3 MARCH 2015 Sponsored by:

q Welcome (Remco de Vries) q Introduction (Lorcan Travers) q Speed dating sessions:

q Jason Straker (JPMorgan) q Jonathan Currie (HSBC) q Ryan McGrath (Cantor Fitzgerald) q Steve Lethaby (Clearstream)

q Q&A q Closing

Cash is King

• Cashflow is the lifeblood of business • Corporate Treasury principles of inves:ng surplus cash: – Safety – Liquidity – yield

Challenging Environment

Short Term

Investment

INCREASING REGULATION

NEGATIVE INTEREST

MARKET ACCESS

FLIGHT TO SAFETY

LOOSE MONETARY POLICY

FINANCIAL SECTOR

RECOVERY

Magic Pill?

• There is no one size fits all solu:on • There are a range of different products and service providers – Create awareness of the offerings – Develop an understanding of the products and markets – Find a combina:on that works

The Format

• “Speed Da:ng” Approach – 4 Speakers – Each Speaker is on :mer – Each Speaker highlights their area of exper:se in the alloXed :me

– Topics • Macroview …tbd • Tri – Party Repo • Fixed Income Investment • Money Markey Fund Solu:ons

The Speakers • Jason Straker, Por]olio Manager, Global Fixed Income & Liquidity,

JP Morgan Asset Management • Jonathon Currie, Head of Sales, Liquidity, EMEA,

HSBC Global Asset Management • Ryan McGrath, Head of Fixed Income Strategy Cantor Fitzgerald • Steve Lethaby, Senior Sales Manager, Global Securi:es Financing, Clearstream

IACT Breakfast Briefing

March 2015

Jason Straker, CFA Client Portfolio Manager Short-Term Fixed Income, J.P. Morgan Asset Management

9

Negative consequences of banking reform facing cash investors

n Basel III is now leading to US and European banks starting to make large non-operational deposits unattractive, and will soon actively withdrawal their service as a deposit taker

n Deposits will either move to smaller, less capitalized banks or to alternatives such as money market funds or repo

n The flow of capital, combined with money market reform, will make high quality, short term assets more scarce

n This supply and demand imbalance will only help to exacerbate low, and negative yields available in the market

n Sluggish growth in Europe shows no sign of abating

10

Looking for positive returns: The levers of risk

n Maturity: The length of time until investment is repaid

n Liquidity: The accessibility to the repayment

n Structure: The complexity of the investment

n Credit: The likelihood the investment is paid in full, on time.

FOR INSTITUTIONAL/WHOLESALE OR PROFESSIONAL CLIENT USE ONLY | NOT FOR RETAIL USE DISTRIBUTION

STRICTLY PRIVATE | CONFIDENTIAL

Accurately forecasting and segmenting your cash

11

When cash is properly segmented by liquidity needs and risk profile, investment opportunities can be fully optimized.

OPTIMIZE operating cash

REDUCE borrowing costs

ENHANCE investment returns

REVIEW FORECAST SEMI-ANNUALLY

RE-BALANCE ALLOCATIONS AS NEEDED

ASSESS CASH FLOWS AND SEGMENT BALANCES

ALIGN CASH SEGMENTS IN TERMS OF LIQUIDITY NEED AND RISK TOLERANCE FO

RE

CA

ST

For illustrative purposes only

FOR INSTITUTIONAL/WHOLESALE OR PROFESSIONAL CLIENT USE ONLY | NOT FOR RETAIL USE DISTRIBUTION

STRICTLY PRIVATE | CONFIDENTIAL

Offering a spectrum of short-term strategies

12

We partner to solve your unique investment objectives across the time horizon.

Liquidity Managed Reserves Short Duration

Objectives

Capital preservation Liquidity

Seek superior performance

Low volatility of principal Liquidity

Seek superior performance

Effective credit and duration

management Seek superior performance

Maximum maturity of individual securities (credit) 13 months 3 years 5 years

Maximum maturity of individual securities (gvt/agency) 2 years 3 years 5 years

Maximum duration 90 days (WAM) 1 year 3 years

Average credit quality A-1 or P-1 AA-/or Aa3 AA- or Aa3

Investment universe: Money markets X X X

Asset-backed securities X (ABCP only) X* X*

A corporates X X X

Mortgages – – X*

BBB corporates – X* X*

* Optional for separately managed portfolios. ** Used as a risk management tool in the respective mutual fund strategies; optional for separately managed portfolios. The manager seeks to achieve the stated objective. There can be no guarantee it will be achieved.

FOR PROFESSIONAL INVESTORS ONLY. NOT FOR RETAIL USE OR DISTRIBUTION. This document has been produced for information purposes only and as such the views contained herein are not to be taken as an advice or recommendation to buy or sell any investment or interest thereto. Reliance upon information in this material is at the sole discretion of the reader. Any research in this document has been obtained and may have been acted upon by J.P. Morgan Asset Management for its own purpose. The results of such research are being made available as additional information and do not necessarily reflect the views of J.P.Morgan Asset Management. Any forecasts, figures, opinions, statements of financial market trends or investment techniques and strategies expressed are unless otherwise stated, J.P. Morgan Asset Management’s own at the date of this document. They are considered to be reliable at the time of writing, may not necessarily be all-inclusive and are not guaranteed as to accuracy. They may be subject to change without reference or notification to you. Both past performance and yield may not be a reliable guide to future performance and you should be aware that the value of securities and any income arising from them may fluctuate in accordance with market conditions. There is no guarantee that any forecast made will come to pass. J.P. Morgan Asset Management is the brand name for the asset management business of JPMorgan Chase & Co and its affiliates worldwide. You should note that if you contact J.P. Morgan Asset Management by telephone those lines may be recorded and monitored for legal, security and training purposes. You should also take note that information and data from communications with you will be collected, stored and processed by J.P. Morgan Asset Management in accordance with the EMEA Privacy Policy which can be accessed through the following website http://www.jpmorgan.com/pages/privacy. Issued in Continental Europe by JPMorgan Asset Management (Europe) Société à responsabilité limitée, European Bank & Business Centre, 6 route de Trèves, L-2633 Senningerberg, Grand Duchy of Luxembourg, R.C.S. Luxembourg B27900, corporate capital EUR 10.000.000. Issued in the UK by JPMorgan Asset Management (UK) Limited which is authorized and regulated by the Financial Conduct Authority. Registered in England No. 01161446. Registered address: 25 Bank St, Canary Wharf, London E14 5JP, United Kingdom.

13

Disclaimer

IACT Presenta:on

CANTOR FITZGERALD IRELAND MARCH 2015

About Cantor Fitzgerald Ireland

15

• Cantor Fitzgerald acquired Dolmen Stockbrokers in December 2012

• Cantor Fitzgerald Ireland were recognised as a primary dealer of Irish Government bonds in June 2013

• Cantor Fitzgerald Ireland traded more €6.5 billion Irish sovereign bonds in 2014, co-‐marketed in Europe and in the US with the NTMA in advance of debt issuance

• Cantor Fitzgerald Ireland was mandated by Allied Irish Bank as a principle on its last senior unsecured bond issue

• There are ten members of the fixed income team offering access to domes:c and global bond markets

• A two member money market and repo desk, offering access to the interna:onal inter bank market

• Easy ‘line set up’ with dedicated point of contacts

Irish Bond Ratings and Performance

16

• Irish Ra:ngs

• Irish Bond Performance

-5%

0%

5%

10%

15%

20%

25%

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14

Irish 2-Year Yield

Moody's downgradeto sub-‐ investment

EU/IMF programmeexit

LTROannounced by ECB

EU/IMFProgramme

OMTannounced

Rating Outlook Next Action DateMOODY Baa1 STABLE May 15th

STANDARD & POOR's A STABLE June 5th FITCH A-‐ STABLE August 7th

Cantor Fitzgerald – Irish Direct Investment Opportuni:es

17

• The NTMA since returning to bond markets have issued across the yield curve • The NTMA’s short-‐term debt programme, comprises of Treasury Bills, Commercial

Paper and Exchequer Notes • Treasury Bills are issued primarily through an auc:on system. Par:cipa:on in auc:ons

is limited to recognised primary dealers in Irish Government Bonds

Source: Bloomberg

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

1 2 3 4 5 6 7 8 9 10 15

Yiel

d

Yrs

Irish Soveriegn Yield Curve Shift over 1y

Ire 23/01/2014 IRE 23/01/2015

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Germany France Belgium Ireland Spain Italy Portugal

10-year Yields

Cantor Fitzgerald Ireland – Financials

18

Irish Bank Covered Bonds • Secured on a pool of assets

• Liquid instruments, trade freely on the secondary market

European Bank Financials • Cantor Fitzgerald offers direct access to any short dated European Financial

names

RatingBank of Ireland Mortgage Bank MOODY 's A1

DBRS A

AIB Mortage Bank MOODY's A3STANDARD & POOR's A

Fitch A

Cantor Fitzgerald – US Direct Investment Opportunities

19

• Cantor Fitzgerald are in the top quar:le in terms of turnover out of 21 primary

dealers in US treasury bonds

• Cantor Fitzgerald Ireland can directly facilitate access to US Treasury bonds and short dated T-‐Bills

• Cantor Fitzgerald sponsors a short term note issuance program where it issues “fully-‐supported” asset-‐backed commercial paper (“ABCP”) rated A-‐1 and Prime-‐1 (by S&P and Moody’s, respec:vely) to money market investors

• Currently has approximately $2.25 billion in commercial paper notes outstanding

Contact Details

20

Ryan Mc Grath : Head of Fixed Income Strategy Telephone : (1) 6333898 E Mail : [email protected] Liam Dorgan : European Bond Sales Telephone : (1) 6333668 E Mail : [email protected] Morgan O’Sullivan : Head of Debt Origina:on Telephone : (1) 6333829 E Mail: [email protected]

21

Disclaimer

Regulatory Information

Cantor Fitzgerald Ireland Ltd, (CFIL), is regulated by the Central Bank of Ireland. Cantor Fitzgerald Ireland Ltd is a member firm of the Irish Stock Exchange and the London Stock Exchange.

This report has been prepared by CFIL for information purposes only and has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The report is not intended to and does not constitute personal recommendations/investment advice nor does it provide the sole basis for any evaluation of the securities discussed. Specifically, the information contained in this report should not be taken as an offer or solicitation of investment advice, or encourage the purchased or sale of any particular security. Not all recommendations are necessarily suitable for all investors and CFIL recommend that specific advice should always be sought prior to investment, based on the particular circumstances of the investor.

Although the information in this report has been obtained from sources, which CFIL believes to be reliable and all reasonable efforts are made to present accurate information CFIL give no warranty or guarantee as to, and do not accept responsibility for, the correctness, completeness, timeliness or accuracy of the information provided or its transmission. Nor shall CFIL, or any of its employees, directors or agents, be liable to for any losses, damages, costs, claims, demands or expenses of any kind whatsoever, whether direct or indirect, suffered or incurred in consequence of any use of, or reliance upon, the information. Any person acting on the information contained in this report does so entirely at his or her own risk.

All estimates, views and opinions included in this report constitute CFIL’s judgment as of the date of the report but may be subject to change without notice. Changes to assumptions may have a material impact on any recommendations made herein.

Unless specifically indicated to the contrary this report has not been disclosed to the covered issuer(s) in advance of publication.

Past performance is not a reliable guide to future performance. The value of your investment may go down as well as up. Investments denominated in foreign currencies are subject to fluctuations in exchange rates, which may have an adverse affect on the value of the investments, sale proceeds, and on dividend or interest income. The income you get from your investment may go down as well as up. Figures quoted are estimates only; they are not a reliable guide to the future performance of this investment It is noted that research analysts' compensation is impacted upon by overall firm profitability and accordingly may be affected to some extent by revenues arising other CFIL business units including Fund Management and Stock broking. Revenues in these business units may derive in part from the recommendations or views in this report. Notwithstanding, CFIL is satisfied that the objectivity of views and recommendations contained in this report has not been compromised. CFIL permits staff to own shares and/ or derivative positions in the companies they disseminate or publish research, views and recommendations on. Nonetheless CFIL is satisfied that the impartiality of research, views and recommendations remains assured.

This report is only provided in the US to major institutional investors as defined by s.15 a-6 of the Securities Exchange Act, 1934 as amended. A US recipient of this report shall not distribute or provide this report or any part thereof to any other person.

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Triparty Repo – The benefit for Corporate Treasurers IACT breakfast briefing – 3rd March 2015

Steve Lethaby - Clearstream GSF Senior Sales Manager for UK, Ireland and South Africa

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

23

Who are Clearstream?

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

- We are AA rated European bank and a neutral service provider.

- We have the strength of Deutsche Börse Group behind us.

- We’ve been offering award winning triparty repo services for over 20 years.

- We have wholesale access to 53 markets worldwide and over EUR 12 trillion of assets.

- Over 475 companies already use our triparty services including central banks, commercial banks, asset managers, corporates

- EUR 650 billion managed daily within our triparty programme

24 6 July 2015

Triparty for Corporate Treasurers Who are Clearstream

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 25

Triparty for Corporate Treasurers Why is collateral important to Treasurers?

Why is collateral becoming important for Treasurers: ‒ Reduction of

unsecured activities

‒ Threat of bail-in risk

‒ Money market fund reform

‒ The ability to re-use collateral within the programme

‒ Basel III and the evolving needs of financial institutions

Counterparty risk

Access to collateral

Operational burden Automated solutions

Counterparty diversification

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 26

Triparty for Corporate Treasurers What are repos?

Repos are a secured form of money market instrument: ‒ ‘Repo’ is the

abbreviated term for repurchase agreement.

‒ A repo (or reverse repo) transaction sees a counterparty sell securities and agree to buy them back at a pre-determined date.

Cash Provider (Collateral Receiver)

Cash Taker (Collateral

Giver) Delivery of securities vs

cash principal

Day 1

Cash Provider (Collateral Receiver)

Cash Taker (Collateral

Giver) Return of securities vs

cash principal plus accrued interest

Day T + n

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 27

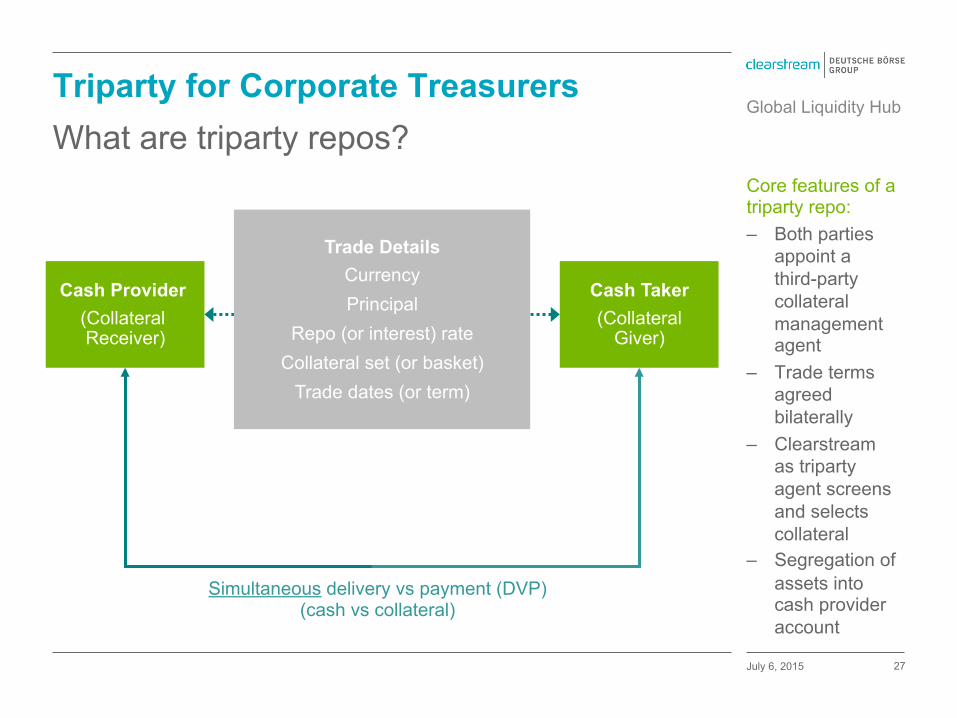

Triparty for Corporate Treasurers What are triparty repos?

Core features of a triparty repo: ‒ Both parties

appoint a third-party collateral management agent

‒ Trade terms agreed bilaterally

‒ Clearstream as triparty agent screens and selects collateral

‒ Segregation of assets into cash provider account

Cash Provider (Collateral Receiver)

Cash Taker (Collateral

Giver)

Trade Details Currency Principal

Repo (or interest) rate Collateral set (or basket)

Trade dates (or term)

Simultaneous delivery vs payment (DVP) (cash vs collateral)

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 28

Triparty for Corporate Treasurers How do I start a triparty repo relationship?

Legals

Baskets

Trade

- A triparty repo relationship can be started using the

following five easy steps:

- Appoint a collateral management agent

- Sign legal agreements with your counterparty: - Either separate bilateral terms (GMRA) and

triparty agreement - Or an ‘all-in-one’ document - Collateral

Management Service Agreement (CMSA) and Clearstream Repurchase Conditions (CRC’s)

- Agree and set up your collateral eligibility criteria - Confirm operational requirements and treasury SSIs - Open the triparty account and trade!

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 29

Triparty for Corporate Treasurers How do CRC’s differ from GMRA’s?

The difference is in the approach: ‒ GMRA’s are

individually negotiated between parties

‒ GMRA’s don’t include any triparty repo provisions

‒ CRC’s are standardized and multi-lateral

‒ CRC’s + CMSA are an ‘all in one’ triparty repo agreement

CG

CR

Clearstream Repurchase Conditions

(CRC’s) +

Collateral Management Service Agreement

(CMSA)

CG

CR

CR CR

CG CG

CG CG

CR CR

GMRA GMRA GMRA

GMRA GMRA GMRA

GMRA GMRA GMRA

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 30

Triparty for Corporate Treasurers What type of securities are eligible?

How to set up a basket of collateral: ‒ Only select

the assets that fit your risk appetite (‘SLY’)

‒ Set up single basket or multiple baskets to cover different investment scenarios

‒ Daily mark-to-market of assets

‒ Daily eligibility monitoring

Government Bonds

Corporate Bonds

Equities Funds

Security, Liquidity, Yield (‘SLY’) ü Credit ratings ü Countries / Indices ü Currencies ü Concentration limits ü Price age ü …..and more

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 31

Triparty for Corporate Treasurers Benefits

The ‘4 Cs’ help you to reduce counterparty risk: ‒ Secured

investment through use of collateral

‒ An alternative to other money market products

‒ Use of a reputable third-party custodian

‒ You control the collateral requirements and trade terms

Cash Counterparty

Collateral Clearstream

R 51 G 153 B 153

R 102 G 102 B 102

R 0 G 0 B 0

R 0 G 0

B 153

R 95 G 55

B 153

R 191 G 34

B 150

R 224 G 0

B 52

R 255 G 102

B 0

R 255 G 204

B 0

R 119 G 183

B 0

R 0 G 199 B 139

R 0 G 165 B 192

Global Liquidity Hub

July 6, 2015 32

Triparty for Corporate Treasurers Other key factors

‒ Use Clearstream’s own portal to manage all activities ‒ Process trades via Bloomberg, 360T plus more ‒ Full end-to-end integration based upon SWIFT format

messaging possible

Default management

System integration

Costs

‒ Immediate access to the collateral if your counterparty defaults

‒ Ability to liquidate or re-finance assets through your own house bank or broker

‒ The golden rule of triparty – ‘the collateral giver pays’

‒ No set-up costs at Clearstream

‒ Free ‘marriage broking service’ and access to innovative services such as Clearstream’s CRCs

Steve Lethaby – Senior Sales Manager UK, Ireland and South Africa Tel - +44 (0)207-862-7133 Email - [email protected]

Dates for your diary: Ø 10 September - Dublin Staff Relay Ø 2 October - IACT Annual Dinner Ø 19 November – IACT Annual Conference

Update from the IACT: Ø EMIR consultation Central Bank Ø BEPS consultation OECD