The competitive landscape of IoTCompetitive forces and companies shaping the Internet of Things

Vienna Global IoT Day, 9 April 2015

Knud Lasse Lueth, Founder of IoT Analytics @KnudLueth

@AnalyticsIoT

1

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Agenda

Introduction

Part 1: How IoT changes competitive forces

Part 2: The companies and technologies making IoT happen

2

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Starting point: The internet changed our lives

In 1994, the Internet was the next

big thing…

Time Magazine Cover 1994

Source: Time Magazine, Wikipedia

3

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Starting point: The internet changed our lives

In 1994, the Internet was the next

big thing…

… and created a whole new

industry

Time Magazine Cover 1994 List of biggest Internet companies 2014Source: Time Magazine, Wikipedia

# Company Headquarters IndustryRevenue

($B)

1 Amazon Seattle, WA E-commerce $74.45

2 Google Mountain View, CA Search $59.82

3 eBay San Jose, CA E-commerce $16.05

4 Tencent Shenzhen Social $9.91

5 Alibaba Hangzhou E-commerce $8.57

6 Facebook Menlo Park, CA Social $7.87

7 Rakuten Tokyo E-commerce $5.56

8 Priceline.com Norwalk, CT Travel $5.26

9 Baidu Beijing Search $5.21

10 Yahoo Sunnyvale, CA Web portal $4.68

11 Salesforce.com San Francisco, CA Cloud comp. $4.07

12 Yandex Moscow Search $1.21

13 Flipkart Bangalore E-commerce $1+

4

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

How will IoT change our lives?

In 2014, the Internet of Things

has arrived…

HBR Cover 2014

Source: HBR, IoT Analytics

5

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

How will IoT change our lives?

In 2014, the Internet of Things

has arrived…

Who will dominate the industry

in 20 years?

HBR Cover 2014

Source: HBR, IoT Analytics

IoT Analytics tries to understand: What

determines IoT success and who is it?

6

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

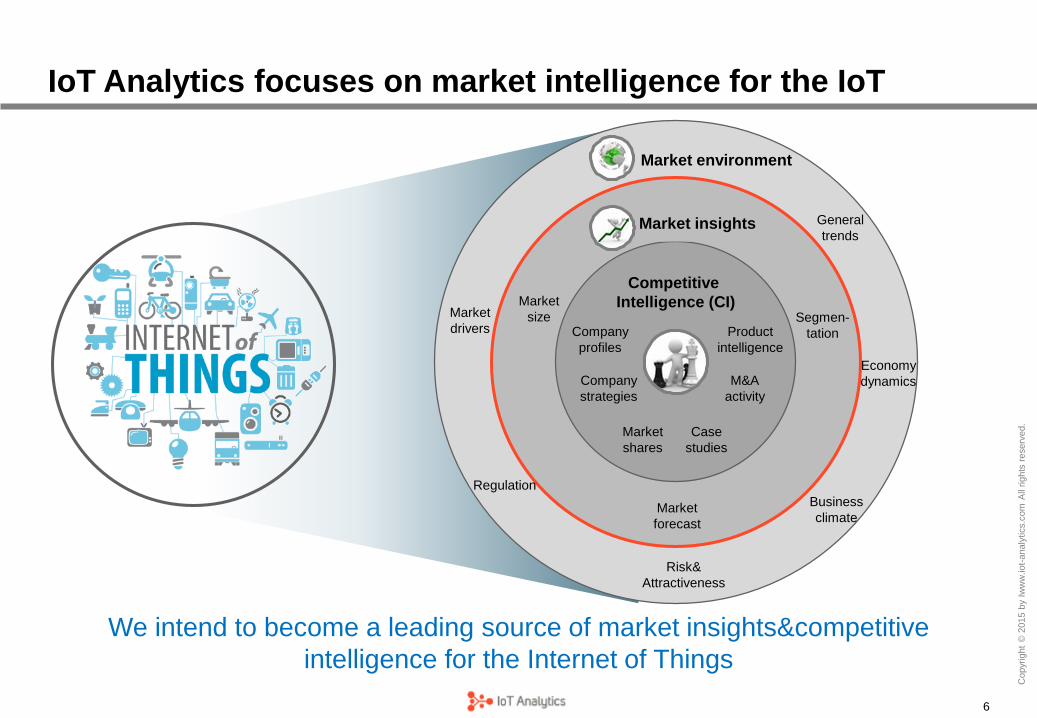

IoT Analytics focuses on market intelligence for the IoT

Competitive

Intelligence (CI)

Market environment

Market insights General

trends

Business

climate

Risk&

Attractiveness

Market

drivers

Economy

dynamics

Market

size

Regulation

Market

forecast

Segmen-

tation

Company

strategies

Company

profiles

M&A

activity

Case

studies

Market

shares

Product

intelligence

We intend to become a leading source of market insights&competitive

intelligence for the Internet of Things

7

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

A few of our recent publications and current work

Intro to IoT IoT market analysis Smart Home primer IoT strategy primer

White papers Case studies

The Nest story

(not yet published)

Structured company lists Market share analysis

2000+ IoT

companies

350+ Smart Home

companies250+ Wearables

companies

300+ publicly listed

IoT companiesCompany popularity

ranking

Bottom-up

Smart Home

market share model

(not yet published)

www.iot-analytics.com

8

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Agenda

Introduction

Part 1: How IoT changes competitive forces

Part 2: The companies and technologies making IoT happen

9

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Most value of IoT lies beyond the connectivity

Value (to the end customer)

high

high

low

low

1 “Dumb”Physical device/product

3 MonitoredRemote conditionmonitoring

4 ControlledRemote control of device/product

5 OptimizedAlgorithms,Decision-support, additional services, etc.

6 AutonomousSelf-coordinationAutomated decision-making

7 Ecosystem-enabledSmart interactionwith other smart objectsIn same ecosystem

2 DigitalDigitally-enableddevice/product

8 Cross-Ecosystem OptimizedSmart interaction With devices in other ecosystems

Maturity (of the offering)

The IoT value-maturity curve

Connected deviceNon-connected device

10

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Do you know Nest?

One of the most mature early examples of a “dumb” product becoming “smart”

11

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Would you buy it today?

Nest vs. conventional thermostats 2014

Reasons NOT to

buy Nest

Reasons to buy

Nest

12

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Would you buy it in 2 years?

Nest vs. conventional thermostats 2016 (forecast)

Reasons NOT to

buy Nest

Reasons to buy

Nest

13

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Most of the value for Nest has not yet been unlocked

Value (to the end customer)

high

high

low

low

1 “Dumb”

3 Monitored4 Controlled

5 Optimized.

6 Autonomous

7 Ecosystem-enabled

2 Digital

8 Cross-Ecosystem optimized

Maturity (of the offering)

Manual Thermostat

1883

DigitalThermostat

1980s

AutonomousThermostat

2011-14

Ecosystem thermostat2016?

Nest today

Connected deviceNon-connected device

14

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

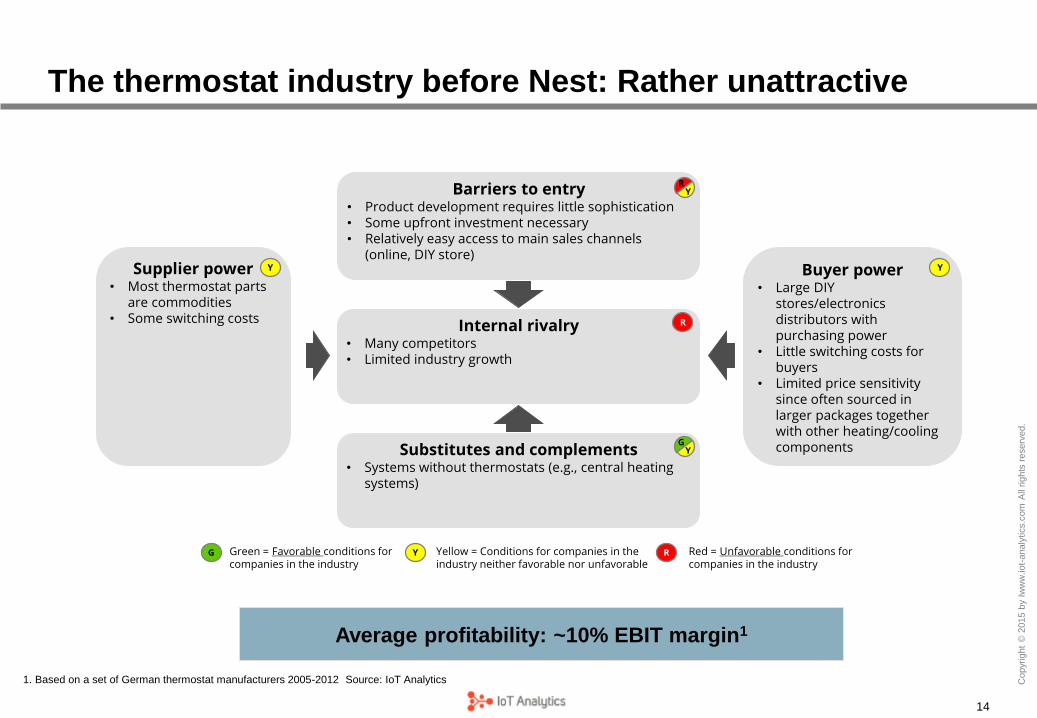

The thermostat industry before Nest: Rather unattractive

G Y RGreen = Favorable conditions for companies in the industry

Barriers to entry• Product development requires little sophistication• Some upfront investment necessary• Relatively easy access to main sales channels

(online, DIY store)

Internal rivalry• Many competitors• Limited industry growth

Substitutes and complements• Systems without thermostats (e.g., central heating

systems)

Supplier power• Most thermostat parts

are commodities• Some switching costs

Buyer power• Large DIY

stores/electronics distributors with purchasing power

• Little switching costs for buyers

• Limited price sensitivity since often sourced in larger packages together with other heating/cooling components

Yellow = Conditions for companies in the industry neither favorable nor unfavorable

Red = Unfavorable conditions for companies in the industry

YG

Y Y

R

YR

Average profitability: ~10% EBIT margin1

1. Based on a set of German thermostat manufacturers 2005-2012 Source: IoT Analytics

15

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

After the arrival of smart thermostats:

IoT changes the industry forces

Average profitability: Likely higher in the future!

Source: IoT Analytics

G Y RGreen = Favorable conditions for companies in the industry

Barriers to entry• Complex product development • Significant upfront investment in product and

talent• Relatively easy access to main sales channels

(online, DIY store)• Learning from own captured data

Internal rivalry• Many competitors• High industry growth

Substitutes and complements• Systems without thermostats (e.g., central heating

systems)

Supplier power• Most thermostat parts

are commodities• Some switching costs

Buyer power• Large DIY

stores/electronics distributors with purchasing power

• High switching costs for buyers due to existing smart home ecosystem

• Limited price sensitivity since often sourced in larger packages together with other heating/cooling components

Yellow = Conditions for companies in the industry neither favorable nor unfavorable

Red = Unfavorable conditions for companies in the industry

YG

Y

Y

G

YG

16

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Agenda

Introduction

Part 1: How IoT changes competitive forces

Part 2: The companies and technologies making IoT happen

17

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

The new technology landscape of the Internet of Things (1/4)

18

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

The new technology landscape of the Internet of Things (2/4)

19

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

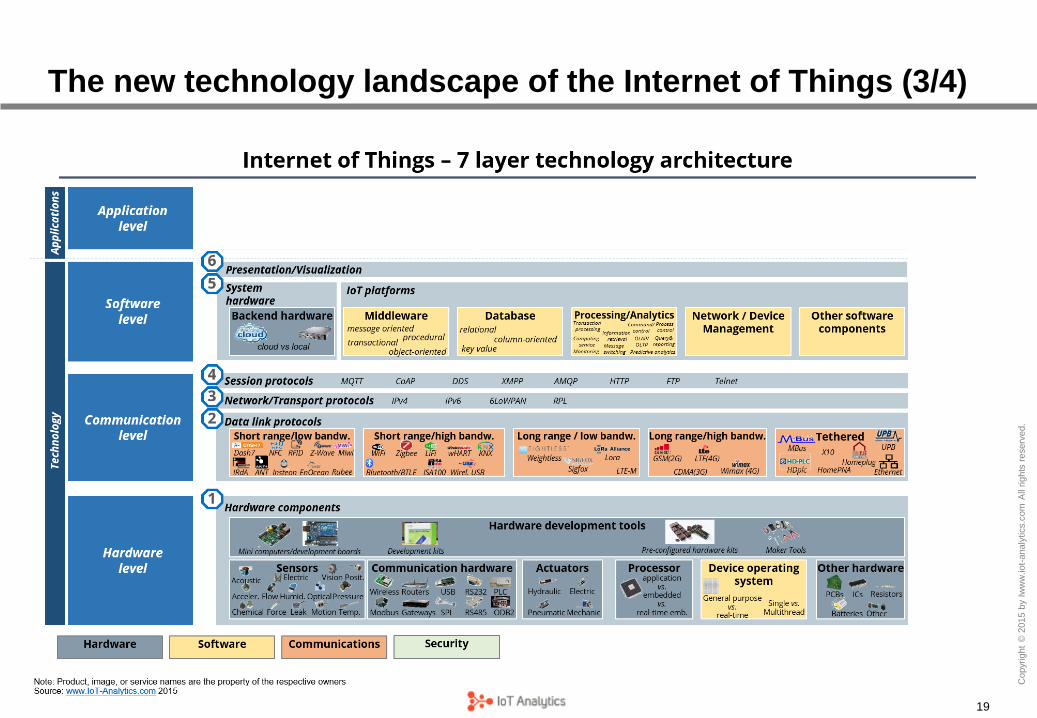

The new technology landscape of the Internet of Things (3/4)

20

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

The new technology landscape of the Internet of Things (4/4)

21

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

The top 10 IoT companies creating the biggest buzz

3

2

1

4

5

6

7

8

9

10

Company Overall popularity1 Specific products

1. Popularity ranking based on popularity in Google searches, Twitter tweets, LinkedIn posts, and news headlines in Q1/2015. 2. Com. Hardw = Communication hardware 3. M2M platform in

partnership with other companies

Source: Google, Twitter, LinkedIn, Company websites, IoT Analytics

22%

24%

26%

31%

34%

55%

59%

66%

69%

72%

Oracle

Gartner

SAP

Apple

Samsung

IBM

Cisco

Microsoft

Intel

• IoT-enabled ERP• Hana database• M2M platform3

Technology offering2

Sen-

sors

Proce

ssors

Com.

hardw

De-

vices

Plat-

form

Ana-

lytics

Data-

base Other

✓ ✓

✓ ✓✓

✓ ✓

✓ ✓

✓✓ ✓

✓ ✓

✓

✓ ✓ ✓ ✓

• IoT cloud platform

• Market research

• Wearables• Smart Home platform

• Processors• Gilileo developer kit• IoT platform

• Azure platform• Streaming analytics• Wearable camera

• Smart watch• Smart home platform• Smart health platf.

• Routers/Gateways/etc• Security solutions

• Analytics• Databases (eg Cloudant)• Application infrastr.

• Nest/Revolv smart home• Physical web platform• Google Glass• Self-driving car

✓

( )

✓ ✓

✓ ✓

22

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Biggest US startups much larger than Austrian counterparts Top IoT startups by country

Name Segment Location Funding

Jawbone Wearables San Francisco $520m

Prodea

Syst.

Smart home Richardson, TX $160m

iRhythm Connected

health

San Francisco $120m

Nest Labs Smart home Palo Alto $80m

Name Segment Location Funding

AlertMe Smart home Cambridge $36m

Electric-

imp

Smart home Cambridge $23m

Roli Conn. music London $13m

Evrythng IoT platform London $7m

Name Segment Location Funding

Tado Smart home Munich $16m

Yetu Smart home Berlin $8m

Relayr Dev. board Berlin $3m

Gestigon Gesture contr. Lübeck $1m

Name Segment Location Funding

Flatout Smart home Vienna $1m

Tractive Wearables Pasching $0.5m

Linemetrics Industrial Haidershofen $0.4m

Indoo.rs Indoor

localization

Brunn am

Gebirge

n/a

23

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Conclusion

1. The value of the Internet of Things lies beyond the connectivity – It comes with smart

analytics and ecosystem-enablement

2. Entire industry forces are changing due to IoT. Some industries may experience higher

profits. Companies need to be aware of potential lock-out.

3. The “new” IoT infrastructure is being created now – Hardware including sensors and

processors, communication, software, and application.

4. The top IoT companies in terms of “share-of-voice” currently are: Intel, Microsoft, Cisco,

Google, IBM

5. US startup funding in the IoT area is much larger than German or Austrian IoT investment

activity

24

Copyr

ight

© 2

015 b

y Iw

ww

.iot-

analy

tics.c

om

All

rights

reserv

ed.

Questions?

Knud Lasse Lueth

IoT Analytics

www.iot-analytics.com

Hamburg/Berlin

Germany

@KnudLueth

@AnalyticsIoT