Strategic sectors and niche opportunitiesMedAlliance Round Table – Thursday 8 October 2009, MarseilleMedAlliance Round Table Thursday 8 October 2009, Marseille

Studies conducted by Emmanuel Noutary, Jeanne Lapujade, Pierre Henry, ANIMA Investment NetworkContributions by ANIMA staff and Investment Promotion Agencies

www.invest-in-med.euwww.invest-in-med.euOct 09 © ANIMA-Invest in Med 1

Matching public priorities & investors’ targetsMatching public priorities & investors targets

A id b k i i MED25 fi h i h k t b i A guide book reviewing MED sectoral & territorial investment policies

25 fiches on niches markets being developed today in the Mediterranean (9 MED countries mainly)

ETUDE N° 7 / Octobre 2009Version de travailée

édite

rrané

vest

ir en

M

La carte des investissements en Méditerranée

Guide sectoriel à travers les politiques publiques

pour l’investissement en Méditerranée

Allia

nce

Inv

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 2

MED

-A

Towards an economic atlas of the MediterraneanTowards an economic atlas of the Mediterranean

Offer the Mediterranean ergonomic and reactive informative Offer the Mediterranean ergonomic and reactive informative tools to guide enterprises in the region Influence the location decision of investors

Aggregate the economic zones database (investment map) with the foreign direct investment database (MIPO)the foreign direct investment database (MIPO) Develop an economic Geographic Information System for Invest in

Med

Put up a network of players within the MedAlliance in charge of updating the datasp g Info on public policies and infrastructure by administrations Info on markets, sectors and players by CCI and Biz Feds

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 3

The current positioning of the MediterraneanThe current positioning of the Mediterranean Still important needs, numerous opportunities

The catching p on inf ast ct es is still ongoing The catching up on infrastructures is still ongoing Med countries remain competitive destinations

A number of value chains in which gaps are to be filled: A number of value chains in which gaps are to be filled: Traditional businesses re-inventing themselves:

The Euro-African logistic hub Agri-food: producers, transformers and technologies A new textile positioning: Short fashion and special fabrics Diversification in tourism to serve a new economic development C t ti dd i l d d Construction: addressing real demand

New businesses being built from (almost) scratch An ICT positioning on its way BPO & new services to businesses Health industries Renewable Energies

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 4

8 market segments in the spotlight of investors emblematic of 9 Med countries development strategies

Animal health opportunitiesR&D ( tibi ti & i f fi h lt lt t ) d

A growing market with less barriers to entry than in human health

R&D (antibiotics & vaccine for fish culture, poultry, etc.), drugsmanufacturing, rural distribution, veterinary equipement

A growing market with less barriers to entry than in human health Booming global animal health market since 2000 (Vetnosis): USD 19.2 bn in 2007. Huge

growth potential in emerging markets: meat consumption & pet care. Markets: regional sheep, cows & poultry breeders, agrofood industries, pet doctors. Markets: regional sheep, cows & poultry breeders, agrofood industries, pet doctors.

MED: existing production capacities ready to gear up! R&D is weak in spite of specific MED pathologies (West Nile fever, Rift Valley fever, etc.),

but development costs are relatively lower & production can be competitive (underbut development costs are relatively lower & production can be competitive (under license or not). See for instance Pfizer Egypt or CEVA Santé Animale in Rabat.

Growth fostered by public initiatives: strengthening of veterinary prophylactic obligations + gradual liberalisation of distribution & importation (Tunisia 2010-11) +

f t f IPR (WTO’ TRIPS)enforcement of IPR (WTO’s TRIPS).

Getting closer to promising markets though JVs or greenfield projects Foreign SMEs and majors joining forces with local skills & capital: Algerian Animal Health

P d ABIC Bi l i l L b i i I l Af i d i T i i J d ’ A di & iProduct, ABIC Biological Laboratories in Israel, Afrimed in Tunisia, Jordan’s Acdima & its subsidiaries in Syria, Egypt, Algeria, etc. See 2009 deal between French Mérial and Morocco’s MCI Santé Animale for the production of bacterial vaccines in Casablanca.

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 5

Growth factors : meat consumption patterns, non-tariff trade bareers for exports, traceability, harmonization of industrial norms

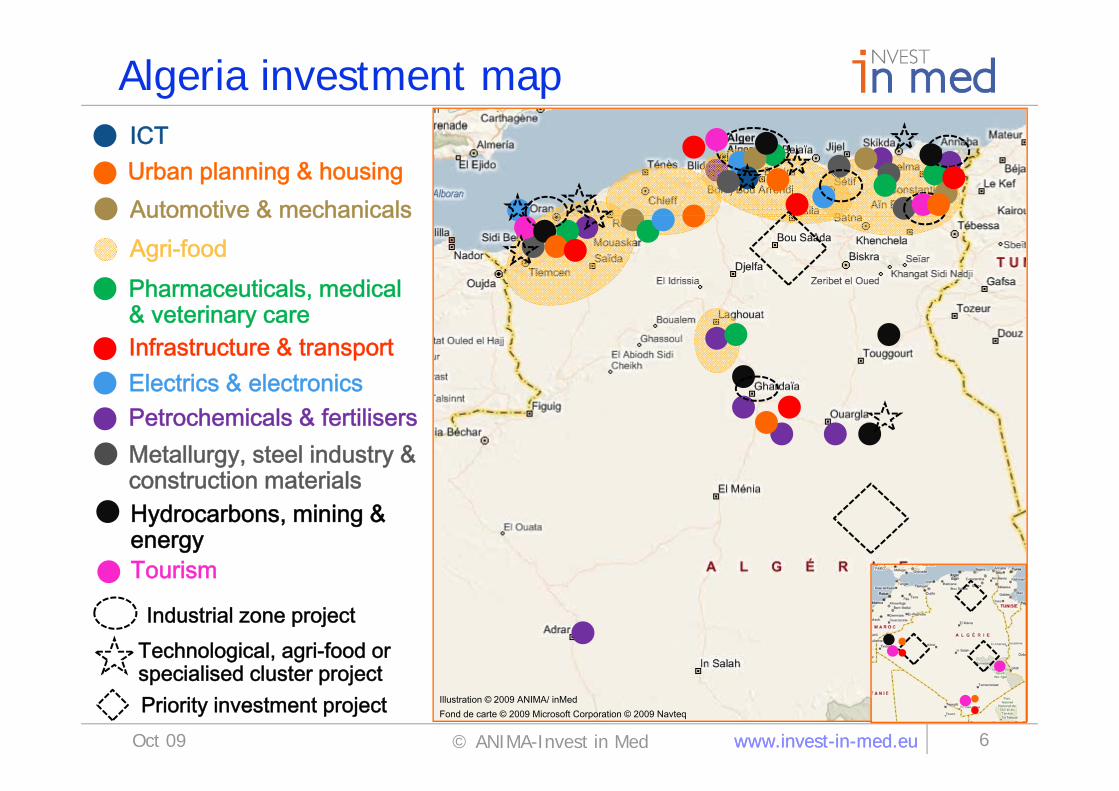

Algeria investment mapICTUrban planning & housingAutomotive & mechanicalsAutomotive & mechanicalsAgri-foodPharmaceuticals, medical & t i& veterinary careInfrastructure & transportElectrics & electronics

Metallurgy, steel industry & construction materials

Petrochemicals & fertilisers

Hydrocarbons, mining & energy

construction materials

Tourism

Industrial zone projectTechnological, agri-food or

Tourism

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 6

Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

Oct 09

Priority investment projectspecialised cluster project

Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

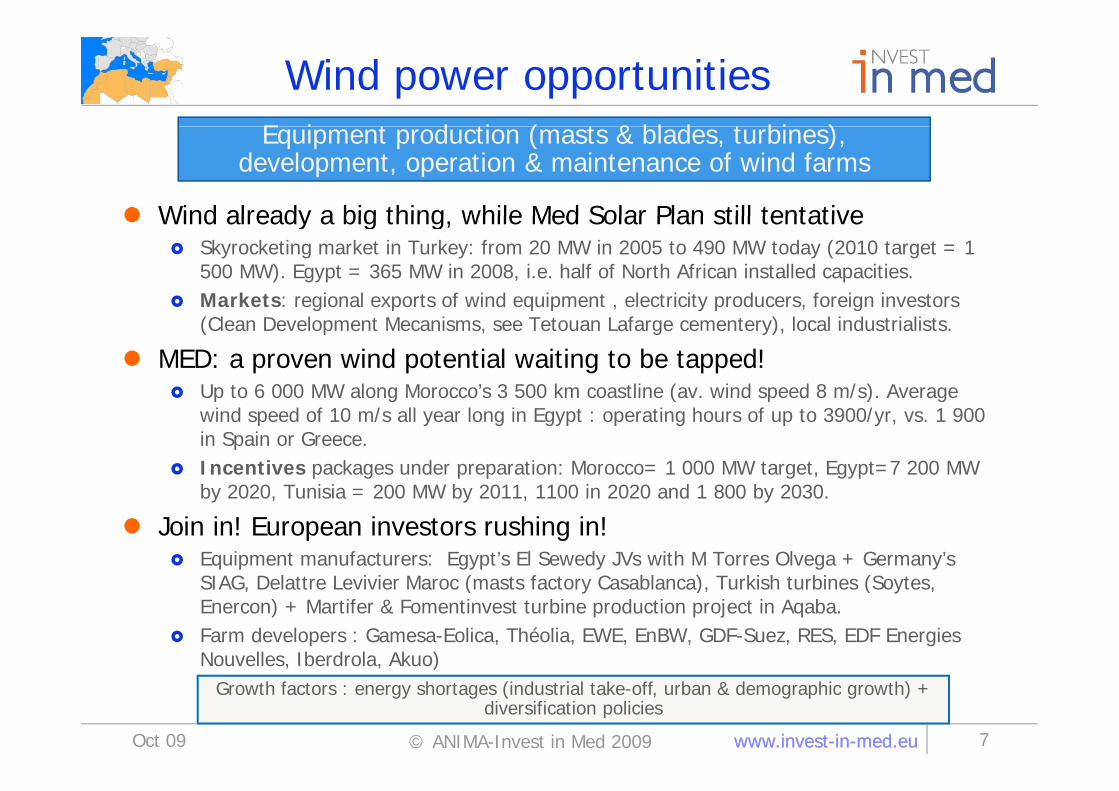

Wind power opportunitiesE i t d ti ( t & bl d t bi )

Wind already a big thing while Med Solar Plan still tentative

Equipment production (masts & blades, turbines), development, operation & maintenance of wind farms

Wind already a big thing, while Med Solar Plan still tentative Skyrocketing market in Turkey: from 20 MW in 2005 to 490 MW today (2010 target = 1

500 MW). Egypt = 365 MW in 2008, i.e. half of North African installed capacities. Markets: regional exports of wind equipment , electricity producers, foreign investors Markets: regional exports of wind equipment , electricity producers, foreign investors

(Clean Development Mecanisms, see Tetouan Lafarge cementery), local industrialists.

MED: a proven wind potential waiting to be tapped! Up to 6 000 MW along Morocco’s 3 500 km coastline (av. wind speed 8 m/s). Average Up to 6 000 MW along Morocco s 3 500 km coastline (av. wind speed 8 m/s). Average

wind speed of 10 m/s all year long in Egypt : operating hours of up to 3900/yr, vs. 1 900 in Spain or Greece.

Incentives packages under preparation: Morocco= 1 000 MW target, Egypt=7 200 MW b 2020 T i i 200 MW b 2011 1100 i 2020 d 1 800 b 2030by 2020, Tunisia = 200 MW by 2011, 1100 in 2020 and 1 800 by 2030.

Join in! European investors rushing in! Equipment manufacturers: Egypt’s El Sewedy JVs with M Torres Olvega + Germany’s

SIAG D l L i i M ( f C bl ) T ki h bi (SSIAG, Delattre Levivier Maroc (masts factory Casablanca), Turkish turbines (Soytes, Enercon) + Martifer & Fomentinvest turbine production project in Aqaba.

Farm developers : Gamesa-Eolica, Théolia, EWE, EnBW, GDF-Suez, RES, EDF Energies Nouvelles, Iberdrola, Akuo)

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009

Nouvelles, Iberdrola, Akuo)

Oct 09 7

Growth factors : energy shortages (industrial take-off, urban & demographic growth) + diversification policies

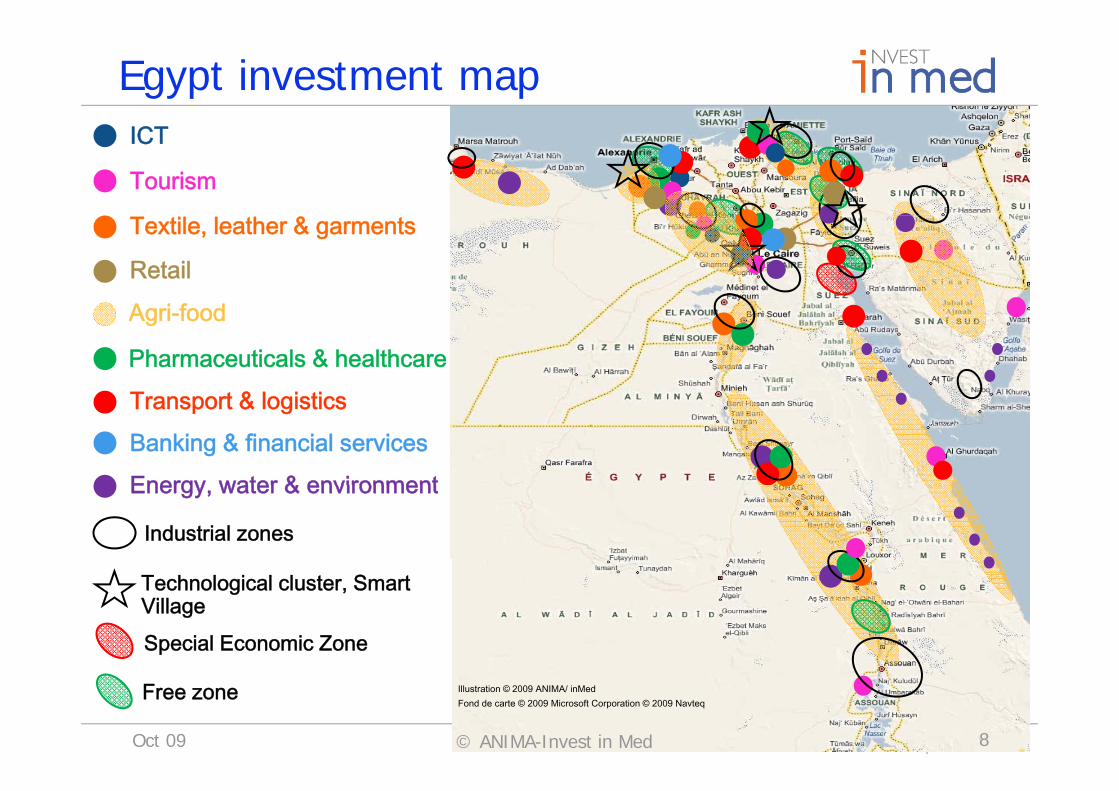

Egypt investment mapICT

Tourism

Textile, leather & garments

Retail

A i f dAgri-food

Pharmaceuticals & healthcare

T t & l i tiTransport & logisticsBanking & financial servicesEnergy water & environmentEnergy, water & environment

Industrial zones

T h l i l l S

Special Economic Zone

Technological cluster, Smart Village

www.invest-in-med.euwww.invest-in-med.eu 8

Free zone

Oct 09 © ANIMA-Invest in Med

Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

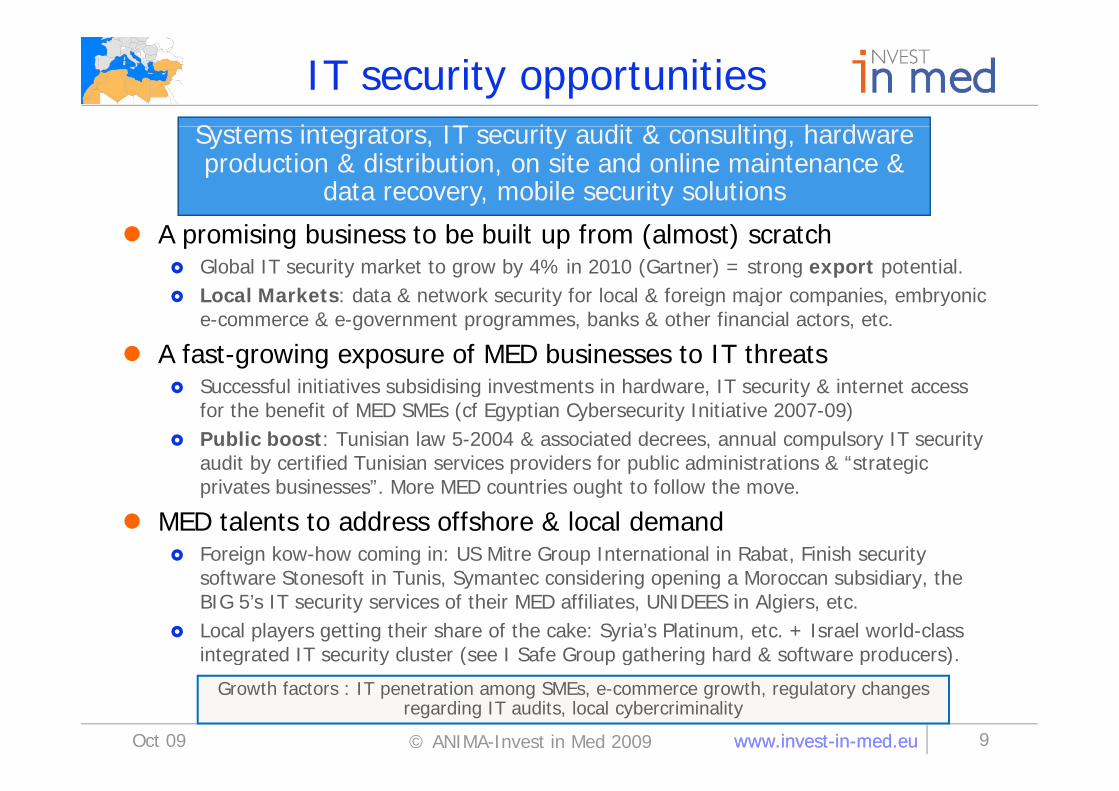

IT security opportunitiesS t i t t IT it dit & lti h dSystems integrators, IT security audit & consulting, hardware production & distribution, on site and online maintenance &

data recovery, mobile security solutions

A promising business to be built up from (almost) scratch Global IT security market to grow by 4% in 2010 (Gartner) = strong export potential. Local Markets: data & network security for local & foreign major companies, embryonic y g j p y

e-commerce & e-government programmes, banks & other financial actors, etc.

A fast-growing exposure of MED businesses to IT threats Successful initiatives subsidising investments in hardware, IT security & internet access g , y

for the benefit of MED SMEs (cf Egyptian Cybersecurity Initiative 2007-09) Public boost: Tunisian law 5-2004 & associated decrees, annual compulsory IT security

audit by certified Tunisian services providers for public administrations & “strategic privates businesses” More MED countries ought to follow the moveprivates businesses . More MED countries ought to follow the move.

MED talents to address offshore & local demand Foreign kow-how coming in: US Mitre Group International in Rabat, Finish security

software Stonesoft in Tunis Symantec considering opening a Moroccan subsidiary thesoftware Stonesoft in Tunis, Symantec considering opening a Moroccan subsidiary, the BIG 5’s IT security services of their MED affiliates, UNIDEES in Algiers, etc.

Local players getting their share of the cake: Syria’s Platinum, etc. + Israel world-class integrated IT security cluster (see I Safe Group gathering hard & software producers).

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009

g y ( p g g p )

Oct 09 9

Growth factors : IT penetration among SMEs, e-commerce growth, regulatory changes regarding IT audits, local cybercriminality

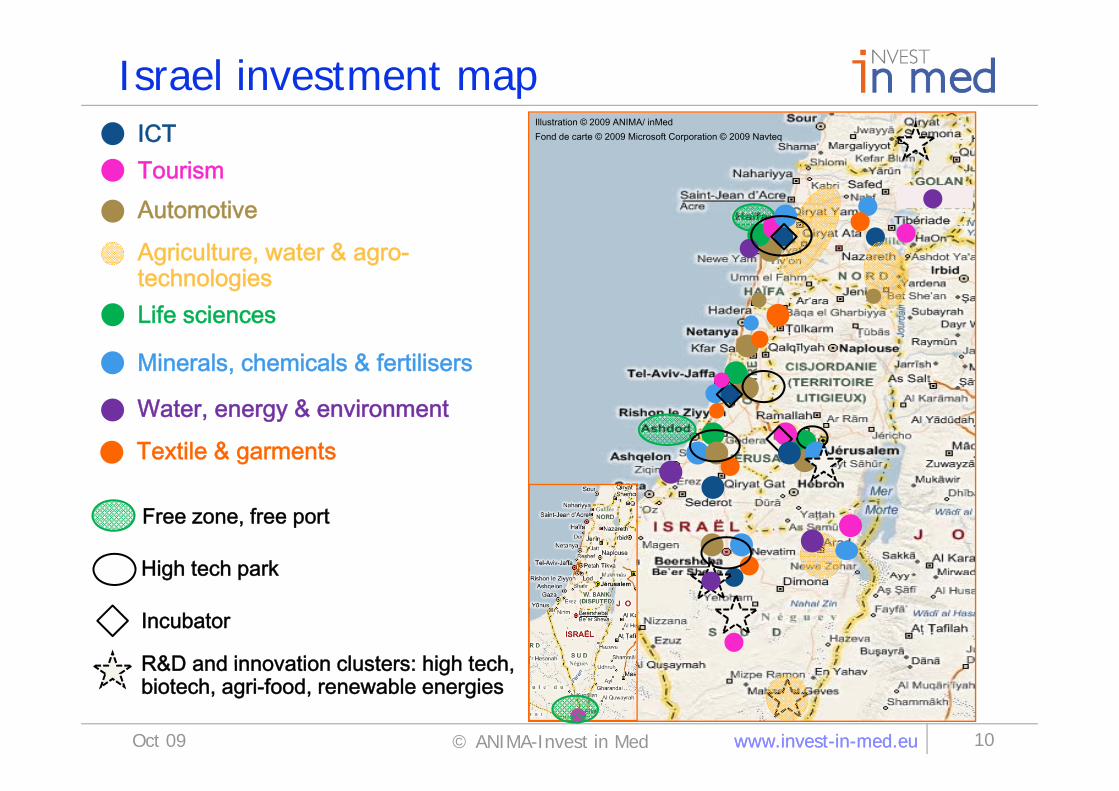

Israel investment mapICT Illustration © 2009 ANIMA/ inMedICT

AutomotiveTourism

Fond de carte © 2009 Microsoft Corporation © 2009 Navteq

Automotive

Agriculture, water & agro-technologiesLif iLife sciences

Minerals, chemicals & fertilisers

Water, energy & environment

Textile & garments

High tech park

Free zone, free port

Incubator

High tech park

R&D and innovation clusters: high tech

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 10Oct 09

R&D and innovation clusters: high tech, biotech, agri-food, renewable energies

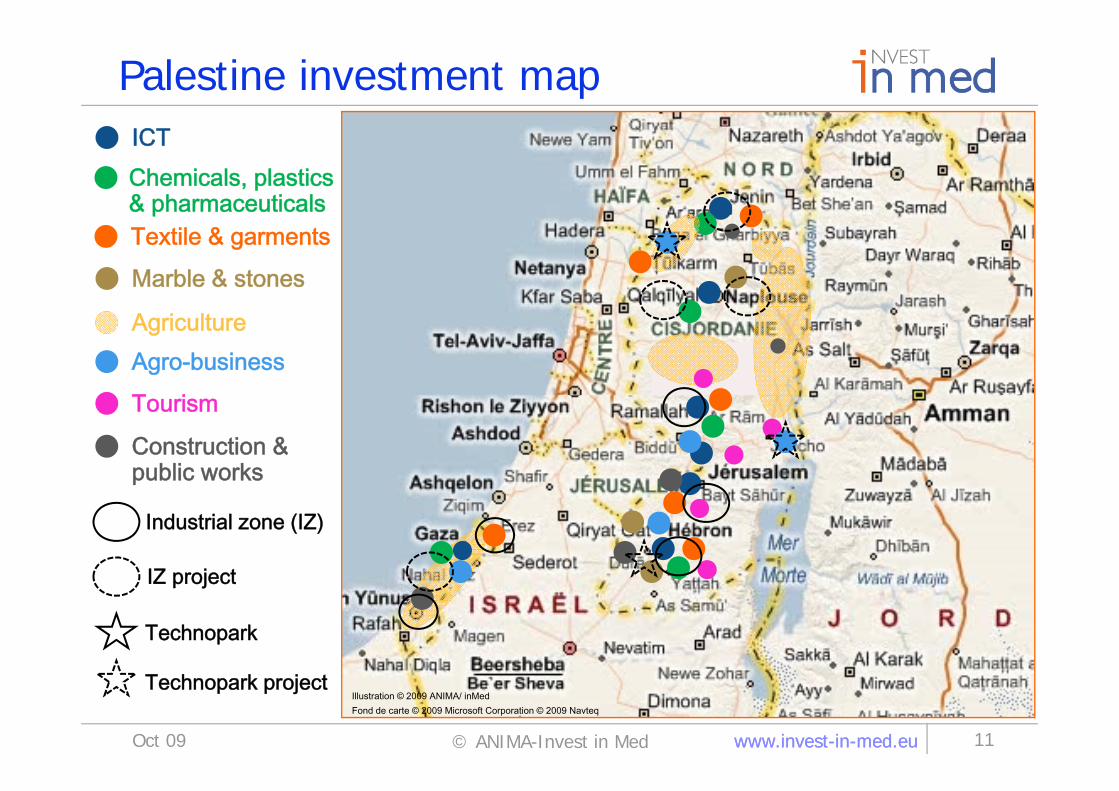

Palestine investment mapICTChemicals, plastics & pharmaceuticalspTextile & garmentsMarble & stones

Agriculture

T iAgro-businessTourism

Construction & public works

Industrial zone (IZ)

IZ projectIZ project

Technopark

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 11

Technopark projectIllustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Coporation © 2009 Navteq

Oct 09

Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

Eco-tourism opportunities E t l i t l lt l t i id

The “green washing” temptation

Eco travel agencies, sport, rural, cultural ecotourism, ecoguide, ecolodge, Bedouin camps, training-consulting-engineering

The green washing temptation Beyond the likes of the “Adopt a coral sampling” clever Aqaba promotional campaign,

little genuine eco offer. Int’al Ecotourism Society def. “responsible travel to natural areas that conserves the environment and improves the well-being of local people“). p g p p )

Potential market is big : sensitized Western tourists weigh up to 20% of world tourism market (+ domestic tourists in long term).

MED: a strong eco potential lost in mass tourism policiesg p p Rich natural & cultural heritage deserving better enforcement of public protection (see

USD 22 bn Preatoni project in protected regions of Tunisia) in order to be valued through ecotourism: more & more MED natural reserves (23 covering 9% of Egypt)

Open up to natural beauty! Many MED success stories, based on public and private initiatives: Fayoum Ecotourism project in Egypt or the Lebanese Mountain Trail (LMT), going

through 75 typical villages on 400 km and also through the Chouf Cedar Reserve (20 to 30 000 yearly visits), the Ouednoujoum project in Morocco, Jordan’s Feynan Eco Lodge, ranked in world top 10 desert lodges by National Geographic, etc.

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 12

Growth factors : micro-finance, integration of eco-tourism into tourism strategies (seeMorocco & Tunisia) rather than rural development or biodiversity policies (Egypt)

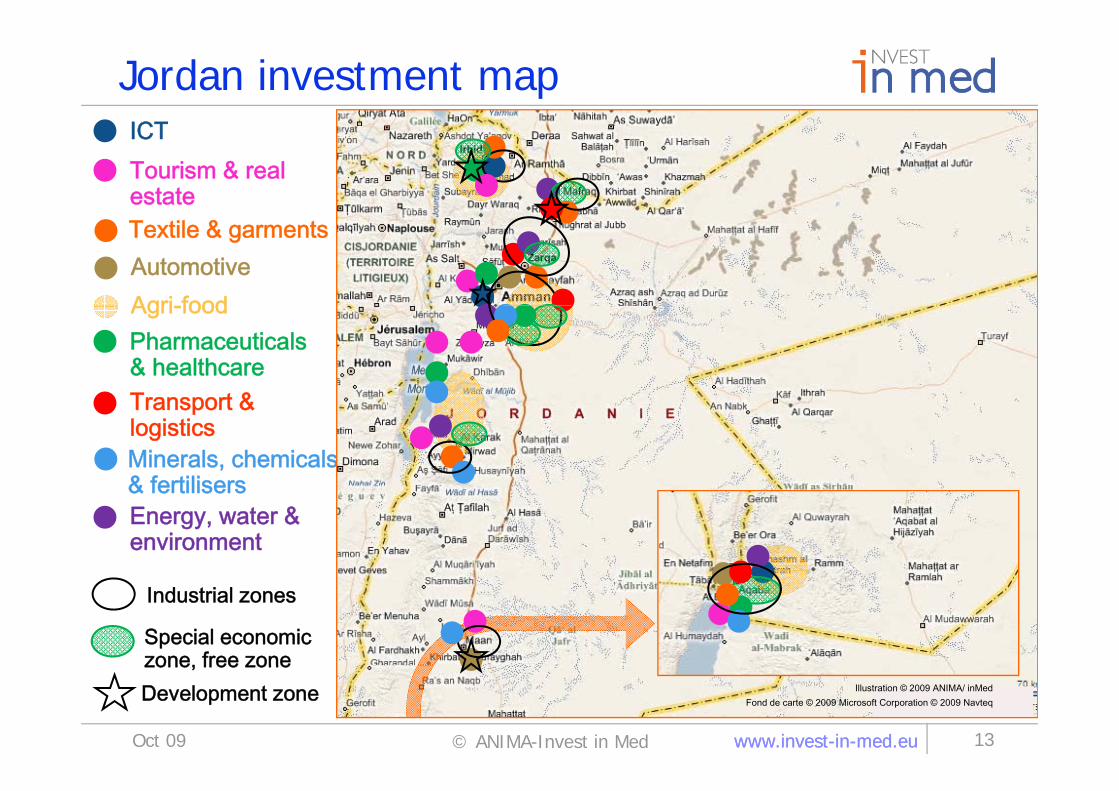

Jordan investment mapICTICTTourism & real estateTextile & garmentsAutomotiveAgri foodAgri-foodPharmaceuticals & healthcareT t &Transport & logisticsMinerals, chemicals& fertilisers& fertilisersEnergy, water & environment

Industrial zones

Special economic zone free zone

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 13

zone, free zone

Oct 09

Development zone Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

Facility management opportunitiesF ilit & t t lti t h i l i

Integration is key

Facility & property management, multi-technical services, industrial maintenance, corporate rental management, etc.

Integration is key... Gaps to be filled individually : technical maintenance (air conditioning, electric power,

plumbing and lighting systems; cleaning; groundskeeping & security) & modern property management services (rental management)+ new demand for integrated services.management services (rental management) new demand for integrated services.

…to adress new demands Need for property managers: high-end tertiary & residential real estate promotion is

booming, as well as commercial projects (retail, shopping malls) + new Assisted Livingbooming, as well as commercial projects (retail, shopping malls) + new Assisted Living Facilities (ageing residents, luxury hotel-villas, long term residence with para-hotel services for expats, etc.).

Need for facility managers: modern logistical platforms, foreign industrial investors used t t t b i & l l l t f ll i th ( t ti lto concentrate on core business & local conglomerates following the move (potential competition from maintenance spin-offs, cf Sonatrach & Somiz).

Follow your key accounts or face new competitors!S iété Gé é l A t M t’ i t t i C bl (t ti & l t Société Générale Asset Management’s investments in Casablanca (tertiary & long term residences for expats)= creation by local Tenor Group of Property Solutions

Foreign SMEs or majors : see UK-based Stirling Facilities Management’s JVs in Libya and Algeria, Auxigene Maintenance in Casablanca, Globe Williams Int’al in Amman, etc.

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009

Algeria, Auxigene Maintenance in Casablanca, Globe Williams Int al in Amman, etc.

Oct 09 14

Growth factors : conversion to outsourcing of top management in public administrations & conglomerates, as well as MED family businesses

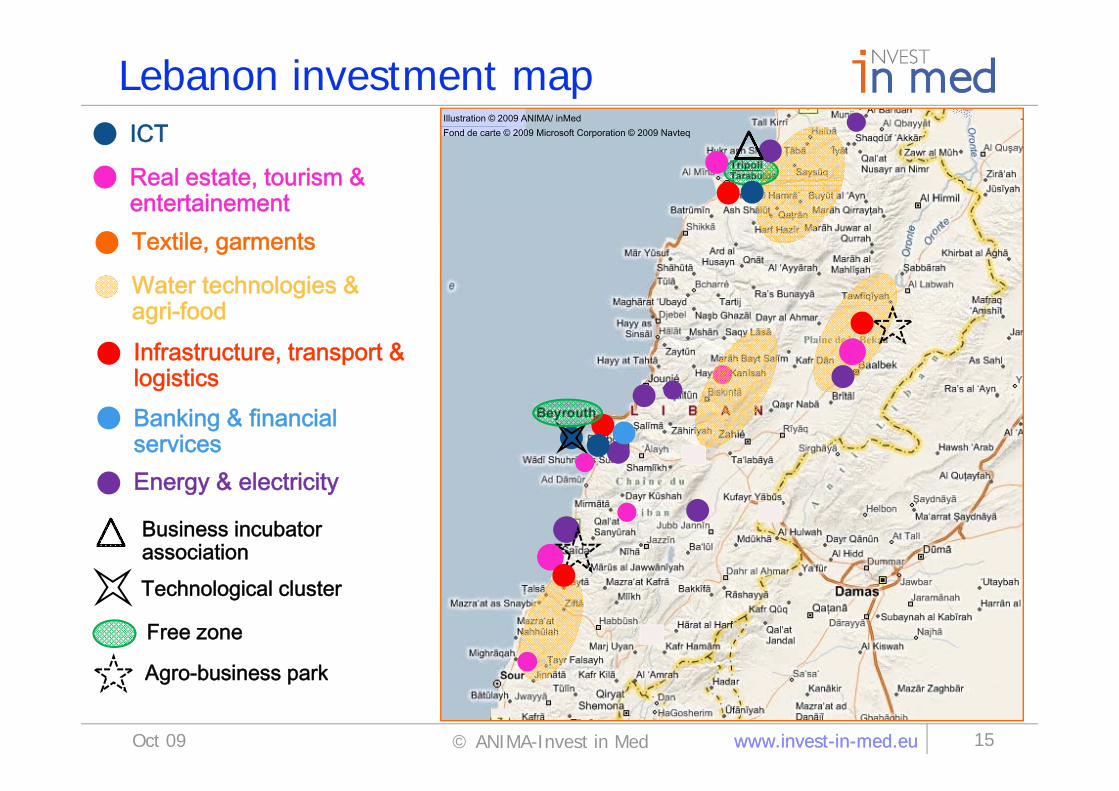

Lebanon investment mapICT

Illustration © 2009 ANIMA/ inMed

ICT

Real estate, tourism & entertainement

Fond de carte © 2009 Microsoft Corporation © 2009 Navteq

Textile, garments

Water technologies & i f dagri-food

Infrastructure, transport & logisticsBanking & financialservicesEnergy & electricityEnergy & electricity

Business incubator associationTechnological cluster

Free zone

A b i k

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 15Oct 09

Agro-business park

Aromatic & medicinal plants (AMP)C lti ti (bi ) l t t ti ( ti l il fCultivation (bio), plant extraction (essential oil, perfume,

flavoring, coloring, antioxidant & nutraceutical), processingindustries (freezing, drying), packaging

Riding the bio wave.... AMP find growing outlets in the perfume, cosmetics, pharmaceutical & agro-food

industries: bio agrofood, phytotherapy, etc. are trendier than ever! Strong export potential: global bio products markets = USD 27.8 bn in 2006 (Europe + USA =96%).

Turning tradition into a globalised business Europe’s traditional aromatic plants provider (Moroccan and Tunisian rosemary & thyme)

offers a great pool of AMP resources waiting for a better valorization: Naturex provides antioxidant compounds beneficial for human cells (ellagitannins) from the pomegranate tree + natural antioxydant additive for agrofood based on rosemary extracts.

Need for industry standards and public support (incl R&D): American-Tunisian project on Need for industry standards and public support (incl.R&D): American Tunisian project on desert flora valorization + Morocco’s Aromatic Codex (harmonisation with int’al standards, etc.) + Egypt looking for foreign investors for onion & garlic drying plants + essential oil extraction plants in Beni Souef, al Minya, New valley, Sinai & Sohag regions.

From rural cooperative to global leaders Naturex (Avignon), EUR 185 mln in annual sales, big factory and R&D centre near

Casablanca with initial Proparco support vs. Catalunya-backed Women Cooperative Bni Boufrah rural development micro project (Moroccan Rif)

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009

Boufrah rural development micro-project (Moroccan Rif)

Oct 09 16

Growth factors : integration to EU bio comestics & agrofood clusters + R&D effort to identify promising nutraceuticals principles

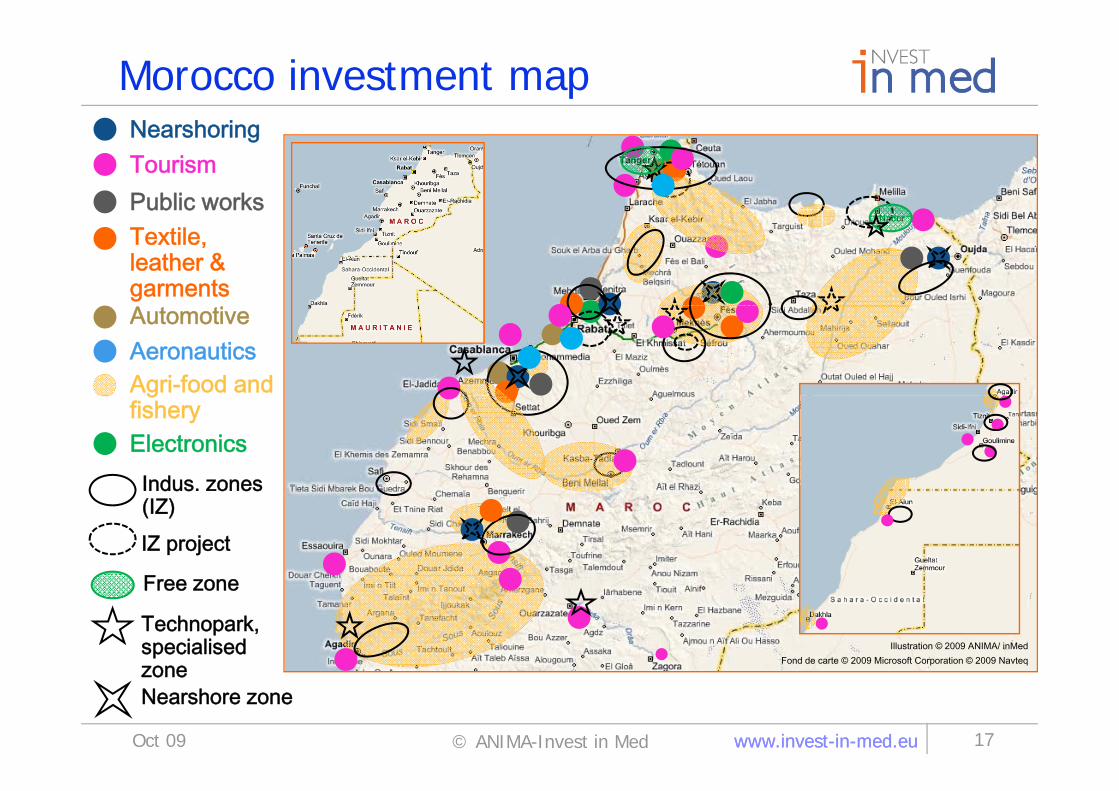

Morocco investment mapNearshoringNearshoringTourismPublic worksTextile, leather &garmentsAutomotive

Agri-food and Aeronautics

gfishery

Indus zones

ElectronicsIndus. zones(IZ)IZ project

F

Technopark, specialised

Free zone

Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 17

zone Nearshore zone

Oct 09

p q

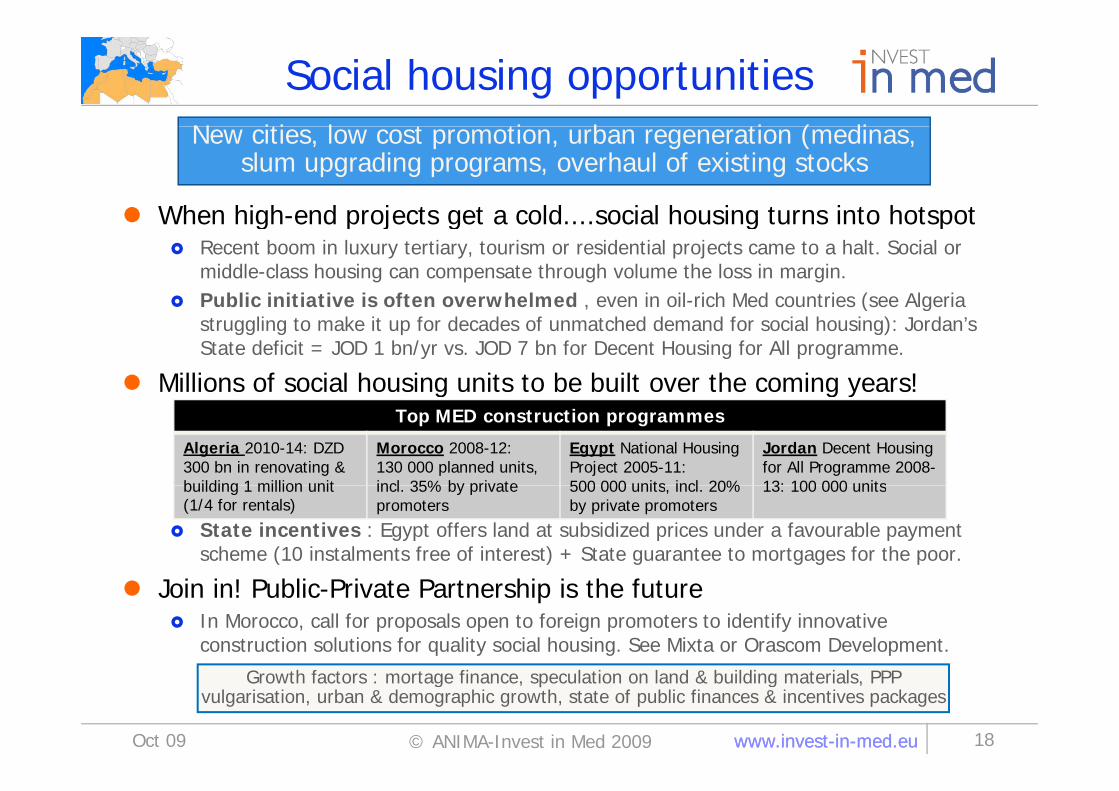

Social housing opportunitiesN iti l t ti b ti ( di

When high-end projects get a cold social housing turns into hotspot

New cities, low cost promotion, urban regeneration (medinas, slum upgrading programs, overhaul of existing stocks

When high-end projects get a cold....social housing turns into hotspot Recent boom in luxury tertiary, tourism or residential projects came to a halt. Social or

middle-class housing can compensate through volume the loss in margin. Public initiative is often overwhelmed , even in oil-rich Med countries (see Algeria Public initiative is often overwhelmed , even in oil rich Med countries (see Algeria

struggling to make it up for decades of unmatched demand for social housing): Jordan’sState deficit = JOD 1 bn/yr vs. JOD 7 bn for Decent Housing for All programme.

Millions of social housing units to be built over the coming years!g g yTop MED construction programmes

Algeria 2010-14: DZD 300 bn in renovating &building 1 million unit

Morocco 2008-12: 130 000 planned units, incl 35% by private

Egypt National HousingProject 2005-11: 500 000 units incl 20%

Jordan Decent Housing for All Programme 2008-13: 100 000 units

State incentives : Egypt offers land at subsidized prices under a favourable payment scheme (10 instalments free of interest) + State guarantee to mortgages for the poor.

building 1 million unit (1/4 for rentals)

incl. 35% by privatepromoters

500 000 units, incl. 20% by private promoters

13: 100 000 units

Join in! Public-Private Partnership is the future In Morocco, call for proposals open to foreign promoters to identify innovative

construction solutions for quality social housing. See Mixta or Orascom Development.

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 18

Growth factors : mortage finance, speculation on land & building materials, PPP vulgarisation, urban & demographic growth, state of public finances & incentives packages

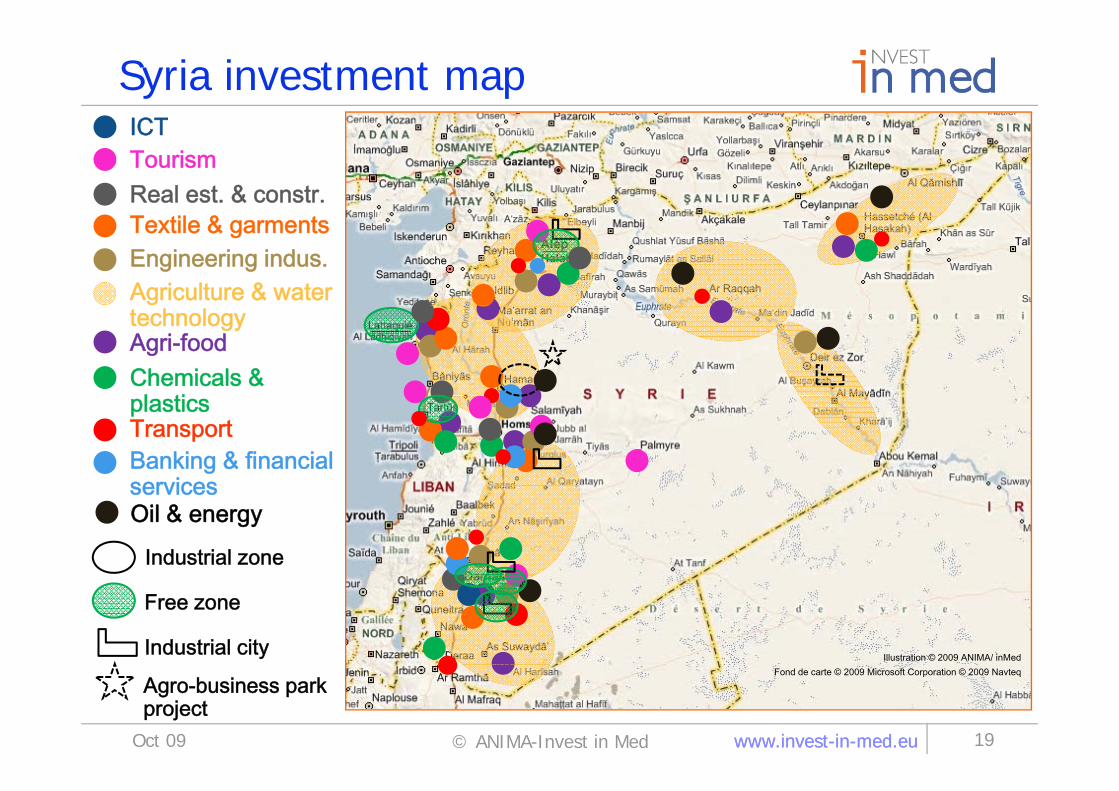

Syria investment mapICTICT

T il &

TourismReal est. & constr.Textile & garmentsEngineering indus.Agriculture & water technology

Chemicals & l ti

Agri-food

plasticsTransportBanking & financialservices

Industrial zone

servicesOil & energy

Industrial city

Free zone

Illustration © 2009 ANIMA/ inMed

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 19Oct 09

Fond de carte © 2009 Microsoft Corporation © 2009 Navteq

Agro-business park project

Industrial textile opportunitiesD i & d ti f k i i i t t ( t

Industrial textiles as a way out of RMG addiction

Design & production for packaging, mining, transport (auto, aero), agrotextiles (crop protection), construction, etc.

Industrial textiles as a way out of RMG addiction Global technical textile market = EUR 100 bn in 2010 (Clubtex), incl. 60% for industrial

uses (26% for transport). Construction is the fastest-growing segment. Local & export markets: booming MED infrastructure & housing markets industrial Local & export markets: booming MED infrastructure & housing markets, industrial

take-off (aeronautics & automotive clusters moving southward), strong mining & agrofood industry (experiments in Tangiers, zucchinis for export: +326% profit margin)

Agadir block & European innovation as catalysers?gad b oc & u opea o at o as cata yse s Preparation of an Agadir Textile Association + Agadir Clever Fabrics Plan TextTech Med initiative, launched by the European Business & Innovation Centre

Network (Invest in Med programme): fostering the birth of a Euromed cluster (European demand, MED production) through technical & commercial ventures.

Follow the pioneers! See German stands & tents manufacturer Röder EUR 10 million greenfield investment in

Düzce, Turkey, Spanish Antolin or Portuguese Sunviauto in automotive subcontracting in Tangiers or Tunisia’s Altea Packaging Euromediterranean success story…

Growth factors : vulgarisation of technical textile uses among agrofood & construction

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 2009 Oct 09 20

Growth factors : vulgarisation of technical textile uses among agrofood & construction profesionnals, North-South R&D public and private projects, MED support policies

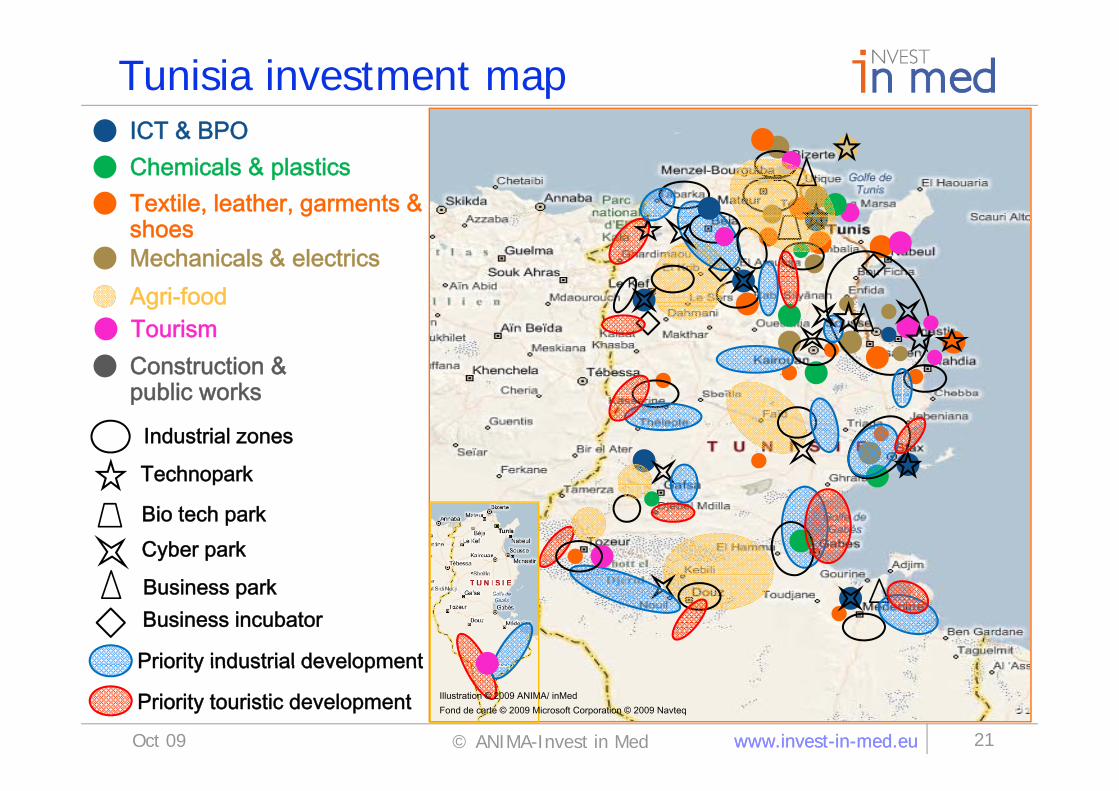

Tunisia investment mapICT & BPOICT & BPOChemicals & plasticsTextile, leather, garments & gshoesMechanicals & electricsAgri-foodgTourismConstruction & public workspublic works

Industrial zones

Technopark

Bio tech parkCyber park

Business incubator

Priority industrial development

Business park

www.invest-in-med.euwww.invest-in-med.eu© ANIMA-Invest in Med 21Oct 09

Illustration © 2009 ANIMA/ inMedFond de carte © 2009 Microsoft Corporation © 2009 Navteq

Priority industrial development

Priority touristic development

Thank you / Contact usThank you / Contact usPierre HENRY [email protected]

Coordination

Jeanne [email protected]

Coordination Emmanuel Noutary, Programme Director,

ANIMA Investment Network Clémentine Brisson-Lesage, Assistant T l +33 4 96 11 67 60 /F +33 4 96 11 67 61 Tel. +33 4 96 11 67 60 /Fax +33 4 96 11 67 61 [email protected] [email protected]

Executive CommitteeExecutive Committee Dirk Vantyghem, Dir. International

EUROCHAMBRES Tel. +32 2 282 08 76 /Fax: +32 2 230 00 38 lemcke@eurochambres eu B t [email protected]

MedAlliance Board Galal Zorba, President, BusinessMed Tel. + 216 71 280 177 /Fax + 216 71 281 495

Boost Investment

and Business

www.invest-in-med.euwww.invest-in-med.eu

Tel. + 216 71 280 177 /Fax + 216 71 281 495 [email protected]

and Business in the Mediterranean

© ANIMA-Invest in Med 2009 22Oct 09