Chapter-II

TEXTILE INDUSTRY OF INDIA

In this chapter, an attempt has been made to bring out the

development perspective of Textile Industry of India. This brief review

helps us to forecast the future opportunities for Indian textile

industry.

2.1 Introduction

The Indian textile industry is a personification of Indian culture.

It has always occupied a place of honour in the industrial system of

India. The spindles and the spinning wheels found in the excavation of

the Sindhu Valley have proved that the textile industry is as old as

Sindhu Valley civilization1.

India had traditionally been the cotton textile producing

country. Cotton was grown, spun and cloth was woven in our country

even much earlier than other countries started manufacturing it.

Indian textiles were famous for their exquisite beauty and fineness. It

had become the symbol of aristocracy, gracefulness and artistry in the

high society of Europe. It reached the zenith of glory before the dawn

of industrial revolution in the west.

Mahatma Gandhi discovered the power of Charaka and used it

to spin the dream of Swaraj / Independence from the British Yoke.

Khadi being spun on Charaka has been associated with our heritage

and history since time immemorial.

32

But due to British Supremacy over India and impact of

industrial research and technology, unsystematic attitude of the

Government, lack of capital and severe competition from the foreign

countries, the Indian textile industry is facing many challenges, to

which there is need to find out solutions.

Today textile industry of India comprises of Khadi, Woolen, Silk

traditional handloom sector with primitive technology; powerloom

sector which is technologically improved form of the handloom sector

and the composite mill sector with its advanced technology. Among all

the three, the handloom sector is most scattered and spread

throughout the country and is seen even in remote country side.

Powerloom sector is decentralized and scattered in and around some

identified centers of handloom sector. The mill sector is well organised

and integrated with spinning, weaving and processing in the same

roof.

2.2 Handlooms of India

The process of weaving primarily constitutes interlacement of

two sets of threads viz warp and weft and the equipment which

operates this interlacement is called ‘loom’. The handloom is made up

of a stick or wooden frame for weaving but more often it is defined as

a frame for weaving equipped with some wooden devices2.

In India various types of looms are traditionally in practice. They

can be noted on the nature of cloth produced or the places of their

origin. They are generally named as pit loom, frame loom, Manipuri

33

loom, Rajasthani loom, Kashmiri loom etc. Very recently automatic

and semi automatic jacquard looms and mechanical jacquard looms

are becoming familiar in India.

Pit looms are the most widely used handlooms in India.

Interestingly, even today the finest varieties of fabrics, known for their

beautiful designs and textures, are produced on throw shuttle pit

looms. The famous ‘brocades’ of Varanasi, the ‘Jamdanies’ of Tanda,

the ‘Patola’ Saris of Patan, the Himroos’ of Aurangabad, to mention

only a few of a vast range of exquisite hand-woven fabric of India, are

produced on these simple throw shuttle pit looms. As the name

implies, the loom stands over a pit and the process of picking is done

by throwing the shuttle across the sley by hand3.

Frame looms have come into existence due to certain

advantages they have in weaving designed varieties with more than

two treadles. These are also helpful in weaving fabric requiring mass

production. Frame looms are employed in manufacturing attractive

furnishings, bed sheets and made up items on a large scale.

Semi-automatic looms are now acquiring popularity in some

weaving centers in the country. Only a limited range of fabrics can be

manufactured on these semi-automatic looms. These looms are

operated by human effort by pedaling with legs or by moving the sley

by hand.

34

Though the methods employed in making handloom fabric are

simple, the results are rather extra ordinary. The human involvement

and ingenuity results in creations which are unique and aesthetically

delightful.

According to the statistics available the handloom industry of

India provides livelihood to nearly 124 lakhs people4. Out of which

60% are women, 12% SC and 20% ST (Ministry of Textiles 2001) while

the exact numbers are not available, a chunk of handloom weavers

belong to minorities.

Indian handloom products range from coarse cloth to very fine

fabrics from a variety of fibers such as cotton, silk, tasar, jute, wool

and synthetic blends. Handlooms are developed in different regions of

the country. There are independent weavers, weavers organised into

co-operatives, and there are those working under master weavers. We

do not have up dated figures on the number of looms or people. The

first handloom census was conducted in 1988 and the second census

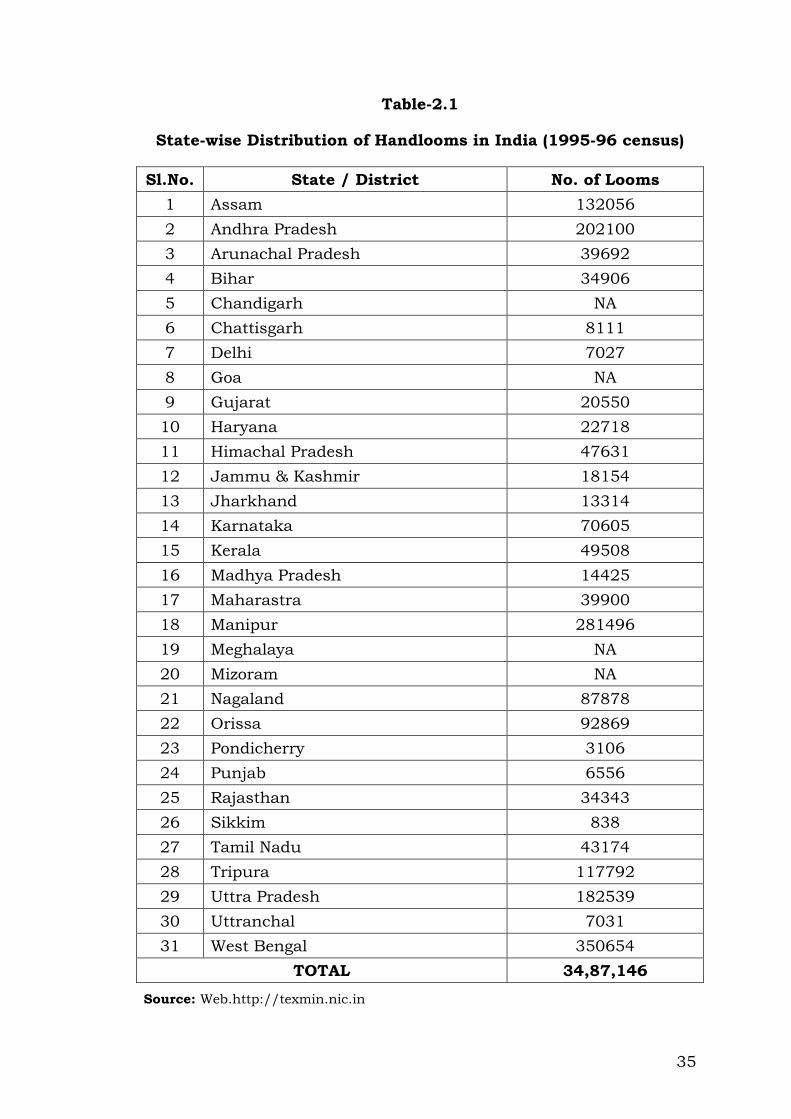

was conducted in 1995-96. According to the 1995-96 census the state

wise distribution of the handlooms in the country is as given in the

table 2.1

35

Table-2.1

State-wise Distribution of Handlooms in India (1995-96 census)

Sl.No. State / District No. of Looms

1 Assam 132056

2 Andhra Pradesh 202100

3 Arunachal Pradesh 39692

4 Bihar 34906

5 Chandigarh NA

6 Chattisgarh 8111

7 Delhi 7027

8 Goa NA

9 Gujarat 20550

10 Haryana 22718

11 Himachal Pradesh 47631

12 Jammu & Kashmir 18154

13 Jharkhand 13314

14 Karnataka 70605

15 Kerala 49508

16 Madhya Pradesh 14425

17 Maharastra 39900

18 Manipur 281496

19 Meghalaya NA

20 Mizoram NA

21 Nagaland 87878

22 Orissa 92869

23 Pondicherry 3106

24 Punjab 6556

25 Rajasthan 34343

26 Sikkim 838

27 Tamil Nadu 43174

28 Tripura 117792

29 Uttra Pradesh 182539

30 Uttranchal 7031

31 West Bengal 350654

TOTAL 34,87,146

Source: Web.http://texmin.nic.in

36

According to the handloom census conducted in 1995-96 it is

the West Bengal, which has the highest number of handlooms

(3,50,654), followed by Manipur (2,81,496), Andhra Pradesh

(2,02,100) and Uttar Pradesh (1,82,539). Karnataka has 70,605

handloom units. As the nature of handloom industry in India is, it is

scattered and unorganized; it is difficult to get updated statistics.

Third Handloom Census:

The third census of handlooms was conducted in April 2008.

The National Council of Applied Economic Research (NCAER) was

asked to conduct the third census of Handloom workers and issue

photo Identity cards to weavers and Allied workers by Development

Commissioner (Handloom). The challenge before NCAER was not only

the coverage of eligible handloom households and workers but also to

photograph all adults for the issuance of photo identity Cards. The

survey for the Third census of handlooms was initiated in September

2009 and covered all the 30 states / Union territories of India, across

both rural and urban locations. The coverage of the third census of

handlooms in 2009-10 is larger compared to the earlier census

exercises conducted in 1987-88 and 1995-96.

Objectives of Third Handloom Census:

1. Assessment of the total number of units both households and non-

households engaged in handloom activities.

2. Assessment of the total number of workers involved in the activities

of weaving, pre-loom and post-loom activities.

37

3. Assessment of the total number of looms both households and

non-households and assessment of working and idle looms.

4. Assessment of the employment structure of the handloom sector

for weavers and allied workers; and.

5. Undertake the photography of all handloom weavers and allied

activity workers aged 18 and above, and collect their individual

details for photo identity cards5.

Major Highlights of the Third Handloom Census:

Handloom activity is mainly a rural phenomenon. 87% of total

household units (27.83 lakh) are located in rural areas.

Nearly 61% handloom worker households reside in the north-east

and are into domestic production.

Majority (82%) are weaver households, only 13% households

exclusively are engaged in allied activities.

But a little over half of the total household units are engaged

exclusively in commercial activities.

Nearly 47% of handloom worker households are BPL and rest are

non-BPL.

The majority of the household looms in India are Frame looms

(59%) followed by Pit looms (25%). While over 78% of looms in

north-eastern states are Frame looms, other regions are dominated

by pit looms.

38

Nearly 75% of total workforce engaged in handloom activities is

female.

A majority (60%) of adult handloom work force has attained little or

no schooling.

Nearly 67% weavers are engaged on a full-time basis.

The third census of handlooms is an e-census, i.e. paperless

exercise, since entire exercise was undertaken using personal digital

assistant mobile technology. Not only does it provide a data base of

weavers and allied workers and handlooms throughout the country, it

also has photo-linked data base of all eligible handloom weavers and

allied workers in the handloom sector.

As in the case of every census, there are some limitations in the

survey. Third census enumeration has been conducted primarily in

the list of the locations provided by the state government, although

additional concentrations have been covered as well using local

knowledge. Additionally, all information collected from eligible

households has been based on their self-declaration, and it has been

only possible to physically verify the information on the looms.

The report of the Third Handloom Census (2009-10) has been

published on the eve of the formulation of the 12th Five year plan and

it is hoped that this census will facilitate in formulating a more

effective policy and business decisions for the development of the

sector and the welfare of weavers and allied workers6.

39

2.3 Khadi Handlooms of India

One can’t think of textile industry of India without mentioning

about khadi handlooms. Before independence, khadi handlooms

acquired great importance due to efforts of Mahatma Gandhiji who

used the weaving instrument ‘Charaka’ as an instrument to achieve

Swaraj / independence.

But before independence promotion of khadi was mainly

undertaken by the voluntary agencies in a decentralized manner.

However, after independence the development of khadi handlooms in

an organized manner was felt essential for the overall rural

employment generation in the country. Accordingly, the Khadi and

Village Industries Commission (KVIC) was constituted by the

Government of India by an Act of parliament passed in 1956 and KVIC

came into being in April 1957.

KVIC is one of the key players engaged in the task of rural

industrialization and keeping alive the khadi weaving activity in the

country. KVIC is operating through 34 number of state and Divisional

Offices and with the partnership of 33 number of states’ and Union

territories’ Khadi and Village Industries Boards as well as 27 public

sector Banks for implementing its schemes.

The khadi and village Industries sector has a wide network in

the form of around 5000 institutions, more than 4 lakhs rural

entrepreneurs and 7050 sales outlets run by its implementing

Agencies to market its products. The sector involves more than one

40

crore people and the 11th plan envisages providing employment to

1.44 crore people under khadi and village industries activities. KVIC is

working day and night to achieve this target. KVIC has a ‘Vision’ for

bringing self-reliance and self sufficiency among the village artisans,

spinners and weavers.

KVIC looks after the khadi handloom activity by creating 6

zones throughout the country.

1. North zone: It includes the states / union territories like-

Chandigarh, Delhi, Haryana, Himachal Pradesh, Jammu and

Kashmir, Punjab and Rajasthan.

2. East zone: Which consists of states /union territories like-

Andaman and Nicobar Islands, Bihar, Jharkhand, Orissa, and West

Bengal.

3. North-East zone: In which there are states / union territories like-

Arunachal Pradesh, Assam, Manipur, Meghalay, Mizoram,

Nagaland, Sikkim, and Tripura.

4. South zone: Includes states / union territories like- Andhra

Pradesh, Karnataka, Kerala, Lakshadweep, Pondicherry, Tamil

Nadu.

5. West zone: There are the states / union territories like- Dadra and

Nagar Haveli, Daman and Diu, Goa, Gujarat, Maharastra.

6. Central zone: Which includes states / union territories like-

Chattisgarh, Madhya Pradesh, Uttarakhand, and Uttar Pradesh.

41

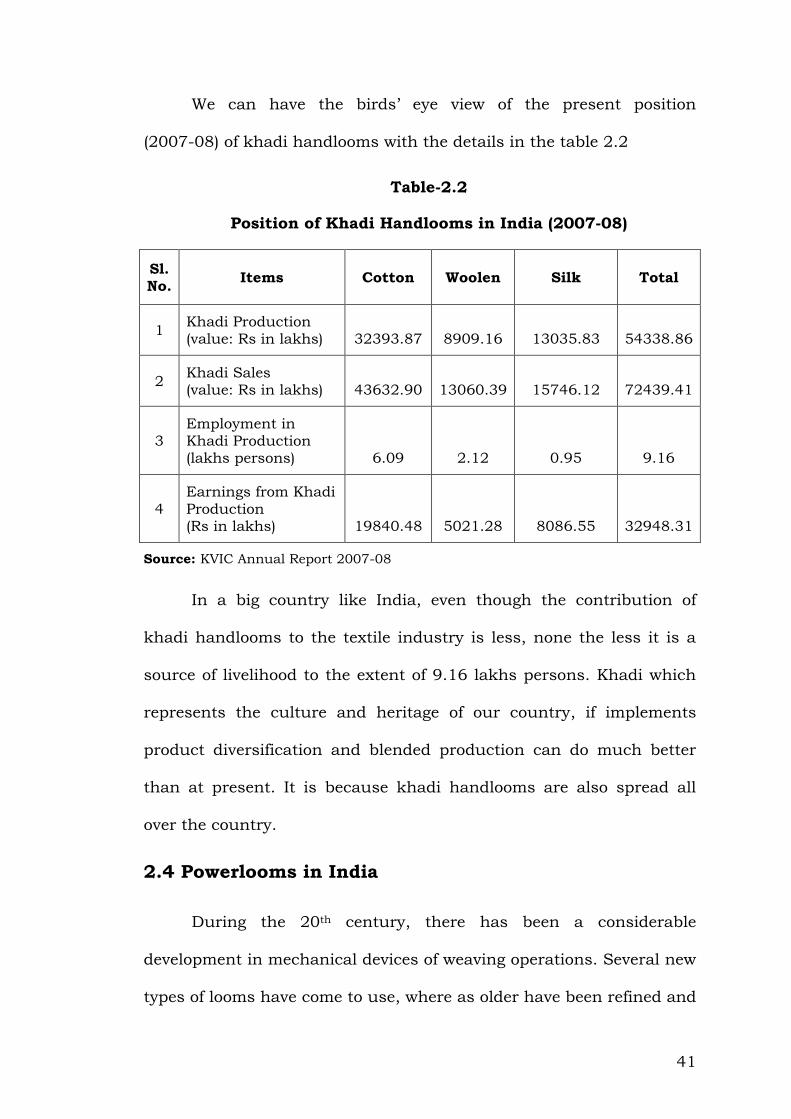

We can have the birds’ eye view of the present position

(2007-08) of khadi handlooms with the details in the table 2.2

Table-2.2

Position of Khadi Handlooms in India (2007-08)

Sl. No.

Items Cotton Woolen Silk Total

1 Khadi Production (value: Rs in lakhs) 32393.87 8909.16 13035.83 54338.86

2 Khadi Sales (value: Rs in lakhs) 43632.90 13060.39 15746.12 72439.41

3 Employment in Khadi Production (lakhs persons) 6.09 2.12 0.95 9.16

4

Earnings from Khadi

Production (Rs in lakhs) 19840.48 5021.28 8086.55 32948.31

Source: KVIC Annual Report 2007-08

In a big country like India, even though the contribution of

khadi handlooms to the textile industry is less, none the less it is a

source of livelihood to the extent of 9.16 lakhs persons. Khadi which

represents the culture and heritage of our country, if implements

product diversification and blended production can do much better

than at present. It is because khadi handlooms are also spread all

over the country.

2.4 Powerlooms in India

During the 20th century, there has been a considerable

development in mechanical devices of weaving operations. Several new

types of looms have come to use, where as older have been refined and

42

their scope extended. Powerloom means a loom which is worked by

power and which is used or may be used for weaving cloth7, Power

represents electrical energy or any other form of energy which is

mechanically transmitted and is not generated by human or animal

agency8. Thus powerloom sector consists of manufacturing cloth with

the help of up-graded handloom technology by the weavers.

The introduction of powerlooms in India in the decentralized

sector dates back to 1904 when the Jahagirdar of Ichalkaranji (the

princely state) gave encouragement to weavers to install powerlooms

and improve their standards of living9. Later they were introduced in

the Indian weaving industry in 1922. Till 1927 the growth of this

industry was slow. Infact, this was major breakthrough in the

decentralized weaving industry as manpower was substituted by

mechanical power.

In the early thirties many small entrepreneurs purchased looms

discarded by mills in Bombay and Ahmadabad and converted them

into powerlooms. This practice of using discarded looms continues

even today but looms manufactured as powerlooms are also in

evidence. Since these looms are reducing the strain of weaving

operation and are relatively less expensive with better efficiency,

productivity and higher margin of profit, the powerlooms have become

more popular.

During the II world war, the increased requirement of defence

demand for cloth and also the civilian population boosted the

43

development of powerlooms. Further the expansion of electricity

services in the country also helped the powerloom sector to strengthen

its roots during this period.

The post independence period, with Government supporting

conversion plan i.e. conversion of handlooms to powerlooms also

helped. Allthis changing situation gave the proliferation of powerlooms

in the decentralized sector of the textile industry.

The table 2.3 gives the picture of growth of powerlooms in India

since 1951 to the present day.

Table-2.3

Growth of Powerlooms in the Country

Year No. of Powerlooms

1951 24078

1961 160465

1971 221200

1981 599020

1991 1057000

2001 1661550

2011 2269469

Source:1. Ambedkar Institute for labour studies, Bombay 2. AIFCOSPIN Silver Jubilee Annual 1988 and year Book, 1991, Bombay. 3. Abid Hussain Committee Report, 1990, New Delhi. 4. www.indiastat.com

The table 2.3 gives the estimated number of powerlooms in

decentralized sector. Unlike the handlooms, the powerlooms are of

recent origin. The growth of powerlooms was actually started in the

44

1960s decade and year after year there is tremendous growth in

number of powerlooms. As a result presently we have more than 22.69

lakhs powerlooms. Looking at the speed of increase in number of

powerlooms, one may calculate the good future and prospect for

powerlooms industry.

DIAGRAM 2.3 (a)

Presently the powerlooms are also established throughout the

country. But some states are far ahead in developing powerlooms. The

table 2.4 gives the details of state wise registration of powerlooms and

employment in India.

The table 2.4 clearly states that Maharashtra has the highest

number of registered powerlooms (11,06,474) employing 27,66,185

persons followed by Tamil Nadu (38,73,79) employing 96,84,45

persons and third state in respect number of registered powerlooms is

45

Gujarat (32,33,39) employing 80,83,48 persons, and then comes

Madhya Pradesh with 10,48,23 registered powerlooms, providing

employment to 26,20,58 persons. Karnataka is the 5th state in respect

of number of registered powerlooms (88,566), giving employment to

2,04,725 persons.

It is evident from these details that the states which have

provided all the basic facilities and incentives for production of cloth

in powerlooms are also economically well developed. It means to

increase the contribution of powerlooms towards the development of

states, there is need to provide good facilities for the establishment of

powerlooms in the state.

46

Table-2.4

State-wise Registration of Powerlooms and Employment in India

(2008-09)

Sl. No.

State / Union Territories

No of looms registered

Employment (Anticipated)

1 Andhra Pradesh 45138 112780

2 Assam 2726 6815

3 Bihar 2894 7235

4 Delhi 1102 2755

5 Goa 122 305

6 Gujarat 323339 808348

7 Haryana 9933 24833

8 Himachal Pradesh 1461 3653

9 Jammu and Kashmir 65 163

10 Karnataka 88566 204725

11 Kerala 2800 7000

12 Madhya Pradesh 104823 262058

13 Maharastra 1106474 2766185

14 Orissa 3321 8303

15 Punjab 23620 59059

16 Rajasthan 34159 85396

17 Tamil Nadu 387379 968445

18 Uttar Pradesh 65993 164983

19 West Bengal 5687 14218

20 Chandigarh 42 105

21 Dadar and Nagar Haveli 962 2405

22 Puducherry 830 2075

TOTAL 2204734 5511835

Source: www.indiastat.com

47

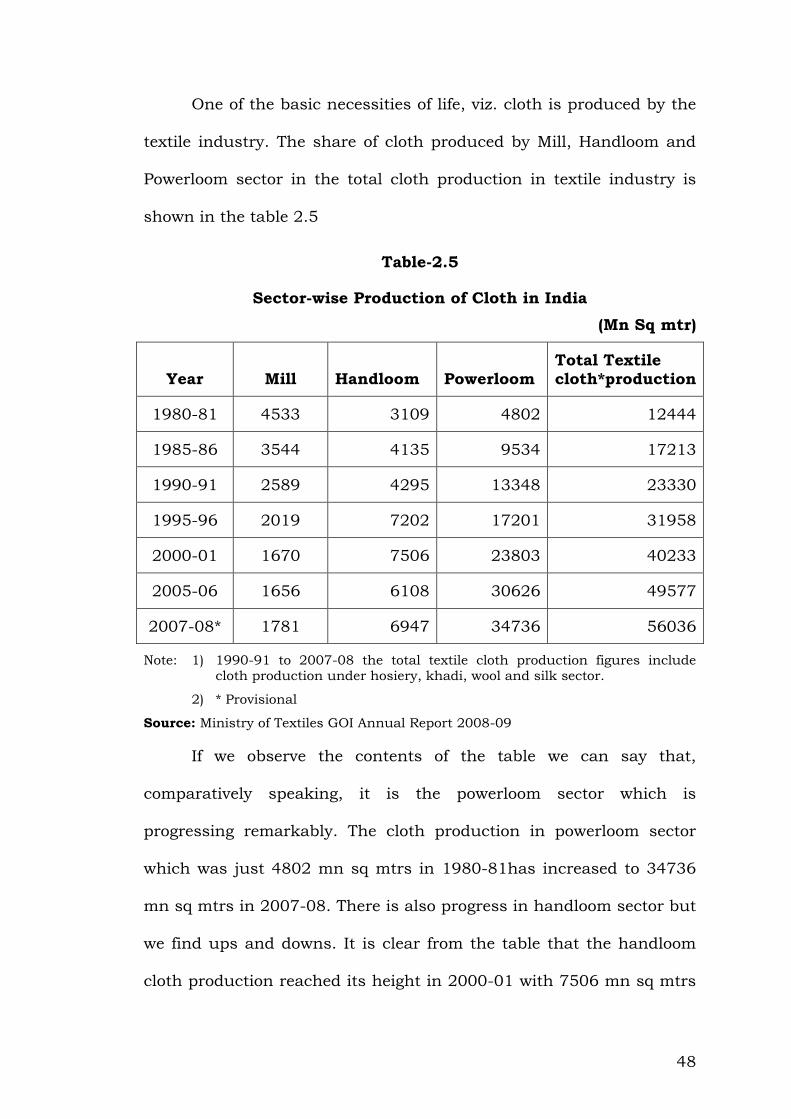

2.5 Production of cloth in India:

MAP-I

STATE WISE DISTRIBUTION OF Handlooms

(1995-96) and Powerlooms (2008-09) in India

Handlooms

Powerlooms

48

One of the basic necessities of life, viz. cloth is produced by the

textile industry. The share of cloth produced by Mill, Handloom and

Powerloom sector in the total cloth production in textile industry is

shown in the table 2.5

Table-2.5

Sector-wise Production of Cloth in India

(Mn Sq mtr)

Year Mill Handloom Powerloom

Total Textile

cloth*production

1980-81 4533 3109 4802 12444

1985-86 3544 4135 9534 17213

1990-91 2589 4295 13348 23330

1995-96 2019 7202 17201 31958

2000-01 1670 7506 23803 40233

2005-06 1656 6108 30626 49577

2007-08* 1781 6947 34736 56036

Note: 1) 1990-91 to 2007-08 the total textile cloth production figures include cloth production under hosiery, khadi, wool and silk sector.

2) * Provisional

Source: Ministry of Textiles GOI Annual Report 2008-09

If we observe the contents of the table we can say that,

comparatively speaking, it is the powerloom sector which is

progressing remarkably. The cloth production in powerloom sector

which was just 4802 mn sq mtrs in 1980-81has increased to 34736

mn sq mtrs in 2007-08. There is also progress in handloom sector but

we find ups and downs. It is clear from the table that the handloom

cloth production reached its height in 2000-01 with 7506 mn sq mtrs

49

but then on wards in the decade 2000 the handloom sector is facing

critical time due to internal and external reasons. Speaking about Mill

sector, there is downward trend and so both the mills and handlooms

have been conquered by the powerlooms.

From the same table 2.5 we can also infer the relative

percentage share of Mill, Handloom and Powerloom sector in the total

production of cloth in textile industry.

Table-2.6

Percentage Share of Mill, Handloom and Powerloom Sector in Total Cloth Production in India (Percentage)

(1980-81 to 2007-08)

Sector /

Year

1980-

81

1985-

86

1990-

91

1995-

96

2000-

01

2005-

06

2007-

08

Mill 36.42 20.58 11.09 6.31 4.15 3.34 3.17

Handloom 24.98 24.02 18.4 22.53 18.65 12.32 12.39

Powerloom 38.58 55.38 57.21 58.82 59.16 61.77 61.98

DIAGRAM 2.6 (a)

50

The percentage bar diagram represents the percentage share of

Mill, Handloom and Powerloom sector in total cloth production in

India from 1980-81 to 2007-08. This is made clear that the relative

share of Mill, Handloom and Powerloom sector which was 36.42%,

24.98%and 38.58% respectively in 1980-81 changed to 3.17%,

12.39% and 61.98% respectively in 2007-08.

The cloth production by Mill sector and handloom sector has

declined by 33.25% and 12.59% respectively, while that of powerloom

sector has increased by 23.40%. So the contribution by the powerloom

sector to the total cloth production in textile industry of India is

remarkable.

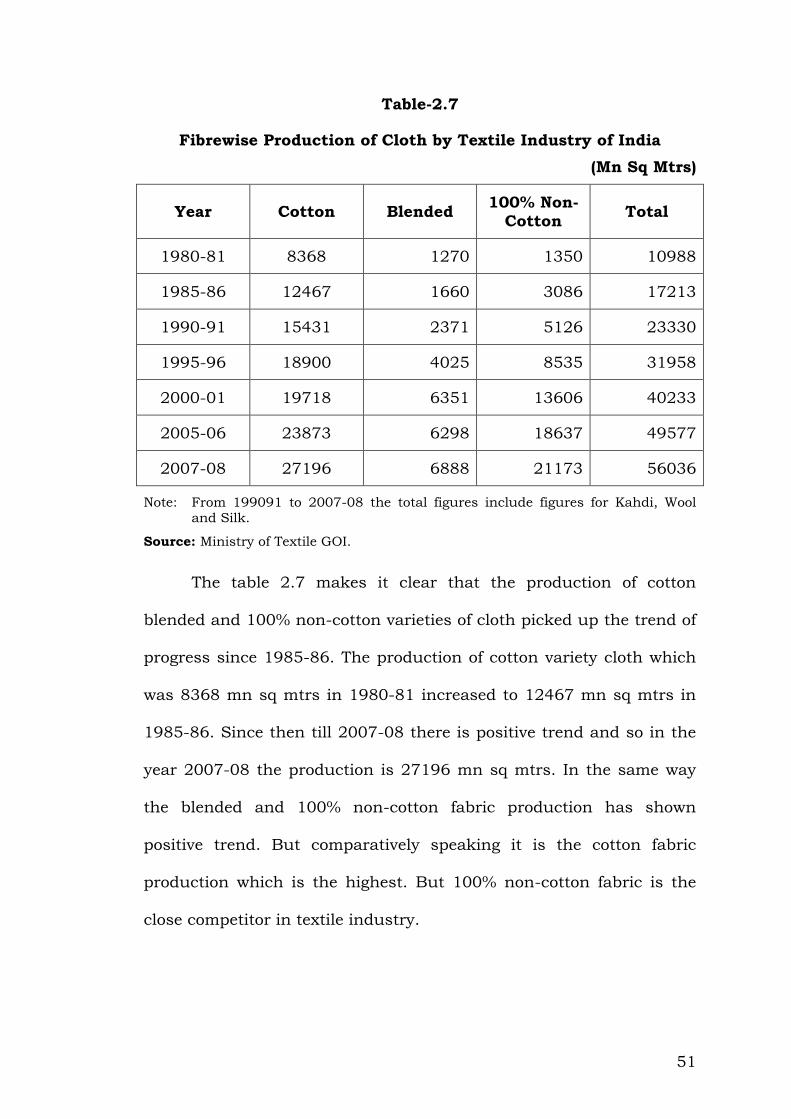

Fibrewise Production of Cloth:

The segments of textile industry produce cloth of different

variety such as cotton, blended, 100% non-cotton, Khadi, wool and

Silk. The fibrewise production of cloth is shown in the table 2.7

51

Table-2.7

Fibrewise Production of Cloth by Textile Industry of India

(Mn Sq Mtrs)

Year Cotton Blended 100% Non-

Cotton Total

1980-81 8368 1270 1350 10988

1985-86 12467 1660 3086 17213

1990-91 15431 2371 5126 23330

1995-96 18900 4025 8535 31958

2000-01 19718 6351 13606 40233

2005-06 23873 6298 18637 49577

2007-08 27196 6888 21173 56036

Note: From 199091 to 2007-08 the total figures include figures for Kahdi, Wool and Silk.

Source: Ministry of Textile GOI.

The table 2.7 makes it clear that the production of cotton

blended and 100% non-cotton varieties of cloth picked up the trend of

progress since 1985-86. The production of cotton variety cloth which

was 8368 mn sq mtrs in 1980-81 increased to 12467 mn sq mtrs in

1985-86. Since then till 2007-08 there is positive trend and so in the

year 2007-08 the production is 27196 mn sq mtrs. In the same way

the blended and 100% non-cotton fabric production has shown

positive trend. But comparatively speaking it is the cotton fabric

production which is the highest. But 100% non-cotton fabric is the

close competitor in textile industry.

52

This can be made more clear by observing the percentage share

of fibrewise production of cloth by textile industry of India (table-2.8).

Table-2.8

Percentage Fibrewise Production of Cloth by Textile Industry

(Percentage)

Fibre / Year

1980-81

1985-86

1990-91

1995-96

2000-01

2005-06

2007-08

Cotton 76.15 72.42 66.14 59.14 49.00 48.15 48.54

Blended 11.15 9.64 10.16 12.59 15.78 12.70 12.29

100% non-cotton 12.28 17.92 21.97 26.70 33.81 36.60 37.79

This table 2.8 is translated into Percentage Bar diagram.

DIAGRAM 2.8 (a)

The comparative statistics of percentages with regard to

fibrewise production of cloth reveal that there is sharp fall (by 27.61%)

in the production of cotton fabrics in 2007-08 compared to production

53

in 1980-81. At the same time the production of 100% non-cotton

fabric has increased by 25.51% in 2007-08 compared to production in

1980-81. Another fact is that there is little progress in the production

of blended fabric i.e. by 1.14% in the year 2007-08 compared to the

production of blended fabric in 1980-81. All this means that the

textile industry is turning towards product diversification and wants

to expand its production base.

2.6 Indian Textile Exports

Today the textile industry of India contributes around 14% to

industrial production in the country, 4% to the GDP, is estimated to

directly employ approximately 35 million people apart from the

indirect employment in allied sectors, thus making it the second

largest employer after agriculture. It accounts for about 15% of the

country’s exports, and is, in sum, an important economic engine for

the nation10.

Textiles US

$ 10Bn

Clothing US $ 30Bn

Textiles US

$ 12Bn

Clothing

US $ 10Bn

Exports US

$ 22Bn

Domestic Market US

$ 40Bn

Indian Textile and Apparel Market US $

62Bn

54

The Indian textile export basket consists of wide range of items

containing cotton yarn and fabrics, man-mad yarn and fabrics, wool

and silk fabrics, made-ups and variety of garments.

The present size of Indian textile and appeared market is US $

62 Billion of which US $ 22 Billion is exports while the rest US $ 40

Billion is the domestic market. According to the latest statistics by

Apparel Export Promotion Council (AEPC), India’s textile exports have

reached US $ 12 Billion and US $ 10.64 Billion of garment exports in

2009-10. With the revival of demand in western markets, India’s

textile exports may grow up to US $ 24 billion in 2010-11 with the

support of the government.

2.6 (A) Global Perspectives:

According to the world Trade Organization (WTO) report11 the

Global textile Production will grow up to 25% by the year 2010 and

50% by 2014. The world textile and apparel industry has gone into a

phase of transformation since the elimination of quota in the year

2005. Over the years production has converged towards Asia from

western countries leading to increase in Global Textile and Apparel

Trade.

55

Table-2.9

Global Textile and Apparel Trade (US $ Billions)

US $ Billion 2000 2006 2007 2008 2009 2015 2020

Textile 157 220 240 250 200 300 350

Apparel 198 309 346 362 310 500 650

Total 355 529 586 612 510 800 1000

Source: WTO, UN Contrade and Technopak Analysis 2010.

DIAGRAM 2.9(a)

With the WTO replacing the Multi Fibre Agreement (MFA), the

global textile industry is stated to undergo major structural changes.

The globalization of the textile trade will increase sourcing from

developing countries owing to low labour costs and local availability of

raw material. Countries like China and India are likely to emerge as

the largest beneficiaries in the post quota regime.

56

Under the MFA regime, the world trade in textiles was restricted

and the developing countries were allowed to protect their domestic

industry against the competitive imports. With removal of quota, cost

competitiveness and quality are expected to be only two factors

determining the success of a country’s textile sector in global market.

While the new regime opens up the market to fierce competition it also

provides opportunities to countries like India, which have a natural

competitive edge on account of availability of raw material, cost-

effective labour and healthy domestic market.

Hence there is an opportunity for India to reach US $ 80 Billion

exports by 2020. This is clear by the table 2.10 regarding growing

world trade in textile between 1990-2020.

Table-2.10

Growth of World Textile Trade 1990-2020

Sl. No.

US $ Billion 1990 2000 2005 2008 2009 2015 2020

1 World GDP 23000 32000 45400 61000 57000 82000 111027

2 World Trade 4338 7902 12752 19344 15341 24600 33308

3 World Textile and Apparel Trade

213 353 486 612 510 800 1000

4 China Textile and Apparel exports

16 52 104 175 157 236 350

5 India Textile and Apparel exports

4.6 11.4 15 21 23 45 80

6 India’s Share in

Global Textile and Apparel Trade

2.10% 3.20% 3.10% 3.40% 4.50% 5.60% 8.00%

Source: WTO. UN Comtrade and Techno pack Analysis 2010.

57

So the table 2.10 makes it clear, the potential for India to

almost double global export share. China will remain the biggest

exporter but with rising costs and rising domestic demand, it may

cede some export opportunity. So we must grab opportunity to earn

more through our textile items by producing high quality goods at

reasonable prices12. Further, going forward, Indian economy has a

very positive outlook.

58

REFERENCES

1. Government of Karnataka-(1993): ‘ Textile Policy’, P-I (Ministry of

Textile).

2. Dr. M. Sundarapandian: ‘Growth and prospects of Handloom

sector in India’, occasional Paper-22 NABARD Mumbai.

3. Ibid.

4. K. Rajendra Nair: ‘India’s Handloom sector’ 11th F.Y.Plan VIII Vol.,

p. 107.

5. Government of India: ‘Third National Handloom Census of

Weavers and Allied workers-2010’, Chapter-I.

6. Rajesh Shukla: ‘Census Weaves Rich Handloom Data’, The

Economic Times, February 7th 2011.

7. Government of India: ‘Textile Control Order, 1986’.

8. Government of India: ‘Factories Act, 1948’ section 2 clause (9).

9. Government of India: ‘Report of the Powerloom Enquiry,

Committee (Ashok Mehta)’ May, 1964.

10. Souvenir: ‘66th All India Textile conference’ January 28th, 29th,

2011.

11. Ibid.

12. Editorial: ‘Opportunities for Entrepreneur Indian Textile Industry’

Science Tech Entrepreneur August 2007.