Tax Planning for Federal EmployeesA NARFE Federal Benefits Institute Webinar

Presented by Mark Keen, CFP®Federal Benefits Expert

Closed Captioning (CC) is available on the recorded version of this webinar.

1

Agenda

Income Tax Basics

Traditional vs. Roth

Tax-Smart TSP Contributions

Make the Most of Tax-Advantaged Plans

Other Tax Savings Options

Resources

2

Income Tax Basics

3

Income Tax Basics

U.S. Tax System

• Progressive tax system

▪ Tax rate increases as taxable income increases

• Seven tax brackets

▪ Ranging from 10-37 percent

• Not all income is taxed equally

▪ Ordinary income

▪ Investment income

4

Income Tax Basics

Marginal Tax Rates

5

2021 Income Tax Brackets

MarginalTax Rate Single

MarriedFiling Jointly

10% $0 to $9,950 $0 to $19,900

12% $9,951 to $40,525 $19,901 to $81,050

22% $40,526 to $86,375 $81,051 to $172,750

24% $86,376 to $164,925 $172,751 to $329,850

32% $164,926 to $209,425 $329,851 to $418,850

35% $209,426 to $523,600 $418,851 to $628,300

37% $523,601 or more $628,301 or more

Income Tax Basics

Important Tax Rates to Know

• Marginal rate

▪ Rate paid on an additional dollar of income

• Effective rate

▪ Actual percentage of taxes you pay on all your taxable income

• Effective marginal rate

▪ True tax rate paid on next dollar of income

6

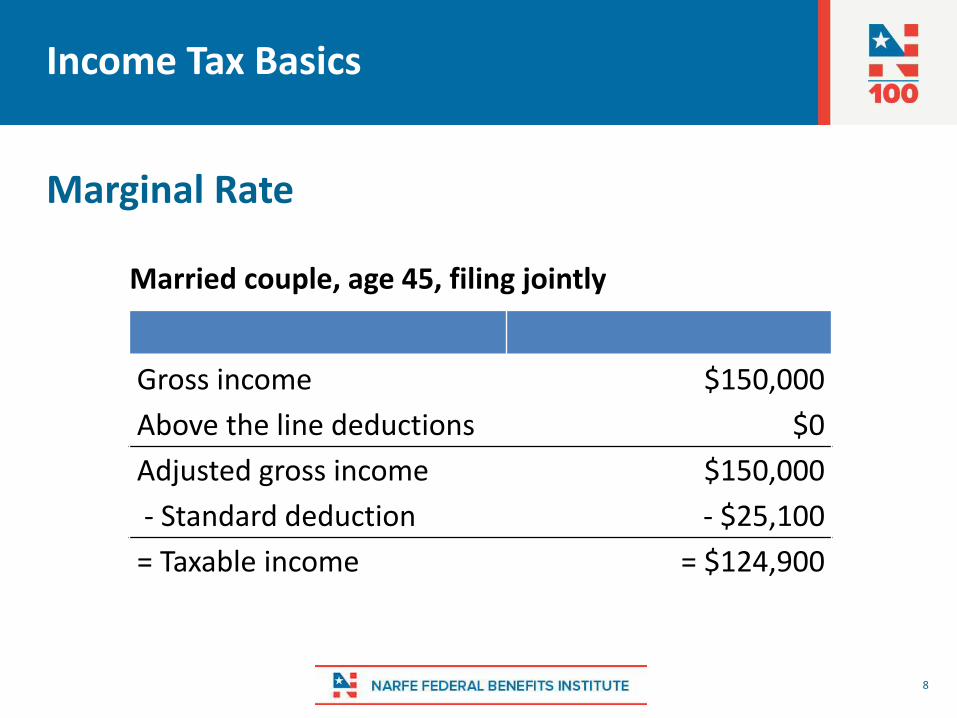

Income Tax Basics

Marginal Rate

• Based on taxable ordinary income

7

Gross income

- above-the-line deductions

= Adjusted gross income (AGI)

- below-the-line deductions

= Taxable income

Income Tax Basics

Marginal Rate

8

Gross income $150,000

Above the line deductions $0

Adjusted gross income $150,000

- Standard deduction - $25,100

= Taxable income = $124,900

Married couple, age 45, filing jointly

Income Tax Basics

Marginal Rate vs. Effective Rate

9

2021 Income Tax Brackets

MarginalTax Rate

MarriedFiling Jointly

10% $0 to $19,900 12% $19,901 to $81,05022% $81,051 to $172,75024% $172,751 to $329,85032% $329,851 to $418,85035% $418,851 to $628,30037% $628,301 or more

Tax Calculation

$124kIncome Tax Rate Tax

$19,900 10% $1,990$61,150 12% $7,338$43,850 22% $9,647

$18,975

Income Tax Basics

Marginal Rate vs. Effective Rate

10

Federal tax liability $18,975

Marginal rate 22%

Effective rate 15.2%

Married couple, age 45, filing jointly

Gross income $150,000

Above-the-line deductions $0

Adjusted gross income $150,000

- Standard deduction - $25,100

= Taxable income = $124,900

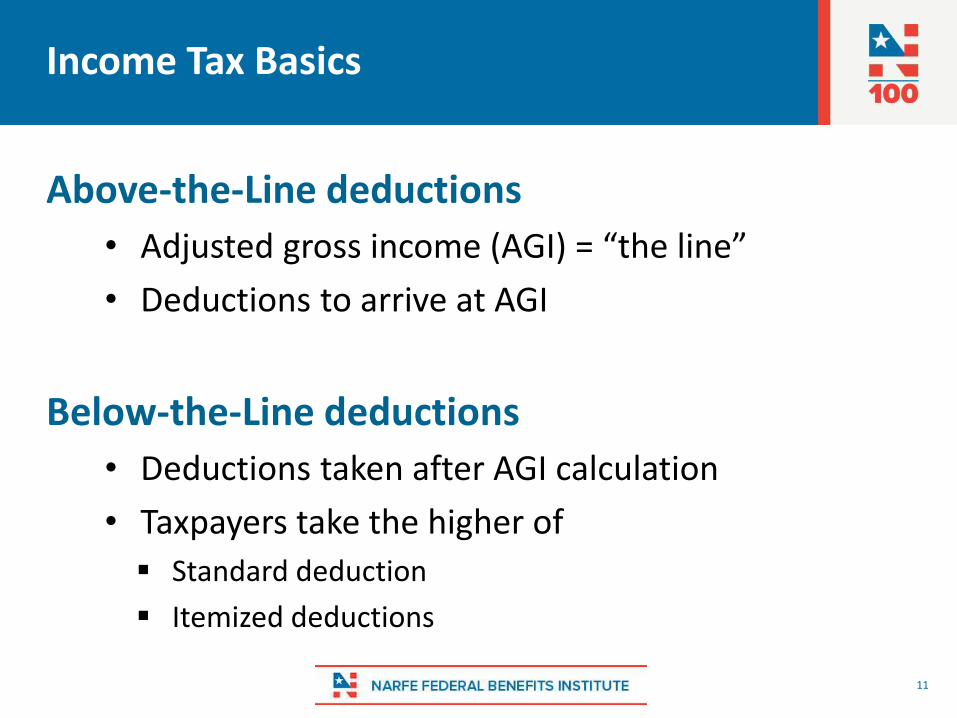

Above-the-Line deductions

• Adjusted gross income (AGI) = “the line”

• Deductions to arrive at AGI

Below-the-Line deductions

• Deductions taken after AGI calculation

• Taxpayers take the higher of

▪ Standard deduction

▪ Itemized deductions

11

Income Tax Basics

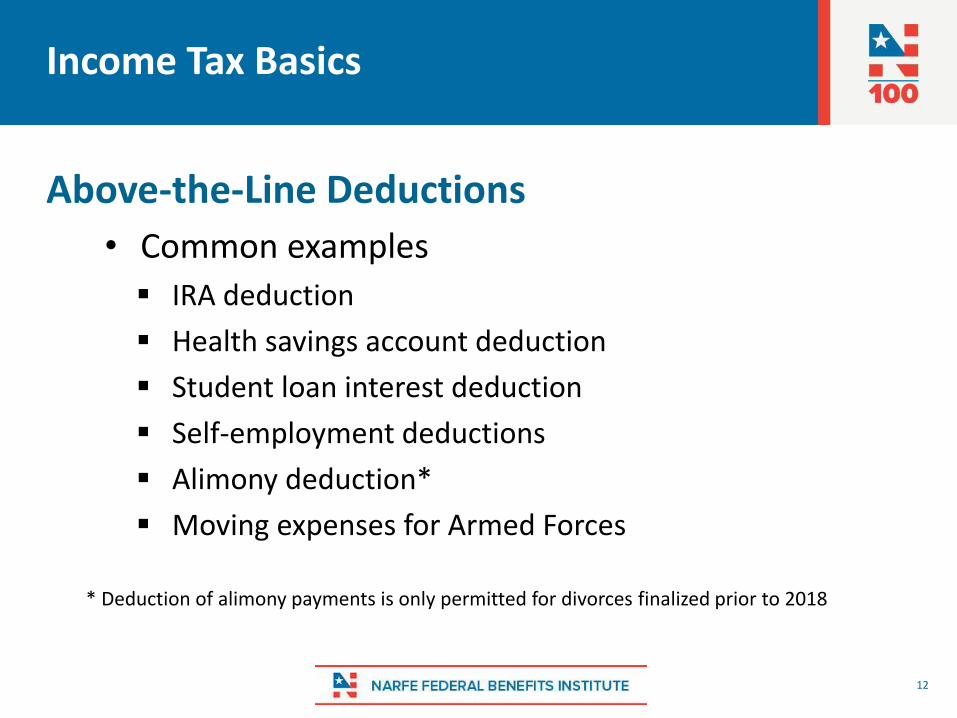

Above-the-Line Deductions

• Common examples

▪ IRA deduction

▪ Health savings account deduction

▪ Student loan interest deduction

▪ Self-employment deductions

▪ Alimony deduction*

▪ Moving expenses for Armed Forces

12

* Deduction of alimony payments is only permitted for divorces finalized prior to 2018

Income Tax Basics

Below-the-Line Deductions

Standard deduction

13

Itemized deductions• Common deductions

▪ Medical expenses

▪ State and local taxes

▪ Property taxes

▪ Mortgage interest

▪ Charitable contributions

Filing Status 2021 Tax Year

Single or married filing separately

$12,550

Married filing jointly or qualifying widower

$25,100

Head of household $18,800

Add’l for >65 or BlindSingle = $1,700MFJ = $1,350

Income Tax Basics

Income Tax Basics

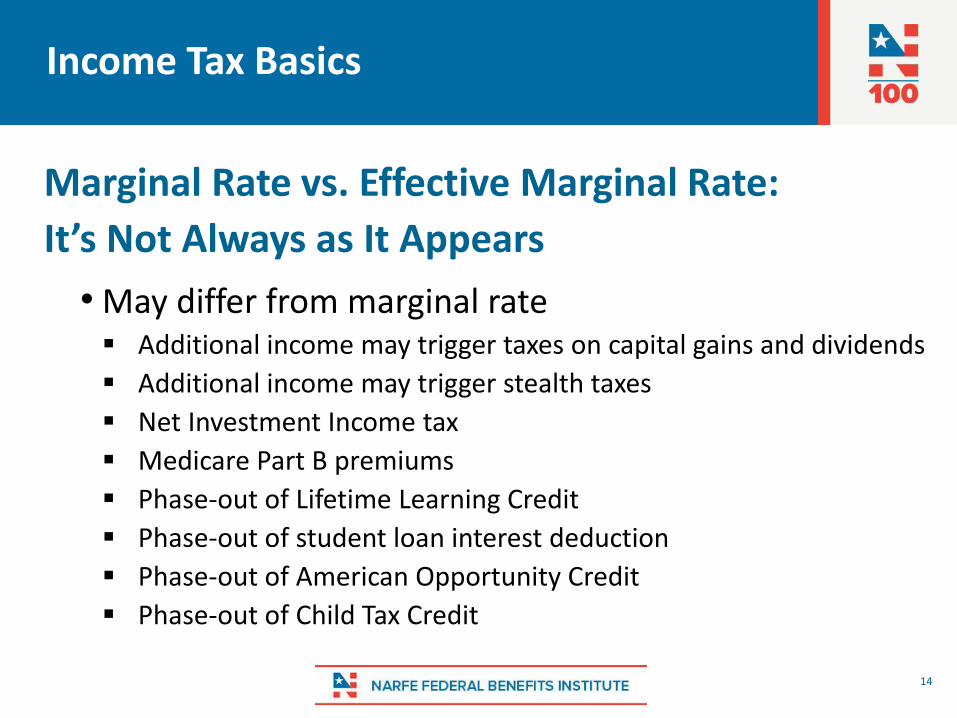

Marginal Rate vs. Effective Marginal Rate:

It’s Not Always as It Appears

• May differ from marginal rate▪ Additional income may trigger taxes on capital gains and dividends

▪ Additional income may trigger stealth taxes

▪ Net Investment Income tax

▪ Medicare Part B premiums

▪ Phase-out of Lifetime Learning Credit

▪ Phase-out of student loan interest deduction

▪ Phase-out of American Opportunity Credit

▪ Phase-out of Child Tax Credit

14

Income Tax Basics

Not All Income Is Treated Equally

• Interest income

▪ Ordinary income

• Dividends

▪ Nonqualified – ordinary income

▪ Qualified – 0, 15 or 20 percent

• Capital gains

▪ Short-term – ordinary income

▪ Long-term – 0, 15 or 20 percent

15

Traditional Versus Roth

16

Traditional Versus Roth

17

Traditional TSP Roth TSP

Maximum Contribution limit(2021)

$19,500 (under age 50)$26,000 (above 50)Reduced by Roth TSP Contribution

$19,500 (under age 50)$26,000 (above 50)Reduced by Traditional TSP Contribution

Contribution Income Limit None None

Federal Tax treatment of contributions1

• Made with pre-tax dollars• Taxable upon distribution

• Made with after-tax dollars• Never taxable upon distribution

Federal Tax treatment of earnings1 Taxable upon distribution Tax-free with qualified withdrawal2

Required minimum distributions Yes – typically required beginning at age 72

Yes3 – typically required beginning at age 72

1 Rules vary by state2 Roth account has been open for at least 5 years and distribution occurred after age 59 ½3 While the Roth TSP is subject to required minimum distributions, Roth IRAs are not

$10,000

$2,200Tax liability (22%)

After-tax balance $7,800

$0

$7,800

$20,000

$4,400

$15,600

$0

$15,600=

$15,600

Contribution

Tax liability (22%)

After-tax balance

Balance after 10 years

Traditional TSP Roth TSP

Return = 7.2%

All things equal. No economic difference!

$7,800

18

Traditional Versus Roth

Traditional vs. Roth TSP: Constant Tax Rates

$15,000$15,600

$4,400$5,000

$20,000

Tax Liability (22%)Tax liability (25%)

$10,000

$25,000Tax liability (22%)

$75,000

$0

$15,600=

$15,600

Contribution

After-tax balance

Balance after 10 years

Traditional TSP Roth TSP

Return = 7.2%

<

19

Increasing tax rates = Roth is more valuable!

Traditional Versus Roth

Traditional vs. Roth TSP: Increasing Tax Rates

$7,800

$15,600$17,600

$4,400$2,400

$20,000

Tax Liability (22%)Tax liability (12%)

$10,000

$25,000Tax liability (22%)

$75,000

$0

$15,600=

$15,600

Contribution

After-tax balance

Balance after 10 years

Traditional TSP Roth TSP

Return = 7.2%

>

20Decreasing tax rates = Traditional is more valuable!

Traditional Versus Roth

Traditional vs. Roth TSP: Decreasing Tax Rates

$7,800

Not a One-Time DecisionThings to take into consideration

• Income-related deductions and credits

• Required minimum distributions (RMDs)

• Medicare income-related monthly adjusted amount (IRMAA)

• Tax Cuts and Jobs Act

• Future state of domicile

• Change in tax filing status

• Estate planning objectives

• Large distribution

21

Traditional Versus Roth

Don’t Underestimate the Impact of RMDs• Janice, 45 years old

• $150,000 salary*

• $350,000 TSP

• Contributes maximum each year ($19,500 & $26,000 at age 50)*

• 5 percent agency contributions*

• Retiring at 65

• No distributions before age 72

• 6 percent hypothetical annual return

22

$0.00

$1,000,000.00

$2,000,000.00

$3,000,000.00

$4,000,000.00

$5,000,000.00

6566676869707172737475767778798081828384858687888990919293

Projected TSP Balance

$0.00

$50,000.00

$100,000.00

$150,000.00

$200,000.00

$250,000.00

$300,000.00

$350,000.00

$400,000.00

6566676869707172737475767778798081828384858687888990919293

Projected RMDs

* Salary, employee contributions and agency contributions all increased by 2% annually. The above example is for illustrative purposes only and not indicative of any investment. Values are based on a hypothetical 6% return. References to future returns are not promises or even estimates of actual returns an investor may achieve.

Traditional Versus Roth

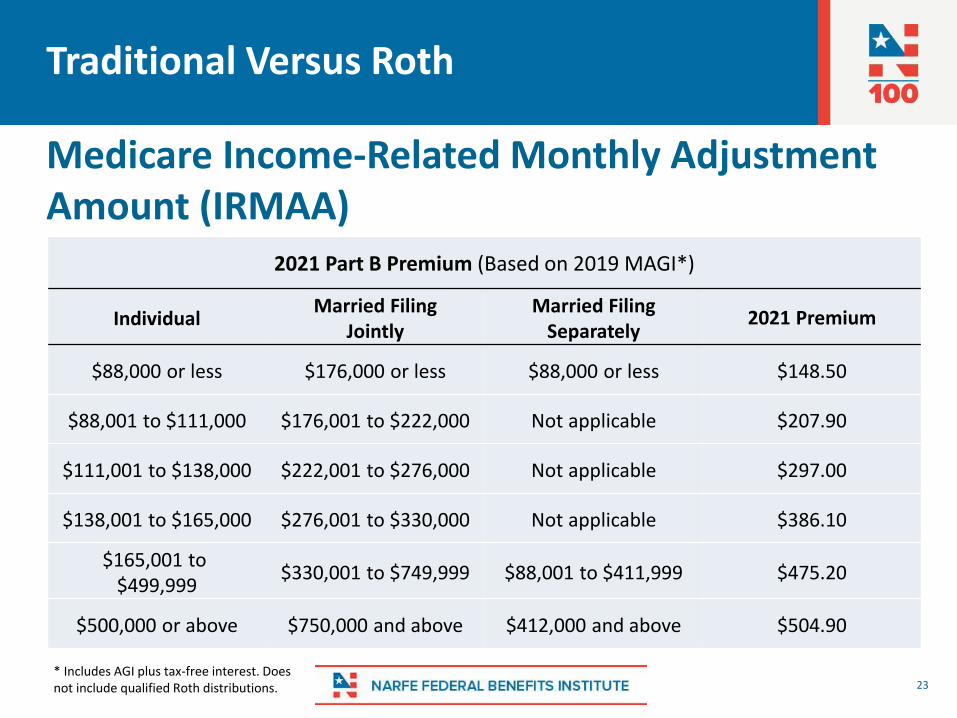

Medicare Income-Related Monthly Adjustment Amount (IRMAA)

2021 Part B Premium (Based on 2019 MAGI*)

IndividualMarried Filing

JointlyMarried Filing

Separately2021 Premium

$88,000 or less $176,000 or less $88,000 or less $148.50

$88,001 to $111,000 $176,001 to $222,000 Not applicable $207.90

$111,001 to $138,000 $222,001 to $276,000 Not applicable $297.00

$138,001 to $165,000 $276,001 to $330,000 Not applicable $386.10

$165,001 to$499,999

$330,001 to $749,999 $88,001 to $411,999 $475.20

$500,000 or above $750,000 and above $412,000 and above $504.90

* Includes AGI plus tax-free interest. Does not include qualified Roth distributions.

Traditional Versus Roth

23

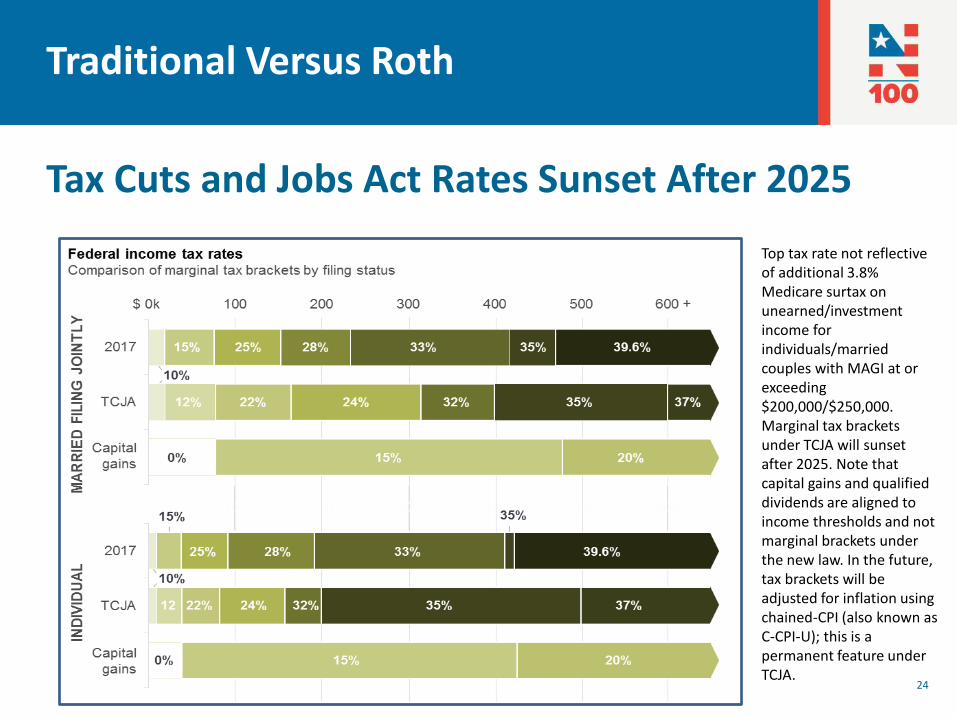

Tax Cuts and Jobs Act Rates Sunset After 2025

Top tax rate not reflective of additional 3.8% Medicare surtax on unearned/investment income for individuals/married couples with MAGI at or exceeding $200,000/$250,000. Marginal tax brackets under TCJA will sunset after 2025. Note that capital gains and qualified dividends are aligned to income thresholds and not marginal brackets under the new law. In the future, tax brackets will be adjusted for inflation using chained-CPI (also known as C-CPI-U); this is a permanent feature under TCJA.

Traditional Versus Roth

24

Tax-Smart TSP Contributions

25

Tax-Smart TSP Contributions

26* $13,850 contributed to Traditional TSP & $12,150 contributed to Roth TSP** $81,050 is the top of the 12% tax bracket. The next dollar of ordinary income will be taxed at the 22% marginal rate.

Wages- Traditional TSP ContributionAdjusted Gross Income

- Standard Deduction= Taxable Income

Federal Tax LiabilityMarginal Rate

Income Taxed at 22%Income Taxed at 12%Income Taxed at 10%

$26,000

Traditional

Contribution $ 120,000 $ 26,000 $ 94,000 $ 25,100 $ 68,900

$ 7,870 12%

$ -$ 49,000$ 19,900

$26,000

Roth

Contribution $ 120,000 $ -$ 120,000 $ 25,100 $ 94,900

$ 12,375 22%

$ 13,850 $ 61,150$ 19,900

Split

Trad. & Roth

Contribution $ 120,000 $ 13,850* $ 106,150 $ 25,100 $ 81,050

$ 9,328 12%**

$ -$ 61,150$ 19,900

Difference $ -$ (12,150*)$ 7,950 $ -$ 12,150 $ -$ 1,458

$ -$ 12,150 $ -

Traditional TSP vs Roth TSP: Not a Choice of One or the Other

Make the Most of Tax-Advantaged Plans

27

Make the Most of Tax-Advantaged Plans

The TSP Isn’t the Only Tax-Advantaged Plan

Other tax-advantaged plans include

• Individual Retirement Arrangements (IRAs)

▪ Traditional IRA

▪ Roth IRA

• Health Savings Accounts

▪ Requires high-deductible health plan

28

29

1. Must have a qualifying high-deductible health plan to make contributions. Funds in the HSA may be withdrawn tax free for qualified expenses unless a credit or deduction for medical expenses is clamed. After age 65 funds also may be withdrawn for any reason and taxed as ordinary income without penalty. Some health insurance premiums may be qualified expenses such as COBRA coverage, coverage while receiving state or federal unemployment compensation, Medicare Part B and D premiums and qualified long-term care (LTC) insurance premiums up to certain limits but excludes Medicap/Medicare supplement policies and most hybrid products that combine LTC with annuities and the life insurance. See IRS Publications 969 and 502. This is not intended to be individual tax advice, consult your tax professional.The above example is for illustrative purposes only and not indicative of any investment. Does not include account fees. Present value of illustrated HSA after 15 years is $170,452. Estimated savings from tax deductions at a 37% marginal rate are $55,016. Assumes cash or income used for health care expenses is not withdrawn from an account with a tax liability. The example assumes the HSA is fully invested, if $2,000 was held in a cash account, the illustrated cumulative HAS account value would be $224,780. 2021 family contribution limit is $7,200 adjusted for inflation of 2.0% for 30 years with catch-up contributions of $1,000 per person (adjusted for inflation) starting at age 55 in 2026. Individual 2021 contribution limit is $3,600. $229,406 is enough to fund about 13 years of projected average qualified Medicare-related health care expenses for a couple.

2021 Contribution LimitsIndividual: $3,600 Family: $7,200

Make the Most of Tax-Advantaged Plans

Make the Most of Tax-Advantaged Plans

30

Thrift Savings Plan Traditional IRA Roth IRA

Contribution limit $19,500 (under age 50)$26,000 (above 50)

$6,000 (under age 50)1

$7,000 (above 50) 1

Reduced by Roth IRA Contribution

$6,000 (under age 50) 1

$7,000 (above 50) 1

Reduced by Traditional IRA Contribution

Contribution income limit

No No income limits to contribute

• Single: $124k - $139k• MFJ: $198k - $208k

Tax deductibility income limit

Traditional: NoRoth: Contributions not deductible

MFJ:Covered spouse: $105k -$125k2

Non-covered spouse: $198k - $208k2

Single:Covered: $65k - $75k2

Contributions not deductible

Required minimum distributions

Yes – both Traditional and Roth TSP subject to RMDs

Yes No

1 Must have earned income to contribute to IRAs2 Covered refers to a participant in an employer’s retirement plan. If single and not covered or married and neither spouse is a participant in an employer’s retirement plan, a traditional IRA contribution is deductible regardless of income.

Other Tax Saving Concepts

31

Other Tax Saving Options

Backdoor Roth IRA Strategy

• When income is too high to contribute to a Roth IRA

▪ Step 1. Nondeductible contribution to traditional IRA

▪ Step 2. Convert nondeductible contribution to Roth IRA• Tax-free conversion*

• Be aware of pro-rata rule

• Isolate basis if IRA contains pretax funds

32

* Conversion is nontaxable if the amount converted consists entirely of nondeductible contributions. Any pre-tax money converted will be subject to tax.

Other Tax Saving Options

Isolate IRA Basis for Tax-Free Conversion• What is basis?

▪ Established in a Traditional IRA with after-tax contributions

▪ After-tax contributions are not the same as Roth contributions

▪ TSP does not permit after-tax contributions

• Why not leave basis in Traditional IRA?▪ Earnings on after-tax contributions will be taxed upon

distribution▪ Converting to Roth IRA offers opportunity for tax-free

earnings

33

Isolate IRA Basis for Tax-Free Conversion

• IRS Pro-Rata Rule

▪ Prevents IRA owners from distributing or converting only their basis when pretax money exists

▪ Must determine how much basis represents as percentage of IRAs• Must aggregate value of all IRAs (Traditional IRAs, SEP IRAs,

SIMPLE IRAs)

• Employer plans are not included in the pro-rata calculation

▪ Distributions and/or conversions will consist proportionately of basis and pretax money

34

Other Tax Saving Options

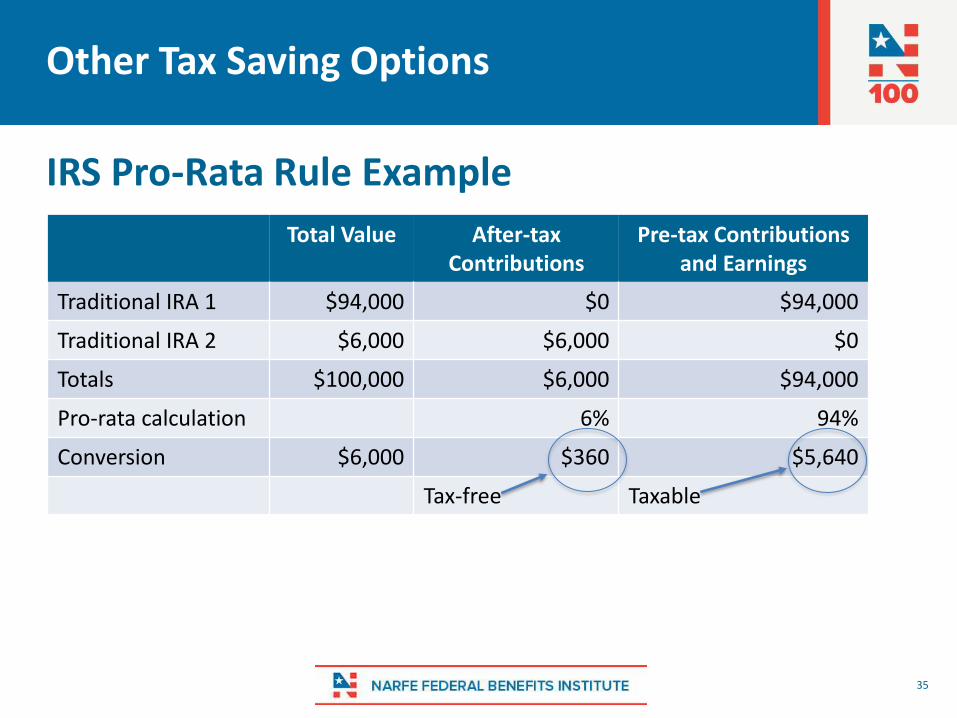

IRS Pro-Rata Rule Example

35

Other Tax Saving Options

Total Value After-tax Contributions

Pre-tax Contributions and Earnings

Traditional IRA 1 $94,000 $0 $94,000

Traditional IRA 2 $6,000 $6,000 $0

Totals $100,000 $6,000 $94,000

Pro-rata calculation 6% 94%

Conversion $6,000 $360 $5,640

Tax-free Taxable

Other Tax Saving Options

Isolate IRA Basis for Tax-Free Conversion

• IRS Pro-Rata Rule

▪ Applies to all distributions and conversions, exceptrollovers to employer-based retirement plans

• Strategy

▪ Isolate your IRA basis by transferring all pretax money from IRA to TSP

▪ Then free to convert IRA basis tax-free to Roth IRA

36

Example: Transfer $94,000 in Pretax Money to TSP

37

Other Tax Saving Options

Total Value After-tax Contributions

Pre-tax Contributions and Earnings

Traditional IRA 1 $0 $0 $0

Traditional IRA 2 $6,000 $6,000 $0

Totals $100,000 $6,000 $0

Pro-rata calculation 100% 0%

Conversion $6,000 $6,000 $0

Tax-free Taxable

Other Tax Saving Options

38

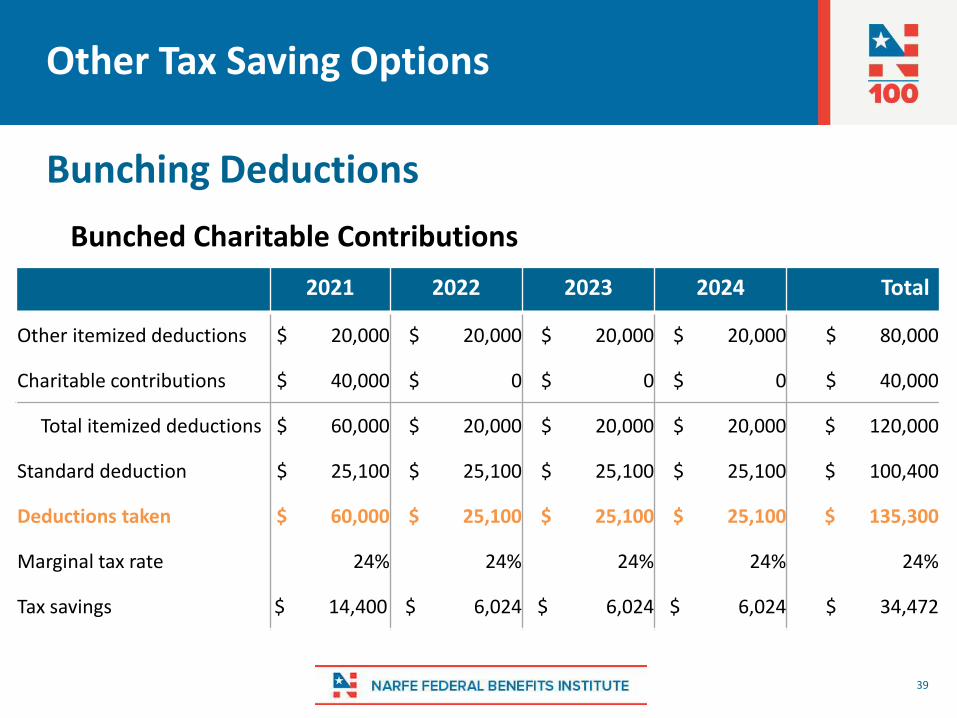

Consistent Charitable Contributions

Bunching Deductions

2021 2022 2023 2024 Total

Other itemized deductions $ 20,000 $ 20,000 $ 20,000 $ 20,000 $ 80,000

Charitable contributions $ 10,000 $ 10,000 $ 10,000 $ 10,000 $ 40,000

Total itemized deductions $ 30,000 $ 30,000 $ 30,000 $ 30,000 $ 120,000

Standard deduction $ 25,100 $ 25,100 $ 25,100 $ 25,100 $ 100,400

Deductions taken $ 30,000 $ 30,000 $ 30,000 $ 30,000 $ 120,000

Marginal tax rate 24% 24% 24% 24% 24%

Tax savings $ 7,200 $ 7,200 $ 7,200 $ 7,200 $ 28,800

Other Tax Saving Options

39

Bunched Charitable Contributions

Bunching Deductions

2021 2022 2023 2024 Total

Other itemized deductions $ 20,000 $ 20,000 $ 20,000 $ 20,000 $ 80,000

Charitable contributions $ 40,000 $ 0 $ 0 $ 0 $ 40,000

Total itemized deductions $ 60,000 $ 20,000 $ 20,000 $ 20,000 $ 120,000

Standard deduction $ 25,100 $ 25,100 $ 25,100 $ 25,100 $ 100,400

Deductions taken $ 60,000 $ 25,100 $ 25,100 $ 25,100 $ 135,300

Marginal tax rate 24% 24% 24% 24% 24%

Tax savings $ 14,400 $ 6,024 $ 6,024 $ 6,024 $ 34,472

Resources

40

Resources

IRS Publication 590 A - Contributions to Individual Retirement Arrangements (IRAs)

IRS Publication 590 B - Distributions From Individual Retirement Arrangements (IRAs)

Managing Money NARFE Magazine articles• Five-Year Rule for Tax-Free Roth Distributions (January 2020)• The SECURE Act: A Game Changer (March 2020)• Roth Conversions in the Tax Cuts and Jobs Act Era (May, June, July 2019)• Qualified Charitable Distributions and the TSP (June 2018)

TSP-BK02 Withdrawing From Your TSP Account• For separated and beneficiary participants

TSP-775 Important Tax Information About Your TSP Withdrawal and RMDs

TSP-536 Important Tax Information About Payments From Your TSP Account

41

Thank You!

A NARFE Federal Benefits Institute WebinarPresented by Mark Keen, CFP®

[email protected]@narfe.org

Closed Captioning (CC) is available on the recorded version of this webinar.

42