The Pension Crisis

& Utah’s Response

Senator Dan LiljenquistJohn F. Kennedy School of Government

Harvard UniversityNovember 30, 2011

“Politics is the Art of the Possible”Otto Von Bismark

“Politics is NOT the art of the possible. It consists in choosing

between the disastrous and the

unpalatable”John Kenneth Galbraith

6

Utah has never borrowed money from its pension trust fund

Utah has always paid the full actuary recommended contribution

rates

Utah has not increased retirement benefits in over 20 years

Utah’s funded ratio averaged 95.1% between 1997 and 2007

Background on Utah Retirement System

7Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31

2000 2001 2002 2003 2004 2005 2006 2007

104.0% 103.0%

93.6% 92.5% 92.4% 92.2%96.4%

100.8%

Utah’s Retirement System was 100% funded in 2007

Utah’s Actual Funded Ratio – 2000 to 2007

8

2000 2001 2002 2003 2004 2005 2006 2007 2008-$4,000

-$3,000

-$2,000

-$1,000

$0

$1,000

$2,000

$3,000

Utah’s pension funds lost 22.3% of their value in 2008

Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31

Investment Income (in Millions)

Step 1: Demand the Data

Pension Reform Steps

10

Unanswered questions…o What impact would the losses have on

Utah’s budget now and in the future?

o Would the market recover the losses?

o How would the losses impact employer contribution rates?

o How long would it take for the pension system to recover?

o What would happen if Utah had another year like 2008?

11

o Forty year actuarial projections, with market returns of 6%, 7%, 7.75%, and 8.5%

o Modeled scenarios included:o Standard option (increase contribution

rates)o Do-Nothing option (freeze contribution

rates at existing levels)o Delay options (freeze contribution rates

for 3 or 5 years and then increase contribution rates)

Unanswered questions…

12Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31; and

Memo to the Honorable Daniel R. Liljenquist, Senate Chair, from Gabriel Roeder Smith & Company, November 10, 2009

2007 2008 2009 2010 2011 2012 2013

100.8%96.5%

? ? ? ? ?

Utah’s pension system still appeared to be in excellent shape, however…

Utah’s Projected Funded Ratio

13

2007 2008 2009 2010 2011 2012 2013

100.8%96.5%

87.8% 85.8%80.6%

75.1%70.5%

The 2008 losses blew a 30% hole in Utah’s pension system

Utah’s Projected Funded Ratio

Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31; and

Memo to the Honorable Daniel R. Liljenquist, Senate Chair, from Gabriel Roeder Smith & Company, November 10, 2009

14

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016

13.3%

15.4%

? ? ? ? ?

Required employer contribution increases in 2008 were manageable, however…

Utah’s Projected Employer Contribution Rates

Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31; and

Memo to the Honorable Daniel R. Liljenquist, Senate Chair, from Gabriel Roeder Smith & Company, November 10, 2009

15

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016

13.3%

15.4% 16.2%

18.2%

20.5%

22.8% 23.1%

Required contribution rates will increase by 75% over the coming years

Utah’s Projected Actuarial Required Contribution Rates

Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31; and

Memo to the Honorable Daniel R. Liljenquist, Senate Chair, from Gabriel Roeder Smith & Company, November 10, 2009

16

Brutal reality of the 2008 crash

Utah will have to commit ~10% of its General Fund for 25 years to pay for the 2008 Market Crash

Step 1: Demand the Data

Pension Reform Steps

Step 2: Frame the Debate

18

FY 2010

FY 2011

FY 2012

FY 2013

FY 2014

FY 2015

FY 2020

FY 2025

FY 2030

FY 2035

FY 2040

FY 2045

FY 2050

8.5% Return

7.75% Re-turn

7% Return

6% Return

100%

80%

60%

40%

20%

Message #1 - Doing nothing leads to bankruptcy

Utah’s Projected Funded Ratio with Employer Contributions Frozen at 2010 Rates

Source: Utah Retirement Systems Comprehensive Annual Financial Reports - 2000-2009 - for year ending Dec. 31; and

Memo to the Honorable Daniel R. Liljenquist, Senate Chair, from Gabriel Roeder Smith & Company, November 10, 2009

Message #2 - 2008 crash is like a “Chemical Spill”

o First, you have to contain the situation

o Second, you have to work over time to clean things up

Message #3 - 2008 crash will devastate public

educationo Approximately 8,000 teachers kept

out of classrooms for 25 years

o 100% of public education growth for the next five years, increasing class sizes by up to 8 children per class

o Increased contributions will equate to 19% of current state public education funding

Message #4 – We cannot afford another year like

2008

22

Message #5 – We are determined to meet our current commitments

Meet Current Pension

Obligations•Pay full actuary recommended contribution rates•Shore-up the current retirement system by closing incentives for post-retirement reemployment

Eliminate Pension Related Bankruptcy Risk

•Pay off the unfunded liability as quickly as possible•Create a new system for new employees with:•Lower costs, and•Predictable employer contributions

23

Message #6 – Pension reform is the “Wage Liberation Act”

Raises

COLAs

Healthca

re

PensionCosts

Step 1: Demand the Data

Pension Reform Steps

Step 2: Frame the Debate

Step 3: Move Forward

25

Thousands of Utah public employees protested the

reforms

26

Be Polite and RespectfulThank you for reaching out and sharing your thoughts about the Utah Retirement System. I appreciate the sacrifices you have made and make to educate the children of our State.

As you may know, the Utah Retirement System lost $6.5 Billion last year ($4.8 Billion in actual losses and $1.7 Billion that we needed to earn on the overall portfolio but didn't). To make the current system sound, the State will need to come up with $400 Million per year for the next 25 years to make up the $6.5 Billion gap. This is equivalent to 8% of our total State payroll for the next 25 years to meet the commitments we have made to our current employees. With the severe budget issues we are facing (we are down $850 Million this year) and the growth we are seeing in our public schools, we cannot afford to ramp into the higher contribution rates and will likely need to make changes to the retirement system.

As we look at our options, I want you to know that I am determined to meet the commitments we have made to our current and retired employees. It is the right thing to do. To ensure that we are able to meet that commitment, however, we will likely need the flexibility to adjust the retirement system for new employees and to change the post-retirement reemployment rules.

Please know that we are looking at all options and working with all of the interested parties to determine the best approach.

Thank you again for reaching out.

27

Build Coalitions

28

Educate through the Media

Anticipate Objections

There is No Problem

We need to “Study” the issue

We will grow out of this

Transition costs are too high

401Ks don’t work

Actuaries and URS Disagree

Second actuarial analysis & 1.5 year

before implementation

Updated actuarial reports & URS letter

showing we can’t grow out of it

Kept same vesting schedule & Focused on blended contribution

rates

URS will manage 401K program & No

Borrowing

Argument Resolution

30

Ask the hard questions / demand data

Be hypothesis driven / avoid ideology

Involve ALL parties / build partnerships

Circulate reform proposals broadly

Be kind, polite and responsive

Keep moving forward

Other keys to the pension reform process

31

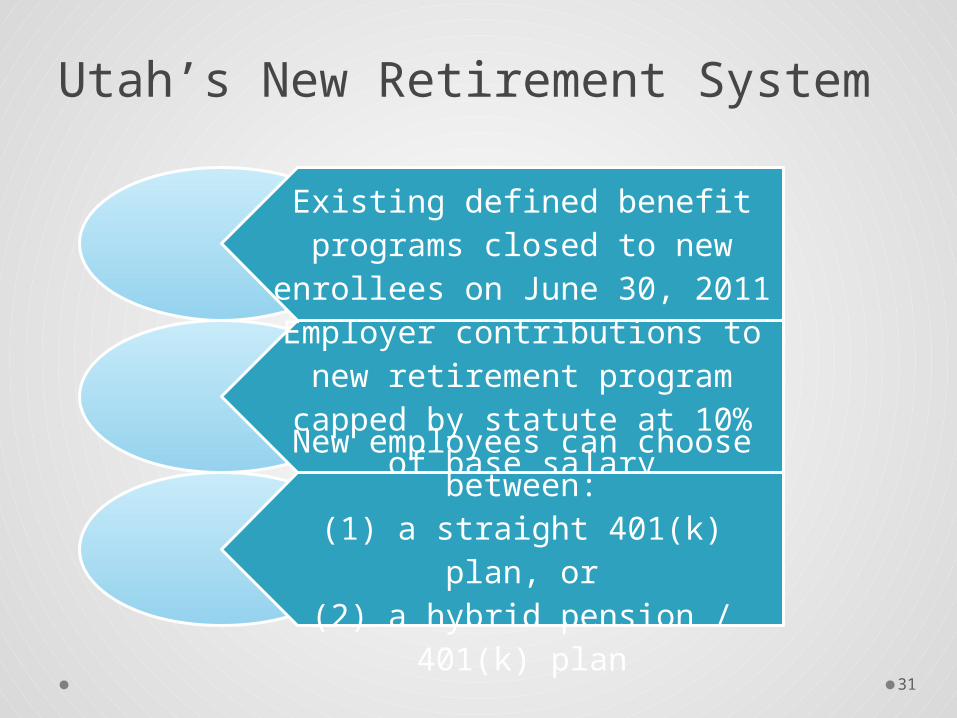

Utah’s New Retirement System

Existing defined benefit programs closed to new

enrollees on June 30, 2011

Employer contributions to new retirement program capped by statute at 10% of base salaryNew employees can choose

between:(1) a straight 401(k) plan, or(2) a hybrid pension / 401(k)

plan

32

Utah’s New Retirement System

Defined Contribution 401(k) Plan

Hybrid Pension / 401(a) Plan

• Employer contribution:• Employee contribution:

• Vesting period:

• Restrictions:

• 10% of salary • 10% of salary

• N/A • Employee pays all pension related contributions:• If > 10%, then

automatic payroll deduction

• If < 10%, then balance goes into 401(k) plan

• 4 years • 4 years

• No borrowing from plan

• 401(k) plan self-directed with URS investment options

• No borrowing from plan• URS manages pension

investing; 401(k) portion self-directed with URS investment options

33

Expected results of Utah’s pension reforms

oCombined retirement systems and statutory restrictions will help prevent “pension creep”

oUtah will gradually reduce pension related bankruptcy risk until the risk is eliminated

oEach new employee costs will be less than half the cost of old employees (10% vs. 23.1%), freeing up resources to fund the “tail” of the current programs

oCombined retirement contribution rates for public employees will peak in 7 years and gradually decline

34

Recap of Lessons learned

oMOVE FORWARD – oBe polite and respectfuloBuild coalitions and educate the publicoAnticipate objections

oFRAME THE DEBATE –oTranslate the data into tangible tradeoffsoTailor the message to each different group

oDEMAND THE DATA – oDemand comprehensive, long-term financial

modeling from pension actuariesoReality is NOT negotiable – let the data do the

work

It’s time!