Uncovered interest parity Uncovered interest parity and deviations from and deviations from

uncovered interest parityuncovered interest parity

The Academy of Economic Studies,The Academy of Economic Studies,Doctoral School of Finance and Doctoral School of Finance and

BankingBanking

MSc student, Costescu Silvia Mihaela

Dissertation paper Dissertation paper outlineoutline

The importance of uncovered interest parityThe importance of uncovered interest parityThe aims of the paperThe aims of the paperLiterature reviewLiterature reviewThe modelThe modelThe dataThe dataEmpirical analysisEmpirical analysis Concluding remarksConcluding remarksReferencesReferences

The importance of the The importance of the uncovered interest parityuncovered interest parity

UIP has an analytical importance and appears as a UIP has an analytical importance and appears as a key behavioral relationship in virtually all of the key behavioral relationship in virtually all of the prominent models of exchange rate determination.prominent models of exchange rate determination.

UIP is a key feature of linearized open-economy UIP is a key feature of linearized open-economy models, it reflects the market’s expectations of models, it reflects the market’s expectations of exchange rate changes and represents the starting exchange rate changes and represents the starting point for any analysis which depends on future point for any analysis which depends on future exchange rate values.exchange rate values.

Because there are reasons to believe that UIP will not Because there are reasons to believe that UIP will not hold precisely, an investor must be able to identify hold precisely, an investor must be able to identify the source of deviation and respond accordingly.the source of deviation and respond accordingly.

The aims of the paperThe aims of the paper

I propose to test the UIP hypothesis for Czech I propose to test the UIP hypothesis for Czech Republic, Cyprus, Poland, Romania and in Panel over Republic, Cyprus, Poland, Romania and in Panel over the sample period March 1999 – November 2007.the sample period March 1999 – November 2007.

If this hypothesis does not hold, I identify and If this hypothesis does not hold, I identify and calculate the deviations from uncovered interest calculate the deviations from uncovered interest parity. parity.

I identify which is the main component of UIP I identify which is the main component of UIP deviations for every country. deviations for every country.

I will try to explain why the deviations occur.I will try to explain why the deviations occur.

Literature reviewLiterature review A lot of paper, back to Fama(1984)A lot of paper, back to Fama(1984) test for uncovered test for uncovered

interest parity at distant horizons and evidence that interest interest parity at distant horizons and evidence that interest rate differentials tends to be negatively, rather than rate differentials tends to be negatively, rather than positively, correlated with future currency movements, positively, correlated with future currency movements, thereby wrongly predicting their direction.thereby wrongly predicting their direction.

Flood and Rose(2001) find considerably heterogeneity across Flood and Rose(2001) find considerably heterogeneity across countries and detect signs that uncovered interest parity at countries and detect signs that uncovered interest parity at the short horizon holds better in crisis countries, where both the short horizon holds better in crisis countries, where both exchange and interest rates display high volatility.exchange and interest rates display high volatility.

Cochrane(1999), Alexius(2001), Chinn and Meredith(2005), Cochrane(1999), Alexius(2001), Chinn and Meredith(2005), Chinn(2006) and Zhang(2006) suggest that uncovered Chinn(2006) and Zhang(2006) suggest that uncovered interest parity tends to hold for financial instruments of interest parity tends to hold for financial instruments of longer maturities.longer maturities.

For several industrialized countries, Gokey(1994) finds that For several industrialized countries, Gokey(1994) finds that movements in the real exchange rate are more important movements in the real exchange rate are more important than those in the risk premium to explain the deviations than those in the risk premium to explain the deviations from UIP.from UIP.

The modelThe model In the condition of risk free arbitrage, the ratio of the In the condition of risk free arbitrage, the ratio of the

forward to the spot exchange rate is equal the forward to the spot exchange rate is equal the interest differential between two countries. interest differential between two countries.

Covered Interest Parity (CIP) can be expressed as: Covered Interest Parity (CIP) can be expressed as: (1) (1) All variables are expressed in logarithms, whereAll variables are expressed in logarithms, where – – nominal spot exchange rate at time nominal spot exchange rate at time tt

expressed as the price, in “home-country” monetary expressed as the price, in “home-country” monetary units, of foreign exchange (EUR) ; units, of foreign exchange (EUR) ;

– – forward rate of s for a contract expiring k forward rate of s for a contract expiring k periods in the future;periods in the future;

– – k period nominal interest rate in home k period nominal interest rate in home country; country;

– – k period nominal interest rate in foreign k period nominal interest rate in foreign country (EA); country (EA);

ktkttktt iisf ,*

,,

kttf ,

kti ,

kti ,*

ts

The modelThe model

If the investors are risk averse, the If the investors are risk averse, the forward rate can differ from the expected forward rate can differ from the expected future spot rate by a risk premium. future spot rate by a risk premium.

Uncovered interest parity says that Uncovered interest parity says that changes in the expected exchange rate changes in the expected exchange rate equals the current interest differential, if equals the current interest differential, if the investors are risk-neutral: the investors are risk-neutral:

(2) (2) Where, is expected nominal spot Where, is expected nominal spot

exchange rate from period t to period t+k, exchange rate from period t to period t+k, expressed in logarithmexpressed in logarithm

ktkttktte iiss ,

*,,

kttes ,

The dataThe dataThe source of data is Eurostat, The National Bank of The source of data is Eurostat, The National Bank of Czech Republic, The National Bank of Cyprus, The Czech Republic, The National Bank of Cyprus, The National Bank of Poland and The National Bank of National Bank of Poland and The National Bank of Romania database. The periods covered areRomania database. The periods covered are: : MarchMarch 1999- November 2007.1999- November 2007. Empirical analysis has been Empirical analysis has been made using monthly data for:made using monthly data for:

The average nominal exchange rate, of four European The average nominal exchange rate, of four European Union currencies against the euro, namely the Czech Union currencies against the euro, namely the Czech koruna (CZK), the Cyprus pound (CYP), the Polish zloty koruna (CZK), the Cyprus pound (CYP), the Polish zloty (PLN) and the Romanian new leu (RON). Each exchange (PLN) and the Romanian new leu (RON). Each exchange rate is quoted as number of national currency units per rate is quoted as number of national currency units per euro.euro.

The average active money market interest rate used by The average active money market interest rate used by banks for the Czech koruna (CZK), the Cyprus pound banks for the Czech koruna (CZK), the Cyprus pound (CYP),the Polish zloty (PLN), the Romanian new leu (CYP),the Polish zloty (PLN), the Romanian new leu (RON) and EUR operations using maturities of 3 and 6 (RON) and EUR operations using maturities of 3 and 6 month.month.

Empirical analysisEmpirical analysis

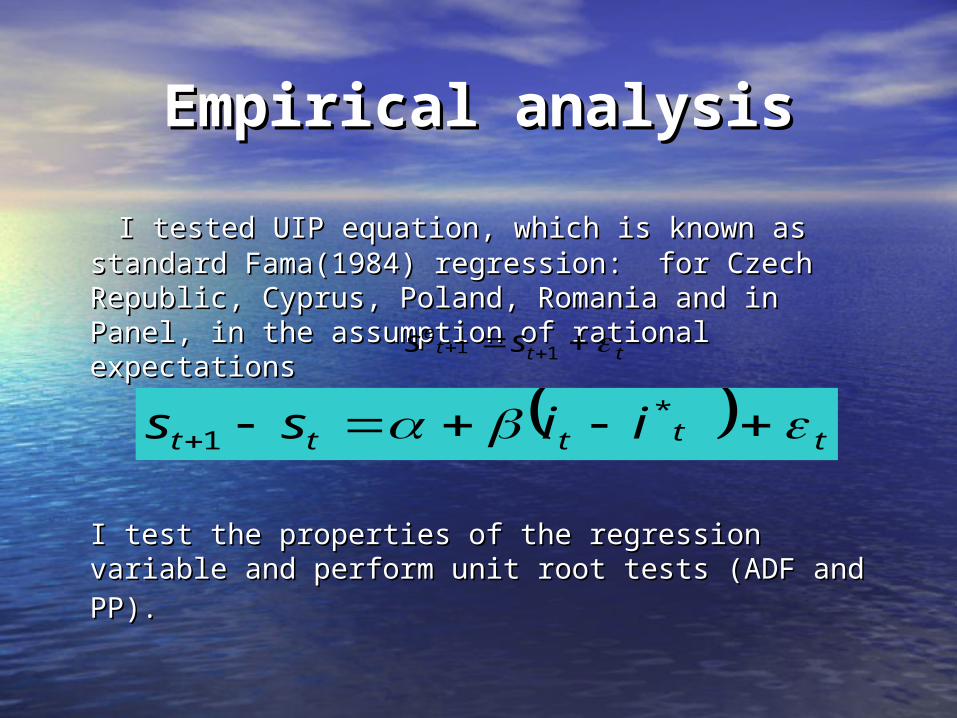

I tested UIP equation, which is known as I tested UIP equation, which is known as standard Fama(1984) regression: for Czech standard Fama(1984) regression: for Czech Republic, Cyprus, Poland, Romania and in Panel, Republic, Cyprus, Poland, Romania and in Panel, in the assumption of rational expectations in the assumption of rational expectations

I test the properties of the regression variable I test the properties of the regression variable and perform unit root tests (ADF and PP).and perform unit root tests (ADF and PP).

ttte ss 11

ttttt iiss *

1

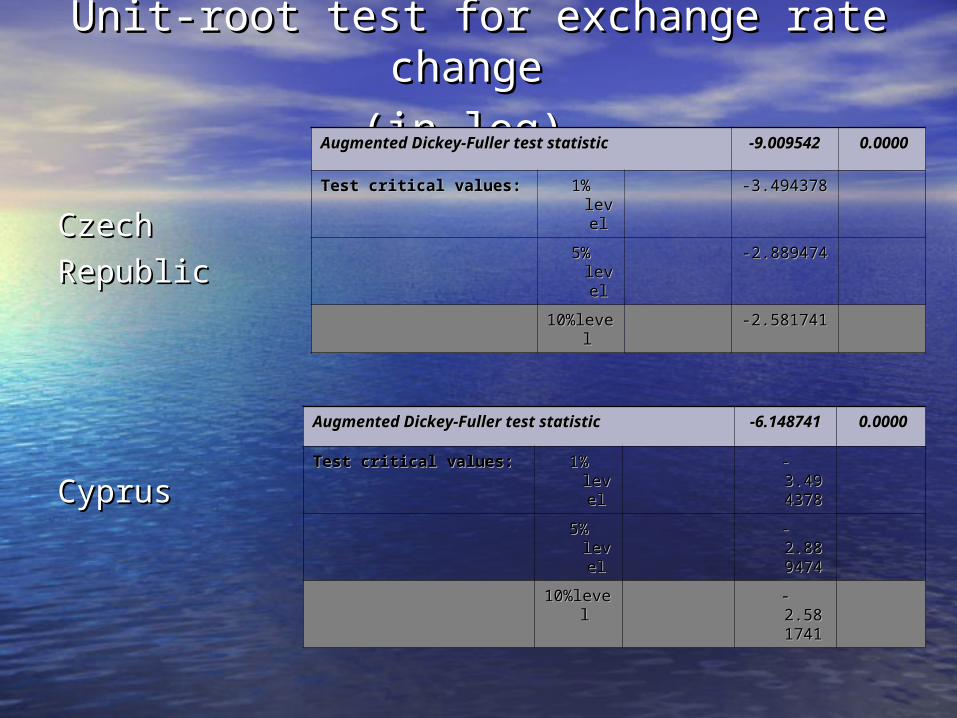

Unit-root test for exchange rate Unit-root test for exchange rate change change

(in log)(in log)

Czech Czech

RepublicRepublic

CyprusCyprus

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic --9.0099.009542542

0.00000.0000

Test critical values:Test critical values: 1% 1% levlevelel

-3.494378-3.494378

5% 5% levlevelel

-2.889474-2.889474

10%lev10%levelel

-2.581741-2.581741

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic --6.146.1487418741

0.00000.0000

Test critical values:Test critical values: 1% level1% level -3.494378-3.494378

5% level5% level -2.889474-2.889474

10%lev10%levelel

-2.581741-2.581741

Unit-root test for exchange rate Unit-root test for exchange rate change change (in log)(in log)

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic --7.107.1094269426

0.00000.0000

Test critical values: Test critical values:

1% level1% level --3.493.4943784378

5% level5% level --2.882.8894749474

10%leve10%level l

--2.582.5817411741

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic --4.524.5215361536

0.00030.0003

Test critical values:Test critical values: 1% level1% level -3.497029-3.497029

5% level5% level -2.890623-2.890623

10%leve10%levell

-2.582353-2.582353

Poland

Romania

Unit-root test for nominal interest rate Unit-root test for nominal interest rate

differential (in log) - 3 monthdifferential (in log) - 3 month maturities maturities

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-3.205539-3.205539 0.02250.0225

Test critical values:Test critical values: 1% level1% level -3.495021-3.495021

5% level5% level -2.889753-2.889753

10%level10%level -2.581890-2.581890

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-1.949065-1.949065 0.04940.0494

Test critical values:Test critical values: 1% level1% level -2.587607-2.587607

5% level5% level -1.943974-1.943974

10%level10%level -1.614676-1.614676

Czech Czech

RepublicRepublic

CyprusCyprus

Unit-root test for nominal interest rate Unit-root test for nominal interest rate

differential (in log) - 3 monthdifferential (in log) - 3 month maturities maturities

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-2.277253-2.277253 0.02270.0227

Test critical values:Test critical values: 1% level1% level -2.587607-2.587607

5% level5% level -1.943974-1.943974

10%level10%level -1.614676-1.614676

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-2.889941-2.889941 0.00420.0042

Test critical values:Test critical values: 1% level1% level -2.587607-2.587607

5% level5% level -1.943974-1.943974

10%level10%level -1.614676-1.614676

Poland

Romania

Estimates of βEstimates of β

MaturityMaturity

CurrencyCurrency 3 month3 month 6 month6 month

Czech korunaCzech koruna -0.010041-0.010041 -0.008061-0.008061

Cyprus poundCyprus pound -0.003079-0.003079 -0.003234-0.003234

Polish zlotyPolish zloty -0.007126-0.007126 -0.007568-0.007568

Romanian new leuRomanian new leu -0.014064-0.014064 -0.014675-0.014675

PanelPanel -0.046097-0.046097 -0.047345-0.047345

In line with Chinn and In line with Chinn and Meredith (2005) and Meredith (2005) and

Chinn (2006) I use GMM Chinn (2006) I use GMM to correct the standard to correct the standard errors of the parameter errors of the parameter estimates for MA serial estimates for MA serial correlation.correlation.

The coefficient is negative and the hypothesis that β equal unity is strongly rejected. A negative β coefficient suggests that interest rates differentials explain future currency movements systematically in the “wrong” direction. This is a standard result in empirical literature of international finance and constitutes the “forward discount puzzle”.

Mean, variance and t-ratio for Mean, variance and t-ratio for ex-ex-post deviations from UIPpost deviations from UIP 3 month3 month

Country Country Mean Mean VarianceVariance T-RatioT-Ratio

Czech RepublicCzech Republic 0.04990.0499 0.06600.0660 0.19410.1941

CyprusCyprus 0.32910.3291 0.04860.0486 1.49261.4926

PolandPoland 0.79750.7975 0.17920.1792 1.88391.8839

RomaniaRomania 1.66841.6684 0.57250.5725 2.20512.2051

I test the deviations from UIP to see if it works. The ex-post deviations from UIP are: xtxtxtt iisst *

I perform unit root tests (ADF and PP) for UIP deviation to see whether it fluctuates around the mean or drifts boundlessly.

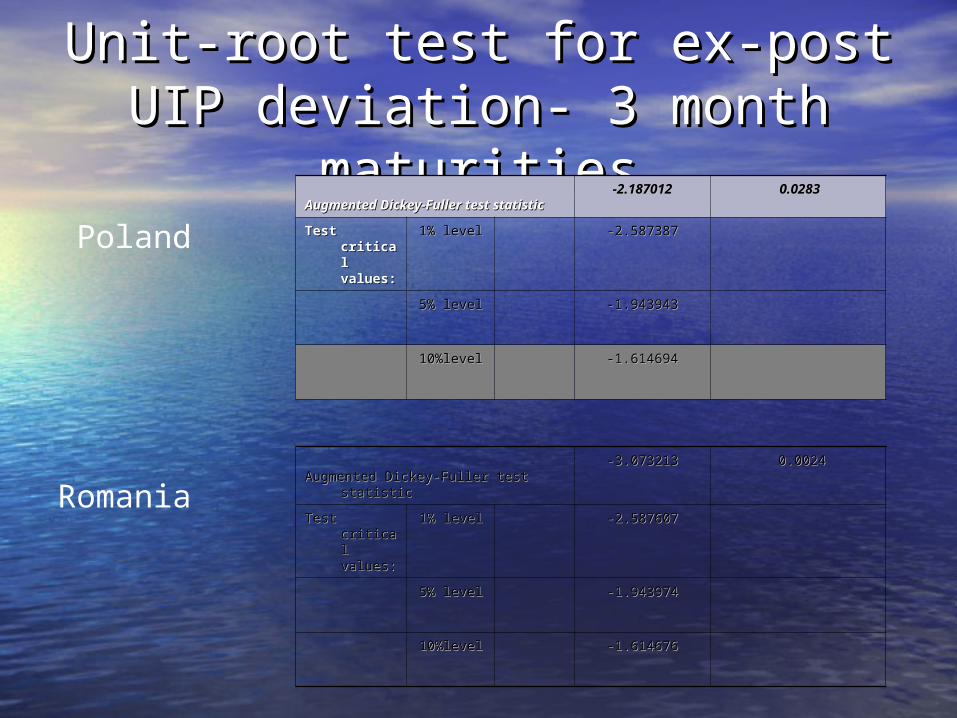

Unit-root test for ex-post UIP Unit-root test for ex-post UIP deviation- 3 month maturities deviation- 3 month maturities

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-3.489749-3.489749 0.00060.0006

Test critical values:Test critical values: 1% level1% level -2.587831-2.587831

5% level5% level -1.944006-1.944006

10%level10%level -1.614656-1.614656

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-1.953394-1.953394 0.04900.0490

Test critical values:Test critical values: 1% level1% level -2.587607-2.587607

5% level5% level -1.943974-1.943974

10%level10%level -1.614676-1.614676

Czech Czech

RepublicRepublic

CyprusCyprus

Unit-root test for ex-post UIP Unit-root test for ex-post UIP deviation- 3 month maturitiesdeviation- 3 month maturities

Augmented Dickey-Fuller test Augmented Dickey-Fuller test statisticstatistic

-2.187012-2.187012 0.02830.0283

Test critical Test critical values:values:

1% level1% level -2.587387-2.587387

5% level5% level -1.943943-1.943943

10%level10%level -1.614694-1.614694

Augmented Dickey-Fuller test statisticAugmented Dickey-Fuller test statistic-3.073213-3.073213 0.00240.0024

Test critical Test critical values:values:

1% level1% level -2.587607-2.587607

5% level5% level -1.943974-1.943974

10%level10%level -1.614676-1.614676

Poland

Romania

Ex-post deviations from UIPEx-post deviations from UIP

I can conclude that UIP works only for I can conclude that UIP works only for Czech Republic, because is the only one Czech Republic, because is the only one who has the mean of the UIP deviation not who has the mean of the UIP deviation not statistically different from zero, the t-ratio statistically different from zero, the t-ratio very low and less than unity and both ADF very low and less than unity and both ADF and PP tests suggest that ω is stationary. and PP tests suggest that ω is stationary.

Similar results for 6 month horizon Similar results for 6 month horizon

Deviations from UIPDeviations from UIP

Fama(1984) suggest that deviations from UIP represent either a Fama(1984) suggest that deviations from UIP represent either a risk premium ( as measured by the real interest differentials) or an risk premium ( as measured by the real interest differentials) or an unexpected change in the real exchange rate: unexpected change in the real exchange rate:

The exchange rate growth can be written as: The exchange rate growth can be written as: Where, is the matrix of variables known at or before time t, Where, is the matrix of variables known at or before time t,

including inflation rate differential, nominal exchange rate including inflation rate differential, nominal exchange rate changes and nominal interest rate differential and is vector changes and nominal interest rate differential and is vector of corresponding coefficients.of corresponding coefficients.

I first estimate the equation with all the predictable variable, then I first estimate the equation with all the predictable variable, then

I eliminate the variable that are not statistically significant I eliminate the variable that are not statistically significant (nominal interest rate differential for all the countries and nominal (nominal interest rate differential for all the countries and nominal exchange rate changes for Cyprus), and I obtained: exchange rate changes for Cyprus), and I obtained:

ttt q

ttixtq 0

t

i

The exchange rate growth equationThe exchange rate growth equation

Dependent Variable: DQT_CZECHDependent Variable: DQT_CZECHMethod: Least SquaresMethod: Least SquaresDate: 07/07/08 Time: 22:18Date: 07/07/08 Time: 22:18Sample: 1999M03 2007M11Sample: 1999M03 2007M11Included observations: 105Included observations: 105

VariableVariable CoefficientCoefficient Std. ErrorStd. Error t-Statistict-Statistic Prob. Prob.

CC 0.0026110.002611 0.0010460.001046 2.4956692.495669 0.01420.0142

DIF_INFL_CZECDIF_INFL_CZECHH -0.001072-0.001072 0.0003980.000398 -2.694454-2.694454 0.00820.0082

DST_CZECHDST_CZECH 0.9881510.988151 0.0510130.051013 19.3705419.37054 00

R-squaredR-squared 0.7975140.797514 Mean dependent varMean dependent var -0.003255-0.003255

Adjusted R-Adjusted R-squaredsquared 0.7935440.793544 S.D. dependent varS.D. dependent var 0.01240.0124

S.E. of S.E. of regressionregression 0.0056340.005634 Akaike info criterionAkaike info criterion -7.491831-7.491831

Sum squared Sum squared residresid 0.0032380.003238 Schwarz criterionSchwarz criterion -7.416004-7.416004

Log likelihoodLog likelihood 396.3211396.3211 F-statisticF-statistic 200.8695200.8695

Durbin-Watson Durbin-Watson statstat 1.9488761.948876 Prob(F-statistic)Prob(F-statistic) 00

The exchange rate growth equationThe exchange rate growth equationDependent Variable: DQT_CYPRUSDependent Variable: DQT_CYPRUS

Method: Least SquaresMethod: Least Squares

Date: 07/07/08 Date: 07/07/08

Time: 13:11Time: 13:11

Sample: 1999M03 2007M11Sample: 1999M03 2007M11

Included observations: 105Included observations: 105

VariableVariable CoefficientCoefficient Std. ErrorStd. Error t-Statistict-Statistic Prob. Prob.

CC 0.0053830.005383 0.0020360.002036 2.6436452.643645 0.00950.0095

DIF_INFL_CYPRUSDIF_INFL_CYPRUS -0.001003-0.001003 0.0003990.000399 -2.516111-2.516111 0.01340.0134

R-squaredR-squared 0.0579050.057905 Mean dependent varMean dependent var 0.0006670.000667

Adjusted R-squaredAdjusted R-squared 0.0487590.048759 S.D. dependent varS.D. dependent var 0.0083590.008359

S.E. of regressionS.E. of regression 0.0081530.008153 Akaike info criterionAkaike info criterion -6.762087-6.762087

Sum squared residSum squared resid 0.0068460.006846 Schwarz criterionSchwarz criterion -6.711536-6.711536

Log likelihoodLog likelihood 357.0096357.0096 F-statisticF-statistic 6.3308176.330817

Durbin-Watson statDurbin-Watson stat 1.5879921.587992 Prob(F-statistic)Prob(F-statistic) 0.0134090.013409

The exchange rate growth equationThe exchange rate growth equationDependent Variable: DQT_POLANDDependent Variable: DQT_POLANDMethod: Least SquaresMethod: Least Squares Date: 07/07/08 Date: 07/07/08 Time: 22:23Time: 22:23 Sample: 1999M03 2007M11Sample: 1999M03 2007M11 Included observations: 105Included observations: 105

VariableVariable CoefficientCoefficient Std. ErrorStd. Error t-Statistict-Statistic Prob. Prob.

CC 0.0082180.008218 0.0013610.001361 6.0371926.037192 0.00000.0000

DIF_INFL_POLANDDIF_INFL_POLAND -0.000598-0.000598 0.0001090.000109 -5.491140-5.491140 0.00000.0000

DST_POLANDDST_POLAND 0.9802150.980215 0.0178680.017868 54.8594354.85943 0.00000.0000

R-squaredR-squared 0.9676750.967675 Mean dependent varMean dependent var -0.000591-0.000591

Adjusted R-squaredAdjusted R-squared 0.9670410.967041 S.D. dependent varS.D. dependent var 0.0220290.022029

S.E. of regressionS.E. of regression 0.0039990.003999 Akaike info criterionAkaike info criterion -8.177290-8.177290

Sum squared residSum squared resid 0.0016310.001631 Schwarz criterionSchwarz criterion -8.101462-8.101462

Log likelihoodLog likelihood 432.3077432.3077 F-statisticF-statistic 1526.7281526.728

Durbin-Watson statDurbin-Watson stat 1.8916121.891612 Prob(F-statistic)Prob(F-statistic) 0.0000000.000000

The exchange rate growth equationThe exchange rate growth equation

Dependent Variable: DQT_ROMANIADependent Variable: DQT_ROMANIAMethod: Least SquaresMethod: Least Squares Date: 07/07/08 Date: 07/07/08 Time: 22:24Time: 22:24 Sample: 1999M03 2007M11Sample: 1999M03 2007M11 Included observations: 105Included observations: 105

VariableVariable CoefficientCoefficient Std. ErrorStd. Error t-Statistict-Statistic Prob. Prob.

CC 0.0303150.030315 0.0018910.001891 16.0295016.02950 0.00000.0000

DIF_INFL_ROMANIADIF_INFL_ROMANIA -9.66E-05-9.66E-05 8.35E-068.35E-06 -11.57491-11.57491 0.00000.0000

DST_ROMANIADST_ROMANIA 1.0837561.083756 0.0386020.038602 28.0750328.07503 0.00000.0000

R-squaredR-squared 0.9323460.932346 Mean dependent varMean dependent var 0.0203330.020333

Adjusted R-squaredAdjusted R-squared 0.9310190.931019 S.D. dependent varS.D. dependent var 0.0288520.028852

S.E. of regressionS.E. of regression 0.0075780.007578 Akaike info criterionAkaike info criterion -6.899066-6.899066

Sum squared residSum squared resid 0.0058570.005857 Schwarz criterionSchwarz criterion -6.823238-6.823238

Log likelihoodLog likelihood 365.2010365.2010 F-statisticF-statistic 702.8334702.8334

Durbin-Watson statDurbin-Watson stat 1.7954311.795431 Prob(F-statistic)Prob(F-statistic) 0.0000000.000000

Deviations from UIPDeviations from UIP

Tanner(1998) decomposes ex-post deviations from UIP into unanticipated Tanner(1998) decomposes ex-post deviations from UIP into unanticipated and anticipated component of real exchange rate growth: and anticipated component of real exchange rate growth:

(resid series for every above equations),(resid series for every above equations), (the difference between real exchange rate growth and (the difference between real exchange rate growth and

resid series)resid series) The deviation from UIP can be written: ω = ρ + ε + θ The deviation from UIP can be written: ω = ρ + ε + θ Nothing that cov(ε,θ)=0, I can write the variance equation of ω as:Nothing that cov(ε,θ)=0, I can write the variance equation of ω as: var(ω)= var(ρ)+ var (ε) + var (θ) +2[ cov(ρ,ε)+ cov(ρ,θ)]var(ω)= var(ρ)+ var (ε) + var (θ) +2[ cov(ρ,ε)+ cov(ρ,θ)]

This equation tell us how much of the variance in ω is due to changes in This equation tell us how much of the variance in ω is due to changes in

the real interest rate differential, anticipated changes in the real exchange the real interest rate differential, anticipated changes in the real exchange rate and unanticipated real exchange rate growth, or the covariance rate and unanticipated real exchange rate growth, or the covariance between interest rate differential and every component of exchange rate between interest rate differential and every component of exchange rate growth. growth.

titt q *0 tit *0

Variance of deviationsVariance of deviationsVariance and covariance for 3 months

CountriesCountries var(ω)var(ω) var(ρ)var(ρ) varvar ( (εε)) var (θ)var (θ) covcov((ρρ,ε),ε) covcov((ρρ,θ),θ)

Czech RepublicCzech Republic 0.0005300.000530 0.0003380.000338 0.0000310.000031 0.0001230.000123 -0.000001-0.000001 0.0000200.000020

CyprusCyprus 0.0005550.000555 0.0004260.000426 0.0000660.000066 0.0000040.000004 -0.000009-0.000009 0.0000380.000038

PolandPoland 0.0040140.004014 0.0034270.003427 0.0000160.000016 0.0004700.000470 0.0000200.000020 0.0000300.000030

RomaniaRomania 0.1352030.135203 0.1235620.123562 0.0000560.000056 0.0007760.000776 0.0000200.000020 0.0000300.000030

Variance and covariance as a fraction of var(ω) for 3 months

CountriesCountries %var(ρ)%var(ρ) % var% var ( (εε)) % var (θ)% var (θ) %%covcov((ρρ,ε),ε) %%covcov((ρρ,θ),θ)

Czech RepublicCzech Republic 0.6380370.638037 0.0587940.058794 0.2315660.231566 -0.001917-0.001917 0.0373780.037378

CyprusCyprus 0.7680620.768062 0.1186400.118640 0.0072920.007292 -0.015389-0.015389 0.0678880.067888

PolandPoland 0.8539000.853900 0.0039080.003908 0.1169930.116993 0.0049290.004929 0.0075510.007551

RomaniaRomania 0.9138960.913896 0.0004170.000417 0.0057400.005740 0.0030570.003057 0.0365360.036536

Variance of deviationsVariance of deviationsVariance and covariance for 6 months

CountriesCountries var(ω)var(ω) var(ρ)var(ρ) varvar ( (εε)) var (θ)var (θ) covcov((ρρ,ε),ε) covcov((ρρ,θ),θ)

Czech RepublicCzech Republic 0.0005160.000516 0.0003240.000324 0.0000310.000031 0.0001230.000123 -0.00000006-0.00000006 0.0000200.000020

CyprusCyprus 0.0005540.000554 0.0004260.000426 0.0000660.000066 0.0000040.000004 -0.000009-0.000009 0.0000380.000038

PolandPoland 0.0039170.003917 0.0033410.003341 0.0000160.000016 0.0004700.000470 0.0000200.000020 0.0000300.000030

RomaniaRomania 0.1233110.123311 0.1119960.111996 0.0000560.000056 0.0007760.000776 0.0003690.000369 0.0049400.004940

Variance and covariance as a fraction of var(ω) for 6 months

CountriesCountries %var(ρ)%var(ρ) % var% var ( (εε)) % var (θ)% var (θ) %%covcov((ρρ,ε),ε) %%covcov((ρρ,θ),θ)

Czech RepublicCzech Republic 0.6285730.628573 0.0603630.060363 0.2377450.237745 -0.000124-0.000124 0.0383750.038375

CyprusCyprus 0.7688440.768844 0.1189130.118913 0.0073090.007309 -0.016066-0.016066 0.0680330.068033

PolandPoland 0.8529400.852940 0.0040040.004004 0.1198730.119873 0.0052090.005209 0.0077370.007737

RomaniaRomania 0.9082400.908240 0.0004570.000457 0.0062940.006294 0.0029920.002992 0.0400590.040059

Concluding remarksConcluding remarks In the covered period the results confirm the rejection of In the covered period the results confirm the rejection of

uncovered interest parity, for Czech Republic, Cyprus, Poland uncovered interest parity, for Czech Republic, Cyprus, Poland and Romania.and Romania.

I calculate UIP deviations and found that for analyzed countries I calculate UIP deviations and found that for analyzed countries real interest differential is the main component of UIP deviations.real interest differential is the main component of UIP deviations.

The interest rate differential accounts for nearly 64%(Czech The interest rate differential accounts for nearly 64%(Czech Republic), 77%(Cyprus), 85%(Poland), 91%(Romania) of Republic), 77%(Cyprus), 85%(Poland), 91%(Romania) of deviations from UIP.deviations from UIP.

These results are in line with developing countries, and one These results are in line with developing countries, and one explanation can be the variability of inflation in these countries, explanation can be the variability of inflation in these countries, and the fact that the prices rise rapidly.and the fact that the prices rise rapidly.

For Czech Republic and Cyprus I obtain the negative covariance For Czech Republic and Cyprus I obtain the negative covariance between interest rate differential and unanticipated real between interest rate differential and unanticipated real exchange rate growth, implying that changes in the real interest exchange rate growth, implying that changes in the real interest differential will be offset to some degree by movements in real differential will be offset to some degree by movements in real exchange rate growth, thus reducing the deviations from UIP. exchange rate growth, thus reducing the deviations from UIP.

Selected ReferencesSelected References Alexius A(2001), “Uncovered Interest Parity Revised”, Alexius A(2001), “Uncovered Interest Parity Revised”,

Review of International Economics”,9(3).Review of International Economics”,9(3). Cochrane, J (1999),”New Facts in Finance”, Economic Cochrane, J (1999),”New Facts in Finance”, Economic

Perspectives, Federal Reserve Bank of Chicago, XXIII(3).Perspectives, Federal Reserve Bank of Chicago, XXIII(3). Chaboud, A and J Wright(2005), : Uncovered Interest Parity: Chaboud, A and J Wright(2005), : Uncovered Interest Parity:

It works, but not for Long”, Journal of International It works, but not for Long”, Journal of International Economics, 66Economics, 66

Edison H. J. and Pauls B.D(1993) “A Re-Assessment of the Edison H. J. and Pauls B.D(1993) “A Re-Assessment of the Relationship Between Real Exchange Rates and Retal Relationship Between Real Exchange Rates and Retal Interest Rates: 1974-1990”, Interest Rates: 1974-1990”, Journal of Monetary Economics Journal of Monetary Economics 31,31,165-187165-187

Engel, Charles (2000), „Comments on Obstfeld and Rogoff’s Engel, Charles (2000), „Comments on Obstfeld and Rogoff’s “The Six MajorPuzzles in International Macroeconomics: Is “The Six MajorPuzzles in International Macroeconomics: Is There a Common Cause?””, NBER working paper 7818There a Common Cause?””, NBER working paper 7818

Fama E. (1984), “Forward and Spot Exchange RateS”, Fama E. (1984), “Forward and Spot Exchange RateS”, Journal of Monetary Economics, 14.Journal of Monetary Economics, 14.

Flood R. and A. Rose(2001)-“Uncovered Interest Parity in Flood R. and A. Rose(2001)-“Uncovered Interest Parity in Crisis:The interest Rate Defense in the 1990s”, IMF Working Crisis:The interest Rate Defense in the 1990s”, IMF Working Paper. No 01/207Paper. No 01/207

Selected ReferencesSelected References Froot K. And R. Thaler(1990), “Foreign exchange “, Journal of Froot K. And R. Thaler(1990), “Foreign exchange “, Journal of

Economic Perspectives, 4Economic Perspectives, 4 Gorkey T. C.(1994), “What explains the risk premium in foreign Gorkey T. C.(1994), “What explains the risk premium in foreign

exchange returns?” Journal of International Money and Finance13,6exchange returns?” Journal of International Money and Finance13,6 McCallum, Bennett T. (1992), „A Reconsideration of the Uncovered McCallum, Bennett T. (1992), „A Reconsideration of the Uncovered

Interest ParityRelationship”, NBER working paper 4113Interest ParityRelationship”, NBER working paper 4113 MacDonald R.(1997)“What Determines Real Exchange Rates: The MacDonald R.(1997)“What Determines Real Exchange Rates: The

Long and Short of It, “ IMF Working Paper 97/21(Washington: Long and Short of It, “ IMF Working Paper 97/21(Washington: International Monetary Fund)International Monetary Fund)

Marston R(1997),” Tests of three parity conditions: distinguishing Marston R(1997),” Tests of three parity conditions: distinguishing risk premia and systematic forecast errors”, Journal of International risk premia and systematic forecast errors”, Journal of International Money and Finance,16,2.Money and Finance,16,2.

Menzie D. Chinn, Guy Meredith(2005),“ Testing uncovered interest Menzie D. Chinn, Guy Meredith(2005),“ Testing uncovered interest parity at short and long horizons during the post-breton woods era” parity at short and long horizons during the post-breton woods era” –NBER working paper 11077.–NBER working paper 11077.

Meese R and Rogoff K (1988) “Meese R and Rogoff K (1988) “ What IS Real? The Exchange Rate-What IS Real? The Exchange Rate-Interest Differential Relation Over the Modern Floating- Rate Interest Differential Relation Over the Modern Floating- Rate Period” Period” Journal of Finance, Journal of Finance, Vol XLIII, No. 4, pp 933-948Vol XLIII, No. 4, pp 933-948

Tanner, Evan (1998), „Deviations From Uncovered Interest Parity: Tanner, Evan (1998), „Deviations From Uncovered Interest Parity: A Global Guide to Where the Action Is”, IMF working paper A Global Guide to Where the Action Is”, IMF working paper wp/98/117.wp/98/117.