IN THIS UNIT WE WILL STUDY ABOUT

• Business finance- financial need of business

• Methods and sources of finance

• Security market

• Money market

• Study of stock exchange and SEBI

MEANING OF BUSINESS FINANCE

• Business finance refers to money and credit employed in

business.

• It involves procurement and utilization of funds so that

business firms may be able to carry out their operations

efficiently.

• It encompasses a wide range of activities and disciplines

revolving around the management of money and other

valuable assets.

CHARACTERISTICS OF BUSINESS FINANCE

• Business finance includes all type of funds used in business.

• Business finance is needed in all types of organisation- large orsmall, manufacturing or trading

• The amount of business finance differs from one business firm toanother depending upon its nature and size. It also varies from timeto time

• Business finance involves estimation of funds. It is concerned withraising funds from different sources as well as investment of fundsfor different purposes.

FINANCIAL NEED OF BUSINESS

To purchase fixed assets

To funds business growth

To meet contingencies

To meet day to day expenses

To bridge the time gap between production and sales

To avail of business opportunities

IMPORTANCE OF BUSINESS FINANCE

Need for large-

scale operation

Use of

modern

Technology

Promotion

of sales

TYPES OF BUSINESS FINANCE

Types of finance Period of Repayment Purpose

Short Term less than a yearPurchase of raw materials, payments of wages, rent, insurance etc.

Medium term One year to five yearsExpenditure on modernization, renovation, heavy advertising etc.

Long-Term more than five yearspurchase of land and building, plant and machineries etc.

FIXED CAPITAL AND WORKING CAPITAL

• Fixed capital refers to the total value of assets in a business which is of durable nature

and used in a business over a considerable period of time. It comprises of assets like

land, building, machinery, furniture etc.

• The capital invested in these assets is fixed in the sense that these are required for

permanent use in business and not for sale.

• Working capital consist of those assets which are either in the form of cash or can

easily be converted into cash, e.g., cash and bank balances, debtors, bills receivables,

stock, etc. These assets are also knows as ‘current assets’.

• Working capital is needed for day to day operations of business. However a part of

working capital is required at all times to maintain minimum level of stock and cash to

pay wages and salaries, etc. This part of working capital is called ‘permanent working

capital’.

DIFFERENCE BETWEEN FIXED CAPITAL AND WORKING CAPITAL FIXED CAPITAL WORKING CAPITAL

Fixed capital may be defined as capital invested in

long-term assets.

Working capital may be defined as capital invested

in current assets

Requirement

Fixed capital is required for establishment of

business.

Working capital is required to utilize fixed assets of

the company.

Sources of Funds

The industrial units mobilize fixed capital from

various sources like shares, debentures, banks etc.

which are to be repaid over long time period.

The industrial units mobilize working capital from the

commercial bank loans, profits retained, etc. which

are repayable before one year.

Conversion

The fixed capital which is used for fixed assets is

not easily convertible into cash.

The working capital investments have high liquidity

and can be easily convertible into cash.

Nature

Fixed capital is a one-time investment to purchase

fixed assets for starting a business or for expanding

a business.

Working capital is required constantly for day to day

business activities of the organization.

Duration

Fixed capital in long-term investment i.e it is

invested at the for long periods of time.

Working capital is usually a short term investment

for running of businesses day to day operations.

METHOD AND SOURCES OF FINANCE

METHODS AND SOURCE OF FINANCE

Internal

sources

External

Source

LONG TERM SOURCE OF FINANCE

EQUITY SHARES

• Equity shareholders are the real owners of the company as they have the voting

rights and enjoy decision making authority on important matters, related to the

company.

• The shareholders’ return is in the form of dividend, which is dependent on the

profits of the company and capital gain/loss, at the time of their sale.

• They enjoy higher returns if the company performs well and may not get any

dividend at all, if the company does not do well or when the board of directors do

not recommend any dividend for payment.

FEATURES OF EQUITY SHARES

Maturity

Claims on

Income

Cost of

Equity

Claims on

Asset

Control

Pre-Emptive

Right

ADVANTAGES OF EQUITY SHARES

Capital profit

Interest in the company’s activities

Best for investment

More income

Right to interfere in management

ADVANTAGES TO COMPANY

No-fixed burden of dividend

No outflow of cash

Bear the risk

Simple and cheap source

Increase in debt capacity

Availability of fixed capital

DISADVANTAGES OF EQUITY SHARES

Uncertainty of income

Irregular income

Capital loss

Less attractive to modest investors

Loss in the case of liquidation

DISADVANTAGES TO COMPANY

Difficult to remove over capitalization

Centralization of control

Change in management policy

Speculation

PREFERENCE SHARES

• Preference shares are those shares which carry certain special or priorityrights. Firstly, dividend at a fixed rate is payable on these shares beforeany dividend is paid on equity shares.

• Secondly, at the time of winding up of the company, capital is repaid topreference shareholders prior to the return of equity capital.

• Preference shares do not carry voting rights. However, holders ofpreference shares may claim voting rights if the dividends are not paid fortwo years or more on cumulative preference shares and three years ormore on non-cumulative preference shares.

FEATURES OF PREFERENCE SHARES

Accumulation of dividends

Call-ability

Convertibility

Redeem ability

Participation in surplus profits and assets

Voting power

ADVANTAGES OF PREFERENCE SHARES TO INVESTORS

Priority in

repayment

of capital

Best security

Regular and

fixed income

Less risk

Safety of

interest

ADVANTAGES OF PREFERENCE SHARES TO INVESTORS

No

interference in

management

Economical

financing

Availability of

wide capital

market

No change in

assets

DISADVANTAGES OF PREFERENCE SHARES TO INVESTORS

Limited voting

right

Uncertain position

of redeemable

preference shares

Dividend at fixed

rate

DISADVANTAGES OF PREFERENCE SHARES TO COMPANY

Difficult to

receive

additional

capital

High cost of

capital

Disadvantage

to equity

shareholders

Fixed economic

burden

DIFFERENCE BETWEEN PREFERENCE SHARES AND EQUITY SHARES

DEBENTURES

• A debenture is an instrument executed by the company under its common seal

acknowledging indebtedness to some person or persons to secure the sum advanced.

• It is thus a security issued by a company against the debt.

• In India, a public limited company is allowed to raise debt capital through debentures

after getting certificate of commencement of business, if permitted by its

memorandum of association

• Debenture is defined as an instrument issued by the company under its common seal

acknowledging a debt and setting forth the terms under which they are issued and

are to be paid.

FEATURES OF DEBENTURES

Fixed

interest rate

Maturity

No voting

right

Secured

assets

TYPES OF DEBENTURES

From

security

point of view

From

permanence

point of view

From records

point of view

From

convertibility

point of view

From priority

point of view

FROM SECURITY POINT OF VIEW

Simple

Debenture

Mortgage

Debenture

FROM PERMANENCE POINT OF VIEW

Redeemable

Debentures

Irredeemable

Debentures

FROM RECORD POINT OF VIEW

Bearer

Debentures

Registered

Debentures

FROM CONVERTIBILITY POINT OF VIEW

Convertible

Debentures

Non-Convertible

Debentures

FROM PRIORITY POINT OF VIEW

First

Debentures

Second

Debentures

ADVANTAGES OF DEBENTURES

Advantages of the

company

Advantages

to Investors

ADVANTAGES OF THE COMPANY

Consolidation of debt

Controlling over capitalization

Boon during depression

Capital from moderate investors

Certainty of finance

Tax benefits

Freedom in management

Trading on equity

Lower rate of interest

ADVANTAGES OF THE INVESTORS

Fixed and

stable

income

Safety

investment

Liquidity fixed

maturity

period

Conversion of

loan

DISADVANTAGES OF DEBENTURES

Disadvantages of the

company

Disadvantages

to Investors

DISADVANTAGES TO COMPANY

Fixed charge on

Assets

Fixed

burden

Risk of

winding Up

DISADVANTAGES TO INVESTORS

No Control

No extra

profits

Uncertainty

RETAINED EARNINGS

• Retained earnings is also referred as ploughing back of profits

means the reinvestments by concern of its surplus earnings in its

business.

• It is an external source of finance and is most suitable for an

established firm for its expansion, modernization and replacement

etc.

ADVANTAGES OF RETAINED EARNING TO THE COMPANY

• Cushion to absorb the shock of economy

• Economical method of financing

• Aids in smooth and undisturbed running of business

• Helps on following stable dividend policy

• Flexible financial structure

• Makes the company self dependent

• Helps in making good the deficiencies of depreciation

• Enables the redeem long term liabilities

ADVANTAGES OF RETAINED EARNING TO THE SHAREHOLDERS

• Increase in value of shareholders

• Safety of investment

• Enhanced earning capacity

• No dilution of control

• Evasion of super tax

ADVANTAGES OF RETAINED EARNING TO THE SOCIETY AND NATION

• Increase the rate of capital formation

• Stimulates industrialization

• Increase productivity

• Decreases the rate of industrial failure

• Higher standard of living

DISADVANTAGE OF RETAINED EARNING

• Over capitalization

• Creation of monopolies

• Depriving the freedom of the investors

• Misuse of retained earnings

• Manipulation in the value of shares

• Evasion of taxes

• Dissatisfaction among the shareholders

LOANS FROM FINANCIAL INSTITUTIONS

• Financial institutions such as commercial banks, life insurance corporations,

industrial finance corporations, industrial development bank of India etc., also

provide short-term, medium term, and long term loans.

• This source of finance is more suitable to meet the medium term demands of

working capital.

• Interest is charged on such loans at a fixed rate and the amount of the loan is to

be repaid by way of instalments in a number of years.

FEATURES OF LOANS FROM FI

Security

Interest payment

and principal

repayment

Restrictive

covenants

ADVANTAGES OF LOAN FROM FI

Borrowers

point of view Lender’s point of

view

BORROWERS POINT OF VIEW

• In post-tax terms, the cost of term loans is lower than the cost of equity capital or

preference capital.

• Term loans do not result in dilution of control, as lenders do not have the right to

vote

LENDER’S POINT OF VIEW

• Term loans earns a fixed rate of interest and have a definite maturity

period.

• Term loans represent secured loans

• Term loans carry several restrictive covenants to protect the interest if the

lender

DISADVANTAGES OF LOAN FROM FI

Borrowers

point of view Lender’s point of

view

BORROWERS POINT OF VIEW

• The interest and principal repayment are obligatory payments. Failur to meet

these payments may threaten the existence of the firm.

• Term loans contracts carry restrictive covenants which may reduce managerial

freedom. Further , they entitle the lenders to put their nominee on the board of

the borrowing company.

• Term loans increase the financial risk of the firm. This, in turn, tend to raise the

cost of equity capital

LENDER’S POINT OF VIEW

•Term loans do not carry the right to vote

•Term loans are not represented by

negotiable securities.

SHORT TERM SOURCES OF FINANCE

Public

depositsFactoring

Certificates

of depositsAdvances

Commercial

paper

Commercial

banksTrade credit

Installment

credit

INSTALMENT CREDIT

• Instalment credit is the method by which the assets are purchased and the

possession of goods is taken immediately but the payment is made in

instalments over a predetermined period of time.

• Generally, interest is charged on the unpaid price or it may be adjusted in

the price.

• But, in any case, it provides funds for sometime and is used as a source of

short term working capital by many business houses which have difficult

fund position.

ADVANTAGE OF INSTALMENT CREDIT

Facilitates expansion

and modernization

of business and

office

Saving of one time

investment

Convenient payment

for assets and

equipment's

Immediate

possession of assets

DISADVANTAGE OF INSTALMENT CREDIT

Cash does not

flow

Additional

burden in case

of default

Obligation to

pay interest

Committed

expenditure

ADVANCES

• Some business houses get advances from their customers and

agents against orders and this source is a short term source of

finance of them.

• It is a cheap source of finance and in order to minimize their

investment in working capital, some firms having long production

cycle, especially the firms manufacturing industrial products prefer

to take advances from their customers.

ADVANTAGES OF ADVANCES

Interest free

No

tangible

security

No

repayment

obligation

DISADVANTAGES OF ADVANCES

Limited amount

Limited period

Penalty in case of non-

delivery of goods

TRADE CREDIT

• Trade credit refers to the credit extended by the suppliers of goods in the normal course of business. As

present day commerce is build upon credit, the trade credit arrangement of a firm with its suppliers in an

important source of short term finance.

• The credit worthiness of a firm and the confidence of its suppliers are the main basis of securing trade credit.

It is mostly granted on an open account basis whereby supplier sends goods to the buyer for the payment to

be received in future as per terms of the sales invoice.

• It may also take the form of bills payable whereby the buyer signs a bill of exchanges payable on a specified

future date.

ADVANTAGES OF TRADE CREDIT

informalityflexibilityEasy

availability

DISADVANTAGES OF TRADE CREDIT

• Finance is charging of higher prices by the

suppliers

• Loss of cash discount

CERTIFICATE OF DEPOSIT

• The certificate is a document evidencing the existence of a bank deposit and it is tradable, so

that, in effect, the bank deposit can be transferred between different owners before it comes o

be repaid.

• This is one money market security which does not operate on the basis of discounts.

• Interest is paid in the normal way on the bank deposit but the price of the certificate of deposit

will vary in the market depending on how the rate of interest on the deposit, which is fixed,

compares with general interest rates.

• Certificates of deposits are issued by banks as a means of encouraging the making of short-term

deposits.

ADVANTAGES OF CERTIFICATE OF DEPOSIT

Better return

Safe return

Good and

long term

effect

DISADVANTAGES OF CERTIFICATE OF DEPOSIT

Loss

return

Long

maturity

period

Penalty

Need

patience

COMMERCIAL PAPER

• Commercial papers are those unsecured promissory notes which are

issued by well-reputed companies. Their buyers are bank, insurance

companies, unit trust, and firms

• They can be sold in two ways-directly and indirectly.

• In other words, the company can directly sell the commercial paper

to the buyer or can take the help of some agency.

ADVANTAGES OF COMMERCIAL PAPER

• The advantage of CPs lies on the simplicity they offer, as large amounts can be

raised without having aby underlying transaction

• CPs provide flexibility to the company to raise funds in the money market

wherever it is favourable

• CPs can raise fund from inter-corporate market which is not under the control of

any monetary authority

• CPs provide cheaper finance to the borrowers and at the same time offer good

rate of return to the investors.

DISADVANTAGES OF COMMERCIAL PAPER

• It is impersonal method of financing. If a firm is unable to redeem its paper due

to financial difficulties, it may not be possible for it to get the maturity of paper

extended.

• It is available always to financially sound and highest rated companies. A firm

facing temporary liquidity problems may not be able to raise funds by issuing

new paper.

• The mount of loanable funds available in the commercial paper market is limited

to the amount of excess liquidity of the various purchasers f commercial paper

• It can not redeemed until maturity. Thus if a firm no more needs the funds, it

cannot repay until maturity and will have to incur interest costs.

FACTORING

• Credit management is a specialised activity and involves a lot of

time and effort f a company collection of receivables poses a

problem, particularly for small-scale enterprises. Banks have the

policy of financing receivable.

• However, this support is available for a limited period and the seller

of goods and services has to bear the risk of default by debtors. A

company can assign its credit management and collection of

specialist organisation called factoring organization.

ADVANTAGES OF FACTORING

Advantages to

clients

Advantages

to the

customer

Advantages

to banks

ADVANTAGES TO THE CLIENT

• The client can offer competitive credit terms to his buyers which, in turn, enable

him to increase his sales and profits

• The cash realized from credit sales can be used to accelerate the production cycle.

• The client is free from the tensions of monitoring his sales ledger and can

concentrate on production, marketing, and other aspects. This results in a

reduction in overhead expenses and an increase in sales and profit.

• Factoring results in a close alteration among working capital components of the

business. Efficient management of one component can have positive impact on

other components.

ADVANTAGES TO THE CUSTOMERS

• Factoring facilitates the credit purchases o the customers as they get adequate

credit period

• Customers save on bank charges and expenses

• The customers has not to furnish any documents. He has merely to acknowledge

the notification letter,. i.e., an undertaking to make payment of the invoices to the

factor.

• Factoring does not impinge on the customer’s rights vis a vis the suppliers in

respect of quality of goods, contractual obligations, and so on

ADVANTAGES TO BANKS

• Factoring improves liquidity of the clients and

thereby, improves the quality of advances of

banks. Factoring is not a threat to banking; it is a

financial service complementary to hat of the

banks.

LIMITATIONS

costlier

Deleterious

effect on the

creditworthiness

Credit limits on

trade

Difficult to exit

the agreement

Reliance on

factor

COMMERCIAL BANKS

• Commercial banks are the main institutional sources of working capital finance in

India. After trade credit, bank credit is the most important source of financing

working capital requirements in India.

• Commercial banks are those banks which perform all kinds of banking functions

such as accepting deposits, advancing loans, credit creation, and agency function

• In India 20 major commercial banks have been nationalised, whereas in

developed countries they run like joint stock companies in the private sector.

• Some of the commercial banks in India are Andra Bank, Canara Bank, Indian bank

etc.

ADVANTAGES OF COMMERCIAL BANKS

Smooth

functioning of

foreign trade

Provides

documentary

proof

General utility

services

Attractive rate

of interest

Agency

service

Financial

assistance

DISADVANTAGES OF COMMERCIAL BANKS

Lack of

expert

Declining

trends in

profitability

Lower

efficiency

Increasing

overdues

Regional

imbalance

Insufficient

growth

PUBLIC DEPOSITS

• Public deposits are the fixed deposits accepted by a business enterprise directly

from the public.

• This source of raising short-term and medium-term finance was very popular in

the absence of banking facilities.

• Many firms, large and small, have solicited unsecured deposits from the public in

recent years, mainly to finance their working capital requirements.

ADVANTAGES OF PUBLIC DEPOSITS

Simple

and easy

No charge

on assets

Economical

Flexibility

DISADVANTAGES OF PUBLIC DEPOSITS

FINANCIAL MARKETS

FINANCIAL MARKET

• A financial market is a mechanism that allows

people to buy and sell financial securities (such as

stock and bonds), commodities and other fungible

items of value at low transaction costs and at

prices that reflect the efficient-market hypothesis

CHARACTERISTICS OF FINANCIAL MARKETS

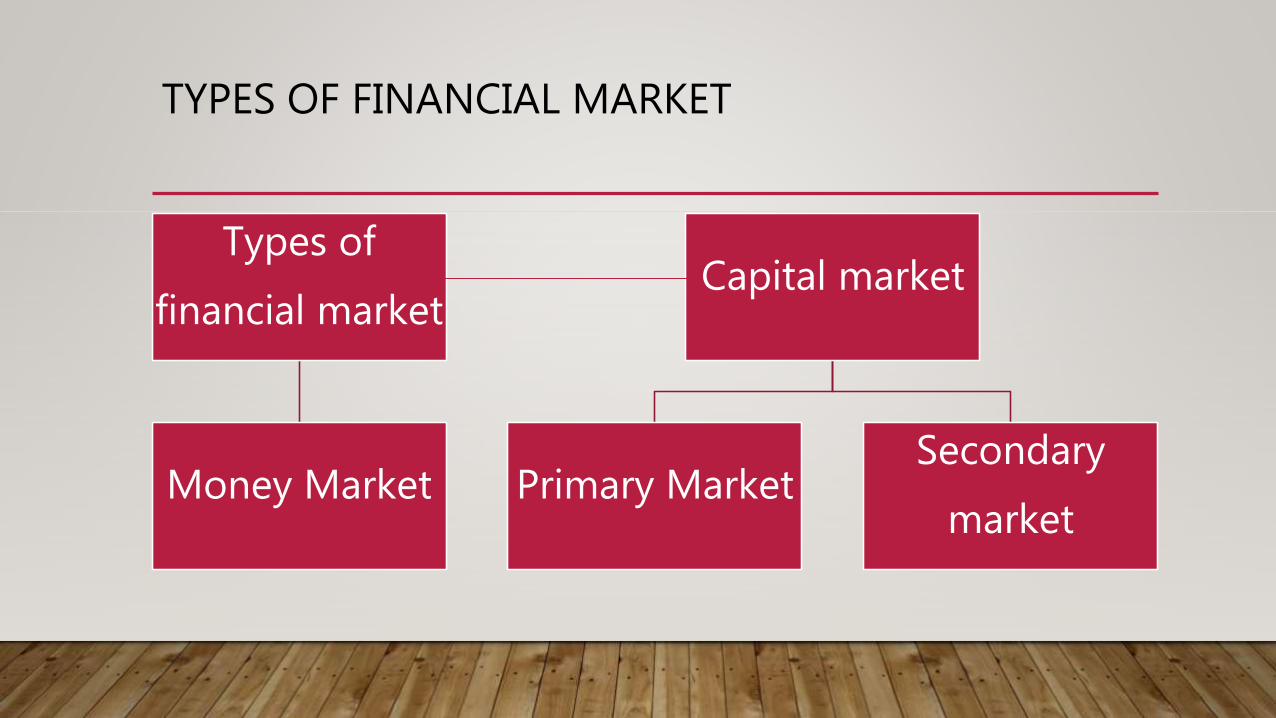

TYPES OF FINANCIAL MARKET

Types of

financial market

Money Market

Capital market

Primary MarketSecondary

market

MONEY MARKET

MONEY MARKET

• The term money market is used in a composite sense to mean financial

institutions which deal with short term funds in the economy.

• It refers to the institutional arrangements facilitating borrowings and

lending of short term funds.

• The money market brings together the lenders who have surplus short

term investible funds and the borrowers who are in need of short term

funds. In a money market, funds can be borrowed for a short period

varying from a day, a week, a month, or 3 to 6 months and against

different types of instruments, such as bill of exchange, bankers’,

acceptance, bonds, etc., called ‘near money’.

DEFINITION

• The center for dealings mainly of a short term

character, in monetary assets; it meets the short-

term requirements of borrowers and provides

liquidity or cash to the lenders

Reserve bank of India

NATURE AND CHARACTERISTICS OF MONEY MARKET

• Highly organised commercial banking system

• Apex central bank

• Adequate availability of credit instruments

• Number of dealers

• Existence of a large number of sub-markets

• Integrated interest structures

• Responsive

• Remittance facilities

• other factors

MONEY MARKET INSTRUMENTS

ADVANTAGES OF MONEY MARKET

Source of

capital

Ideal

investment

Effective

monetary

management

Economic

development

Efficient

banking

system

Facilitating

trade

Helpful to

government

DISADVANTAGES OF MONEY MARKET

• Purchasing power of investors money goes down, in case of increase in

inflation

• Irrational structure of interest rates

• Highly volatile market

• Seasonal stringency of loanable funds

• Lack of funds in the money market

• Inadequate banking facilities

CAPITAL/SECURITIES MARKET

CAPITAL/ SECURITIES MARKET

• Where a security is traded (primary or secondary trading) is called a market.

• The capital market refers to the institutional arrangements for facilitating the

borrowing and lending of long-term funds

• In the widest sense, it consists of a series of channels through which the savings of the

community are made available for industrial and commercial enterprises and public

authorities.

• It is concerned with those private savings, individual as well as corporate, that are

turned in investments through new capital issues and also new public loans floated by

government and semi government bodies.

NATURE OF CAPITAL MARKET

• The Indian capital market consists of organised and unorganised sector

• The demand for funds in the organised sector is mostly for productive investment, a large part

of the demand for funds in the unorganised market is for consumption purposes

• The demand for funds comes mostly from corporate enterprises, government and semi

government institutions.

• The supply of funds comes from households savings and institutional investors like banks,

investments trusts, insurance companies, finance corporations, government and international

financing agencies.

• The Indian capital market is characterized by the existence of multiplicity of interest rate,

exorbitant rates o interest and lack of uniformity in the business dealings.

FEATURES OF CAPITAL MARKET

Security

market

Security

prices

Participants

Location

FUNCTION OF CAPITAL MARKET

Merger

function

Transfer

function

Savings and

investment

function

Indicative

function

Liquidity

function

Allocation

function

IMPORTANCE OF CAPITAL MARKET

• Capital market serves as reliable guide to the performance and financial position of

company

• A continuous valuation of companies as reflected in the share price and the implied

possibility of in merger and takeovers

• Stock market promotes growth through the creation of liquidity

• Stock market attracts foreign investment, which leads to improved accounting,

reporting standards and exposes domestic companies to advances managerial

techniques

• Stock market at times helps companies to obtain equity finance in the absence of

loans from money market.

CONSTITUENTS OF CAPITAL/SECURITY MARKET

Primary market

Secondary market

PRIMARY MARKET

• The primary market represents the new issue market where new

securities, i.e., shares or bonds that have never been previously

issued, are offered. Both the new companies and the existing ones

can raise capital on the new issue market.

• The prime function of the new issue market is to facilitate the

transfer of funds from the willing investors to the entrepreneurs,

setting up new corporate enterprises or going in for expansion,

diversification, growth or modernization

FEATURES OF PRIMARY MARKET

• Primary market concerns new long-term capital

• Securities are sold for the first time in this market

• It is also known as new issue market

• Securities are issued directly to investors

• Security certificates are issued to investors

• Securities are issued by companies for setting new business and for expanding or modernization existing business.

• It facilitates capital formation in the economy

• Funds generated in this market are utilized for the purchase of fixed assets

• It does not include long-term loans from financial institutions

ROLE AND FUNCTION OF PRIMARY MARKET

Origination

Underwriting

Distribution

LIMITATIONS OF PRIMARY MARKET

STOCK EXCHANGES/ SECONDARY MARKET

STOCK EXCHANGE/ SECONDARY MARKET

• The secondary market, also known as ‘aftermarket’, is the financial market where

previously issued securities and financial instruments such as stock, bonds,

options and futures are bought and sold.

• The term secondary market is also used to refer to the market for any used goods

or assets or an alternative use for an existing product or asset where the customer

base is the second market.

• Stock exchanges are organised and regulated markets are various securities

issued by corporate sector and other institutions. The stock exchanges enable

free purchase and sale of securities as commodity exchange allow trading in

commodities

FEATURES OF STOCK EXCHANGE

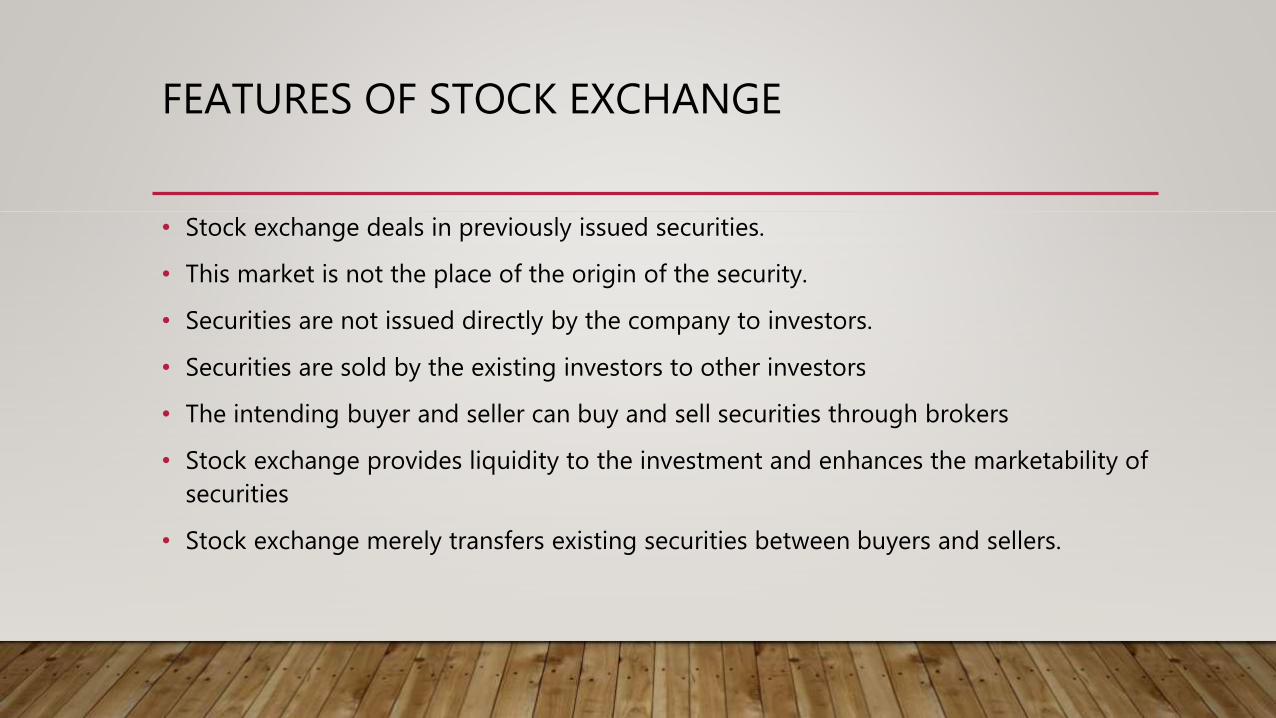

• Stock exchange deals in previously issued securities.

• This market is not the place of the origin of the security.

• Securities are not issued directly by the company to investors.

• Securities are sold by the existing investors to other investors

• The intending buyer and seller can buy and sell securities through brokers

• Stock exchange provides liquidity to the investment and enhances the marketability of

securities

• Stock exchange merely transfers existing securities between buyers and sellers.

ROLE AND FUNCTION OF STOCK/EXCHANGE

PROCEDURE FOR DEALING AT SECONDARY MARKET/STOCK EXCHANGE

Settlement Contract

note

Marketing

the

contract

Placing an

order

Selection of

broker

LIMITATIONS OF SECONDARY MARKET

STOCK EXCHANGE IN INDIA

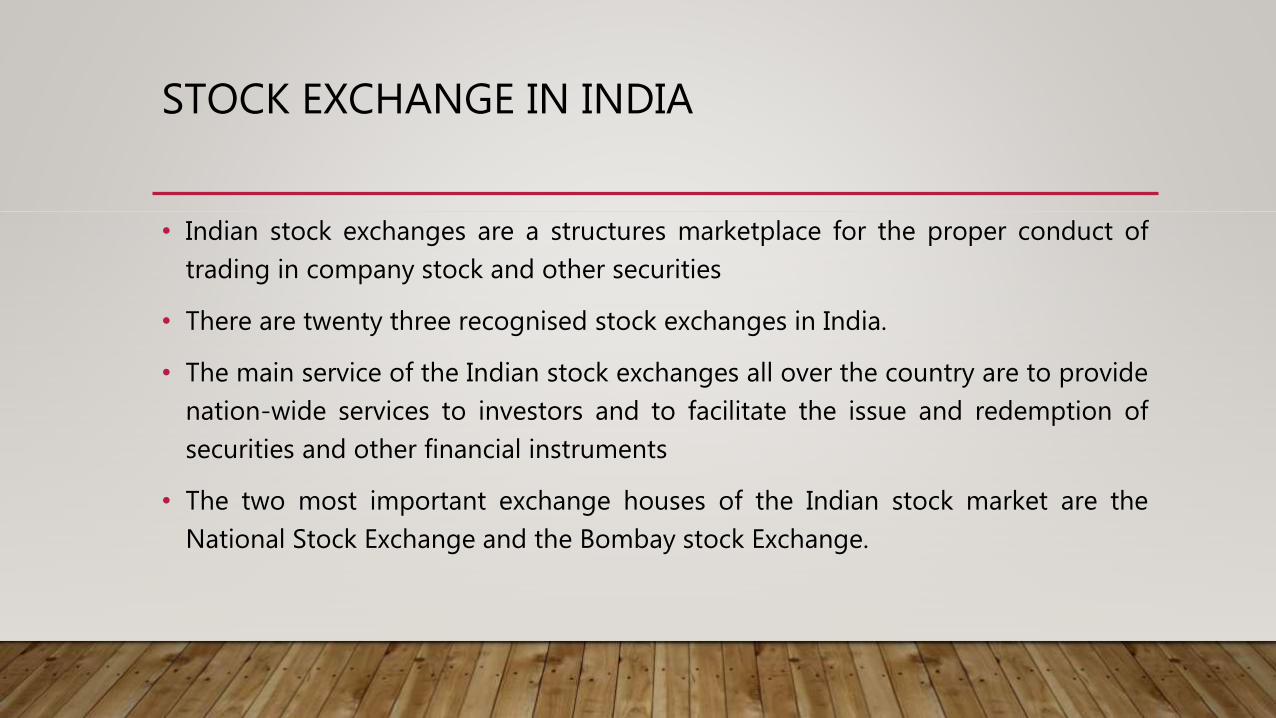

• Indian stock exchanges are a structures marketplace for the proper conduct of

trading in company stock and other securities

• There are twenty three recognised stock exchanges in India.

• The main service of the Indian stock exchanges all over the country are to provide

nation-wide services to investors and to facilitate the issue and redemption of

securities and other financial instruments

• The two most important exchange houses of the Indian stock market are the

National Stock Exchange and the Bombay stock Exchange.

BOMBAY STOCK EXCHANGE (BSE)

• Bombay stock exchange is the oldest stock exchange in Asia and what is now

popularly known as the BSE. It was established as ‘The Native Share and Stock

Brokers’ Association in 1875.

• Over the past 135 years, BSE has facilitated the growth of the Indian corporate

sector by providing it with efficient capital raising platform.

• BSE is the first exchange in India, and the second in the world to obtain an ISO

9001:2000 certifications. It is also the first exchange in the country and second in

the world to receive information security management system.

FEATURES OF BSE

• It is the oldest and largest stock exchange in Asia

• It is fifth largest stock market in the world

• Approximately 6,000 Indian companies are listed with Bombay Stock Exchange.

• It is the first stock exchange that introduced equity derivates in India.

• Free Float Index, US$ version of BSE Sensex and internet trading platform wre

launched initially by Bombay Stock exchange in India

• It is the first amongst all stock exchange in the country to collect ISO certification

from Surveillance, clearing and settlement

NATIONAL STOCK EXCHANGE (NSE)

• The national stock exchange (NSE) is India’s largest securities exchange in terms

of daily trade numbers.

• It offers automated electronic trading of a variety of securities, including equity,

corporate debt, Central and state government securities, commercial paper,

certificate of deposits and exchange traded funds.

• The exchange has more than 1,000 listed members. Owned by more than twenty

different financial and insurance institutions. NSE specialize in three market

segments-wholesale debt, spatial market and future options

SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI)

• In 1988, the securities and exchange board of India

(SEBI) was established by the Government of India

through an executive resolution, and was

subsequently upgraded as a fully autonomous

body in the year 1992 with the passing of SEBI Act

on 30 January 1992.

OBJECTIVES OF SEBI ACT

• To protect the interests of investors in securities

• To promote the development of the securities

market

• To regulate the securities market

• For matters connected there with or incidental

thereto.

FUNCTIONS OF SEBI

• To register and regulate the working of stockbrokers

• To register and regulate the working of bankers to an issue

• To control and regulates securities market

• To exercise the powers under SEBI Act.

• To regulate the working of mutual funds

• To perform such other functions as may be prescribed

• To control fraudulent and unfair trade practices relating to securities market.