SRT510 Business Case Studies

Financial Statements: Income Statement

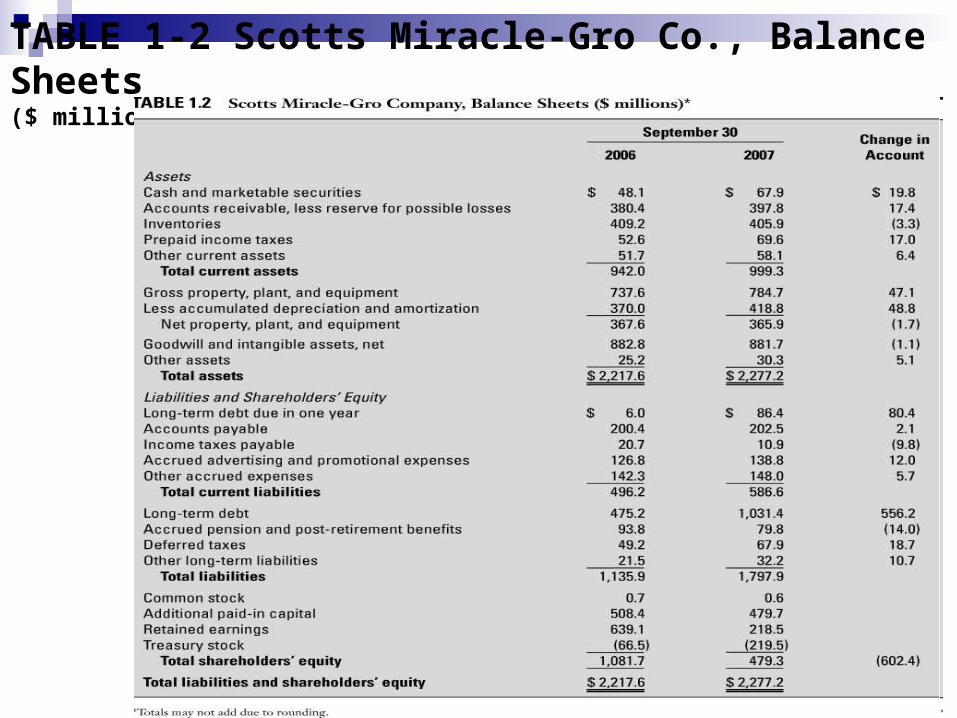

TABLE 1-2 Scotts Miracle-Gro Co., Balance Sheets ($ millions)

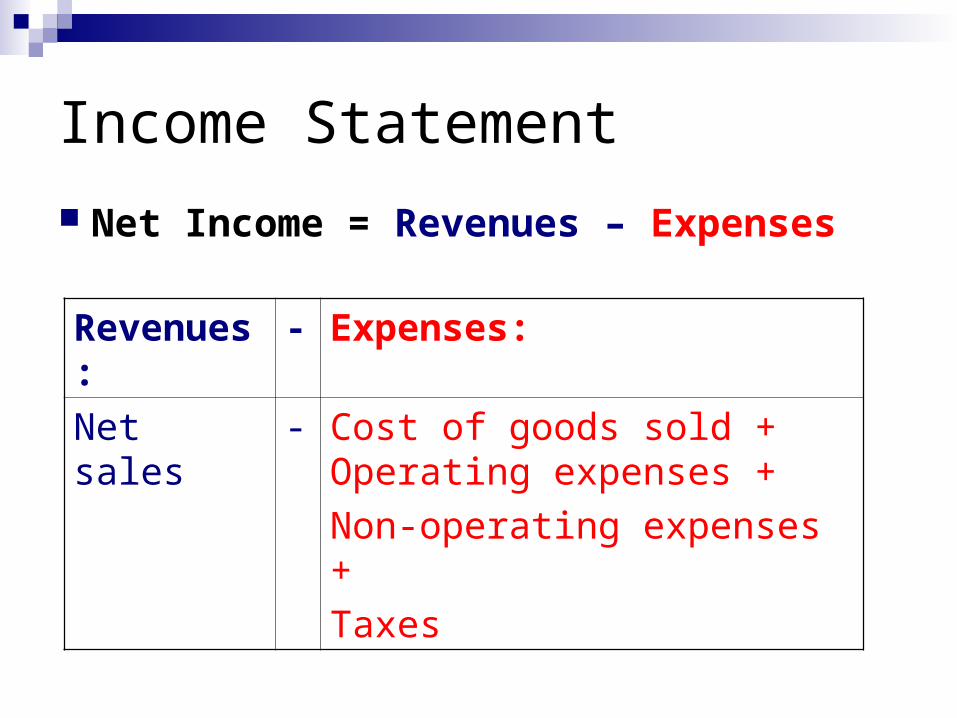

Income Statement

Net Income = Revenues – Expenses

Revenues: - Expenses:

Net sales - Cost of goods sold +Operating expenses +

Non-operating expenses +

Taxes

Understanding the Income Statement

Net Income sometimes called:(net) earnings(net) profits

Net Sales sometimes called:(net) revenues

Cost of goods sold sometimes called:cost of sales

TABLE 1-3 Scotts Miracle-Gro Co., Income Statement ($ millions)

Revenues – Expenses

Understanding the Income Statement Accrual Accounting

(aka “A Cruel Accounting)” Recognize the revenue “as soon as the effort

required to generate the sale is substantially complete and there is reasonable certainty that payment will be received”

For credit sales…the “sale” might come significantly before the payment

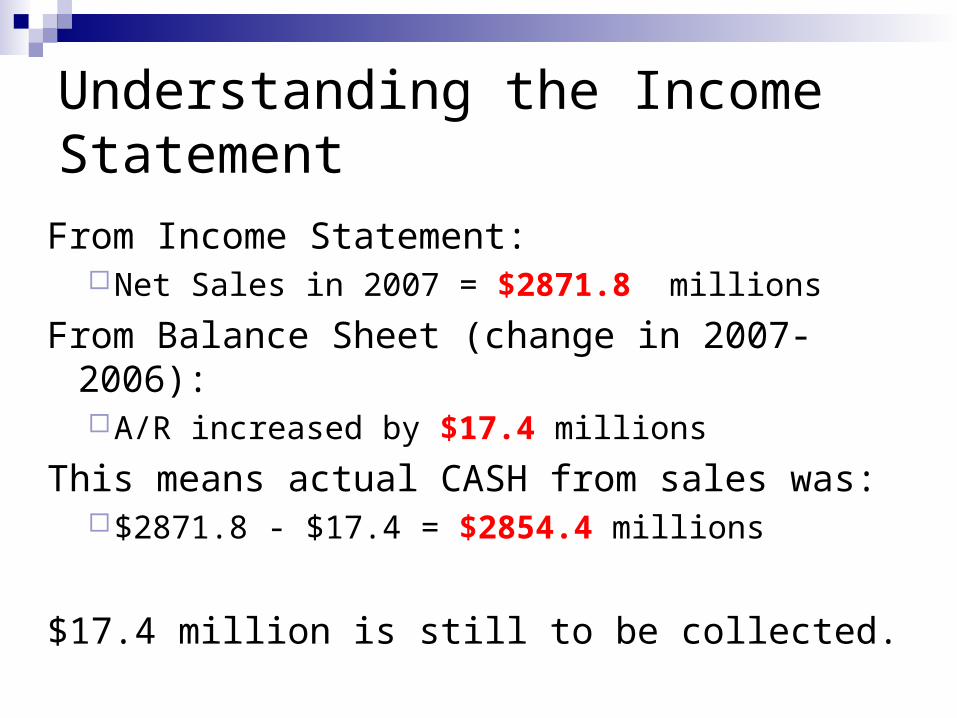

Understanding the Income Statement

From Income Statement:Net Sales in 2007 = $2871.8 millions

From Balance Sheet (change in 2007-2006):A/R increased by $17.4 millions

This means actual CASH from sales was:$2871.8 - $17.4 = $2854.4 millions

$17.4 million is still to be collected.

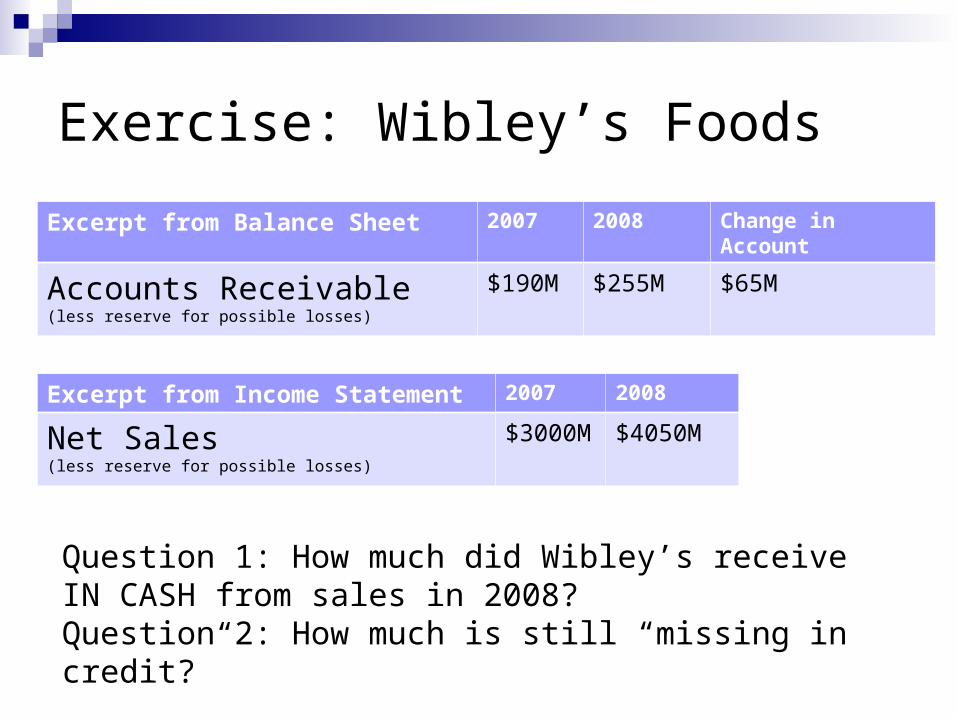

Exercise: Wibley’s Foods

Excerpt from Balance Sheet 2007 2008 Change in Account

Accounts Receivable (less reserve for possible losses)

$190M $255M $65M

Excerpt from Income Statement 2007 2008

Net Sales(less reserve for possible losses)

$3000M $4050M

Question 1: How much did Wibley’s receive IN CASH from sales in 2008?Question 2: How much is still “missing in credit?”

Understanding the Income Statement Depreciation

Build a new facility for $50million in 2009 If entire cost is assigned to 2009 (as an

expense), what does that do to financial results for 2009?

Depreciation allows “evening out”: allocate past expenses to future periods

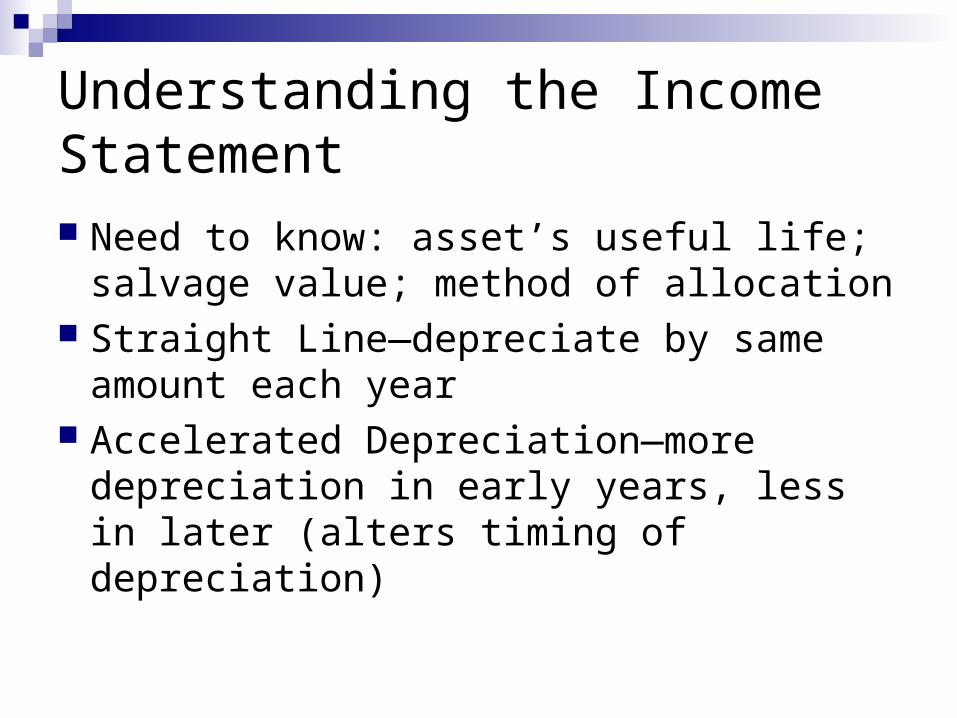

Understanding the Income Statement Need to know: asset’s useful life; salvage

value; method of allocation Straight Line—depreciate by same amount

each year Accelerated Depreciation—more

depreciation in early years, less in later (alters timing of depreciation)

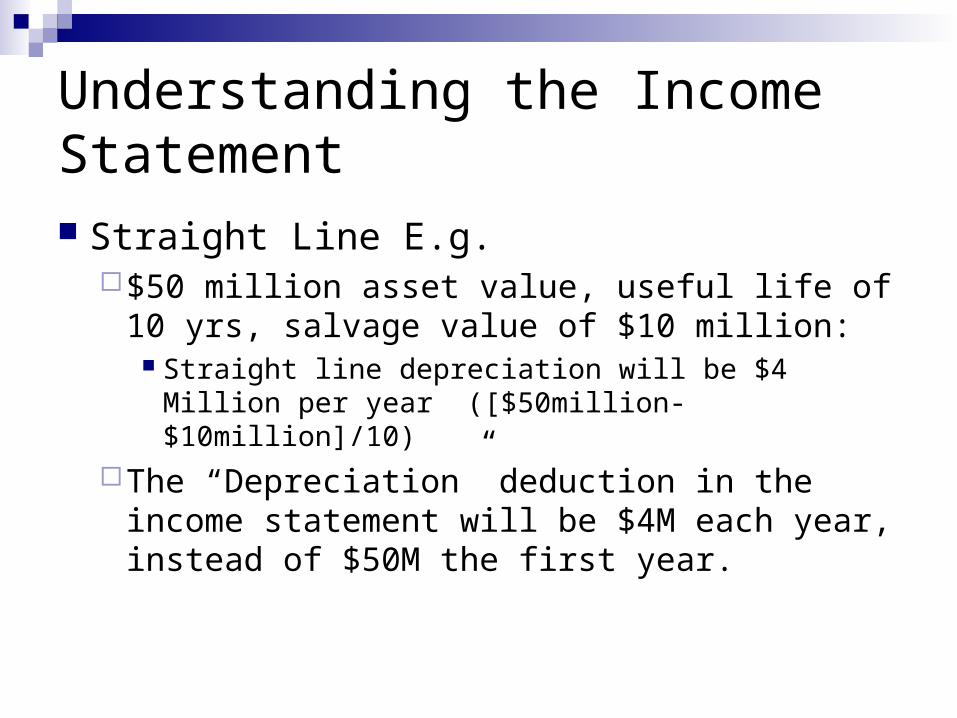

Understanding the Income Statement Straight Line E.g.

$50 million asset value, useful life of 10 yrs, salvage value of $10 million:

Straight line depreciation will be $4 Million per year ([$50million-$10million]/10)

The “Depreciation” deduction in the income statement will be $4M each year, instead of $50M the first year.

Understanding the Income Statement What does depreciation method chosen

mean?Straight line might tend to overstate earningsAccelerated might tend to understate earnings

Reporting Taxes: Be Aware

For shareholders: Accurately portray performance

For government Minimize tax payable (e.g. rapid depreciation)

This means actual tax payments may differ from “provision for

taxes” on income statement

“Enough said” We aren’t going to get into this. But be aware that

how taxes are handled can create a “false” picture of performance.

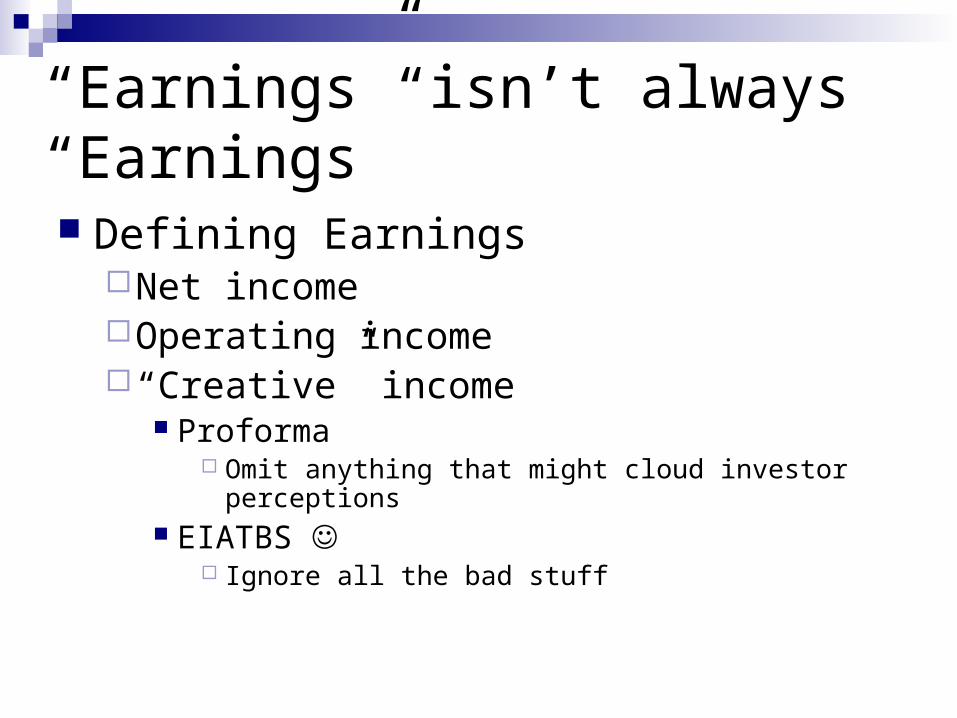

“Earnings” isn’t always “Earnings”

Defining EarningsNet incomeOperating income“Creative” income

Proforma Omit anything that might cloud investor perceptions

EIATBS Ignore all the bad stuff

Exercise

Explain what this means:

“Financial statements are like fine perfume; to be sniffed but not swallowed”

- Abraham Brilloff