Summary Comparison of New Accounting Standards for Private Enterprises

(Part II of the revised CICA Handbook — Accounting) to XFI Version (Part V)

16 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

About this Comparison

As of December 31, 2009

This comparison has been prepared by the staff of the Accounting Standards Board (AcSB) and has not been approved by the AcSB.

This document provides a high-level comparison of accounting standards for private enterprises (Part II) and the XFI version of Part V of the CICA Handbook – Accounting (Handbook). It covers significant recognition and measurement differences only and does not necessarily include all of the differences that might arise in a particular entity’s circumstances. Presentation and disclosure requirements are not within the scope of this comparison. Presentation requirements for Part II are provided in Section 1520, Income Statement, Section 1521, Balance Sheet, and Section 1540, Cash Flow Statement. A compilation of disclosure requirements is also provided in Part II of the Handbook.

This document should not be used in preparing finan-cial statements. To understand fully the implications of preparing financial statements in accordance with Part II of the Handbook, users of this comparison must refer to the standards themselves.

17The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

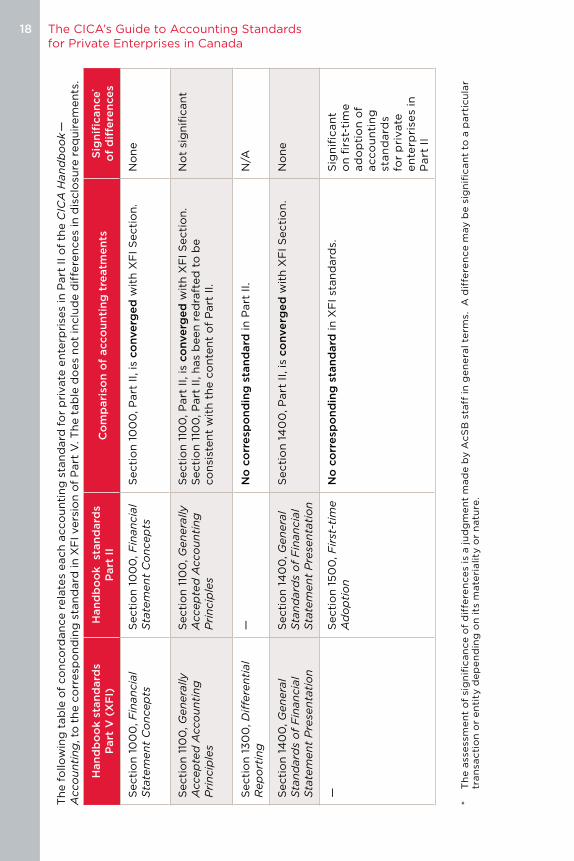

The standards in Part II and the XFI Version of Part V of the Handbook are based on common conceptual frameworks. Part V of the Handbook was used as a starting point in developing the standards in Part II. Standards in Part V that are largely irrelevant to the private enterprise sector have been excluded from Part II and a limited number of issues that have caused significant concern for private enterprises have been reconsidered. However, the majority of the recognition and measurement requirements in Part V of the Handbook do not cause significant concern for private enterprises and have been retained in Part II “as is”. Emerg-ing Issues Committee (EIC) Abstracts of Issues Discussed have been excluded from Part II but in a limited number of instances, guidance on significant issues addressed in EIC Abstracts has been incorporated into Part II.

This comparison is organized according to Handbook Sec-tions and Accounting Guidelines and reflects standards issued as of December 31, 2009. The term “converged” has been used in the comparison when the standards in Part II are substantially the same as the relevant standards in the XFI version of Part V. Similar requirements compiled in a single standard in Part II that were previously reflected in two or more standards in Part V, are not considered “differences” for the purpose of this comparison.

18 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Th

e f

ollo

win

g t

ab

le o

f co

nco

rdan

ce r

ela

tes

each

acco

un

tin

g s

tan

dard

fo

r p

rivate

en

terp

rise

s in

Part

II o

f th

e C

ICA

Han

db

oo

k —

A

cco

un

tin

g, t

o t

he c

orr

esp

on

din

g s

tan

dard

in

XF

I vers

ion

of

Part

V. T

he t

ab

le d

oes

no

t in

clu

de d

iffe

ren

ces

in d

isclo

sure

req

uir

em

en

ts.

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

10

00

, F

inan

cia

l S

tate

men

t C

on

cep

tsS

ecti

on

10

00

, F

inan

cia

l S

tate

men

t C

on

cep

tsS

ecti

on

10

00

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

110

0, G

en

era

lly

Acc

ep

ted

Acc

ou

nti

ng

P

rin

cip

les

Secti

on

110

0, G

en

era

lly

Acc

ep

ted

Acc

ou

nti

ng

P

rin

cip

les

Secti

on

110

0, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Secti

on

110

0, P

art

II,

has

been

red

raft

ed

to

be

co

nsi

sten

t w

ith

th

e c

on

ten

t o

f P

art

II.

No

t si

gn

ifican

t

Secti

on

13

00

, D

iffe

ren

tial

Rep

ort

ing

—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

N/A

Secti

on

14

00

, G

en

era

l S

tan

dard

s o

f F

inan

cia

l S

tate

men

t P

rese

nta

tio

n

Secti

on

14

00

, G

en

era

l S

tan

dard

s o

f F

inan

cia

l S

tate

men

t P

rese

nta

tio

n

Se

cti

on

14

00

, Part

II, is

co

nve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

—S

ecti

on

15

00

, F

irst

-tim

e

Ad

op

tio

nN

o c

orr

esp

on

din

g s

tan

dard

in

XF

I st

an

dard

s.S

ign

ifican

t o

n fi

rst-

tim

e

ad

op

tio

n o

f acco

un

tin

g

stan

dard

s fo

r p

rivate

e

nte

rpri

ses

in

Part

II

* T

he a

sse

ssm

en

t o

f si

gn

ifica

nce o

f d

iffe

ren

ce

s is

a ju

dg

me

nt

ma

de b

y A

cS

B s

taff

in

ge

ne

ral te

rms.

A

dif

fere

nce m

ay b

e s

ign

ifica

nt

to a

pa

rtic

ula

r tr

an

sac

tio

n o

r e

nti

ty d

ep

en

din

g o

n its

mate

ria

lity

or

natu

re.

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

19The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

15

05

, D

isclo

sure

of

Acc

ou

nti

ng

Po

licie

sS

ecti

on

15

05

, Dis

clo

sure

o

f A

cco

un

tin

g P

olic

ies

All

req

uir

em

en

ts in

th

is S

ecti

on

rela

te t

o d

isclo

sure

s,

wh

ich

are

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

Secti

on

15

06

, A

cco

un

tin

g

Ch

an

ges

Secti

on

15

06

, A

cco

un

tin

g C

han

ges

Secti

on

15

06

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

, excep

t th

at

Secti

on

15

06

, P

art

II,

perm

its

cert

ain

acco

un

tin

g p

olic

y c

ho

ices

to b

e c

han

ged

wit

ho

ut

meeti

ng

th

e c

rite

rio

n in

15

06

.06

of

pro

vid

ing

mo

re

rele

van

t o

r re

liab

le in

form

ati

on

(se

e 1

50

6.0

9).

Sig

nifi

can

t

Secti

on

15

08

, M

easu

rem

en

t U

nce

rtain

tyS

ecti

on

15

08

, M

easu

rem

en

t U

nce

rtain

ty

All

req

uir

em

en

ts in

th

is S

ecti

on

rela

te t

o d

isclo

sure

s,

wh

ich

are

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

Secti

on

15

10, C

urr

en

t A

ssets

an

d C

urr

en

t L

iab

iliti

es

Secti

on

15

10, C

urr

en

t A

ssets

an

d C

urr

en

t L

iab

iliti

es

Secti

on

15

10, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Th

e f

ollo

win

g S

ecti

on

s in

Part

V h

ave b

een

in

co

rpo

rate

d in

to S

ecti

on

15

10, P

art

II:

• S

ecti

on

30

00

(se

e 1

510

.07);

an

d•

Secti

on

30

40

(se

e 1

510

.06

).

Cert

ain

gu

idan

ce f

rom

th

e f

ollo

win

g E

IC A

bst

racts

has

been

in

clu

ded

in

Secti

on

15

10, P

art

II:

• E

IC-5

9 (

see 1

510

.14

); a

nd

• E

IC-1

22 (

see 1

510

.13

).

No

ne

20 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

15

20

, In

com

e

Sta

tem

en

tS

ecti

on

15

20

, In

com

e

Sta

tem

en

tT

his

pre

sen

tati

on

Secti

on

refl

ects

in

co

me s

tate

men

t p

rese

nta

tio

n r

eq

uir

em

en

ts f

rom

oth

er

Secti

on

s –

pre

sen

tati

on

is

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

—S

ecti

on

15

21,

Bala

nce

S

heet

Th

is p

rese

nta

tio

n S

ecti

on

refl

ects

bala

nce s

heet

pre

sen

tati

on

req

uir

em

en

ts f

rom

oth

er

Secti

on

s –

pre

sen

tati

on

is

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

Secti

on

15

35

, C

ap

ital

Dis

clo

sure

s—

N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

N/A

Secti

on

15

40

, C

ash

Flo

w

Sta

tem

en

tS

ecti

on

15

40

, C

ash

F

low

Sta

tem

en

tS

ecti

on

15

40

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Ho

wever, u

nd

er

Part

II,

all

en

terp

rise

s m

ust

pro

vid

e a

cash

flo

w s

tate

men

t.

Sig

nifi

can

t fo

r en

terp

rise

s th

at

do

no

t p

rovid

e

a c

ash

flo

w

state

men

t u

nd

er

XF

I st

an

dard

s

Secti

on

15

82, B

usi

ness

C

om

bin

ati

on

sS

ecti

on

15

82, B

usi

ness

C

om

bin

ati

on

sS

ecti

on

15

82, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Secti

on

15

82 is

eff

ecti

ve o

n a

do

pti

on

of

Part

II as

Part

II d

oes

no

t in

clu

de S

ecti

on

15

81.

Sig

nifi

can

t fo

r en

terp

rise

s ad

op

tin

g P

art

II

pri

or

to 2

011

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

21The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

15

90

, S

ub

sid

iari

es

Secti

on

15

90

, S

ub

sid

iari

es

Secti

on

15

90

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

, excep

t as

no

ted

belo

w.

Un

der

Secti

on

15

90

, P

art

II,

an

en

terp

rise

may a

cco

un

t fo

r su

bsi

dia

ries

by c

on

solid

ati

ng

th

em

, o

r u

sin

g e

ith

er

the c

ost

or

eq

uit

y m

eth

od

. T

his

is

co

nsi

sten

t w

ith

th

e

dif

fere

nti

al re

po

rtin

g o

pti

on

in

XF

I S

ecti

on

. H

ow

ever

an

invest

men

t in

a s

ub

sid

iary

wh

ose

eq

uit

y s

ecu

riti

es

are

qu

ote

d in

an

acti

ve m

ark

et

is n

ot

acco

un

ted

fo

r at

co

st, b

ut

may b

e a

cco

un

ted

fo

r at

fair

valu

e.

Sig

nifi

can

t fo

r a

sub

sid

iary

th

at

wo

uld

no

w b

e

acco

un

ted

fo

r at

fair

valu

e r

ath

er

than

co

st

Secti

on

16

01,

Co

nso

lidate

d

Fin

an

cia

l S

tate

men

tsS

ecti

on

16

01,

C

on

solid

ate

d F

inan

cia

l S

tate

men

ts

Secti

on

16

01,

Part

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

. N

on

e

Secti

on

16

02, N

on

-co

ntr

olli

ng

In

tere

sts

Secti

on

16

02, N

on

-co

ntr

olli

ng

In

tere

sts

Secti

on

16

02, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Secti

on

16

02 is

eff

ecti

ve o

n a

do

pti

on

of

Part

II as

Part

II d

oes

no

t in

clu

de S

ecti

on

16

00

.

Sig

nifi

can

t fo

r en

terp

rise

s ad

op

tin

g P

art

II

pri

or

to 2

011

Secti

on

16

25

, C

om

pre

hen

sive

Reva

luati

on

o

f A

ssets

an

d L

iab

iliti

es

Secti

on

16

25

, C

om

pre

hen

sive

R

eva

luati

on

of

Ass

ets

an

d L

iab

iliti

es

Secti

on

16

25

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

excep

t fo

r th

e a

cco

un

tin

g f

or

inco

me t

ax b

en

efi

ts (

see

1625

.43

-44

).

No

t si

gn

ifican

t

22 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

16

50

, F

ore

ign

C

urr

en

cy T

ran

slati

on

Secti

on

16

51,

Fo

reig

n

Cu

rren

cy T

ran

slati

on

Secti

on

16

51,

Part

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

16

50

.

Hed

ge a

cco

un

tin

g (

oth

er

than

a h

ed

ge o

f an

in

vest

men

t in

a s

elf

-su

stain

ing

fo

reig

n o

pera

tio

n)

is a

dd

ress

ed

in

Secti

on

38

56

, P

art

II,

rath

er

than

in

S

ecti

on

16

51,

Part

II,

an

d d

iffe

rs f

rom

XF

I S

ecti

on

16

50

.

No

ne, excep

t fo

r h

ed

ge

acco

un

tin

g

ad

dre

ssed

in

S

ecti

on

38

56

, P

art

II

Secti

on

170

1, S

eg

men

t D

isclo

sure

s—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

N/A

Secti

on

175

1, In

teri

m

Fin

an

cia

l S

tate

men

ts—

N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

N/A

Secti

on

18

00

, U

nin

corp

ora

ted

Bu

sin

ess

es

Secti

on

18

00

, U

nin

corp

ora

ted

B

usi

ness

es

Secti

on

18

00

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

30

00

, C

ash

—N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

Gu

idan

ce f

rom

X

FI S

ecti

on

in

co

rpo

rate

d in

Secti

on

15

10, P

art

II (s

ee

1510

.07).

N/A

Secti

on

30

10, Te

mp

ora

ry

Inve

stm

en

ts—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

Measu

rem

en

t an

d im

pair

men

t re

qu

irem

en

ts a

re p

rovid

ed

in

Secti

on

3

85

6, P

art

II.

Desi

gn

ati

on

as

“tem

po

rary

” is

no

lo

ng

er

rele

van

t.

Fin

an

cia

l in

stru

men

ts a

re c

lass

ified

as

cu

rren

t if

th

ey m

eet

the r

eq

uir

em

en

ts in

Secti

on

15

10,

Part

II.

Sig

nifi

can

t

Secti

on

30

20

, A

cco

un

ts a

nd

N

ote

s R

ece

ivab

le—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

Gu

idan

ce f

rom

X

FI S

ecti

on

in

co

rpo

rate

d in

Secti

on

38

56

, P

art

II (s

ee

38

56

.16

-.19

).

N/A

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

23The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

30

25

, Im

pair

ed

Lo

an

s—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

Gu

idan

ce

pro

vid

ed

in

Secti

on

38

56

, P

art

II,

dif

fers

fro

m t

hat

in S

ecti

on

30

25

(se

e 3

85

6.16

-.19

) in

th

at

alt

ern

ati

ve

measu

rem

en

ts a

re p

oss

ible

. W

hen

measu

rem

en

t o

f im

pair

men

t is

base

d o

n r

eco

vera

ble

am

ou

nts

, th

ese

est

imate

s are

dis

co

un

ted

usi

ng

mark

et

inte

rest

rate

s ra

ther

than

th

e o

rig

inal eff

ecti

ve in

tere

st r

ate

.

Oft

en

no

t si

gn

ifican

t

Secti

on

30

31,

Inve

nto

ries

Secti

on

30

31,

In

ven

tori

es

Secti

on

30

31,

Part

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

30

40

, P

rep

aid

E

xp

en

ses

—N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

Gu

idan

ce f

rom

X

FI S

ecti

on

in

co

rpo

rate

d in

Secti

on

15

10, P

art

II (s

ee

1510

.06

).

N/A

24 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

30

50

, Lo

ng

-term

In

vest

men

tsS

ecti

on

30

51,

In

vest

men

tsS

ecti

on

30

51,

Part

II d

iffe

rs f

rom

XF

I S

ecti

on

30

50

.

Sig

nifi

can

t d

iffe

ren

ces

are

no

ted

belo

w.

Un

der

Secti

on

30

51,

Part

II,

an

en

terp

rise

may a

cco

un

t fo

r si

gn

ifican

tly in

flu

en

ced

invest

ees

usi

ng

eit

her

the

co

st o

r eq

uit

y m

eth

od

. T

his

is

co

nsi

sten

t w

ith

th

e

dif

fere

nti

al re

po

rtin

g o

pti

on

in

XF

I S

ecti

on

30

50

. H

ow

ever, a

n invest

men

t in

a s

ign

ifican

tly in

flu

en

ced

in

vest

ee w

ho

se e

qu

ity s

ecu

riti

es

are

qu

ote

d in

an

acti

ve m

ark

et

is n

ot

acco

un

ted

fo

r at

co

st b

ut

may b

e

acco

un

ted

fo

r at

fair

valu

e.

Un

der

Secti

on

38

56

, P

art

II,

an

invest

men

t in

an

eq

uit

y

secu

rity

th

at

is t

rad

ed

in

an

acti

ve m

ark

et

an

d n

ot

sub

ject

to s

ign

ifican

t in

flu

en

ce is

acco

un

ted

fo

r at

fair

valu

e r

ath

er

than

at

co

st.

Th

e im

pair

men

t p

rovis

ion

s in

Secti

on

30

51,

Part

II,

are

co

nsi

sten

t w

ith

th

ose

in

Secti

on

38

56

, P

art

II.

Sig

nifi

can

t

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

25The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

30

55

, In

tere

sts

in

Join

t V

en

ture

sS

ecti

on

30

55

, In

tere

sts

in J

oin

t V

en

ture

sS

ecti

on

30

55

, P

art

II,

dif

fers

fro

m X

FI S

ecti

on

.

Sig

nifi

can

t d

iffe

ren

ces

are

no

ted

belo

w.

Un

der

Secti

on

30

55

, P

art

II,

an

en

terp

rise

may a

cco

un

t fo

r in

tere

sts

in jo

int

ven

ture

s u

sin

g p

rop

ort

ion

ate

co

nso

lidati

on

, th

e c

ost

meth

od

or

the e

qu

ity m

eth

od

. T

his

is

co

nsi

sten

t w

ith

th

e d

iffe

ren

tial re

po

rtin

g

op

tio

ns

in X

FI S

ecti

on

. H

ow

ever

an

invest

men

t in

a

join

t ven

ture

wh

ose

eq

uit

y s

ecu

riti

es

are

qu

ote

d in

an

acti

ve m

ark

et

is n

ot

acco

un

ted

fo

r at

co

st b

ut

may b

e

acco

un

ted

fo

r at

fair

valu

e.

Th

e im

pair

men

t p

rovis

ion

s in

Secti

on

30

55

, P

art

II,

are

co

nsi

sten

t w

ith

th

ose

in

Secti

on

38

56

, P

art

II.

Sig

nifi

can

t

Secti

on

30

61,

Pro

pert

y

Pla

nt

an

d E

qu

ipm

en

tS

ecti

on

30

61,

Pro

pert

y

Pla

nt

an

d E

qu

ipm

en

tS

ecti

on

30

61,

Part

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

30

63

, Im

pair

men

t o

f Lo

ng

-liv

ed

Ass

ets

Secti

on

30

63

, Im

pair

men

t o

f Lo

ng

-liv

ed

Ass

ets

Secti

on

30

63

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

26 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

30

64

, G

oo

dw

ill a

nd

In

tan

gib

le A

ssets

Secti

on

30

64

, G

oo

dw

ill

an

d In

tan

gib

le A

ssets

Secti

on

30

64

, P

art

II d

iffe

rs f

rom

XF

I S

ecti

on

. S

ign

ifican

t d

iffe

ren

ces

are

no

ted

belo

w.

Inte

rnally

develo

ped

in

tan

gib

le a

ssets

Secti

on

30

64

, P

art

II,

perm

its

an

en

terp

rise

to

make

an

acco

un

tin

g p

olic

y c

ho

ice t

o c

ap

italiz

e o

r exp

en

se

develo

pm

en

t co

sts.

Go

od

will

an

d o

ther

inta

ng

ible

ass

ets

– im

pair

men

t te

stin

gS

ecti

on

30

64

, P

art

II,

req

uir

es

en

terp

rise

s to

test

g

oo

dw

ill a

nd

oth

er

inta

ng

ible

ass

ets

no

t su

bje

ct

to

am

ort

izati

on

on

an

even

ts a

nd

cir

cu

mst

an

ces

basi

s,

rath

er

than

each

year.

Th

is is

co

nsi

sten

t w

ith

th

e d

iffe

ren

tial re

po

rtin

g o

pti

on

in

XF

I S

ecti

on

.

Secti

on

30

64

, P

art

II,

req

uir

es

go

od

will

im

pair

men

t te

stin

g t

o b

e d

on

e a

t th

e r

ep

ort

ing

un

it level,

rem

ovin

g

the r

eq

uir

em

en

t in

XF

I S

ecti

on

to

dete

rmin

e f

air

valu

es

of

ind

ivid

ual ass

ets

an

d lia

bili

ties.

Cert

ain

gu

idan

ce f

rom

EIC

-13

3 h

as

been

in

co

rpo

rate

d

in S

ecti

on

30

64

, P

art

II (s

ee 3

06

4.6

8).

Sig

nifi

can

t

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

27The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

30

65

, Lease

sS

ecti

on

30

65

, Lease

sS

ecti

on

30

65

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

, excep

t th

at

the r

eq

uir

em

en

ts f

or

(a)

rem

ovin

g a

lease

lia

bili

ty f

rom

a less

ee’s

bala

nce s

heet,

an

d (

b)

the

imp

air

men

t te

stin

g o

f le

ase

receiv

ab

les

of

a less

or

in S

ecti

on

30

65

, P

art

II,

are

co

nsi

sten

t w

ith

th

ose

in

S

ecti

on

38

56

, P

art

II.

Cert

ain

gu

idan

ce f

rom

th

e f

ollo

win

g E

IC A

bst

racts

has

been

in

co

rpo

rate

d in

to S

ecti

on

30

65

, P

art

II:

• E

IC-1

9 (

see 3

06

5.0

3(r

);•

EIC

-21

(see 3

06

5.2

7);

• E

IC 2

5 (

see 3

06

5.6

4 a

nd

Illu

stra

tive E

xam

ple

s 3

an

d

4);

• E

IC-5

2 (

see 3

06

5.2

5 a

nd

Illu

stra

tive E

xam

ple

5);

an

d•

EIC

-97 (

see 3

06

5.2

6).

No

t si

gn

ifican

t

Secti

on

311

0, A

sset

Reti

rem

en

t O

blig

ati

on

sS

ecti

on

311

0, A

sset

Reti

rem

en

t O

blig

ati

on

sS

ecti

on

311

0, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

excep

t th

at

the m

easu

rem

en

t re

qu

irem

en

ts h

ave b

een

si

mp

lified

.

Un

der

Secti

on

311

0, P

art

II,

ass

et

reti

rem

en

t o

blig

ati

on

s are

measu

red

at

the b

est

est

imate

of

the e

xp

en

dit

ure

re

qu

ired

to

sett

le t

he p

rese

nt

ob

ligati

on

at

the e

nd

of

the r

ep

ort

ing

peri

od

, ra

ther

than

at

fair

valu

e.

Sig

nifi

can

t

Secti

on

3210

, Lo

ng

-term

D

eb

t—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

Gu

idan

ce p

rovid

ed

in

Secti

on

38

56

, P

art

II.

N/A

28 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

324

0, S

hare

Cap

ital

Secti

on

324

0, S

hare

C

ap

ital

Secti

on

324

0, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

325

0, S

urp

lus

Secti

on

325

1, E

qu

ity

All

req

uir

em

en

ts in

th

is S

ecti

on

rela

te t

o p

rese

nta

tio

n,

wh

ich

is

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

Th

e s

co

pe o

f S

ecti

on

325

1, P

art

II,

is b

road

er

than

XF

I S

ecti

on

325

0.

Cert

ain

gu

idan

ce f

rom

EIC

-13

2 h

as

been

in

co

rpo

rate

d

into

Secti

on

325

1, P

art

II (s

ee 3

25

1.10

).

N/A

Secti

on

326

0, R

ese

rves

Secti

on

326

0, R

ese

rves

Secti

on

326

0, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

328

0, C

on

tractu

al

Ob

ligati

on

sS

ecti

on

328

0,

Co

ntr

actu

al O

blig

ati

on

sA

ll re

qu

irem

en

ts in

th

is S

ecti

on

rela

te t

o d

isclo

sure

s,

wh

ich

are

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

Secti

on

329

0,

Co

nti

ng

en

cie

sS

ecti

on

329

0,

Co

nti

ng

en

cie

sS

ecti

on

329

0, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

34

00

, R

eve

nu

eS

ecti

on

34

00

, R

eve

nu

eS

ecti

on

34

00

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Cert

ain

gu

idan

ce f

rom

th

e f

ollo

win

g E

ICs

has

been

in

co

rpo

rate

d in

to S

ecti

on

34

00

, P

art

II:

• E

IC-7

8 (

see 3

40

0.17);

• E

IC-7

9 (

see 3

40

0.2

2);

• E

IC-1

23

(se

e 3

40

0.2

3-.

24

);•

EIC

-14

1 (s

ee 3

40

0.0

7-.

10);

• E

IC-1

42 (

see 3

40

0.0

11);

• E

IC-1

44

(se

e 3

40

0.2

5-.

27);

an

d•

EIC

-15

6 (

see 3

40

0.2

8).

No

ne

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

29The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

34

61,

Em

plo

yee

Fu

ture

Ben

efi

tsS

ecti

on

34

61,

Em

plo

yee

Fu

ture

Ben

efi

tsS

ecti

on

34

61,

Part

II d

iffe

rs f

rom

XF

I S

ecti

on

.

Secti

on

34

61,

Part

II,

perm

its

defi

ned

ben

efi

t p

lan

s to

b

e r

eco

gn

ized

an

d m

easu

red

usi

ng

eit

her:

• an

“im

med

iate

reco

gn

itio

n a

pp

roach

,” w

here

by

the a

cco

un

tin

g is

base

d o

n a

fu

nd

ing

valu

ati

on

, th

e f

un

ded

sta

tus

of

the p

lan

is

reco

gn

ized

on

th

e b

ala

nce s

heet

an

d t

here

is

no

defe

rral o

r am

ort

izati

on

of

actu

ari

al g

ain

s an

d lo

sses

or

past

se

rvic

e c

ost

s; o

r•

the “

defe

rral an

d a

mo

rtiz

ati

on

ap

pro

ach

” as

in t

he

XF

I S

ecti

on

, w

hic

h r

eq

uir

es

a s

ep

ara

te v

alu

ati

on

fo

r acco

un

tin

g p

urp

ose

s an

d d

efe

rral an

d a

mo

rtiz

ati

on

is

req

uir

ed

fo

r p

ast

serv

ice c

ost

s an

d p

erm

itte

d f

or

actu

ari

al g

ain

s an

d lo

sses.

Th

e d

efi

nit

ion

of

a d

efi

ned

ben

efi

t an

d d

efi

ned

co

ntr

ibu

tio

n p

lan

has

been

mo

difi

ed

. T

he d

iffe

ren

ce

is n

ot

exp

ecte

d t

o b

e s

ign

ifican

t fo

r m

ost

pri

vate

en

terp

rise

s.

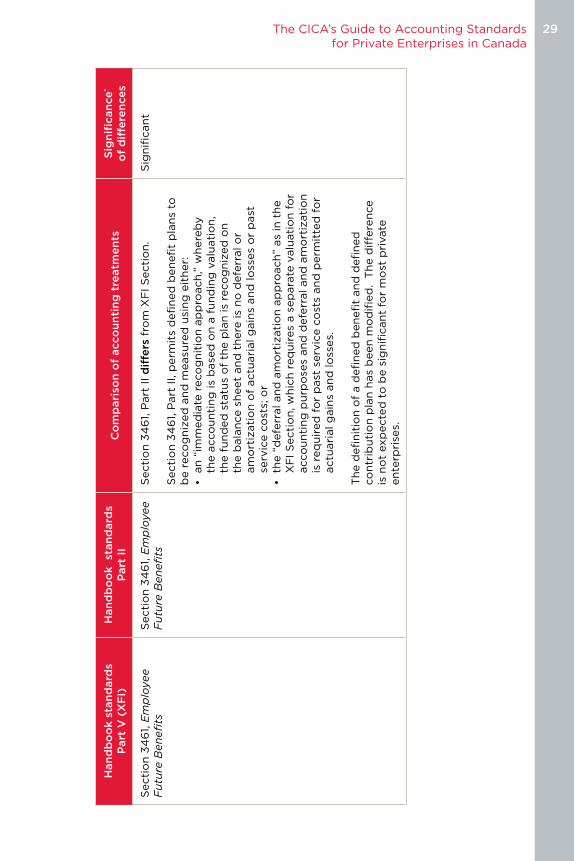

Sig

nifi

can

t

30 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

34

65

, In

com

e T

axe

sS

ecti

on

34

65

, In

com

e

Taxe

sS

ecti

on

34

65

, P

art

II, is

co

nve

rge

d w

ith

XF

I S

ecti

on

. U

nd

er

Se

cti

on

34

65

, P

art

II, e

ith

er

the t

axe

s p

ayab

le

meth

od

or

the f

utu

re in

co

me t

axe

s m

eth

od

may

be c

ho

sen

. T

his

is

co

nsi

ste

nt

wit

h t

he d

iffe

ren

tial

rep

ort

ing

op

tio

n in

XF

I S

ecti

on

.

Ce

rtain

gu

idan

ce f

rom

th

e f

ollo

win

g E

IC A

bst

racts

h

as

be

en

in

co

rpo

rate

d in

to S

ecti

on

34

65

, P

art

II:

• E

IC-1

04

(se

e 3

46

5.7

5);

an

d•

EIC

-14

6 (

see 3

46

5.6

5).

No

ne

Secti

on

34

75

, D

isp

osa

l o

f Lo

ng

-liv

ed

Ass

ets

an

d

Dis

con

tin

ued

Op

era

tio

ns

Secti

on

34

75

, D

isp

osa

l o

f Lo

ng

-liv

ed

Ass

ets

an

d D

isco

nti

nu

ed

O

pera

tio

ns

Secti

on

34

75

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

34

80

, E

xtr

ao

rdin

ary

It

em

s—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

N/A

Secti

on

35

00

, E

arn

ing

s p

er

Sh

are

—N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

N/A

Secti

on

36

10, C

ap

ital

Tran

sacti

on

sS

ecti

on

36

10, C

ap

ital

Tran

sacti

on

sS

ecti

on

36

10, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

38

00

, G

ove

rnm

en

t A

ssis

tan

ceS

ecti

on

38

00

, G

ove

rnm

en

t A

ssis

tan

ceS

ecti

on

38

00

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

31The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

38

05

, In

vest

men

t Ta

x C

red

its

Secti

on

38

05

, In

vest

men

t Ta

x C

red

its

Secti

on

38

05

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

38

20

, S

ub

seq

uen

t E

ven

tsS

ecti

on

38

20

, S

ub

seq

uen

t E

ven

tsS

ecti

on

38

20

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

38

31,

No

n-m

on

eta

ry

Tran

sacti

on

sS

ecti

on

38

31,

No

n-

mo

neta

ry T

ran

sacti

on

sS

ecti

on

38

31,

Part

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.N

on

e

Secti

on

38

40

, R

ela

ted

Part

y

Tran

sacti

on

sS

ecti

on

38

40

, R

ela

ted

P

art

y T

ran

sacti

on

sS

ecti

on

38

40

, P

art

II,

is c

onve

rge

d w

ith

XF

I S

ecti

on

.

Cert

ain

gu

idan

ce f

rom

th

e f

ollo

win

g E

IC A

bst

racts

has

been

in

co

rpo

rate

d in

to S

ecti

on

38

40

, P

art

II:

• E

IC-6

6 (

see 3

84

0.4

4(a

));

• E

IC-7

7 (

see 3

84

0.3

8);

• E

IC 8

9 (

see 3

84

0.4

4(b

)); an

d•

EIC

-10

3 (

see 3

84

0.3

3).

No

ne

Secti

on

38

41,

Eco

no

mic

D

ep

en

den

ceS

ecti

on

38

41,

Eco

no

mic

D

ep

en

den

ceA

ll re

qu

irem

en

ts in

th

is S

ecti

on

rela

te t

o d

isclo

sure

s,

wh

ich

are

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

Secti

on

38

50

, In

tere

st

Cap

italiz

ed

Secti

on

38

50

, In

tere

st

Cap

italiz

ed

All

req

uir

em

en

ts in

th

is S

ecti

on

rela

te t

o d

isclo

sure

s,

wh

ich

are

ou

tsid

e t

he s

co

pe o

f th

is s

um

mary

co

mp

ari

son

.

N/A

32 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

—S

ecti

on

38

56

, F

inan

cia

l In

stru

men

tsS

ecti

on

38

56

, P

art

II, d

iffe

rs f

rom

eq

uiv

ale

nt

req

uir

em

en

ts u

nd

er

XF

I st

an

dard

s.

Th

e r

eq

uir

em

en

ts

in S

ecti

on

38

56

, P

art

II, c

orr

esp

on

d t

o o

r re

pla

ce

gu

idan

ce in

Se

cti

on

s 3

02

0, 3

02

5, 3

210

, 3

86

0, A

cG

-4,

AcG

-12 a

nd

AcG

-13

.

Th

e s

ign

ifican

t d

iffe

ren

ce

s b

etw

ee

n t

he g

uid

an

ce o

n

fin

an

cia

l in

stru

me

nts

in

XF

I st

an

dard

s an

d S

ecti

on

3

85

6, P

art

II, in

clu

de t

he f

ollo

win

g:

• In

ve

stm

en

ts in

eq

uit

ies

that

are

tra

de

d in

an

acti

ve

mark

et

are

me

asu

red

at

fair

valu

e, w

ith

ch

an

ge

s re

co

gn

ize

d in

net

inco

me

. A

n e

nti

ty m

ay a

lso

ir

revo

cab

ly e

lect

on

in

itia

l re

co

gn

itio

n t

o m

easu

re

an

y o

the

r fi

nan

cia

l in

stru

me

nt

at

fair

valu

e.

De

rivati

ve

s, o

the

r th

an

th

ose

in

qu

alify

ing

he

dg

es,

co

nti

nu

e t

o b

e m

easu

red

at

fair

valu

e.

• A

sin

gle

mo

de

l is

ap

plie

d t

o t

he r

eco

gn

itio

n a

nd

m

easu

rem

en

t o

f im

pair

me

nt

for

all

fin

an

cia

l ass

ets

.•

All

fin

an

cia

l in

stru

me

nts

are

re

co

gn

ize

d o

n t

rad

e

date

.•

Tra

nsa

cti

on

co

sts

on

fin

an

cia

l in

stru

me

nts

m

easu

red

at

am

ort

ize

d c

ost

are

cap

italiz

ed

.

Tra

nsa

cti

on

co

sts

on

fin

an

cia

l in

stru

me

nts

m

easu

red

at

fair

valu

e a

re e

xp

en

sed

.•

Th

e e

qu

ity c

om

po

ne

nt

of

co

nve

rtib

le d

eb

t an

d

warr

an

ts o

r o

pti

on

s is

sue

d w

ith

, an

d d

eta

ch

ab

le

fro

m, fi

nan

cia

l liab

ilit

ies

may b

e m

easu

red

at

ze

ro.

Sig

nifi

can

t

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

33The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

• H

ed

ge a

cco

un

tin

g is

availab

le b

y d

esi

gn

ati

on

fo

r re

lati

on

ship

s sp

ecifi

ed

in

th

e S

ecti

on

if

the c

riti

cal

term

s o

f th

e h

ed

gin

g in

stru

me

nt

matc

h t

ho

se o

f th

e

he

dg

ed

in

stru

me

nt.

• P

refe

rre

d s

hare

s is

sue

d in

a s

pe

cifi

ed

tax p

lan

nin

g

arr

an

ge

me

nt

mu

st b

e c

lass

ifie

d a

s e

qu

ity. (T

his

is

co

nsi

ste

nt

wit

h t

he d

iffe

ren

tial re

po

rtin

g o

pti

on

in

X

FI S

ecti

on

38

60

.)

Ce

rtain

gu

idan

ce f

rom

th

e f

ollo

win

g S

ecti

on

s,

Acco

un

tin

g G

uid

elin

es

an

d E

IC A

bst

racts

an

d h

as

be

en

in

clu

de

d in

Se

cti

on

38

56

, P

art

II:

• S

ecti

on

30

20

(se

e 3

85

6.1

6-.

19);

• S

ecti

on

30

25

(se

e 3

85

6.1

6-.

19);

• A

cG

-4 (

see 3

85

6.0

7);

• A

cG

-12 (

see 3

85

6, A

pp

en

dix

B.)

;•

AcG

-13

(se

e 3

85

6.3

0-.

36

);•

EIC

-88

, 9

6 a

nd

10

1 (s

ee 3

85

6.2

6-.

29

);•

EIC

-14

9 (

see 3

85

6.2

0-.

23

); a

nd

• E

IC-1

58

(se

e 3

85

6.1

4).

Secti

on

38

60

, F

inan

cia

l In

stru

men

ts –

Dis

clo

sure

an

d P

rese

nta

tio

n

—N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

Gu

idan

ce

pro

vid

ed

in

Secti

on

38

56

, P

art

II.

N/A

34 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

Secti

on

38

70

, S

tock-

base

d

Co

mp

en

sati

on

an

d O

ther

Sto

ck-

base

d P

aym

en

ts

Secti

on

38

70

, S

tock-

base

d C

om

pen

sati

on

an

d O

ther

Sto

ck-

base

d

Pay

men

ts

Secti

on

38

70

, P

art

II,

dif

fers

fro

m X

FI S

ecti

on

.

Secti

on

38

70

, P

art

II,

rep

laces

the m

inim

um

valu

e

meth

od

(i.e

., th

e a

bili

ty t

o ig

no

re v

ola

tilit

y in

m

easu

rin

g s

tock-b

ase

d c

om

pen

sati

on

) w

ith

th

e

calc

ula

ted

valu

e m

eth

od

. U

nd

er

the c

alc

ula

ted

valu

e

meth

od

an

en

terp

rise

est

imate

s th

e v

ola

tilit

y t

hat

is

use

d a

s an

in

pu

t to

a s

tock o

pti

on

pri

cin

g m

od

el b

ase

d

on

an

ap

pro

pri

ate

secto

r in

dex.

Sig

nifi

can

t

Secti

on

410

0, P

en

sio

n P

lan

s—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

Th

e a

cco

un

tin

g

stan

dard

s fo

r p

en

sio

n p

lan

s can

be f

ou

nd

in

Part

IV

.N

/A

Secti

on

4211

, L

ife In

sura

nce

E

nte

rpri

ses

– S

pecifi

c Ite

ms

—N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

N/A

Secti

on

425

0, F

utu

re-

ori

en

ted

Fin

an

cia

l In

form

ati

on

—N

o c

orr

esp

on

din

g s

tan

dard

in

Part

II.

N/A

Secti

on

44

00

, N

ot-

for-

pro

fit

Org

an

izati

on

s—

No

co

rre

spo

nd

ing

sta

nd

ard

in

Part

II.

Part

III h

as

been

re

serv

ed

fo

r th

e a

cco

un

tin

g s

tan

dard

s fo

r n

ot-

for-

pro

fit

org

an

izati

on

s.

N/A

AcG

-2, F

ran

ch

ise F

ee

Reve

nu

eA

cG

-2, F

ran

ch

ise F

ee

Reve

nu

eA

cG

-2, P

art

II,

is c

onve

rge

d w

ith

XF

I G

uid

elin

e.

No

ne

AcG

-3, F

inan

cia

l R

ep

ort

ing

b

y P

rop

ert

y a

nd

Casu

alt

y

Insu

ran

ce C

om

pan

ies

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II.

N/A

The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

35The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

AcG

-4, F

ees

an

d C

ost

s A

sso

cia

ted

wit

h L

en

din

g

Acti

vit

ies

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II.

Gu

idan

ce p

rovid

ed

in

Secti

on

38

56

, P

art

II (s

ee

38

56

.07).

N/A

AcG

-7, T

he M

an

ag

em

en

t R

ep

ort

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II.

N/A

AcG

-8, A

ctu

ari

al L

iab

iliti

es

of

Lif

e In

sura

nce

En

terp

rise

s –

Dis

clo

sure

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II.

N/A

AcG

-9, F

inan

cia

l R

ep

ort

ing

b

y L

ife In

sura

nce

E

nte

rpri

ses

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II

N/A

AcG

-11,

En

terp

rise

s in

th

e

Deve

lop

men

t S

tag

e—

No

co

rre

spo

nd

ing

Gu

ide

lin

e in

Part

II.

N/A

AcG

-12, Tr

an

sfers

of

Rece

ivab

les

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II.

Gu

idan

ce

pro

vid

ed

in

Secti

on

38

56

, P

art

II (s

ee 3

85

6,

Ap

pen

dix

B).

N/A

AcG

-13

, Hed

gin

g

Rela

tio

nsh

ips

—N

o c

orr

esp

on

din

g G

uid

elin

e in

Part

II.

Gu

idan

ce

pro

vid

ed

in

Secti

on

38

56

, P

art

II (s

ee 3

85

6.3

0-.

36

).

AcG

-14

, D

isclo

sure

of

Gu

ara

nte

es

AcG

-14

, D

isclo

sure

of

Gu

ara

nte

es

AcG

-14

, P

art

II,

is c

onve

rge

d w

ith

XF

I G

uid

elin

e.

No

ne

36 The CICA’s Guide to Accounting Standards for Private Enterprises in Canada

Han

db

oo

k s

tan

dard

sP

art

V (

XF

I)H

an

db

oo

k

stan

dard

sP

art

II

Co

mp

ari

son

of

acco

un

tin

g t

reatm

en

tsS

ign

ifican

ce

* o

f d

iffe

ren

ce

s

AcG

-15

, C

on

solid

ati

on

of

Vari

ab

le In

tere

st E

nti

ties

AcG

-15

, C

on

solid

ati

on

o

f V

ari

ab

le In

tere

st

En

titi

es

AcG

-15

, P

art

II,

is c

onve

rge

d w

ith

XF

I G

uid

elin

e. A

cG

-15

, P

art

II,

do

es

no

t ap

ply

to

an

en

terp

rise

th

at

ch

oo

ses

to p

rep

are

no

n-c

on

solid

ate

d fi

nan

cia

l st

ate

men

ts.

No

ne

AcG

-16

, O

il an

d G

as

Acc

ou

nti

ng

– F

ull

Co

stA

cG

-16

, O

il an

d G

as

Acc

ou

nti

ng

– F

ull

Co

stA

cG

-16

, P

art

II,

is c

onve

rge

d w

ith

XF

I G

uid

elin

e.