Success Story

C O A S T A L C O M M U N I T Y C R E D I T U N I O N

A N N U A L R E P O R T 2 0 0 3

OUR VISIONThe islands’ choice for financial

and community leadership.

OUR MISSIONWe are a democratic, member- owned

organization that provides financial services and

contributes to the well being of our communities.

The Values and Principlesthat Guide Our Vision & Mission are:

AccountabilityWe maintain the highest level of financial

accountability to our members and our community.

CooperationWe work together in a fair, open and

caring way for the benefit of those we serve.

ExcellenceWe are enthusiastic, team-oriented,

and dedicated professionals.

InnovationWe are an empowering organization

that encourages innovative ideas.

IntegrityWe are honest, trustworthy, ethical, and

respectful in our relationships with everyone.

ResponsibilityWe are committed to being an organization

that embraces corporate social responsibility.

ResponsivenessWe are responsive to the needs of our

members, our community and each other.

C O N T E N T S

Report to the Membership 1

Board of Directors 4

Success Stories 7

Consolidated Financial 20Statements

Management’s Report 20

Audit Committee Report 21

Investment & Lending 21Committee Report

Auditors’ Report 22

Financial Statements 23

Notes to Consolidated 26Financial Statements

Branch Information 37

A N N U A L R E P O R T

2 0 0 3

After celebrating life to its fullest, Kerm Culham passed away unexpectedly

on March 31, 2004. He was born in 1943 to Iva and Russell Culham in

Cabri, Saskatchewan.

A well-respected human resources professional, Kerm joined the

Coastal Community Credit Union team in April 1992, and headed the

human resources area during his twelve years with us. He brought vast

experience, wisdom and innovative human resource practices to the

credit union.

Kerm thoroughly enjoyed the people part of his career, which spanned

40 years. He truly cared about the well-being of our employees. Under

his direction and his commitment to employee participation, education,

mutual respect, and workplace wellness, our Human Resources department

has helped Coastal Community achieve its status as a healthy, supportive

and vibrant workplace.

Kerm leaves many dear friends at Coastal Community, in the credit union

industry, and in our communities. Those who knew Kerm will remember

his wonderful sense of humour and optimistic outlook on life.

An avid sportsman throughout his life, the game of golf captivated him

more and more as time progressed, which he shared with close friends

and family.

His greatest passion in life was his dedication to, and love for, his family.

He is survived by his wife and best friend, Deborah; son Harry; daughter

Dannielle Nichol; daughter Jessica; and grandson Kyran. He is also

survived by mother Iva, and predeceased by father Russell. Kerm leaves

behind five siblings, Ken, Karen, Lloyd, Lyle, and Kathy, and many dear

friends and colleagues.

Our credit union and administration office will not be the same.

We will miss Kerm's good friendship, calm leadership, vast experience

and wonderful smile.

In Memoriam

KERMIT (KERM) RUSSELL CULHAM

Vice President, Human Resources

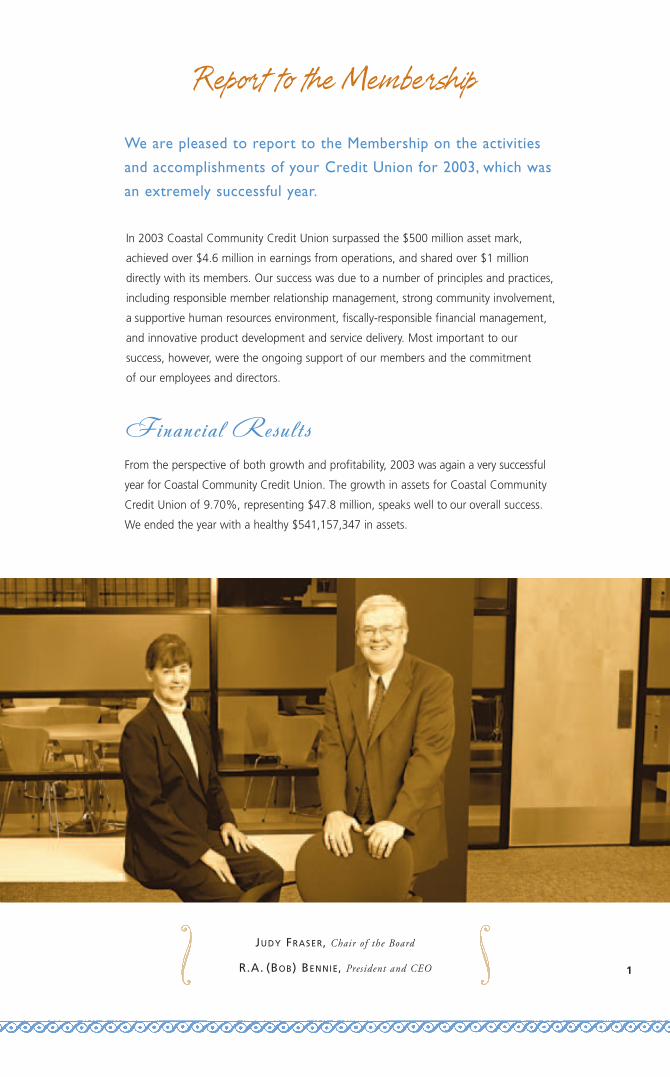

In 2003 Coastal Community Credit Union surpassed the $500 million asset mark,

achieved over $4.6 million in earnings from operations, and shared over $1 million

directly with its members. Our success was due to a number of principles and practices,

including responsible member relationship management, strong community involvement,

a supportive human resources environment, fiscally-responsible financial management,

and innovative product development and service delivery. Most important to our

success, however, were the ongoing support of our members and the commitment

of our employees and directors.

Financial ResultsFrom the perspective of both growth and profitability, 2003 was again a very successful

year for Coastal Community Credit Union. The growth in assets for Coastal Community

Credit Union of 9.70%, representing $47.8 million, speaks well to our overall success.

We ended the year with a healthy $541,157,347 in assets.

1

We are pleased to report to the Membership on the activities

and accomplishments of your Credit Union for 2003, which was

an extremely successful year.

Report to the Membership

JUDY FRASER, Chair of the Board

R.A. (BOB) BENNIE, President and CEO

0

100

200

300

400

500

600

AssetsDepositsLoans

2003200220010

100

200

300

400

500

600

AssetsDepositsLoans

200320022001

Loans, Deposits & AssetsIn Millions of Dollars

Financial Results continued from 1

The local economies – in all of our communities – were

vibrant and growing during 2003. A very strong real estate

market contributed to exceptional growth in our loans

portfolio. Loans growth at 9.89% continued the strong

growth trend of the previous year. Deposit growth during

2003 was also robust, with growth in member deposits

of 9.25% compared to the provincial credit union system

average of 8.24%.

Our portfolio of assets under administration (not included

in our consolidated statements), which includes the Family

of Ethical Funds and the balances administered by our

financial advisors, grew by $12.2 million, reflecting both

increased consumer confidence and a stronger market

performance. This brings the total off-balance sheet assets

under administration to $101.9 million.

In the fall of 2003, CCCU purchased the building that

houses our Harbourfront Branch, resulting in an increase

in the value of our premises and equipment.

This purchase is a very tangible statement of our

commitment to downtown Nanaimo and confirms

our position as one of the major financial institutions

in Nanaimo.

Earnings from operations were $4.6 million, before

distributions to members and payment of income taxes.

We were very pleased to transfer $2.9 million of these

earnings to our retained earnings. Capital adequacy

at 11.26% exceeds the 8.00% base as required by

provincial regulations, and reflects another year of

good growth in capital.

Given this strong operating income, your Board

of Directors declared an Investment Equity Share

Dividend of 6.0% and a Membership Equity Share

Dividend of 3.0%.

Report to the Membership

2

0.0

0.2

0.4

0.6

0.8

1.0

Return on Average Assets

In Percent

200320022001

.89

.68

.52

0

1000

2000

3000

4000

5000

Net IncomeEarnings

200320022001

Human ResourcesOne of the many initiatives for Human Resources during

2003 was the creation of our WOW (Working on Wellness)

employee committee. This strategic initiative with guiding

values of Confidentiality, Voluntary and Open Participation,

Integrity, Empowerment and Support, has been well received

by our employees. Over 91% of employees participated in

an introductory survey and based on their input, the WOW

committee has coordinated evening seminars, web-based information distribution, library

contributions, and support for personal wellness initiatives. We thank the WOW Committee

members for their innovative contributions to employee wellness.

A principal theme for the human resources program of Coastal Community Credit Union

is “education.” We are committed to supporting and encouraging educational endeavors

for all of our employees, managers and directors. Our Education Centre, located below the

Bowen Community Branch location was in use 145 days last year, offering a variety of

courses. In total, 195 employees from the credit union, insurance and financial planning

divisions participated in over 900 courses during 2003.

Our focus is on the future needs of our credit union and our membership, and our

commitment is to prepare and support all of our employees as they strive to meet those needs.

3

RecognitionIn 2003, the Marketing Association for Credit Unions again recognized Coastal Community

Credit Union. A first place Achievement in Marketing Excellence Award was won for the

2002 Annual Report. We were also recognized with two Certificates of Excellence for the

2003 RRSP Campaign and the 2002 Community Savings Bond (An Investment with Real

Heart) Campaign. At the local front, readers of the Nanaimo News Bulletin rated Coastal

Community Credit Union as the “Best Bank” in Nanaimo; we thank them for this honour.

Report to the Membership

With respect to Patronage Rebates, the Board of Directors

was pleased to approve patronage rebates in the amount of

$790,397. Patronage rebates were paid based on rebates of

loan interest paid by members, bonuses on deposit interest

received by members, and rebates of service fees paid by

members for the operation of their savings and chequing

accounts. In total, distributions to members in the form of

dividends and rebates amount to $1,020,201, up 9.40%

over 2002. This is truly “Sharing our Success” with those

who contributed to it !

Financial Results continued from 2

During 2003, the Board of Directors reconfirmed the mission and principles of Coastal

Community Credit Union. We also affirmed our commitment to a new vision, which

is to be: “The islands’ choice for financial and community leadership.” We reviewed

our growth strategy in light of the unsuccessful merger with Island Savings Credit

Union, and we continue to believe that mergers, partnerships and alliances with other

like-minded Vancouver Island credit unions are the way of the future. To that end,

we are exploring opportunities with a number of Vancouver Island credit unions.

While not a new initiative, Corporate Social Responsibility has been given an elevated

priority for our organization. During 2004, we will be doing an audit of our current

practices, and evaluating our programs and processes in regards to a socially responsible

organization. We are committed to operating in an economically and environmentally

sustainable manner while recognizing the interests of our stakeholders. Stakeholders

include members, employees, business partners, local communities,

the environment and society at large.

BOARD OF DI R ECTORS: ( clockwise from bottom left )

JOHN NEWALL, JAY MUSSELL, BOB SMITS, MICHELLE BUTTS, JOE SIEBER,

JUDY FRASER, LEN TOWNSEND, AND SUSANNE JAKOBSEN.

( Missing from photo: JOHN F. LITTLE )4

Report to the Membership

Board of Directors

Considerable effort has been directed towards reviewing board fiduciary responsibilities

to ensure that our policies and processes are above reproach. Prudent fiscal

management demands that we constantly monitor the risks inherent in our financial

operations. The board also continued to focus on governance and has initiated a

board self-evaluation process.

The Board of Directors approved funding for a number of major initiatives during 2003.

The purchase of the Harbourfront Community Branch building was finalized; the

branch renovations at the Qualicum Beach Community Branch were completed; and

the much needed renovations for the Hammond Bay Community Branch were approved.

The administration offices on Victoria Crescent are being expanded to support the

centralization of loans processing - a move that will allow our branch employees to

focus more on the member and less on the paperwork. We also approved funding

for the Member Relationship Management project. This project will provide tools

for our employees that will enable them to provide even more personalized

service to our members.

5

Report to the Membership

Board of Directors continued from 4

COASTAL COMMUNITY EXECUTIVE GROUP: ( from left to right )

LORNE PURCHASE, Vice President, Operations

LOIS STEWART, Executive Assistant

LYNNE FRASER, Vice President, Finance and Community Relations

BRUNO DRAGANI, Vice President, Retail Services

KERMIT CULHAM, Vice President, Human Resources

JOE CRISTIANO, Vice President, Marketing

Community InvolvementOur community involvement during 2003 proved again to be well received by all of

our communities – from Gabriola Island to Qualicum Beach. Financial and in-kind

contributions were made to a variety of groups – over 250 organizations received our

support and funding during this past year. Our directors, managers, and employees

were again at the forefront in contributing their time and energies to many

worthwhile projects.

Our corporate funding, branch fundraising and employee commitment activities were

provided to various categories of groups and events – Community Service, Seniors,

Youth, Culture, Education, Medical, Sports, Environment and Ecology. During 2003, a

total of $250,000 was returned to the communities we serve in the form of corporate

donations, sponsorships, scholarships, in-kind donations, as well as through our

Fundraising Fridays program. During 2003, our Fundraising Fridays program passed

a milestone – since inception in 1997 our employee fundraising has exceeded

$100,000 in funds raised for local non-profit organizations!

We were also pleased to increase our scholarship funding levels and to add two new

scholarships for 2004. The Leaders of Tomorrow scholarships are available to students

who have shown leadership qualities in community activities as well as academic

proficiency. Funds are available to students of all of our communities with preference

given to members of our credit union and may be used for academic or

vocational pursuits.

We are currently working on a Community Branching Initiative which would see even

stronger contributions and engagement by our branches to their local communities.

Coastal Community Credit Union recognizes the significance of the local identity of

each branch and community, and the need to preserve its uniqueness. This is an

exciting concept that we look forward to working on in 2004.

2003 was an exciting year. Sharing our success with our members and communities

continues to demonstrate the difference between being a bank and being a credit union

– and even more importantly for members, the difference between being a customer

and being a member. At Coastal Community Credit Union we remain committed to

our employees, our members and our communities.

Thank you for your continued support. It is what drives our success.

Respectfully submitted,

Judy Fraser R.A. (Bob) BennieChair, Board of Directors President and CEO

6

Report to the Membership

7

Success Stories

The last several years have been very successful for Coastal Community Credit Union,

with 2003 being the most successful experienced by many measurements.

Overall asset growth, earnings, and membership growth were solid and well over the

provincial average. We surpassed several milestones in 2003 - the half a billion asset

mark, the 40,000 membership mark, and the $4 million earnings mark. Our success will

allow us to share the greatest amount ever directly with our members - over $1 million.

The success of any organization is dependent on many factors - both external and

internal. Some of the external factors that contributed positively include an improving

local economy and low interest rates.

As identified earlier in the annual report there are a number of internal factors that

contributed to our success. These include solid board governance, responsible member

relationship management, strong community involvement, supportive human resources

practices, fiscally-responsible financial management, and innovative product

development and service delivery.

While there are many more than we are able to identify in the annual report, the

following pages list a number of internal success activities. We also highlight six

stories from 2003 that provide a sampling of the various initiatives that contributed

to our success.

Once again I would like to thank members for their ongoing patronage, and

employees and directors for their hard work and commitment. It is through your

actions that Coastal Community Credit Union is such a success.

R.A. (BOB) BENNIE,

President and CEO

Sharing our SuccessDistributing over $1 million to our members

and our communities

CO

AS

TA

L C

OM

MU

NIT

YS

ucce

ss S

tori

esColin and Christine Moore, members

of Coastal Community since 1991,

figured prominently in our Sharing

our Success communication campaign

in spring 2003.

S U C C E S S E S

JanuaryDividends totaling over $400,000

are paid to members on their

share holdings, including

Membership and Investment

Equity Shares.

The Parksville Civic and

Technology Centre of Malaspina

University-College is given funding

by Coastal Community for a

state-of-the-art sound system.

Our local Crime Stoppers receives

special donation from Coastal

Community to help fund its

community improvement activities.

The Fundraising Fridays program

begins the year by raising funds

and awareness for the District 69

Volunteer Centre Association and

Nanaimo Volunteer and Information

Centre Society. The Fundraising

Fridays program provides funds

for different community groups

each month.

S U C C E S S E S

FebruaryCoastal Community conducts

a very successful RRSP campaign.

While members benefit from

an excellent range of RRSP products,

the credit union later receives a

Certificate of Excellence Award

for the campaign by the Marketing

Association for Credit Unions.

The Ballenas High School

Dry Grad receives a boost from

employees of our Parksville

Community Branch, as they hold

special fundraising activities for

the important initiative.

The Fundraising Fridays

community partners for the

month are Project Literacy,

serving the Parksville/Qualicum

areas and Literacy Nanaimo.

Sharing our success with our members and communities is at

the heart of our credit union.

Members will remember the beginning of 2003 as the time when we

shared almost $1 million of our profits with them. Members received

cheques and direct deposits to their accounts based on the amount of

business they conducted with us.

Member Rewards resulting from our credit union’s success in 2003 will

be even more memorable, as we share over $1 million with members –

an increase of 9.4% over the previous year!

For 2003, dividends are based on share balances, while patronage

rebates are calculated based on loan interest paid by members, deposit

interest received by members, and service fees paid by members for

the operation of their savings and chequing accounts. This is truly

“Sharing our Success” with those who contribute to it !

In addition to sharing with members, we also share our profits with

the larger communities we serve. During 2003, we provided $250,000

in donations and sponsorships to various organizations. Not only did we

offer financial support to over 250 community organizations, but also

our employees contributed thousands of hours, serving as volunteers,

directors and advisors for our vital community groups.

Overall, our success in 2003 will result in the sharing of over $1.25 million

with members we serve and the communities we live in. Sharing more

than one-quarter of our profits with our members and communities simply

makes sense. After all, it’s the trust our members

and communities place in us that

drives our growth and success.

Sharing our Success

9

Innovative Products forMembers and Communities

Preserving a green space in Nanaimo

Supporters of the Nanaimo Area

Land Trust and members of

Coastal Community Credit Union,

the Thomas family enjoys an

afternoon in Linley Park.

CO

AS

TA

L C

OM

MU

NIT

YS

ucce

ss S

tori

es

S U C C E S S E S

MarchThe 6th annual Community Builder

GIC is launched, in support of the

Linley Valley Park Campaign by

the Nanaimo Area Land Trust

(see feature story for more).

The spring fundraising campaign

of the Canadian Cancer Society

is supported by Coastal Community

Credit Union with a donation

as well as an insert through

its monthly statement.

The new Neighbourhood Heroes

Hidden Hero Program receives

a special donation to fund the

development of its website.

Fundraising Fridays features

Community Kitchens in District 69

and Nanaimo. These groups offer

support for low-income families.

S U C C E S S E S

AprilCoastal Connection, an exciting

and well-received employee

newsletter is launched for 2003.

Enhancements to MasterCard

credit cards are introduced to

members. Among the changes

are the addition of Platinum

and Business cards.

Coastal Community Credit Union's

annual report for 2002 is produced.

The report would later win an

Achievement in Marketing Excellence

award from the Marketing Association

for Credit Unions.

Fundraising Fridays supports

the Canadian Cancer Society.

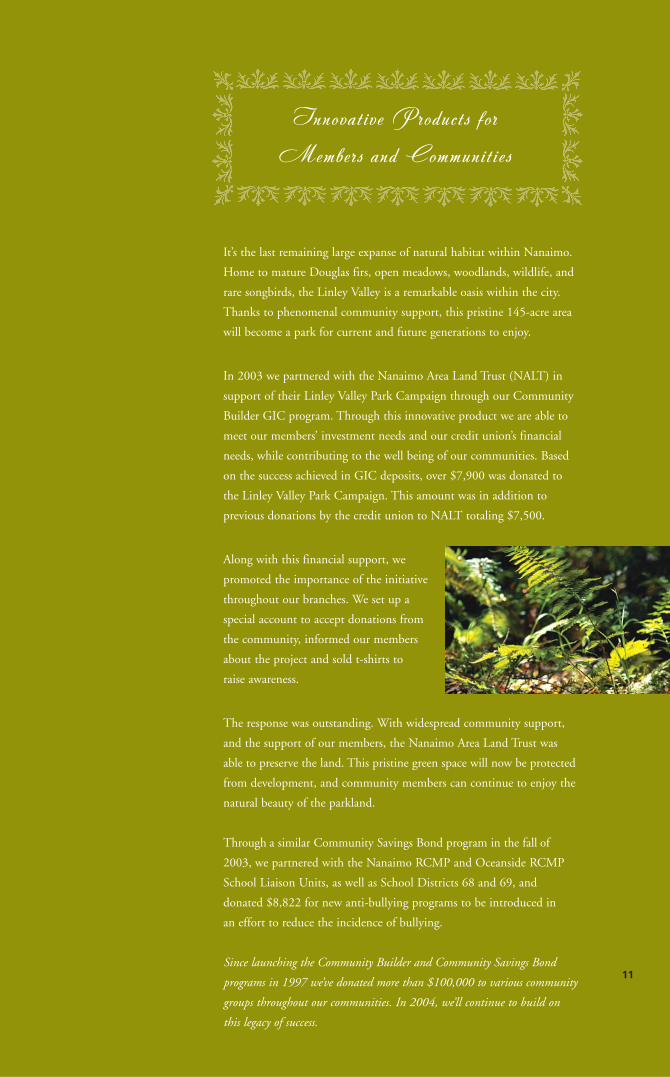

It’s the last remaining large expanse of natural habitat within Nanaimo.

Home to mature Douglas firs, open meadows, woodlands, wildlife, and

rare songbirds, the Linley Valley is a remarkable oasis within the city.

Thanks to phenomenal community support, this pristine 145-acre area

will become a park for current and future generations to enjoy.

In 2003 we partnered with the Nanaimo Area Land Trust (NALT) in

support of their Linley Valley Park Campaign through our Community

Builder GIC program. Through this innovative product we are able to

meet our members’ investment needs and our credit union’s financial

needs, while contributing to the well being of our communities. Based

on the success achieved in GIC deposits, over $7,900 was donated to

the Linley Valley Park Campaign. This amount was in addition to

previous donations by the credit union to NALT totaling $7,500.

Along with this financial support, we

promoted the importance of the initiative

throughout our branches. We set up a

special account to accept donations from

the community, informed our members

about the project and sold t-shirts to

raise awareness.

The response was outstanding. With widespread community support,

and the support of our members, the Nanaimo Area Land Trust was

able to preserve the land. This pristine green space will now be protected

from development, and community members can continue to enjoy the

natural beauty of the parkland.

Through a similar Community Savings Bond program in the fall of

2003, we partnered with the Nanaimo RCMP and Oceanside RCMP

School Liaison Units, as well as School Districts 68 and 69, and

donated $8,822 for new anti-bullying programs to be introduced in

an effort to reduce the incidence of bullying.

Since launching the Community Builder and Community Savings Bond

programs in 1997 we’ve donated more than $100,000 to various community

groups throughout our communities. In 2004, we’ll continue to build on

this legacy of success.

Innovative Products for

Members and Communities

11

Personal ServiceBringing banking services

into the community

Member of Coastal Community

Ann Clowes (center), gets help

with her banking at her home from

Brenda Light, Assistant Manager,

and April Mathers, Member Service

Representative, of our Hammond Bay

Community Branch.

CO

AS

TA

L C

OM

MU

NIT

YS

ucce

ss S

tori

es

S U C C E S S E S

MayCoastal Community reaches

a special milestone -

$500 million in assets!

Member Reward cheques and

direct deposits of over $500,000

are distributed to members,

bringing the total amount shared

directly with members to almost

$1 million based on 2002 results.

The BC credit union system

contributes more than $1 million

towards establishing the BC

Credit Union Centre of Excellence

in Depression Research, in

conjunction with the VGH/UBC

Hospital Foundation.

Coastal Community donates

$39,000 to this project,

representing $1 per member.

The Angel Program of the

Vancouver Island International

Children's Festival is sponsored.

Fundraising Fridays partner is

the Multiple Sclerosis Society,

Central Island Chapter.

S U C C E S S E S

JuneMember support of branch

activities helps raise over $10,000

in the annual Financial Institutions

Campaign to benefit the Vancouver

Island Hospital Foundation.

Coastal Community Credit Union

wins first prize in the "Best Bank"

category as rated by the readers

of the Nanaimo News Bulletin.

The Choices program wraps up

for another school season. Through

a variety of engaging activities in

classroom presentations, Coastal

Community employees emphasize

the long-term benefits of ongoing

education to all grade 8 students in

School Districts 68 and 69.

Errington Therapeutic Riding

Association and Nanaimo Saori

Weaving Society are the focus

of June's Fundraising Fridays.

Great personal service is one of the qualities that has made Coastal

Community such a popular place to do business. While we offer a full

complement of hi-tech financial services like Internet banking, we are

still committed to taking care of our members in person.

This commitment to personal service even extends out of the branch.

Realizing that many seniors have limited access to transportation, we

decided to go to them. In June of 2003, employees from our Hammond

Bay Community Branch began weekly visits to the Long Lake Chateau,

a seniors residence in Nanaimo. We meet most of the banking needs of

our members at the residence – whether it’s cashing a cheque, paying

bills, or setting up term deposits.

Our Bowen Community branch has developed similar relationships.

Since 1999, Bowen employees have been visiting Berwick on the Lake

and Lakeside Gardens.

The program has become very popular,

and not only with the seniors. Our

employees take great pride in helping

our members and look forward to the

weekly visits. And now when the

members from these seniors’ residences

come into the branch, they feel very

comfortable as they already recognize

familiar faces.

Coastal Community is committed to high quality personal service

that will continue to be the foundation of our organization and one

of the keys to our success.

Personal Service

13

Supporting Our EmployeesPromoting wellness at work and in life

Members of the Beach Day Committee

enjoy Parksville Beach. From left are

Sandra Kokorudz, Mary Brouilette,

Janice Krall, Carol Thompson, Melissa Young,

Paula Blazina, Laura McCafferty,

and Marnie Weeks. Missing from photo

is Wendy MacLachlan.

CO

AS

TA

L C

OM

MU

NIT

YS

ucce

ss S

tori

es

S U C C E S S E S

JulyA special renovation loan

campaign featuring a credit union

member is launched.

The Nanaimo Youth Services

Association receives $10,000

from a special youth campaign

of the Savings and Credit Unions

of British Columbia.

Fun, games, food & sunshine

are enjoyed by Coastal Community

employees and their families at the

first annual Family BBQ and Beach

Day at beautiful Parksville Beach.

Coastal Community is the major

sponsor of the largest baseball

tournament in Nanaimo's history.

The North American competition

brings 17 teams of 11 year old

baseball players together for

the tournament.

Fundraising Fridays partners

are Springboard Family Centre

and Nanaimo Foodshare.

S U C C E S S E S

AugustNanaimo Foodshare's

Summer Lunch Munch program

receives support through a

golf tournament held by the

employees of our Bowen

Community Branch.

Employees of our Nanoose Bay

Community Branch volunteer

once again at the celebrated

Nanoose Bay Teddy Bear Picnic.

In support of the Kelowna

fire victims, funds are raised

though a BBQ and bake sale

by the employees of our

Southgate Community Branch.

Symphony in the Park,

a unique presentation of the

Vancouver Island Symphony,

is sponsored by

Coastal Community.

Fundraising Fridays supports

Arrowsmith Search and Rescue

and Nanaimo Search and Rescue.

We care about the well-being of our employees. Through professional

and personal education, employee involvement, fun group activities,

and team commitment, Coastal Community works hard at creating a

healthy and vibrant workplace.

We recognize continuing education is critical to the success of our

employees and the credit union. We provide professional and personal

learning activities to enrich the quality of work life and member service

through a variety of innovative programs. In 2003, nearly 200 of our

250 employees attended personal and professional development courses.

We covered topics specific to our business, as well as programs on people

management, coaching, sales training and leadership development.

Although we place a high value on professional training and education,

other initiatives also help make us a healthy and supportive place to

work. We encourage employee involvement through a variety of methods

such as the Ideas Into Action suggestion program, and the Coastal

Connections employee newsletter. Last year a Working on Wellness

campaign was launched by a newly-formed Wellness Committee,

composed of employees from our various locations. The campaign

included evening seminars on wellness topics and an intranet site

providing employees with access to a wealth of information on

health and wellness.

But it’s not always about work – we also believe strongly in celebrating

our successes by having fun ! Last year we hosted our first annual

Beach Day. An employee driven initiative, this highly successful event

brought 180 people together on Parksville Beach for games, music,

food and fun. Plans are already underway by our employee Beach Day

Committee for an even better celebration

in 2004.

Through education, participation, mutual

respect and having fun, Coastal Community

is committed to the promotion of wellness

in our workplace and to the success of our

employees, our credit union, and ultimately

our communities.

Supporting Our Emp loyees

15

Financial Services forBusinesses and Organizations

Growing Businesses and Communities

CO

AS

TA

L C

OM

MU

NIT

YS

ucce

ss S

tori

esCoastal Community's Joel Scobie,

Senior Account Manager, Business Centre,

and Kevin Wilson, Executive Director

of the Society of Organized Services,

in front of the new S.O.S. Thrift Shop

in Parksville.

S U C C E S S E S

SeptemberMemberDirect Internet banking

is enhanced, offering members

new online banking services

including: hyperWALLET, multiple

bill payments, enhanced account

inquiries and a secure online

message centre.

The kids activity corner at

the Heart & Stroke Foundation's

Mother-Daughter Walk is sponsored

by Coastal Community.

A special contest by Coastal

Community Insurance Agencies

awards seven students in

School Districts 68 & 69 with

driving lessons for their winning

submissions on safe driving.

The 2003 -2004 Jazz Series by

the Port Theatre is sponsored by

Coastal Community Credit Union.

St. John's Brigade receives

our Fundraising Fridays support

this month.

S U C C E S S E S

OctoberCoastal Community purchases

the building that houses our

Harbourfront Community Branch,

solidifying our commitment to

economic development in

downtown Nanaimo.

The fall 2003 Community Savings

Bonds become available for member

investment, with a donation of

$8,822 being provided to

partnering Nanaimo & Oceanside

RCMP School Liaison Units and

School Districts 68 & 69, as

they introduce new anti -bullying

programs.

Coastal Community earmarks

$1 million to lend as part of

the $10 million BC credit union

provincial GrowthStart initiative

to provide loans to rural

and small businesses.

The Ravensong Aquatic Centre

in Parksville receives a donation

by Coastal Community to install

a lift chair for individuals

with disabilities.

Support for Habitat for Humanity

is provided this month by the

Fundraising Fridays program.

When businesses and community organizations succeed, we all benefit –

through increased economic development and stronger communities.

We opened our Business Centre in 1996 to act as a hub for our

commercial lending expertise. The Centre specializes in providing

commercial financing for small and mid-sized local businesses and

community organizations.

In 2003, financing provided by our Business Centre assisted the Society

of Organized Services (SOS) in the construction of their new building

in Parksville. This 18,000 square foot retail space is now home to the

organization’s very popular thrift shop, which generates revenues to fund

SOS’s vital community services. This expansion made it possible for SOS

to convert its old thrift shop into a new child, youth and family centre,

providing additional support for the

community. We are proud to be

a financial partner for this important

organization.

Coastal Community is also participating

in a new provincial initiative

to help small businesses achieve their

goals. GrowthStart is a $10 million

business development fund that provides loans of up to $500,000 for

rural and small businesses. As one of the nine participating credit unions,

Coastal Community has earmarked $1 million to lend as part of this

program.

Our business banking services and the support we provide help businesses

and organizations succeed – just another way that we are strengthening

our local communities.

Financial Services for

Businesses and Organizations

17

Community InvolvementGiving back to the communities we serve

Michelle Butts,member of the Board

of Directors at Coastal Community,

and Corinne James, Coordinator of

the Old School House Arts Centre,

browse the gallery at the

Old School House in Qualicum.

CO

AS

TA

L C

OM

MU

NIT

YS

ucce

ss S

tori

es

S U C C E S S E S

NovemberAn innovative promotion of

Registered Education Savings Plans

features a special coin gift set.

The Working on Wellness

Committee provides employees

of Coastal Community with

enhanced information and

links on wellness through

its intranet website.

A total of $3,000 is raised

for the United Way Campaign.

Credit union employees contribute

through a payroll deduction program

and members contribute through

branch fundraising events.

Fundraising Fridays supports

District 69 Family Resource Centre

and the Boys & Girls Club

of Nanaimo and District.

S U C C E S S E S

DecemberAnother important milestone is

achieved as credit union membership

increases to 40,000 !

Coastal Community employees

and families enjoy the 12th annual

Coastal Community Skating Party,

held at the new twin rinks arena

in Parksville.

Our Qualicum Beach Community

Branch wins "Best Theme"

in the Moonlight Madness

Christmas Decorating Contest.

Harbourfront Community Branch

employees enter their first

themed float in the Santa Clause

Parade in Downtown Nanaimo.

Family Day at the Malaspina

University-College's Festival of Trees

is sponsored by Coastal Community.

Hospice organizations in our

communities are the recipients of

December's Fundraising Fridays.

Our commitment to all of our communities is a core value of Coastal

Community Credit Union. We are known for our innovative approach

to supporting those groups that contribute to the well-being of

our communities.

A total of $250,000 in cash and in-kind donations were made during

2003 to over 250 groups and organizations from Gabriola Island to

Qualicum Beach, which supported a broad range of projects and events.

Our corporate funding, branch fundraising and employee commitment

activities are provided to various categories of groups and events –

Community Service, Seniors, Youth, Culture, Education, Medical,

Sports, Environment and Ecology.

The Old School House Arts Centre in Qualicum Beach was one of many

organizations that received our support. The Centre, with two galleries

and eight studios for resident artists, will receive $10,000 over the next

five years to assist with operating costs and projects to upgrade their

facilities. One of the first projects undertaken was a renovation of the

Centre’s exterior.

Investing in local organizations makes our communities better

for all of us. We are very proud of the work we have done so far

and are striving to remain a leader in our communities.

Community Involvement

19

Management’s ReportThe consolidated financial statements and other financial information in this annual

report have been prepared by the management of Coastal Community Credit Union,

which is responsible for their reliability, completeness and integrity. They were

developed in accordance with requirements of the Financial Institutions Act of British

Columbia and conform in all material respects with Canadian generally

accepted accounting principles.

Systems of internal control and reporting procedures have been designed to provide

reasonable assurance that the financial records are complete and accurate so as to

safeguard the assets of the Credit Union. These systems include establishment and

communication of standards of business conduct throughout all levels of the

organization to provide assurance that all transactions are authorized and proper

records maintained. Further, the systems of control are reviewed by the Credit Union’s

external auditors.

The Board of Directors has approved the consolidated financial statements. The Audit

Committee of the Board, composed of three directors, has reviewed the statements

with the external auditors, in detail, and received regular reports on internal control

findings. BDO Dunwoody LLP, the external auditors appointed by the membership,

have examined the consolidated financial statements and attendant notes of the Credit

Union in accordance with Canadian generally accepted auditing standards. They have

had full and free access to employees of the credit union and the Audit Committee

of the Board. Their report outlines the scope of their examination and their opinion.

R. A. (Bob) Bennie Lynne Fraser

President & CEO Vice President,Finance & Community Relations

Consolidated Financial Statements ofCoastal Community Credit Union

Year ended December 31, 2003

20

Investment &Lending Committee ReportThe Investment and Lending Committee meets throughout the year to review and approve theCredit Union’s Investment and Lending Policies, process individual loan approvals, review ourprovision for losses, recommend bad debt write-offs to the Board of Directors, and monitorliquidity and capital adequacy levels. For 2003, the total loan portfolio grew from $421.5 millionto $463.1 million, representing healthy growth of 9.87% for the year. The growth was primarilydriven through personal mortgages and personal loan products. Overall loan delinquency atyear-end was 0.86%, which represents a decrease over the last two years from 1.89% (2001)and 0.97% (2002).

The weak economic conditions in 2000 and 2001 kept delinquency levels somewhat higher thanhistorically experienced. A recovery in the real-estate market in 2002 and 2003, however, hasserved to lower current delinquency levels. Write-offs during 2003 decreased over 2002 by$236,910.63. Contributions towards monthly loan loss reserves remained the same in 2002and 2003. Even with decreasing delinquency the Credit Union maintained the same reservelevels through 2003, to mitigate the impact of future loan losses.

I would like to thank the other members of the committee for their work and involvement:Susanne Jakobsen, John Newall, Joe Sieber and Bob Smits. I would also like to thank allemployees for their efforts put forth this past year, and the membership for their continuedsupport of the credit union’s products and services.

Len Townsend,Chair, Investment & Lending Committee

Audit Committee ReportDuring 2003, the Audit Committee met frequently to review the results of external and internalaudits. We also met to review and approve the annual budget and year-end financial statements.The committee reviewed and approved the 2003 audit plan and in all areas we are confident thatcurrent policies and procedures, and monitoring processes provide a safe and sound organizationfor our members.

Our internal auditors, Peter Reimer and Associates, of Delta, again concentrated on the risk andcontrols aspect of audit. In addition to regular branch audits, we have instituted technology andnetwork security reviews, database audits and an initial audit of the Money Laundering andProceeds of Terrorism policies and procedures.

Our external auditors, BDO Dunwoody, of Vancouver, and Church Pickard & Co., of Nanaimo,worked with the Audit Committee and the Board of Directors to ensure the timely and successfulcompletion of the external audit. Our thanks to Bill Cox, Lorana Laporte and the staff of both firms.

I wish to acknowledge the contributions of management and staff for their assistance andsupport. Also, my thanks to my fellow Audit Committee members – Bob Smits, Joe Sieber,Len Townsend, Susanne Jakobsen and Michelle Butts for their commitment to the audit process.

Respectfully submitted,

John LittleChair, Audit Committee

Consolidated Financial Statements ofCoastal Community Credit Union

Year ended December 31, 2003

21

Auditors’ ReportTo the Members of Coastal Community Credit Union

We have audited the consolidated Balance Sheet of Coastal Community Credit Union

as at December 31, 2003 and the consolidated statements of Earnings and Retained

Earnings and Cash Flows for the year then ended. These consolidated financial statements

are the responsibility of the Credit Union’s management.Our responsibility is to express an

opinion on these financial statements based on our audit.

We conducted our audit in accordance with Canadian generally accepted auditing

standards. Those standards require that we plan and perform an audit to obtain reasonable

assurance whether the consolidated financial statements are free of material misstatement.

An audit includes examining, on a test basis, evidence supporting the amounts and

disclosures in the consolidated financial statements. An audit also includes assessing the

accounting principles used and significant estimates made by management, as well as

evaluating the overall financial statement presentation.

In our opinion, these consolidated financial statements present fairly, in all material respects,

the financial position of the Credit Union as at December 31, 2003 and the results of its

operations and its cash flows for the year then ended in accordance with Canadian

generally accepted accounting principles. As required by the British Columbia Financial

Institutions Act, we report that, in our opinion, these principles have been applied on a

basis consistent with that of the preceding year.

Chartered Accountants

Nanaimo, British Columbia

February 6, 2004

Consolidated Financial Statements of

Coastal Community Credit Union

Year ended December 31, 2003

22

2003 2002

AssetsCash resources (note 3) $52,756,193 $50,531,751

Loans (note 4) 463,181,285 421,481,422

Investments (note 6) 11,870,853 12,920,318

Premises and equipment,

net of amortization (note 7) 8,634,715 4,963,765

Other assets (note 8) 4,714,301 3,420,529

$541,157,347 $493,317,785

LiabilitiesMember deposits (note 9) $514,127,006 $470,593,506

Short-term borrowings from Credit Union

Central of British Columbia (note 10) 500,045 –

Accounts payable and accrued liabilities 5,121,313 4,232,287

519,748,364 474,825,793

Members’ equityRetained earnings 21,408,983 18,491,992

$541,157,347 $493,317,785

See accompanying notes to consolidated financial statements.

On behalf of the Board:

Judy Fraser John Little

Director Director

Coastal Community Credit Union

Consolidated Balance Sheet

December 31, 2003, with comparative figures for 2002

23

2003 2002

Financial income:

Loans $28,379,100 $26,571,917

Cash resources and investments 3,205,446 2,641,206

31,584,546 29,213,123

Financial expenses:

Deposit 12,694,068 12,001,276

Borrowings 168,000 57,189

12,862,068 12,058,465

Financial margin 18,722,478 17,154,658

Other income (expenses):

Other income (note 12) 8,859,527 8,437,011

Provision for credit losses,

net of recoveries (note 4) (744,957) (840,265)

Other expenses (note 13) (2,588,218) (2,628,547)

5,526,352 4,968,199

Operating margin 24,248,830 22,122,857

Operating expenses (note 14) 19,584,279 18,979,279

Earnings from operations 4,664,551 3,143,578

Gain on dispositions (note 22) 154,080 2,314,955

Non-controlling interest (128,672) 13,963

Distribution to members (note 15) (1,020,201) (932,555)

Earnings before income taxes 3,669,758 4,539,941

Income taxes 752,767 569,001

Net earnings 2,916,991 3,970,940

Retained earnings, beginning of year 18,491,992 14,521,052

Retained earnings, end of year $21,408,983 $18,491,992

See accompanying notes to consolidated financial statements.

Coastal Community Credit Union

Consolidated Statement of Earnings and Retained Earnings

Year ended December 31, 2003, with comparative figures for 2002

24

2003 2002

Cash provided by (used in):Operations:

Net earnings $2,916,991 $3,970,940

Items not involving cash:

Amortization of premises

and equipment 939,595 1,025,097

Amortization of goodwill – 41,570

Gain on dispositions (154,080) (2,314,955)

Provision for loan losses 744,957 840,265

Change in non-cash operating

working capital (406,011) (363,161)

4,041,452 3,199,756

Financing:

Deposits 43,533,500 37,739,542

Short-term borrowings (repayments) 500,045 –

44,033,545 37,739,542

Investments:

Loans (46,470,713) (39,460,569)

Investments 1,049,465 (10,032,336)

Purchase of premises and equipment (4,609,280) (636,127)

Proceeds on dispositions 4,179,973 2,087,665

(45,850,555) (48,041,367)

Increase (Decrease) in cash position 2,224,442 (7,102,069)

Cash resources, beginning of year 50,531,751 57,633,820

Cash resources, end of year $52,756,193 $50,531,751

Supplemental Financial Information:Interest received $31,414,094 $29,007,301

Interest and dividends paid 12,250,465 12,354,847

Income taxes paid 553,266 399,255

Non-cash Investing Activity:Receivable relating to land disposition $ 640,000 $ 800,000

See accompanying notes to consolidated financial statements.

Coastal Community Credit Union

Consolidated Statement of Cash Flows

Year ended December 31, 2003, with comparative figures for 2002

25

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

Coastal Community Credit Union (“Credit Union”) is incorporated under the British ColumbiaCredit Union Incorporation Act. The operation of the Credit Union is subject to the BritishColumbia Financial Institutions Act. The Credit Union predominately serves members in thecentral Vancouver Island area.

1. Significant accounting policies:

(a) Basis of presentation:

These consolidated financial statements have been prepared in accordance with generallyaccepted accounting principles in Canada.

(b) Principles of consolidation:

These consolidated financial statements include the assets, liabilities, and operating resultsof the Credit Union and its wholly owned subsidiary, Coastal Community FinancialManagement Inc. and Coastal Community Insurance Agencies Ltd. (50% interest ownedby CCCU).

(c) Use of estimates:

The preparation of the financial statements of the Credit Union in accordance withCanadian generally accepted accounting principles requires management to makeestimates and assumptions, mainly considering values, which affect reported amounts ofassets, liabilities, net income, and related disclosures. Amounts are based on bestestimates but actual amounts may vary from the amounts recorded. Areas subject toestimation include provisions for credit losses (because of the inherent subjectivityinvolved in estimating the amount and timing of future cash flows) and amortization ofpremises and equipment (because of the difficulty in estimating the useful lives of theassets).

(d) Loans:

Loans to members are stated at the unpaid principal plus accrued interest less anallowance established to provide against potential losses on ultimate realization of theloan portfolio. The allowance is determined by reference to specific loans in arrears, priorloan collection experience, geographical concentration, economic conditions, and otherfactors, which in management’s judgment deserve consideration. Loans considereduncollectible are written off.

(e) Investments and goodwill:

Investments are recorded at lower of cost or net realizable value. Goodwill reflects theexcess of cost over the underlying tangible value of Creduco Insurance Agencies Ltd.assets acquired and is amortized on a straight-line basis over 10 years. On January 2,2002, a 50% interest in Coastal Community Insurance Agencies was sold to CumisServices Ltd.

(f) Premises and equipment:

Premises and equipment are recorded at cost less accumulated amortization.Amortization is provided on the straight-line basis over 5 to 10 years for furniture andequipment, 10 to 15 years for leasehold improvements, 25 years for buildings, and 3 to 5years for computer equipment.

(g) Revenue recognition:

Interest income on loans is recorded on the accrual method, unless the loan is classifiedas impaired. A loan is considered as impaired generally at the earlier of when, in theopinion of management, there is reasonable doubt as to the collectibility of principal orinterest, or when principal or interest is 180 days past due. Thereafter, interest income isrecognized on a cash basis only after any specific provisions or partial write-offs havebeen recovered and provided there is no further doubt as to the collectibility of principal.

26

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

1. Significant accounting policies (continued):

Income received on prepayment or renegotiation of fixed term loans is recorded asearned income in the year it is received.

(h) Dividends:

Dividends on non-equity and equity shares and patronage rebates are charged againstearnings.

2. Capital requirements:

The Financial Institutions Act requires the Credit Union to maintain, at all times, a capital baseadequate in relation to its level of business activities. The level of capital required is based on aprescribed percentage of the total value of its risk-weighted assets, each asset of the CreditUnion being assigned a risk factor based on the probability that a loss may be incurred onultimate realization of that asset.

Effective January 1, 1994, the Financial Institutions Act regulations prescribed a minimumrequired capital ratio of 8% of the risk-weighted value of assets. At December 31, 2003, theCredit Union had attained a capital ratio in excess of 11%.

3. Cash resources:

2003 2002

Cash on hand $3,414,353 $3,117,133

Demand and short-term investments held at Credit Union Central of British Columbia 48,495,791 46,656,691

Accrued interest on cash resources 846,049 757,927

$52,756,193 $50,531,751

In accordance with provincial legislation and the terms of arrangements with Credit UnionCentral of British Columbia, credit unions are required to maintain deposits with Credit UnionCentral of British Columbia totaling 10% of their deposits (net of equity and non-equityshares) and debt liabilities.

4. Loans:

An analysis of the Credit Union’s loan portfolio, (net of allowance for credit losses bycategory), is as follows:

2003 2002

Gross Specific Carrying Carryingamount allowance amount amount

Residential mortgages $300,366,386 $23,567 $300,342,819 $271,717,415

Commercial mortgages 75,759,970 987,281 74,772,689 63,350,752

Personal and other loans 86,799,878 175,041 86,624,837 85,038,445

Accrued interest 1,440,940 – 1,440,940 1,374,810

Net loans $464,367,174 $1,185,889 $463,181,285 $421,481,422

27

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

4. Loans (continued):

Analysis of specificallowance for Residential Commercial Personal Total Totalcredit losses mortgages mortgages and other 2003 2002

Allowance for credit losses, beginning $20,975 $787,451 $243,655 $1,052,081 $1,061,510

Provision, net of recoveries 2,592 499,708 242,657 744,957 840,265

23,567 1,287,159 486,312 1,797,038 1,901,775

Write-offs, less recoveries – 299,878 311,271 611,149 849,694

Allowance for creditlosses, ending $23,567 $987,281 $175,041 $1,185,889 $1,052,081

Allowance as a percentage of total loans 0.26% 0.25%

5. Securitized mortgages:

The Credit Union, as part of its program of managing liquidity, enters into arrangements tosecuritize mortgages through certain intermediaries.

Such securitized mortgages, which are not included in the loan balances, total $1,526,121 asat December 31, 2003 (2002 – $7,696,677). The Credit Union is required to administer thesemortgages until maturity. These securitized mortgages will mature by 2005.

The outstanding principal on securitized mortgages has either been insured with agovernment corporation or the holders have contractually waived recourse against the CreditUnion in the event the mortgage defaults.

6. Investments:

2003 2002

Statutory investments:

Credit Union Central of British Columbia shares $ 1,868,159 $ 1,813,383

Non-statutory investments:

Mortgage packages purchased 8,096,852 10,190,964

Communities First Investment Fund 1,000,000 –

Data Solutions Inc. shares at cost (market value $469,893) 557,297 557,297

Other investments 188,785 154,344

Goodwill, net of accumulated amortization 53,992 110,660

Accrued income on investments 105,768 93,670

$11,870,853 $12,920,318

28

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

6. Investments (continued):

(a) Shares in Credit Union Central of British Columbia are a required investment as acondition of membership in Credit Union Central of British Columbia and provinciallegislation. This investment is determined based on the Credit Union’s assets and isrealizable only on withdrawal from membership.

(b) Mortgages purchased have maturities in the range from 1 to 4 years with an averageanticipated yield of between 4.41% and 5.70%.

7. Premises and equipment:

2003 2002

Accumulated Net book Net bookCost amortization value value

Land $1,603,019 $ – $ 1,603,019 $1,003,630

Buildings 4,397,948 352,627 4,045,321 1,072,282

Leasehold improvements 2,819,690 1,640,318 1,179,372 1,366,784

Furniture and equipment 4,919,342 3,625,657 1,293,685 1,243,009

Computer equipment 2,755,376 2,242,058 513,318 278,060

$16,495,375 $7,860,660 $8,634,715 $4,963,765

8. Other assets:

2003 2002

Accounts receivable $1,307,073 $671,462

Prepaid expenses 903,017 634,751

Receivable – land sale 640,000 800,000

Advance payments for data processing services (note 18) 1,886,515 1,261,201

Property acquired in settlement of loans – –

Non – controlling interest (22,304) 53,115

$4,714,301 $3,420,529

The non-controlling interest consists of equity of CCIA held by a third party.

29

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

9. Member deposits:

2003 2002

Demand $156,563,560 $144,338,734

Term 249,214,081 226,240,979

Registered savings plans 97,850,228 90,133,215

Accrued interest on member deposits 5,381,554 4,769,995

509,009,423 465,482,923

Non-equity shares:

Non-voting, $1 par value, unlimited number authorized 216,911 233,988

Equity shares:

Membership equity shares, voting, $1 par value, unlimited number authorized 2,358,932 2,355,016

Investment equity shares, non-voting, $1 par value, unlimited number authorized 2,541,740 2,521,579

$514,127,006 $470,593,506

Non-equity shares:

Amounts contributed by members for non-equity shares can be withdrawn on demand orredeemed by the Credit Union. The holders of these shares may be entitled to a life insurancepolicy of up to $2,000 in accordance with the original purchase terms. The Credit Union hasceased issuance of these shares.

Equity shares:

The equity shares of the Credit Union are divided into two classes designated as membershipequity shares and investment equity shares having the following rights and restrictions:

• Each member shall purchase not less than 5 and may purchase not more than 1,000membership equity shares; a member may purchase a maximum of $5,000 in investmentequity shares; and, holding of non-equity shares is not restricted.

• Redemption of membership equity and investment shares is subject to certain conditionsand to approval of the directors, subject to an overall restriction that the Credit Union maynot be required to redeem in any financial year more than 10% of the total amount of suchshares issued and outstanding on the last day of the preceding financial year.

• Dividends declared may, at the discretion of the directors, be different for each class ofshares, and such dividends may be paid as an allocation of membership equity shares ornon-equity shares.

• Equity shares are not insured by the Credit Union Deposit Insurance Corporation ofBritish Columbia.

30

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

9. Member deposits (continued):

Deposit insurance protection:

The Credit Union Deposit Insurance Corporation of British Columbia, a governmentcorporation, protects the deposits of all British Columbia credit union members up to amaximum of $100,000 per “separate deposit” (as defined by Regulation) per credit union.

10. Credit facilities:

The Credit Union has an operating line of credit secured by a demand debenture in theamount of $30,000,000 in favour of Credit Union Central of British Columbia. The debenturecreates a floating charge on certain assets and undertakings of the Credit Union.

11. Commitments:

Computer services:

The Credit Union is committed to acquire on-line data processing services until January 1,2010. Data processing charges are based on the level of equipment and services utilized andon the number of Credit Union members.

Premises:

The Credit Union has committed to lease premises until 2011. The minimum lease payments,including estimated operating costs incorporated into lease agreements, in each of the nextfive years are $898,074 in 2004, $902,502 in 2005, $992,979 in 2006, $1,050,392 in 2007,and $863,336 in 2007.

12. Other income:

2003 2002

Member services:

Chequing and savings accounts $2,397,870 $2,433,221

Other service income 1,136,338 1,111,007

Insurance administration fees 553,453 482,608

Loan fees 653,229 597,589

Mortgage payout and prepayment income 710,188 561,100

Safety deposit boxes 139,740 140,423

5,590,818 5,325,948

Building and property income 119,796 97,551

Commission income from subsidiaries 3,148,913 3,013,512

$8,859,527 $8,437,011

31

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

13. Other expenses:

2003 2002

Electronic services $ 986,832 $ 990,994

Automated teller machine services 368,636 439,540

Other services 824,720 834,773

Chequing services 408,030 363,240

$ 2,588,218 $ 2,628,547

14. Operating expenses:

2003 2002

Salaries and benefits $11,883,399 $11,315,183

Premises and equipment 1,814,372 1,899,292

Other administrative 1,950,810 1,850,819

Data processing 1,367,952 1,279,970

Amortization of premises and equipment 939,595 1,025,097

Advertising and member relations 724,467 567,795

Professional services 460,329 458,886

Regulatory costs 195,060 359,666

Capital tax 248,295 181,001

Amortization of goodwill – 41,570

$19,584,279 $18,979,279

15. Distribution to members:

2003 2002

Dividends on equity shares $ 229,620 $ 397,766

Dividends on non-equity shares 184 2,362

Patronage rebate 790,397 532,427

$ 1,020,201 $ 932,555

16. Employee future benefits:

The Credit Union contributes toward retirement benefits for its employees.

(a) Group registered retirement savings plan

The contributions made for the majority of employees are made to a group registeredretirement savings plan at rates varying from 8% to 10% of annual salary. Contributionsmade during the year totaled $ 678,056 (2002 – $667,517). Employees contributed atotal of $207,842 (2002 – $175,378) during the year.

32

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

16. Employee future benefits (continued):

(b) Multi-employer defined benefit pension plan

A multi-employer defined benefit pension plan exists where the members are employeesfrom various credit unions in British Columbia. Contributions totaling $57,270 (2002 –$45,087) were made to this plan during the year on behalf of certain employees.Employees contributed a further $39,253 (2002 – $29,284) to the pension plan.

The plan is a defined benefit pension plan and is subject to actuarial review every threeyears. The latest available actuarial review is for December 31, 2000. As of the December31, 2000 valuation, plan assets exceeded plan liabilities by approximately $15,100,000.The actuary does not attribute portions of the plan surplus to individual employers. TheCredit Union records contributions to the plan as an expense in the year which paymentsare made.

(c) Individual pension plans

Individual pension plans are maintained for certain employees. The plans generally havethe characteristics of a defined contribution plan. Contributions made to these plansduring the year totaled $75,910 (2002 – $68,743) and by the employees totaled $44,538(2002 – $42,934).

17. Other Information:

At December 31, 2003 loans to directors, officers, management and members of a committeeof the Credit Union amounted to $ 4,194,535 (2002 – $4,264,590).

Directors received remuneration of $57,140 in 2003 (2002 – $49,693).

18. Related party transactions:

The Credit Union is under contract to purchase data processing services from DatawestSolutions Inc. until January 1, 2010.

The President and Chief Executive Officer of the Credit Union was, at December 31, 2003, amember of the Board of Datawest Solutions Inc.

Advance payments for data processing services have been made totaling $1,886,515 (2002 –$1,259,940). Advance payments of $152,379 bear interest at between 9% and 10%. The2002 advance payments of $867,470 bear a floating interest rate (prime) plus 2.5% perannum. The 2003 advance payments of $866,666 bear interest at prime plus 2%. Theadvance payments have been recovered by reduction of amounts otherwise payable for dataprocessing services. The advance payments will be fully recovered by the end of the contract,January 1, 2010.

This transaction is recorded at the exchange amount, being the consideration established andagreed to by the related parties.

19. Derivative financial instruments:

Index-linked swaps are being used by the Credit Union to hedge risk for registered and non-registered term products linked to changes in various stock indexes. The notional principal of$259,978 related to these contracts is not included in the non-consolidated balance sheet(2002 – $838,901).

Expenses from these contracts are deferred and amortized over the term of the swap contract.

Fixed – Received Interest rate swaps are being used by the Credit Union to increase thematurity structure of the asset base to better align rate sensitivity to the overall liability base.The notional value of $42,500,000 (2002 – $45,000,000) related to the contracts in placeDecember 31, 2003 is not included in the balance sheet. Interest earned on these swaps isbeing accrued over the term of the swap.

33

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

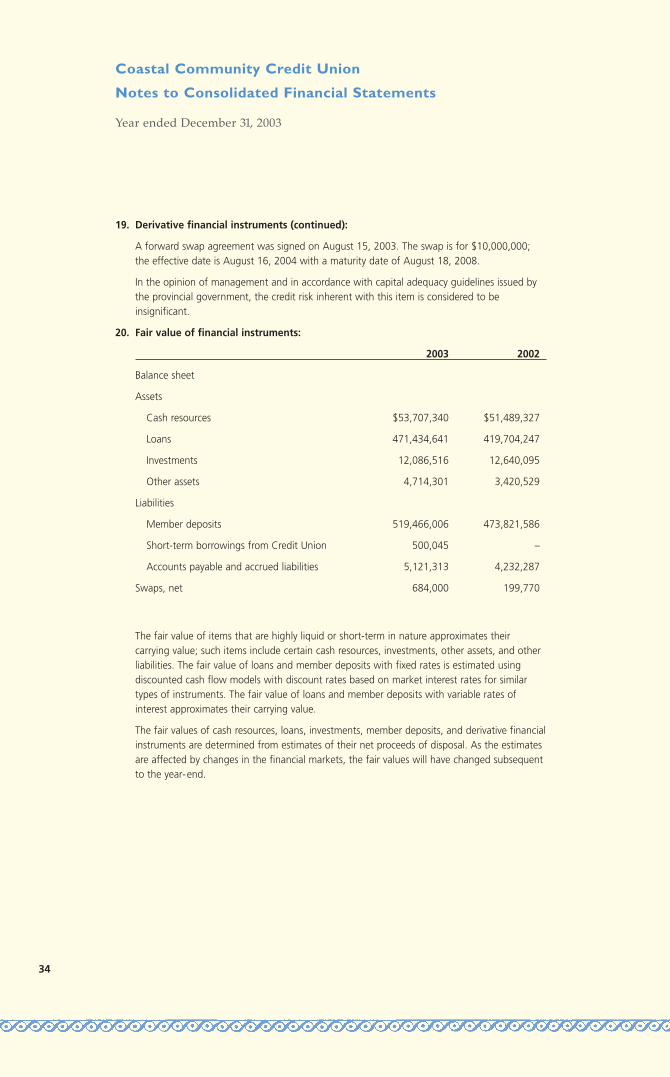

19. Derivative financial instruments (continued):

A forward swap agreement was signed on August 15, 2003. The swap is for $10,000,000;the effective date is August 16, 2004 with a maturity date of August 18, 2008.

In the opinion of management and in accordance with capital adequacy guidelines issued bythe provincial government, the credit risk inherent with this item is considered to beinsignificant.

20. Fair value of financial instruments:

2003 2002

Balance sheet

Assets

Cash resources $53,707,340 $51,489,327

Loans 471,434,641 419,704,247

Investments 12,086,516 12,640,095

Other assets 4,714,301 3,420,529

Liabilities

Member deposits 519,466,006 473,821,586

Short-term borrowings from Credit Union 500,045 –

Accounts payable and accrued liabilities 5,121,313 4,232,287

Swaps, net 684,000 199,770

The fair value of items that are highly liquid or short-term in nature approximates theircarrying value; such items include certain cash resources, investments, other assets, and otherliabilities. The fair value of loans and member deposits with fixed rates is estimated usingdiscounted cash flow models with discount rates based on market interest rates for similartypes of instruments. The fair value of loans and member deposits with variable rates ofinterest approximates their carrying value.

The fair values of cash resources, loans, investments, member deposits, and derivative financialinstruments are determined from estimates of their net proceeds of disposal. As the estimatesare affected by changes in the financial markets, the fair values will have changed subsequentto the year-end.

34

Coastal Community Credit Union

Notes to Consolidated Financial Statements

Year ended December 31, 2003

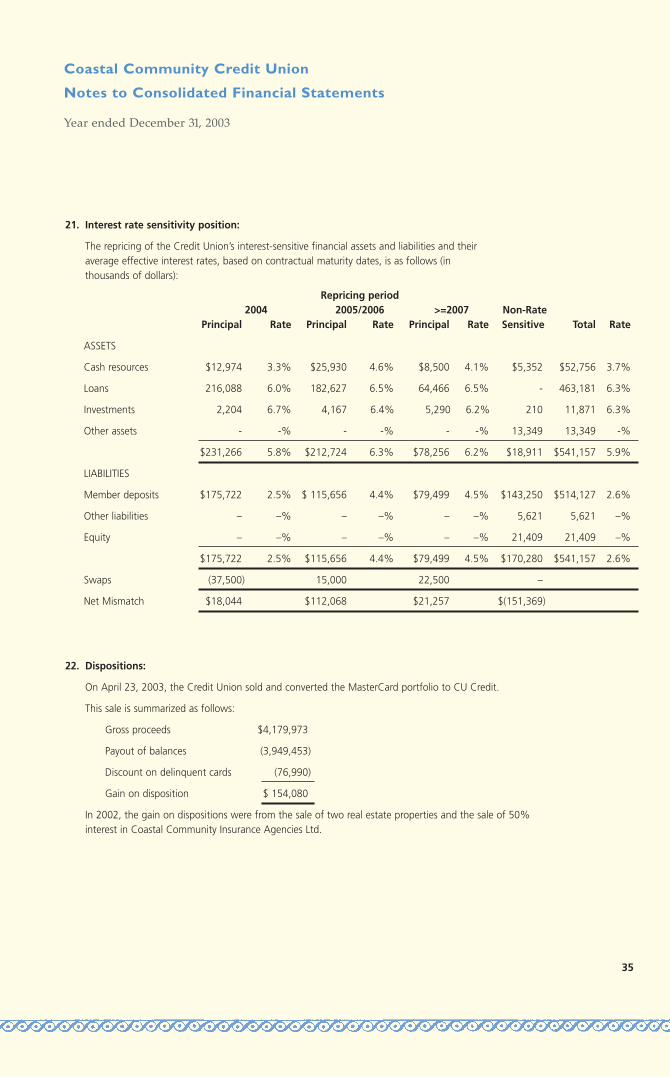

22. Dispositions:

On April 23, 2003, the Credit Union sold and converted the MasterCard portfolio to CU Credit.

This sale is summarized as follows:

Gross proceeds $4,179,973

Payout of balances (3,949,453)

Discount on delinquent cards (76,990)

Gain on disposition $ 154,080

In 2002, the gain on dispositions were from the sale of two real estate properties and the sale of 50%interest in Coastal Community Insurance Agencies Ltd.

21. Interest rate sensitivity position:

The repricing of the Credit Union’s interest-sensitive financial assets and liabilities and theiraverage effective interest rates, based on contractual maturity dates, is as follows (inthousands of dollars):

35

Repricing period2004 2005/2006 >=2007 Non-Rate

Principal Rate Principal Rate Principal Rate Sensitive Total Rate

ASSETS

Cash resources $12,974 3.3% $25,930 4.6% $8,500 4.1% $5,352 $52,756 3.7%

Loans 216,088 6.0% 182,627 6.5% 64,466 6.5% - 463,181 6.3%

Investments 2,204 6.7% 4,167 6.4% 5,290 6.2% 210 11,871 6.3%

Other assets - -% - -% - -% 13,349 13,349 -%

$231,266 5.8% $212,724 6.3% $78,256 6.2% $18,911 $541,157 5.9%

LIABILITIES

Member deposits $175,722 2.5% $ 115,656 4.4% $79,499 4.5% $143,250 $514,127 2.6%

Other liabilities – –% – –% – –% 5,621 5,621 –%

Equity – –% – –% – –% 21,409 21,409 –%

$175,722 2.5% $115,656 4.4% $79,499 4.5% $170,280 $541,157 2.6%

Swaps (37,500) 15,000 22,500 –

Net Mismatch $18,044 $112,068 $21,257 $(151,369)

Bowen2350 Labieux Rd.(250) 729 -2550

Hammond Bay6365 Hammond Bay Rd.(250) 390 - 8900

Harbourfront#111 – 59 Wharf St.(250) 741-3100

Southgate#111 – 50 Tenth St.(250) 741 -1233

MemberLink24 hr banking

Nanaimo(250) 741-10101- 888-741- 4040

Parksville(250) 248- 65701-800-303-6570

Administration#21-13 Victoria Cres.Nanaimo,B.C.V9R 5B9(250) 741-32001- 888 -741-1010

Business Centre2350 Labieux Rd.Nanaimo,B.C.(250) 729-2569

Coastal Community Credit UnionA N D

Coastal Community Financial Management Inc.

Community Branch Locations

Coastal Community Insurance Agencies Ltd.

Internet Sitewww.cccu.ca

Gabriola Island#7 – 580 North Rd.(250) 247- 8521

Nanoose Bay#2 -2451 Collins Cres.(250) 468 -7624

Parksville140 Alberni Hwy.(250) 248-3275

Qualicum Beach118 2nd Ave.(250) 752-9244

Nanaimo

Nanaimo

Bowen2350 Labieux Rd.(250) 729-2570

Hammond Bay6365 Hammond Bay Rd.(250) 390-8940

Harbourfront#111 – 59 Wharf St.(250) 741-3175

Southgate#111 – 50 Tenth St.(250) 741- 8600

Gabriola Island#7 – 580 North Rd.(250) 247- 8521

Nanoose Bay#2-2451 Collins Cr.(250) 468-9944

Parksville140 Alberni Hwy(250) 248- 5725

Qualicum Beach120A 2nd Ave.West(250) 752- 3331

Coastal Community Credit Union

Success Story