Tax Aspects of Selling Your Business

Bradley S. Dimond, CPAHenry & Horne, LLP

February 3, 2011

Overview Assumptions

Tax Aspects

Legal Structure of Business

• Sole Proprietor (or SMLLC)

• LLC (Multi Member)

• S Corporation

• C Corporation

Tax Result from Sale – Why it Matters

• Sale of Assets or Equity

• LTCG v. Ordinary Income

• Section 1231- Gain almost but not quite = LTCG

• Ordinary Income Recapture

• Purchase Price Allocation

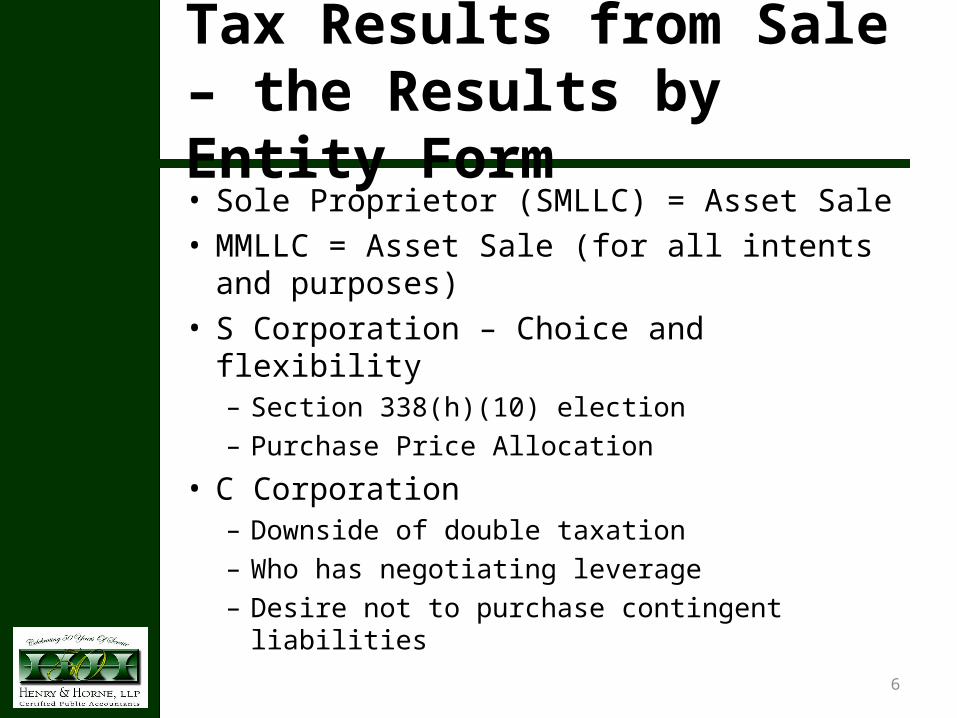

Tax Results from Sale – the Results by Entity Form• Sole Proprietor (SMLLC) = Asset Sale• MMLLC = Asset Sale (for all intents and

purposes)• S Corporation – Choice and flexibility

– Section 338(h)(10) election– Purchase Price Allocation

• C Corporation– Downside of double taxation– Who has negotiating leverage– Desire not to purchase contingent liabilities

6

Other Considerations

• Non-compete Agreement?• Personal Goodwill• Installment Sale

– Recapture issue– $5 million rule

• Charitable or Estate Planning– CRT? – converting LTCG to Ordinary Income– Income of gain shifting – Current gifts of

equity– GRATs– Other

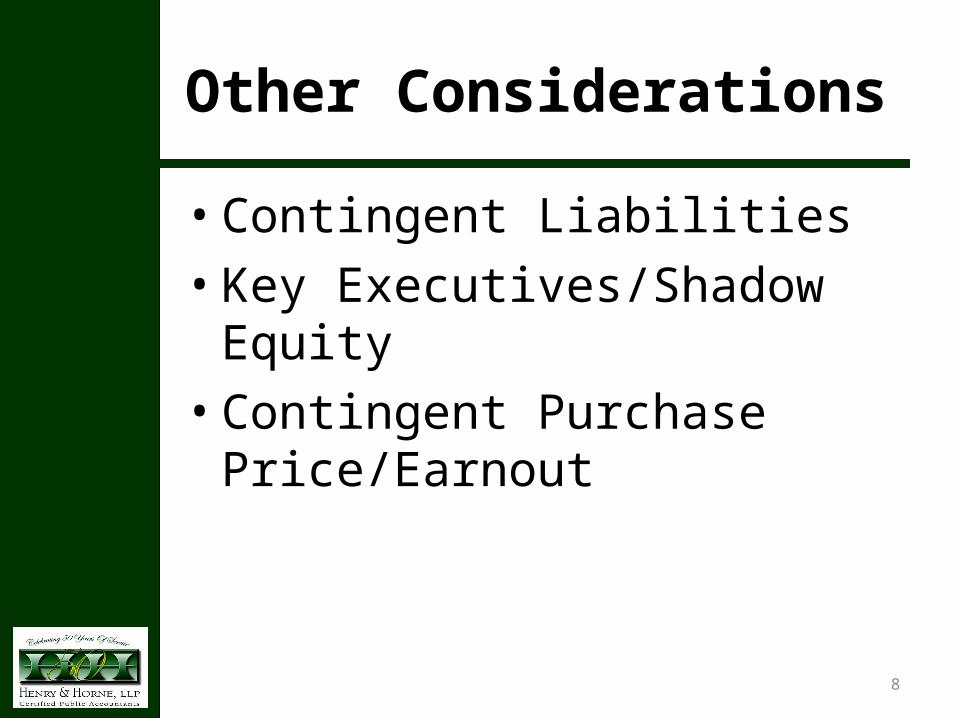

Other Considerations

• Contingent Liabilities

• Key Executives/Shadow Equity

• Contingent Purchase Price/Earnout

8

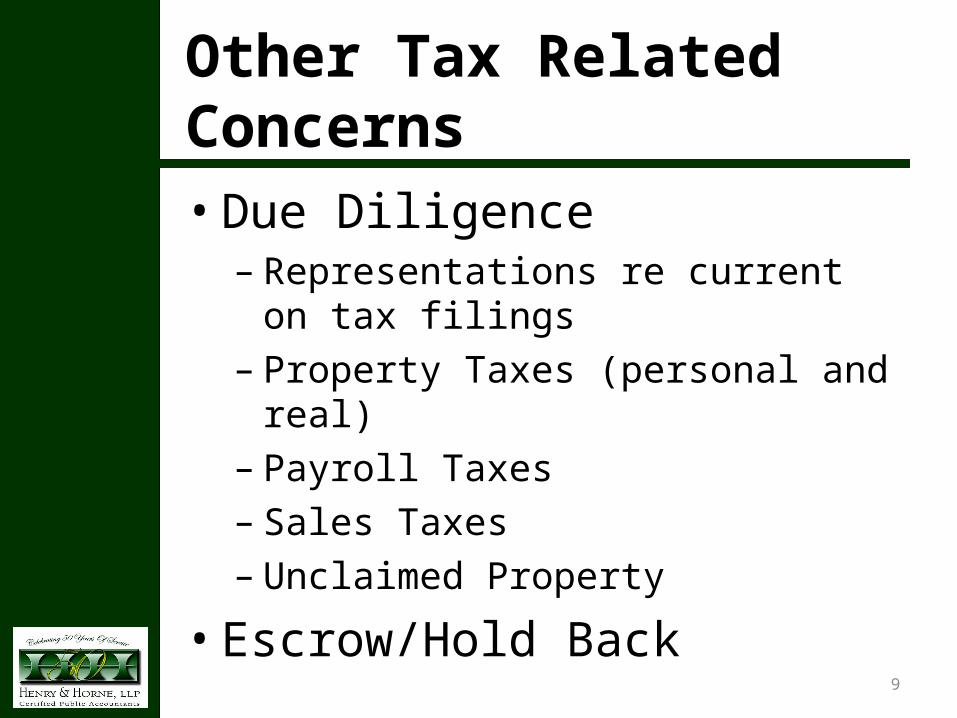

Other Tax Related Concerns• Due Diligence

– Representations re current on tax filings

– Property Taxes (personal and real)– Payroll Taxes– Sales Taxes– Unclaimed Property

• Escrow/Hold Back

9

Summary

10

Thank You!