Unit 6.3 Part 1 Budget

Categories

What is a Budget?

• A plan for spending and saving money

• Most people think

budgets are:– Rigid and inflexible

– Painful – who wants to

eat Top Ramen every

night!

– No fun!

A budget takes the fun out of money – Mason Cooley

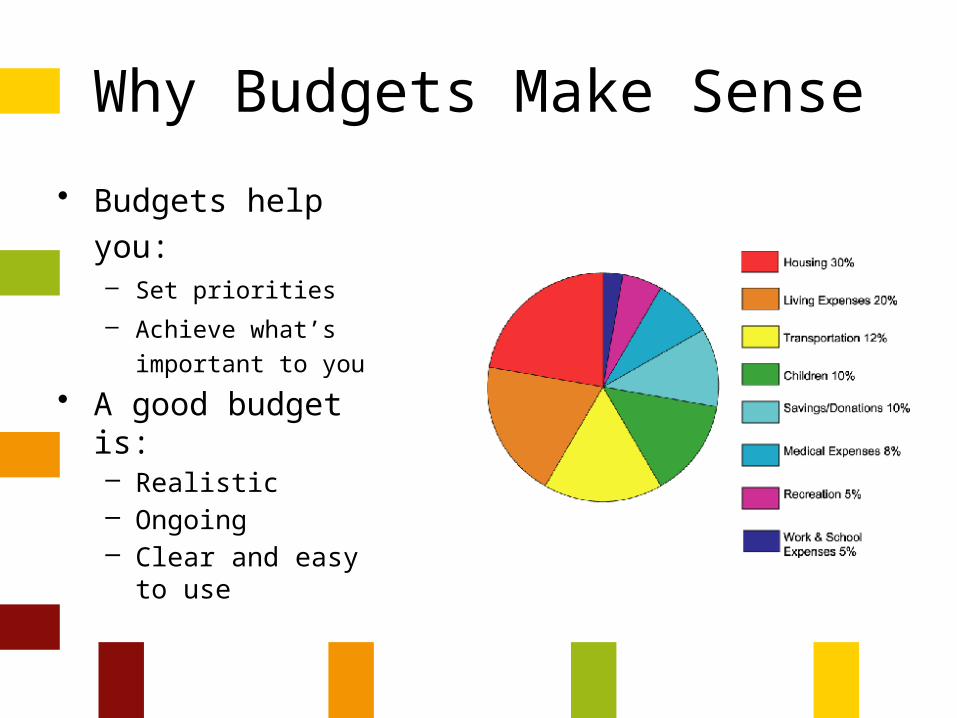

Why Budgets Make Sense

• Budgets help you:– Set priorities

– Achieve what’s

important to you

• A good budget is:– Realistic– Ongoing– Clear and easy to

use

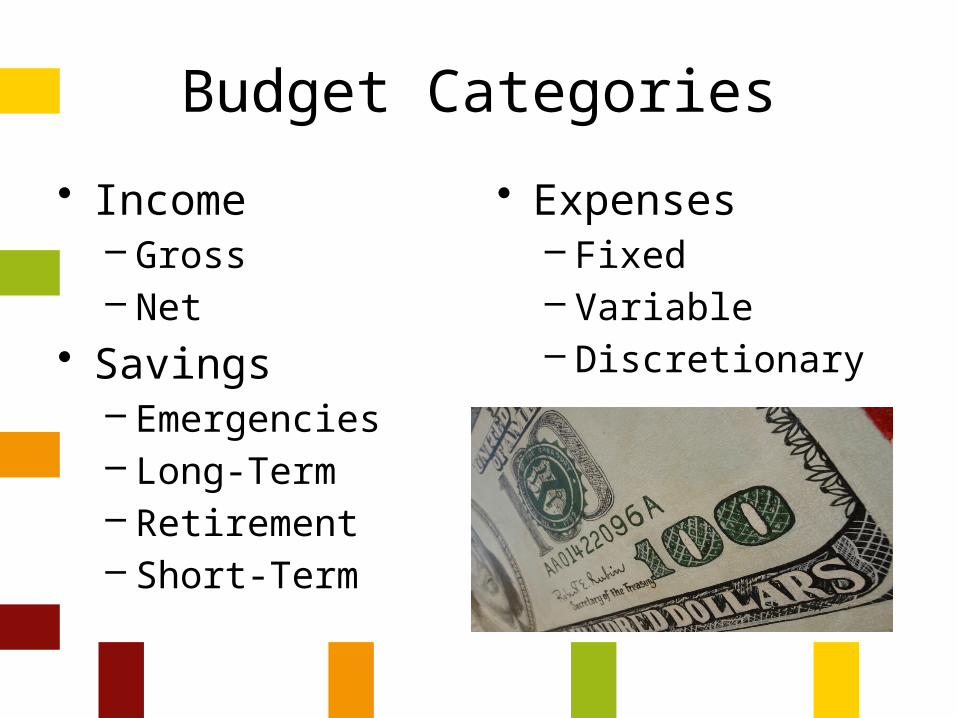

Budget Categories

• Income– Gross– Net

• Savings– Emergencies– Long-Term– Retirement– Short-Term

• Expenses– Fixed– Variable– Discretionary

Income: Money Earned

• Gross income: An individual’s income before taxes.

• Net income: Income after taxes are paid.

• Taxes can range from 15% to 31%.

It is important that you use your NET INCOME when creating your budget!

Taxes and Deductions

• First job pays $30,000/year. • Your salary is your gross income. Take off at least 25% for taxes

and other deductions. That’s what’s left for you to spend.• Example:

Gross salary = $30,000Minus 25% taxes and deductions - 7,500Net income $22,500

Total Your Monthly Earnings

• Bonus pay• Dividends and interest• Commissions• Alimony and/or child support• Public assistance• Pension or retirement income

List your salary or self-employment wages as well as any other income you receive, such as:

Savings: Pay Yourself First

• Savings: unspent income• Types

– Emergencies: Plan to set aside Three – Six months’ living expenses

– Long-term: Large ticket items (house, car, college)

– Retirement: It’s never to early to start

– Short-term: Vacation, clothes, new skis

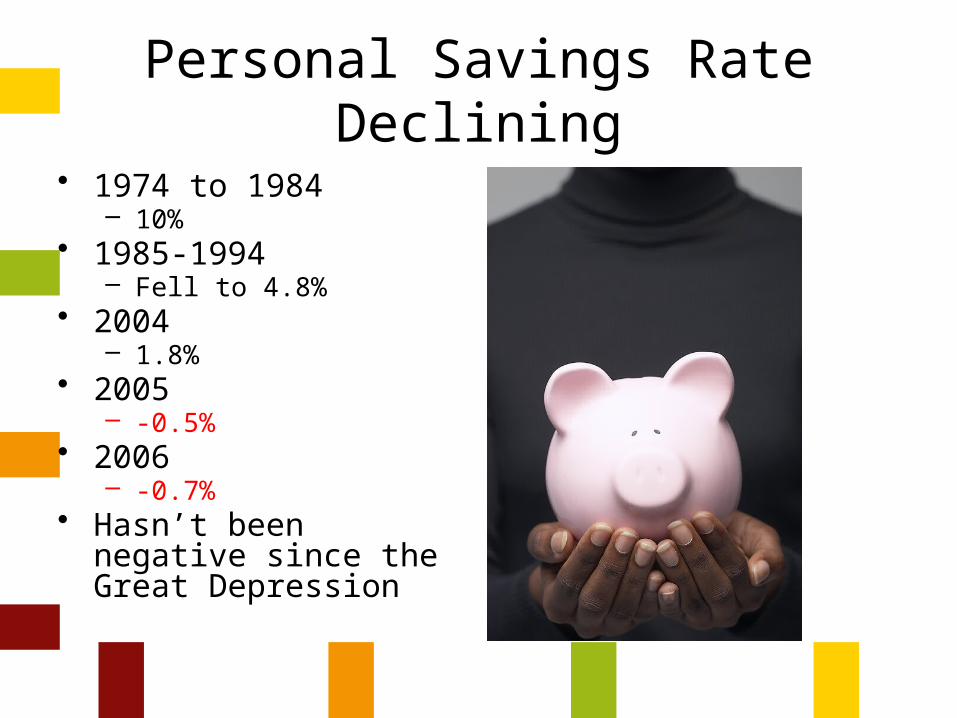

Personal Savings Rate Declining

• 1974 to 1984– 10%

• 1985-1994– Fell to 4.8%

• 2004– 1.8%

• 2005– -0.5%

• 2006– -0.7%

• Hasn’t been negative since the Great Depression

Start Saving Young!

• Save $2,000 per year from age 19 – 26– $1,035,148 by age 65

• Save $2,000 per year from age 27 – 65– $805,185 by age 65

• Time value of money– Invest fewer dollars at

a younger age but have 25% more

Expenses

• Expense: A cost to meet a need or pay a debt

• Types of expenses– Fixed– Variable– Discretionary

Fixed Expenses

A cost that occurs regularly and doesn’t vary in amount

– Rent– Mortgage– Car payment– Insurance premium– School loans– Others?

Variable Expenses

A cost that occurs regularly but may vary in amount:

– Electricity– Water and Garbage– Telephone– Gasoline– Groceries– Others?

Discretionary Expenses

A cost determined by personal wants that may be controlled

– Movies, videos, CDs– Sports– Eating out– Grooming and clothes– Concerts and plays– Vacations– Others?

Budget Summary

• Establish a budget:– Income

– Savings

– Expenses• Fixed

• Variable

• Discretionary

• End up with a budget

surplus and you’re a

success!

Preparing a Budget

Budgeting is about:

• Choosing how to use your money

• Knowing what your income and expenses are every month

Four Steps to Preparing a Budget

1. Keep track of your daily spending

2. Determine what your monthly income and expenses are the month before they are due

3. Decrease spending

4. Increase income

Step 1: Keep Track of Daily Spending

Many people spend all their money—Do you know where your money goes each month?

• Have you ever had any money and then spent it?

• Do you remember exactly what you bought?

Control Your Money!• Know where your money goes• Keep a personal spending diary

Set Your Goals

Consider them when planning a budget:

• Be realistic

• Be specific

• Have a time frame

• Say what you want to do

• Have milestones

Daily Spending Diary

Watch Spending Closely

• Use a daily spending diary or log

• Know where your money goes

• Cut expenses to save for goals

Step 2: Income

Income comes in the form of:

• Allowances• Wages from a job• Miscellaneous work (like cutting

grass)• Interest and dividends from

investments

Expenses: items you pay for each month

• Housing and car payments

• Insurance• Food and clothing• Utility bills• Personal, child or

pet care

Step 2: Expenses

• Eating out or other entertainment

• Educational costs

Expenses

Expenses: Everything you pay for in a time period

There are three types of expenses:

–Fixed –Variable–Discretionary

Fixed Expenses do not change• Car payment• Rent

Variable Expenses might change• Electricity• Food

Discretionary Expenses (can be considered variable expenses)• Clothing or entertainment

Periodic Expenses (fixed or variable) occur regularly, not frequently• Insurance• Subscriptions

Expenses (continued)

• Warranties/ Service Agreements• License renewals

Step 3: Find Ways to Decrease Spending

• Carrying little cash and controlling your credit card use

• Not shopping “for fun”

• Remembering your savings goals

• Buying only what you need

• Paying your bills on time to avoid extra fees and charges

You can decrease spending by:

Step 4: Find Ways to Increase Income

• Get a second job or a job that pays more to increase income

• Use certain tax credits that can help you increase your income (or pay fewer taxes so that you get more in your paycheck)

You can increase income by:

Budgeting ToolsThese help you manage your budget:

• Monthly payment schedule (Envelope Method)

• Monthly payment calendar

• Computer system (Mint.com)

Envelope Method• Easiest but least safe method of

budgeting method• You divide each of your

paychecks up into separate expense labeled envelopes

• When a bill is due, simply take money from envelope and apply towards the bill

Monthly Payment Calendar

Month________________________________

Sunday Monday Tuesday Wednesday

Thursday Friday Saturday

1 2$400 paycheck$25 savings$150 car$25personal$30 insurance

3$16600 transportation

4 5$25 interest (income)

6$30 cell phone

7

8 9 10 11 12 13 14

15 16$40 phone bill

17 18 19 20$10 credit card/ loan

21

22 23 24 25 26 27 28$40 entertain-

ment

29 30

Computerized Budgeting System

• Budget is set up and maintained on a computer.– Through your financial institution– Personally setting up a budget using any

computer application your comfortable with– Independent websites:

• Mint.com

Help! I Can’t Pay My Bills!

Scenario: You add up your bills and the total is $900, but your income is

only $600….

What do you do?

Think about the bills that would

be the most important!

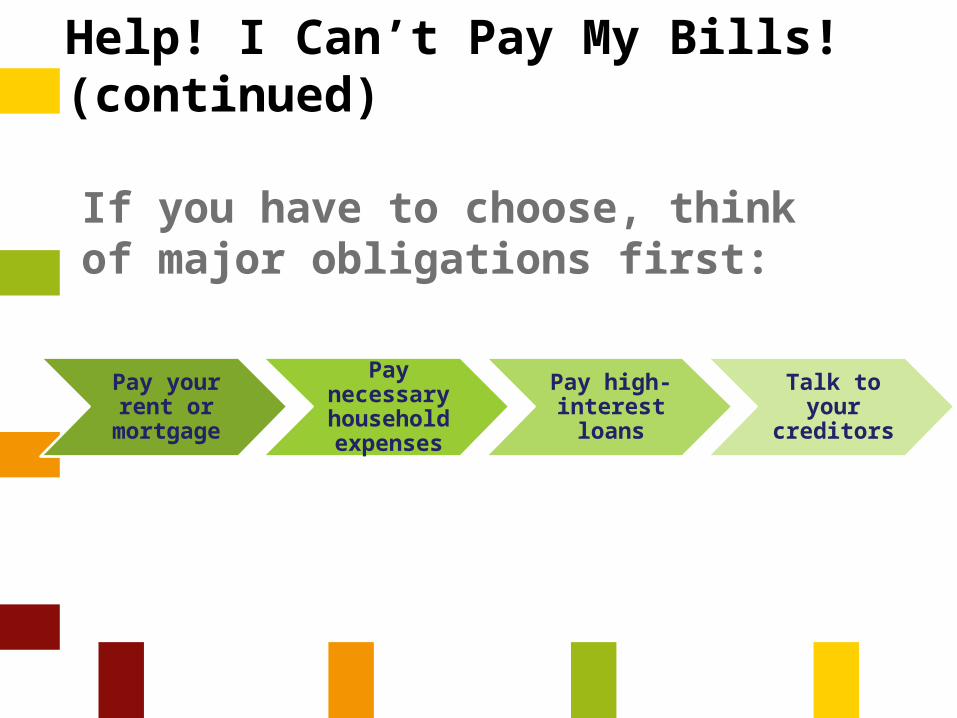

Help! I Can’t Pay My Bills! (continued)

If you have to choose, think of major obligations first:

Pay your rent or

mortgage

Pay necessary household expenses

Pay high-interest loans

Talk to your creditors