FEATURE ARTICLE

1 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

By Monetary Management Department

Understanding Foreign Exchange Derivatives Using Trade Repository Data: The non-deliverable Forward market

1 BasedonturnoverstatisticsfromBankforInternationalSettlements(BIS)(2016),TriennialCentralBankSurvey–ForeignExchangeTurnoverinApril2016(www.bis.org/publ/rpfx16fx.pdf)andinternalcalculationsusingHKTRdata.

2 Formoreinformationonthedatausedinthisarticle,seeBox3:Traderepositoriesasadatasource.

1. Introduction

Inrecentyears,HongKonghasestablishedaregulatoryframeworkforover-the-counter(OTC)derivativesconsistentwithglobalstandards,andimplementedreformsinregulatoryreporting,centralclearing,aswellascapitalandmarginrequirementsonunclearedderivatives.ThesedevelopmentsareinlinewiththeG20commitmentin2009toenhancetransparencyandreducesystemicriskintheOTCderivativesmarket.

StartingfromJuly2017,undertherequirementofregulatoryreporting,allentitiessupervisedbytheHKMAorregulatedbytheSecuritiesandFuturesCommission(SFC),andcertaincentralcounterparties(CCPs),havetoreporttheirOTCderivativestransactionsinthefiveassetclassesofinterestrate,foreignexchange(FX),credit,equityandcommodity.Amongtheseassetclasses,themandatoryreportingofinterestrateswapsandFXnon-deliverableforwards(NDFs)startedtwoyearsearlierinJuly2015.

HongKongisamajortradingcentreforFXderivatives,andNDFsinparticular,withanestimated10%ofglobalturnoverofFXderivativestradingand30%ofNDFtrading.1SimilartootherFXderivatives,theNDFisaforwardcontractforhedgingcurrencyriskorprofitingfromcurrencyvolatility,albeitsubjecttoadifferentsettlementprocessthatmakesitsuseattractiveforcertaincurrencies(seeBox1formoredetail).NDFsrepresentanestimated16%oftheoverallFXderivativesmarketinHongKongbygrossnotionalvalue.

ThisarticlepresentsadescriptionoftheNDFmarketasseenthroughthedatacollectedinHongKongatthebeginningof2018,andsetsoutthemajordevelopmentsinthemarketoverthetwoyearsof2016–2017.Theresultsarederivedfromanalysisoftrade-leveldatareportedtotheHongKongTradeRepository(HKTR).2Intermsofmarketstructure,theNDFmarketismostlytradedatveryshortmaturities.Themajornon-deliverablecurrenciesaretheTaiwanesedollar,theKoreanwonandtherenminbi.Mostoftheoutstandingpositionsareheldbybanksandotherfinancialentities.Overthepasttwoyears,theNDFmarketexperiencedthreemajorchanges:amarkedincreaseincentralclearing;achangeincurrencycomposition;andanincreasinginvolvementbyotherfinancialinstitutionsrelativetobanks.

Box 1

nDF: What is it?

TheNDFisaforwardcontractwithadifferentsettlementprocess.Asinastandardforwardcontract,twocounterpartiesagreetobuy/sellacurrencyataspecifiedfuturedateatanagreedexchangerate.Thepurposeistolockinanexchangerateforacertainperiodinthefuture.Atsettlement,insteadofexchangingtheunderlyingcurrencies,NDFcounterpartiessettlethetrade’sprofitorlossinawidelytraded(“deliverable”)currency,mostoftentheUSdollar.Theamountsettledisthedifferencebetweentheexchangerateagreedinthecontractandtheprevailingexchangerateobservedataspecifiedfuturedate,multipliedbytheagreednotionalamount.Themostprevalentnon-deliverablecurrenciesareAsianandLatinAmericancurrencies.

2 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

2. StylisedfactsontheNDFmarket

a. SizeoftheNDFmarket

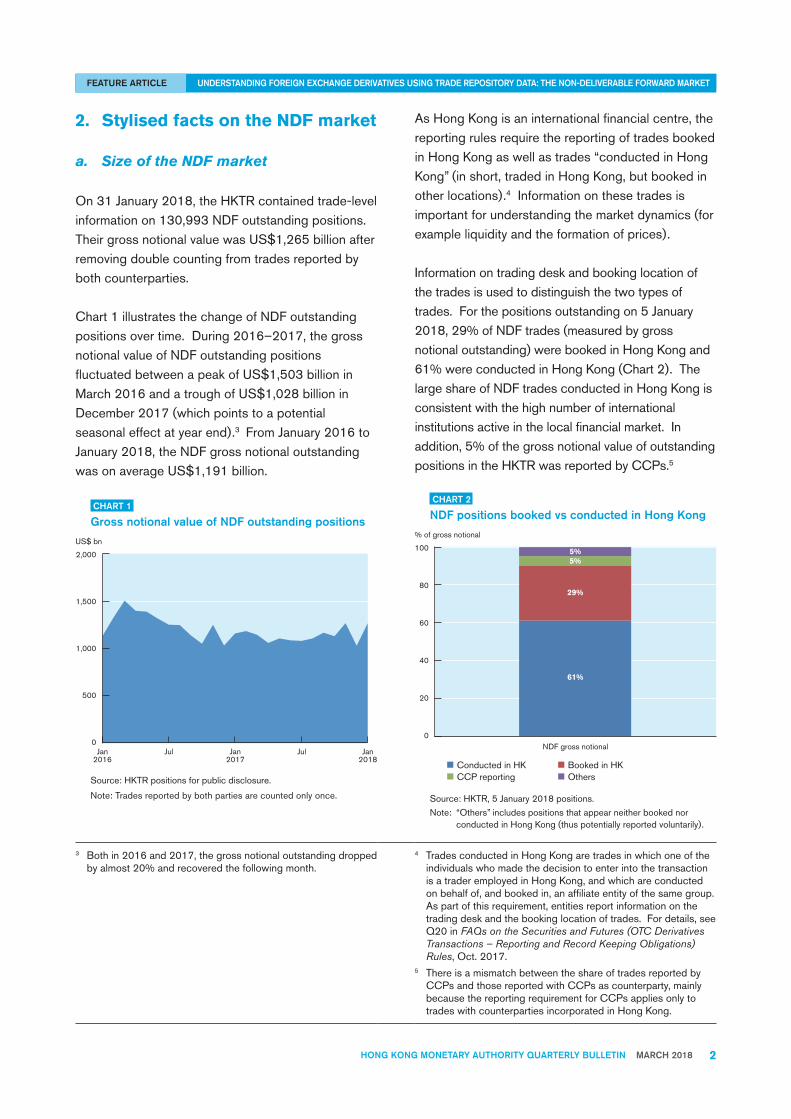

On31January2018,theHKTRcontainedtrade-levelinformationon130,993NDFoutstandingpositions.TheirgrossnotionalvaluewasUS$1,265billionafterremovingdoublecountingfromtradesreportedbybothcounterparties.

Chart1illustratesthechangeofNDFoutstandingpositionsovertime.During2016–2017,thegrossnotionalvalueofNDFoutstandingpositionsfluctuatedbetweenapeakofUS$1,503billioninMarch2016andatroughofUS$1,028billioninDecember2017(whichpointstoapotentialseasonaleffectatyearend).3FromJanuary2016toJanuary2018,theNDFgrossnotionaloutstandingwasonaverageUS$1,191billion.

CHART 1

gross notional value of nDF outstanding positions

0

500

1,000

2,000

1,500

US$ bn

Jan2016

Jul Jan2017

Jul Jan2018

Source:HKTRpositionsforpublicdisclosure.

Note:Tradesreportedbybothpartiesarecountedonlyonce.

AsHongKongisaninternationalfinancialcentre,thereportingrulesrequirethereportingoftradesbookedinHongKongaswellastrades“conductedinHongKong”(inshort,tradedinHongKong,butbookedinotherlocations).4Informationonthesetradesisimportantforunderstandingthemarketdynamics(forexampleliquidityandtheformationofprices).

Informationontradingdeskandbookinglocationofthetradesisusedtodistinguishthetwotypesoftrades.Forthepositionsoutstandingon5January2018,29%ofNDFtrades(measuredbygrossnotionaloutstanding)werebookedinHongKongand61%wereconductedinHongKong(Chart2).ThelargeshareofNDFtradesconductedinHongKongisconsistentwiththehighnumberofinternationalinstitutionsactiveinthelocalfinancialmarket.Inaddition,5%ofthegrossnotionalvalueofoutstandingpositionsintheHKTRwasreportedbyCCPs.5

CHART 2

nDF positions booked vs conducted in Hong Kong

0

20

40

60

80

100 5%

61%

29%

5%

% of gross notional

Conducted in HK Booked in HKCCP reporting Others

NDF gross notional

Source:HKTR,5January2018positions.

Note: “Others”includespositionsthatappearneitherbookednorconductedinHongKong(thuspotentiallyreportedvoluntarily).

3 Bothin2016and2017,thegrossnotionaloutstandingdroppedbyalmost20%andrecoveredthefollowingmonth.

4 TradesconductedinHongKongaretradesinwhichoneoftheindividualswhomadethedecisiontoenterintothetransactionisatraderemployedinHongKong,andwhichareconductedonbehalfof,andbookedin,anaffiliateentityofthesamegroup.Aspartofthisrequirement,entitiesreportinformationonthetradingdeskandthebookinglocationoftrades.Fordetails,seeQ20inFAQs on the Securities and Futures (OTC Derivatives Transactions – Reporting and Record Keeping Obligations) Rules,Oct.2017.

5 ThereisamismatchbetweentheshareoftradesreportedbyCCPsandthosereportedwithCCPsascounterparty,mainlybecausethereportingrequirementforCCPsappliesonlytotradeswithcounterpartiesincorporatedinHongKong.

FEATURE ARTICLE

3 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

6 Globally,LatinAmericancurrenciesrepresentanimportantclusterofnon-deliverablecurrencies,buttheyarenotheavilytradedinHongKong,likelyduetotimezonedifferences.

7 “Unidentified”entitiesarethosethatareunabletobeclassifiedintermsofsectorofactivityandcountryofincorporation.

b. Currenciesandmaturities

Unsurprisingly,Asiancurrenciesrepresentthelion’sshareofnon-deliverablecurrenciestradedinHongKong.InJanuary2018,theTaiwanesedollarwasthemostprevalentnon-deliverablecurrency,accountingfor26%oftheoutstandinggrossnotional(Chart3).Othermajornon-deliverablecurrenciesweretheKoreanwon(25%ofgrossnotional),therenminbi(23%),theIndianrupee(15%)andtheMalaysianringgit(2%).Theremaining9%ofgrossnotionalwascomprisedofaverybroadrangeofcurrencies,includinganumberofLatinAmericancurrencies,eachaccountingforlessthan2%ofthegrossnotional.6USdollarwasthesettlementcurrencyinnearlyalloftheNDFtrades(99%ofthegrossnotional).

ThematurityofNDFtradestendstoberelativelyshort.OverthreequartersoftheNDFoutstandingtrades,measuredbygrossnotionalvalue,hadaresidualmaturityofuptothreemonths(Chart3).Maturitiesbetweenthreemonthsandoneyearaccountedforanother23%.NDFtradeswitharemainingmaturityoveroneyearaccountedforlessthan2%.

CHART 3

Currency and maturity breakdown of nDF positions

0

20

40

60

80

100%

By non-deliverable currency By residual maturity

TWD 26%

KRW 25%

CNY 23%

IND 15%

MYR 2%

Others 10%

0-3M 76%

3-6M 12%

6-9M 6%9-12M 5%

12M+ 2%

Source:HKTR,5January2018positions.

Note: Percentagesdonotsumto100duetoroundingeffects.

c. Marketparticipants

InlinewiththeOTCderivativesmarketingeneral,theNDFmarketisrelativelyconcentratedaroundthetopdealers.AsshownintheHKTRdataasat5January2018,129financialentities(whichbelongto70groups)reportedNDFtradestotheHKTR.Thetopfiveinstitutionsaccountedfor48%oftheoutstandinggrossnotionalwhilethetoptenentitiesaccountedfor64%ofthegrossnotional(Chart4).

CHART 4

market participants subject to mandatory reporting

%

0

25

50

75

100

NDF gross notional

Others:36%

Top 10entities:

64%

Top 6-10entities:

16%

Top 5entities:

48%

Source:HKTR,5January2018positions.

Note:ExcludesCCPs.

Tradecounterpartiesaresignificantlymorediverse.Asshowninthesamesetofdata,2,400distinctentities,whichbelongtoaround1,600groups,wereidentified.Chart5presentsabreakdownoftradecounterpartiesbysector.In48%ofthetrades(byoutstandinggrossnotional),bankswerethecounterparty.Thenon-bankfinancialsector(whichincludesinvestmentbanks,assetmanagers,hedgefundsandinsurers)wascounterpartyto22%oftheoutstandinggrossnotional.CCPswerecounterpartyto23%oftrades(byoutstandinggrossnotional),reflectingtheirincreasinginvolvementinprovidingcentralclearingtotheNDFmarket.Thecorporatenon-financialsectoraccountedfor2%oftheoutstandinggrossnotional,whilepublicsectorinstitutions,privateindividualsandunidentifiedentitiesaccountedfortheremaining5%.7

4 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

CHART 5

sectoral breakdown of market participants on the counterparty side

4%

1%

2%

23%

22%

48%

0 10 20 30 40 50% of gross notional

Individual/Unidentified

Non-financial firms

Public sector

CCPs

Other financial entities

Banks

Source:HKTR,5January2018positions.

Geographically,tradecounterpartiesweredomiciledmainlyintheUKandtheUS,representing28%and19%oftheoutstandinggrossnotionalrespectively(Chart6).CounterpartiesdomiciledinHongKongmadeup10%ofthegrossnotional,whileFrancetookup7%oftheshare,andAustraliaandTaiwaneachconstituted5%.Alargenumberofothercountries,eachcontributingsmallshares,accountedfortheremainderoftheoutstandinggrossnotional.

CHART 6

geographical split of market participants on the counterparty side

UK28%

US19%

HK10%

FR7%

AU5%

TW5%

DE4%

CH4%

SG4%

JP3%

Others12%

% of gross notional

Source:HKTR,5January2018positions.

Note: ExcludesCCPs.“Other”includesUnidentifiedcounterparties,whichaccountfor5%.

d. Currencyrisktransferbyeconomicsectorofcounterparties

FXforwards,includingNDFs,havetheprimarypurposeoftransferringcurrencyriskbetweentwocounterpartiesbylockinginanexchangerateforacertainperiodinthefuture.Basedontheexchangerateprevailinginthemarketatthespecifiedfuturedate,onecounterpartywillgainaprofitandtheotherwillexperiencealoss.

MarketparticipantsentertheNDFmarketfordifferentreasons.SomemarketparticipantsuseNDFstooffload(“hedge”)thecurrencyriskarisingfromeitherlongorshortcurrencypositionslinkedtobusinessactivitiesandinvolvinganon-deliverablecurrency.Thecurrencyriskisacquiredbytheirtradecounterparties,whodosopossiblytospeculateonthefuturemovementoftheexchangerate,ortoarbitragebetweenratesinthespotandforwardmarkets,ortohedgeotherpositions.

ThequestionariseswhetherNDFmarketparticipantsbelongingtodifferentsectorstakesystematicpositionsinonedirectionortheother.Asa“thoughtexperiment”,weplotthenetnotionalvalueofpositionsatthesectorallevel(Chart7).Thisiscomputedbyconvertingallpositionsinacommoncurrency(USdollar)andoffsettingshortandlongpositionsacrossentitieswithinthesamesector.Theresultshowsthat,onasectoralbasis,non-financialfirmsandthepublicsectortendtotakenetpositionsaimedatoffloadingcurrencyriskfromnon-deliverablecurrencies.ThisisconsistentwiththeNDFmarketservingaprimaryeconomicfunctionofhedging.Ontheotherhand,banksandotherfinancialentitiestendtoacquirecurrencyrisk.TheyareeffectivelytheprovidersofmarketliquidityforthisOTCderivativeproduct.

FEATURE ARTICLE

5 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

CHART 7

Currency risk transfer in the nDF market by types of counterparty(Netnotionalpositionsinnon-deliverablecurrenciesbysector)

-20

-10

-15

-5

0

5

Sell non-deliverable currencyBuy deliverable currencySell deliverable currencyBuy non-deliverable currency

Non-financialfirms

Publicsector

Other financialentities

Unidentified

Banks

US$ bn

Source:HKTR,5January2018positions.

Notes:

1. ExcludesCCPsandIndividuals.2. Whilenetnotionalpositionscomputedacrossthewholemarketby

definitionoffseteachother,inthecharttheorangeandbluebarsdonothavetooffseteachotherinsize.EachsectorhasentitiesengaginginbothsidesofNDFtrades.Thesizeofthebarisfromoffsettinglongandshortpositionswithinthesamesector,whereasinrealitymanyNDFtradesarebetweenentitiesfromdifferentsectors.

3. ChangesinthestructureoftheNDFmarket

TheanalysisofHKTRdatasuggeststhatduring2016–2017,theNDFmarketstructurechangedalongthreedimensions:

• SharpincreaseofcentralclearingofNDFs;• ChangeinthecurrencycompositionofNDFs;

and• ShiftofsomeNDFactivitiesfrombankstoother

financialinstitutions.

a. SharpincreaseofcentralclearingofNDFs

During2016–2017,theNDFmarketexperiencedamarkedincreaseinNDFtradesbeingclearedthroughcentralcounterparties(Chart8).ThisisconsistentwithothermarketreportsanalysingCCPs’publicdisclosures.8TheriseincentralclearingintheNDFmarketisvoluntaryascentralclearingofNDFisnotmandatedinanymajorjurisdiction.

CHART 8

gross notional value of outstanding nDF positions being centrally cleared

0

500

1,500

1,000

2,000

US$ bn

NDF - intended to clearNDF - positions

NDF - not intended to clear

Jan2016

Jul Jan2017

Jul Jan2018

Source:HKTRpositionsforpublicdisclosure.

Note: “Intendedtoclear”isafieldreportedbythereportingentity.Tradesreportedbybothpartiesarecountedonlyonce.

AsshownintheHKTRdataasat31January2018,thegrossnotionaloutstandingintendedforcentralclearing(whichincludestradesthathadbeenclearedaswellasbilateraltradesthatwereexpectedtogothroughcentralclearing)wasUS$372billion,upfromUS$181billionayearearlierandfromUS$56billiontwoyearsearlier.

8 ChrisBarnes(2017),FX Clearing–The$750BNmarketthatkeepsgrowing,Clarus FT(www.clarusft.com/fx-clearing-the-750bn-market-that-keeps-growing).

6 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

Thepercentageofnewtradesbeingclearedcentrally,whichwaspreviouslystableataround2%to4%levels,rosesharplyto12%inthefourthquarterof2016(Chart9).Itcontinuedtoriseandreached29%inthefourthquarterof2017.TakingintoaccountalloutstandingpositionsatthebeginningofJanuary2018,24%ofthetotaloutstandinggrossnotionalwascentrallycleared.

CHART 9

percentage of cleared nDF positions

24%

3%2%

4%

12%

15%

19%

22%

29%

0

35

30

25

20

15

10

5

% gross notional cleared

Cleared new tradesCleared positions

Q12016

Q2 Q3 Q4 Q2 Q3 Q4Q12017

Source:HKTR.

Note: Theredlinereferstonewtradesoriginatedin2016–2017.Thegreybarreferstooutstandingpositionson5January2018.

ClearingisnotequallycommonacrossAsiancurrencies.Inthepositionsoutstandingon5January2018,thecurrencieswiththelargestclearedvolumesweretheTaiwanesedollar,therenminbi,theIndianrupeeandtheKoreanwon(Chart10).Amongthesecurrencies,theclearingratewas27%fortheTaiwanesedollarandtheIndianrupee,22%forthe

renminbiand15%fortheKoreanwon.ThePhilippinepeso,theIndonesianrupiahandtheMalaysianringgithadsignificantlysmallerclearedvolumesandarangeofclearingrates.ThePhilippinepesohadthehighestpercentageofclearedtradesamongallAsiancurrenciesat31%.

CHART 10

Cleared nDF positions by currency

0

20

40

60

80

100

120

0

5

10

15

20

25

30

35

27%

22%

27%

15%

31%

22%

15%

US$ bn

% cleared positions (rhs)Cleared positions, gross notional outstanding (lhs)

TWD CNY INR KRW PHP IDR MYR

% gross notional

Source:HKTR,5January2018positions.

OnedriverofthevoluntaryincreaseincentralclearingofNDFsislikelytohavebeentheimplementationofreformsonmarginrequirements,whichalteredtherelativepricesofclearedandunclearedderivatives.Box2outlineshowmarginrequirementswereimplementedinmajorjurisdictionsandhow,bymakingitmorecostlytoholdunclearedOTCderivatives,thereformhascreatedincentivesforvoluntaryclearing.

FEATURE ARTICLE

7 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

Box 2

How reforms on margin requirements affected the nDF market

Theyears2016–2017sawtheintroductionoftwonewmajorpoliciesintheOTCderivativesmarket:mandatoryclearingofcertainproductsandmarginrequirementsonunclearedderivatives.Thelatterreferstotherequirementthatcounterpartiespostcollateraltoeachotherinrelationtoderivativesthatarenotcentrallycleared.TheaimofbothpoliciesistoincreasetheclearingoftradesthroughcentralcounterpartiestoreducethelevelofbilateralcounterpartyriskintheOTCderivativesmarket.

Thetwopoliciesactthroughdifferentchannels.Mandatoryclearingrequirestheclearingofcertainproductsdeemedliquidbyregulators.Marginrequirementsoperatethroughprivateincentivesbychangingtherelativepricesofclearedandunclearedderivatives.9

During2016–2017,FXproductswerenotcoveredbymandatoryclearinginanyofthemajorjurisdictions.MarginrequirementsappliedinsteadtonewOTCderivativestradesinallassetclasses,withminorexclusionswhichdidnotaffectNDFs.

ThemajorjurisdictionsimplementedmarginrequirementsbetweenSeptember2016andSeptember2017.Theexacttimingvaried(Table1).Asaresult,HKTRdatafor2016–2017includedanincreasingnumberoftradessubjecttomarginrequirements,forwhichtherelativecostofholdinganunclearedderivativewouldhaverisen,allelsebeingequal.

TABLE 1

Timeline of implementation of margin requirements in major jurisdictions

1 Sep 2016 4 Feb 2017 1 Mar 2017 1 Sep 2017

USCanadaJapan

EU

Initial Margin (IM)

Korea

Variation Margin (VM)All the above

countries

Hong KongAustraliaSingapore

Note:Doesnotincludetransitionalarrangementsappliedincertainjurisdictions.

9 Marginrequirementshavetwocomponents:anInitialMargin,postedbyeachpartyatthestartofatradetoprovidecollateraltooffsetlossescausedbyitsownpotentialfuturedefault,andaVariationMargin,exchangeddailyasafunctionofthemark-to-marketvalueofthederivative.

8 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLEFEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

b. ChangeincurrencycompositionofNDFs

The2016BISTriennialsurveyhighlightedareshuffleinthecurrencycompositionofNDFsovertheperiod2013–2016,withariseinNDFsintheKoreanwonandtheTaiwanesedollar,andareductioninNDFsintherenminbi,whichwasmainlyattributabletotheincreasinguseofthedeliverableforwardmarket.10

Chart11plotsthecurrencycompositionofNDFsasshownintheHKTRdataatthreepointsintime.ThetrendsareconsistentwiththeearliertrendshighlightedbytheBISTriennialSurvey.InJanuary2018,theTaiwanesedollarandtheKoreanwonwerethelargestnon-deliverablecurrencies,followedbytherenminbi.Whiletherenminbiwasstillthelargestnon-deliverablecurrencyin2016asshownintheHKTRdata,itsuseintheNDFmarketdeclinedby32%during2017.Ontheotherhand,theTaiwanesedollargrewby89%,theKoreanwonby11%andtheIndianrupeeby76%betweenJanuary2016andJanuary2018.

CHART 11

Change in non-deliverable currencies

0

100

200

300

400

15 Jan 2016 6 Jan 2017 5 Jan 2018

TWD KRW CNY INR MYR Others

US$ bn

Source:HKTR,positionsat15January2016,6January2017and5January2018.

AnotherdevelopmentinthemarketistheemergenceofNDFsthatusedeliverablecurrenciesonbothsidesofthetrade.WhiletheseaccountedforonlyanegligibleshareofgrossnotionaloutstandingintheHKTRdatafornow,marketreportssuggestthattheiruseisgrowingforriskmanagementpurposesunderthenewlyimplementedpolicyofmarginrequirements.11

c. ShiftofsomeNDFactivitiesfrombankstootherfinancialinstitutions

ThethirdchangethattookplaceinthemarketstructureofNDFsover2016–2017wastherelativedeclineofNDFpositionsbybanksandtheincreaseinpositionsbyotherfinancialentities.Theseincludedinvestmentbanks,assetmanagers,hedgefundsandinsurers.Amongreportingentities,therelativeshareofbanksfellfrom85%inthefirstquarterof2016to63%inthefourthquarterof2017(Chart12).Correspondingly,theshareofotherfinancialentities(relativetobanks)increasedfrom15%to37%.

CHART 12

nDF gross notional reported by banks vs other financial entities

0

25

50

75

100

%

Q12016

Q2 Q3 Q4 Q2 Q3 Q4Q12017

2016Q1:15%

2017Q1: 28%

2017 Q4:37%

2016 Q1:85%

2017 Q1:72%

2017 Q4:63%

Banks

Other financial entities

Other financial entities Banks

Source:HKTR,5January2018positions.

Note: ThetotalistheoutstandingNDFgrossnotionalreportedatapointintimebybanksorbyotherfinancialinstitutions.Excludestradesreportedbyotherentitiesaswellasintragrouptrades.Thesharesarebasedonwhoreportedthepositions.

10McCauleyRandCShu(2016),“Non-deliverableforwards:impactofcurrencyinternationalisationandderivativesreform”,Quarterly Review, Bank for International Settlements,December(www.bis.org/publ/qtrpdf/r_qt1612h.pdf).

11ChrisBarnes(2017),G10FXNDFClearing,Clarus FT(www.clarusft.com/g10-fx-ndf-clearing).

FEATURE ARTICLE

9 Hong Kong monETARy AUTHoRITy QUARTERLy BULLETIn mARCH 2018

FEATURE ARTICLE UnDERsTAnDIng FoREIgn ExCHAngE DERIvATIvEs UsIng TRADE REposIToRy DATA: THE non-DELIvERABLE FoRWARD mARKET

Non-bankfinancialentitiescontributedsignificantlytotheincreaseinclearingintheNDFmarket.Inthefourthquarterof2017,theyclearedonaverage47%oftheirownnewtrades,ascomparedwith27%bybanks(Chart13).

CHART 13

percentage of cleared new nDF trades by banks vs other financial entities

12%14% 15%

19%

27%

5%

23%

28%

35%37%

47%

0

50

40

30

20

10

%

Other financial entitiesBanks

Q12016

Q2 Q3 Q4 Q2 Q3 Q4Q12017

Source:HKTR,newtradesoriginatedin2016–2017.

Note: Basedonwhoreportedthetrades.Thegreylinerepresentstheshareofclearedtradesreportedbybanksoutofthetotalgrossnotionalofnewtradesreportedbybanks.Theredlinedoesthesameforotherfinancialentities.

4. Conclusion

ThisarticlepresentsananalysisoftheNDFmarketusingdatafromtheHKTR.NDFisatypeofforwardcontractsforhedgingcurrencyriskorprofitingfromcurrencyvolatility,withasettlementprocessthatmakesitsuseattractive,inparticular,forAsianandLatinAmericancurrencies.

Intermsofmarketstructure,theNDFmarketismostlytradedatveryshortmaturities.ThemajorcurrenciestradedinHongKongaretheTaiwanesedollar,theKoreanwonandtherenminbi.Mostoftheoutstandingpositionsareheldbybanksandotherfinancialentities.Whilenon-financialcompaniesarelessintensiveusersofNDFs,theyareimportantholdersofnetpositionsinNDFs,typicallytooffloadthecurrencyriskfromnon-deliverablecurrencies.

Overthepasttwoyears,theNDFmarketexperiencedthreemajorchanges:amarkedincreaseincentralclearing;achangeincurrencycomposition;andincreasinginvolvementbyotherfinancialinstitutionsrelativetobanks.ThemagnitudeandspeedoftheincreaseinvoluntaryclearingofNDFsaresignificant.Reformsonmarginrequirementsareaplausibledriverofthisphenomenon.BymakingitmorecostlytoholdunclearedOTCderivatives,thereformislikelytohavecreatedincentivesforvoluntaryclearing.

Box 3

Trade repositories as a data source

ThedatausedforthisarticlearefromtheHKTR,thetraderepositoryforOTCderivativessetupinHongKongaspartoftheframeworkformandatoryreportingofOTCderivatives.

Traderepositorydataareeffectivelyaformof“bigdata”onbanksandotherentitiesoperatingintheOTCderivativesmarket.DataarecollectedcontinuouslyfromreportingentitiesontradesandpositionsinthevariousOTCderivativeproductssubjecttomandatoryreporting.Thelargevolumeofdatarequiressuitableanalyticalmethodsfordetailedexamination.

Exploitingthisnewsourceofdataallowsregulatorstoanalysethedatainaflexibleway,testhypothesesandmapconcentrationsandinterconnections.