Journal of Business StrategyEmerald Article: TURNAROUND STRATEGIESCharles W. Hofer

Article information:

To cite this document: Charles W. Hofer, (1980),"TURNAROUND STRATEGIES", Journal of Business Strategy, Vol. 1 Iss: 1 pp. 19 - 31

Permanent link to this document: http://dx.doi.org/10.1108/eb038886

Downloaded on: 21-01-2013

Citations: This document has been cited by 98 other documents

To copy this document: [email protected]

This document has been downloaded 846 times since 2008. *

Users who downloaded this Article also downloaded: *

Charles W. Hofer, (1980),"TURNAROUND STRATEGIES", Journal of Business Strategy, Vol. 1 Iss: 1 pp. 19 - 31http://dx.doi.org/10.1108/eb038886

Charles W. Hofer, (1980),"TURNAROUND STRATEGIES", Journal of Business Strategy, Vol. 1 Iss: 1 pp. 19 - 31http://dx.doi.org/10.1108/eb038886

Charles W. Hofer, (1980),"TURNAROUND STRATEGIES", Journal of Business Strategy, Vol. 1 Iss: 1 pp. 19 - 31http://dx.doi.org/10.1108/eb038886

Access to this document was granted through an Emerald subscription provided by INDIAN INSTITUTE OF MANAGEMENT AT AHMEDABAD For Authors: If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service. Information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comWith over forty years' experience, Emerald Group Publishing is a leading independent publisher of global research with impact in business, society, public policy and education. In total, Emerald publishes over 275 journals and more than 130 book series, as well as an extensive range of online products and services. Emerald is both COUNTER 3 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Related content and download information correct at time of download.

TURNAROUND STRATEGIES Charles W. Hofer

No matter what the state of the economy, no company is immune from internal hard times—stagnation or declining performance. How can management pinpoint the right turnaround strategy when it is needed—and make it work?

In the 1950s,.George Romney became the president of the newly created American Motors Corporation. For three years, he waged a "Campaign Survival" to keep AMC afloat by discontinuing low-volume products, shutting plants, cutting overhead (including executive salaries), and selling off nonautomotive assets. Still the red ink flowed. He even took to the road in the middle of a recession to convince Americans that the Rambler was the answer to the "gas-guzzling dinosaurs" of the Big 3. He succeeded, and AMC was saved.

About the same time, John T. Brown took over the reins at J.I. Case, which was struggling to regain its position in farm equipment after a year-and-a-half strike a few years earlier. He expanded R&D, acquired a manufacturer of light commercial construction equipment, set up several overseas subsidiaries, increased sales efforts, and opened several new plants. When performance did not improve, the board replaced him with Marc Rojtman, who launched Case on a major sales and expansion program, which included substantially increased R&D and more rapid diversification into construction equipment. Three years later, he was replaced as Case teetered on the brink, with dealer and company inventories in excess of a year's sales and massive service/repair problems on products that had been brought to the market too rapidly. His successor, William Grede, slammed on the brakes

Charles W. Hofer is Visiting Associate Professor, New York University Graduate School of Business Administration.

hard and Case skidded along for two years until he was replaced with a new CEO from Ford. Unfortunately, by this time, Case was only a shadow of its former self and faced years of struggle as a distant follower in an industry where it had once been a leader.

A decade later, Arthur Keller became the general manager of a major Swedish dress manufacturer when it was acquired by the German yarn producer for whom he worked. Upon arriving in Sweden, he found the company's sales had fallen to half their former level because of delivery delays and increased competition from imports as well as local manufacturers. Moreover, the company's fall line was due in two weeks, and a key designer had quit. Over a half million dollars in new equipment was on order despite the fact that the firm was operating at only 25 percent of existing capacity. A substantial volume of work was subcontracted while a large percentage of the company's work force had little work. The result: Losses for the past two years exceeded the company's cumulative retained earnings. Keller agonized between selling off much of the firm's assets to get down to a profitable core or trying to double volume to reach break-even. Finally, he choose to try to double volume by cutting the number of styles in the current line to get it out on time, introducing interim collections, adding a newer, lower-priced line, and making fabric, all of which was supported by a strong sales effort. He succeeded and was well rewarded for his efforts.

These three situations each represent a different variation of a problem that most organizations face

19

20 THE JOURNAL OF BUSINESS STRATEGY

at some time in their existence: a major decline in performance. The response to such situations is almost always a major effort to "turn the company around." The key questions that must be answered in all cases are: "Are such efforts worthwhile?" "Can they be successful?" and "What type of turnaround strategy has the best prospects for success?" Clearly, what is needed most in a turnaround situation is some clear-cut strategy for guiding all organizational actions so that scarce resources are not dissipated in unproductive ways. (See Exhibit 1.)

This article describes a framework for designing such overall turnaround strategies for single-industry firms or the independent divisions (SBUs) of multi-industry firms, including (1) the types of turnaround strategies possible, (2) the nature of turnaround situations, and (3) a framework for deciding which type of turnaround should be used in a particular situation.

Strategic vs. Operating Turnarounds There are two broad types of turnaround strategies that may be followed at the individual business/ SBU level: strategic and operating. Strategic turnarounds can be divided into those that involve a change in the organization's strategy for competing in the same business and those that call for entering a new business or businesses. This article focuses only on strategies for "saving" the existing business. Such turnarounds may be further subdivided according to the degree of competitive position change desired or according to the key functional area emphasis around which the strategy is built. In terms of competitive position changes, it is useful to distinguish among strategic turnarounds that seek (1) no change in market share, (2) one-level shifts in share (i.e., changes of about 100 percent), and (3) two-level shifts in market share (i.e., increases of 200 percent). In terms of functional area emphasis, most strategic turnarounds are built around key skills in marketing, production, and/or engineering.

Operating turnarounds are usually of four types, none of which require changing the firm's business-level strategy. These emphasize: increasing revenues,1 decreasing costs, decreasing assets, or a combination effort. Of course, these same categories

1These usually involve regaining lost position rather than increased penetration of the market. Most such increases vary between 10 and 90 percent, though larger increases of an operating character do occasionally occur.

Exhibit 1 Patterns of Decline and Turnaround Schendel, Ratton, and Riggs examined the patterns of decline and turnaround of fifty-four companies with average sales of $400 million that competed in seventeen different industrial sectors of the economy and forty different industries. They categorized the reasons for the declines and types of turnaround actions taken as follows: Strategic Causes Decreased Profit Margins Increased Wages Increased Competition Raw Material Supply

Management Difficulties Operating Causes Depressed Price Levels

Recessions

Strikes and Labor Problems Excess Plant Capacity

Strategic Responses Vertical Integration

Diversification Divestment Top Management Changes

Operating Responses* Major Plant Expenditures Functional Area Emphasis Improved Efficiency Ratios

* These researchers found that operating responses seldom cured strategic problems.

could also be used to describe strategic turnarounds. In strategic turnarounds, however, the focus is on the strategy changes sought. Performance becomes a derivative of the strategy change. In operating turnarounds, the primary focus is on the performance targets to be achieved. Any actions that can help achieve them are to be considered, whether they make good long-run strategic sense or not.

In practice, of course, the distinction between strategic and operating actions and turnarounds becomes blurred. Thus, actions that substantially decrease the firm's asset base also often require a change in strategy to be most effective, and so on. The distinction is still relevant, though, because of the different priorities and tradeoffs with short-term versus long-term actions in the two types of strategies.

The Nature of Turnaround Situations Traditionally, turnaround situations have been discussed either in terms of the areas of organization performance to be improved or the time criticality of the turnaround situation. Thus, the most frequently encountered turnaround situations have

TURNAROUND STRATEGIES 21

been those involving declines in organizational profitability, with those involving declines in sales or market share not far behind. Much less attention has been given to turnarounds involving improved asset utilization (ROI). With increasing inflation and interest rates, however, more attention has been given to such turnarounds recently. In most turnaround strategies, regardless of the performance area affected, the time criticality of the firm's situation is quite severe. There is some imminent danger to survival. The most likely reason for this is our "cultural" emphasis on adventure and danger; not all turnaround situations develop suddenly.

Unfortunately, these methods of classifying turnaround situations, while popular, are not the most useful for deciding on the type of turnaround to be selected in a particular situation. Much more useful are assessments of the current operating and strategic health of the organization.

In making each of these assessments, it is necessary to examine four different aspects of the firm's operations, namely its financial, market, technological, and production capabilities and position. Such analysis can become quite detailed and, therefore, cannot be covered completely in this article. A brief discussion of the key aspects of each is in order, though.

Assessing Current Operating Health

Financial Condition

One should check a company's current operating health before trying to assess its strategic health for one simple reason: The latter is irrelevant if the company goes bankrupt in the near term. Therefore, the first step in assessing a firm's current operating health is to look at its current financial condition. The purpose of such a diagnosis is to determine the following:

• How probable it is that the firm may go bankrupt in the near future without changes in its strategy.

• How much time is available before it would go bankrupt.

• The magnitude of the turnaround needed to avoid bankruptcy.

• The financial resources that could be raised short term to aid in the battle.

Over the years, every industry has developed a number of ratios, such as the current ratio and the quick ratio, to help assess liquidity. These can and should be used as a first cut at assessing the firm's short-term financial condition. Two much better

indicators of impending disaster, however, are pro forma cash-flow projections and a cash-flow breakeven chart, both of which should usually be calculated as a matter of routine in turnaround situations. The latter computation is particularly useful because, together with a net income break-even point, it indicates the magnitude of the turnaround effort that will be needed.2 One final calculation that should be made at this time is a projection of the cash that can be freed up by squeezing the firm's inventories and accounts receivable.

Before beginning a turnaround, make sure the going-concern value of the firm is substantially greater than its liquidation value.

Market Position

In terms of current market position, two calculations are relevant. One is a comparison of the size of the business' current product/market segments versus its break-even points. The second is an assessment of the maximum sales that could be achieved from all other products that the firm has made and still has the capacity to make.

The logic behind these calculations is quite simple. In the short term, it is seldom possible for a struggling firm to successfully introduce very many totally new products. These calculations, therefore, give a rough idea of whether the business can generate enough sales from its current and/or past products so that it can exceed its break-even point. If not, then the only feasible options are major asset reductions or liquidation.

Technological Stance

With respect to short-term technological position, two separate evaluations are necessary. The first is whether there is any new or modified products the development of which could be completed in one year if all the firm's R&D efforts were focused on

2 In the past decade, several sophisticated techniques for predicting the likelihood of bankruptcy have been developed. The best of these are Beaver's cash flow to total debt ratio test, Altman's Z-score, and Wilcox's probability of ultimate failure and linear gambler's ruin scores. See references for further information.

22 THE JOURNAL OF BUSINESS STRATEGY

them. If so, then the sales/profits of such products need to be considered as one of the turnaround options. If not, then product innovation should receive little or no attention in the near term unless one has outside sources of funds, say, a parent company, to pay for such efforts.

The second technological evaluation that needs to be made is of the relative quality of the firm's products. If these are about average, no efforts should be made to change the situation short term. If they are substantially above average, then the firm should consider the introduction of a lower-quality line through the use of lower-quality components or fewer features than in its existing line to capitalize on its quality image.

Alternatively, price increases might be possible if there is a real demand for the level of quality the firm is producing. The exact moves that should be made, however, must be carefully considered since they can have extremely long-term implications. Packard, for instance, destroyed its image by marketing a lower-quality "Packard" model to try to weather the depression.3 If the firm's products are viewed as substantially below average in quality and it cannot easily get its quality up, it may have no other option than liquidation.

3 The Packard example and many others like it suggest that if a lower price/quality line is introduced, a different brand name should usually be applied to it.

Production Capabilities

In terms of production capabilities, three short-term assessments must be made:

• First, the variable cost position of the business relative to its competition should be estimated. If it is too far out of line, either liquidation or long-term financial support from outside the business is usually the only viable option.

• Next, an evaluation has to be made of the facilities that absolutely must be replaced to continue in business in the short term.

• Finally, an assessment should be made of the facilities that could be sold off in the short term as well as the firms to whom they might be sold. If such sales seem at all likely, these determinations should be made as quickly as possible. The value that one can get for such facilities if they are sold before bankruptcy is four to five times what they will bring in a bankruptcy sale.

Assessing Current Strategic Health

Assessing an organization's current strategic health requires looking at the same areas but from a different perspective. For example, finances often dictate the moves that can or must be made in other functional areas in the short term. In the longer

TURNAROUND STRATEGIES 23

term, however, finances will usually take care of themselves if the business is healthy in terms of its markets, technology, and production facilities. Thus, finances are usually examined last when assessing the firm's current strategic health.

Product/Market Matrix

To assess its current strategic market position, a business should determine its position on a product/ market evolution/competitive position matrix, like the one shown in Exhibit 2. Two aspects of such an assessment deserve comment. First, if one's position is too weak, either liquidation or niche marketing is usually the only strategic option that is feasible. The reason for this is the economies of scale and/ or the technology that usually develops in an industry over time. Both raise the minimum absolute costs of competing in the industry. As a consequence, a business usually has to be a certain minimum size to hack it as a full-line producer. Even above that point, though, efforts to substantially expand one's share may be counterproductive unless one has developed some unique competitive advantages or is in the developmental or shakeout stages, when share increases are easier to achieve because of the changing bases of competition in the industry. In fact, without such conditions, some type of segmentation strategy is usually called for unless the problem is poor operating performance by one of the industry leaders. If the industry is approaching decline, then a market concentration/ asset reduction turnaround strategy may be preferable.

A business should assess its current strategic position in its distribution system(s). Quite often, the distribution systems appropriate for different products change as the industries producing them mature. A firm should, therefore, always keep its eyes open for possible opportunities and threats from changes in the distribution system of its industry.

Technological and Production Capabilities

A business should assess its strategic technological capabilities for each of the four dimensions indicated in Exhibit 3. Such assessments are used in two ways. First, they should be checked against the stage of product/market segment evolution in which the firm finds itself, since much research indicates that the type of technological developments that occur in an industry are strongly linked to stage of product/market evolution. Major product improvements are usually developed in the

Exhibit 3 Assessing Strategic Technological Position

Basic R&D on New Product Concepts Major Product Improvements

Product Modifications

Process Improvements

Leader Average Follower Copy Cat

None

growth and early shakeout stages of market development. Then during the late shakeout and maturity stages, product modifications and process improvements predominate. The development of entirely new product forms usually occurs late in the saturation stage. Thus, if a firm's R&D efforts are inconsistent with these findings, it usually indicates wastage of strategic resources and possible weaknesses that competitors could attack. Such strategies should also be consistent with the functional area emphasis the firm has chosen to pursue.

From a production perspective, two considerations tend to dominate all others with respect to the assessment of a firm's current strategic position. First, an evaluation must be made of when the business will need increases in capacity, and where and how it should try to meet these needs. In particular, its manufacturing system should be planned with careful attention to the size and specialization of plants and to whether they should be located near raw materials, labor, or markets. Consideration must also be given to the proportionate investment that should be made in plant and equipment and the firm's inventory and physical distribution system.

The second strategic production assessment that must be made is whether and to what degree experience curve phenomena are likely to influence the firm's cost structure. In particular, if a business is in an industry in which experience curve effects are relatively important, then it will need to determine its relative cost position as accurately as it can. It will have to project the degree of cost reduction that it will have to achieve in the future and design its turnaround strategy accordingly. For example, if experience curve effects are important

24 THE JOURNAL OF BUSINESS STRATEGY

and if the business currently has substantially higher costs than its competitors, it should not plan to compete on price. Instead it should consider a segmentation strategy in areas such as quality where it excels. Moreover, in terms of manufacturing, it should probably plan to subcontract its major parts production to suppliers to take advantage of their experience curve effects, which are probably better than those the firm could achieve on its 6wn. If experience curve effects are not important, then greater consideration should be given to designing flexibility into the firm's production system.

Financial Capabilities

Two calculations should be made regarding the long-term financial health of the business. First, the long-term investment needs of the business should be calculated based on its expected growth rate and planned asset structure. Then, its long-term internal cash flows should be projected to determine whether the turnaround is within the financial capability of the firm. If so, the only remaining task is to decide on the type of turnaround strategy to be pursued. If the needs exceed the funds available, one must either go back to determine the maximum possible growth rate and whether that will be consistent with all the other strategy elements or select a different type of turnaround strategy.

Selecting the Turnaround Strategy and Putting it in Motion In trying to decide the type of turnaround strategy that should be pursued in a particular situation, three questions should be asked:

• Is the business worth saving, or is it better to liquidate it now?

• If the business is worth saving, what is its current operating health?

• What is the business' current strategic health?

Question one requires two different calculations. First, can the business be profitable over the long term; can it earn a good return on the assets invested in it? A "yes" answer is not sufficient by itself, however. Before beginning a turnaround strategy, a company should also make sure that the going-concern value of the firm is substantially greater than its liquidation value. If not, it is usually better to liquidate the business right away than to invest the substantial energies required by a turnaround for only a marginal payoff.

Questions two and three require a detailed analysis of the company's operations as well as of the structure of the industry in which it operates. Once these assessments are completed, one can turn to the task of selecting the type of turnaround strategy to be followed.

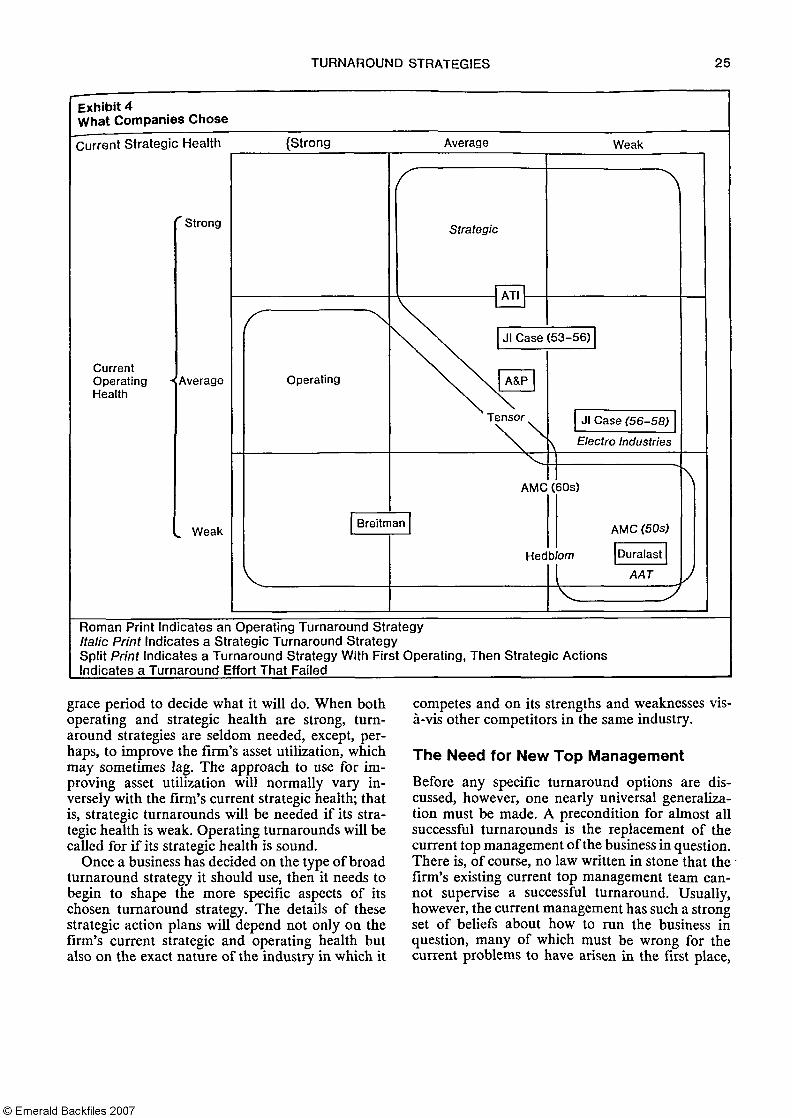

In general, the choice will vary according to the current operating and strategic health of the firm, as indicated in Exhibit 4. If both operating strategic factors are weak, liquidation is probably the best option unless the firm has no other businesses in which it could invest. In that case, a segmentation, niche, or asset reduction strategic turnaround with tight operating controls might be possible. Alternatively, a combination, revenue-increasing, or asset reduction operating turnaround might be attempted in the short term to be followed immediately by a strategic rebuilding effort. The choice of which approach would depend on the specifics of

Check your current operating health before assessing strategy health. The latter is irrelevant if the company goes bankrupt in the near term.

the situation. Before selecting the approach, however, the firm should make a final check of whether liquidation might not be the best option of all.

With a weak operating position and a moderate or strong strategic position, an operating turnaround strategy is usually needed, although divestiture/sale is sometimes also reasonable when the business' strategic position is only average.

With an average operating position and an average or weak strategic position, strategic turnaround is normally indicated. Usually, however, few firms explicitly consider turnaround efforts in the former circumstances, although this would be a most propitious time to do so. When a firm has a strong strategic position and average operating health, turnarounds are seldom needed. Occasionally, though, firms in such positions will undertake aggressive action plans to significantly improve their operating efficiencies.

When the business is strong operationally but weak strategically, a strategic turnaround is almost always indicated, although the firm may have a

TURNAROUND STRATEGIES 25

grace period to decide what it will do. When both operating and strategic health are strong, turnaround strategies are seldom needed, except, perhaps, to improve the firm's asset utilization, which may sometimes lag. The approach to use for improving asset utilization will normally vary inversely with the firm's current strategic health; that is, strategic turnarounds will be needed if its strategic health is weak. Operating turnarounds will be called for if its strategic health is sound.

Once a business has decided on the type of broad turnaround strategy it should use, then it needs to begin to shape the more specific aspects of its chosen turnaround strategy. The details of these strategic action plans will depend not only on the firm's current strategic and operating health but also on the exact nature of the industry in which it

competes and on its strengths and weaknesses visà-vis other competitors in the same industry.

The Need for New Top Management Before any specific turnaround options are discussed, however, one nearly universal generalization must be made. A precondition for almost all successful turnarounds is the replacement of the current top management of the business in question. There is, of course, no law written in stone that the firm's existing current top management team cannot supervise a successful turnaround. Usually, however, the current management has such a strong set of beliefs about how to run the business in question, many of which must be wrong for the current problems to have arisen in the first place,

26 THE JOURNAL OF BUSINESS STRATEGY

that the only way to get a more accurate view of the situation is to bring in new top management.

Moreover, increasing evidence from the experiences of General Electric and other similar multi-industry companies indicates that different general managers are skilled at different types of general management tasks. Consequently, the new top management team should be selected, to the degree possible, with the skills appropriate for the type of turnaround strategy that will be followed. For instance, a strategist/entrepreneur should be chosen if a high-growth, strategic turnaround is to be pursued, whereas a hard-nosed, experienced cost-cutter would be more appropriate if an operating turnaround with a major cost reduction effort is to be pursued.

Designing Operating Turnaround Strategies

Although the four different types of operating turnaround strategies—revenue-increasing strategies, cost-cutting strategies, asset reduction strategies, and combination strategies—may seem to correspond in some ways to the different types of strategic turnarounds noted above, attempts to make such a comparison are somewhat misleading. Any similarity is more one of results than of means and, as a consequence, usually exists only in the short term. A comparison of a typical one- or two-level share-increasing strategic turnaround with a typical revenue-increasing operating turnaround should help to illustrate these differences. In the former instance, the business involved would normally invest heavily in R&D, develop a new line of products, slightly overstaff in anticipation of future growth, and possibly change its methods of distribution and/or alter the basic character of its production system. In addition, its growth would be slow at first since the efforts being undertaken are long-term ones. Later, however, its sales would take off for a period of several years before slowing as it reached its new share position.

Revenue-Generating Strategies

In a typical revenue-generating operating turnaround, by contrast, the firm would focus primarily on its existing line of products, although it might supplement these with products it used to make but has discontinued, provided that these past products could be reintroduced quickly and profitably. In addition, the business might produce some products that it has no intention of ever making long term if

these helped utilize its facilities more fully in the short term. At the same time, R&D expenditures would be at moderate or low levels and staffing at low levels relative to sales. Some major efforts such as price cutting, increased advertising, or increased direct sales efforts would be undertaken to stimulate the current sales level. One other difference would also exist: In strategic turnarounds designed to shift share position, there would be few activities undertaken that were not related to the business's long-term direction. In addition, a balanced effort would be made among the two or three key success areas critical to the business' future operations. By contrast, in operating turnarounds designed to increase the firm's current revenues, almost total attention would be focused on a variety of short-term revenue-generating actions with little or no attention given to the other areas of the business. Moreover, a number of the revenue-generating actions undertaken might have no bearing on the long-term strategic health of the business. In short, strategic and operating turnarounds are really substantially different in character even though there sometimes appears to be a similarity in the short-term performance results they produce. Because of the primary focus on short-term operating actions, however, the first step in any operating turnaround should be to identify the resources and skills that the business will need in order to implement its long-term strategy so that these can be protected during the short-term action program that will follow.

Once these resources have been identified, the decision regarding the type of operating turnaround strategy to be followed should be based primarily on how close the firm is to its current break-even position, as indicated in Exhibit 5, although minor adjustments might be made depending on the firm's price/cost structure and its current financial situation.

Cost-Cutting Strategies

If the firm is relatively close to its current breakeven point, or if its sales are about 60 to 80 percent4

of break-even and it has high direct labor costs, high fixed expenses, or limited financial resources, then cost-cutting strategies are usually preferable. Moderately large short-term decreases in costs are usually possible, and cost-cutting actions produce results more quickly than revenue-generating or asset reduction strategies.

4 The percentages used here are approximate and will vary somewhat depending on the industry and firm involved.

TURNAROUND STRATEGIES 27

Asset Reduction Strategies At the opposite extreme, if the business' current sales are less than a third of its break-even, then the only viable option is usually an asset reduction strategy, especially if the business is close to bankruptcy. In such instances, the principal question is: "Which assets should be sold and which should be kept?" The answer depends on the firm's present/ future strategy and the salability of its different assets. As a general rule, the only assets that should be kept are those that the firm will definitely use within the next year or two. Unless bankruptcy is imminent, however, the sale of the remaining assets should be done with deliberateness rather than haste, because the rushed or forced sale of assets will often reduce the price the seller will get for them by 50 percent or more.

If the firm's current sales are between 30 and 60 percent of its current break-even point, then the most appropriate turnaround strategies are normally revenue-generating or asset reduction strategies. There is usually no way to reduce costs sufficiently to reach a new break-even point, and the

time and resources available to the firm are usually not adequate to attempt a combination strategy. The choice between revenue-generating and asset reduction strategies in such situations depends primarily on the long-term potential of the business after the turnaround is completed and on the criti-calness of the firm's financial situation. If the firm's potential is such that its present capacity will be used within a year or two of the turnaround and its finances are not yet desperate, then revenue-generating strategies should be pursued. If its finances are critical but the potential to use all of its existing capacity in the near term is also present, then the firm should follow a combination revenue-generating/asset reduction strategy. The principal focus, though, should be on revenue generation with asset sales limited to the level needed to meet the firm's cash-flow needs for the next three to six months. If the firm's longer-term sales potential is substantially less than its present capacity, however, an asset reduction strategy should be selected with the total amount of assets to be sold being determined by the firm's long-term potential.

28 THE JOURNAL OF BUSINESS STRATEGY

Combination Effort Strategies

Finally, when the firm's current sales are between about 50 and 80 percent of its break-even point, combination strategies are usually the most effective. However, if fixed costs or direct labor costs are low, revenue-generating strategies are sometimes even more effective. Under combination strategies, cost-reducing, revenue-generating, and asset reduction actions are pursued simultaneously and in relatively balanced proportions. The reason for this type of balanced effort is that the benefit/cost ratios for the best cost-reducing and asset reduction actions are substantially higher than those of the third, fourth, or fifth best revenue-generating actions and vice versa. Consequently, the cash flow produced by a balanced effort will be sufficiently higher than that which would be produced by a more narrowly focused strategy so that the greater complexities of a balanced effort are more than adequately compensated for. Such benefit/cost comparisons should be explicitly calculated before beginning any combination strategy. Without a substantial dollar advantage, a "single-focus" turnaround strategy is clearly preferable because of the magnitude and urgency of the various tasks that must be undertaken in any turnaround situation. There are, quite simply, more things to be done than there is time available to do them. Consequently, unless there is a clear and ever-present goal to guide organizational actions, such as revenue generation or cost reduction, it is quite likely that, because of past

Almost all successful turnarounds require the replacement of current top management.

interests and skills, a number of individuals will pursue profitable tasks beyond the point of diminishing returns. They may even focus their major attention on relatively unproductive tasks. Combination strategies are particularly susceptible to such problems because of their lack of a single, clear-cut goal. They should, therefore, be pursued only when the potential payoff more than adequately compensates for the additional managerial complexity and operational difficulties they entail.

No matter what type of operating turnaround strategy is followed, however, the limited financial resources and time urgency associated with most operational turnaround situations require that major attention be given to all actions that will have a substantial short-term cash-flow impact on the business involved. As a consequence, actions such as collecting receivables, cutting inventories, increasing prices when possible, focusing on high-margin products, stretching payables, decreasing wastage, and selling off surplus assets will/should almost always be pursued. Some will be a logical extension of the type of turnaround strategy selected. The others should be used ony if the timing and total impact of their cash-flow contributions warrant taking time away from the firm's chosen turnaround strategy. Among the best tools for addressing the latter question are sensitivity and elasticity analyses, pro forma cash-flow projections, and Donaldson's system for assessing the speed with which various organizational resources can be converted to cash in financial emergencies.

Designing Strategic Turnarounds

Strategic turnarounds are appropriate when the business has a noncrisis current operating position but has lost position strategically. It is possible that the business could be strategically weak only in its technological, production, or financial positions (situations that usually produce declines in profits and ROI) and not in its market position (or market share), but this is not normally the case. Instead, most strategic turnarounds involve circumstances in which there has been a major decline in sales and/ or share position. Consequently, the principal method of differentiating among strategic turnarounds is determined according to the magnitude of the sales and share reversal sought. Three options are possible:

• Maintenance or even reduction of share accompanied by the focusing of the business on one or more defensible product/market segments or niches;

• One-level increases in share position (i.e., move-ment from a dropout position to a follower position, from a follower position to a competitor position, or from a competitor position to a leader position); or

• Two-level increases in share position (i.e., movement from a dropout position to a competitor position or from a follower position to a leader position).

TURNAROUND STRATEGIES 29

Usually, however, two-level increases in share position or even one-level shifts that involve attempts to secure the leadership position are not possible unless the business has some substantial nonfinancial strategic resources that it has thus far failed to exploit, and access to discretionary strategic funds 50 to 100 percent more than it could normally generate on its own. One such source of

Too often, firms embark on turnaround efforts as a "knee-jerk" reaction to the myth that nothing can be worse than failure or liquidation.

funds is a corporate parent that is willing to fund heavy investments in areas of relative competitive advantage over long periods of time, as Philip Morris has done with Miller's Beer. Shifts of such magnitude are possible when the current leader slips, when there is a major change in stage of product/market evolution, or when the turnaround firm is a former leader which has recently fallen from that position.

Normally, therefore, the choice of a strategic turnaround strategy is between a one-level increase in share position or a segmentation or niche strategy. In most such instances, a segmentation/niche strategy will be more profitable in terms of ROI, EPS and other similar asset utilization measures of organizational performance—unless the business has unusual resources or the industry in which the firm competes is in the development or shakeout stages of product/market evolution. However, segmentation/niche strategies usually provide little or no opportunity for eventually seizing leadership in the industry involved. Such strategies usually produce lower dollar sales and net income totals than successful one-level, share-shifting turnaround strategies unless the segments selected for the new focus grow substantially. Consequently, most businesses attempt strategic turnarounds that involve seeking higher dollar sales through one-level shifts in share with a possible, though remote, opportunity for seizing industry leadership should competitors slip or environmental conditions change.

Optimally, of course, one would like to design a strategic turnaround strategy that would segment the market in such a way as to protect the firm from its competitors while at the same time permitting overall sales and share increases. Usually, however, such optimal strategic turnaround strategies are not possible unless there is a newly emerging segment to the market. Even then, the turnaround business must be able to develop superior products for that segment as well as upgrading its competencies in the other functional areas important for serving that segment. In addition, in order to be able to maintain any headstart it might get on its competitors, the firm involved needs to be able to differentiate itself from its key competitors in some lasting way—a most difficult task if its competitors have superior strategic resources.

The major conclusion that can be drawn from industry practice to date, however, is that too much attention is given to strategic turnarounds that involve one-level increases in share position and not enough to strategic turnarounds that involve segmentation and niche hunting.

Applications to Management Practice The proposed model is strongly corroborated by actual management practice in a variety of different companies and industries. In this regard, Exhibit 6 compares the actions taken by management and the performance results these actions produced with the strategy recommendations derived from the model for twelve different turnaround situations faced by ten different companies in ten different industries over the past thirty years. The result: In the six situations in which management's actions corresponded (either exactly or approximately) to the recommendations of the model, performance improved, whereas in the six situations in which management took actions inconsistent with the recommendations of the model, performance deteriorated even further.

Two observations can be made based on the data in Exhibit 6. First, it appears that management typically responds to a turnaround situation with an operating strategy. Specifically, in ten of the twelve situations examined, management used operating turnaround strategies and in the other two management decided to liquidate the businesses involved. Moreover, in one of those two situations, management had tried an operating turnaround

30 THE JOURNAL OF BUSINESS STRATEGY

Exhibit 6 Turnaround Strategies Performance Model

Company Involved

Breilman & Co. (1951-1954) J.I. Case (1953-1956)

American Motors (1954-1958)

J.I. Case (1957-1959)

American Motors (1961-1964) Aerosol Techniques, Inc. (1966-1975) Tensor Corp. (1966-1970)

Hedblom Corp. (1967-1970)

Duralast Products (1968-1972)

Electro-Industries (1971-1972)

American Automatic Typewriter (1971-1974)

A & P (1976-1978)

Current Operating Health

Weak

Average

Very weak

Average to weak

Weak

Average to strong

Average to weak

Very weak

Very weak

Average* to weak Very weak

Average

Current Strategic Health

Average to strong Average to weak

Weak

Weak

Weak to average Average

↓ weak Weak to average

Average to weak

Very weak

Very Weak

Very weak

Average to weak

Indicated Turnaround Strategy

Operating

Strategic

Operating

Strategic Strategic

Operating

Strategic

Strategic

Operating Operating

Strategic

Operating

Strategic Strategic

Operating

Strategic or liquidation Strategic

Actual Turnaround Strategy

Operating

Operating

Operating

Strategic Operating

Strategic

Operating

Operating

Operating

Strategic Operating

Strategic

Operating

Liquidation

Liquidation

Operating

Indicated Substrategy

Cost-cutting

Asset reduction & market concentration Combination + niche marketing

Asset reduction & market concentration

Revenue increasing Market segmentation

Market segmentation + revenue increasing Revenue increasing + one-level market share shifting Combination + market segmentation Niche marketing

Sale of assets

Market segmentation

Actual Substrategy

Revenue increasing Combination

Combination + niche marketing

Revenue increasing + one-level market share shifting Revenue increasing Combination

Combination + new markets

Revenue increasing + one-level market share shifting Revenue increasing

Use of assets elsewhere

Sale of assets

Revenue increasing

Performance Results Achieved

Firm went bankrupt ↓ Sales & BE profits

↑ Sales & profits

↑ Sales, but = 0 profits

↑ Sales & profits

↓ Sales & profits

↑ Sales & profits

↑ Sales & profits

Firm went bankrupt

Cessation of losses

Cessation of losses

Modest sales ↑ & profits

Corroboration of Model

+

+ +

+ +

+ +

+ +

+ +

+

+ +

+ +

+

+ +

+

* Weak if only major product line is considered

strategy before deciding upon liquidation. Overall, then, there appears to be a strong predisposition by management to adopt operating strategies and tactics to deal with turnaround situations, although it is also possible that the current sample is not completely representative of turnaround situations in general.

The second point can be seen even more dramatically from the data in Exhibit 6. It is that in the majority of the cases, four of six, in which a turnaround attempt failed, the problem appears to have been that management attempted an operating turnaround when a strategic turnaround was needed; whereas in the remaining instances, the problem would appear to have been that management attempted the wrong type of operating turnaround. Never, however, was there a failure because management attempted a strategic turnaround when an operating turnaround was needed. In fact, management seldom adopted strategic turnaround strategies at all. There are several possible reasons for this. One is that strategic actions normally take

longer to pay off. Perhaps equally important, however, is the "fact" that effective strategic moves are possible only at certain periods (called "strategic windows") in an industry's evolution, unless a competitor slips or the firm has some unusual strategic resources that it has thus far failed to utilize. The essence of the last observation is that firms usually have fewer opportunities to improve their strategic positions than they do to improve their operating efficiencies. However, even if both of these observations are true, it still appears that management is systematically overlooking or excessively discounting the benefits of strategic turnarounds in many situations.

Conclusion

The critical nature of most turnaround situations normally demands that managerial and organizational attention, effort, and resources be directed

TURNAROUND STRATEGIES 31

toward one or two overall strategies until the organization is "out of the woods." The failure to identify such strategies explicitly is a serious error. It can lead to the dissipation of organizational energy and resources in nonproductive or sometimes even counterproductive efforts.

Turnaround analysis is also critical, however, because the selection of an inappropriate/infeasible turnaround strategy may result in bankruptcy—a situation that is usually far worse than even immediate liquidation. Moreover, even when an inappropriate turnaround strategy does not cause bankruptcy, it normally so dissipates resources that the organization's post-turnaround condition is far less attractive than it would have been had the proper turnaround strategy been followed initially.

Before starting any turnaround, a firm should make an explicit calculation to determine whether it is worth attempting. Too often, firms embark on turnaround efforts as a "knee-jerk" reaction to the myth that nothing can be worse than failure (i.e., liquidation). Such is not the case, however, and in many instances stockholders, employees, and others with a stake in the organization would be better

served if management faced up to the true prospects and benefits of long-run survival and decided to liquidate the business.

Before a strategic turnaround is begun, an explicit investigation should be made of the conditions in the industry involved and, in particular, of its stage of evolution and competitive structure. The reason for such analysis is quite simple: Industry structure is not uniformly flexible at all points in time. There are times when strategic change abounds within an industry. During such periods, shifts in relative competitive position occur frequently. Consequently, appropriately designed strategic turnarounds have reasonably good chances of success during these periods. At other times, though, it is almost impossible to make major shifts in competitive position with the resources available to most firms in the industry. During these periods, strategic turnarounds should not be attempted unless the organization has access to substantial outside resources or unless there are special circumstances, such as a competitor asleep at the switch, that provide unique opportunities in an otherwise barren situation.

REFERENCES

Altman, Edward I. "Financial Ratios, Discriminant Analysis, and the Prediction of Corporate Bankruptcy." Journal of Finance (1968).

—. Corporate Bankruptcy in America. Lexington, MA: Heath-Lexington, 1971. —. "Zeta Analysis: A New Model to Identify Bankruptcy Risk of Corporations." Journal of Banking and Finance (1977). Beaver, William H. "Financial Ratios as Predictors of Failure." Empirical Research in Accounting: Selected Studies, Supplement

to Journal of Accounting Research (1966). —. "Alternative Accounting Measures as Predictors of Failure." The Accounting Review 43: 113-122 (1968). Donaldson, Gordon. Strategy of Financial Mobility. Boston: Harvard University, Graduate School of Business Administration,

Division of Research, 1969. —. "Strategy for Financial Emergencies." Harvard Business Review (Nov.-Dec. 1969). Kami, Michael J., and Ross, Joel E. Corporate Management in Crisis: Why the Mighty Fall. Englewood Cliffs, NJ: Prentice-Hall,

1973. Schendel, Dan G., Ratton, Richard, and Riggs. "Corporate Turnaround Strategies: A Study of Profit Decline and Recovery."

Journal of General Management 3 (1973). Wilcox, Jarrod W. "A Gambler's Ruin Prediction of Business Failure Using Accounting Data." Sloan Management Review (Spring

1971). —. "A Prediction of Business Failure Using Accounting Data," Empirical Research in Accounting: Selected Studies, Supplement

to Journal of Accounting Research (1973). —. "A Gambler's Ruin Approach to Business Risk." Sloan Management Review (Fall 1976).