STRONGER

Strategies for success

2015 Partner Conference

together

BPAS Partner Conference

June 15 – 17, 2015

Barry S. Kublin, Chief Executive Officer

Benefit Plans Administrative Services, Inc.

2015 Partner ConferenceStronger Together 2

WELCOME and THANK YOU

• Attendees• Sponsors• Guest Speakers• BPAS Staff

— Marketing the Program— Developing Program Content— Logistics

• Web Success Agency• BTI Travel

2015 Partner ConferenceStronger Together 3

AGENDA• BPAS Firm Profile• Issues Affecting Retirement Plan Service Providers

— Coverage and Participant Rates— State Initiatives— Fiduciary Regulations

• Service Provider Trends in the Industry• Business Opportunities by Segment

2015 Partner ConferenceStronger Together 4

AGENDA

• Evolution of “401k” Accumulation Plans into “401k” Lifetime Retirement Plans

— “Managing Through Retirement vs. Managing to Retirement for

Plan Participants”

2015 Partner ConferenceStronger Together 5

Firm Profile

• 250 Professional Employees• 9 Office locations

— Rochester, Syracuse, Utica, and NYC, NY— Philadelphia and Pittsburgh, PA— East Hanover, NJ— Houston, TX— San Juan, PR

2015 Partner ConferenceStronger Together 6

Firm Profile

• $18.6 billion assets under custody• 3,600 engagements• 375,000 plan participantsPlus acquisition of the Oneida Financial Group practice, pending regulatory approval

2015 Partner ConferenceStronger Together 7

BPAS Lines of Business

• Plan Administration and Recordkeeping Services— Bundled administration, recordkeeping and custody services for

defined contribution-type plans and IRAs• TPA Services

— Unbundled retirement plan services in support of balance forward and third-party recordkeeping plans

• Actuarial and Pension Services— Actuarial services for traditional defined benefit, cash balance,

executive supplemental retirement and other post-retirement benefit plans

2015 Partner ConferenceStronger Together 8

BPAS Lines of Business• Benefit Consulting Services

— Health and welfare benefit plan consulting

• VEBA/HRA Services— Bundled administration for retiree medical plans

• Fiduciary Services— ERISA 3(21) and 3(38) services for retirement and VEBA plans, in

support of brokers and directed trustees

2015 Partner ConferenceStronger Together 9

BPAS Lines of Business

• AutoRollover and MyPlanLoan Services— Service bureaus for other providers supporting EGTRAA

distributions and non-payroll-deduct loan administration

• BPAS Trust Company of Puerto Rico— Directed trustee services for PR 1081 plans

• Hand Benefits & Trust, a BPAS Company— Collective Investment Fund administration

2015 Partner ConferenceStronger Together 10

BPAS Sales Map

2015 Partner ConferenceStronger Together 11

BPAS DC Differentiators• Auto Escalation Plans• Employer Stock / PR 1081 Plans• Multiple Employer Plans / Multiple Employer Trusts• VEBA / HRA• TRO / HR Outsourcing Solutions

— 3(16)— 180° / 360°payroll integration

• Commitment to Financial Advisor Service Model— Level comp by fund service model

2015 Partner ConferenceStronger Together 12

BPAS DB and EBT Differentiators

• Actuarial and Pension Services— 27 actuaries supporting plans with 1 – 20,000 participants— Expert knowledge of PR 1081/PBGC and PR Cash Balance plans— Bundled provider of GASB 45, VEBA/HRA services

• EBT Services— NSCC Member Firm, vertical integration of daily valuation

administration and custodial processes— Administering CIFs since 1964 (51 years), 287 tickers— BPAS Trust Company of PR

2015 Partner ConferenceStronger Together 13

Issues Affecting Retirement Plan Service Providers

• Retirement Savings Crisis— Not having enough money for retirement is the number one

concern for Americans in every age bracket

— Over 20 million private sector workers earning between $30 - $100k do not have access to a retirement plan at work

2015 Partner ConferenceStronger Together 14

Issues Affecting Retirement Plan Service Providers

• Federal Response— Senator Tom Harkin USA Retirement Funds

• Auto-enrollment into a series of collective funds• Benefits payable as lifetime annuity• No distributions until retirement• According to GAO, IRS takes in $5 billion annually in early withdrawal

penalties— Senator Marco Rubio TSP Proposal

• “That is why I propose we give Americans who do not have access to an employer sponsored plan the option of enrolling in the federal Thrift Plan.”

2015 Partner ConferenceStronger Together 15

STATE INITIATIVESEnacted in California, Connecticut, Illinois, Massachusetts,

Utah, Virginia, Washington

Issues Affecting Retirement Plan Service Providers

2015 Partner ConferenceStronger Together 16

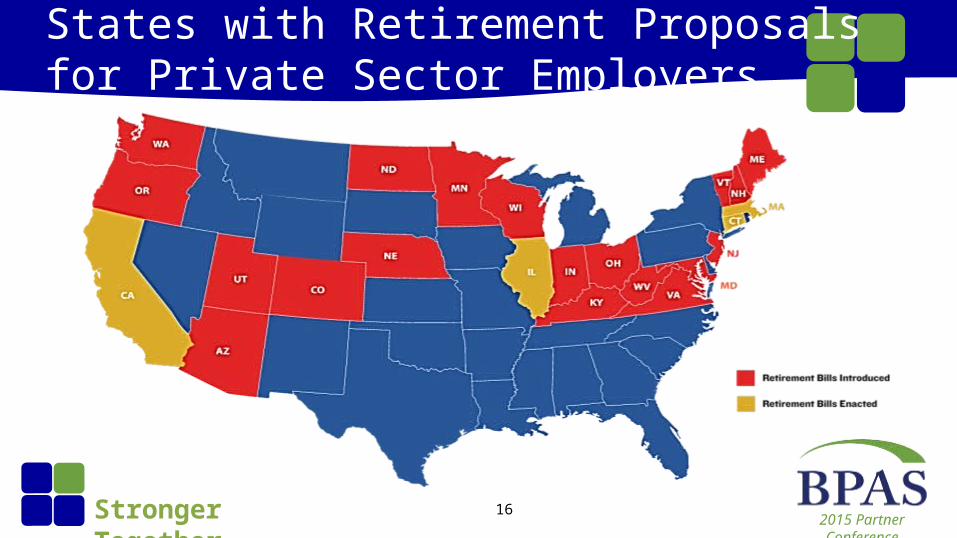

States with Retirement Proposals for Private Sector Employers

2015 Partner ConferenceStronger Together 17

Elements of State Run Plans• No required employer contribution, no employer

administrative fees• Exempt from ERISA• Illinois Secure Choice Savings Program

— 25+ employees, $250 fine per employer per year for non-compliance— Auto-enroll at 3%, non-ERISA plan— Roth IRA contribution limit ($5,500/$6,500)— Participant directed— Expense ratio not to exceed 75 bps— State Board to create vendor website to assist employers

in identifying provider

2015 Partner ConferenceStronger Together 18

Competing Against the States• Private Sector Service Providers

— Commit to participation rates, not just AUM— Expand coverage to part-time employees, notwithstanding

statutory exclusions for employer contributions• Expanded use of Multiple Employer Plans and Trusts for

small businesses• Competitive HR outsourcing model – 180 / 360 integration• Expanded use of auto features, including escalation• Deliver value-added education

— Financial literacy vs. savings rates and asset allocation

2015 Partner ConferenceStronger Together 19

Fiduciary Regulations• Impacts any investment professional or organization

that works with plan sponsors, participants or IRA account owners• Covers advice about buying, selling or holding

investments in plans or IRAs— Recommendations to take a distribution from a plan or IRA— Recommendations of persons to serve as investment

manager or to provide investment advice to plan or IRA owners

2015 Partner ConferenceStronger Together 20

Fiduciary Regulations

• How to Avoid Prohibited Transactions— The Best Interest Contract Exemption

• Written contract committing to Best Interest Standard• Disclose any material conflicts of interest

— Level comp, Limitations on investment offerings

2015 Partner ConferenceStronger Together 21

Fiduciary Regulations• Accelerated migration of plans from

generalists to specialists• Open architecture• Level compensation• Directed Trustee vs Discretionary Trustee

Model• IRA Rollovers vs Plan to Plan transfers

2015 Partner ConferenceStronger Together 22

Fiduciary Regulations

• 401k Accumulation Plans vs 401k for Life Plans• 401k Accumulation Plans vs 401k for Life Plans• Increase in non-revenue sharing investment

products• Education models vs CIFs

2015 Partner ConferenceStronger Together 23

Service Provider Trends

• There has been a bifurcation of advisors into generalists and specialists with very different product preferences and support needs• Rapid growth of fee-based advisors and a

commensurate decline of the commission compensation model• Rapidly growing presence of the fiduciary advisor

2015 Partner ConferenceStronger Together 24

Service Provider Trends

• Insurance-based advisors, typically commission-based and non-fiduciary, have declined from 25% of all advisors in 2011 to 12% in 2015 (RRI, 2015)

• Channel Affiliation— Growing: Ind BD, RIA, Bank Trust— Declining: Insurance, Wirehouse

2015 Partner ConferenceStronger Together 25

Business Opportunities

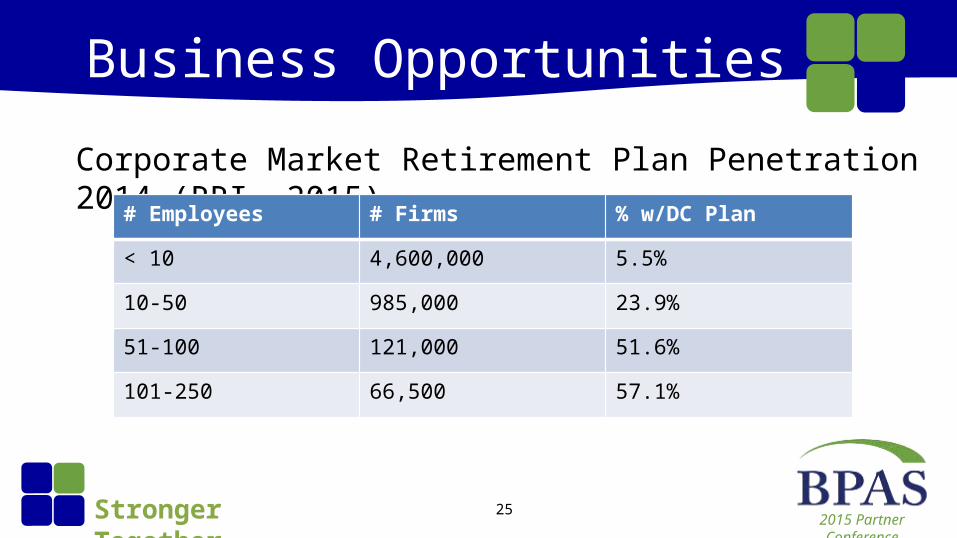

Corporate Market Retirement Plan Penetration 2014 (RRI, 2015)# Employees # Firms % w/DC Plan

< 10 4,600,000 5.5%

10-50 985,000 23.9%

51-100 121,000 51.6%

101-250 66,500 57.1%

2015 Partner ConferenceStronger Together 26

Business Opportunities

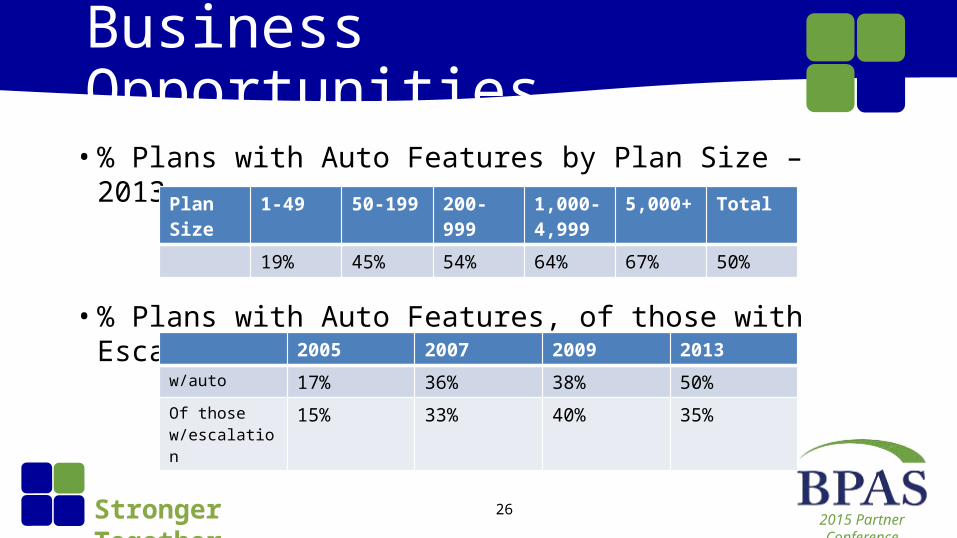

• % Plans with Auto Features by Plan Size – 2013

• % Plans with Auto Features, of those with Escalation

Plan Size 1-49 50-199 200-999 1,000-4,999

5,000+ Total

19% 45% 54% 64% 67% 50%

2005 2007 2009 2013w/auto 17% 36% 38% 50%Of those w/escalation

15% 33% 40% 35%

2015 Partner ConferenceStronger Together 27

Business Opportunities

Reasons Cited for Not Using Auto Features – 2013Reason 1-49 50-199 200-999 1,000-

4,9995,000+ Total

Satisfied w/participation rate

73.1% 56.1% 22.0% 19.0% 13.8% 43.7%

Philosophy 19.2% 43.9% 36.6% 40.5% 34.5% 32.5%

Cost 3.8% 2.4% 17.1% 35.7% 41.4% 16.5%Added work 10.3% 19.5% 14.6% 11.9% 3.4% 12.1%

2015 Partner ConferenceStronger Together 28

Business OpportunitiesProjected Corporate DC Sales in 2015

Book Turnover Sales

Plans (000) Plans Assets (B)

< $1 m 352.0 6.5% 22,900 $9.8

$1-5 m 205.0 8.0% 16,400 $40.4

$5-10 m 31.2 8.5% 2,700 $20.8

$10-25 m 18.1 8.5% 1,550 $26.3

$25-50 m 6.2 7.0% 435 $17.2

$50-250m 5.6 6.5% 365 $44.8

$250-1b 1.4 6.0% 85 $46.5

>$1b .5 5.5% 30 $116.0

2015 Partner ConferenceStronger Together 29

Business Opportunities

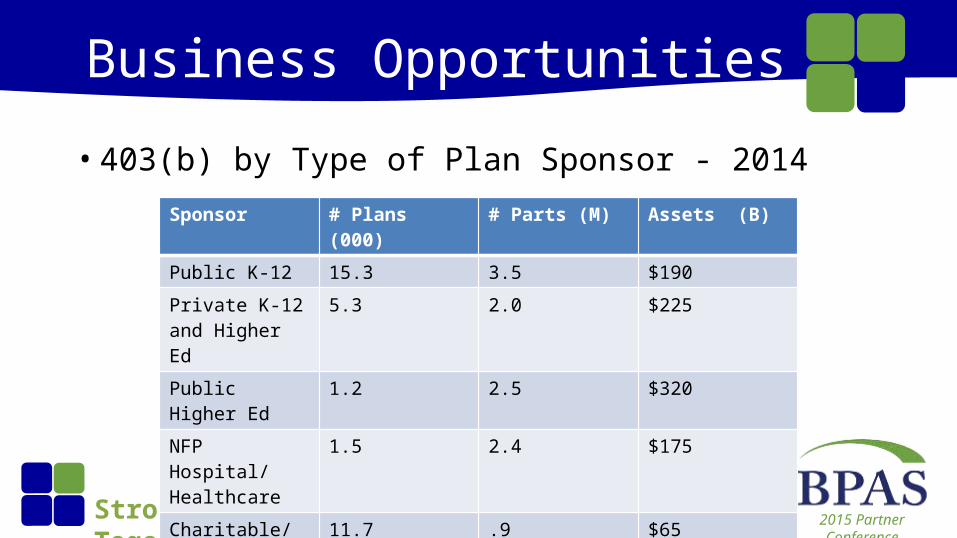

• 403(b) by Type of Plan Sponsor - 2014Sponsor # Plans (000) # Parts (M) Assets (B)

Public K-12 15.3 3.5 $190

Private K-12 and Higher Ed

5.3 2.0 $225

Public Higher Ed 1.2 2.5 $320

NFP Hospital/Healthcare

1.5 2.4 $175

Charitable/Other NFP

11.7 .9 $65

Total 403(b) 35.0 11.3 $975

2015 Partner ConferenceStronger Together 30

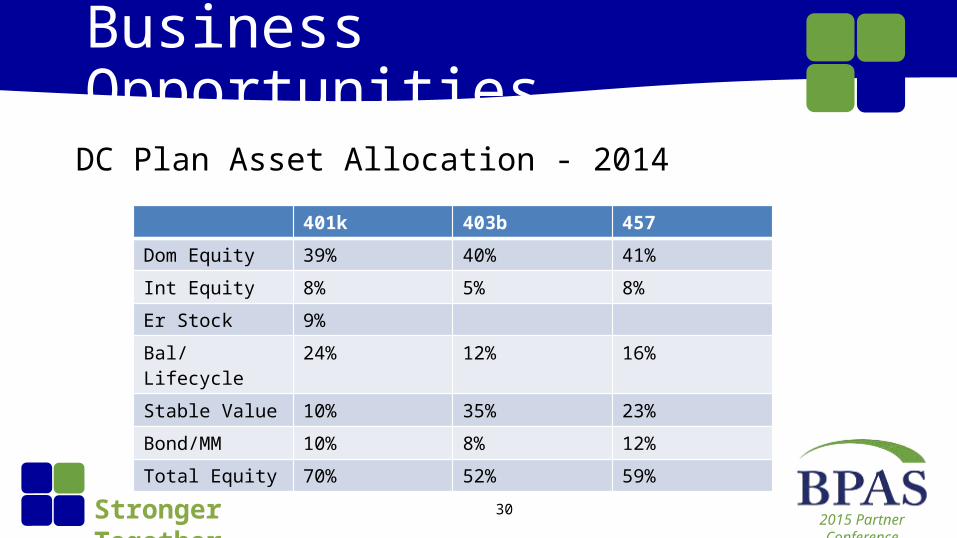

Business Opportunities

DC Plan Asset Allocation - 2014

401k 403b 457

Dom Equity 39% 40% 41%

Int Equity 8% 5% 8%

Er Stock 9%

Bal/Lifecycle 24% 12% 16%

Stable Value 10% 35% 23%

Bond/MM 10% 8% 12%

Total Equity 70% 52% 59%

2015 Partner ConferenceStronger Together 31

Business OpportunitiesPercentage Cash Balance Plans – 2012 (5500 data)

Total Plans Total Assets

# Parts # Plans (000) % CB (Billions) % CB

<10 24.7 19% $21.4 12%

10-50 8.6 37% $12.7 27%

51-100 2.2 20% $8.9 21%

101-250 2.4 10% $23.2 13%

251-500 1.8 9% $34.9 12%

501-1,000 1.5 8% $58.1 9%

1,001-5k 2.5 15% $320.6 16%

>5k 1.3 30% $2,223.5 35%

Total 45.0 21% $2,703.3 32%

2015 Partner ConferenceStronger Together 32

Evolution of 401k Plans

“Houston, in addition to coverage and other systemic plan and regulatory issues, we have a

spending problem.”

2015 Partner ConferenceStronger Together 33

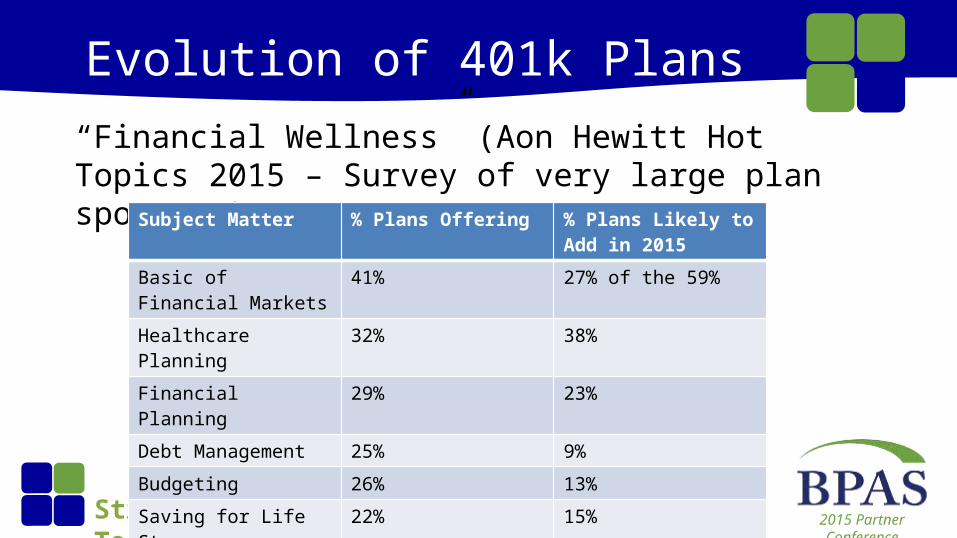

Evolution of 401k Plans“Financial Wellness” (Aon Hewitt Hot Topics 2015 – Survey of very large plan sponsors)

Subject Matter % Plans Offering % Plans Likely to Add in 2015

Basic of Financial Markets

41% 27% of the 59%

Healthcare Planning 32% 38%

Financial Planning 29% 23%Debt Management 25% 9%Budgeting 26% 13%Saving for Life Stages 22% 15%

2015 Partner ConferenceStronger Together 34

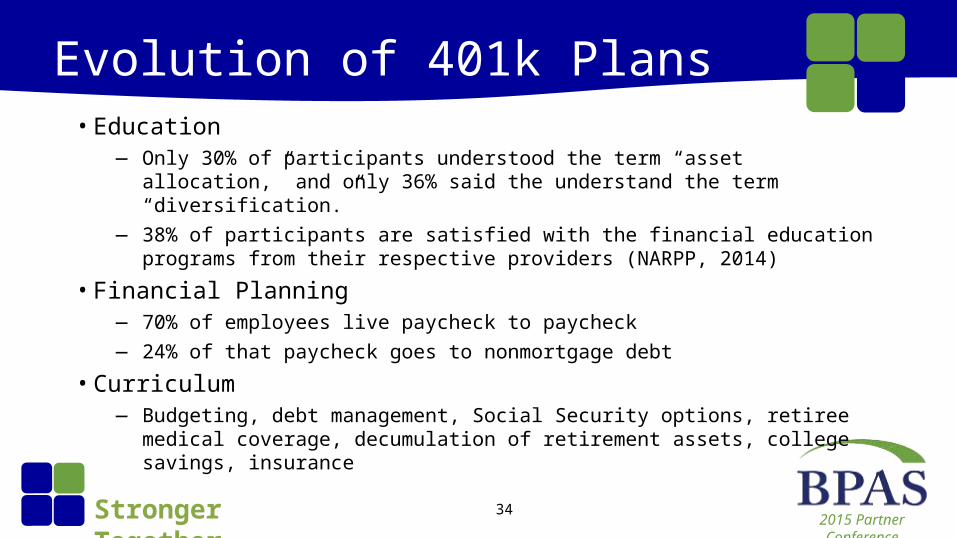

Evolution of 401k Plans• Education

— Only 30% of participants understood the term “asset allocation,” and only 36% said the understand the term “diversification.”

— 38% of participants are satisfied with the financial education programs from their respective providers (NARPP, 2014)

• Financial Planning— 70% of employees live paycheck to paycheck— 24% of that paycheck goes to nonmortgage debt

• Curriculum— Budgeting, debt management, Social Security options, retiree medical

coverage, decumulation of retirement assets, college savings, insurance

2015 Partner ConferenceStronger Together 35

Evolution of 401k Plans• “Participants”

— The fiduciary regulations will lead to more participants leaving their balances in the plan

— Accordingly, education programs should consider the terminated participant audience

— Traditional methods of workplace education should be re-evaluated

• Education and Fee Compression— Holistic financial planning commands a premium— Financial wellness has a proven ROI

• Stress, absenteeism, turnover, positive turnover

2015 Partner ConferenceStronger Together 36

Evolution of 401k Plans• Coverage and Participation Rates

— Expanded use of MEP and MET arrangements— Universal eligibility for K participant

• Similar to 403b regs— Fees for non-statutory eligible participants

• Similar to terminated participant regs— Expanded use of auto features

• State plan provisions will create pressure for a mandate within qualified plans

— Federal pre-emption for auto plans in non-ERISA plans• 403b and 457

2015 Partner ConferenceStronger Together 37

Evolution of 401k Plans• Reducing Leakage and Retaining Assets Post Termination of

Employment – 401k for Life— Installment payment plan provisions— Rollover plan provisions— Loan plan provisions (limits and continuity)— Lifetime income products— Longevity insurance— Plan vs. participant level advice— “Distributable event”

2015 Partner ConferenceStronger Together 38

Evolution of 401k Plans• Regulatory Issues

— Plan audits attributable to terminated participant counts— Fiduciary liability for terminated participant balances— Electronic notices

• Service Requirements— 3(16) level for terminated participants

2015 Partner ConferenceStronger Together 39

Summary

• We, as a professional society, must increase the percentage of working Americans who are retirement income ready• Many of the tools to accomplish such are available; we

need to find more cost effective ways to serve the non-covered constituency

2015 Partner ConferenceStronger Together 40

Summary

• We must break through the resistance to auto plans— Auto enrollment without auto escalation is an ineffective and

misleading strategy

• Addressing broader aspects of financial wellness will create opportunities for higher retirement savings rates• Limits on IRA rollover transactions will create opportunities

for Specialist Investment Advisors to increase AUM through reduced leakage

2015 Partner ConferenceStronger Together 41

Next Up!• Paul Neveu, President, BPAS Plan Administration and

Recordkeeping Services• Steve Saxon, Groom Law Group

— Update on Proposed Fiduciary Regs• Ralph Acampora, Altaira Wealth Management• Tom Kmak, Fiduciary Benchmarks, Inc.• Brian Bouchard, Thornburg Investment Management

— Fee Policy Statements• Several Panel and Group Presentations

2015 Partner ConferenceStronger Together

Questions

Thank you

Barry S. Kublin, Chief Executive Officer

Benefit Plans Administrative Services, Inc.