9/28/2016

1

The Great Plunge in Oil Prices:Causes, Consequences and Policy Responses

September 28, 2016

M. Ayhan [email protected]

Disclaimer! The views presented in this presentation are those of the authors and do not necessarily reflect the views of the World Bank Group or World Bank Policy.

• Global Economic Prospects – January 2017 (January and June)

• Commodity Markets Outlook – October 2016(January, April, July, and October)

• Global Monthly, Global Weekly, and Global Daily

• Negative Interest Rate Policies: Sources and Implications Arteta, Kose, Stocker and Taskin, Policy Research Working Paper – August 2016

Select Publications on Global Economy

2

9/28/2016

2

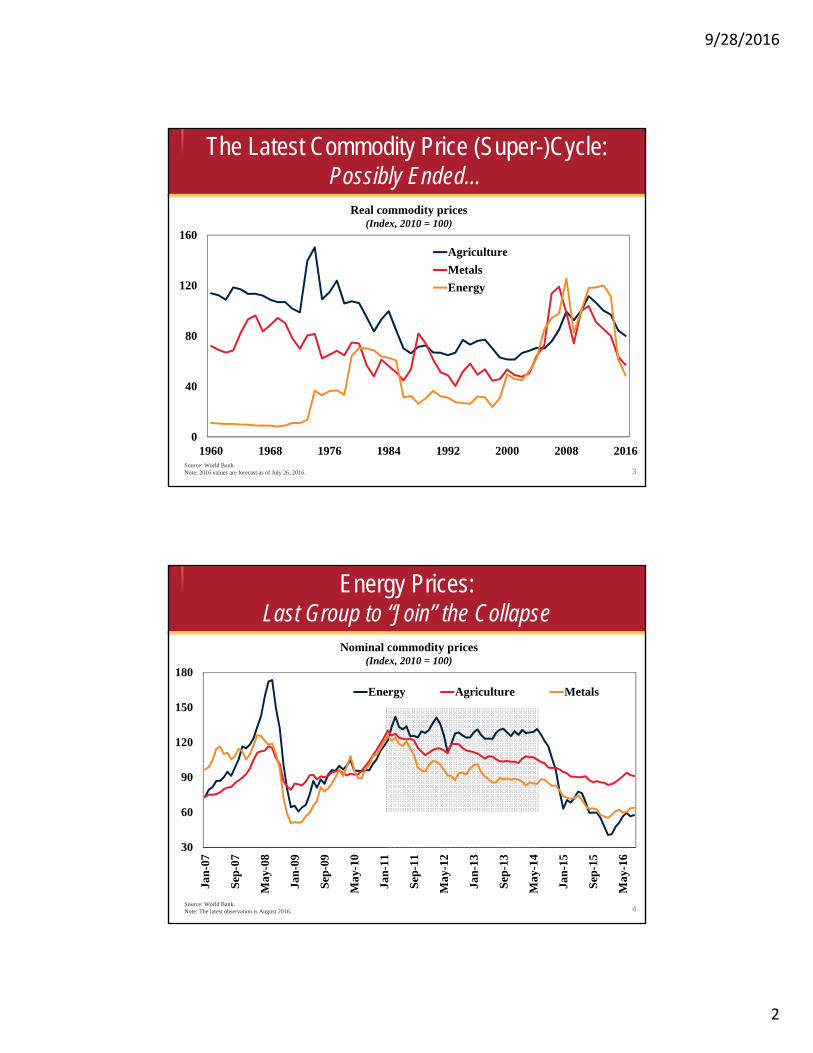

Real commodity prices(Index, 2010 = 100)

Source: World Bank.Note: 2016 values are forecast as of July 26, 2016.

The Latest Commodity Price (Super-)Cycle:Possibly Ended…

3

0

40

80

120

160

1960 1968 1976 1984 1992 2000 2008 2016

Agriculture

Metals

Energy

Nominal commodity prices(Index, 2010 = 100)

Source: World Bank.Note: The latest observation is August 2016.

Energy Prices:Last Group to “Join” the Collapse

4

30

60

90

120

150

180

Jan

-07

Sep

-07

May

-08

Jan

-09

Sep

-09

May

-10

Jan

-11

Sep

-11

May

-12

Jan

-13

Sep

-13

May

-14

Jan

-15

Sep

-15

May

-16

Energy Agriculture Metals

9/28/2016

3

Commodity price changes(Percent, change from 2011Q1 to 2014Q2)

Source: World Bank.Right Panel. Fraction of commodities (out of a total of almost 50 commodities) for which prices declined from the previous year.

Commodity Prices:Resilient Oil Prior to 2014:2; But Then..

5

-60-50-40-30-20-10010

CottonCoal

SilverNickel

CopperAluminum

RiceTin

LeadPlatinum

ZincCocoa

GoldTea

WheatCrude oil

Commodities with lower prices from previous years

(Percent, share of commodities)

0

20

40

60

80

100

2009 2010 2011 2012 2013 2014 2015

Maximum 1980-2008

Minimum 1980-2008

Four Questions

1 What has been the role of supply?Looks like played a major role

2

3

What has been the role of demand?Somewhat smaller role but..

6

What has been the driving force behind the collapse in oil prices?Mostly supply…

4 What are the implications for commodity-exporters?Weak growth in commodity-exporters; stronger policy support needed…

9/28/2016

4

20

50

80

110

140

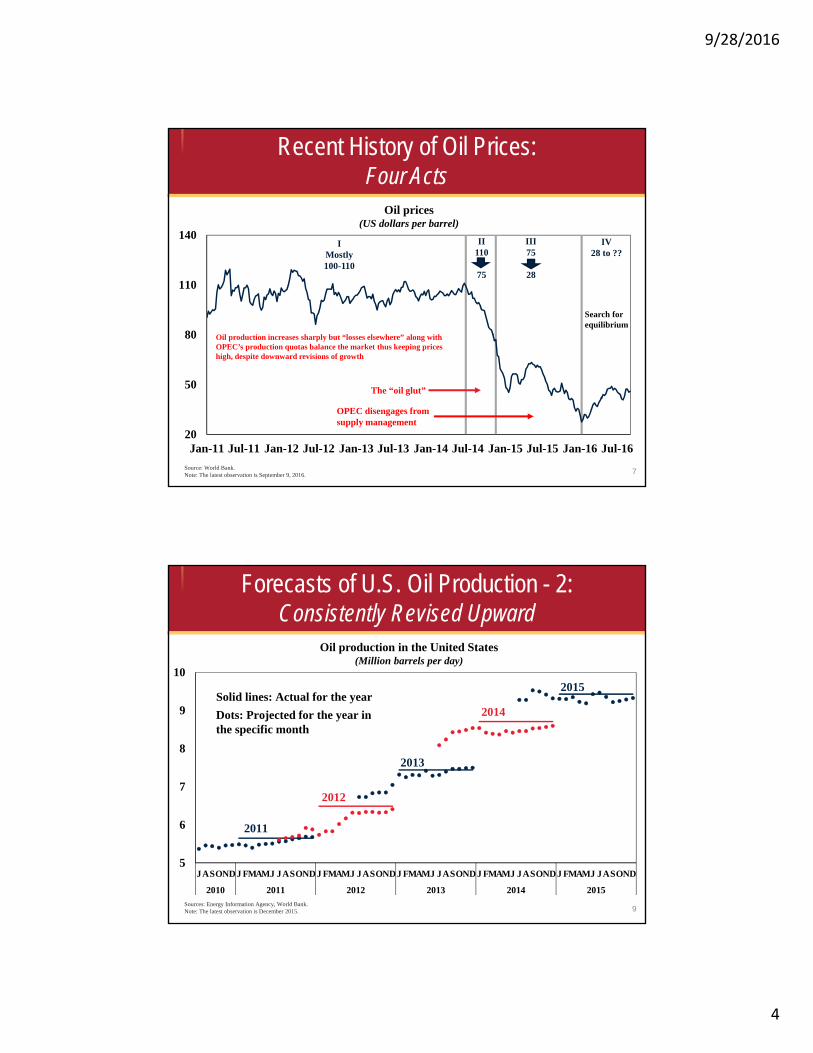

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

IMostly 100-110

Oil prices(US dollars per barrel)

Source: World Bank.Note: The latest observation is September 9, 2016.

Recent History of Oil Prices:Four Acts

7

II110

75

Oil production increases sharply but “losses elsewhere” along with OPEC’s production quotas balance the market thus keeping prices high, despite downward revisions of growth

The “oil glut”

OPEC disengages from supply management

Search for equilibrium

III75

28

IV28 to ??

Oil production in the United States(Million barrels per day)

Sources: Energy Information Agency, World Bank.Note: The latest observation is December 2015.

Forecasts of U.S. Oil Production - 2:Consistently Revised Upward

9

5

6

7

8

9

10

JASONDJ FMAMJ JASONDJ FMAMJ JASONDJ FMAMJ JASONDJ FMAMJ JASONDJ FMAMJ JASOND

2010 2011 2012 2013 2014 2015

2011

2012

2014

2013

2015Solid lines: Actual for the year

Dots: Projected for the year in the specific month

9/28/2016

5

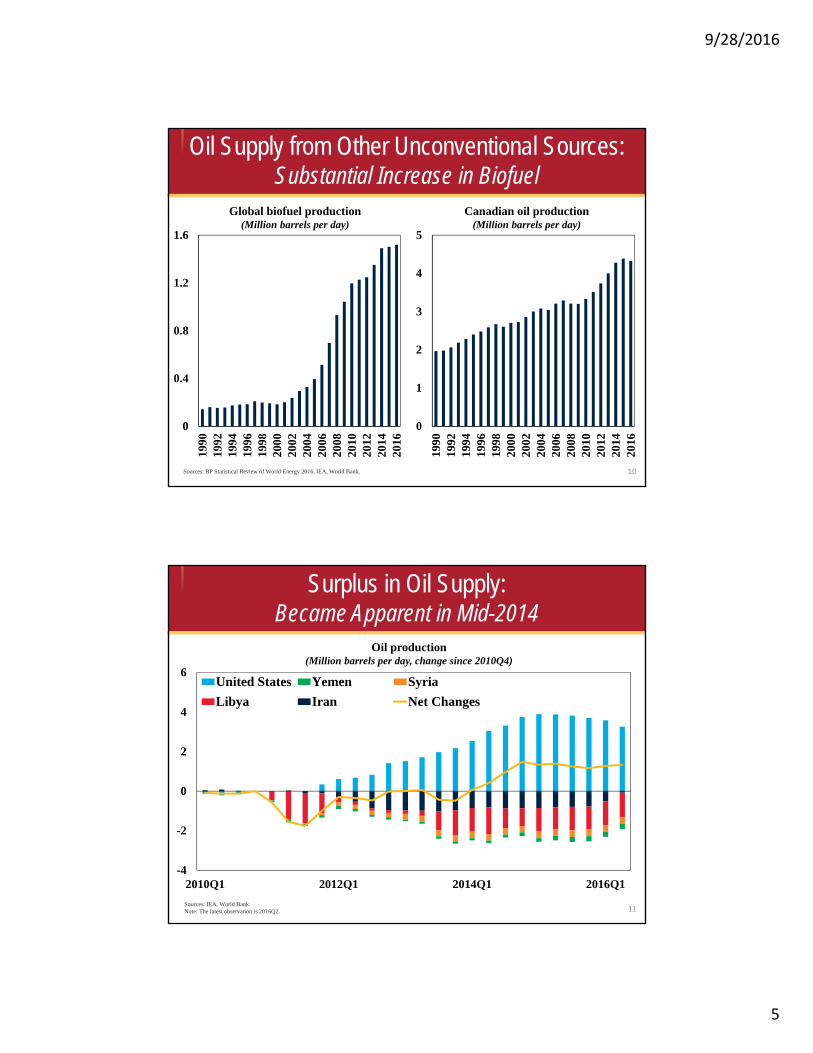

Global biofuel production(Million barrels per day)

Oil Supply from Other Unconventional Sources:Substantial Increase in Biofuel

Sources: BP Statistical Review of World Energy 2016, IEA, World Bank. 10

Canadian oil production(Million barrels per day)

0

0.4

0.8

1.2

1.6

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0

1

2

3

4

5

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

Oil production(Million barrels per day, change since 2010Q4)

Sources: IEA, World Bank.Note: The latest observation is 2016Q2.

Surplus in Oil Supply:Became Apparent in Mid-2014

11

-4

-2

0

2

4

6

2010Q1 2012Q1 2014Q1 2016Q1

United States Yemen Syria

Libya Iran Net Changes

9/28/2016

6

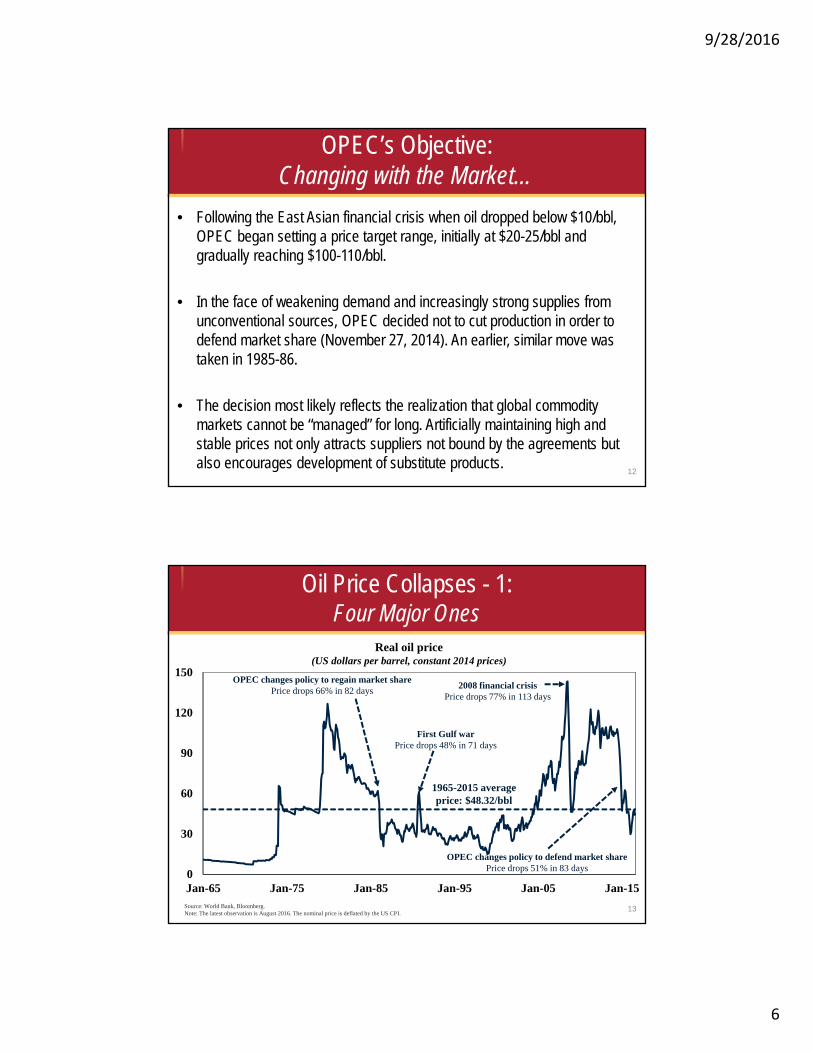

OPEC’s Objective:Changing with the Market…

12

• Following the East Asian financial crisis when oil dropped below $10/bbl, OPEC began setting a price target range, initially at $20-25/bbl and gradually reaching $100-110/bbl.

• In the face of weakening demand and increasingly strong supplies from unconventional sources, OPEC decided not to cut production in order to defend market share (November 27, 2014). An earlier, similar move was taken in 1985-86.

• The decision most likely reflects the realization that global commodity markets cannot be “managed” for long. Artificially maintaining high and stable prices not only attracts suppliers not bound by the agreements but also encourages development of substitute products.

Real oil price(US dollars per barrel, constant 2014 prices)

Source: World Bank, Bloomberg.Note: The latest observation is August 2016. The nominal price is deflated by the US CPI.

Oil Price Collapses - 1:Four Major Ones

13

0

30

60

90

120

150

Jan-65 Jan-75 Jan-85 Jan-95 Jan-05 Jan-15

1965-2015 average price: $48.32/bbl

2008 financial crisisPrice drops 77% in 113 days

OPEC changes policy to regain market sharePrice drops 66% in 82 days

First Gulf warPrice drops 48% in 71 days

OPEC changes policy to defend market sharePrice drops 51% in 83 days

9/28/2016

7

Real oil price(US dollars per barrel, constant 2014 prices)

Source: World Bank, Bloomberg.Note: The latest observation is August 2016. The nominal price is deflated by the US CPI.

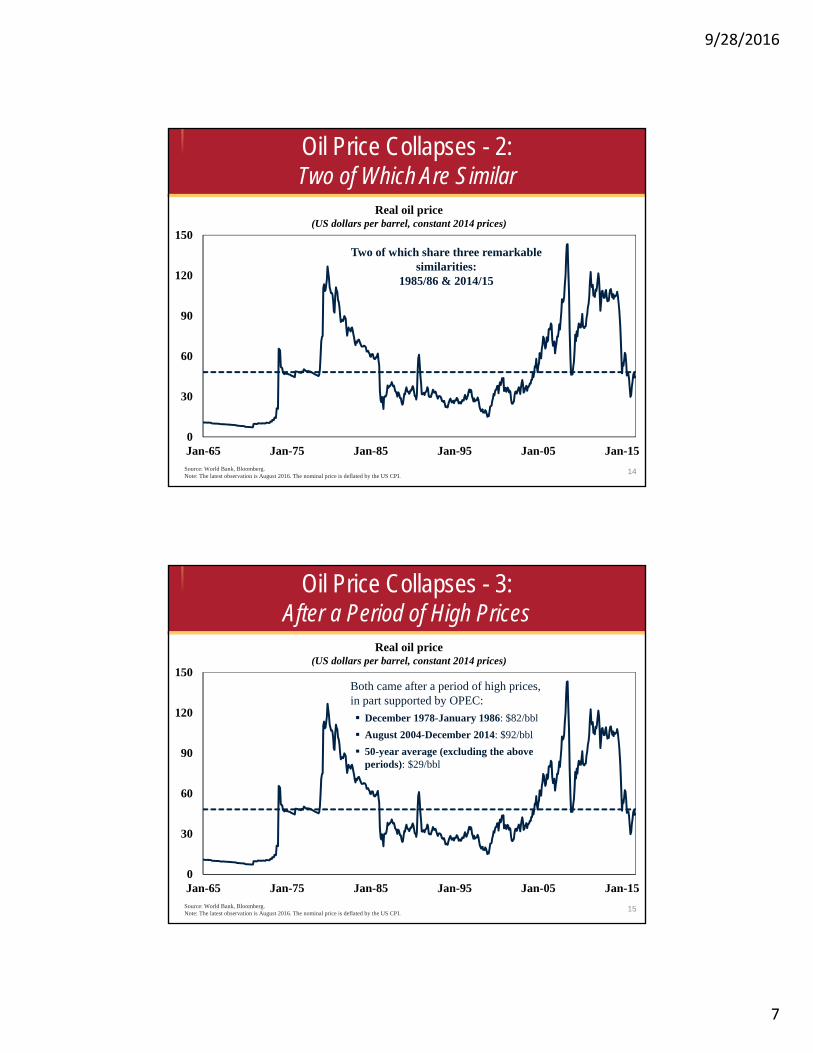

Oil Price Collapses - 2:Two of Which Are Similar

14

0

30

60

90

120

150

Jan-65 Jan-75 Jan-85 Jan-95 Jan-05 Jan-15

Two of which share three remarkable similarities:

1985/86 & 2014/15

Real oil price(US dollars per barrel, constant 2014 prices)

Source: World Bank, Bloomberg.Note: The latest observation is August 2016. The nominal price is deflated by the US CPI.

Oil Price Collapses - 3:After a Period of High Prices

15

0

30

60

90

120

150

Jan-65 Jan-75 Jan-85 Jan-95 Jan-05 Jan-15

Both came after a period of high prices, in part supported by OPEC:

December 1978-January 1986: $82/bbl

August 2004-December 2014: $92/bbl

50-year average (excluding the above periods): $29/bbl

9/28/2016

8

Real oil price(US dollars per barrel, constant 2014 prices)

Source: World Bank, Bloomberg.Note: The latest observation is August 2016. The nominal price is deflated by the US CPI.

Oil Price Collapses - 4:New Supplies Brought by High Prices

16

0

30

60

90

120

150

Jan-65 Jan-75 Jan-85 Jan-95 Jan-05 Jan-15

In both periods, high oil prices brought new oil supplies:

Prior to 1985/86: (i) Alaska, (ii) North Sea, and (iii) Gulf of Mexico (brought 5 mb/d in the 8 years prior to the collapse, 9% of world total)

Prior to 2014/15: (i) Biofuels, (ii) Canadian oil sands, and (iii) U.S. shale oil (brought 7 mb/d in the decade prior to the collapse, 8% of world total)

Real oil price(US dollars per barrel, constant 2014 prices)

Source: World Bank, Bloomberg.Note: The latest observation is August 2016. The nominal price is deflated by the US CPI.

Oil Price Collapses - 5:…and OPEC Responses

17

0

30

60

90

120

150

Jan-65 Jan-75 Jan-85 Jan-95 Jan-05 Jan-15

In both cases, OPEC disengaged from managing supplies exacerbating the price collapse--delayed response in 1985, quick action in 2014.

9/28/2016

9

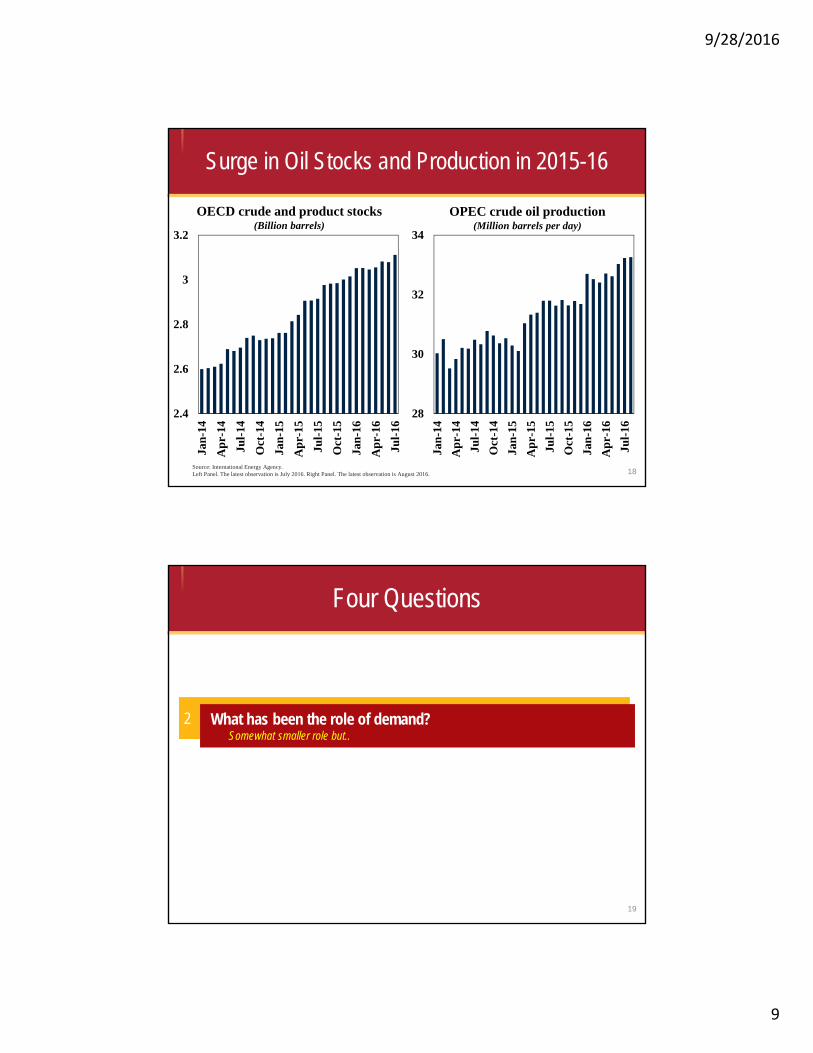

Source: International Energy Agency.Left Panel. The latest observation is July 2016. Right Panel. The latest observation is August 2016.

Surge in Oil Stocks and Production in 2015-16

OECD crude and product stocks(Billion barrels)

18

OPEC crude oil production(Million barrels per day)

2.4

2.6

2.8

3

3.2

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Ap

r-15

Jul-

15

Oct

-15

Jan

-16

Ap

r-16

Jul-

16

28

30

32

34

Jan

-14

Ap

r-14

Jul-

14

Oct

-14

Jan

-15

Ap

r-15

Jul-

15

Oct

-15

Jan

-16

Ap

r-16

Jul-

16

Four Questions

2 What has been the role of demand?Somewhat smaller role but..

19

9/28/2016

10

20

GDP Growth (Percent)

Source: World Bank.Note: The shared area indicates forecasts. EMDEs refer to emerging market and developing economies.

Global Economy:A Mediocre Expansion with Repeated Disappointments…

-4

-2

0

2

4

6

8

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

World Advanced economies EMDEs

GDP growth(Percent)

Source: World Bank.Note: Weighted average growth.

Advanced Economies and EMDEs:Slow Growth All Around

21

0

2

4

6

8

2011

2012

2013

2014

2015

2016

2017

2011

2012

2013

2014

2015

2016

2017

2011

2012

2013

2014

2015

2016

2017

World Advanced economies EMDEs

1990-2008 Average 2003-08 Average

9/28/2016

11

BRICS demand for key commodities(Percent of global)

Growth of Commodity Demand in BRICS:Weaker Now..

Sources: BP Statistical Review of World Energy 2016, U.S. Department of Agriculture, World Bureau of Metal Statistics.Right Panel. The declines in the growth rate of oil and primary energy are nearly identical because declines in the growth rate of coal have been compensated by corresponding increases in natural gas.

22

Commodity consumption growth in China(Percent, annual average)

0

20

40

60

1990

-95

2010

-15

1990

-95

2010

-15

1990

-95

2010

-15

1990

-95

2010

-15

1990

-95

2010

-15

Edibleoils

Grains Oil Gasandcoal

Metals

Brazil China India Russia

0

5

10

15

20

Metals Oil Primaryenergy

2002-07 2011-15

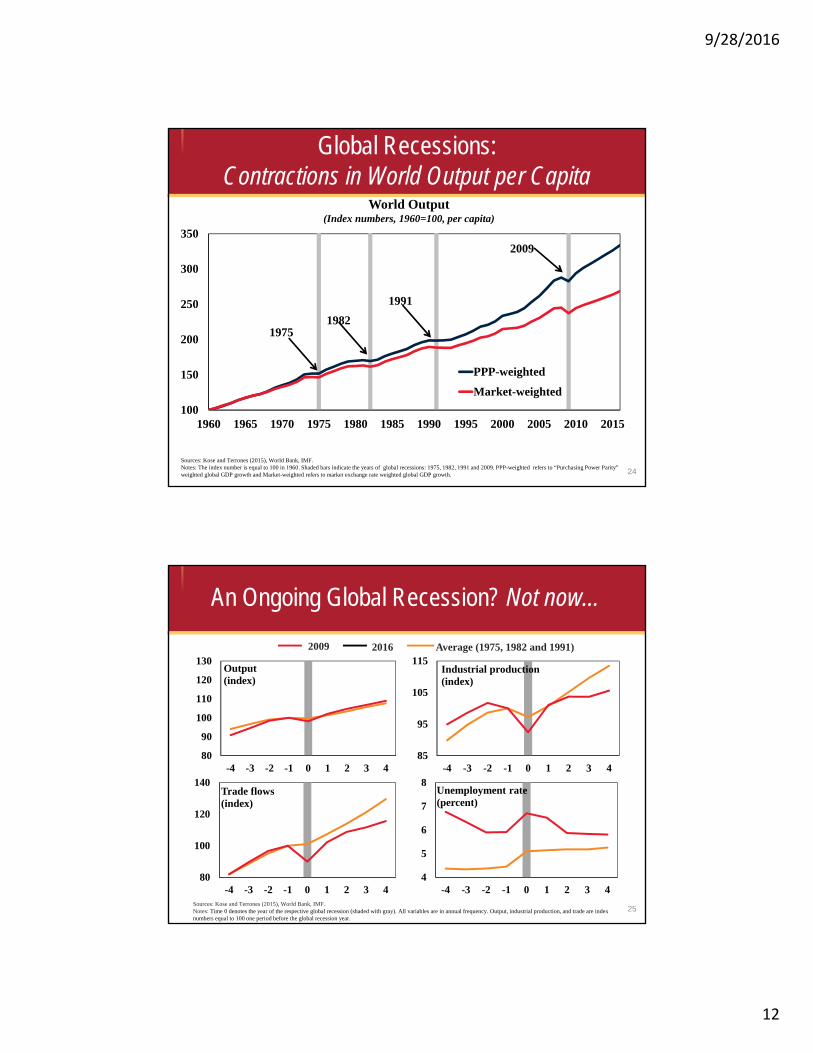

A Constant Question:Is a Global Recession Coming?

• A global recession is defined as a decline in world real GDP per capita accompanied by a broad synchronized deceleration in multiple measures of global economic activity (IP, trade, capital flows, employment, energy consumption).

• Four global recessions: 1975 (1.5; -0.4), 1982 (0.7; -1.0);

1991 (1.1; -0.5), 2009 (-2.0; -3.2)

• The average decline in world per-capita output is 1.3 percent during these episodes; about 3 percentage points lower than the average (with market weights)

• Two global downturns: Lowest global growth except recessions

1998 (2.3; 0.9), 2001 (1.7; 0.4)

23

9/28/2016

12

24

World Output(Index numbers, 1960=100, per capita)

Sources: Kose and Terrones (2015), World Bank, IMF. Notes: The index number is equal to 100 in 1960. Shaded bars indicate the years of global recessions: 1975, 1982, 1991 and 2009. PPP-weighted refers to “Purchasing Power Parity” weighted global GDP growth and Market-weighted refers to market exchange rate weighted global GDP growth.

100

150

200

250

300

350

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

PPP-weighted

Market-weighted

19751982

1991

2009

Global Recessions: Contractions in World Output per Capita

25Sources: Kose and Terrones (2015), World Bank, IMF. Notes: Time 0 denotes the year of the respective global recession (shaded with gray). All variables are in annual frequency. Output, industrial production, and trade are index numbers equal to 100 one period before the global recession year.

80

90

100

110

120

130

-4 -3 -2 -1 0 1 2 3 4

Output(index)

80

100

120

140

-4 -3 -2 -1 0 1 2 3 4

Trade flows(index)

85

95

105

115

-4 -3 -2 -1 0 1 2 3 4

Industrial production(index)

4

5

6

7

8

-4 -3 -2 -1 0 1 2 3 4

Unemployment rate(percent)

2009 2016 Average (1975, 1982 and 1991)

An Ongoing Global Recession? Not now…

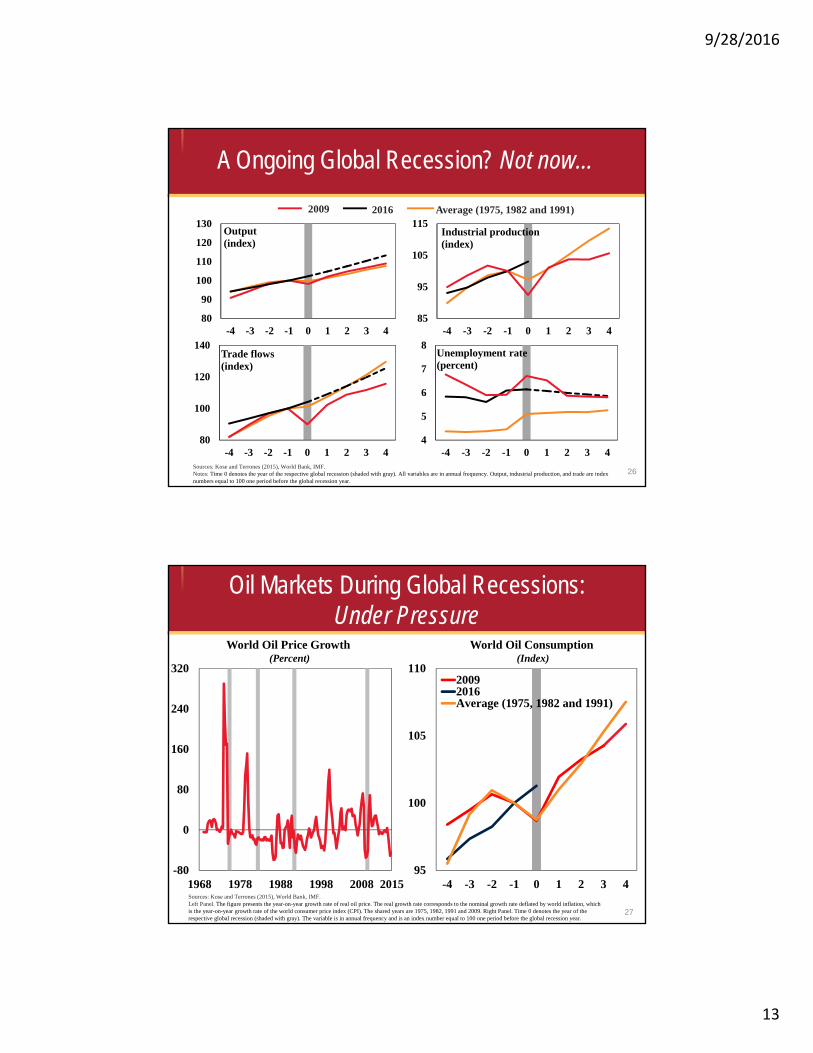

9/28/2016

13

26Sources: Kose and Terrones (2015), World Bank, IMF. Notes: Time 0 denotes the year of the respective global recession (shaded with gray). All variables are in annual frequency. Output, industrial production, and trade are index numbers equal to 100 one period before the global recession year.

80

90

100

110

120

130

-4 -3 -2 -1 0 1 2 3 4

Output(index)

80

100

120

140

-4 -3 -2 -1 0 1 2 3 4

Trade flows(index)

85

95

105

115

-4 -3 -2 -1 0 1 2 3 4

Industrial production(index)

4

5

6

7

8

-4 -3 -2 -1 0 1 2 3 4

Unemployment rate(percent)

2009 2016 Average (1975, 1982 and 1991)

A Ongoing Global Recession? Not now…

27

Oil Markets During Global Recessions:Under Pressure

Sources: Kose and Terrones (2015), World Bank, IMF. Left Panel. The figure presents the year-on-year growth rate of real oil price. The real growth rate corresponds to the nominal growth rate deflated by world inflation, which is the year-on-year growth rate of the world consumer price index (CPI). The shared years are 1975, 1982, 1991 and 2009. Right Panel. Time 0 denotes the year of the respective global recession (shaded with gray). The variable is in annual frequency and is an index number equal to 100 one period before the global recession year.

World Oil Price Growth(Percent)

-80

0

80

160

240

320

1968 1978 1988 1998 2008 201595

100

105

110

-4 -3 -2 -1 0 1 2 3 4

20092016Average (1975, 1982 and 1991)

World Oil Consumption(Index)

9/28/2016

14

28Sources: Kose and Terrones (2015), World Bank, IMF. Notes: Each bar represents the average growth of the respective variable during the years of the global expansions (excluding the first year).

0

2

4

6

1977-81 1984-90 1993-2008 2011-16

Output(percent)

0

2

4

6

8

1977-81 1984-90 1993-2008 2011-16

Investment(percent)

Advanced Economies Emerging Market Economies

0

2

4

6

1977-81 1984-90 1993-2008 2011-16

Output(percent)

0

2

4

6

8

1977-81 1984-90 1993-2008 2011-16

Investment(percent)

But Risks Rising…Recovery: Weakest for Advanced, Weakening for Emerging

Growth in 2020: Forecasts in 2010 and 2016(Percent)

Sources: World Bank, Consensus Economics.Note: Weighted average growth. October forecasts for 46 countries for which long-term consensus forecasts are available.

Persistent Growth Pessimism:Long-Term Forecast Downgrades

29

0

2

4

6

8

World Advanced economies EMDEs

Forecast in 2010

Forecast in July 2016

9/28/2016

15

Four Questions

3

30

What has been the driving force behind the collapse in oil prices?Mostly supply…

Methodology:A Simple VAR Model

31

• The reduced-form VAR model is:y = a +A y +A y +⋯+A y + u • The variables included in the model are: oil prices, equity

prices, and U.S. exchange rates.

9/28/2016

16

Methodology:Shock Identification

32

• Supply and demand shocks are identified using sign restrictions

• Two orthogonal shocks with impulse responses that satisfy certain signs are estimated using the model

• Adverse demand shock: Oil and equity prices decline reflecting a weak economy

• Favorable supply shock: Oil prices decline but equity prices increase

• The differing movement of equity prices allows one to discriminate between supply and demand shocks

Contributions of supply and demand shocks to the oil price decline(Percentage points)

Sources: Baffes (2015), Bloomberg, FRED, Haver Analytics, World Bank.Note: Based on estimates from the model, identifying the demand and supply shocks using sign restrictions. All shocks except the shock of interest are shut off by setting them to zeros and the model is used to trace out the counterfactual oil price. This exercise is performed separately for supply and demand shocks. The red (blue) counterfactual shows how much oil prices would have declined since the second half of 2014 only with the estimated supply (demand) shocks. Numbers shown are in cumulative percentages.

Oil Price Collapse:Mostly (60 - 40) Due to Supply Shocks

33

-50

-40

-30

-20

-10

0

10

-90

-60

-30

0

Jul 14

Sep

14

Nov 14

Jan 15

Mar 15

May 15

Jul 15

Sep

15

Nov 15

Jan 16

Mar 16

May 16

Jul 16

Au

g 16

Supply (RHS)Demand (RHS)Actual

9/28/2016

17

Four Questions

34

4 What are the implications for commodity-exporters?Weak growth in commodity-exporters; stronger policy support needed…

GDP growth(Percent)

Source: World Bank.Note: Weighted average growth

Commodity Exporting EMDEs:After a Sharp Slowdown, Pick Up in 2017?

35

0

2

4

6

8

10

2011

2012

2013

2014

2015

2016

2017

2011

2012

2013

2014

2015

2016

2017

2011

2012

2013

2014

2015

2016

2017

2011

2012

2013

2014

2015

2016

2017

EMDEs EMDE commodityimporters

EMDE commodityexporters

Advanced economies

1990-2008 Average 2003-08 Average

9/28/2016

18

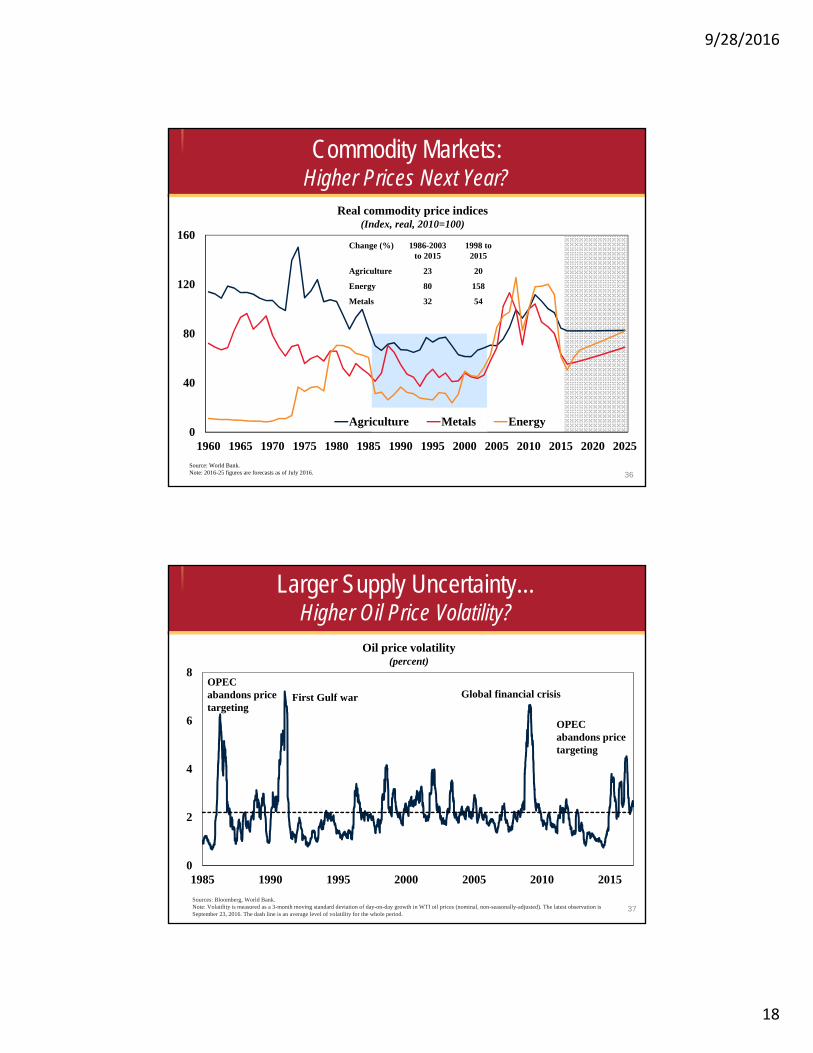

36

Commodity Markets: Higher Prices Next Year?

Source: World Bank.Note: 2016-25 figures are forecasts as of July 2016.

Real commodity price indices(Index, real, 2010=100)

0

40

80

120

160

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025

Agriculture Metals Energy

Change (%) 1986-2003to 2015

1998 to 2015

Agriculture 23 20

Energy 80 158

Metals 32 54

Sources: Bloomberg, World Bank.Note: Volatility is measured as a 3-month moving standard deviation of day-on-day growth in WTI oil prices (nominal, non-seasonally-adjusted). The latest observation is September 23, 2016. The dash line is an average level of volatility for the whole period.

Larger Supply Uncertainty…Higher Oil Price Volatility?

Oil price volatility(percent)

37

0

2

4

6

8

1985 1990 1995 2000 2005 2010 2015

OPEC abandons price targeting

OPEC abandons price targeting

First Gulf war Global financial crisis

9/28/2016

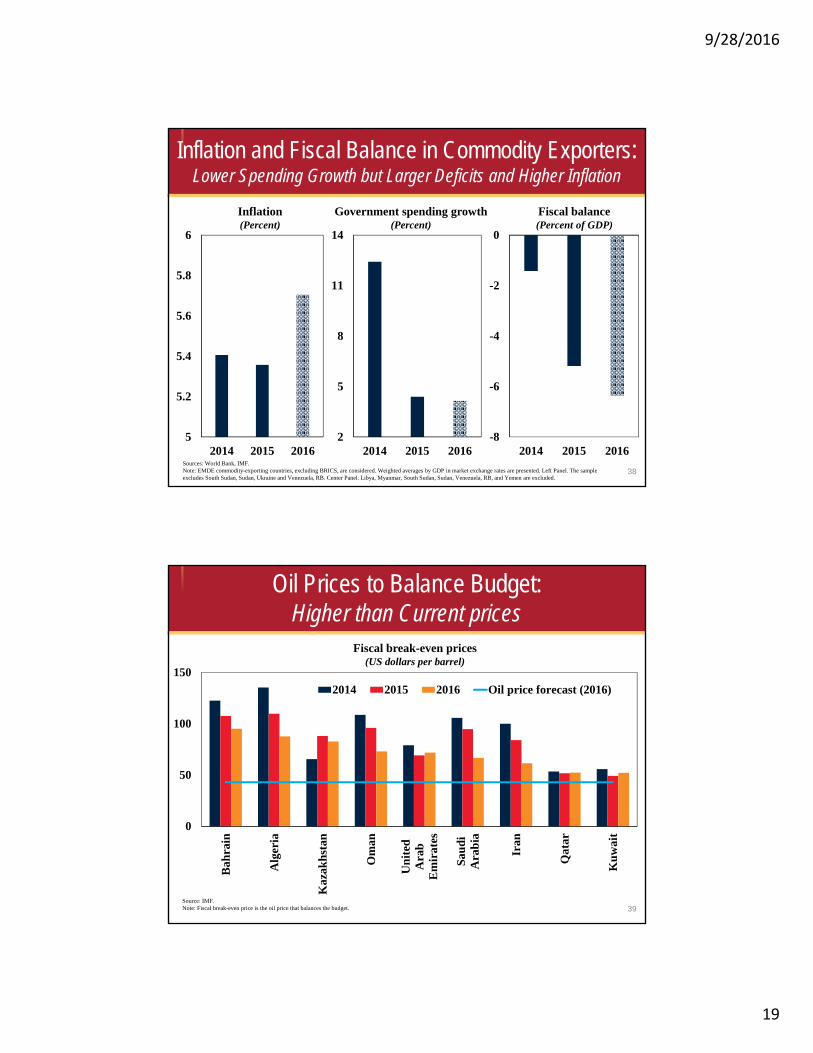

19

Sources: World Bank, IMF.Note: EMDE commodity-exporting countries, excluding BRICS, are considered. Weighted averages by GDP in market exchange rates are presented. Left Panel. The sample excludes South Sudan, Sudan, Ukraine and Venezuela, RB. Center Panel. Libya, Myanmar, South Sudan, Sudan, Venezuela, RB, and Yemen are excluded.

38

Inflation and Fiscal Balance in Commodity Exporters:Lower Spending Growth but Larger Deficits and Higher Inflation

Inflation(Percent)

Government spending growth(Percent)

Fiscal balance(Percent of GDP)

5

5.2

5.4

5.6

5.8

6

2014 2015 20162

5

8

11

14

2014 2015 2016-8

-6

-4

-2

0

2014 2015 2016

Oil Prices to Balance Budget:Higher than Current prices

39

Fiscal break-even prices(US dollars per barrel)

Source: IMF.Note: Fiscal break-even price is the oil price that balances the budget.

0

50

100

150

Bah

rain

Alg

eria

Kaz

akh

stan

Om

an

Un

ited

Ara

bE

mir

ates

Sau

diA

rab

ia

Iran

Qat

ar

Ku

wai

t

2014 2015 2016 Oil price forecast (2016)

9/28/2016

20

An Umbrella of Growth Enhancing Policies: To Address Cyclical and Structural Challenges

What types of policies needed?

Effective; Efficient; Medium-Term fiscal plan

Credible; Price stability; Financial stability

Effective; Demand side implications; Supportive measures

Promotion of trade and financial integration; Supportive measures; Pooling resources for investment

Fiscal

Monetary

Structural

Global

40

Four Questions

1 What has been the role of supply?Looks like played a major role

2

3

What has been the role of demand?Somewhat smaller role but..

41

What has been the driving force behind the collapse in oil prices?Mostly supply…

4 What are the implications for commodity-exporters?Weak growth in commodity-exporters; stronger policy support needed…

9/28/2016

21

Questions & CommentsThanks!

M. Ayhan [email protected]

Development Prospects GroupWorld Bank Group

43