University of Montana - September 15, 2006

Repurchases, Employee Stock Option Grants, and

Hedging

Daniel A. Rogers

Portland State University

Elevator pitch

What’s the rationale for observed relation between employee options and stock repurchases? Partial explanation: repurchases serve as hedge against uncertainty

surrounding option obligations. Provides more “economic” justification than EPS management

hypothesis. Findings:

Employee stock option grants exhibit positive relation with repurchases.

For firms in which this relation is strongest, I find evidence consistent with an optimal hedging motive (although there might be more to the story.

Background on options and repurchases

Microsoft: “We repurchase our common shares primarily to manage the dilutive effects of our stock option and stock purchase plans, and other issuances of common shares.” - 2003 10-K Footnote 14 to financial statements.

Existing empirical evidence Substitution of repurchases vs. dividends (exec story): Fenn

and Liang (2001 JFE) and Kahle (2002 JFE). Option funding: Kahle (2002 JFE). Earnings management (anti-dilution): Bens et al. (2003 JAE)

and Weisbenner (2000 wp).

Another Story?

Granting options to employees creates uncertain future liability for shareholders. Current shareholders incur an opportunity cost when employee

stock options are exercised. Amount of the opportunity cost = (stock price at exercise date –

exercise price). Do shareholders hedge this uncertainty? Hedging strategy: repurchase shares when options are

granted. Similar to a forward purchase of currency or commodity. Strategy implies positive relation between repurchases and option

grants over time.

Example

Assume: Stock price = $20; Option granted at the money;

Cost of equity = 8%; and Dividend yield = 3% What is the ultimate cost borne by existing

shareholders? Exercise price at time of exercise – grant date price Suppose exercise occurs in 5 years: FV of $20

invested in 5 years = $25.68 ($20 * 1.055) Ex post economic cost = $5.68 if repurchase (known

at time of grant and repurchase) Ex post economic cost = ??? if no repurchase

How does situation differ from other hedging

problems? Typical hedging situation: “bad” outcomes = low

cash flows or earnings. In this case: “bad” outcome is high stock price at

time of exercise. “Normal” opportunity cost: stock price increases by

dividend-adjusted cost of equity. If stock price change between grant and exercise dates

exceeds dividend-adjusted cost of equity, repurchasing stock at grant date provides a positive payoff against excess opportunity cost.

Why might a high stock price be bad?

Jensen (2005) arguments Management “games” market expectations stock

price > intrinsic value Wealth-destroying acquisitions (Moeller et al., 2005 JF)

Employees choose when to exercise: If employees exercise options when price is above intrinsic value rent extraction.

If company repurchases stock at high prices, its alternatives to fund growth opportunities are 1) less investment, 2) tap external capital markets

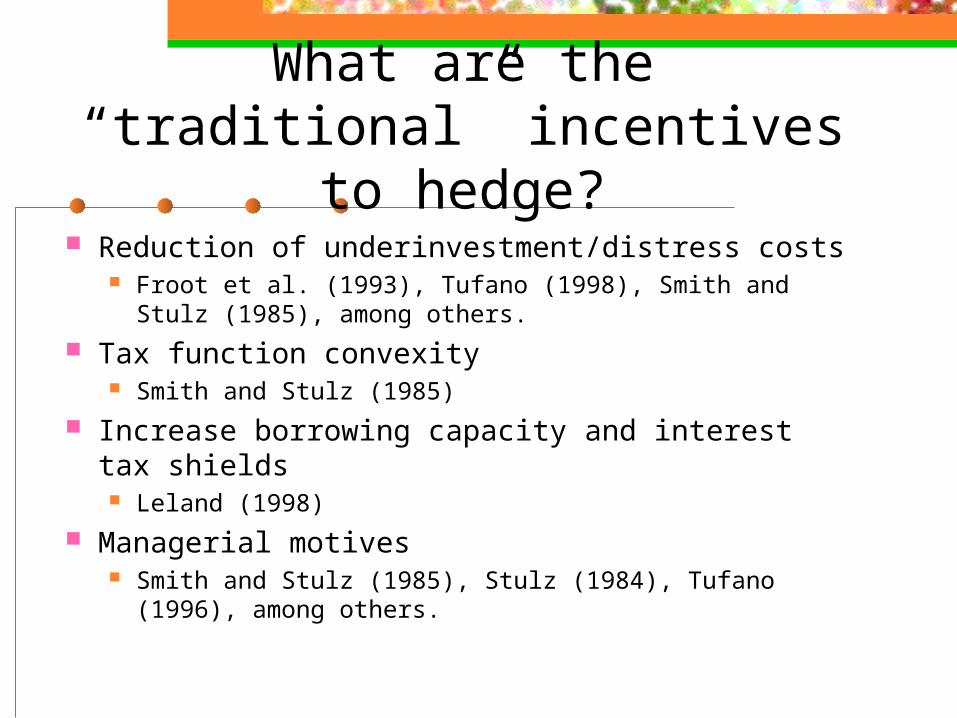

What are the “traditional” incentives to hedge?

Reduction of underinvestment/distress costs Froot et al. (1993), Tufano (1998), Smith and Stulz (1985), among

others.

Tax function convexity Smith and Stulz (1985)

Increase borrowing capacity and interest tax shields Leland (1998)

Managerial motives Smith and Stulz (1985), Stulz (1984), Tufano (1996), among

others.

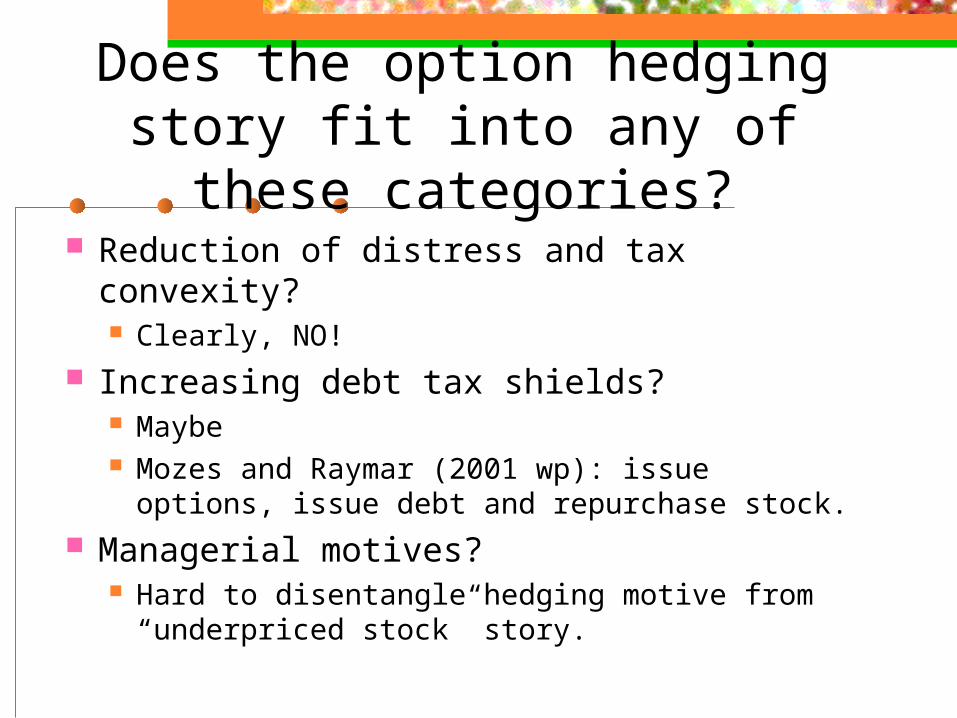

Does the option hedging story fit into any of these

categories? Reduction of distress and tax convexity?

Clearly, NO!

Increasing debt tax shields? Maybe Mozes and Raymar (2001 wp): issue options, issue debt

and repurchase stock.

Managerial motives? Hard to disentangle hedging motive from “underpriced

stock” story.

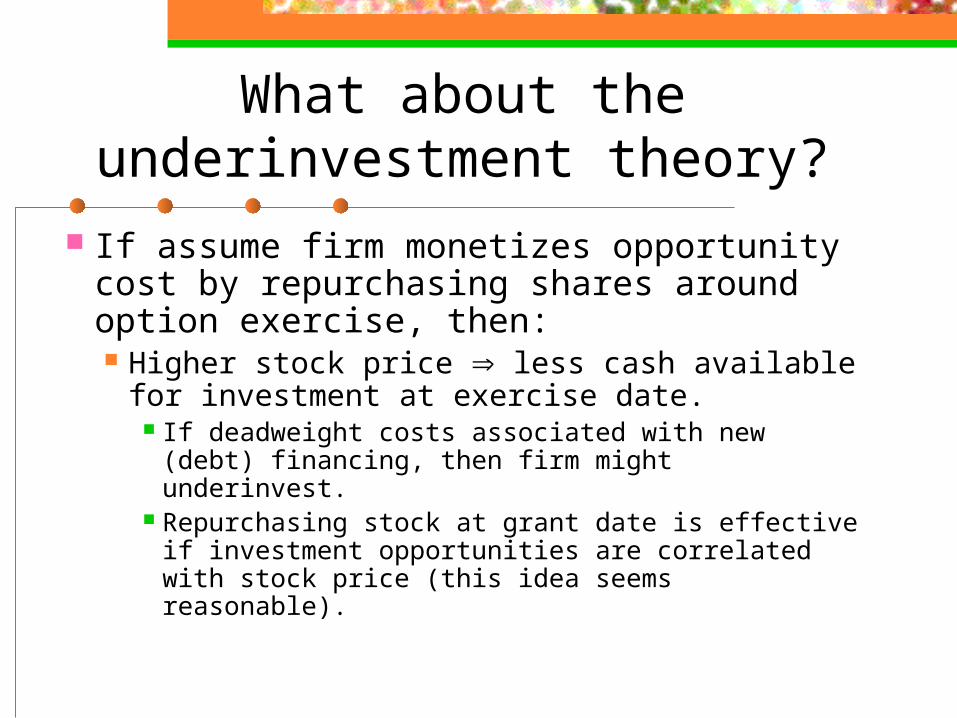

What about the underinvestment theory?

If assume firm monetizes opportunity cost by repurchasing shares around option exercise, then: Higher stock price less cash available for

investment at exercise date. If deadweight costs associated with new (debt)

financing, then firm might underinvest. Repurchasing stock at grant date is effective if

investment opportunities are correlated with stock price (this idea seems reasonable).

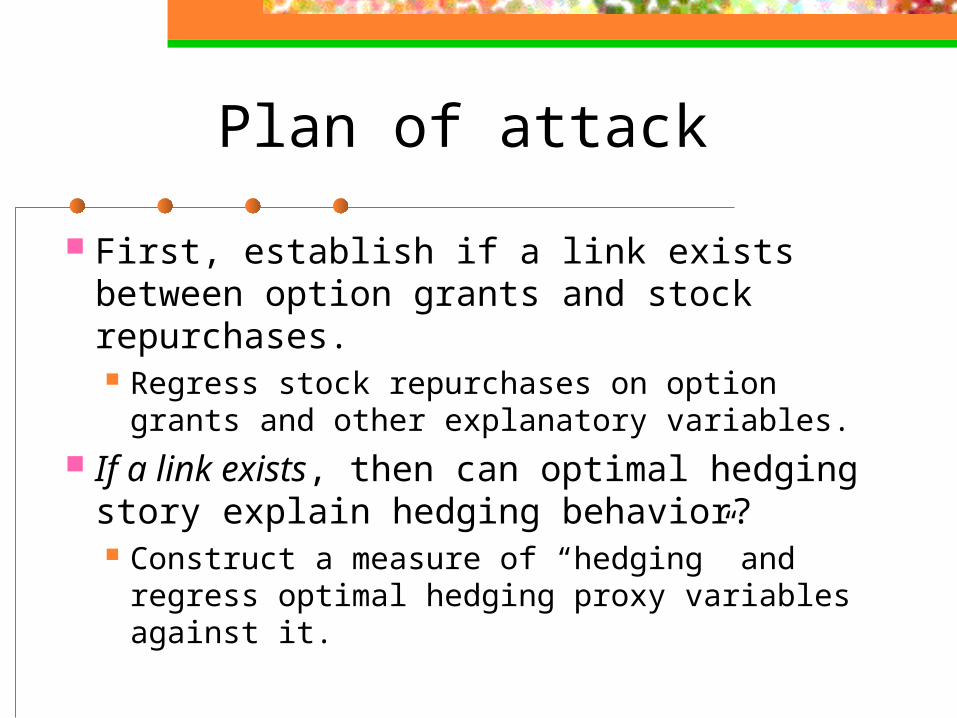

Plan of attack

First, establish if a link exists between option grants and stock repurchases. Regress stock repurchases on option grants and

other explanatory variables. If a link exists, then can optimal hedging

story explain hedging behavior? Construct a measure of “hedging” and regress

optimal hedging proxy variables against it.

Sample

151 randomly selected S&P 500 firms. Manual data collection of employee

option data. Time frame: 1993 – 2003 (or

maximum 10-K filings available from EDGAR).

Research design - Option grants & repurchases

Dependent variable = number of shares repurchased Independent variables:

log of market capitalization free cash flow market-to-book of assets capital expenditures long-term debt dividend yield stock price change stock price volatility option grants this is the variable of interest! exercised options

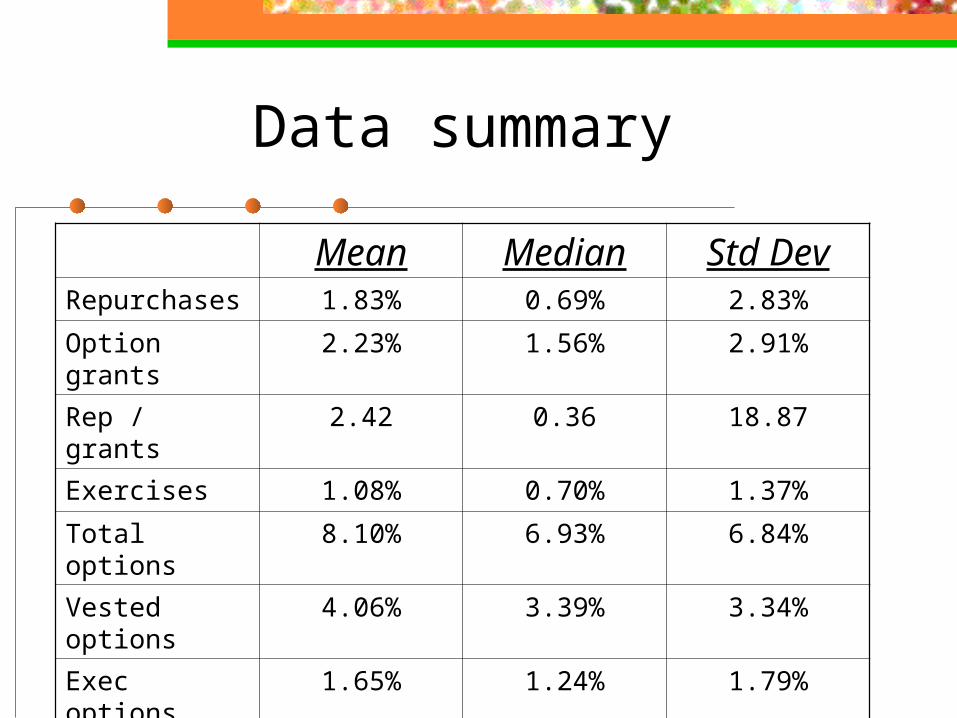

Data summary

Mean Median Std DevRepurchases 1.83% 0.69% 2.83%

Option grants 2.23% 1.56% 2.91%

Rep / grants 2.42 0.36 18.87

Exercises 1.08% 0.70% 1.37%

Total options 8.10% 6.93% 6.84%

Vested options 4.06% 3.39% 3.34%

Exec options 1.65% 1.24% 1.79%

Vested exec options 0.90% 0.60% 1.08%

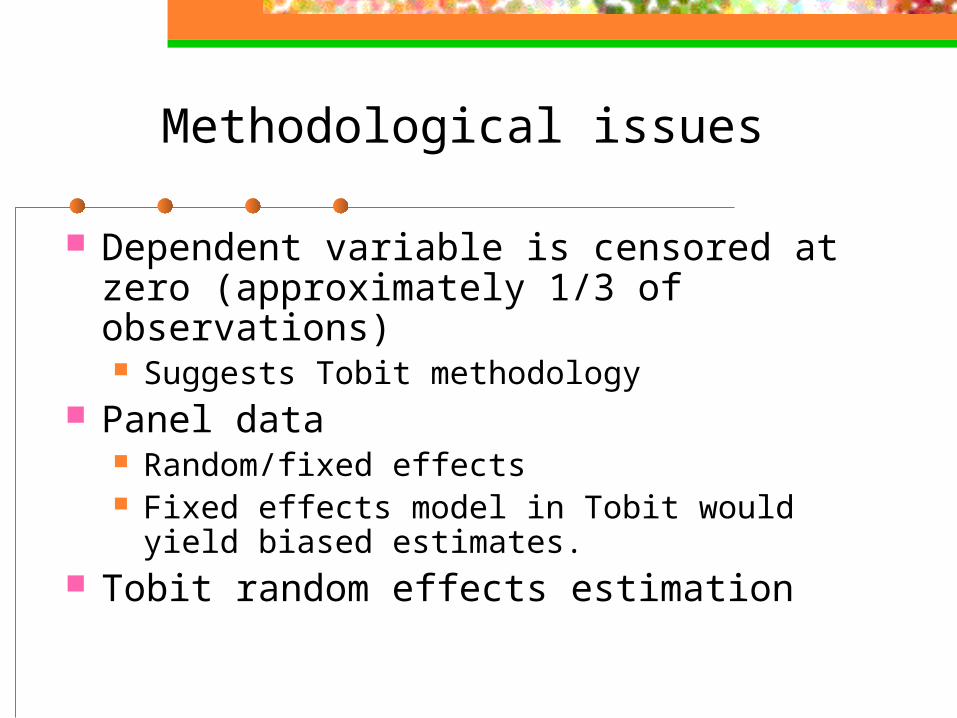

Methodological issues

Dependent variable is censored at zero (approximately 1/3 of observations) Suggests Tobit methodology

Panel data Random/fixed effects Fixed effects model in Tobit would yield biased

estimates. Tobit random effects estimation

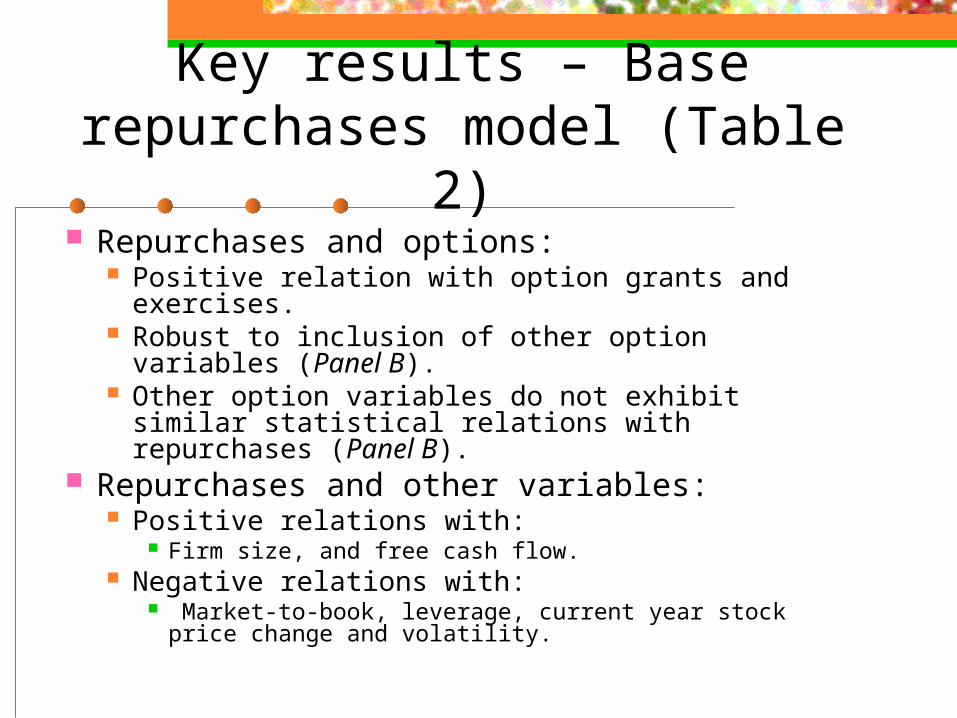

Key results – Base repurchases model (Table 2)

Repurchases and options: Positive relation with option grants and exercises. Robust to inclusion of other option variables (Panel B). Other option variables do not exhibit similar statistical

relations with repurchases (Panel B). Repurchases and other variables:

Positive relations with: Firm size, and free cash flow.

Negative relations with: Market-to-book, leverage, current year stock price change and

volatility.

Robustness results – Table 3

“Excess” grants are positively related to repurchases (two-stage model).

Controlling for lagged option grants back 4 years. Concurrent grants remain positively related to repurchases. Evidence of stronger relations for 1 and 2-year lagged grants.

Controlling for Bens et al. (2003) earnings management variables. Option grants remain positively related to repurchases.

How Is Hedging Defined?

Cannot directly observe “hedging” from disclosures.

Derived measure: Coefficient of variation for repurchases-to-

grants ratio = inverse hedging measure. Effectively captures a population driving

positive relation between grants and repurchases in multivariate.

Coefficient of variation and mean: Repurchases-to-grants

ratioFull sample = 140 firms (at least 1 yr of

repurchases)

Coefficient of variation Mean

Average 1.58 2.64

Median 1.40 1.13

Standard deviation 0.73 6.17

25th percentile 1.02 0.50

75th percentile 2.05 2.38

Minimum 0.24 0.01

Maximum 3.32 57.67

What variables explain option grant hedging?

Table 5 – differences between models Model 1: no industry controls Model 2: industry controls, but no control for variation of repurchases-to-

exercises Model 3: includes variation of repurchases-to-exercises, but no industry

controls Model 4: Controls for variation of repurchases-to-exercises and industry

effects Model 4 results - Effect on “hedging”:

Leverage: Negative relation R&D expenditures: Positive relation Vested exec options: Positive relation Firm size: Negative relation Market-to-book: Negative relation Exec shares held: Positive relation

What about the “non-hedgers?”

Table 6 results Difference between non-repurchasing

firms vs. those that repurchase (logit) Lower free cash flow Greater leverage More R&D

“Continuous” measure of option grant hedging Very similar results relative to Table 5

Summary of Most Notable Results

Option grants are positively related to repurchase activity. Even if not intentional, this pattern provides a hedge for

shareholders against uncertain opportunity cost of options.

Firms that exhibit less variation in repurchase activity relative to option grants also exhibit greater R&D spending and less leverage. This set of results fits underinvestment costs rationale

for hedging.