Korea Energy Economics Institute 1

The impact of oil price increase The impact of oil price increase

on the global economyon the global economy

Hyunjoon Chang

Korea Energy Economics Institute 2

The third oil shock?The third oil shock?

Korea Energy Economics Institute 3

Previous oil shocks’ featuresPrevious oil shocks’ features

Common features

1. When the world economy was expanding at a rapid rate

2. When the world’s crude oil capacity was being stretched to

the limit

3. When investment in oil and gas exploration had tapered off,

making it impossible to achieve a speedy increase in non-

OPEC output

Korea Energy Economics Institute 4

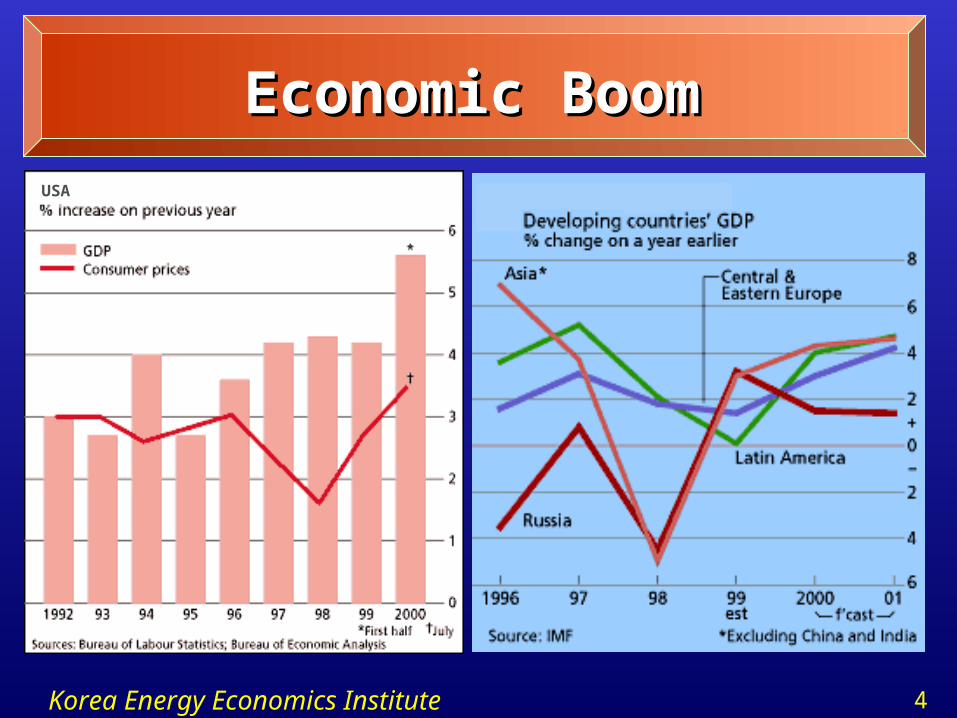

Economic BoomEconomic Boom

USA

Korea Energy Economics Institute 5

Commercial stock in OECDCommercial stock in OECD

Korea Energy Economics Institute 6

Investment expenditureInvestment expenditure

Korea Energy Economics Institute 7

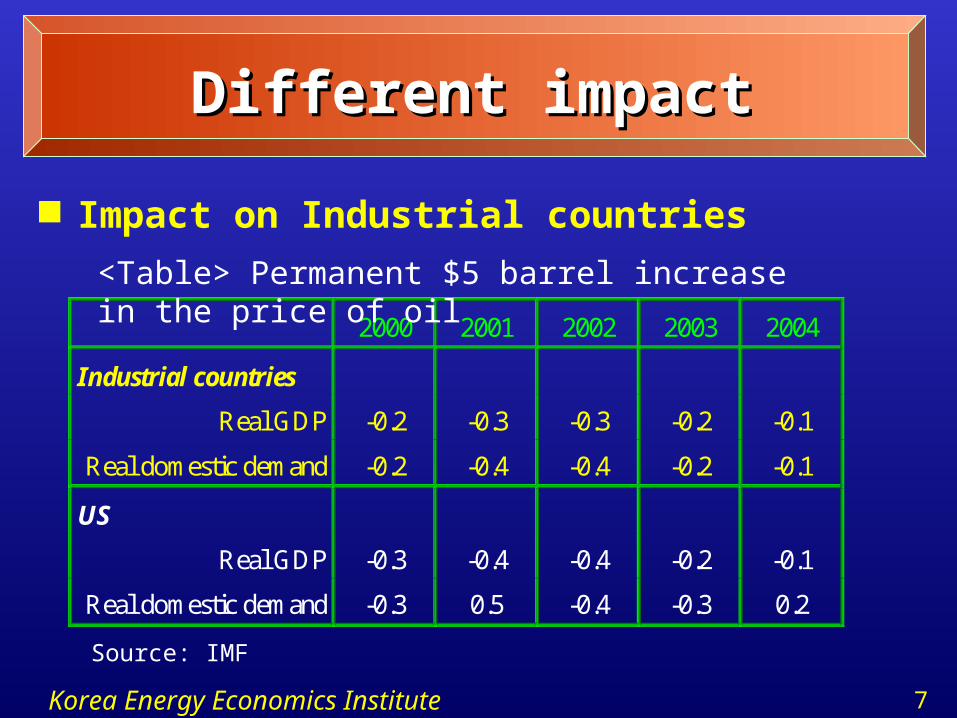

Different impactDifferent impact

Impact on Industrial countries

2000 2001 2002 2003 2004

Industrial countries

Real GDP -0.2 -0.3 -0.3 -0.2 -0.1

Real domestic demand -0.2 -0.4 -0.4 -0.2 -0.1

US

Real GDP -0.3 -0.4 -0.4 -0.2 -0.1

Real domestic demand -0.3 0.5 -0.4 -0.3 0.2

<Table> Permanent $5 barrel increase in the price of oil

Source: IMF

Korea Energy Economics Institute 8

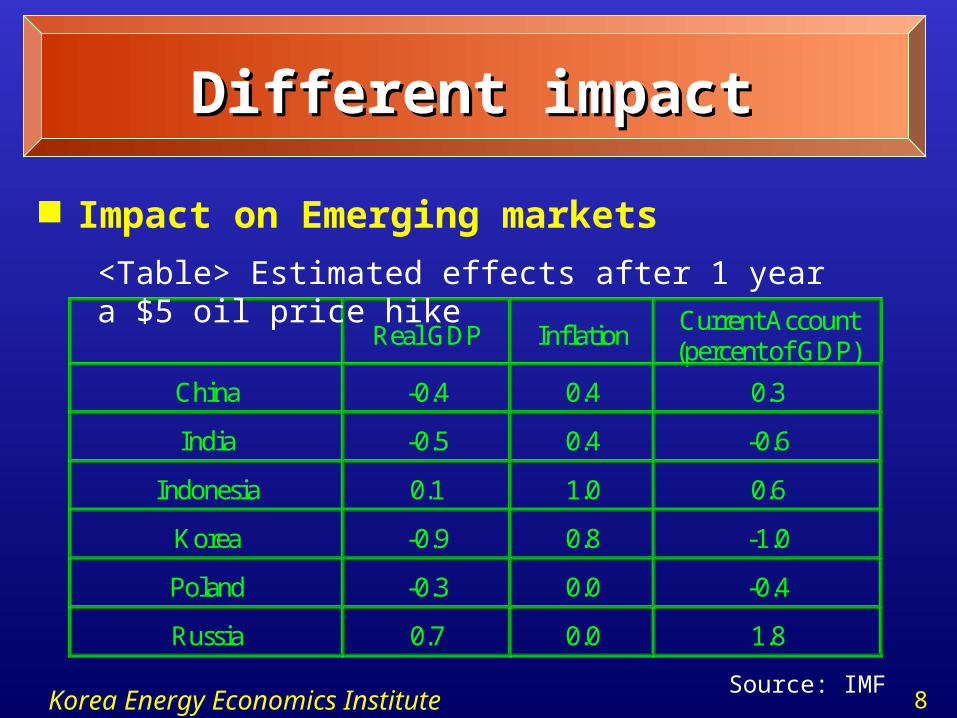

Different impactDifferent impact

Impact on Emerging markets

Real GDP InflationCurrent Account(percent of GDP)

China -0.4 0.4 0.3

India -0.5 0.4 -0.6

Indonesia 0.1 1.0 0.6

Korea -0.9 0.8 -1.0

Poland -0.3 0.0 -0.4

Russia 0.7 0.0 1.8

<Table> Estimated effects after 1 year a $5 oil price hike

Source: IMF

Korea Energy Economics Institute 9

Why different?Why different?

Energy Intensity

Source: OECD, Economic Outlook, no 68, Dec 2000

Korea Energy Economics Institute 10

Why different?Why different?

“New” Economy

High economic growth

Low growthin energy use

IT industries contributed 1/3 of real U.S. economic growth

(1995~1999)

Energy consumptionper dollar of GDP

fell by 4%(1997~1998)

New Economy

Korea Energy Economics Institute 11

Higher PriceHigher Price

Less higher PriceLess higher Price

Why different?Why different?

Competition– Rotemburg and Woodford(1996)

Under perfectUnder perfectCompetitionCompetition

Under imperfectUnder imperfectCompetitionCompetition

Oil price hike

cost

cost

margin

margin

PricePrice

cost marginNormal times

Korea Energy Economics Institute 12

Why different?Why different?

Oil to natural gas

Oil Gas

1980 1997 1980 1997

Low income 25.8 8.8 1.8 5.6

Excluding China & India 43.7 24.5 5.8 24.3

East Asia & Pacific 35.9 11.6 0.3 8.9

High Income 17.7 6.9 11.3 13.8

Europe EMU 22.9 8.8 10.0 11.9

Source: The World Bank(2000)

Korea Energy Economics Institute 13

Concluding remarksConcluding remarks

Developing countries’ limitation in impact mitigation

– Policy measures against oil price volatility

• Strategic oil stock

• Improve energy efficiency

– Developing countries’ constraint

• Difficulties in financial access

• Technological limitation

Need to cooperate with developed countries

Korea Energy Economics Institute 14

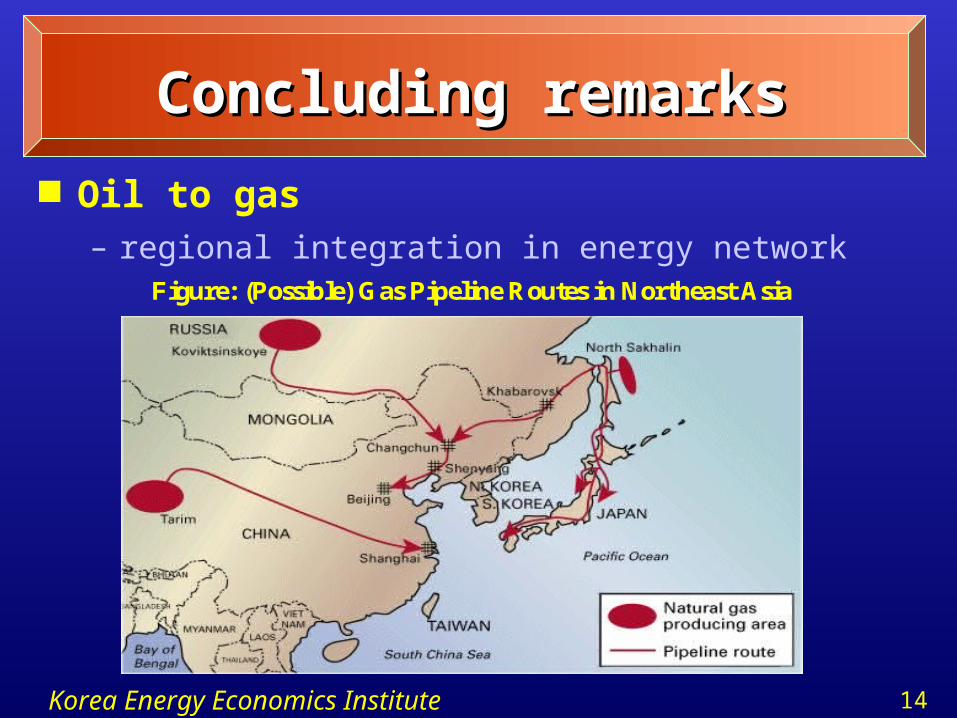

Concluding remarksConcluding remarks

Oil to gas– regional integration in energy network

Figure: (Possible) Gas Pipeline Routes in Northeast Asia