10/03/2016

The Real World March 2016

The

Posters

Laptops

Tablets Duty Free /

Retail Media &

Assets

Owned OOH

(e.g. buildings

or jet bridges)

Networked

Video Screens Content

Physical

Experiences

(sampling)

Experiential

Stands / Zones

Platforms

Apps &

Games

Commerce

& Coupons

Mobile etc

Data

Technology

Ads

People

& Places

Services /

Utilities

(e.g. wifi)

Out-of-Home ecosystem

Understanding The Connected Consumer

OCS

Constantly

consumer-

centric

Constantly

consumer-

centric

OCS in Numbers

6,765 Total sample in UK

7th Version

Release Date Feb 2015

100,000+ Global respondents

30 Countries OCS is run in

250 Brands now included on the

survey

41 Number of OOH formats

analysed within OCS

%

TouchPoints

Did you know…

TouchPoints

The average adult

spends 10 hours a

week travelling

Source: Touchpoints 6

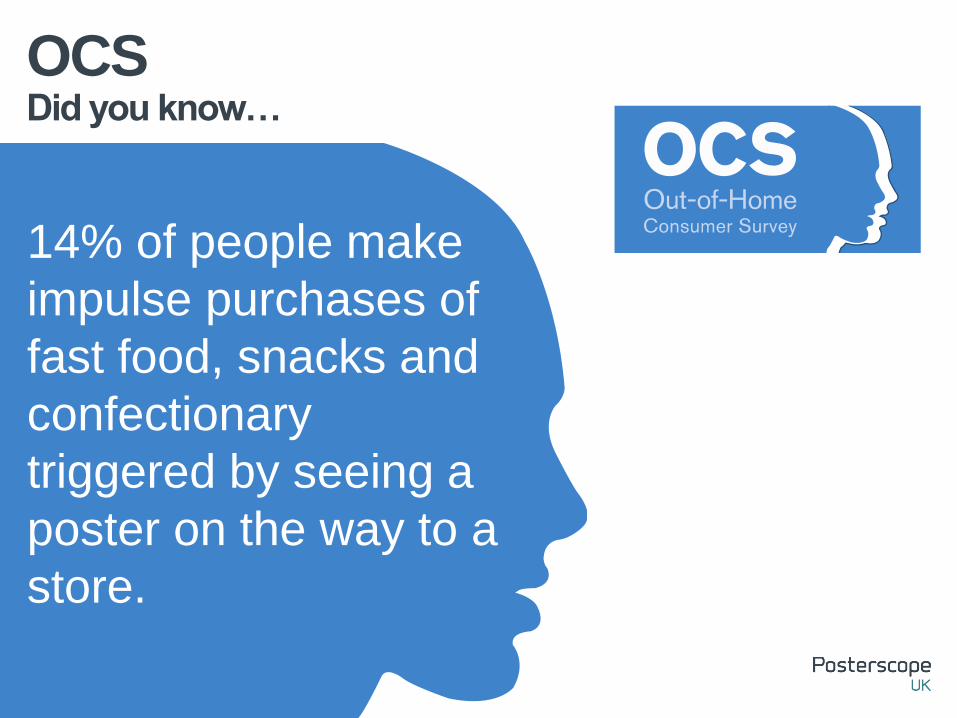

Did you know…

OCS

14% of people make

impulse purchases of

fast food, snacks and

confectionary

triggered by seeing a

poster on the way to a

store.

JCDecaux

Connected

Clear Channel Tribes

Clear Channel

Ngen

Exterion Insight Tools

Exterion Media

work.shop.play

Our own research suite

Primesight

Primemobile

Our unique market research

technique, including the

Primemobile Live Portal

Prime Design

Creative

analysis tool

EPOS Data

(Measures sales uplift

in convenience stores)

Data Driven Targeting

A pioneering new travel survey

Measuring audiences whilst OOH

Revolutionising the way we plan

OOH

We Live in a Convergent World

It’s a convergent World…

Gateway to Mobile

content

Networked OOH:

Real Time

Experiential OOH

Owned OOH Interactive interfaces Live video streaming

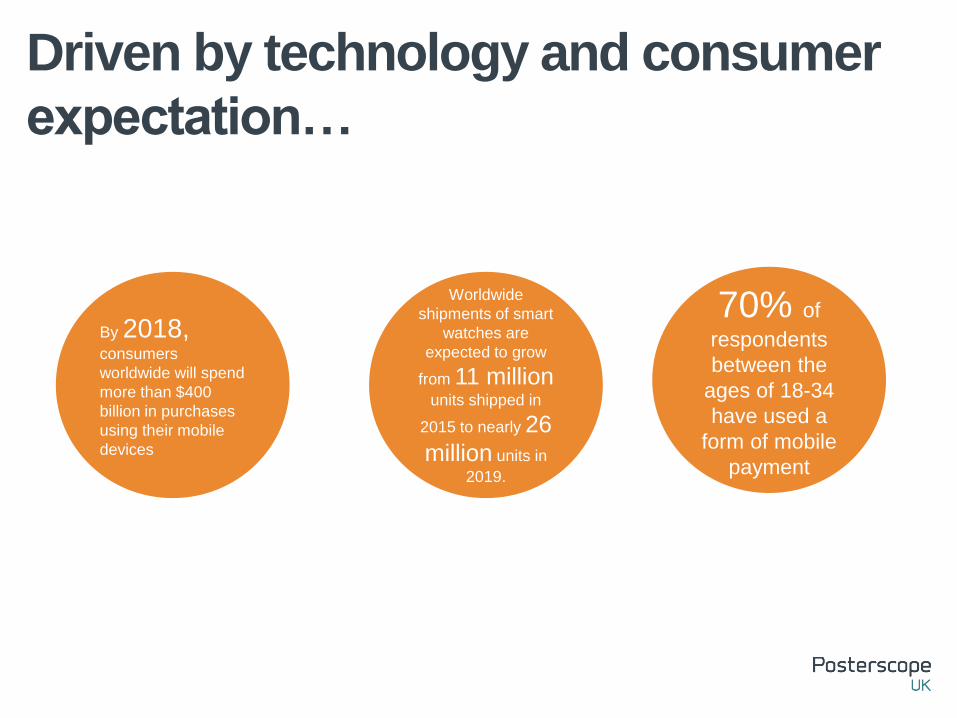

Driven by technology and consumer

expectation…

1.1bn Connected Things will

be used by smart

cities in 2015

370 contactless

transactions are

made every

minute in the UK By 2018, consumers

worldwide will spend

more than $400

billion in purchases

using their mobile

devices

70% of

respondents

between the

ages of 18-34

have used a

form of mobile

payment

Worldwide

shipments of smart

watches are

expected to grow

from 11 million units shipped in

2015 to nearly 26

million units in

2019.

Index of tweets vs. the

norm in proximity to

posters in Nottingham

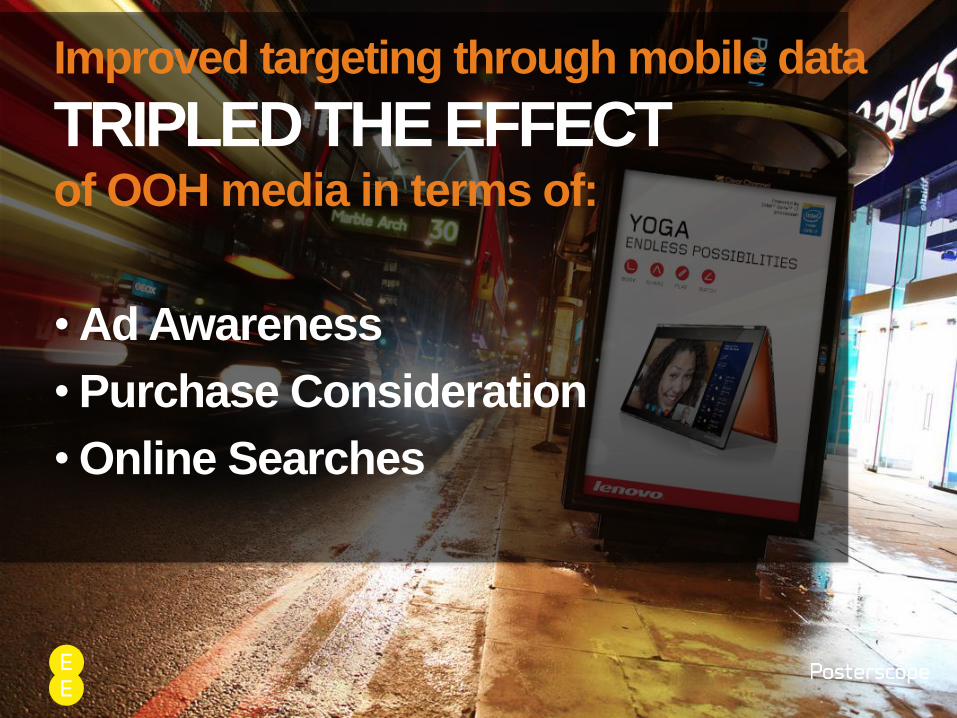

Data-led planning

Data-led planning

Data-led planning

Improved targeting through mobile data

TRIPLED THE EFFECT of OOH media in terms of:

• Ad Awareness

• Purchase Consideration

• Online Searches

Data-led planning

The Out-of-Home Marketplace

1999-2014 Media Revenue

Media Revenue Growth

Source: Dentsu Aegis Media & WARC

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Internet

Outdoor

Cinema

Radio

TV

Magazines

Newspapers

Media

Year

An

nu

al

tota

l m

ed

ia s

pen

d in

£m

Media OOH Revenue 2015 (Jan-Dec)

Source: Outsmart / ** 2015 Q1 data is Posterscope estimate

+6%**

-3.6%

5.2% £m

£0.0

£50.0

£100.0

£150.0

£200.0

£250.0

£300.0

£350.0

2012

2013

2014

2015

5.3%

0

50

100

150

200

250

300

350

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

UK Digital OOH Revenue

Source: OMC/Posterscope estimates

Forecast

The top OOH spending categories: January 2016

Top 10 Categories

Entertainment

and leisure

Gov, Social,

Political

organisations

Computers Media

Telecoms

Drink Finance

Motors

£8.7m

-4.6%

£7.1m

52.1%

£4.3m

77.5%

£3.1m

-46.6%

£2.4m

245.8%

£5.3m

44.0%

£2.8m

136.63%

£5.0m

22.6%

£5.6

131.3%

£7.0

-22.6%

Food

Total market £63.9m (-11.6%)

Travel and

Transport

The top OOH spending advertisers: January 2016

Who’s Spending?

£2.5m

2.3%

£1.6m

165.9%

£1.4m

0%

£1.2m

3.3%

£1.1m

26.6%

£0.9m

0%

£1.0m

98.6%

£1.5m

2713%

£1.1m

85.6%

£1.1m

-3.2%

£1.1m

26.6%

Spend by OOH format: January 2016

Spend Trends- Roadside

£8.3m

47.1%

Large Digital 6s

£17.1m

-13.4%

48s

£7.5m

12.3%

96s

£2.3m

-16.23%

Specials

£0.8m

7%

Spend by OOH format: January 2016

Spend Trends- Transport

£7.1m

13.6%

£3.8m

-3.4%

£3.2m

4.6%

£5.3m

136.3%

Consolidated Market Place

35%

17%

23%

12%

8% 5%

2016 Est. Market share based on revenue

OTHERS

In the UK JCDecaux provides opportunities on multiple formats

across roadside, rail, retail, airports and the experiential

landscape.

Nationwide across environments in all the key cities across

the UK.

Roadside: Continued investment in digital across the

country. Key new digital locations include The Salford Arch

and first ever 84” D6’s in Edinburgh.

Rail: Digital expansion continues across D6 and

Transvision networks

Retail: M-Vision expansion to further premium malls, and

portfolio moves towards 100% digital with D6 development.

Continued digital investment at Tesco

Airport: Ongoing development in digital inventory at major

UK airports. New iVision screens and increasing focus on

dynamic content and live updates

Experiential: JCDecaux Live is expanding the multi-

environment portfolio further

Connected Commuter and Connected Consumer, Power of

Big ‘3’ from JCDecaux Insight.

‘Business Traveller 2’ Insight, Audience Typology, Luxury &

Motors category presentations and Perceived Value

Research from JCDecaux Airport.

JCDecaux is a privately owned French OOH advertising

company, founded in 1964 in Lyon when Jean-Claude

Decaux installed the first advertising bus shelter. This local

outdoor company is now a global media owner.

Reporting €2.813 billion in revenue in 2014, JCDecaux is

present in more than 70 countries worldwide and is market-

leader in the UK.

JCDecaux has recently been awarded the £500m TfL Street

Furniture contract across a period of eight years.

jcdecaux.co.uk

About JCDecaux Key Areas For Investment

Key Formats

Geography Proprietary Research

+

Media where it matters

Nationwide across environments in key cities across

the UK

Ngen

Our community of young, social and connected people

gives us deep and rich insight and allows for on-going

engagement for Clear Channel and clients.

In 2016 our we’ll be asking our Ngen’s to explore our

various advertising environments, so expect a wealth of

insight on how their thoughts, habits, behaviours and

moods change with each differing advertising situation.

.

.

About Clear Channel Key Areas For Investment

Key Formats

Geography Proprietary Research

+

clearchannel.co.uk

Clear Channel UK is part of Clear Channel Outdoor (CCO).

Clear Channel Outdoor is one of the world’s largest outdoor

advertising companies with a portfolio of solutions that reaches 600

million people in over 40 countries across Asia, Australia, New

Zealand, Europe, Latin America and North America.

Adshel, Adshel Live, Storm, Wrap, Billboards, Malls, Supermarkets,

Socialite

Adshel Live national roll-out

With 300 already in the ground, we are in the process of rolling out

600 Adshel Live units, a network of digital and beacon enabled

screens. Situated in premium locations, in over 30 towns and cities

across the UK, they give brands the opportunity to engage with

audiences using dynamic, interactive and real-time advertising

creative.

Storm expansion

In 2016 we will continue our portfolio expansion across the UK’s top

10 cities, building on the seven new sites we delivered in 2015,

which included the digitisation of the iconic Storm Cromination.

Storm are now London’s number 1 super premium portfolio in terms

of scale, footprint, audience and quality, always delivering Fame on

Demand.

Underground, bus, retail (Westfield Stratford, Westfield

London and One New Change), National Rail

Formats include, 96s, 48s, 16s, 6s, 4s, LEP’s, TCPs, DEPs,

LCDs, XTP’s, T-sides, Streetliners, Bus interiors, etc.)

National with a dominant presence in London

Increasing digital offering across Rail & London

Underground

Illuminated New Bus For London

Performance 48 sheets National Rail

Expansion of retail offering

Birmingham Express Roadside digital

work.shop.play and All eyes on London

Previously part of American-based CBS Corporation, CBS Outdoor

International was sold in the Autumn of 2013 to LA-based Platinum

Equity and rebranded to Exterion Media in January 2014.

Exterion are currently involved in pitching for the TfL pitch which

combine the ad sales for the Underground, the Overground, the

Tramlink, the Docklands Light Railway (DLR), Victoria Coach

Station and Crossrail, when it launches.

About Exterion Outdoor Key Areas For Investment

Key Formats

Geography

Proprietary Research

+

http://www.exterionmedia.co.uk/

Roadside,Digital ‘Network’ cinema, Glasgow subway

National coverage with sites in all major cities across

the UK and Glasgow Underground

Primesight has heavily invested in Digital by creating the

first national roadside digital ‘Network’ of 48 sheets. It

continues to expand as sites are rolled out across the

country.

Primemobile, Primedesign,, EPOS, Brain Works, Geofencing.

Primesight has also recently innovated ‘Primemobile live’ – a

real time marketing performance dashboard that allows you to

view campaign progress in the moment

Jointly owned by GMT Communications Partners LLP and

the Primesight management team, Primesight is a UK-

based business which has a market share of 8% in

2014/15.

primesight.co.uk

About Primesight Key Areas For Investment

Key Formats

Geography

Proprietary Research

+

Results are our culture

61 screens & displays across 42 locations in 9 cities.

Large-format digital, iconic landmark and super-premium

banner locations including The IMAX.

Ocean has a regional footprint that spans the following

UK cities: London, Birmingham, Liverpool, Manchester,

Leeds, Bristol and Glasgow

, , , , , and .

Ocean practices 'The Art of Outdoor', with every site in the

Ocean portfolio having a unique quality and personality.

Ocean’s strategy of developing iconic digital land premium

formats, is mirrored by its acquisition strategy. Areas of

investment include…

The Grid

Ocean Labs

Regional site expansion

Neuroscience Research projects

- The Science Behind the Art of Outdoor

- Beyond Out of Home

Ocean Outdoor, launched in 2005, is a boutique, UK-based

media company pioneering creativity in digital OOH via an

expanding portfolio of large-format, high profile sites

In May 2012 a management buyout, backed by LDC Capital,

purchased the business from Smedvig Capital for £35m

In 2014, Ocean Group acquired Signature Outdoor and in

2015 expanded further with the acquisition of MediaCo.

Ocean Outdoor reported revenues of £23.4 million in 2012

About Ocean Outdoor Key Areas For Investment

Key Formats

Geography

Proprietary Research

+

oceanoutdoor.com

Posterscope news, views and campaigns

www.pioneeringooh.com

CK2 giant posters dominate the High Street…

OOH Countdown For All New X Files…

Emirates Customise the Colossus…

BBC Three is ‘Too Big For TV’…

Ciroc Vodka Celebrate the Return of Zoolander in

New Campaign…

adidas Search for the Boss in New Campaign…

OOH Industry News

Digital Drives Out of Home Renaissance…

Clear Channel Drops Out of Tube Contest…

Primesight Selects BroadSign for Delivery of

Dynamic Content and Accountability…

JCDecaux Awarded Bus Shelter Contract for the

Royal Borough of Kensington and Chelsea…

London City Airport Launch City Traveller

Network…

Five Trends for OOH In 2016 According to Naren

Patel, CEO, Primesight…

Exterion Media Offers Brands Deep Insight on

Underground Users…

Ocean and British Fashion Council Turn London

Fashion Week into National Celebration…

Outdoor Plus Secures ‘The One’ In a Landmark

Development For the DOOH Sector…

Child Rescue Alert Uses Programmatic DOOH

Ads to Help Find Missing Kids…

3/10/2016

OUTFRONT Media CEO Jeremy Male Rejoins

FEPE International Board…

Clear Channel Wins Asda Advertising Contract…

New Premium Roadside DOOH in Birmingham

for Signature Outdoor…

Exterion Media to launch Media for Equity…

Primesight’s ‘Hyperlocal’ Digital Targeting Deal…

Stuff we like

Fifth Lion Unveiled in Trafalgar Square Highlights

That ‘Time is Running Out’ For African Lions…

Condom Machine Installed With Breathalyzer To

Prevent Drunken Mistakes…

Carlsberg Unveil What Is ‘Probably The Best

Shopping Trolley In The World…

Amsterdam Airport Baggage Car Gets Lost in

Antwerp…

Oreo Wonder Vault Delighting Passersby in New

York City…

Outdoor detects flu systems with live Thermo-

scanner…

Purdy…Paint Any Surface With Ease…

Mood Stockholm Sets Up the Unswipeable Dating

Ads…

Rent a Livable Model of Van Gogh’s ‘Bedroom’ on

Airbnb…

A Bank Set Up This 10-Foot-Tall ATM to Celebrate

the Arrival of NBA All-Stars…

3/10/2016

DIY Brand Creates Peruvian Billboard Stop For

Tired Drivers…

3/10/2016

An Elvis Impersonator on a Digital Billboard Takes

‘Shotgun’ Weddings to New Heights…

Skol Beats makes Masquerade Ball technological

for Carnaval in Brasil…

McDonald’s Billboard Near Whistler Gives Snow

Reports via Espresso Drink Toppings

Lush launches Sun Cinema pop-up experience

Mineral Water Company Donat Mg Creates The

World’s First Portable Royal Toilet…

Delicates and Regulars Battle It Out In LG’s

Outdoor Advertising Campaign…

Find Out More