisfied demand?• Lower funding costs and increasing maturities

Average maturity extension of about 5 years for 18 EMEs

Facilitating active debt management operations• Pre-financing and pre-payment

Brazil pre-financed 2007 FX amortizationsUruguay pre-paid IMF November 2006Colombia pre-paid multilateralsMexico pre-paid multilaterals

Lower Gross Issuance on Lower Gross Issuance on International Market than 2005International Market than 2005

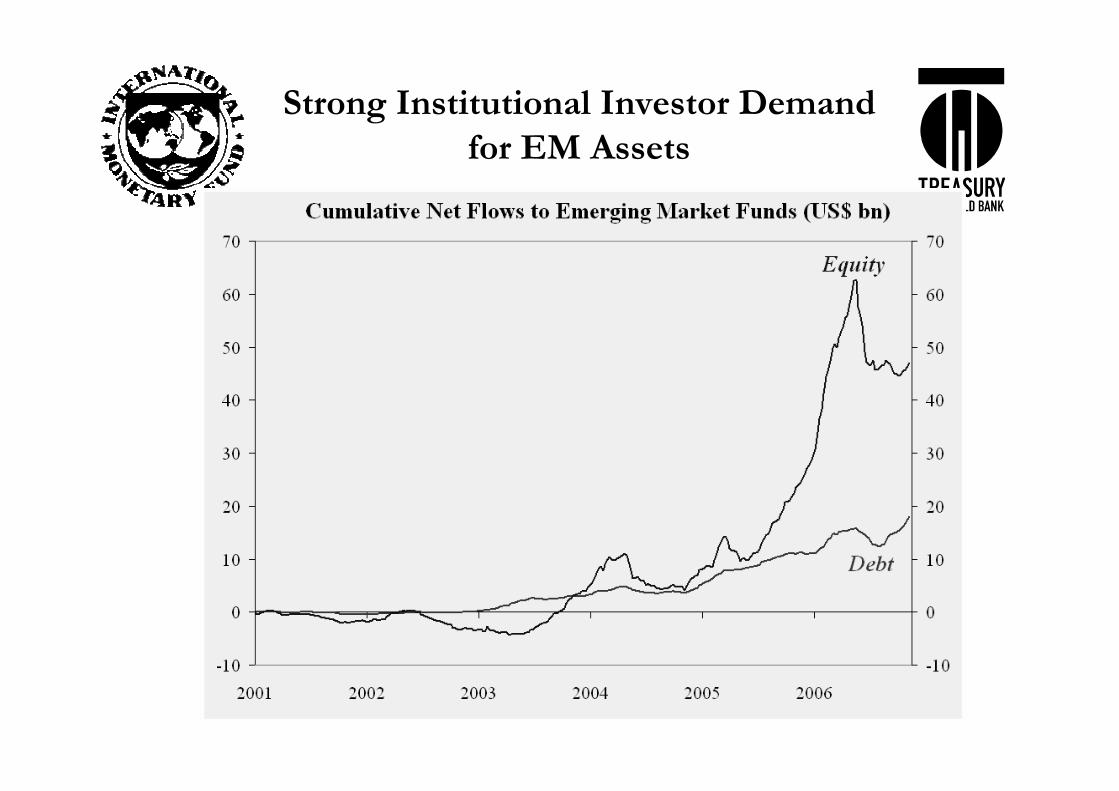

Opportunities: Investor Opportunities: Investor DiversificationDiversification

Retail programs• South Africa’s program continues to grow – 20,000 investors• Brazil’s success with Treasury Direct – 70,000 investors• Indonesia issued first retail bond August 2006• But still small percentage of total stock (e.g Poland savings

bonds < 2% of total stock)

Institutional investors• Continued demand from foreign institutional investors for

EM debt

Strong Institutional Investor Demand Strong Institutional Investor Demand for EM Assetsfor EM Assets

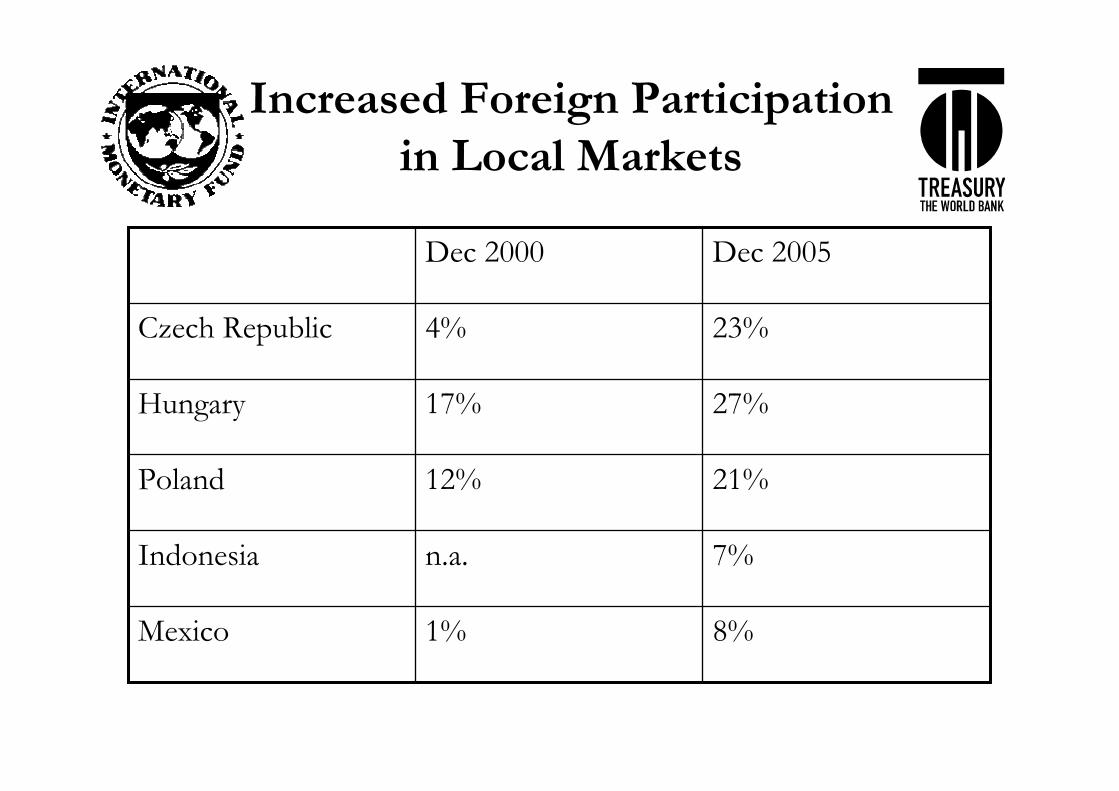

Increased Foreign Participation Increased Foreign Participation in Local Marketsin Local Markets

27%17%Hungary

23%4%Czech Republic

8%1%Mexico

7%n.a.Indonesia

21%12%Poland

Dec 2005Dec 2000

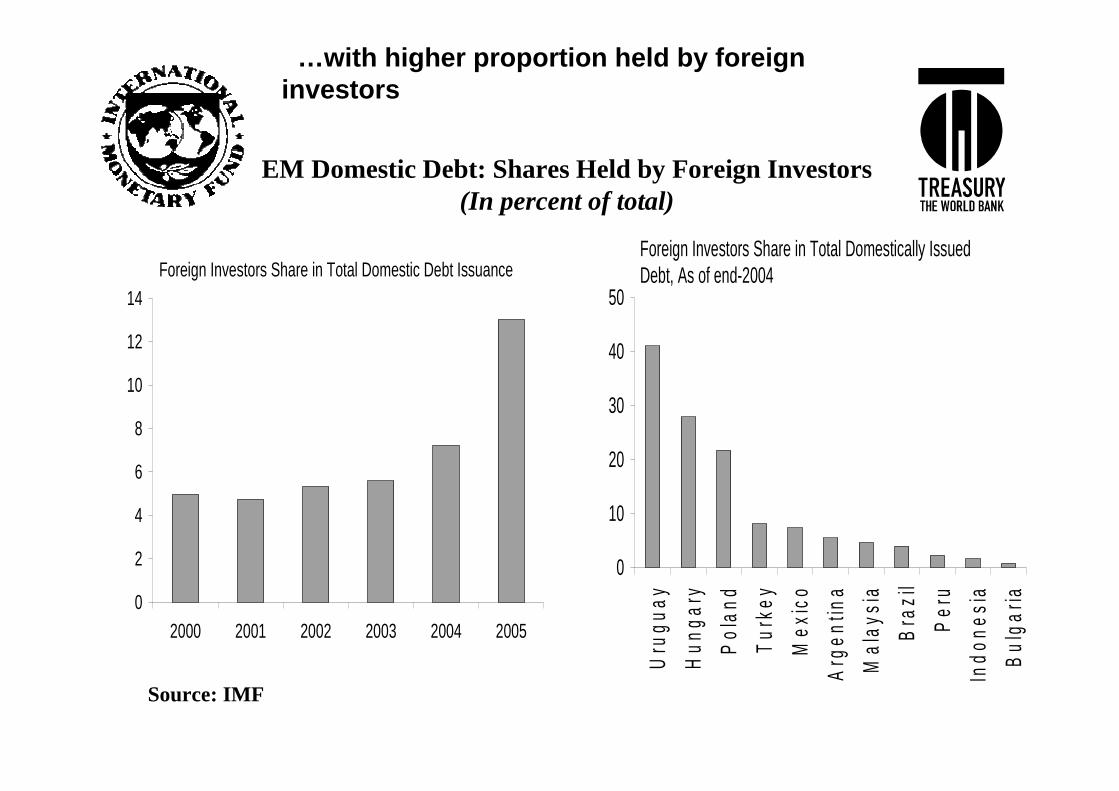

EM Domestic Debt: Shares Held by Foreign Investors(In percent of total)

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005

Foreign Investors Share in Total Domestic Debt Issuance

0

10

20

30

40

50

Uru

guay

Hun

gary

Pol

and

Tur

key

Mex

ico

Arg

entin

a

Mal

aysi

a

Bra

zil

Per

u

Indo

nesi

a

Bul

garia

Foreign Investors Share in Total Domestically Issued Debt, As of end-2004

…with higher proportion held by foreign investors

Source: IMF

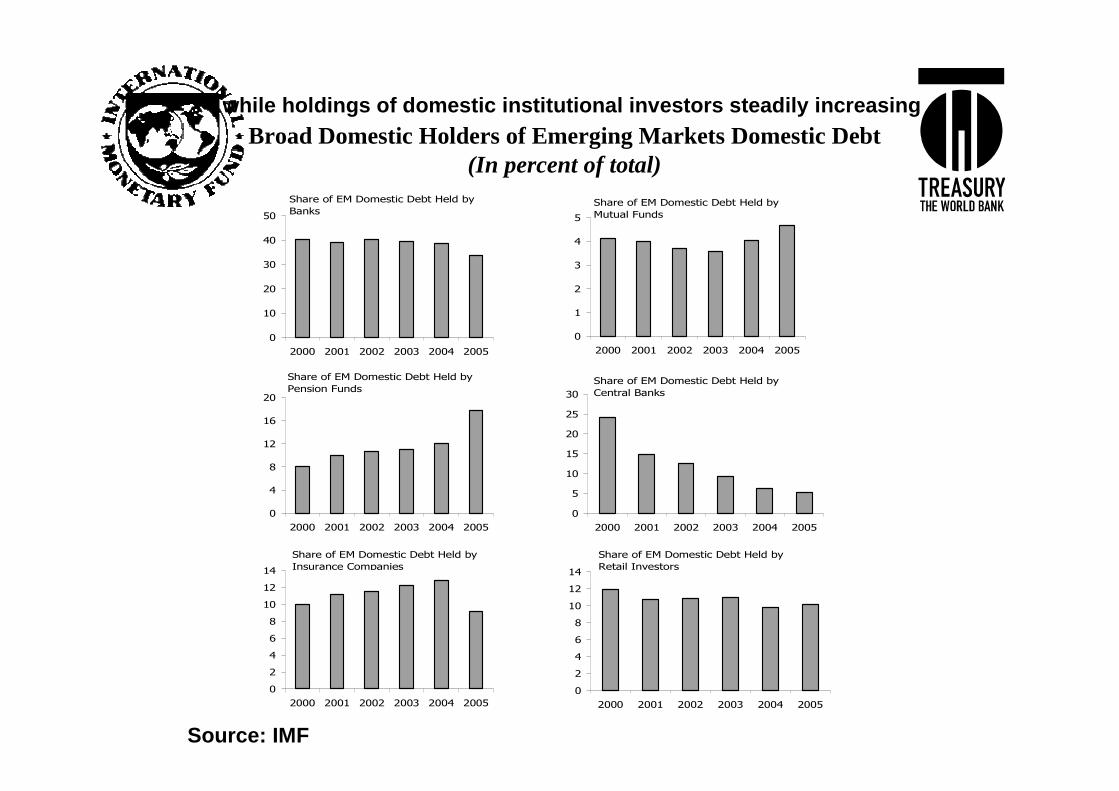

Broad Domestic Holders of Emerging Markets Domestic Debt(In percent of total)

0

10

20

30

40

50

2000 2001 2002 2003 2004 2005

0

4

8

12

16

20

2000 2001 2002 2003 2004 2005

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005

Share of EM Domestic Debt Held by Banks

Share of EM Domestic Debt Held by Pension Funds

Share of EM Domestic Debt Held by Insurance Companies

0

1

2

3

4

5

2000 2001 2002 2003 2004 2005

Share of EM Domestic Debt Held by Mutual Funds

0

5

10

15

20

25

30

2000 2001 2002 2003 2004 2005

Share of EM Domestic Debt Held by Central Banks

0

2

4

6

8

10

12

14

2000 2001 2002 2003 2004 2005

Share of EM Domestic Debt Held by Retail Investors

while holdings of domestic institutional investors steadily increasing

Source: IMF

Innovations in Market InstrumentsInnovations in Market Instruments

Extension of maturity in domestic fixed-rate bonds• Czech republic just launched 30-year bond (Dec

2006)• Mexico introduced 30-year bond (Oct 2006)• Korea introduced 20-year bond ( Jan 2006)

Innovations in Market InstrumentsInnovations in Market Instruments

Exotic instruments• Islamic or “sukuk” gaining in significance

Significant corporate issuesDubai, Malaysia and Pakistan current sovereign issuers

• Special optionsMexican exchange warrants

International markets• Continued tapping of international bonds in local currency

Brazil – September 2005 issued 10-year Global ReaisColombia – tapped the 2015 Global TES in March and August 2006

Strengthening of Debt Management Strengthening of Debt Management FrameworksFrameworks

Enhanced transparency• Korea

Market Development Strategy 2006• Indonesia

Debt management strategyAuction calendarDebt statisticsInvestor relations unit

• MacedoniaDebt management strategyMarket development reportAuction calendar

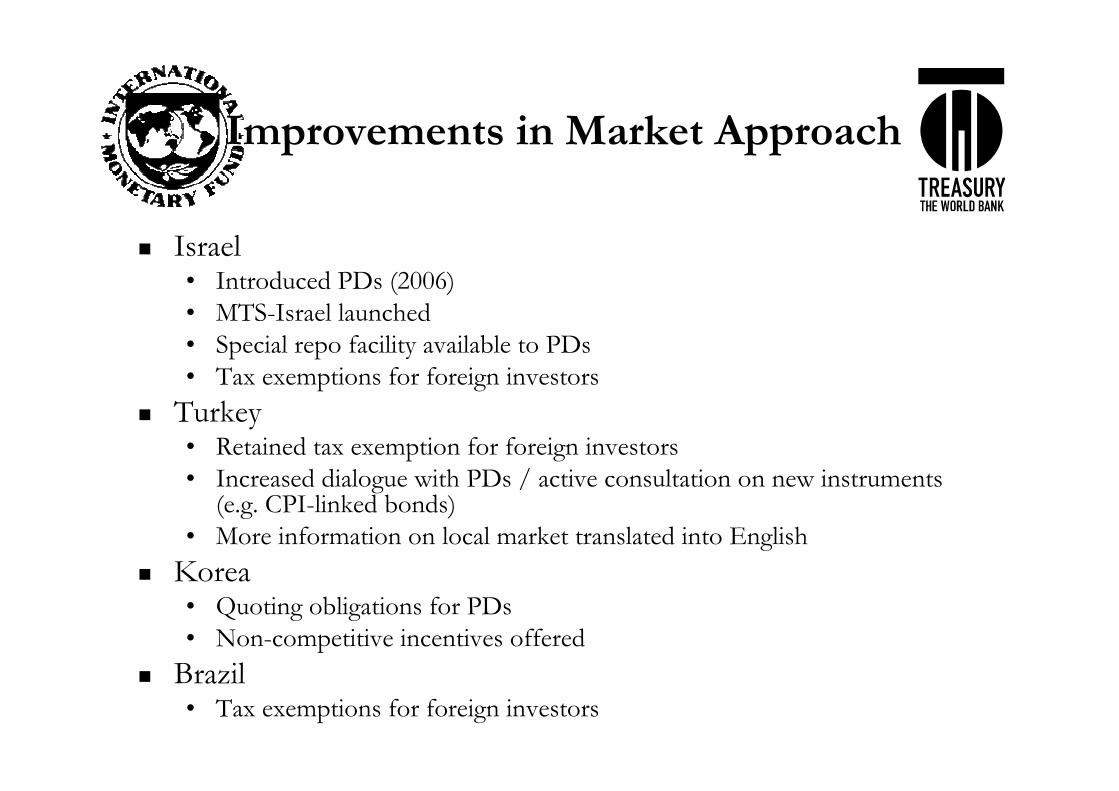

Improvements in Market ApproachImprovements in Market Approach

Israel• Introduced PDs (2006)• MTS-Israel launched • Special repo facility available to PDs• Tax exemptions for foreign investors

Turkey• Retained tax exemption for foreign investors• Increased dialogue with PDs / active consultation on new instruments

(e.g. CPI-linked bonds)• More information on local market translated into English

Korea• Quoting obligations for PDs• Non-competitive incentives offered

Brazil• Tax exemptions for foreign investors

And, for International Bonds…And, for International Bonds…

Euro Global MTS platform• Launched summer 2005• Issuers listed are:

Bulgaria, Romania, Croatia, Brazil, China, Mexico, South Africa,Turkey, Venezuela.Must be supported by 7 market makersBonds euro-denominated benchmarks

• 18 market makers involved• March 2006 total trading volume surpassed EUR 1 billion

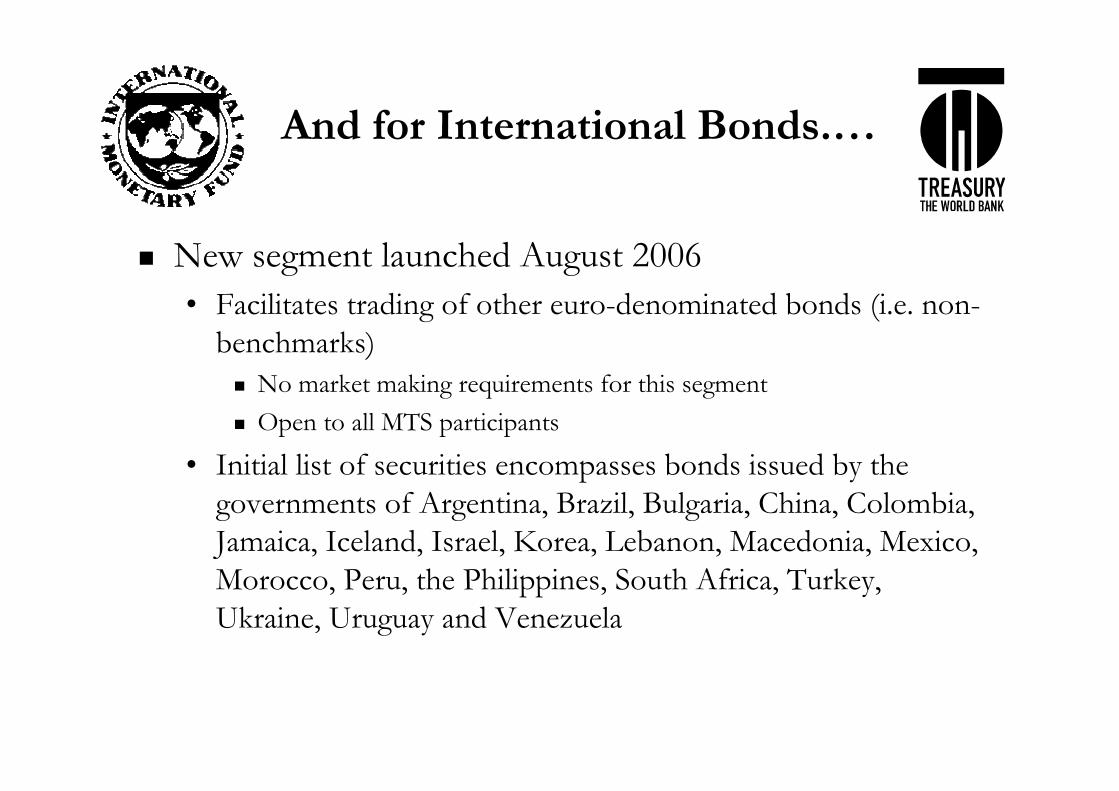

And for International Bonds.…And for International Bonds.…

New segment launched August 2006• Facilitates trading of other euro-denominated bonds (i.e. non-

benchmarks)No market making requirements for this segmentOpen to all MTS participants

• Initial list of securities encompasses bonds issued by the governments of Argentina, Brazil, Bulgaria, China, Colombia, Jamaica, Iceland, Israel, Korea, Lebanon, Macedonia, Mexico, Morocco, Peru, the Philippines, South Africa, Turkey, Ukraine, Uruguay and Venezuela

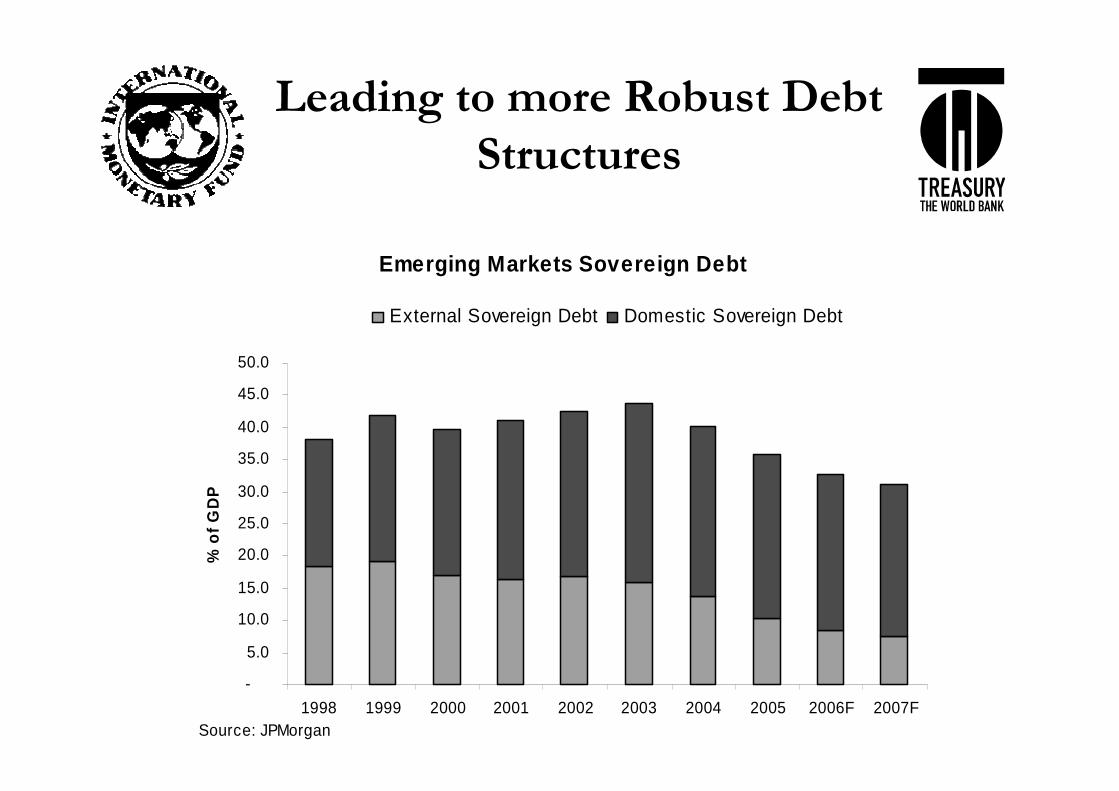

Leading to more Robust Debt Leading to more Robust Debt StructuresStructures

Emerging Markets Sovereign Debt

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

1998 1999 2000 2001 2002 2003 2004 2005 2006F 2007F

% o

f G

DP

External Sovereign Debt Domestic Sovereign Debt

Source: JPMorgan

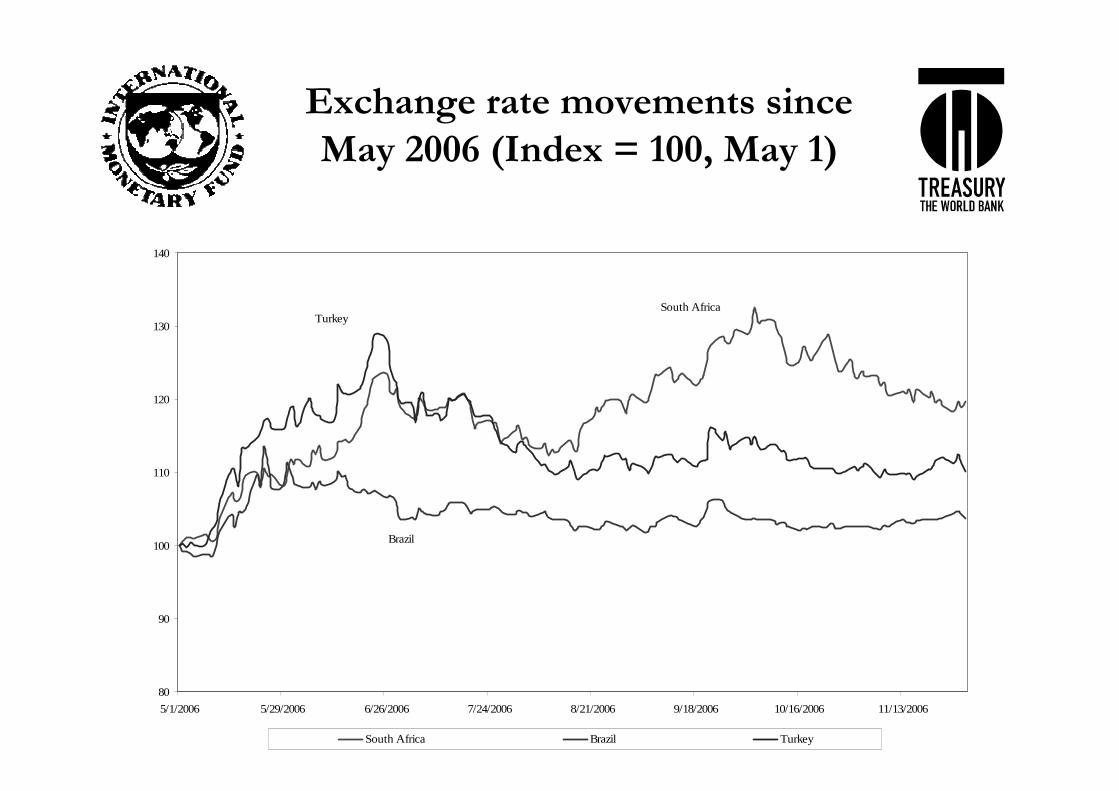

But … Risks RemainBut … Risks Remain

Exchange rate movements since Exchange rate movements since May 2006 (Index = 100, May 1)May 2006 (Index = 100, May 1)

80

90

100

110

120

130

140

5/1/2006 5/29/2006 6/26/2006 7/24/2006 8/21/2006 9/18/2006 10/16/2006 11/13/2006

South Africa Brazil Turkey

TurkeySouth Africa

Brazil

Net Flows out of EM debt …Net Flows out of EM debt …

-800.000

-600.000

-400.000

-200.000

0.000

200.000

400.000

600.000

800.000

1,000.000

1,200.000

May 3 June 7 July 5 August2

Sept 6 Oct 4 Nov 1

US$

mn

EM - Debt Flows

Requiring a Tightening of Local Requiring a Tightening of Local Credit Conditions in Some Markets Credit Conditions in Some Markets

0

2

4

6

8

10

12

14

16

18

20

5/1/2006 6/8/2006 7/18/2006 8/25/2006 10/4/2006 11/13/2006

11.5

12

12.5

13

13.5

14

14.5

15

15.5

16

TURKEY INTERBANK OVERNIGHT SOUTH AFRICAN REPO BRAZIL OVERNIGHT SELIC

No Room for ComplacencyNo Room for Complacency

Fund increasing surveillance of these issues• Encourage development of medium-term debt strategies

within medium-term fiscal frameworks

Increased emphasis on debt sustainability analysis• Both for EMEs and LICs• Improving the capture of domestic debt issues in DSA

Working with multilateral task force on debt statistics• Improve data on debt issued in domestic markets• Continued emphasis on improving transparency

No Room for ComplacencyNo Room for Complacency

Stronger focus on an integrated approach towards risks in a sovereign balance sheet• Set up a Sovereign ALM Unit (3Ms: Macro, Management,

Markets)

Stronger operational link between sustainable debt and its prudent managementNature of global liquidity? Who are the current providers and why/how they provide it? Can one differentiate between reversible and more sticky liquidity?Changes in the local and foreign investor bases; Would asset allocation preferences remain?

No Room for ComplacencyNo Room for Complacency

Petrodollar savings or accumulation of foreign exchange reserves: broadened the investor base? Role of regional investors? Is “home bias” important? Are investor continuing to expand their interest in relatively less well-known (riskier) emerging markets ?

No Room for ComplacencyNo Room for Complacency

Which structural features of local EM capital markets are critical in reducing vulnerabilities? Continuing challenges in implementing an effective institutional framework for debt management. Obstacles and challenges of developing a medium-term debt management strategy. Need for an active role for debt managers in broader economic and financial market development policies.

Sovereign Debt Management in Sovereign Debt Management in Emerging Markets: Emerging Markets:

Country Experiences and ChallengesCountry Experiences and Challenges

AgendaAgenda

Review progress and challenges for developing and emerging market countries in the areas of:

1. Developing government debt management strategies2. Coordination with macroeconomic framework3. Governance4. Capacity5. Implementing reforms

Based on: Managing Public Debt: From Diagnostics to Reform Implementation, World Bank 2006, and Sovereign Debt Management Forum 2006 Questionnaire

What do we mean by a public debt management strategy?

A document that describes the intended composition of the public debt in the medium term:• Provides a “roadmap” for borrowing transactions• Includes assumptions, supporting analysis, limitations,

rationale

1. Developing debt 1. Developing debt management strategiesmanagement strategies

Progress in 12 Country CasesProgress in 12 Country Cases

Countries ranged from low income to high middle income, across six regions

Initially none had a medium-term sovereign debt management strategy:Three countries now have comprehensive strategiesThree others have active work programs with external assistance

Source: Managing Public Debt: From Diagnostics to Reform Implementation, World Bank 2006

Sovereign Debt Management Sovereign Debt Management Forum: Questionnaire ResponsesForum: Questionnaire Responses

33%13%Have strategic targets or benchmarks for domestic debt

27%24%Have strategic targets or benchmarks for foreign currency debt

48%45%Have general guidelines on managing risk

20061999

The major risk to be managed in the debt portfolio:

•Interest rate risk: around 50% of respondents

•Currency risk: around 35%

•Rollover risk: 20% (35% as second most important)

Data on Country StrategiesData on Country Strategies

10071Total3424No formal strategy3424Guidelines

3223Strategic targets%Number of countriesStatus

10047Total with strategies

199Strategy not public

8138Strategy public

%Number of countries

Source: World Bank Staff

Common Challenges in Developing Common Challenges in Developing Strategic TargetsStrategic Targets

Absence of a formal policy framework for total debt management – split responsibilitiesInsufficient staff with the skills to undertake analysis; lack of analytical toolsAbsence, lack of access or unreliable access to developed financial markets

However, most debt managers have a good understanding of the risks that they face – implicitstrategies may address these risks

Reduced Share of External Reduced Share of External DebtDebt

Emerging Markets Sovereign Debt

-

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

1998 1999 2000 2001 2002 2003 2004 2005 2006F 2007F

% o

f G

DP

External Sovereign Debt Domestic Sovereign Debt

Source: JPMorgan

Risk Reduced: 12 Country CasesRisk Reduced: 12 Country Cases

Sovereign debt portfolio changes:

Seven increased domestic debt as share of total public debt, unchanged in three

Eight extended maturities of domestic debt, some considerably (although a few resorted to forced placement with public sector entities)

Source: Managing Public Debt: From Diagnostics to Reform Implementation, World Bank 2006

Clear Progress in Debt Portfolio Clear Progress in Debt Portfolio Composition …butComposition …but

A formal debt management strategy is important

What does this mean?A written document that provides a clear framework for all borrowing transactions and sets out a plan for the medium to long termIt is agreed by the Executive (Minister of Finance, Cabinet, as appropriate)

Why is it important?Reduces the opportunity for short-term fiscal expediency, at the cost of increased risk in the futureEnsures that debt management is not dominated by monetary policyAvoids conflicting “sub-strategies” for different components of the debt portfolioProvides coherence for domestic debt market developmentReduces risk of “supply driven” borrowingIt helps ensure that there is consistency in borrowing strategies

……Strategy Development Can be Strategy Development Can be GradualGradual

Codify and document existing approach – move from implicit to explicitRelatively simple analysis can provide very useful information for decision makersTailor the strategy to country circumstances – for some, a broad direction is a good start

All countries should have an explicit strategy to guide necessary decisions on the composition of the debt

2. Coordination between debt 2. Coordination between debt management and macroeconomic management and macroeconomic

policiespolicies

In an ideal world:

Fiscal policy is conducted within a medium-term framework – debt managers contribute to sustainability analysis, and help to reduce risks to the budget over the medium termMonetary policy and debt management are implemented with separate policy objectives and instrumentsCash management is implemented effectively and supports efficient public debt management

However, Significant Challenges However, Significant Challenges RemainRemain

Coordination with fiscal policy:Evidence of “fiscal dominance” in some countries, especially when public debt levels are high:• Reduce debt interest costs in the short run, but increase risk

Coordination with monetary policy:Separation of debt management and monetary policy difficult in practice for many countries especially when:• Central bank has extensive role in debt management due to weak capacity

in finance ministries; or• Underdeveloped debt market results in sharing of policy instruments.

Risk of policy conflict – credibility of monetary policy undermined or prudent management of government debt sacrificed• Situation is compounded if the central bank has a weak capital position,

e.g. large quasi-fiscal losses

As well as with Cash As well as with Cash ManagementManagement

Poor cash flow forecasting common in many countries, resulting in:

Limited scope for active cash management – debt managers have to time long-term debt issuance to meet short-term cash needs• Predictable calendar not possible for the primary market

Need for high precautionary cash balances – adds to costs when yield curve is positive

Implications for Reform Implications for Reform

A narrow focus on public debt management may miss key policy linkages – a broader program is mutually reinforcingOften need to work with “second best” alternatives, e.g.:• Use of agency agreements to clarify roles when debt

management remains in the central bank• Improved coordination when there are multiple issuers in the

government-risk debt market

3. Governance3. Governance

An effective governance structure is required to:

Ensure that a prudent debt management strategy is developed and adhered to: this is the most important element of public debt management.

Provide accountability - debt managers are responsible for sizeable portfolios with significant risks. The public and investors require assurance that these are well managed.

Increase predictability - disclosure of the borrowing program increases certainty for investors … and lowers the borrowing cost to the Government in the long-run.

Common IssuesCommon Issues

Legal frameworkMost countries meet the minimum requirement of clarifying who has the authority to borrow

• Although it may be scattered across a number of laws (different levels of authority for different types of borrowing)

Few countries have legislation that includes debt management objectives, and that sets out requirements for strategy development, reporting and evaluation

OrganizationManagement of public debt is often split across a number of entities –ministries of finance, central banks, economic and development ministries:

• Can make it difficult to develop an overall strategy, may be inefficient (duplication of resources, coordination costs), hamper accountability, reduce flexibility in choices of borrowing sources

• Institutional and organizational reform may be difficult to implement, but other approaches may be used such as coordination between groups to achieve key outputs, e.g. strategy development

Governance Issues: AccountabilityGovernance Issues: Accountability

ReportingPublic financial reporting (accounts) in many countries has little information on public debtSpecific reporting on public debt may be required under separate laws to compensate for thisMany countries produce substantial information on public debt, even if not required by law – outside sources of demand often the reason (e.g. rating agencies, investors)

AuditSpecialized nature of debt and related transactions may be a challenge for auditors

Operational RiskDocumentation of procedures and processes can reduce operational risk –mixed picture across countriesFew countries have specific codes of conduct for debt management staffAt the extreme, an absence of adequate procedures and due diligence can lead to fraud

4. Capacity4. Capacity

Recruiting, training and retaining staff with the appropriate skills mix for all aspects of modern public debt management remains a challenge for most countries

Accurate and comprehensive IT systems support efficient debt management and enable more advanced analysis – and yet few countries are fully satisfied with the existing systems

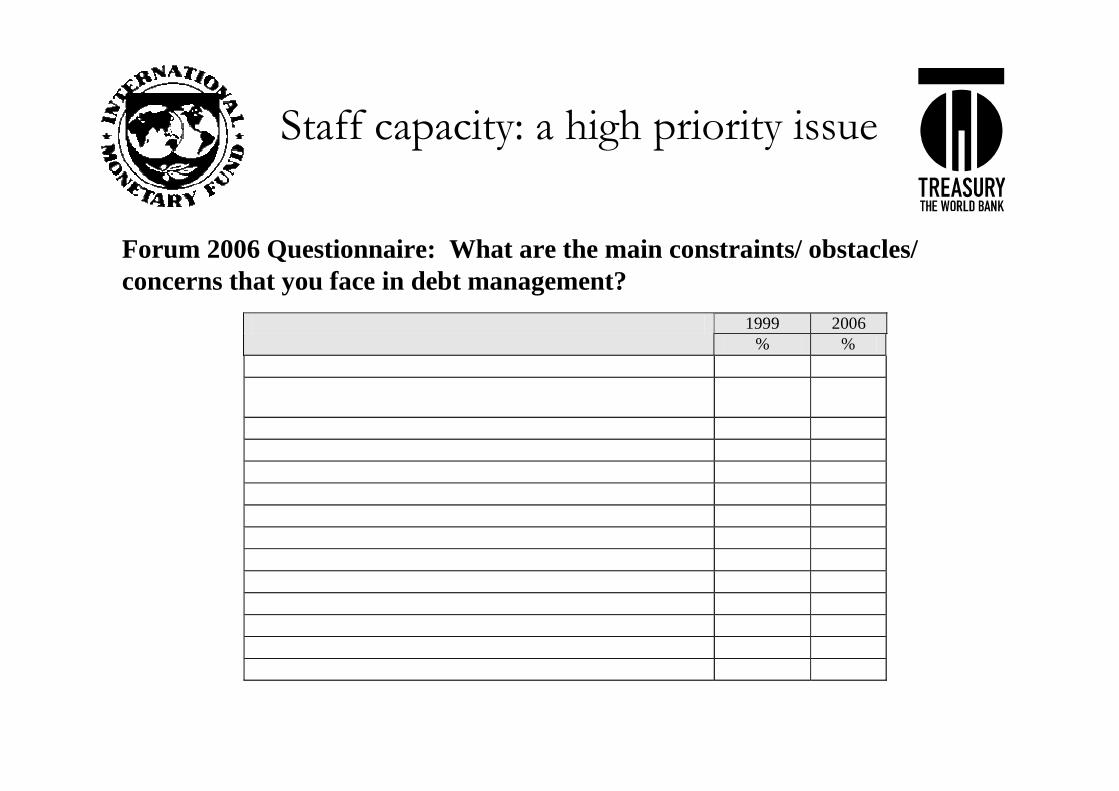

Staff capacity: a high priority issueStaff capacity: a high priority issue

1999 2006 % %

Institutional capacity: 51% 62% Lack of appropriate organizational arrangement with trained staff

31% 18%

Lack of middle-office analytical capacity and staff 12% 35% Back-office limitations 8% 9% Legal framework 6% 0% Macroeconomic risk 14% 9% Developing a deep and liquid local debt market 6% 21% Cost of funds 6% 0% Risk management: 15% 6% Funding risk 8% 6% Liquidity/refinancing risk 3% 0% Contingent liability risk 5% 0% Other 2% 3% Total 100% 100%

Forum 2006 Questionnaire: What are the main constraints/ obstacForum 2006 Questionnaire: What are the main constraints/ obstacles/ les/ concerns that you face in debt management?concerns that you face in debt management?

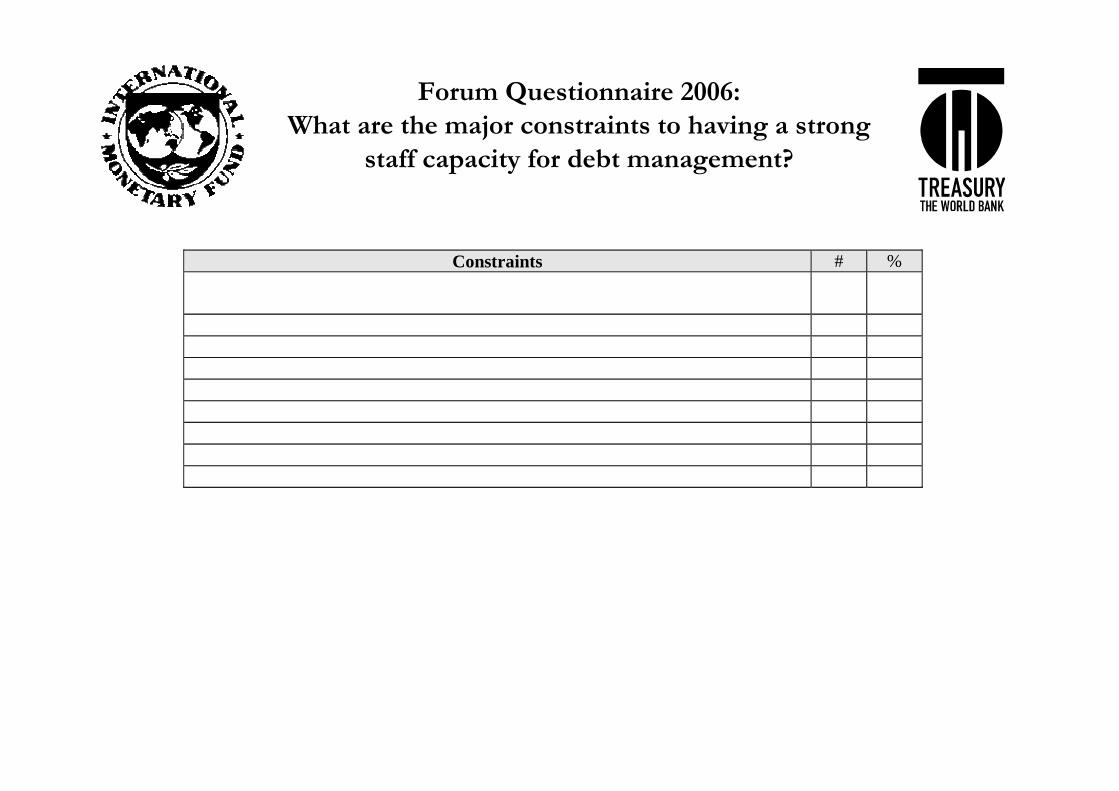

Forum Questionnaire 2006: What are the major constraints to having a strong

staff capacity for debt management?

Constraints # % Bureaucratic constraints (e.g. civil service laws/rules) that limit flexibility in recruitment

17 17

Difficulty in recruiting highly trained university graduates 13 13 Low salaries 22 22 High staff turnover to private sector and/or within the public sector 15 14 Low priority given to debt management by senior policy-makers 7 7 Lack of structured training programs 14 14 Lack of budget for training programs 10 9 Other (please specify) 4 4 Total 102 100

Forum Questionnaire 2006: Forum Questionnaire 2006:

How important is strengthening staff capacity for How important is strengthening staff capacity for public debt management in your country?public debt management in your country?

93 % High priority7 % Medium priority

Forum Questionnaire 2006: Forum Questionnaire 2006:

Which areas of expertise have priority in terms of Which areas of expertise have priority in terms of strengthening staff capacity for debt management?strengthening staff capacity for debt management?

26 % Capital markets, both external and domestic,and bond placement

11% Loan negotiation37% Front office issues

21% Risk identification and quantification11% Debt strategy design32% Middle office issues

11% Debt recording and statistics5% Debt transaction confirmation and registration

16% Back office issues

16% Legal documentation and analysis

Common issues in 12Common issues in 12--country country pilot programpilot program

Needs assessments in the 12 countries revealed some similarities:

• Public sector laws, rules and practices impeded the recruitment and retention of staff with the appropriate skill mix (limits onnumber of staff, new staff determined by personnel office, compulsory staff rotation policies, low salaries)

• High staff turnover, especially as staff gained skills and experience

• Paucity of training opportunities and inadequate budgets for training

Conclusions From the Conclusions From the 1212--country pilot programcountry pilot program

These findings are not unique to public debt management, and affect many other core functions in MoF and other parts of government.

First-best solution would be to focus on improving the quality of government services in general; but this is a long-term endeavour for many countries.

In the near and medium-term, countries have had to be more creative in order to attract and retain skilled staff. Public debt management is highly specialized business, requiring finance, macroeconomics and public sector skills.

Conclusions From 12Conclusions From 12--Country Pilot ProgramCountry Pilot Program

The mechanisms used to address these problems included:• On-the-job training and short-term external assignments• Limited but improved incentives for career progression• Use of existing public sector capacity-building programs and international

support networks• Use of resident advisors, external consultants and secondments from central

banks• Establishing islands of excellence or enclaves (infrequent)

All these mechanisms have their pros and cons have to be used judiciously and according to the best fit in each country given their specific needs.

Information Technology Information Technology SystemsSystems

A common issue is multiple IT systems – separate debt databases present integration problems and increase operational riskNew requirements may exceed capabilities of the existing systems – e.g. expanded domestic borrowing in a range of instruments, use of swap transactionsA full IT system development or acquisition is a significant management challenge – business processes should be reviewed firstSome countries have taken an approach of smaller steps –reduces risk and allows time to better assess longer-term business needs

5. Reforms and Capacity 5. Reforms and Capacity BuildingBuilding

A comprehensive diagnostic – including linkages with other policies and the governance environment – helps identify the nature of tradeoffs and develop realistic reform programs

More important to develop programs that are a ‘good fit’ rather than ‘best practice’

reform programs must reflect country-specific environment and priorities

As is the case for reforms in many areas, political commitment and an effective day-to-day leader of the process are required for successful implementation

Integrating debt management reforms into a broader agenda (e.g. public financial management or financial sector reforms) may assist with implementation