The 2nd edition of the Gira

European Bakery Company Panorama2001- 2011/2012 & 2016

A study completed in November 2012

Bread – Viennoiserie – Patisserie – Savoury PastryFresh and Prepacked – Industrial and Artisanal

Markets – Players – News – Trends & Forecastsfor every Country of the EU-27 + Turkey

The Whole Bakery Sector at Your Fingertips

Essential information for:� Bakery Companies

� Millers and Bakery Ingredients Manufacturers� Wholesalers and Importers in the Bakery Chain

� Modern and Specialist Retailers� Equipment and Machinery Suppliers

� Associations of Industrial Bakers� Banks and Investment Funds

13, chemin du LevantF - 01210 Ferney-Voltaire

Tel : (33) 4 50 40 24 00 Fax : (33) 4 50 40 24 02E-mail : [email protected] Web site : www.girafood.com

November 2012

2

What is the Bakery Panorama – what you get – what's n ew? Page 3

1. Background and issues 6

2. Objectives 8

3. Scope of the Research 9

4. Structure and Contents of the Reports 10

5. Methodology and Staffing 13

6. Price, Reports and Follow-up 14

7. Gira's clients in the bakery sector 15

Appendix: some examples from the Country Reports & EU Synthesis 16

Contents of this Proposal

3

Over 1,000 PAGES of UNIQUE INFORMATION and PERSPECT IVE at a LOW PRICE

This comprehensive report is a focused, one-stop so urce for all the basic information you need on Europe’s industrial bakers in the context of their markets :

• It covers bakery consumption, distribution and production (both artisanal and industrial),

• In each country of the EU and at global EU-27 level – and also for Turkey

• Showing the importance of (and profiling) the key players, and what is happening in the business.

• Markets for bread, viennoiserie, cakes and savouries – but NO biscuits & NO breakfast cereals to cloud the picture• All the major events – in each country – over the last 5 years• Profiles of the top 96 EU bakery companies• League Tables of the top industrial bakers – Pan-EU27, by individual country, & by type of production• The market share of each type of production method for each bakery product in each country

• Data AND quantitative and qualitative market fore casts through 2016• And, for the first time, with a specific focus on Turkey.

With a 110-page strategic Synthesisplacing each bakery product, country and significant company in its current and future context.

HIGHLY OPERATIONAL – all the KEY FACTS at your FINGE RTIPS

The second edition of Gira's groundbreaking EU study– a great deal has changed since the first edition in 2007

Bakery production methods

"Artisanal" scratch baking on the premises

Industrial fresh finished

Industrial bake-off

Industrial prepacked

France Poland Czech Rep. UK

4

The Gira European Bakery Company Panorama2001-2011/2012 & 2016

This Panorama is a comprehensive source of all the fundamental industry and market data that you need, together with informed opinion on what it means.Through it, you will be able to follow and fully comprehend the major events in the Bakery sector, with perspectives at both pan-EU level and for each EU-27 member state & Turkey.

Gira’s new European Bakery Company Panorama concentrates on the bakery industries of the EU – treating separately the four major products: Bread, Viennoiserie, Patisserie and Savoury Pastry.

It situates each of the main bakery companies in the context of its major competitors and by technology (fresh, prepacked, bake-off).

Whichever of the bakery products and technologies y ou are active in, your sector is given full coverag e in the Panorama.

Whatever your role in the EU bakery supply chain – miller – ingredient manufacturer – industrial baker – wholesaler – retailer –caterer – equipment supplier or investor – this Panorama is the unique source of comprehensive, easy-to-access, coherent and comparable information that you need to manage and plan your business. It gives you a reality-check and the ability to understand the inevitable major changes & media-crises of the future and to counteract all the hype that bombards you every day!

It is the only pan-EU industrial bakery data source on the real industrial bakers ( not breakfast cereal & biscuit manufacturers). It is a user-friendly and very value-for-money source of all the basic information about your sector in Europe.

The Panorama contains an array of relevant corporat e, structural and market information that you gener ally cannot find elsewhere , and certainly never in one place. It has 3 main sections:

• Pan-EU summary and analysis

• Country Reports – for each member state of the EU-27, full description of the bakery industry and the market conditions, by bakery product, with a bonus this time in the form of the first ever analysis of the enormous Turkish bakery market

• Profiles of the top 96 European bakery companies.

What is the Gira European Bakery Panorama?

5

The Pan-EU Synthesis gives you a unique and comprehen sive overview of the bakery industry at EU level:• "League tables” of the major bakery companies, by group turnover, by main bakery products (bread, viennoiserie, patisserie,

savoury pastry) and by main technology (fresh, prepacked, bake-off)• All the important news and events on the European bakery industries & markets, over the last 5 years• Bakery markets summary tables : EU tables of consumption, distribution and production for each bakery product and for 2001-

2011/2012 & 2016 forecasts• Overview of the dynamics which are driving the European bakery industry, and of the strategies of the main players.

The individual Country Reports covering EU-27 + Tur key then describe the bakery markets and industry st ructures- for each of the 4 bakery product markets in each country:

• Market context : historical from 2001 to 2011, 2012 estimates, split according to the technology used (fresh, prepacked)• Distribution channels for each bakery product: retail (modern, traditional) and catering (commercial, social)• Production structure breakdown : artisan bakers, modern retailers' in-store scratch baking, and industrial bakers (in the form of

fresh, prepacked and bake-off products)• 2016 Forecasts for all of the above elements: the products, the technologies, the distribution channels, the production structures

and, consequently, the suppliers with strongest growth potential• All the major events affecting your industry over the last 5 years (with the accent placed on the most recent years)• Lists of the main industrial bakery companies – with their production structure overview.

And then there are the Profiles – a focused review of the vital statistics of each of the 96 major EU industrial bakers.

Each Country Report and all the related company Profiles have been prepared by Gira researchers with an intimate knowledge of the industry in that country , using the latest research and interview methods.

All this for just Euro 9 800 (before any taxes).

Available in searchable PDF format, the Panorama is the ultimate in user-friendly information at a use r-friendly price.

E-mail your order to [email protected] - or call us to discuss (+33 450 402 400).

What you get

6

1. Background and issuesThe EU bakery markets are enormous and face major challenges

Gira estimates that the European Union market for bread, viennoiserie, patisserie and savoury pastry snacks amounted 40.1 million tons in 2011.

The Panorama presents and comments all the major ne ws and events of the last 5 years that affect bakery markets – in each country and with an assessment of their importance for the future:

• The main consumer trends, such as health and nutrition concern, snacking habits

• The effects of the economic crisis, which had a major impact on bakery consumption –It has changed some of the long-term trends

• Raw material prices and cost pressures

• The trends in distribution structure for bakery products:• The future of artisan bakeries • The baking activities of the discount retailers• The emergence of new distribution channels.

0

10,000

20,000

30,000

40,000

2001 2006 2011 2012(e)

2016 (f)

Bread

Viennoiserie

Patisserie

Savourypastry

('000t)

Source: Compilation Gira

Consumption trends by product

0

10,000

20,000

30,000

40,000

2001 2006 2011 2012(e)

2016 (f)

Fresh

Prepackedlong-Life

Prepackedhome-baking

('000t)

Source: Compilation Gira

Consumption trends by technology

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Tur

key

Ger

ma

ny

Fra

nce

Uni

ted

Kin

gdo

m

Italy

Pol

and

Spa

in

Ro

man

ia

Net

herl

and

s

Gre

ece

Cze

ch R

epu

blic

Bel

giu

m

Bul

garia

Hu

ngar

y

Por

tuga

l

Aus

tria

Sw

eden

Irel

and

Slo

vaki

a

Den

ma

rk

Fin

land

Lith

uani

a

Latv

ia

Cyp

rus

Slo

veni

a

('000t)

Source: Gira

Bakery products consumption by country - 2011

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2001 2006 2011 2012 (e) 2016 (f)

Catering

Other retail

Bakery chains

Modern retail

Artisan

Source: Gira compilation

Distribution trends in EU-27

7

The industry is constantly changing – requiring up-to-date insight and information

A standard consumption and production breakdown is used as the framework for our overview of the industrial structure and perspectives of each bakery product in each country – as well as for showing the relative importance of each at EU level.

The markets are thus segmented in terms of main supply technology (e.g. scratch artisanal vs. bought fresh vs. baked-off) for each bakery segment in each country.

We have also updated the “league tables” of all the major EU groups – both at individual country level and also at EU level. This is highly useful tool, with so much consolidation, restructuring and cross-border activity taking place.

There is a section of two-page profiles of each of the EU’s 96 leading industrial bakery producers. There is thus a profile for almost every group that appears in the league tables.

Viennoiserie supply structure – France – 2006-2011-2012 (e) & 2016(f)

∆ 06/11 ∆ 11/16(% pa) (% pa)

Artisan bakers 125 86 86 77 -7.2% -2.2%

Retailers in-store 11 9 7 4 -5.5% -15.9%

Others* 0 0 0 0 #DIV/0! #DIV/0!

Total artisanal 137 95 93 81 -7.0% -3.1%

Fresh finished 41 36 36 27 -2.6% -5.5%

Bake-off 243 301 307 338 4.4% 2.3%

Prepacked-long life 169 177 178 183 0.9% 0.7%

Prepacked frozen 6 8 8 9 5.3% 1.6%

Total industrial 460 522 528 557 2.6% 1.3%

596 617 621 638 0.7% 0.7%*: other retail and catering sectorsSource: Gira

('000 tons) 2012(e) 2016(f)20112006

Total

Industrial Supply

Artisanal supply

From 2006 to 2011 and 2012(est.), as well as forecasts for 2016

Tables & graphsFor each bakery product

7% 6% 6% 8%5%

11% 9% 11% 9% 6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

EL FR IT PT BE DE ES AT NL FI DK SE UK IE PL CY RO HU SK SI CZ LT BG LV EE T KArtisan bakers "scratch" Retailers in-store "scratch" Other retail & catering "scratch"Fresh finished "industrial" Bake-off "industrial" Prepacked long-life "industrial"Prepacked home-baking "industrial"

% v

olum

e (c

onsu

mpt

ion)

Source: Gira

Bakery products supply structure by country - 2011

And last but not at all least, there is a full country study of Turkey – which is one of the biggest bakery products consumers in Europe – and which is currently a target for many large EU industrial bakers.

8

2. Objectives of the Panorama

Our objective in preparing this second edition of the Panorama was to provide bakery industry operators and other stakeholders with essential information on the main European bakery c ompanies and their national and EU marketsthat is:

� Up-to-date: the last Panorama was published in 2007 and a lot has happened since then!

� Easy to use: everything in one report, following a standardised structure: key information at your fingertips!

� Of practical use: the information & forecasts that every operator needs – short, medium and long-term – succinct and operational

� Authoritative: over the last 30 years, Gira has built up a unique databank of comparable bakery company and market information. This Panorama is the product of just one part of our European and bakery knowledge

� Comparable, and in perspective: we have adopted standard product definitions and units of measure throughout, with clear indications of what each figure means.

The Panorama provides transparency in an industry which is still clouded by secrecy and reticence to disclose figures … yet which is rapidly becoming more international and ever more concentrated. As EU competition and price pressures continue to grow, it is simply wrong to think that any operator can continue in “splendid isolation”.

There is a real need for more information in the ba kery sector. It needs to be up-to-date and it needs to be affordable.

The Gira Panorama really is unique : there is absolutely no alternative! It covers all four bakery product sectors for each of the EU-27 countries + Turkey, with key data on all the markets, the companies and the events that are shaping the business.

Each Country report & each Profile follow the same structure, to simplify comparison and make the Panorama easy to read and to use.

Coverage of each bakery sector in each Country Report begins by setting the scene, with macro-sectoral forecasts in the framework of historical consumption and production breakdowns (e.g. fresh vs. prepacked products etc.) which immediately provides the market context in which the industrial bakers are operating…

9

2.1 SECTOR SCOPE

� Bakery products : we cover each of bread, viennoiserie, patisserie and savoury pastry snacks (to be consumed hot) – biscuits and cereals are NOT included

• Bakery product definitions are standardised in each country, which is the only way to ensure international comparability

� Products differentiated at consumer level : fresh (un-packed or packed at the point of sales, shelf-life 1-2 days), prepacked long-life (packed at industrial level, branded, shelf-life over 2 days), prepacked for home-baking (needs final baking/thawing at home)

� Production methods : artisanal scratch production (on the premises), industrial production (prepacked, fresh finished, bake-off).

2.2 DISTRIBUTION CIRCUITS

� Retail channels : artisan bakers and confectionery shops, modern retailers and hard-discounters, bakery chains, petrol stations and convenience stores, small grocery stores

� Catering channels : commercial sector (restaurants, hotels, fast-food, transport and leisure), social sector (staff catering, education, health).

2.3 GEOGRAPHIC SCOPE

Country Reports for each member of the EU-27 +Turkey , accompanied by a Pan-EU Summary and Synthesis.

2.4 TIME HORIZON

� Historical series: 2001-2010

� Current situation 2011 and 2012(e)

� 2016 forecasts.

3. Scope: research coverage

10

4. Structure and Contents of the Report

The Report consists of the following sections: (with page numbers)A) EU Synthesis 107 pagesB) EU-27 Country Reports + Turkey 553 pagesC) Profiles of the top 96 Bakery Companies 460 pages

The Pan-EU Synthesis� Bakery products and bakery companies News – all the major events affecting the EU bakery chain since 2008� Market context: Summary tables: EU consumption, distribution, supply methods and production tables – including 2016 forecasts� Price graphs: by product and by country� Top EU industrial bakery groups League Tables: ranked by overall turnover and by technology (fresh, prepacked, bake-off).

Country Reports (35-40 pages)

1. Highlights� Key figures� Recent structural developments and outlook

2. Background� Demographics and economy� Food consumption trends� Distribution overview

3. Bread� Bread consumption dynamics� Bread distribution channels – total and fresh� Bread supply structure – total and fresh

4. Viennoiserie : as above5. Patisserie : as above6. Savoury pastry snacks : as above7. Structure of the industrial bakery sector� Industrial production� Key operators.

Tables and Figures� Economic background – 2001-2011 & 2012(f)� Distribution channels – 2011, 2006 & 2011� Main modern retailers - 2011� Bakery products consumption – 2001-2011, 2012(e) & 20116 (f)� Bakery products consumption by product and by technology� Total bakery products distribution channels – 2011 & 2016(f)� Fresh bakery products distribution channels – 2011 & 2016(f)� Total bakery products supply structure – 2001-2011, 2012(e) & 2016 (f)� Share of bake-off in fresh bakery products consumption – 2011 & 2016(f)

=> Tables and figures as above for:� Bread� Viennoiserie� Patisserie� Savoury pastry

Industrial production:� Industrial bakery products production – 2011 & 2016(f)� Top industrial bakery products producers - 2011

11

Report structure:Contents of the Profiles

Profiles of all the Major EU Bakery Companies (2-3 pages each)

96 of the largest European Bakery companies have been profiled.

Each profile comprises the following elements (where available):

1. Basic information

� Address� Key officers

2. Company background

� Ownership and management structure� Brief historical comments

3. Bakery products activities

� Manufacturing activity by type of bakery product and technology (fresh, prepacked, bake-off)

� Product range, technologies and innovation� Distribution channels and export activity

4. Financial overview

5. Main recent events

6. Apparent strategy.

12

Report Structure: The top 96 EU companies profiled

There follows the list of companies that have been profiled in the current edition of the Panorama.

Company Country

Délifrance IT

Dobrudjanski Hliab BG

Dulcesol ES

Edeka DE

Edna International DE

Elbisco EL

Erlenbacher Backwaren DE

Europastry ES

Européenne des Desserts FR

Fazer FI

Ferrero IT

Finsbury UK

Fletchers Bakeries UK

Fornetti HU

Forns Valencians ES

Greggs UK

Grupo Siro ES

Gunnar Dafgard SE

Hanzas Maiznīca LV

Harry Brot DE

Harry's FR

Haubenberger AT

Hiestand PL

Hiestand & Suhr DE

Company Country

IHE TK

Inter Europol PL

Interpan IT

Irish Pride Bakeries IE

Jacquet-Brossard FR

Joseph Brennan Bakeries IE

Klemme DE

Kohberg Brod DK

La Lorraine BE

La Lorraine CZ

La Lorraine Polska PL

Lanterna Alimentari IT

Lantmännen Unibake BE

Lantmännen Unibake DK

Lantmännen Unibake PL

Lieken DE

Lotus Bakeries BE

Lu FR

Mamut PL

Maple Leaf UK

Michelske Pekarny CZ

Müller Brot DE

Neuhauser - BCS FR

Nutriart EL

Company Country

Ölz Meisterbäcker AT

Oskroba PL

Pågen SE

Pan Star ES

Panavi Vandemoortele FR

Panrico PT

Panrico ES

Penam CZ

Penam SK

Sammontana IT

Simid-1000 BG

Smilde Bakery NL

Ströck Brot AT

Two Sisters UK

United Bakeries CZ

United Bakeries SK

Uno Bakery Corporation TK

Vaasan FI

Vamix CZ

Vandemoortele BE

Vel Pitar RO

Warburtons UK

Wewalka AT

Žito SI

Company Country

Allied Bakeries UK

Ankerbrot AT

Bake Five NL

Bakkersland NL

Barilla IT

Bauli IT

Bellsolà ES

Berlys Alimentacion ES

Bimbo Iberia ES

Bindi IT

Bridor FR

Brioche Pasquier FR

British Bakeries UK

Ceres HU

Chipita EL

Coppenrath & Wiese DE

CSM UK

CSM Benelux BE

CSM Iberia ES

Cuisine de France IE

Dan Cake PT

Dan Cake PL

Delifrance UK

Delifrance FR

13

5. Gira and the Gira Team

Gira has been researching European bakery markets a nd industries on a continuous basis since 1978. Our research has included:

� Major multi client programmes all along the bakery supply chain: e.g. Bakery Markets in the EU, BVP and BVP Company Panorama, Bakery Strategies in Modern Retail, Bakery Ingredients, etc.

� Bake-off Survey forecast and analyses; normally repeated every 5 years (last updated in Dec 2010)

� A wide variety of proprietary consultancy mandates, in all products and on all aspects of the bakery chain

All of this is enriched by Gira’s ongoing work in other food sectors, and particularly dairy, and by its consulting and research in the areas of consumer preferences, health, retail and catering.

We have an unrivalled data bank on bakery markets, and most of the large bakery companies and bakery associations have been clients of our research programmes, giving Gira access to key industry players throughout Europe.

For the Panorama, Gira has supplemented this knowledge with extensive trade interviews and desk and online research.

Staffing:

The Gira team was supervised by Anne Fremaux, the Director responsible for all of Gira’s bakery research projects and well-known for her expertise throughout the European bakery sector.

Our team consisted of Gira consultants with wide experience in the bakery sector, retail and catering, each of whom knows well the individual country market for which he/she is responsible. Many of the team also worked on the 2007 edition of the Panorama and on the 2010 edition of the Bake-off survey.

14

6. Price, Reports and Follow Up

Price

The subscription price is Euros 9 800 (before any applicable taxes).

This price includes an update Newsletter, to be published a year after the Panorama appears and underlining the main events since the publication of the Panorama.

Reports

Published November 2012.

The report is in English.

Clients receive one USB key version of the report.

Hard copies are available at a cost of Euros 250 per copy.

Follow Up

Gira will be pleased to make a tailored, half-day presentation of the findings and conclusions of the Panorama for clients in their offices in Europe, at a cost of Euros 2 000 (before any tax) plus travel expenses.

15

7. A sample of Gira’s ‘blue-chip’ clients in the bakery sector

AB-Mauri IE Délifrance FR Monoprix FRAIBI Duke Street Capital FR Nederlands Bakkerij Centrum NLAIT FR Dupont de Nemours CH Nestlé France FR

Ancel FR EDF FR Neuhauser BCS FRAoste FR Europain FR Nudespa ESAryzta CH Europastry ES Nutrixo FR

Asemac ES European Flour Milling Association Oetker DEAt-Kearney FR European Union Pagen SE

Atlas Advisors UK Européenne des Desserts FR Panotel FRAxa Asset Management FR Fazer FI Pan-Star ES

Bellsola ES Ferrero FR Pasquier FRBerly's ES Fortis Private Equity BE Pastisart ES

Bimbo Sara Lee Group ES Friesland Campina NL Puratos BEBongrain FR GB-Plange FR Phil Savours FR

Boston Consulting Group USA Grands Moulins de Paris FR Pomona FRBridor FR Holder-Château Blanc FR Qualium FR

Carrefour FR Ingredion DE Quartz+Co NOCeres HU Intermarché FR Rabobank NL

Chequers Capital FR Ipasa ES Rhodia FRCIBC USA JBT Food Tech SE Rich Products Corp. USACLFS FR Kerry Ravifruits FR Sasa Industries FRCMA DE Kraft Foods FR Smilde Bakery NL

CNIEL FR Lantmännen Unibake DK Sofrapain FRConfédération de la Boulangerie FR Leclerc Galec FR Système U FR

Copaline FR Lesaffre FR Transgourmet FRCorman BE Lieken DE Unifine Food and Bake DE

Coup de Pâtes FR Limagrains FR Unigrains FRCredit Suisse UK Lion Capital UK Vaasan FI

CSM Bakery Supplies NL LLI Euromills AT Valora CHDanisco FR Mapple Leaf Foods CA Vandemoortele BEDanone FR Mc Key Holdco FR Weinberg Capital FR

Dawn Foods NL Mecatherm FR Yamazaki Baking JPDelices du Palais FR Mitsui & co Benelux BE Zeelandia NL

16

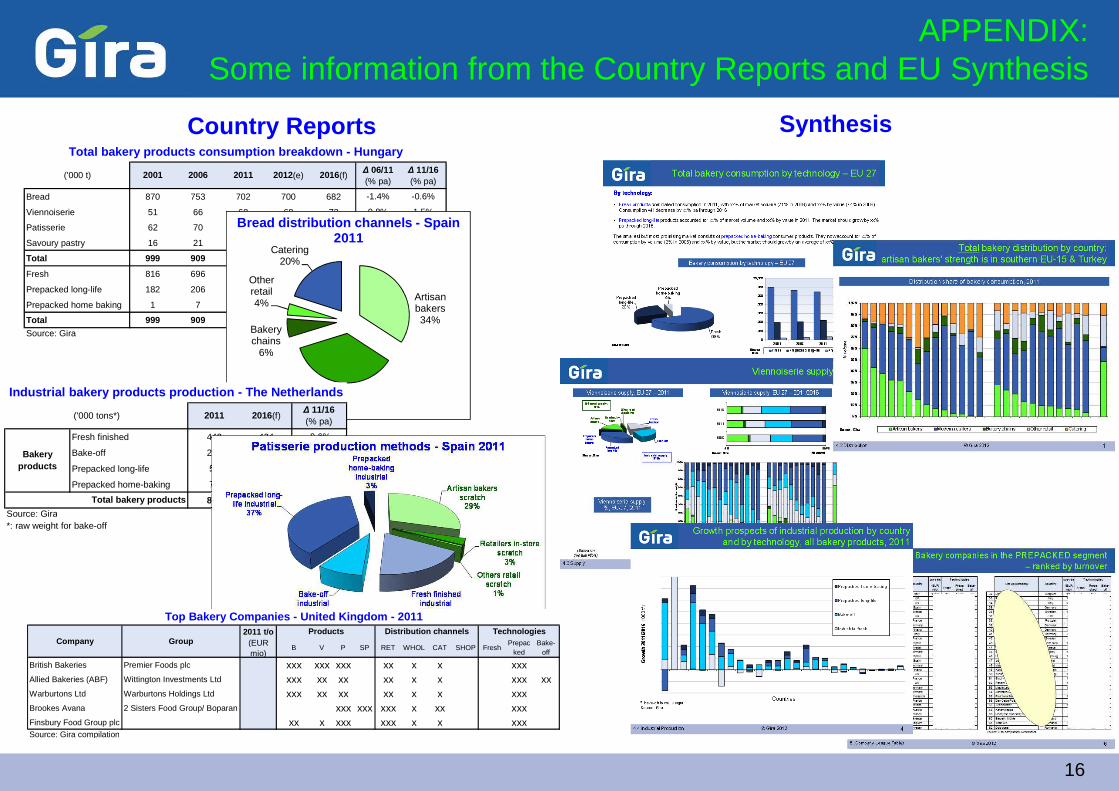

APPENDIX: Some information from the Country Reports and EU Synthesis

Country Reports Synthesis

∆ 06/11 ∆ 11/16(% pa) (% pa)

Bread 870 753 702 700 682 -1.4% -0.6%

Viennoiserie 51 66 68 68 73 0.8% 1.5%

Patisserie 62 70 68 67 72 -0.4% 1.0%

Savoury pastry 16 21 23 23 26 1.7% 2.4%

Total 999 909 862 859 853 -1.1% -0.2%

Fresh 816 696 627 627 593 -2.1% -1.1%

Prepacked long-life 182 206 225 223 249 1.8% 2.0%

Prepacked home baking 1 7 10 10 12 6.3% 4.1%

Total 999 909 862 859 853 -1.1% -0.2%Source: Gira

Total bakery products consumption breakdown - Hunga ry

2011 2012(e) 2016(f)('000 t) 2001 2006

Artisan bakers34%

Modern retailers

36%

Bakery chains

6%

Other retail4%

Catering20%

Source: Gira

Bread distribution channels - Spain 2011

∆ 11/16(% pa)

Fresh finished 448 434 -0.6%

Bake-off 285 323 2.6%

Prepacked long-life 52 54 0.7%

Prepacked home-baking 70 78 2.2%

856 890 0.8%Source: Gira*: raw weight for bake-off

Total bakery products

Industrial bakery products production - The Netherl ands

Bakery products

('000 tons*) 2011 2016(f)

2011 t/o(EUR mio)

B V P SP RET WHOL CAT SHOP FreshPrepac

kedBake-

off

British Bakeries Premier Foods plc 880 xxx xxx xxx xx x x xxxAllied Bakeries (ABF) Wittington Investments Ltd 550 xxx xx xx xx x x xxx xxWarburtons Ltd Warburtons Holdings Ltd 575 xxx xx xx xx x x xxxBrookes Avana 2 Sisters Food Group/ Boparan 227 xxx xxx xxx x xx xxxFinsbury Food Group plc 220 xx x xxx xxx x x xxxSource: Gira compilation

Company GroupProducts Distribution channels Technologies

Top Bakery Companies - United Kingdom - 2011