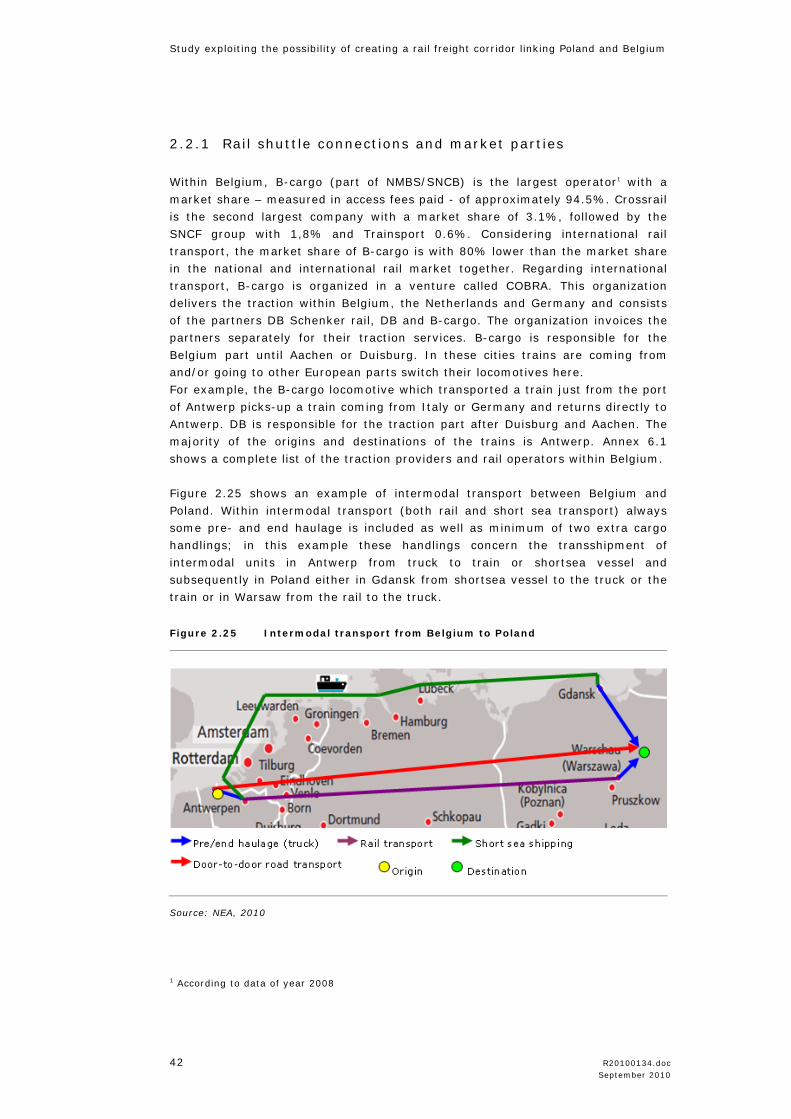

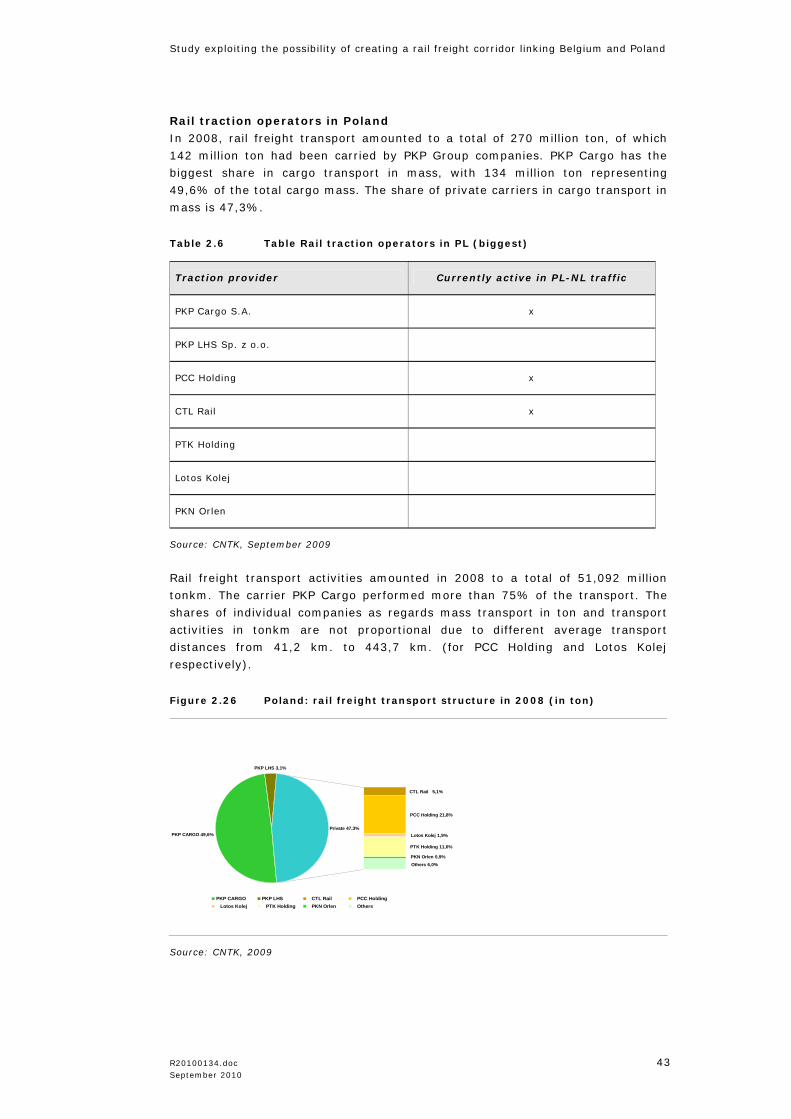

Study exploiting the possibility of creating a rail

freight corridor linking Belgium and Poland

Study exploiting the possibility of creating a rail

freight corridor linking Belgium and Poland

drs. A.A. Roest Crollius

This report has been financed by Infrabel

Reference R20100134/31332000/ARC/LJO

Final version

Zoetermeer, September 2010

© The use of figures and/or text from this report is permitted if the source is clearly

mentioned. Copying of this report is only permitted with written permission from NEA.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 1 September 2010

Contents

1 MANAGEMENT SUMMARY 3 1.1 Introduction 3 1.2 Chapter 1 – Current situation on the market and its’ potential

for further development 3 1.2.1 Freight volumes analysis on the corridor Belgium – Poland /

Czech Republic 3 1.3 Intermodal transport analysis 5 1.4 Chapter 2 - Identification of barriers to further development 8 1.5 Chapter 3 Selection of the Paths 8 1.6 Action Plan focusing on Belgium 9 1.6.1 Elaboration of the action plan 11

2 CURRENT SITUATION ON THE MARKET AND ITS’ POTENTIAL FOR FURTHER DEVELOPMENT 17

2.1 Freight volumes analysis on the corridor Belgium – Poland /

Czech Republic 17 2.1.1 Background and Methodology 17 2.1.2 Results 23 2.1.3 Conclusions 39 2.2 Intermodal transport analysis 40 2.2.1 Rail shuttle connections and market parties 42 2.2.2 Rail transport compared to other transport modes 48 2.3 Conclusions 59

3 IDENTIFICATION OF BARRIERS TO FURTHER DEVELOPMENT 63

3.1 Introduction 63 3.2 Barriers as viewed by the stakeholders 63 3.3 Institutional barriers & issues 64 3.4 Operational barriers & issues 65 3.5 Technical barriers & issues 66 3.6 Market barriers & issues 66 3.7 Conclusions 67

4 SELECTION OF THE PATHS AND RAIL TERMINALS 69

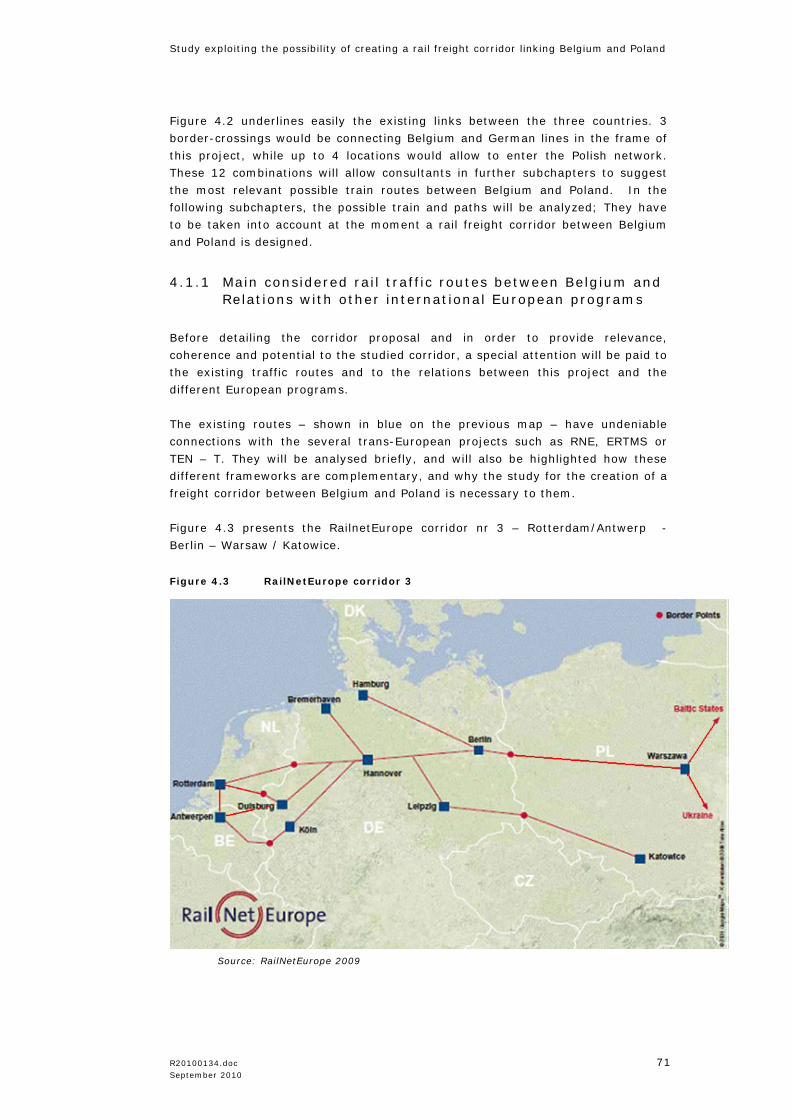

4.1 Introduction 69 4.1.1 Main considered rail traffic routes between Belgium and

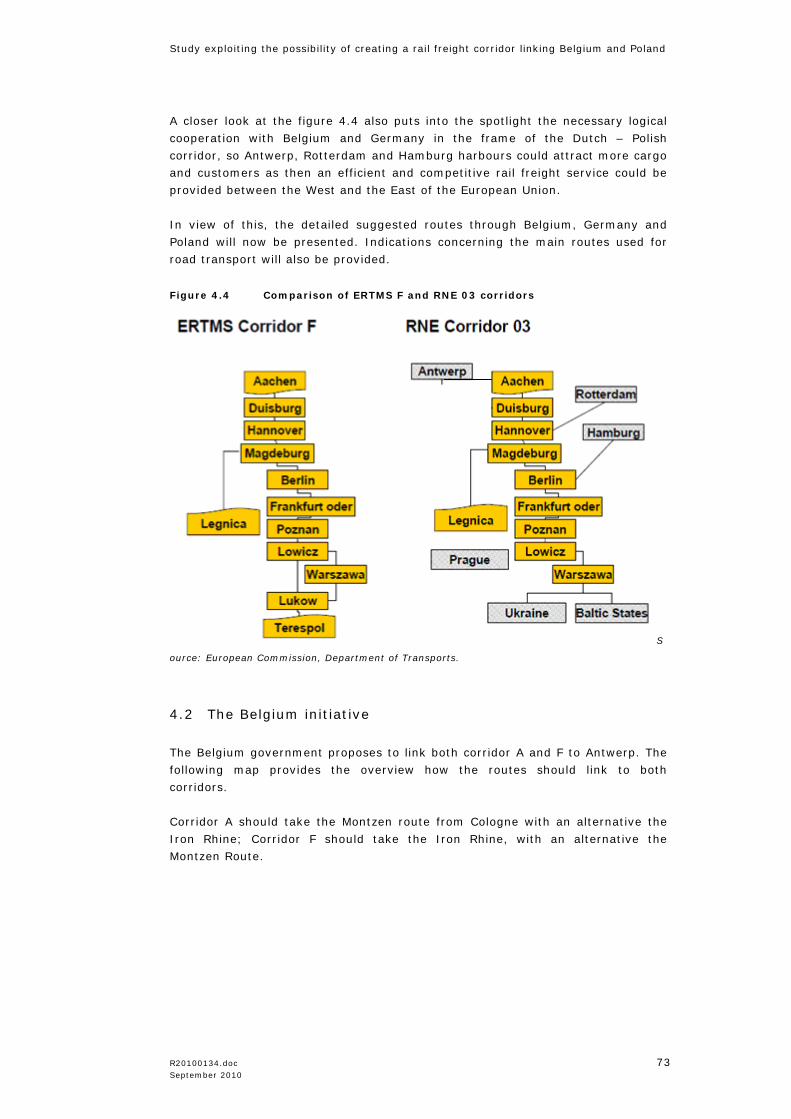

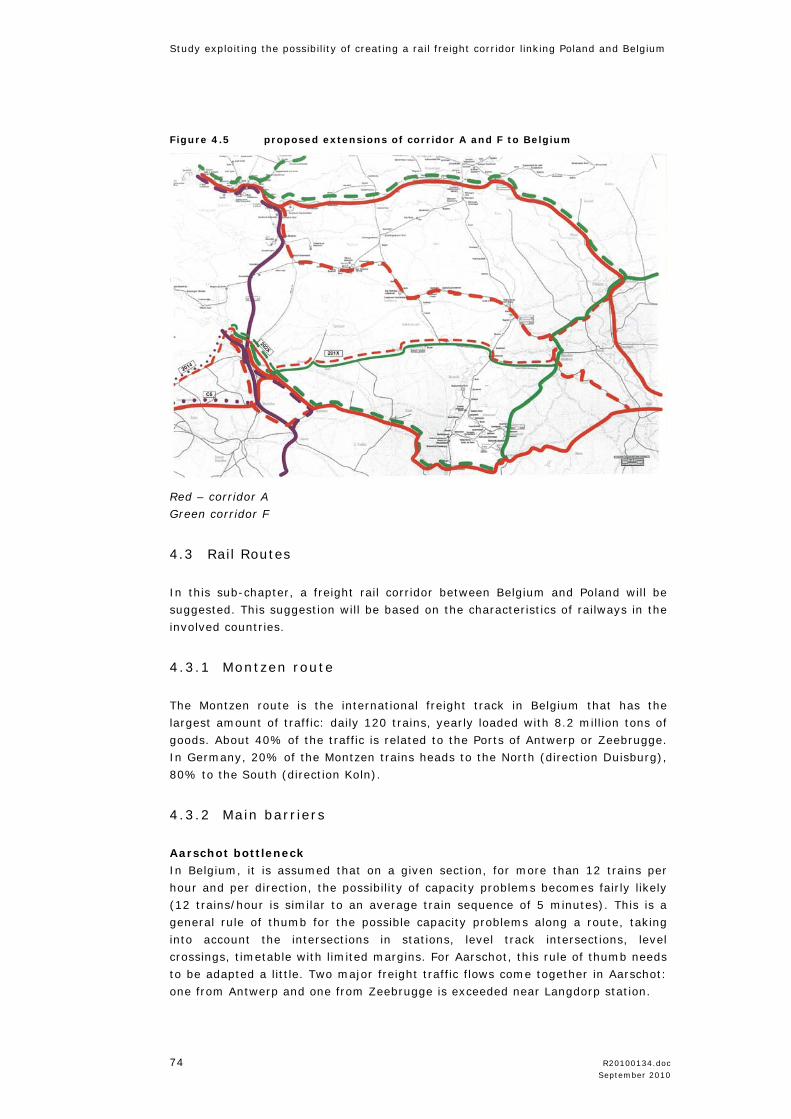

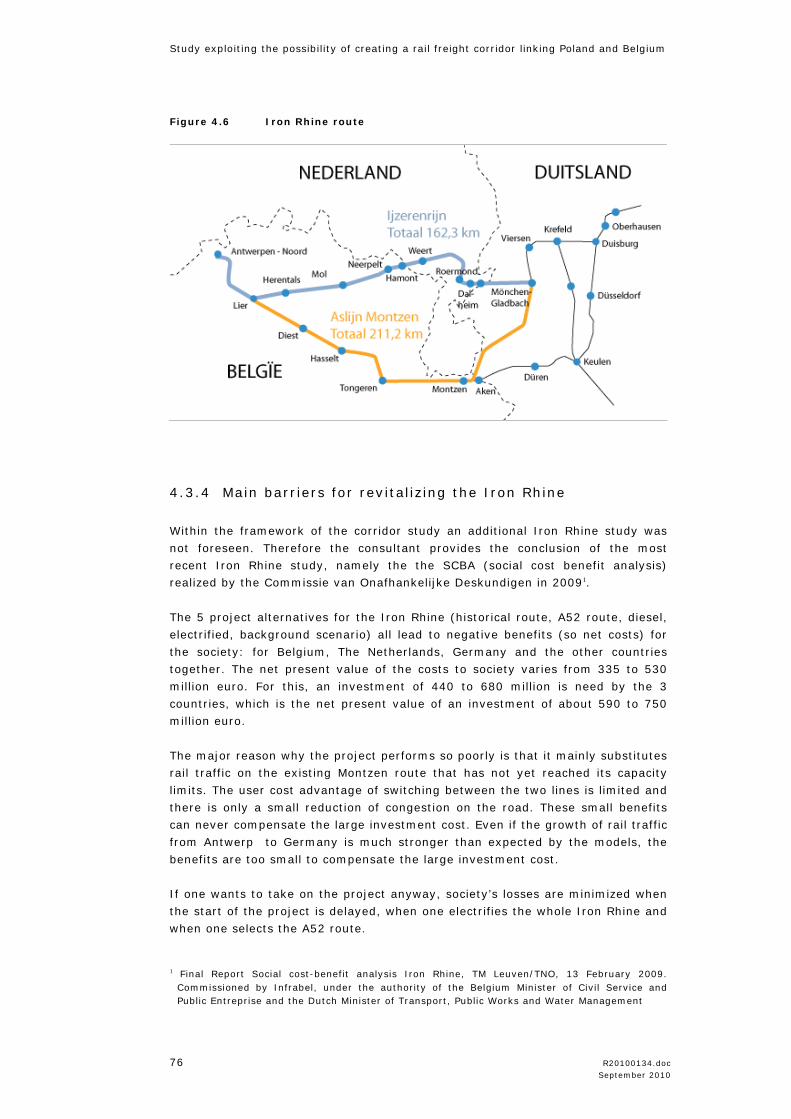

Relations with other international European programs 71 4.1.2 Relations with other international European programs 72 4.2 The Belgium initiative 73 4.3 Rail Routes 74 4.3.1 Montzen route 74 4.3.2 Main barriers 74 4.3.3 Iron Rhine 75 4.3.4 Main barriers for revitalizing the Iron Rhine 76 4.3.5 Via the Netherlands - Rotterdam - Betuwelijn or Osnabruck 77 4.3.6 Comparing routes 77

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

2 R20100134.doc September 2010

4.3.7 Corridor Capacity 79 4.4 Road 79 4.5 Rail terminals 79 4.5.1 Antwerp 80 4.5.2 Zeebrugge 81 4.6 Infrastructure Projects 82 4.6.1 Zeebrugge 84 4.7 Conclusions 85

5 REFERENCES 87

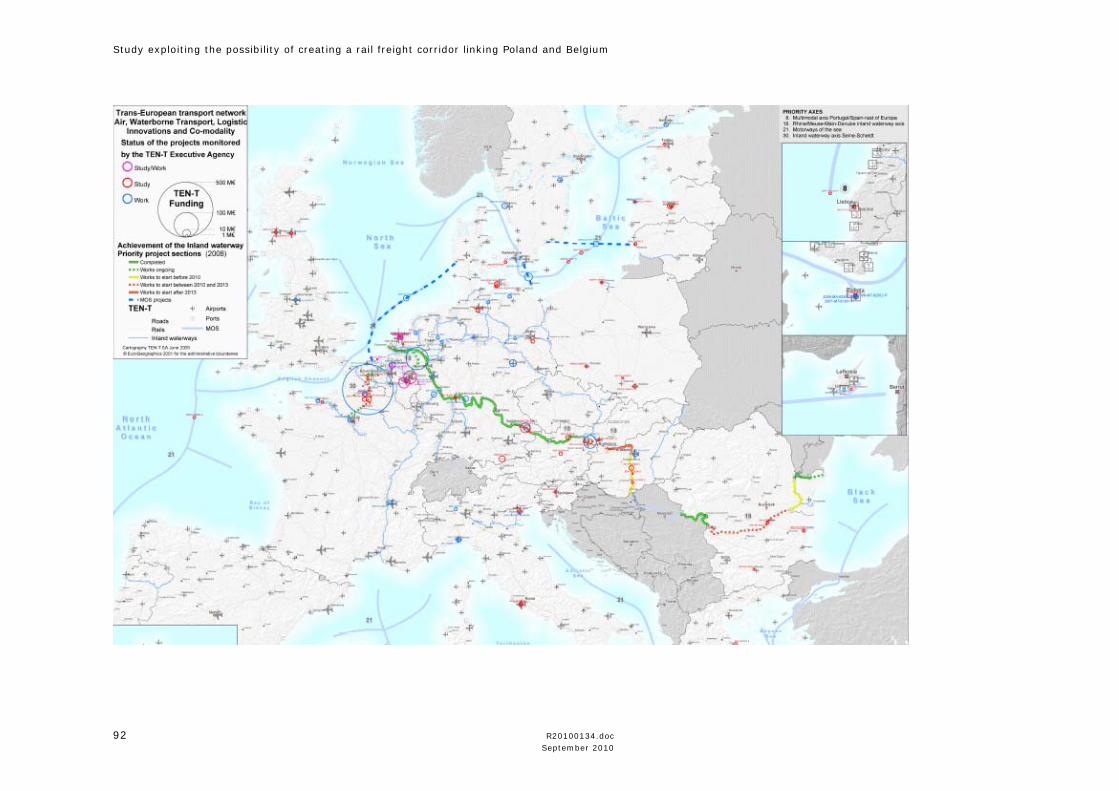

6 APPENDIX 89 6.1 Traction providers and rail operators in Belgium 89 6.2 List of Interviews 90 6.3 A complete list of terminals in Belgium 90 6.4 Rail maps 91 6.1 Table: Action Plan for Rail Freight Corridor Belgium – Poland

(complete version) 96 6.4.1 Elaboration of the action plan 102

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 3 September 2010

1 Management Summary

1.1 Introduction

In addition to the existing rail legislation, a latest legislative development was

that the position (EU) No 2/2010 of the Council at first reading with a view to the

adoption of a Regulation of the European Parliament and of the Council

concerning a European rail network for competitive freight was published 4 May

2010. Within this regulation proposal, a total of nine principle routes of freight

corridors are selected to be used as the base for the establishment of European

rail freight corridors in the near future. In addition, clear and tighter rules are

proposed in this regulation proposal concerning the establishment, organization

and management of the rail freight corridors. This regulation proposal

demonstrates the resolution of policy makers in facilitating the rail freight sector

in Europe. Besides, it shows the crucial role the principle routes will play in

establishing the European rail freight corridors. Among all principle routes, route

Bremerhaven/Rotterdam/Antwerp-Aachen/Berlin-Warsaw-Terespol (Poland-

Belarus border)/Kaunas is one of them. NEA Transport research and training

(NEA) has been executed recently a ‘study exploiting the possibility of creating a

rail freight corridor linking Poland and The Netherlands’. Infrabel has requested

NEA to carry out a similar study for Belgium in order to include Belgium in this

corridor study.

The Management Summary provides an overview of the results of Task 1 (market

situation and forecasting), 2 (barriers to the market) and 3 (corridor description)

and the Action Plan.

1.2 Chapter 1 – Current situation on the market and its’ potential for further development

1.2.1 Freight volumes analysis on the corridor Belgium – Poland / Czech Republic

Overall, it can be concluded that the rail freight volumes in the corridor Belgium

– Poland/Czech Republic are rather limited. Especially compared to other

volumes on the corridor such as between Belgium and Germany or between

Poland and Germany.

In the direction from Belgium to Poland/Czech Republic, the rail freight volume is

169.000 tons or about 223 trains in 2007 towards Poland and 23.000 tons or

about 31 trains towards the Czech Republic. For future years, the volumes

towards Poland ranges between 271.000 tons in the low growth scenario for

2020 (index 1.6) to more than 422,000 tons (index 2.5) in the middle scenario in

2030 to 558.000 tons in the high growth scenario for the year 2030 (index 3.3)

and 718.000 tons (index 4.2) in 2040.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

4 R20100134.doc September 2010

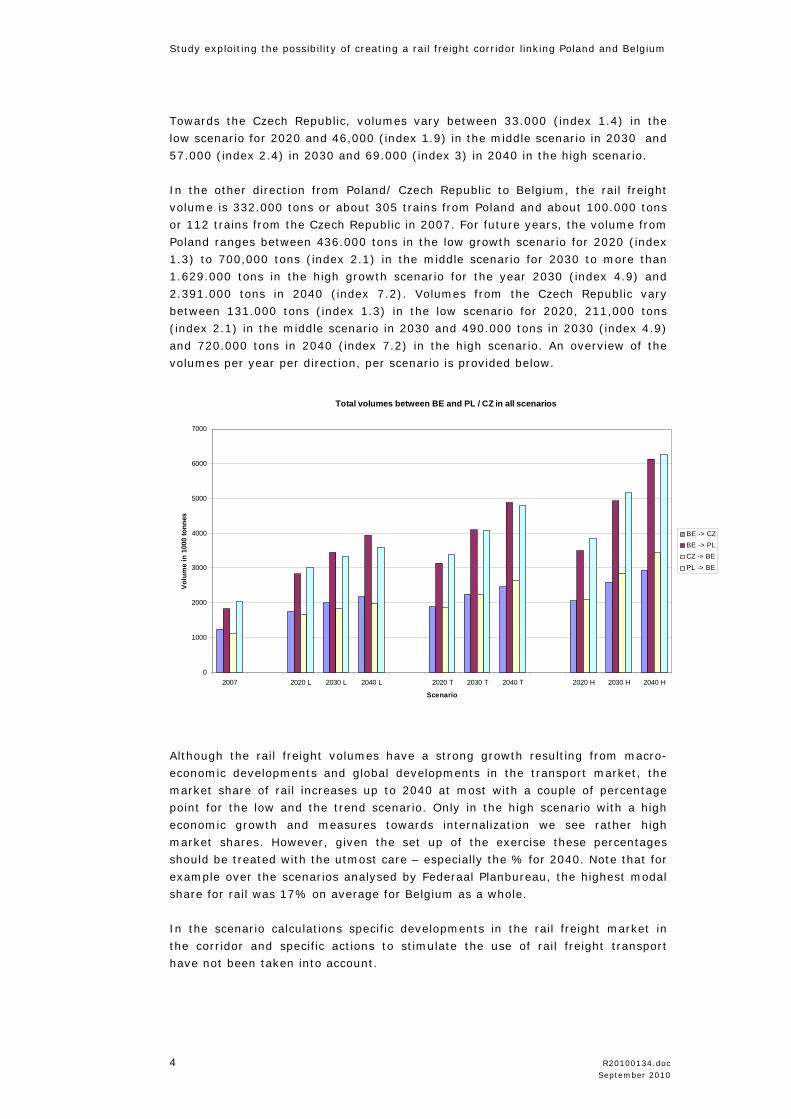

Towards the Czech Republic, volumes vary between 33.000 (index 1.4) in the

low scenario for 2020 and 46,000 (index 1.9) in the middle scenario in 2030 and

57.000 (index 2.4) in 2030 and 69.000 (index 3) in 2040 in the high scenario.

In the other direction from Poland/ Czech Republic to Belgium, the rail freight

volume is 332.000 tons or about 305 trains from Poland and about 100.000 tons

or 112 trains from the Czech Republic in 2007. For future years, the volume from

Poland ranges between 436.000 tons in the low growth scenario for 2020 (index

1.3) to 700,000 tons (index 2.1) in the middle scenario for 2030 to more than

1.629.000 tons in the high growth scenario for the year 2030 (index 4.9) and

2.391.000 tons in 2040 (index 7.2). Volumes from the Czech Republic vary

between 131.000 tons (index 1.3) in the low scenario for 2020, 211,000 tons

(index 2.1) in the middle scenario in 2030 and 490.000 tons in 2030 (index 4.9)

and 720.000 tons in 2040 (index 7.2) in the high scenario. An overview of the

volumes per year per direction, per scenario is provided below.

Total volumes between BE and PL / CZ in all scenarios

0

1000

2000

3000

4000

5000

6000

7000

2007 2020 L 2030 L 2040 L 2020 T 2030 T 2040 T 2020 H 2030 H 2040 H

Scenario

Volu

me

in 1

000

tonn

es

BE -> CZBE -> PLCZ -> BEPL -> BE

Although the rail freight volumes have a strong growth resulting from macro-

economic developments and global developments in the transport market, the

market share of rail increases up to 2040 at most with a couple of percentage

point for the low and the trend scenario. Only in the high scenario with a high

economic growth and measures towards internalization we see rather high

market shares. However, given the set up of the exercise these percentages

should be treated with the utmost care – especially the % for 2040. Note that for

example over the scenarios analysed by Federaal Planbureau, the highest modal

share for rail was 17% on average for Belgium as a whole.

In the scenario calculations specific developments in the rail freight market in

the corridor and specific actions to stimulate the use of rail freight transport

have not been taken into account.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 5 September 2010

If specific developments in the rail freight market are expected and measures

and policies are introduced to stimulate the use of rail freight transport, there

might be a higher potential for rail freight transport on this corridor.

Comparing traffic flows in the Dutch-Poland, Dutch-Czech Republic study to the

Belgium-Poland and Belgium-Czech Republic study shows that there are more or

less two corridors: a strong Belgium-Poland and Dutch-Czech Republic traffic

flow and a much weaker Belgium-Czech Republic and Dutch-Poland traffic flow.

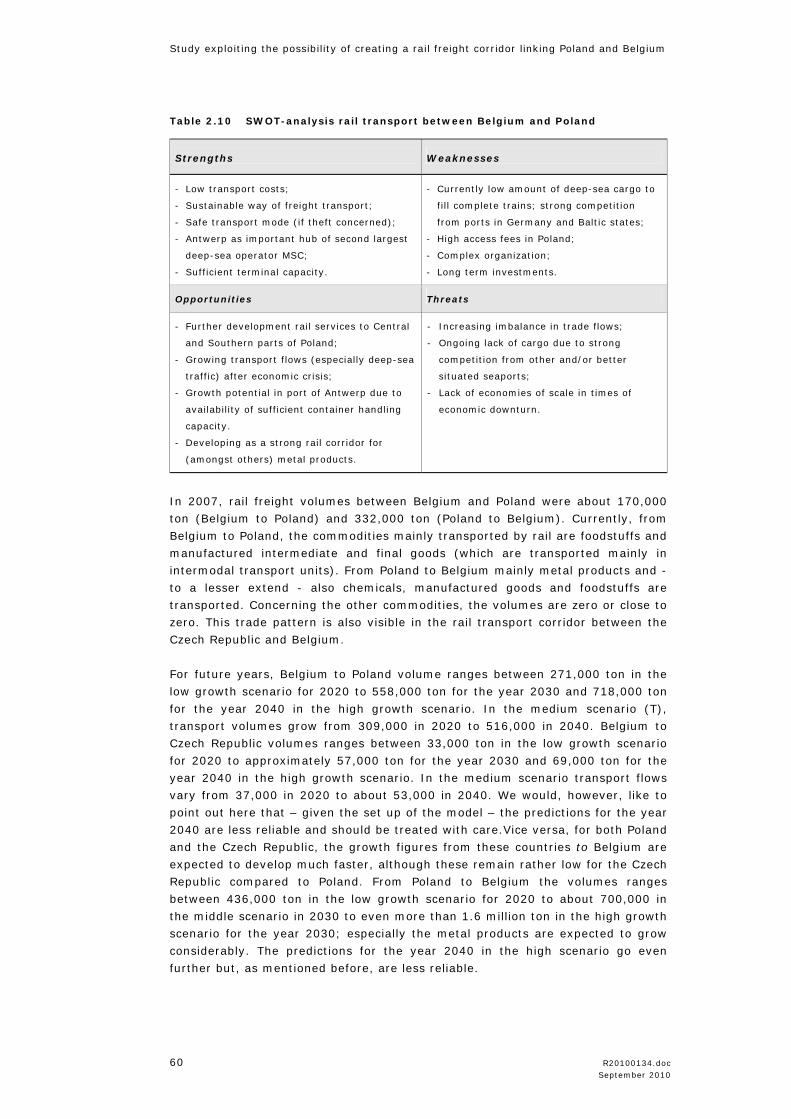

1.3 Intermodal transport analysis

Based on the intermodal transport analysis between Belgium and Poland, a

SWOT-analysis1 can be drawn. This analysis is visible in table 2.9.

Table 1.1 SWOT-analysis rail transport between Belgium and Poland

Strengths Weaknesses

- Low transport costs;

- Sustainable way of freight transport;

- Safe transport mode (if theft concerned);

- Antwerp as important hub of second largest

deep-sea operator MSC;

- Sufficient terminal capacity.

- Currently low amount of deep-sea cargo to

fill complete trains; strong competition

from ports in Germany and Baltic states;

- High access fees in Poland;

- Complex organization;

- Long term investments.

Opportunities Threats

- Further development rail services to Central

and Southern parts of Poland;

- Growing transport flows (especially deep-sea

traffic) after economic crisis;

- Growth potential in port of Antwerp due to

availability of sufficient container handling

capacity.

- Developing as a strong rail corridor for

(amongst others) metal products.

- Increasing imbalance in trade flows;

- Ongoing lack of cargo due to strong

competition from other and/or better

situated seaports;

- Lack of economies of scale in times of

economic downturn.

In 2007, rail freight volumes between Belgium and Poland were about 170,000

ton (Belgium to Poland) and 332,000 ton (Poland to Belgium). Currently, from

Belgium to Poland, the commodities mainly transported by rail are foodstuffs and

manufactured intermediate and final goods (which are transported mainly in

intermodal transport units). From Poland to Belgium mainly metal products and -

to a lesser extend - also chemicals, manufactured goods and foodstuffs are

transported. Concerning the other commodities, the volumes are zero or close to

zero. This trade pattern is also visible in the rail transport corridor between the

Czech Republic and Belgium.

1 SWOT means: Strengths, Weaknesses, Opportunities and Threats.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

6 R20100134.doc September 2010

For future years, Belgium to Poland volume ranges between 271,000 ton in the

low growth scenario for 2020 to 558,000 ton for the year 2030 and 718,000 ton

for the year 2040 in the high growth scenario. In the medium scenario (T),

transport volumes grow from 309,000 in 2020 to 516,000 in 2040. Belgium to

Czech Republic volumes ranges between 33,000 ton in the low growth scenario

for 2020 to approximately 57,000 ton for the year 2030 and 69,000 ton for the

year 2040 in the high growth scenario. In the medium scenario transport flows

vary from 37,000 in 2020 to about 53,000 in 2040. We would, however, like to

point out here that – given the set up of the model – the predictions for the year

2040 are less reliable and should be treated with care.Vice versa, for both Poland

and the Czech Republic, the growth figures from these countries to Belgium are

expected to develop much faster, although these remain rather low for the Czech

Republic compared to Poland. From Poland to Belgium the volumes ranges

between 436,000 ton in the low growth scenario for 2020 to about 700,000 in

the middle scenario in 2030 to even more than 1.6 million ton in the high growth

scenario for the year 2030; especially the metal products are expected to grow

considerably. The predictions for the year 2040 in the high scenario go even

further but, as mentioned before, are less reliable.

These forecasts are much higher than the most optimistic forecast for the

Netherlands in which rail volumes are expected to grow to a maximum of 1.2

million in 2040 (high growth scenario). Hence, these Poland – Belgium forecasts

underline the high potential of the Belgium – Poland rail corridor. From the Czech

Republic to Belgium the volumes ranges between 131,000 ton in the low growth

scenario for 2020 to 211,000 ton in 2030 in the central scenario to 490,000 ton

in the high growth scenario for the year 2030 and even till 720,000 tons in 2040.

In more detail, it can be concluded that especially the metal products (regarding

both Poland and the Czech republic) and containerized goods (between Belgium

and the Czech Republic) show a strong growth on these corridors. Because the

rail freight volumes are expected to grow fast, the market share of rail could

increase from 7% in 2007 to 8% in the middle and 9% in the high growth

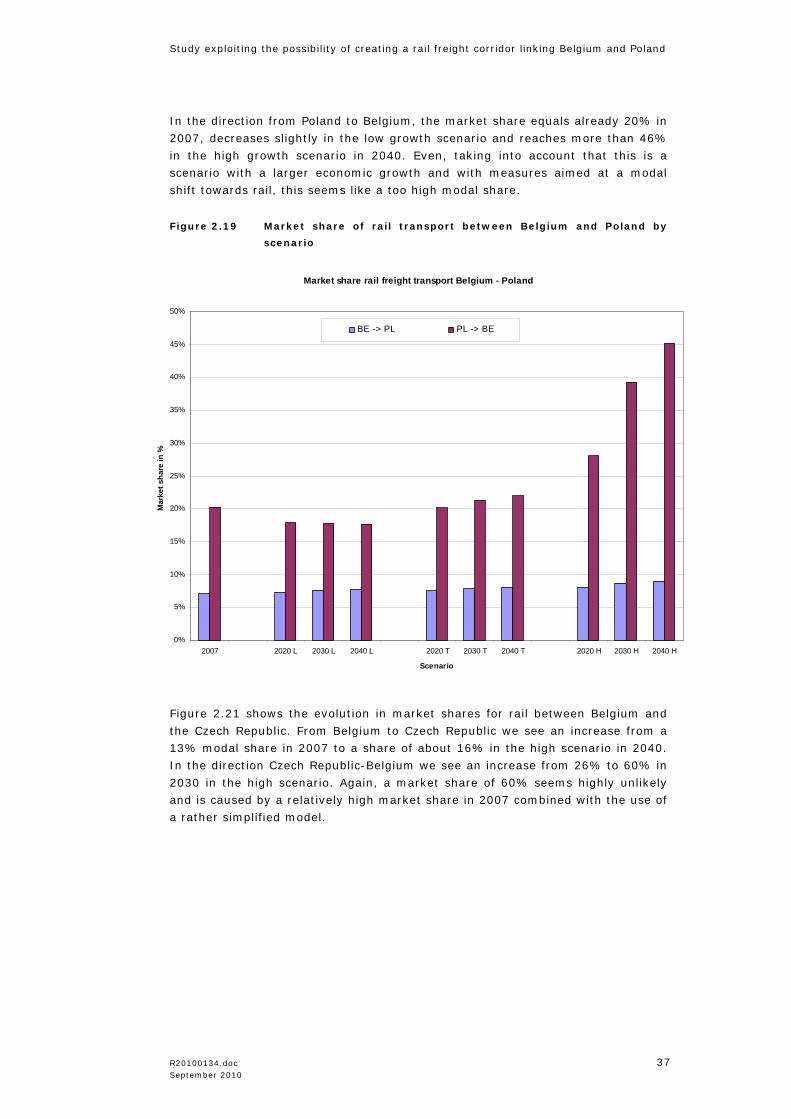

scenario in 2030 (Belgium to Poland) and from 20% in 2007 to 21% in the

medium scenario in 2030 and 39% in the high growth scenario in 2030 (Poland

to Belgium). Finally, the market share of rail could increase from 13% in 2007 to

15% in the medium scenario and 16% in the high growth scenario in 2030

(Belgium to Czech Republic) and from 26% in 2007 to 28% in the medium

scenario in 2030 (Czech Republic to Belgium). In the high scenario this share

increases to 51% in 2030. Even taking into account that this is a scenario with

larger economic growth and measures aimed at a model shift towards rail, this

seems to be a too high modal share. Modal shares for 2040 are even higher, but

are likely overestimated in the case of transport from the Czech Republic/Poland

to Belgium.

Analyzing the intermodal transport market between Belgium and Poland, the

highest potential for rail transport is on the corridor between Belgium and the

centre (Poznan - Warsaw) and the South (Wroclaw – Katowice) of Poland. On

these corridors, rail transport has – especially if lightweight cargo is transported

- a cost advantage over short sea shipping via Polish seaports, due to long

distances of pre- and end haulage. Rail transport has also a clear cost advantage

over road transport if pre/end haulage is limited.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 7 September 2010

The more origin and/or destinations of cargo are located Southwards and near a

rail terminal, the higher is the potential for rail transport. In addition, the

majority (87%) of all rail shipments (measured in weight) from Belgium to

Poland currently has a destination in the central or Southern part of Poland. In

the other direction, these parts in Poland are even stronger involved: 94% of all

rail shipments (measured in weight) from Poland to Belgium has an origin in the

central or Southern part of Poland.

Another important development is the growing consciousness of sustainable

supply chains in which rail transport will play an important role. If cargo transit

times are considered, those supply chains which ‘allow’ some longer transit times

in certain parts of the supply chain, rail transport can be a good transport

alternative. While some rail services have even competitive transit times

compared to road transport, rail transport is for all parts in Poland much faster

than short sea shipping via Polish seaports. Above all, frequencies of rail

transport services between Belgium and Poland are higher than for short sea

shipping. There is not enough cargo to load short sea vessels (almost) full every

day of the week, while rail transport offers a daily service between both

countries; a higher transport frequency means a higher degree of flexibility for

shippers. Finally, it is worth mentioning that especially rail services over the

weekend have an advantage over road transport, because of the driving ban on

Sunday within Germany. Table 2.10 shows the strengths and weaknesses of rail

transport over road and short sea shipping. Regarding transport costs it is clear

that short sea shipping only has an advantage over rail transport if origin and/or

destinations of cargo are located in the Northern part of Poland, close to the

Polish seaports of Gdansk/Gdynia.

Strengths and weaknesses of rail transport compared to other transport modes

Transport costs Transit times Flexibility

Rail versus road

lightweight goods + - -

Rail versus short sea

lightweight goods

+ (Southern regions)

- (Northern regions) + +

Rail versus road

heavy goods + - -

Rail versus short sea

heavy goods

+ (Southern regions)

- (Northern regions) + +

In short, rail transport has potential if cargo is or has:

• Originated and/or a destination in Central/Southern Poland;

• High and low weight density; however the advantage towards the other

modalities is stronger for light weight goods, because of weight restrictions.

• Predictable well in advance;

• Expected to be produced and transported in a sustainable way.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

8 R20100134.doc September 2010

1.4 Chapter 2 - Identification of barriers to further development

The barriers to the transport of goods between Poland and Belgium which have

been presented above, are those reported by the interested parties who are

operating on the market of rail transport. These barriers are subjective opinions

and they do not always coincide with the opinions of others participants of the

market. However, in most cases, the identified barriers are the same or similar.

The barriers focused on Beglium corridor as there are limited operators running

trains to Poland and the Polish are described in detail in the Netherlands-Poland

corridor study.

When analyzing the railway freight market Belgium and Poland it must be noted

that there is a strong competition with the others means of transport and also

inside the railway market (especially between block trains). This competition

results in the most important feature of the services offered to the customer

being the price of carriages of goods between Belgium and Poland. The vast

majority of the interviewees focused on the fact that as regards transport offers,

customers choose the cheapest offer. Only few times the quality of transport was

more stressed on. Indeed, only a few interviewees declared that in addition to

price, other factors such as quality of transport service play an important role. In

addition, significant importance was given to the inadequacy of infrastructure

and the additional scope of services offered.

1.5 Chapter 3 Selection of the Paths

This Task has been presenting the features of the Belgium railways in their

relations to Poland. For each route the advantages and disadvantages are

described including the bottlenecks. The main terminals are described including

some caracteristics and the most important infrastructure projects relevant to

the corridor Belgium – Poland are presented.

An overwiew is provided between the main alternative routes from Antwerp to

Hannover and from Hannover to Poland. Following routes were considered:

• Antwerp – Montzen – Hannover

• Antwerp – Rotterdam – Duisburg – Hannover

• Antwerp – Rotterdam – Osnabruck – Hannover

• Antwerp – Duisburg – Hannover (Iron Rhine)

The three available routes show quite some differences; the route via Rotterdam

and Osnabruck is currently the fastest, the shortest and the cheapest; which will

change with the opening of revitalished Iron Rhine. The Iron Rhine is according

the schedule the fastest, shortest and nearly the cheapest route to Hannover in

future.

Especially the track access charges are (of the existing routes) much lower at the

Rotterdam-Osnabruck route than the other two current options. However for this

last route the locomotive has to been adopted with the Dutch safety and energy

system. Moreover, the route can coop with the current level of freight trains, but

faces congestion when traffic rises.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 9 September 2010

As track access charges in Belgium and the Netherlands are cheaper than in

Germany, it reduces TAC costs when taking the route which is avoiding extra

kilometers in Germany. The Iron Rhine is the shortest, but, most probably, due

to the higher German access charges not the cheapest.

The Anwerp – Montzen – Hannover route is or will be included in the existing and

planned to be implemented European transport rail services corridors such as

ERTMS corridors, TEN-T corridors or RailNetEurope (RNE corridor 3).

The proposed revitalished Iron Rhine Railway line is a future alternative to

Poland being the shortest route to Hannover and much cheaper than the Montzen

route.

In order to allow the efficient implementation of the transport of goods in the

planned corridors, appropriate actions should be proposed and laid down. These

activities should be coordinated one another and should be associated with the

adaptation and adequate maintenance of the railway and terminal

infrastructures.

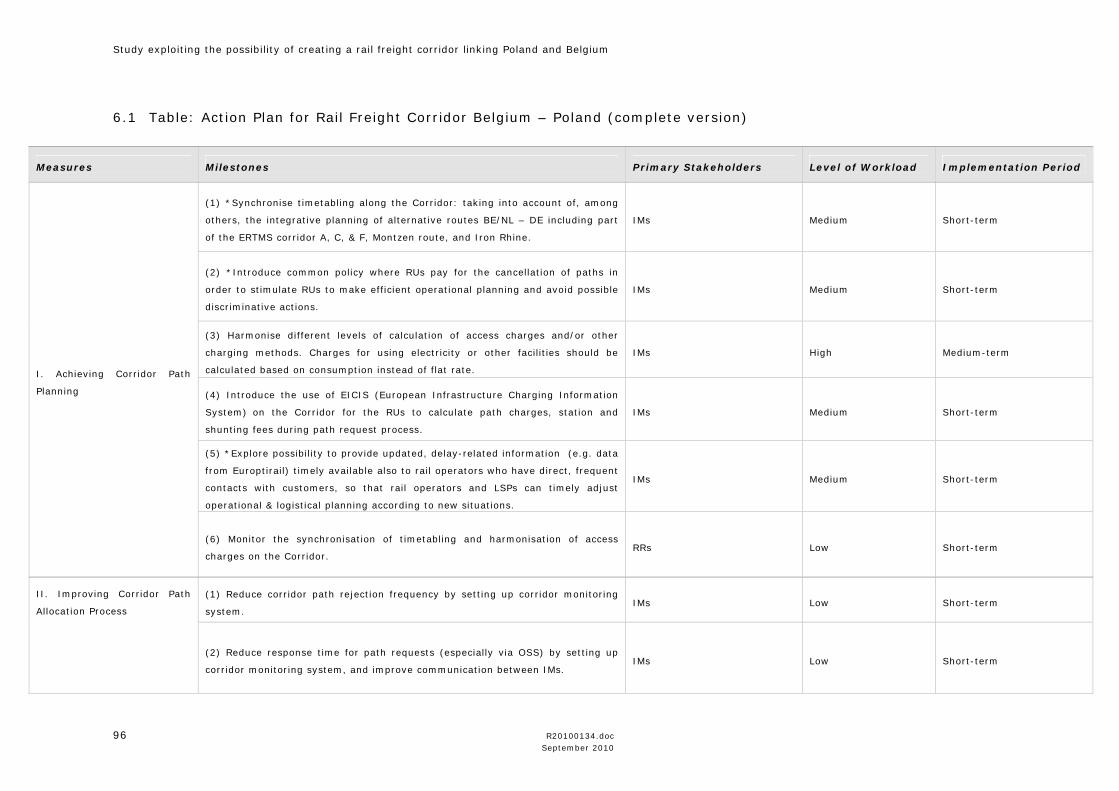

1.6 Action Plan focusing on Belgium

A complete version of Action Plan for Rail Freight Corridor Belgium – Poland

(hereinafter: the Corridor) is made and provided in the Appendix 6.1. This

Action Plan is made on the basis of the Action Plan of developing corridor The

Netherlands – Poland1 with focus on Belgium. In total, seven measures (listed in

the 1st column) are brought forward, each of which presents the development of

one specific aspect of the Corridor. Under each measure a set of milestones

(listed in the 2nd column) are generated, adding up to a total of forty-one

milestones for all seven measures. For each milestone, primary stakeholders are

determined from four types of stakeholders (listed in the 3rd column), namely,

Ministries of Transport (MoTs), Infrastructure Managers (IMs), National Safety

Authorities (NSAs), and Rail Regulators (RRs), to be responsible for the

execution of the milestone. Besides, the level of workload (listed in the 4th

column) and the period for implementation (listed in the 5thcolumn) are

estimated for each milestone.

The timeline for implementing the Action Plan is between 1 to 5 years. Therefore

long term milestones have an estimated 5 year period, short term milestones up

to two years and medium in between. Since Germany, despite being one of the

Corridor states, is not involved in this study, stakeholders concerned in the

Action Plan are those in Belgium, the Netherlands and in Poland.

While all of these milestones are made for the Corridor, a few of them are of

particular relevance for Belgium. Given this, we deduct from the Action Plan

Complete Version the milestones that are custom-made for Belgium.

1 Reference: NEA (2010), Study ‐ Exploiting the Possibility of creating a rail freight corridor linking Poland and the Netherlands, Zoetermeer, 2010

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

10 R20100134.doc September 2010

As seen in Table 1.4, in total fourteen milestones focus on Belgium (They are

also marked * in Appendix 6.1).

Table 1.4: Action plan particularly for Belgium on Rail Freight Corridor Belgium -

Poland

Measures Milestones Primary

Stakeholders

Level of

Work-

load

Implemen-

tation

Period

(1) *Improve synchronisation of timetabling

with the Corridor members: taking into

account of, among others, the integrative

planning of alternative routes BE/NL – DE

including part of the ERTMS corridor A, C, &

F, Montzen route, and Iron Rhine.

IMs Medium Short-term

(2) *Extend to the Corridor the Beligum

policy of surcharge of cancelling train-paths

reserved by RUs in order to stimulate RUs

to make efficient planning and avoid

possible discriminative actions.

IMs Medium Short-term I. Achieving

Corridor Path

Planning (5) *Explore possibility to provide updated,

delay-related information (e.g. data from

Europtirail) timely available also to rail

operators who have direct, frequent

contacts with customers, so that rail

operators and LSPs (logistics service

providers) can timely adjust operational &

logistical planning according to new

situations.

IMs Medium Short-term

III. Achieving

Corridor

Capacity

Planning

(2) *Plan medium/long term scenarios of

state financing on removing capacity

bottlenecks, taking into account its

consistency with TEN-T and ERTMS

progress, and with the maintenance,

upgrade, reconstruction, and charging

planning of the Corridor states.

IMs Medium Long-term

IV. Establishing

Corridor

Performance

Regime

(3) *Derive appropriate incentives for IMs

or RUs to improve the reliability and traffic

performance along the Corridor.

IMs Low Medium-term

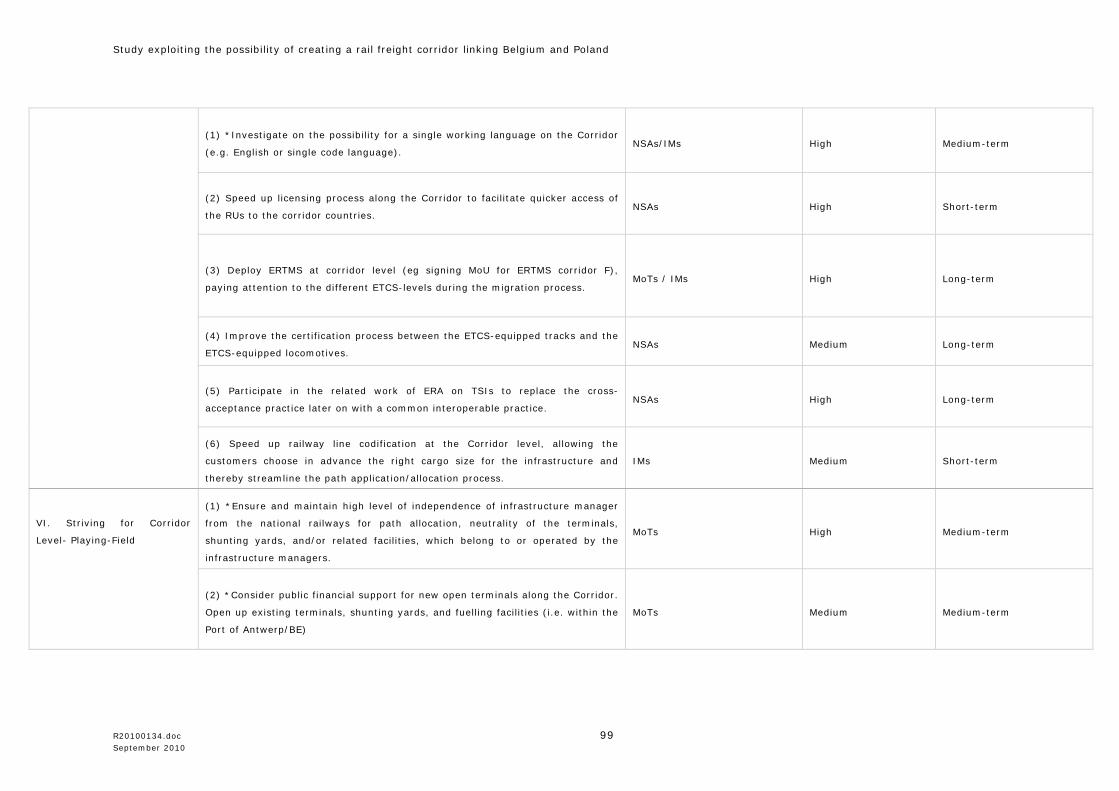

(1) *Investigate on the possibility for a

single working language on the Corridor

(e.g. English or single code language).

NSAs/IMs High Medium-term

V. Improving

Corridor

Interoperability

(2) Speed up licensing process along the

Corridor to facilitate quicker access of the

RUs to the corridor countries.

NSAs High Short-term

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 11 September 2010

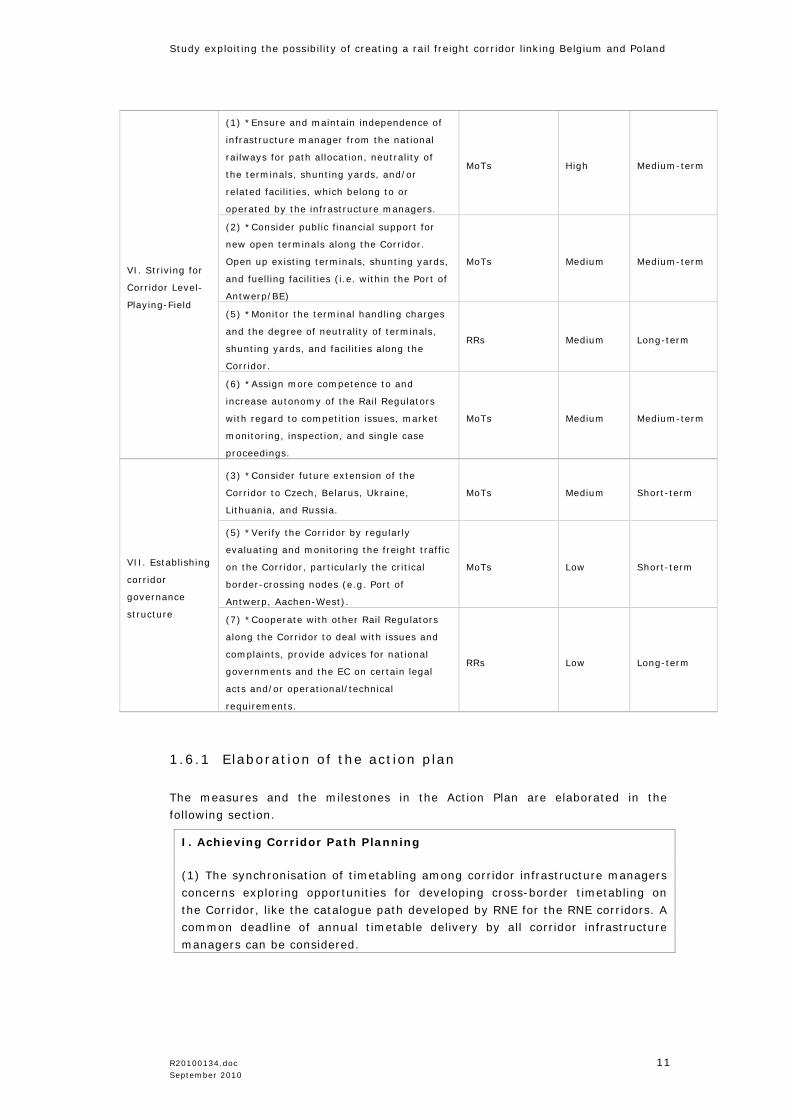

(1) *Ensure and maintain independence of

infrastructure manager from the national

railways for path allocation, neutrality of

the terminals, shunting yards, and/or

related facilities, which belong to or

operated by the infrastructure managers.

MoTs High Medium-term

(2) *Consider public financial support for

new open terminals along the Corridor.

Open up existing terminals, shunting yards,

and fuelling facilities (i.e. within the Port of

Antwerp/BE)

MoTs Medium Medium-term

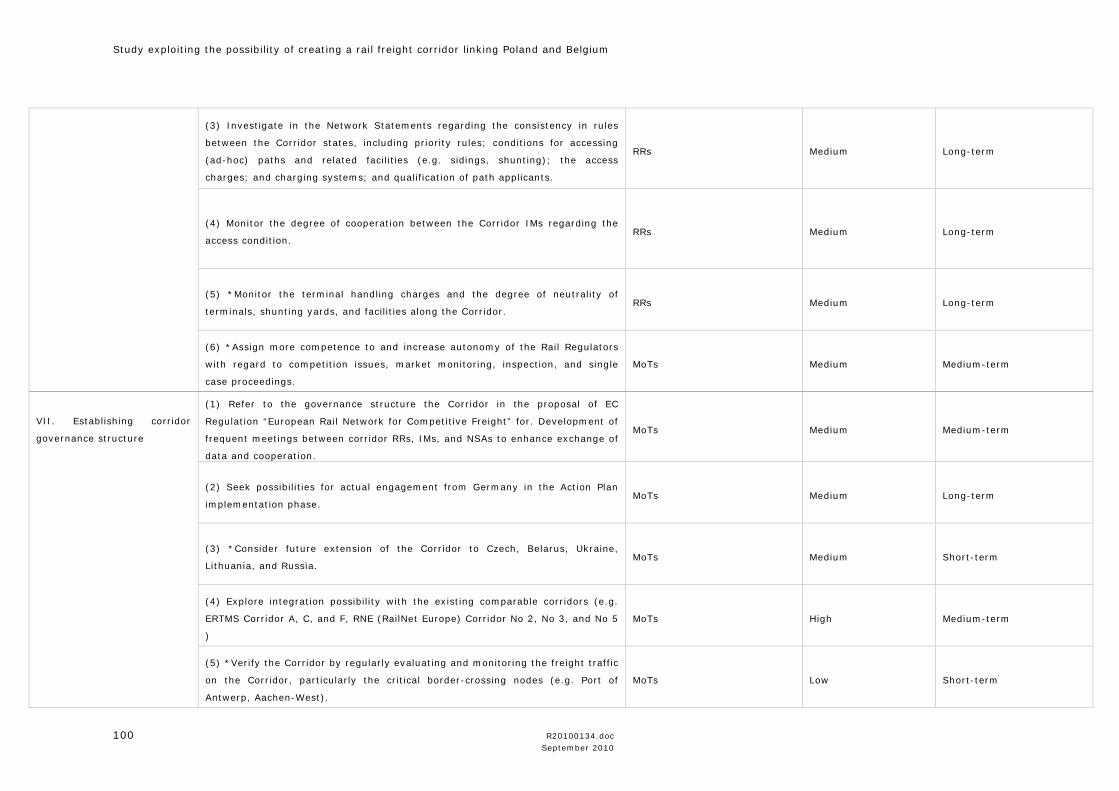

(5) *Monitor the terminal handling charges

and the degree of neutrality of terminals,

shunting yards, and facilities along the

Corridor.

RRs Medium Long-term

VI. Striving for

Corridor Level-

Playing-Field

(6) *Assign more competence to and

increase autonomy of the Rail Regulators

with regard to competition issues, market

monitoring, inspection, and single case

proceedings.

MoTs Medium Medium-term

(3) *Consider future extension of the

Corridor to Czech, Belarus, Ukraine,

Lithuania, and Russia.

MoTs Medium Short-term

(5) *Verify the Corridor by regularly

evaluating and monitoring the freight traffic

on the Corridor, particularly the critical

border-crossing nodes (e.g. Port of

Antwerp, Aachen-West).

MoTs Low Short-term VII. Establishing

corridor

governance

structure (7) *Cooperate with other Rail Regulators

along the Corridor to deal with issues and

complaints, provide advices for national

governments and the EC on certain legal

acts and/or operational/technical

requirements.

RRs Low Long-term

1.6.1 Elaboration of the action plan

The measures and the milestones in the Action Plan are elaborated in the

following section.

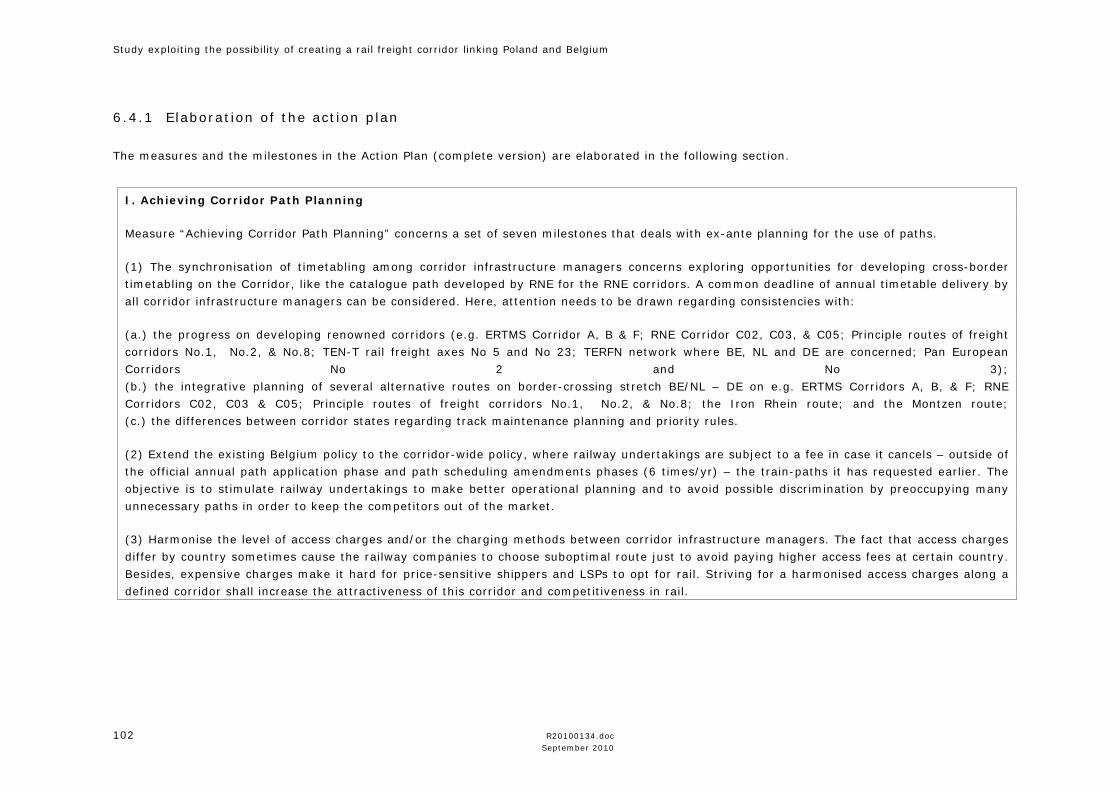

I. Achieving Corridor Path Planning

(1) The synchronisation of timetabling among corridor infrastructure managers

concerns exploring opportunities for developing cross-border timetabling on

the Corridor, like the catalogue path developed by RNE for the RNE corridors. A

common deadline of annual timetable delivery by all corridor infrastructure

managers can be considered.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

12 R20100134.doc September 2010

Here, attention needs to be drawn regarding consistencies with:

(a.) the progress on developing renowned corridors (e.g. ERTMS Corridor A, B

& F; RNE Corridor C02, C03, & C05; Principle routes of freight corridors No.1,

No.2, & No.8; TEN-T rail freight axes No 5 and No 23; TERFN network where

BE, NL and DE are concerned; Pan European Corridors No 2 and No 3);

(b.) the integrative planning of several alternative routes on border-crossing

stretch BE/NL – DE on e.g. ERTMS Corridors A, C, & F; RNE Corridors C02, C03

& C05; Principle routes of freight corridors No.1, No.2, & No.8; the Iron Rhein

route; and the Montzen route,);

(c.) the differences between corridor states regarding track maintenance

planning and priority rules.

(2) Extend the existing Belgium policy to the corridor-wide policy, where

railway undertakings are subject to a fee in case it cancels – outside of the

official annual path application phase and path scheduling amendments phases

(6 times/yr) – the train-paths it has requested earlier. The objective is to

stimulate railway undertakings to make better operational planning and to

avoid possible discrimination by preoccupying many unnecessary paths in order

to keep the competitors out of the market.

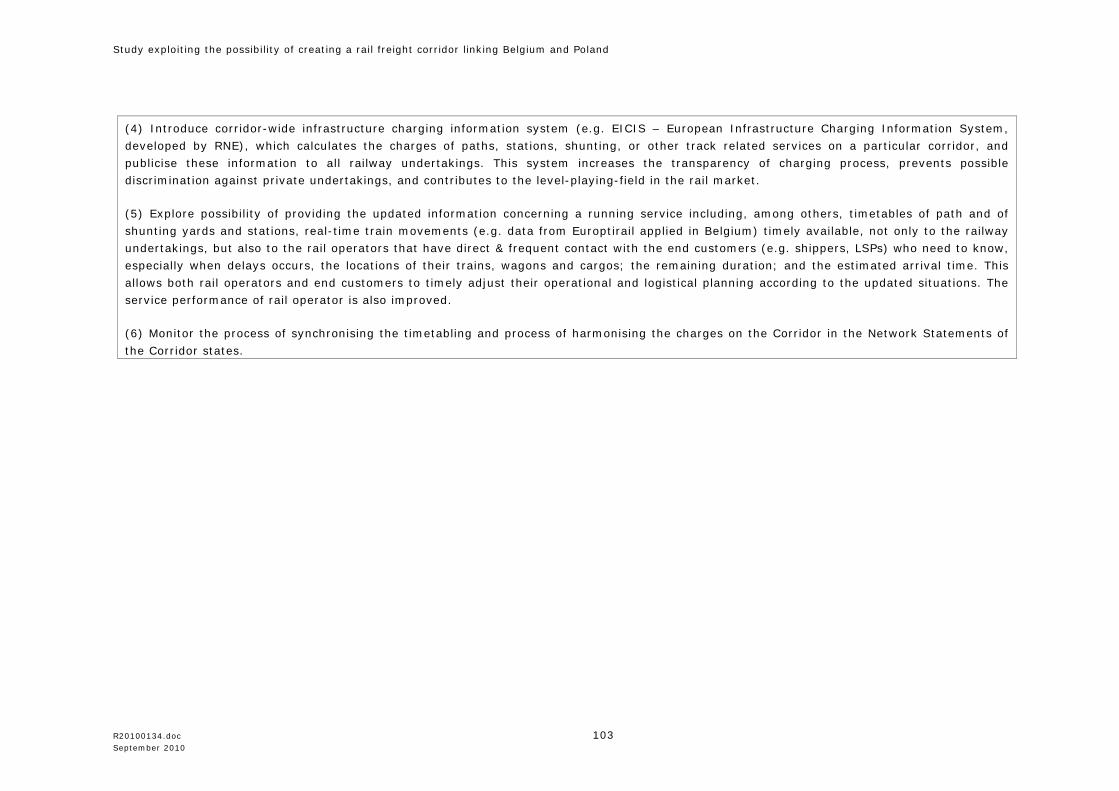

(5) Explore possibility of providing the updated information concerning a

running service including, among others, timetables of path and of shunting

yards and stations, real-time train movements (e.g. data from Europtirail

applied in Belgium) timely available, not only to the railway undertakings, but

also to the rail operators that have direct & frequent contact with the end

customers (e.g. shippers, LSPs) who need to know, especially when delays

occurs, the locations of their trains, wagons and cargos; the remaining

duration; and the estimated arrival time. This allows both rail operators and

end customers to timely adjust their operational and logistical planning

according to the updated situations. The service performance of rail operator is

also improved.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 13 September 2010

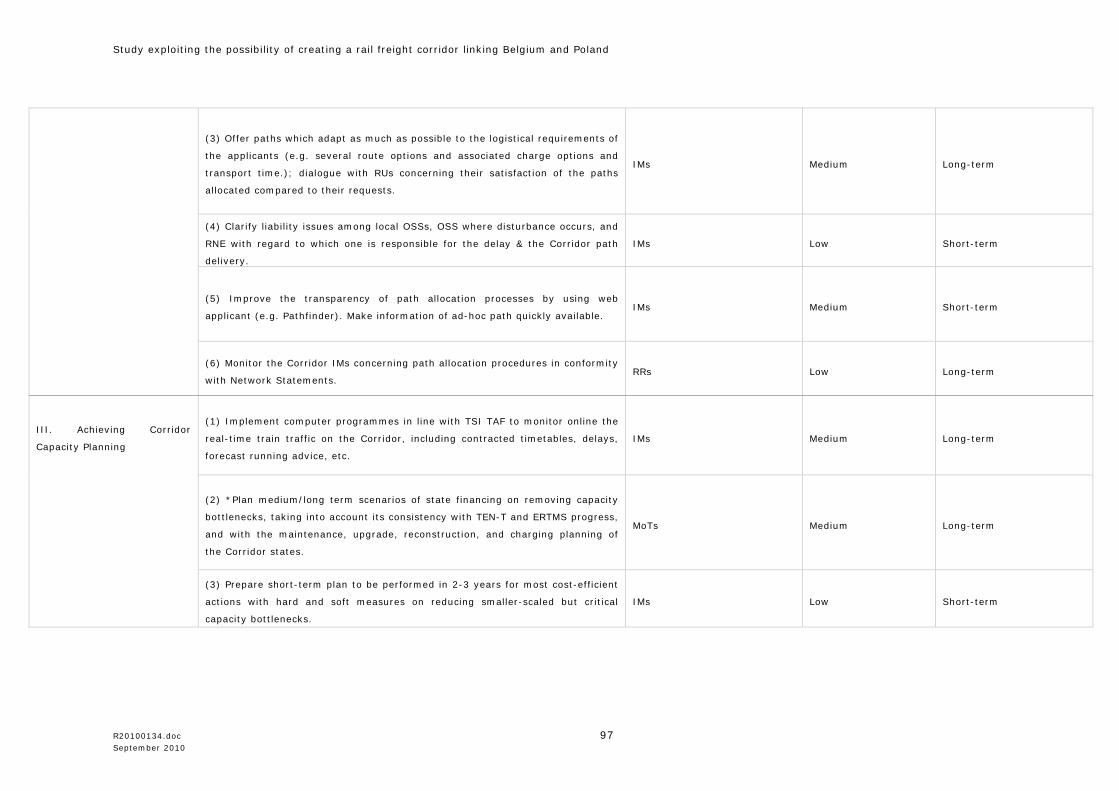

III. Achieving Corridor Capacity Planning

(2) Based on the results of capacity analysis, make medium- and long- term

scenarios of infrastructure financing in order to anticipate capacity growth and

mitigate capacity bottlenecks from technical and operational constraints. These

scenarios need to focus on both the tracks within the country and tracks

linking gates and hubs at border-crossing areas (e.g. Port of Antwerp, terminal

Aachen-West, Port of Rotterdam; Zevenaar – Emmerich; Oldenzaal – Bad

Bentheim; Frankfurt (Oder) – Kunowice; Horka – Bielawa Dolna; Szczecin).

The infrastructure planning also needs to be consistent with the rail projects in

TEN-T (e.g. priority axes No 5), and the progress on ERTMS corridor A, C and

F. This shall also take into account the maintenance, upgrading and

reconstruction, and the charging plan of the corridor states. In Beligum,

current investment plan is for period 2001-2012 and the next investment plan

2013-2025 is under preparation.

IV. Establishing Corridor Performance Regime

(3) Since causes and duration of delays could be monitored via the EPR

(European Performance Regime), implementation of appropriate financial

incentives can be suggested for infrastructure managers or railway

undertakings to improve the traffic performance and the reliability of train

services along the Corridor.

V. Improving Corridor Interoperability

(1) Introduce cross-acceptance of approval procedure of rolling stocks on the

Corridor by using the IRL (International Requirement List) in conformity with

the common checklist according to the EC Directive 2008/57/EC. Scale up the

existing bilateral agreements between NL-DE for cross acceptance of train

crews to a corridor-wide implementation, in conformity with the Directive

2007/59 on engine driver licensing and certification. Consider using the same

approach for cross-acceptance of freight wagon if necessary. Increase time and

cost efficiency of this procedure. Have dialogue with the railway undertakings

for impact assessment of this cross-acceptance action.

(2) Investigate the possibilities to achieve using one single working language

for service operation, for example in English or code language, in accordance

with the TSI regarding working language for service operation that is codified

in TSI Operations Chapter 4.2.1.5. However, it should be born in mind that

compatibility with relevant Belgium legislation (i.e. law of 1962) should be

taken into account.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

14 R20100134.doc September 2010

VI. Striving for Corridor Level-playing-field

(1) Ensure and maintain independence of the infrastructure managers from the

national railway companies for path allocation; and keep neutral and open

those terminals, shunting yards, and/or related facilities which belong to or

operated by the infrastructure managers. To reduce further possible

discriminative behaviours of the national railways, the option to break down

the holding structure to which both infrastructure manager and railway

undertaking belong can be considered, since this structure seems to bring

doubts internally and externally regarding the level of independence of the

infrastructure managers from the national railway undertaking. However, the

compatibility with relevant EC legislation should be taken into account.

However, this only applies if the holding structure is not compatible with

relevant EC legislation.

(2) Public financial support to the construction of new open terminals along the

Corridor (the Netherlands (e.g. in Valburg, and Poland). Open up the existing

terminals, shunting yards, and fuelling facilities in Belgium (i.e. Port of

Antwerp). This milestone shall improve the accessibility of (intermodal)

infrastructure facilities along the entire corridor.

(5) The corridor Rail Regulators are also recommended, if possible, to take the

monitoring role in assessing the discrepancies in handing charges between

different terminals, as well as the degree of neutrality of terminals, shunting

yards, and other facilities open to all railway undertakings.

(6) Increase the scope of competence of the corridor Rail Regulators with

regard to imposing penalty on competition issues, inspection, market

monitoring power, and competence of carrying out single case proceedings. A

complete separation of the Rail Regulator from the government increases its

level of independence and neutrality. This shall help implement the above

tasks more effectively and ensure level-playing-field on the Corridor.

VII. Establishing Corridor Governance Structure

(3) Extension of the Corridor is needed in the future to correspond to the

traffic flows. In particular, extending the Corridor to other bordering countries

on the other side, need to be considered (e.g. Czech, Belarus, Ukraine,

Lithuania and Russia)..

(5) Verify the Corridor by regularly monitoring and evaluating the freight

traffic along the Corridor, paying particular attention to the traffic that passes

critical border-crossing points (e.g. Port of Antwerp; Port of Rotterdam;

Montzen-Aachen; Essen – Roosendaal along Corridor C; Zevenaar – Emmerich;

Odenzaal – Bad Bentheim; Franktfurt (Oder) – Kunowice; Horka – Bielawa

Dolna; Szczecin.)

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 15 September 2010

(7) Cooperate with other Rail Regulators along the Corridor for identifying

crucial issues and dealing with complaints relevant for the Corridor; based on

which provide advices for national governments and the EC regarding

possibilities of adjusting certain legal acts and/or harmonising certain

operational and technical requirements.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 17 September 2010

2 Current situation on the market and its’ potential for further development

2.1 Freight volumes analysis on the corridor Belgium – Poland / Czech Republic

2.1.1 Background and Methodology

In 2008 about 60 million tons of goods were transported over the Belgian railway

system. The rail freight market in Belgium appears to be very international

oriented as in 2008 63% of the transported tons have an international link. This

% even rises to 74% if we consider tonkm instead of tons1. The focus of this

document lies on the transport flows between Poland and the Czech Republic and

Belgium. Previously, TNO(2008) made a similar scenario calculation for the rail

corridor Netherlands-Poland.

TML produced scenario calculations for rail freight transport (and other modes of

transport) between Belgium and Germany, Poland and the Czech Republic. This

has been done for a number of scenarios (low growth, trend growth and high

growth) and for three time horizons 2020, 2030 and 2040. These scenario

calculations provide good insight in the current and future expected rail freight

flows on the corridor Belgium – Germany – Poland – Czech Republic. Besides, by

analyzing transport of other modes also freight flows can be identified that are

potential for rail freight transport.

Methodology

An important starting point for the scenario calculations are the Traffic Forecasts

Iron Rhine (2007), the TNO study on scenario calculations Rail freight transport

on corridor Netherlands – Poland (2009) and the study by the Bundesamt für

Güterverkehr (2010). Furthermore a study analyzing rail freight flows in Belgium

by FOD Economie, KMO, Middenstand en Energie (2010) and data originating

from the TRANS-TOOLS model2 was also used. Note that both the Traffic

Forecasts for the Iron Rhine and the TNO study made forecasts for rail freight

using the European transport model TRANS-TOOLS as a base.

Scenarios

The background scenarios are the same as in the scenarios used in the Traffic

Forecasts of the Iron Rhine and in the TNO study. They differ in the assumed

economic growth and in the assumed transport policy.

1 FOD Economie, KMO, Middenstand en Energie (2010); Analyse van het goederenvervoer per

spoor in België. 2 http://energy.jrc.ec.europa.eu/transtools/TT_model.html

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

18 R20100134.doc September 2010

Key uncertainties in scenarios

The approach used has a number of uncertainties. More specifically, the following

uncertainties are identified:

• Representativeness and validity of base year

• Socio-economic developments

• Developments in the transport market, including the potential reactivation of

the Iron Rhine

The next sections describe the way these uncertainties have been treated in the

modeling approach.

Representativeness and validity of base year

2007 was chosen as a base year as it is also the base year in the TNO report.

This year was chosen as the base given the recent strong development of rail

transport, which was believed to be structural. Using older data would not take

into account these changes.

We first compared data on transport flows, reported in the following studies:

• the traffic forecasts Iron Rhine (2007)

• the TNO study (2008)

• original Transtools data

• the study by Bundesamt für Güterverkehr (2010)

• the study by FOD Economie (2010)

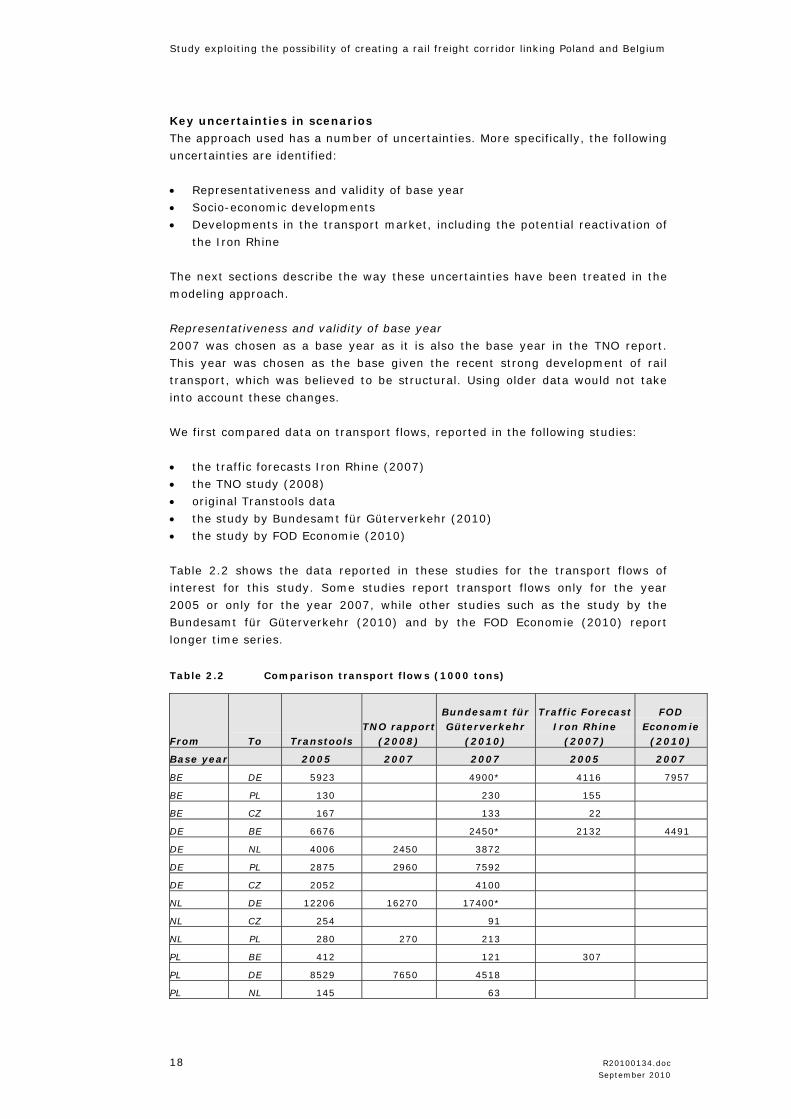

Table 2.2 shows the data reported in these studies for the transport flows of

interest for this study. Some studies report transport flows only for the year

2005 or only for the year 2007, while other studies such as the study by the

Bundesamt für Güterverkehr (2010) and by the FOD Economie (2010) report

longer time series.

Table 2.2 Comparison transport flows (1000 tons)

From To Transtools TNO rapport

(2008)

Bundesamt für Güterverkehr

(2010)

Traffic Forecast Iron Rhine

(2007)

FOD Economie

(2010)

Base year 2005 2007 2007 2005 2007

BE DE 5923 4900* 4116 7957

BE PL 130 230 155

BE CZ 167 133 22

DE BE 6676 2450* 2132 4491

DE NL 4006 2450 3872

DE PL 2875 2960 7592

DE CZ 2052 4100

NL DE 12206 16270 17400*

NL CZ 254 91

NL PL 280 270 213

PL BE 412 121 307

PL DE 8529 7650 4518

PL NL 145 63

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 19 September 2010

CZ BE 296 68 92 99

CZ DE 6142 3721

CZ NL 293 65

* Data for 2008 in stead of for 2007

The comparison is not always straightforward as different base years are

reported, but in general the orders of magnitude correspond. Notable are the

differences between the transport flows reported between:

• Belgium and Germany by the German Bundesamt für Güterverkehr (2010)

and the Belgian FOD Economy (2010). Figures stated differ with a factor 1.6

for the direction Belgium-Germany and a factor 1.8 in the direction Germany-

Belgium.

• Belgium and the Czech Republic, where the Bundesamt für Güterverkehr

(2010) reports a transport flow which is about 6 times higher than the

volumes used in the Traffic Forecasts Iron Rhine. Notable here is that the

German study reports transport flows between Belgium and the Czech

Republic of 49 thousand tons in 2005 and of 45 thousand tons in 2009,

making the difference much smaller. Hence, there seems to be a lot of

fluctuations in these transport flow.

• Germany and Poland in the TNO study and the Bundesamt für Güterverkehr

(2010). The number stated by Bundesamt für Gütereverkehr (2010) is about

2.5 times higher than the numbers stated by TNO (2008).

None of the data sources can be used as a single starting point as none of the

studies report data for all links needed. We have opted for freight rail transport

to combine the results of the Traffic Forecasts and the study by the Bundesamt

für Güterverkehr (2010) as this combination leads to the greatest consistency

and as the Traffic Forecast figures where checked with data from B-rail.

Remember that both studies gave very different results for the Czech Republic.

We have opted to use the number stated by the vervoersprognoses as:

• the time series reported by the Bundesamt für Güterverkehr (2010) show

that in most years traffic flows are closer to the 22 thousand tons used in the

Iron Rhine forecasts than the 133 thousand tons reported for the year 2007.

• it was asked to be as consistent as possible with the Iron Rhine forecast

study.

For freight transport using other modes such as road and inland waterways we

relied on TRANS-TOOLS -data.

Apart from the problems with the initial data itself, opting for 2007 also implies

that the recent economic crisis is not taken into account. The study by

Bundesamt für Güterverkehr (2010) clearly shows a sharp decline in rail

transport between 2008 and 2009. For example, the number of goods train in

the year 2009 fell by 21% to 67 trains a day in each direction for east-west

transport operations. During the same period, the volume of transport from

Germany in the direction of the CEE countries fell by almost 50%, mainly due to

a strong decline in transport between Germany and Poland. In westwards

direction, total transport volume decreased by roughly 9% compared to 2008.

Hence, using data for 2009 – if available – would lead to a very different picture.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

20 R20100134.doc September 2010

Considering both elements, the representativeness and validity of the base year

is one of the key uncertainties in the scenarios.

Socio-economic developments

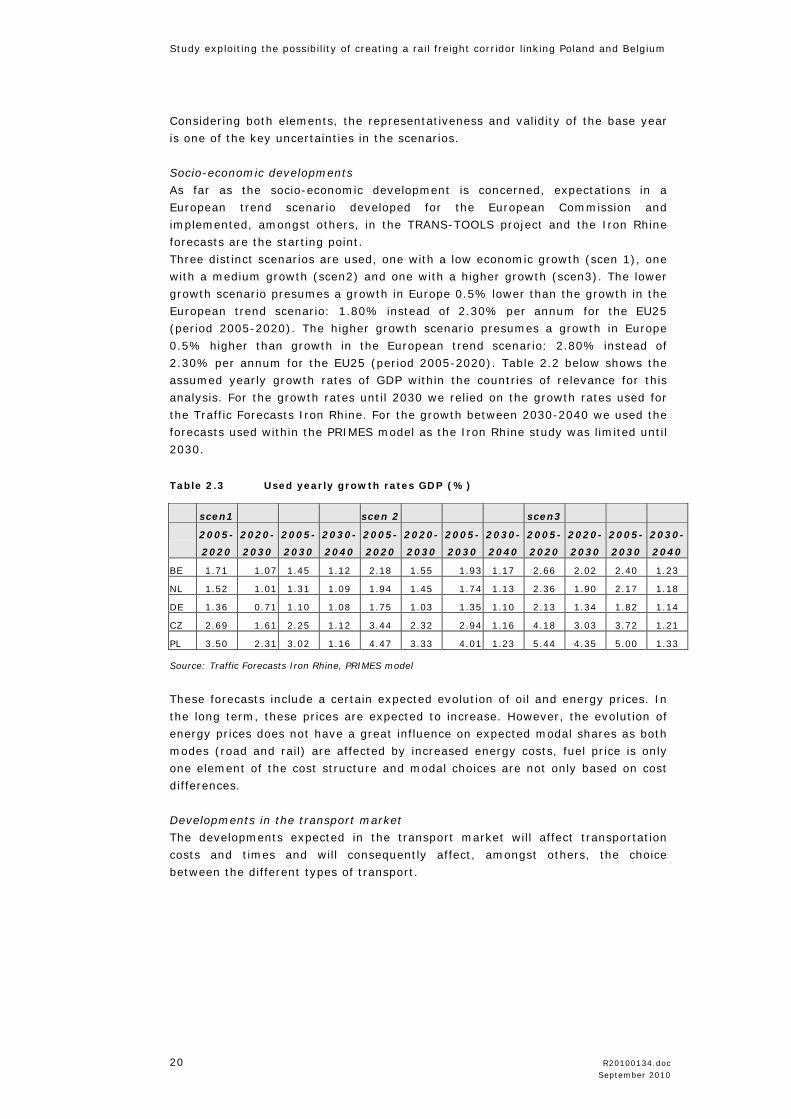

As far as the socio-economic development is concerned, expectations in a

European trend scenario developed for the European Commission and

implemented, amongst others, in the TRANS-TOOLS project and the Iron Rhine

forecasts are the starting point.

Three distinct scenarios are used, one with a low economic growth (scen 1), one

with a medium growth (scen2) and one with a higher growth (scen3). The lower

growth scenario presumes a growth in Europe 0.5% lower than the growth in the

European trend scenario: 1.80% instead of 2.30% per annum for the EU25

(period 2005-2020). The higher growth scenario presumes a growth in Europe

0.5% higher than growth in the European trend scenario: 2.80% instead of

2.30% per annum for the EU25 (period 2005-2020). Table 2.2 below shows the

assumed yearly growth rates of GDP within the countries of relevance for this

analysis. For the growth rates until 2030 we relied on the growth rates used for

the Traffic Forecasts Iron Rhine. For the growth between 2030-2040 we used the

forecasts used within the PRIMES model as the Iron Rhine study was limited until

2030.

Table 2.3 Used yearly growth rates GDP (%)

scen1 scen 2 scen3

2005-

2020

2020-

2030

2005-

2030

2030-

2040

2005-

2020

2020-

2030

2005-

2030

2030-

2040

2005-

2020

2020-

2030

2005-

2030

2030-

2040

BE 1.71 1.07 1.45 1.12 2.18 1.55 1.93 1.17 2.66 2.02 2.40 1.23

NL 1.52 1.01 1.31 1.09 1.94 1.45 1.74 1.13 2.36 1.90 2.17 1.18

DE 1.36 0.71 1.10 1.08 1.75 1.03 1.35 1.10 2.13 1.34 1.82 1.14

CZ 2.69 1.61 2.25 1.12 3.44 2.32 2.94 1.16 4.18 3.03 3.72 1.21

PL 3.50 2.31 3.02 1.16 4.47 3.33 4.01 1.23 5.44 4.35 5.00 1.33

Source: Traffic Forecasts Iron Rhine, PRIMES model

These forecasts include a certain expected evolution of oil and energy prices. In

the long term, these prices are expected to increase. However, the evolution of

energy prices does not have a great influence on expected modal shares as both

modes (road and rail) are affected by increased energy costs, fuel price is only

one element of the cost structure and modal choices are not only based on cost

differences.

Developments in the transport market

The developments expected in the transport market will affect transportation

costs and times and will consequently affect, amongst others, the choice

between the different types of transport.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 21 September 2010

Within the Traffic Forecasts of the Iron Rhine, two distinct scenarios concerning

the developments in the transport market were used:

• A scenario (scenario A) with moderate developments including the

liberalization of rail transport;

• A more extensive scenario (scenario B) including the developments of the

previous scenario and including charges for external costs.

The moderate scenario A is based on a continuation of current policies. This

includes the policy as proposed by the European Commission in its White Paper

(European Commission, 2001), and in addition to it, Keep Europe Moving

(European Commission, 2006). One of the goals of this policy is to achieve a

shift from transportation by road to inland waterways and rail transportation.

For infrastructure, all projects currently in progress and all those that have

passed the definitive decision to be built have been included. For rail, it is

implicitly assumed that the capacity can facilitate any increase in demand, thus

the same transportation time can be offered. There are (except for the well-

known planned projects) no new rail connections expected. With respect to the

reactivation of the Iron Rhine, the traffic forecasts showed that the largest

potential for the Iron Rhine comes from economic growth and shifts from other

rail tracks. The reactivation of the Iron Rhine would cause only a small modal

shift.

The main reason for this small modal shift is that the reactivation of the Iron

Rhine mainly influences transport in the region Antwerp and North-Rhine-

Westfalen. The distance between these areas is relatively short; this is, less than

200 km. For such short distance, no large modal shifts can be expected as – in

general – rail transport is not concurrent on short distances. In summary, the

reactivation of the Iron Rhine does not really influence the scenario forecasts.

For rail transport a user charge of € 2.50 (real) per train kilometer is assumed

for the whole period 2020-2040 throughout Europe. Currently, the rate for most paths is lower in Belgium with prices varying around 1.4-2.5 euro/km1. Prices

vary with traction, time, weight, etc. A rail fee increase is expected in order to

charge all costs caused by the user to the user. A similar charge will be applied

in all countries across Europe. For road, a toll of € 0.15 per vehicle kilometer is

expected for the entire period 2020-2040 for the whole of Europe.

Furthermore, for the whole of Europe liberalization of the rail market across

Europe is expected including the implementation of the so-called "third railway

package". Due to this fact it is expected that the level of rail service will improve

(lower turnaround time and lower transport costs).

In the more extensive scenario B, it is also assumed, in addition to all these

developments, that a charge on external costs is introduced. Table 2.3 shows the

rates for freight.

1 Based on calculations using information stated in Infrabel (2009) for 2 routes and for two time

periods

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

22 R20100134.doc September 2010

Table 2.4 Charges external freight costs.

2020 2030-2040

Road 0,075 euro/vrtgkm 0,15 euro/vrtgkm

Rail 0,005 euro/tkm 0,01 euro/tkm

Inland shipping 0,005 euro/tkm 0,01 euro/tkm

Source: Traffic Forecasts Iron Rhine (2007)

Combination of key uncertainties

By combining the different variants of the socio-economic development (low,

moderate, high) with the variants of the development in the transport market

(moderate, more extensive) 6 different scenarios can be distinguished. The

combination of low economic growth with further developments in the transport

market and the combination of high economic growth with moderate

developments in the transport market will not be used because they add little to

the range of scenarios. Besides that, the combination of moderate economic

growth with further developments in the transport market is not used because

this scenario is slightly distinctive compared to the scenario of moderate

economic growth with moderate developments in the transport market.

Finally, following the TNO study and the Iron Rhine forecasts, the three following

combinations were chosen to be further elaborated:

• Low economic growth, moderate developments in the transport market

(LG scenario);

• Moderate economic growth, moderate developments in the transport

(GG scenario);

• High economic growth, further developments in the transport (HV scenario).

Among these three, the GG scenario can be considered as the reference. This

scenario contains the European trend scenario in terms of economic growth. In

terms of developments in the transport market it is close to the proposed policy

and the anticipated developments of the future. This scenario describes current

and expected future developments, not taking into account 'extreme'

developments. These three scenarios are combined with three time horizons,

namely 2020, 2030 and 2040. This means that there have been made

calculations for 9 scenario situations (3 scenarios for each of the 3 time

horizons).

Table 2.5 Overview of distinguished scenarios

2020 2030 2040

Low economic growth, moderate developments transport market (LG) X X X

Moderate economic growth, moderate developments transport market (GG) X X X

High economic growth, further developments transport markt (HV) X X X

Methodology rail corridor Belgium – Poland/Czech Republic study

For the rail corridor Belgium – Poland/Czech Republic, the transport flows from

the Traffic forecasts Iron Rhine and Bundesamt für Güterverkehr study are the

basis. However, a number of modifications have been made.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 23 September 2010

The modifications mainly concern the base year data. The Iron Rhine study data

is upgraded to the year 2007 using the TNO study and the German study.

Then in a next step new scenario calculations have been made with TRANS-

TOOLS and the results of the TNO study. based on updated base year data. In

the next figure an overview is given of the annual growth of GDP in the European

trendscenario. In the past, total transport grew faster than GDP in the EU25,

while rail transport grew slower than GDP (FOD Economie, 2010).

Concerning the results, it is stressed that the scenario calculations are mainly

based on macro-economic developments. Specific developments in the rail

freight market in this corridor are not taken into account.

2.1.2 Results

Rail freight volumes on the corridor in 2007

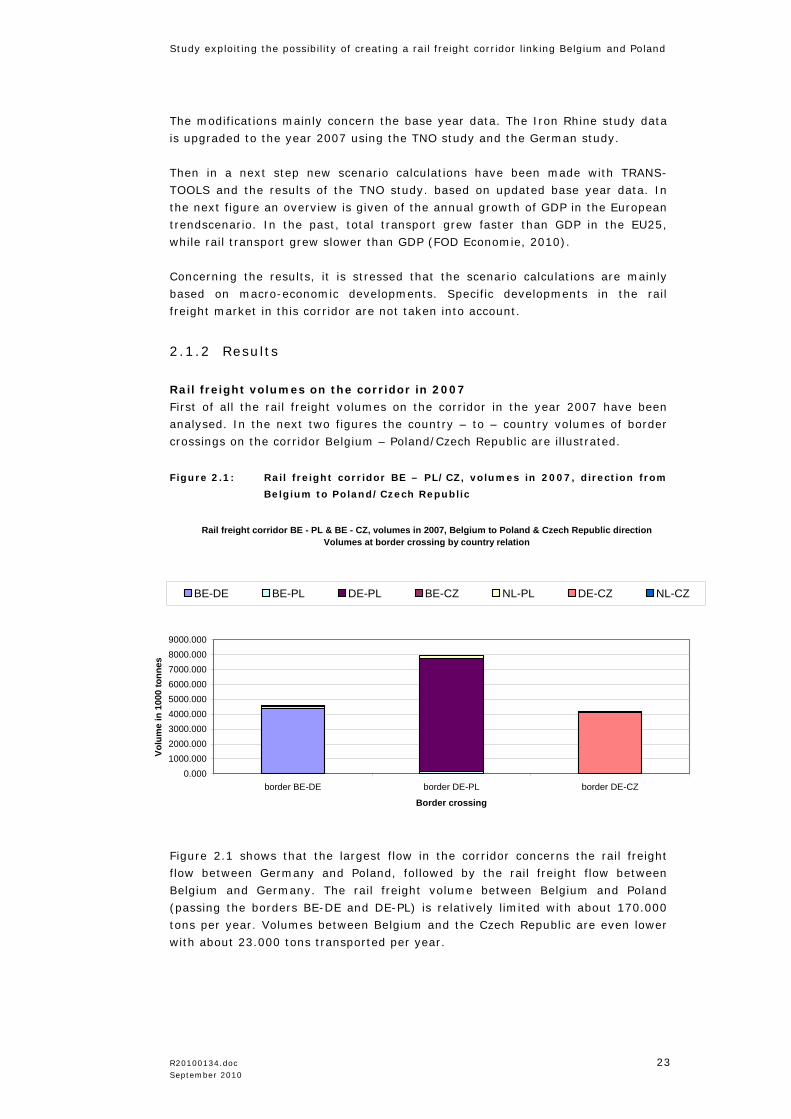

First of all the rail freight volumes on the corridor in the year 2007 have been

analysed. In the next two figures the country – to – country volumes of border

crossings on the corridor Belgium – Poland/Czech Republic are illustrated.

Figure 2.1: Rail freight corridor BE – PL/CZ, volumes in 2007, direction from

Belgium to Poland/Czech Republic

Rail freight corridor BE - PL & BE - CZ, volumes in 2007, Belgium to Poland & Czech Republic directionVolumes at border crossing by country relation

0.0001000.0002000.0003000.0004000.0005000.0006000.0007000.0008000.0009000.000

border BE-DE border DE-PL border DE-CZ

Border crossing

Volu

me

in 1

000

tonn

es

BE-DE BE-PL DE-PL BE-CZ NL-PL DE-CZ NL-CZ

Figure 2.1 shows that the largest flow in the corridor concerns the rail freight

flow between Germany and Poland, followed by the rail freight flow between

Belgium and Germany. The rail freight volume between Belgium and Poland

(passing the borders BE-DE and DE-PL) is relatively limited with about 170.000

tons per year. Volumes between Belgium and the Czech Republic are even lower

with about 23.000 tons transported per year.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

24 R20100134.doc September 2010

Figure 2.2 Rail freight corridor BE – PL/CZ, volumes in 2007, direction from

Poland/Czech Republic to Belgium

Rail freight corridor BE - PL & BE - CZ, volumes in 2007, Poland & Czech Republic to Belgium direction

Volumes at border crossing by country relation

0

1000

2000

3000

4000

5000

6000

border PL-DE border CZ-DE border DE-BE

B or de r c r ossi ng

PL-DE PL-BE PL-NL CZ-DE CZ-BE CZ-NL DE-BE

In the direction from Poland/Czech Republic to Belgium, the flow with the highest

volume is between Poland and Germany, followed by the flow between the Czech

Republic and Germany. The volume between Poland and Belgium is about

332.000 tons in 2007 and about 100.000 tons between Czech Republic and

Belgium. The transport flows between Poland/Czech Republic and Belgium are

larger than the flows towards the Netherlands, while in the direction towards

Poland/Czech Republic the volumes departing in the Netherlands are higher than

the ones departing in Belgium.

Next, we consider the transport flows towards and from Germany and Poland in

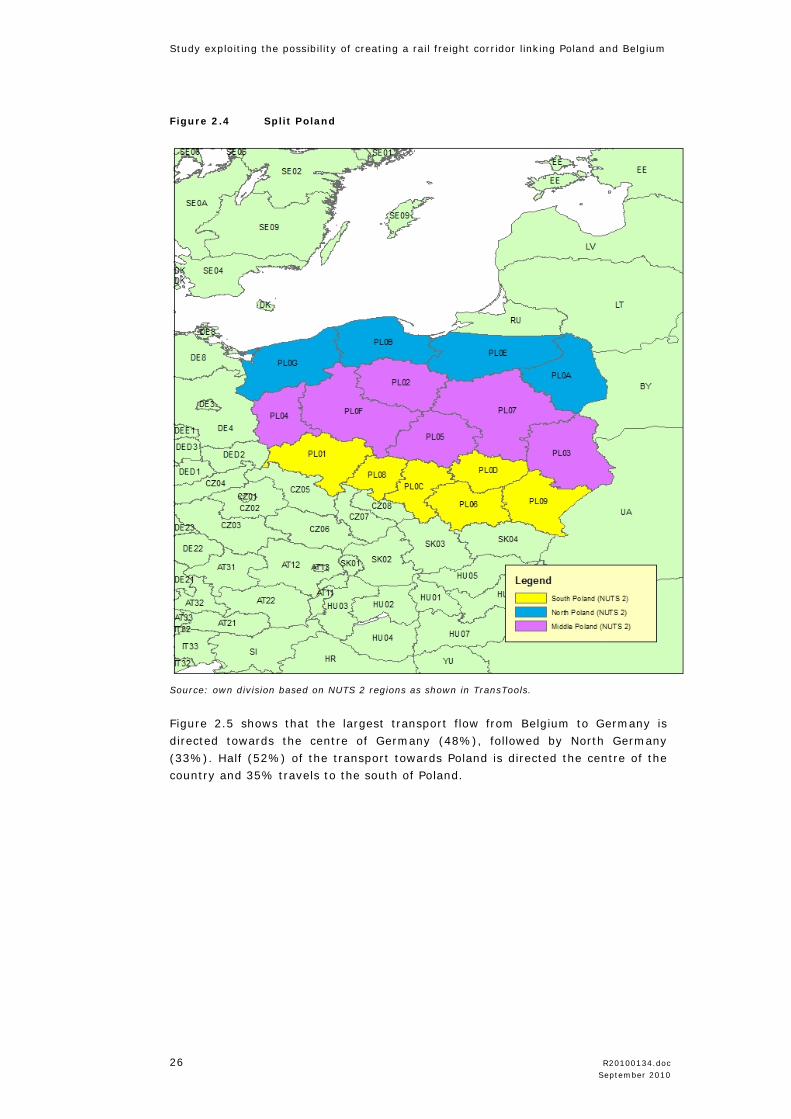

somewhat more detail. We have divided both countries into three parts: a

Northern part, a Central part and a Southern Part. Figures 2.3 and 2.4 show how

both countries are split. Given the size of the country we did not make this

distinction for the Czech Republic.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 25 September 2010

Figure 2.3: Split Germany

Source: own division based on NUTS 2 regions as shown in TransTools

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

26 R20100134.doc September 2010

Figure 2.4 Split Poland

Source: own division based on NUTS 2 regions as shown in TransTools.

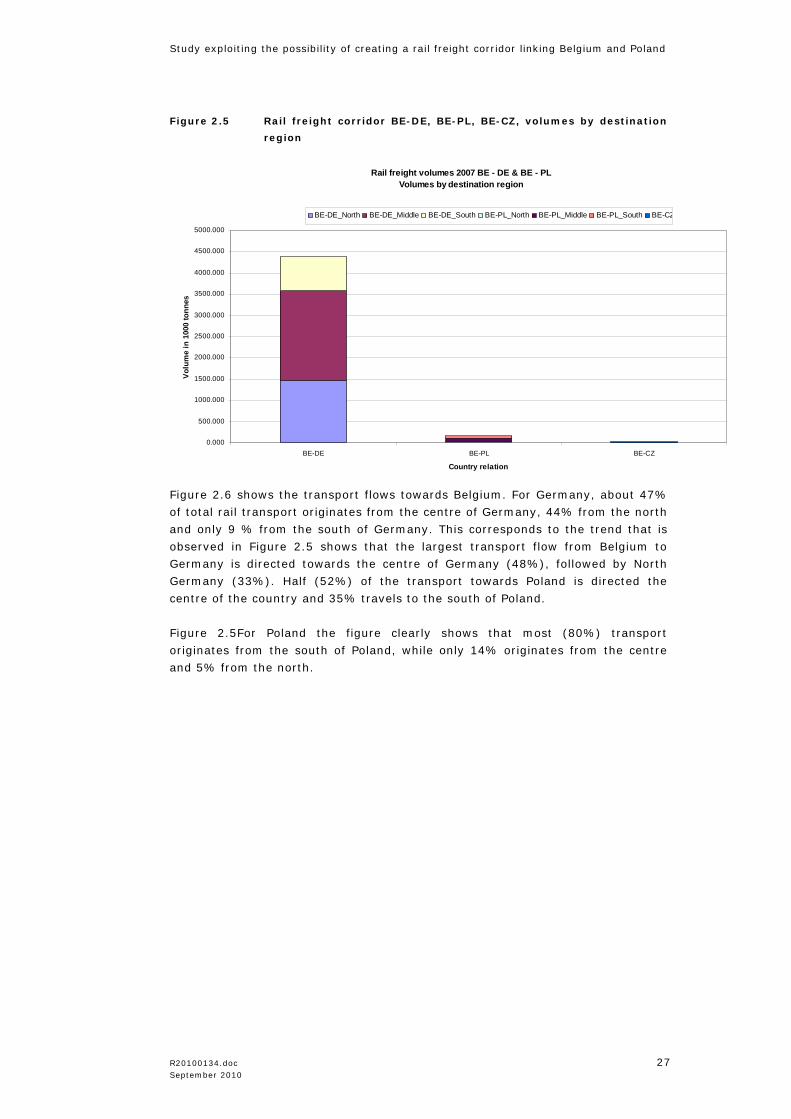

Figure 2.5 shows that the largest transport flow from Belgium to Germany is

directed towards the centre of Germany (48%), followed by North Germany

(33%). Half (52%) of the transport towards Poland is directed the centre of the

country and 35% travels to the south of Poland.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 27 September 2010

Figure 2.5 Rail freight corridor BE-DE, BE-PL, BE-CZ, volumes by destination

region

Rail freight volumes 2007 BE - DE & BE - PL Volumes by destination region

0.000

500.000

1000.000

1500.000

2000.000

2500.000

3000.000

3500.000

4000.000

4500.000

5000.000

BE-DE BE-PL BE-CZ

Country relation

Vol

ume

in 1

000

tonn

es

BE-DE_North BE-DE_Middle BE-DE_South BE-PL_North BE-PL_Middle BE-PL_South BE-CZ

Figure 2.6 shows the transport flows towards Belgium. For Germany, about 47%

of total rail transport originates from the centre of Germany, 44% from the north

and only 9 % from the south of Germany. This corresponds to the trend that is

observed in Figure 2.5 shows that the largest transport flow from Belgium to

Germany is directed towards the centre of Germany (48%), followed by North

Germany (33%). Half (52%) of the transport towards Poland is directed the

centre of the country and 35% travels to the south of Poland.

Figure 2.5For Poland the figure clearly shows that most (80%) transport

originates from the south of Poland, while only 14% originates from the centre

and 5% from the north.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

28 R20100134.doc September 2010

Figure 2.6 Rail freight corridor DE-BE, PL-BE, CZ-BE, volumes by destination

region

Rail freight volumes 2007 DE - BE & PL - BE Volumes by destination region

0.000

500.000

1000.000

1500.000

2000.000

2500.000

DE-BE PL-BE CZ-BE

Country relation

Volu

me

in 1

000

tonn

es

DE_North-BE DE_Middle-BE DE_South-BE PL_North-BE PL_Middle-BE PL_South-BE CZ-BE

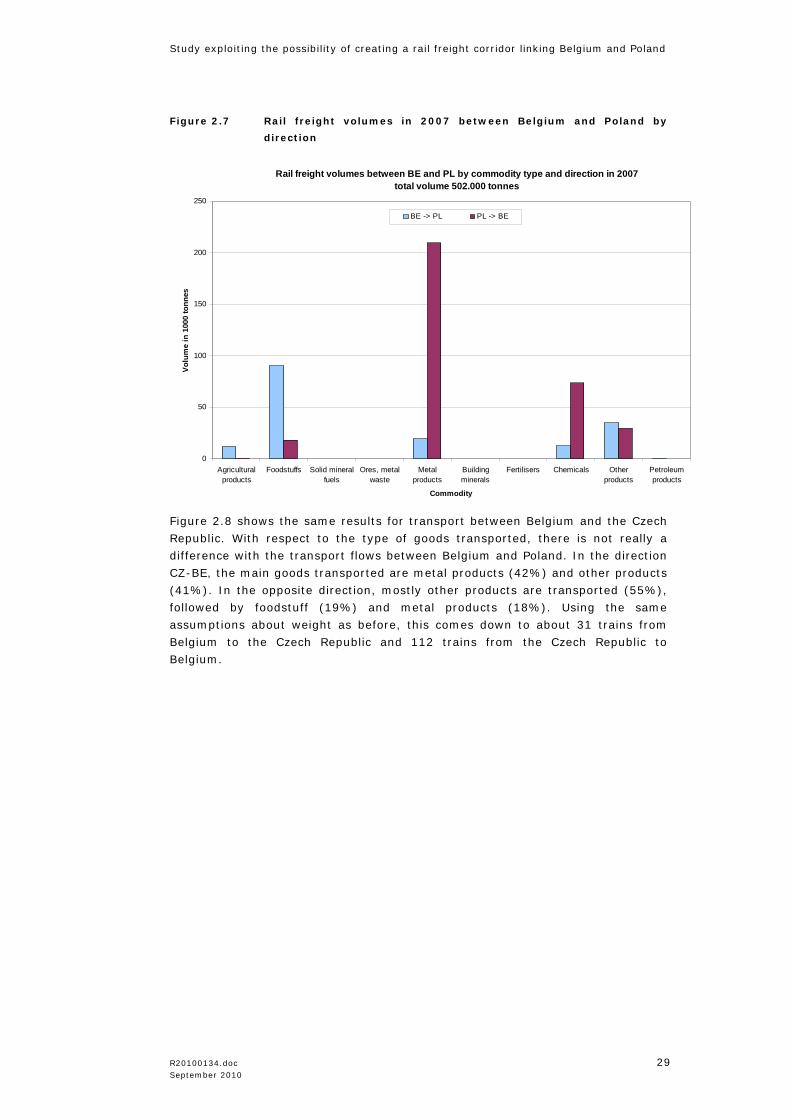

Figure 2.7 shows the rail freight volumes between Belgium and Poland in 2007

by commodity group. The commodity metal products has the highest volumes in

the direction PL-BE, while food stuff and other products have the highest share

in the direction BE-PL. “Other products” concern manufactured goods and

intermediate and final products, these goods are mainly transported in

containers. Lower volumes are transported by rail for the commodities chemicals

and agricultural products. For the other commodities, the volumes are zero or

close to zero. If we assume a loading of 700 ton per train for the goods 0,1,5,8,9

and a loading of about 1200 ton per train for the other types of goods, these

volumes implies that about 223 trains are running from Belgium to Poland and

about 305 trains from Poland to Belgium.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 29 September 2010

Figure 2.7 Rail freight volumes in 2007 between Belgium and Poland by

direction

Rail freight volumes between BE and PL by commodity type and direction in 2007total volume 502.000 tonnes

0

50

100

150

200

250

Agriculturalproducts

Foodstuffs Solid mineralfuels

Ores, metalwaste

Metalproducts

Buildingminerals

Fertilisers Chemicals Otherproducts

Petroleumproducts

Commodity

Volu

me

in 1

000

tonn

es

BE -> PL PL -> BE

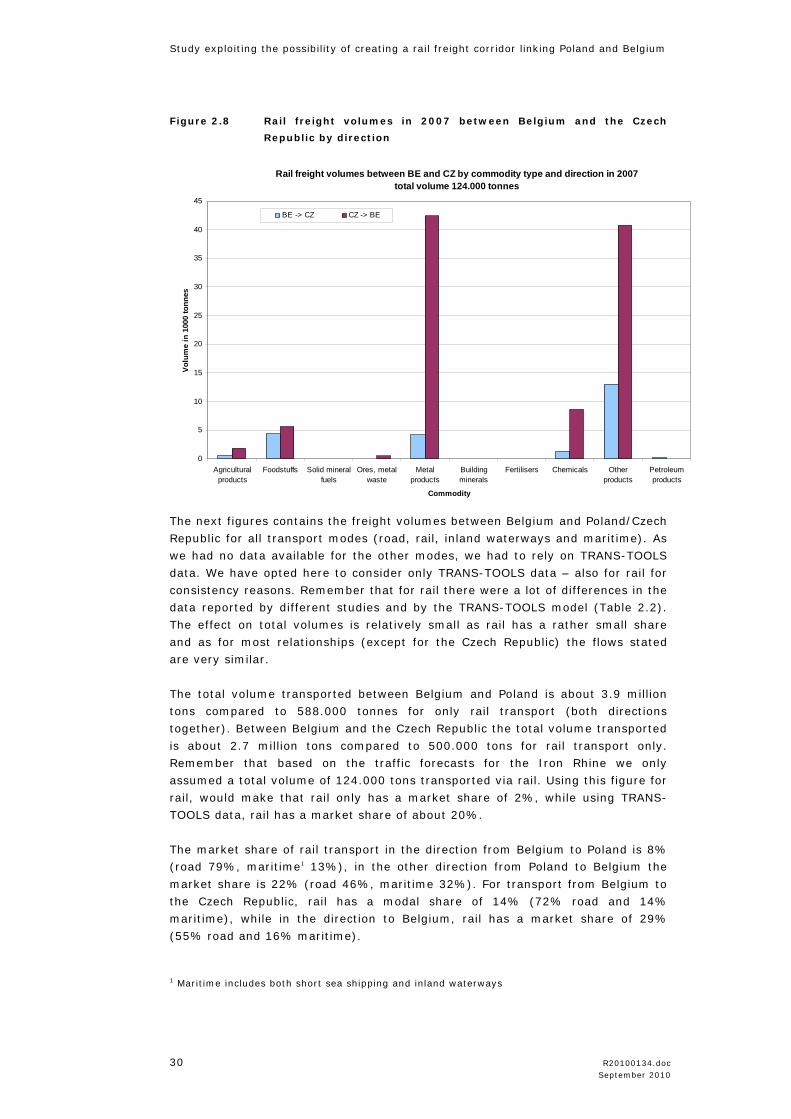

Figure 2.8 shows the same results for transport between Belgium and the Czech

Republic. With respect to the type of goods transported, there is not really a

difference with the transport flows between Belgium and Poland. In the direction

CZ-BE, the main goods transported are metal products (42%) and other products

(41%). In the opposite direction, mostly other products are transported (55%),

followed by foodstuff (19%) and metal products (18%). Using the same

assumptions about weight as before, this comes down to about 31 trains from

Belgium to the Czech Republic and 112 trains from the Czech Republic to

Belgium.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

30 R20100134.doc September 2010

Figure 2.8 Rail freight volumes in 2007 between Belgium and the Czech

Republic by direction

Rail freight volumes between BE and CZ by commodity type and direction in 2007total volume 124.000 tonnes

0

5

10

15

20

25

30

35

40

45

Agriculturalproducts

Foodstuffs Solid mineralfuels

Ores, metalwaste

Metalproducts

Buildingminerals

Fertilisers Chemicals Otherproducts

Petroleumproducts

Commodity

Volu

me

in 1

000

tonn

es

BE -> CZ CZ -> BE

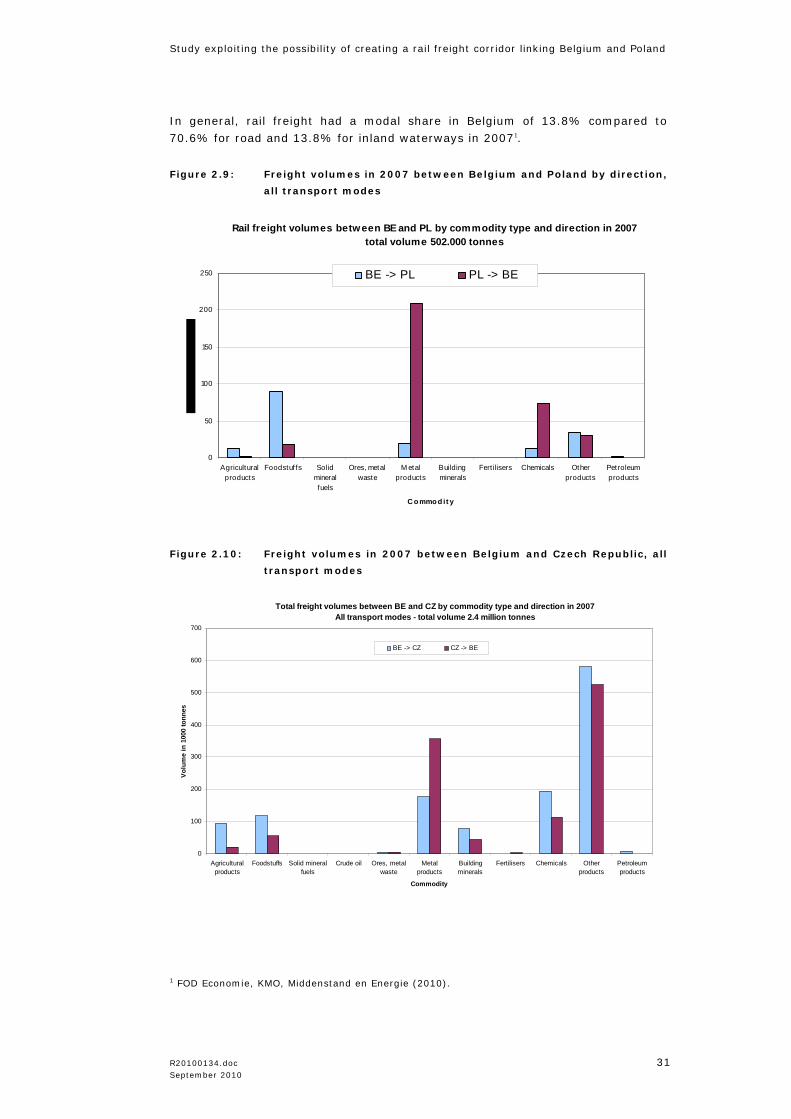

The next figures contains the freight volumes between Belgium and Poland/Czech

Republic for all transport modes (road, rail, inland waterways and maritime). As

we had no data available for the other modes, we had to rely on TRANS-TOOLS

data. We have opted here to consider only TRANS-TOOLS data – also for rail for

consistency reasons. Remember that for rail there were a lot of differences in the

data reported by different studies and by the TRANS-TOOLS model (Table 2.2).

The effect on total volumes is relatively small as rail has a rather small share

and as for most relationships (except for the Czech Republic) the flows stated

are very similar.

The total volume transported between Belgium and Poland is about 3.9 million

tons compared to 588.000 tonnes for only rail transport (both directions

together). Between Belgium and the Czech Republic the total volume transported

is about 2.7 million tons compared to 500.000 tons for rail transport only.

Remember that based on the traffic forecasts for the Iron Rhine we only

assumed a total volume of 124.000 tons transported via rail. Using this figure for

rail, would make that rail only has a market share of 2%, while using TRANS-

TOOLS data, rail has a market share of about 20%.

The market share of rail transport in the direction from Belgium to Poland is 8% (road 79%, maritime1 13%), in the other direction from Poland to Belgium the

market share is 22% (road 46%, maritime 32%). For transport from Belgium to

the Czech Republic, rail has a modal share of 14% (72% road and 14%

maritime), while in the direction to Belgium, rail has a market share of 29%

(55% road and 16% maritime).

1 Maritime includes both short sea shipping and inland waterways

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 31 September 2010

In general, rail freight had a modal share in Belgium of 13.8% compared to

70.6% for road and 13.8% for inland waterways in 20071.

Figure 2.9: Freight volumes in 2007 between Belgium and Poland by direction,

all transport modes

Rail freight volumes between BE and PL by commodity type and direction in 2007total volume 502.000 tonnes

0

50

100

150

200

250

Agriculturalproducts

Foodstuf fs Solidmineralfuels

Ores, metalwaste

M etalproducts

Buildingminerals

Fert ilisers Chemicals Otherproducts

Petroleumproducts

C o mmo d it y

BE -> PL PL -> BE

Figure 2.10: Freight volumes in 2007 between Belgium and Czech Republic, all

transport modes

Total freight volumes between BE and CZ by commodity type and direction in 2007All transport modes - total volume 2.4 million tonnes

0

100

200

300

400

500

600

700

Agriculturalproducts

Foodstuffs Solid mineralfuels

Crude oil Ores, metalwaste

Metalproducts

Buildingminerals

Fertilisers Chemicals Otherproducts

Petroleumproducts

Commodity

Vol

ume

in 1

000

tonn

es

BE -> CZ CZ -> BE

1 FOD Economie, KMO, Middenstand en Energie (2010).

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

32 R20100134.doc September 2010

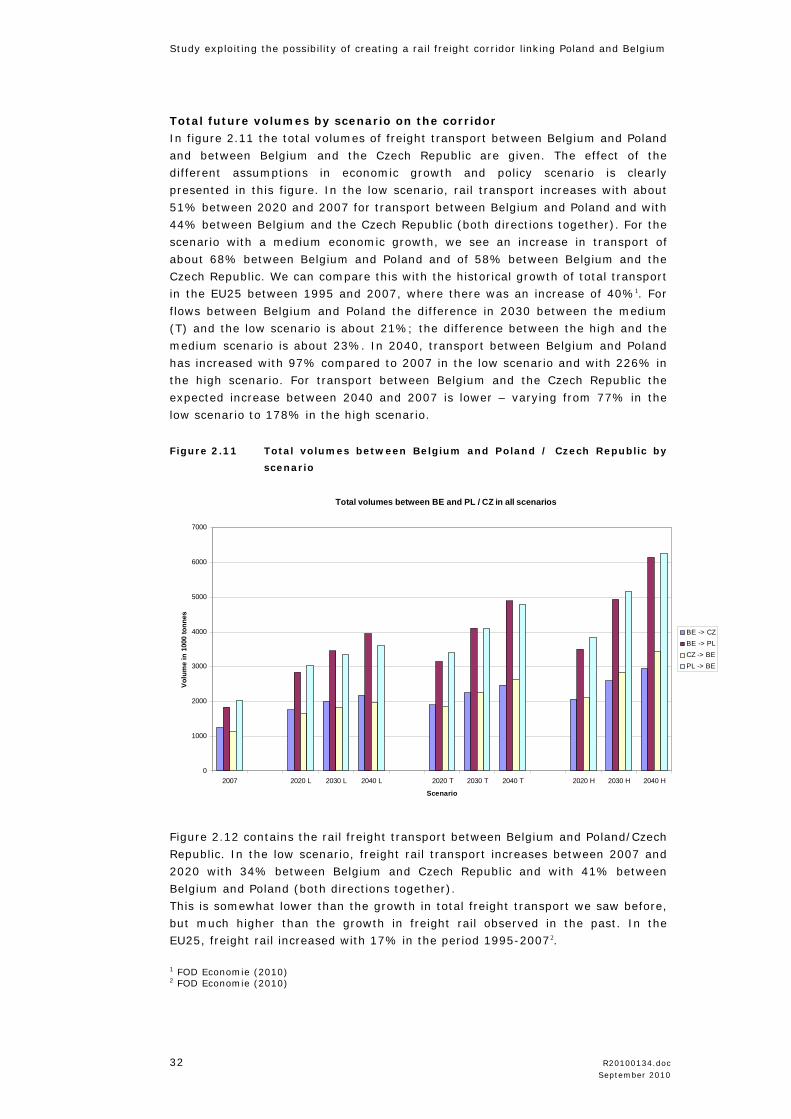

Total future volumes by scenario on the corridor

In figure 2.11 the total volumes of freight transport between Belgium and Poland

and between Belgium and the Czech Republic are given. The effect of the

different assumptions in economic growth and policy scenario is clearly

presented in this figure. In the low scenario, rail transport increases with about

51% between 2020 and 2007 for transport between Belgium and Poland and with

44% between Belgium and the Czech Republic (both directions together). For the

scenario with a medium economic growth, we see an increase in transport of

about 68% between Belgium and Poland and of 58% between Belgium and the

Czech Republic. We can compare this with the historical growth of total transport

in the EU25 between 1995 and 2007, where there was an increase of 40%1. For

flows between Belgium and Poland the difference in 2030 between the medium

(T) and the low scenario is about 21%; the difference between the high and the

medium scenario is about 23%. In 2040, transport between Belgium and Poland

has increased with 97% compared to 2007 in the low scenario and with 226% in

the high scenario. For transport between Belgium and the Czech Republic the

expected increase between 2040 and 2007 is lower – varying from 77% in the

low scenario to 178% in the high scenario.

Figure 2.11 Total volumes between Belgium and Poland / Czech Republic by

scenario

Total volumes between BE and PL / CZ in all scenarios

0

1000

2000

3000

4000

5000

6000

7000

2007 2020 L 2030 L 2040 L 2020 T 2030 T 2040 T 2020 H 2030 H 2040 H

Scenario

Volu

me

in 1

000

tonn

es

BE -> CZBE -> PLCZ -> BEPL -> BE

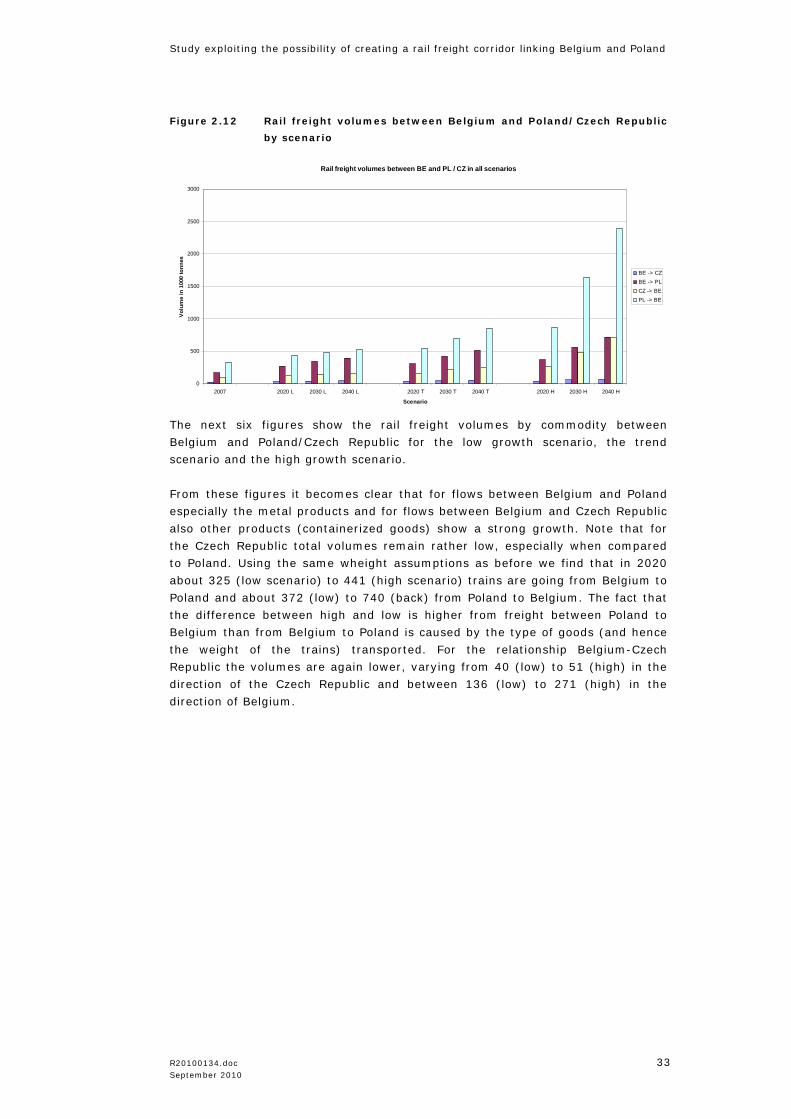

Figure 2.12 contains the rail freight transport between Belgium and Poland/Czech

Republic. In the low scenario, freight rail transport increases between 2007 and

2020 with 34% between Belgium and Czech Republic and with 41% between

Belgium and Poland (both directions together).

This is somewhat lower than the growth in total freight transport we saw before,

but much higher than the growth in freight rail observed in the past. In the

EU25, freight rail increased with 17% in the period 1995-20072.

1 FOD Economie (2010) 2 FOD Economie (2010)

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 33 September 2010

Figure 2.12 Rail freight volumes between Belgium and Poland/Czech Republic

by scenario

Rail freight volumes between BE and PL / CZ in all scenarios

0

500

1000

1500

2000

2500

3000

2007 2020 L 2030 L 2040 L 2020 T 2030 T 2040 T 2020 H 2030 H 2040 H

Scenario

Volu

me

in 1

000

tonn

es

BE -> CZBE -> PLCZ -> BEPL -> BE

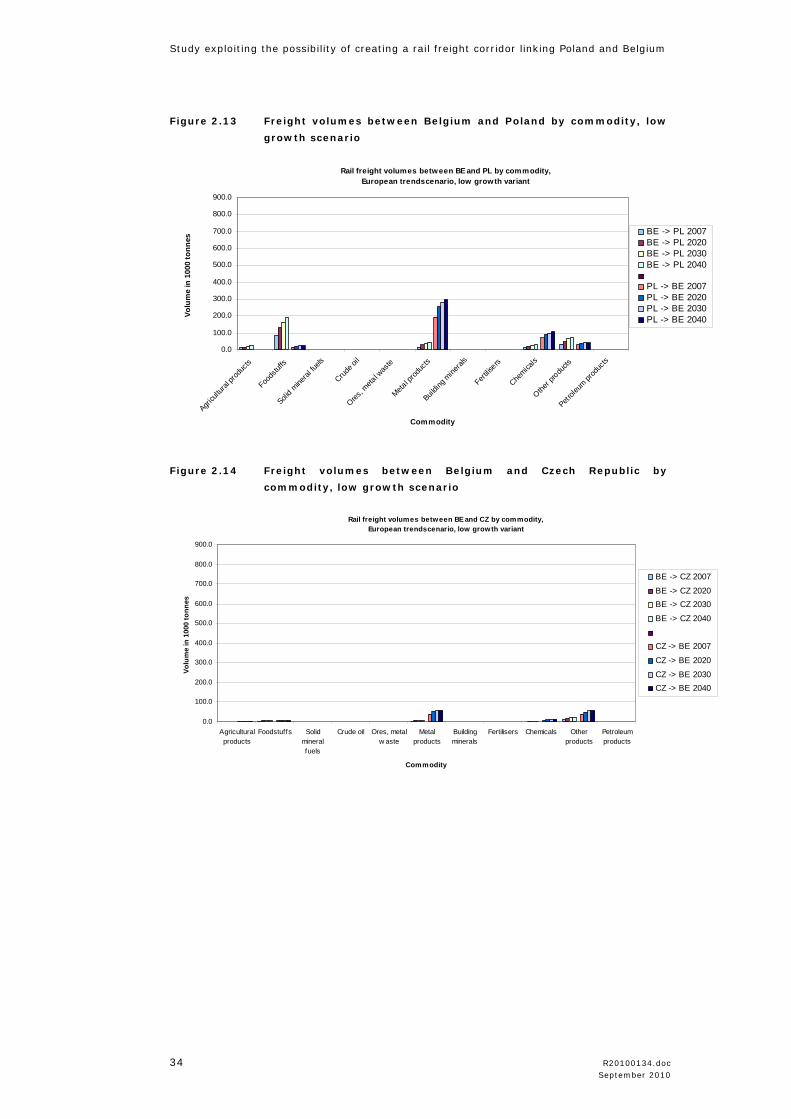

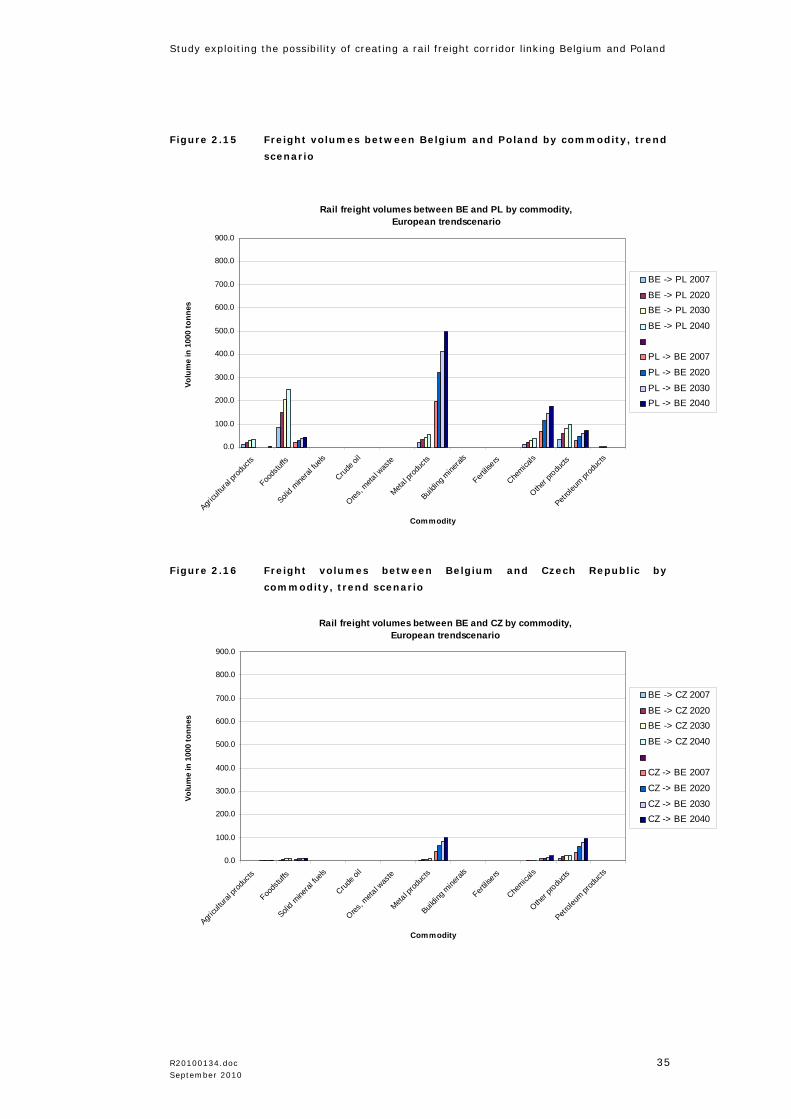

The next six figures show the rail freight volumes by commodity between

Belgium and Poland/Czech Republic for the low growth scenario, the trend

scenario and the high growth scenario.

From these figures it becomes clear that for flows between Belgium and Poland

especially the metal products and for flows between Belgium and Czech Republic

also other products (containerized goods) show a strong growth. Note that for

the Czech Republic total volumes remain rather low, especially when compared

to Poland. Using the same wheight assumptions as before we find that in 2020

about 325 (low scenario) to 441 (high scenario) trains are going from Belgium to

Poland and about 372 (low) to 740 (back) from Poland to Belgium. The fact that

the difference between high and low is higher from freight between Poland to

Belgium than from Belgium to Poland is caused by the type of goods (and hence

the weight of the trains) transported. For the relationship Belgium-Czech

Republic the volumes are again lower, varying from 40 (low) to 51 (high) in the

direction of the Czech Republic and between 136 (low) to 271 (high) in the

direction of Belgium.

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

34 R20100134.doc September 2010

Figure 2.13 Freight volumes between Belgium and Poland by commodity, low

growth scenario

Rail freight volumes betw een BE and PL by commodity, European trendscenario, low grow th variant

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Agricu

ltural

prod

ucts

Foods

tuffs

Solid m

ineral

fuels

Crude o

il

Ores, m

etal w

aste

Metal p

roduc

ts

Buildin

g mine

rals

Fertilis

ers

Chemica

ls

Other p

roducts

Petrole

um pr

oduc

ts

Commodity

Volu

me

in 1

000

tonn

es

BE -> PL 2007BE -> PL 2020BE -> PL 2030BE -> PL 2040

PL -> BE 2007PL -> BE 2020PL -> BE 2030PL -> BE 2040

Figure 2.14 Freight volumes between Belgium and Czech Republic by

commodity, low growth scenario

Rail freight volumes between BE and CZ by commodity, European trendscenario, low growth variant

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Agriculturalproducts

Foodstuffs Solidmineralfuels

Crude oil Ores, metalw aste

Metalproducts

Buildingminerals

Fertilisers Chemicals Otherproducts

Petroleumproducts

Commodity

Volu

me

in 1

000

tonn

es

BE -> CZ 2007

BE -> CZ 2020BE -> CZ 2030

BE -> CZ 2040

CZ -> BE 2007

CZ -> BE 2020

CZ -> BE 2030CZ -> BE 2040

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 35 September 2010

Figure 2.15 Freight volumes between Belgium and Poland by commodity, trend

scenario

Rail freight volumes between BE and PL by commodity, European trendscenario

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Agricu

ltural

prod

ucts

Foods

tuffs

Solid m

ineral

fuels

Crude o

il

Ores, m

etal w

aste

Metal p

roduc

ts

Buildin

g mine

rals

Fertilis

ers

Chemica

ls

Other p

roducts

Petrole

um pr

oduc

ts

Commodity

Volu

me

in 1

000

tonn

es

BE -> PL 2007

BE -> PL 2020BE -> PL 2030

BE -> PL 2040

PL -> BE 2007

PL -> BE 2020

PL -> BE 2030PL -> BE 2040

Figure 2.16 Freight volumes between Belgium and Czech Republic by

commodity, trend scenario

Rail freight volumes between BE and CZ by commodity, European trendscenario

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Agricu

ltural

prod

ucts

Foods

tuffs

Solid m

ineral

fuels

Crude o

il

Ores, m

etal w

aste

Metal p

roduc

ts

Buildin

g mine

rals

Fertilis

ers

Chemica

ls

Other p

roducts

Petrole

um pr

oduc

ts

Commodity

Volu

me

in 1

000

tonn

es

BE -> CZ 2007

BE -> CZ 2020BE -> CZ 2030

BE -> CZ 2040

CZ -> BE 2007

CZ -> BE 2020

CZ -> BE 2030CZ -> BE 2040

Study exploiting the possibility of creating a rail freight corridor linking Poland and Belgium

36 R20100134.doc September 2010

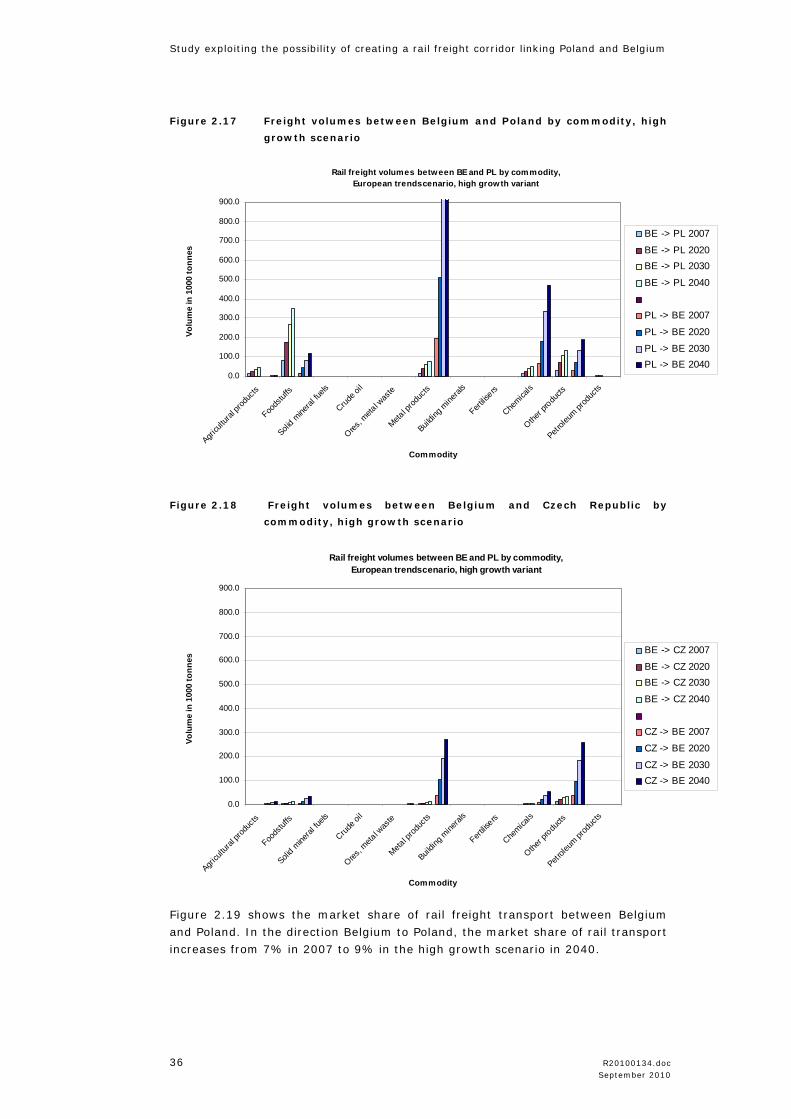

Figure 2.17 Freight volumes between Belgium and Poland by commodity, high

growth scenario

Rail freight volumes between BE and PL by commodity, European trendscenario, high growth variant

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Agricu

ltural

prod

ucts

Foods

tuffs

Solid m

ineral

fuels

Crude o

il

Ores, m

etal w

aste

Metal p

roduc

ts

Buildin

g mine

rals

Fertilis

ers

Chemica

ls

Other p

roducts

Petrole

um pr

oduc

ts

Commodity

Volu

me

in 1

000

tonn

es

BE -> PL 2007

BE -> PL 2020BE -> PL 2030

BE -> PL 2040

PL -> BE 2007

PL -> BE 2020

PL -> BE 2030PL -> BE 2040

Figure 2.18 Freight volumes between Belgium and Czech Republic by

commodity, high growth scenario

Rail freight volumes between BE and PL by commodity, European trendscenario, high growth variant

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

Agricu

ltural

prod

ucts

Foods

tuffs

Solid m

ineral

fuels

Crude o

il

Ores, m

etal w

aste

Metal p

roduc

ts

Buildin

g mine

rals

Fertilis

ers

Chemica

ls

Other p

roducts

Petrole

um pr

oduc

ts

Commodity

Volu

me

in 1

000

tonn

es

BE -> CZ 2007

BE -> CZ 2020BE -> CZ 2030

BE -> CZ 2040

CZ -> BE 2007

CZ -> BE 2020

CZ -> BE 2030CZ -> BE 2040

Figure 2.19 shows the market share of rail freight transport between Belgium

and Poland. In the direction Belgium to Poland, the market share of rail transport

increases from 7% in 2007 to 9% in the high growth scenario in 2040.

Study exploiting the possibility of creating a rail freight corridor linking Belgium and Poland

R20100134.doc 37 September 2010