USAGE OF NATIONAL INBOUND TOURISM STATISTICS AT PROVINCIAL

LEVEL

Khumbu Sithole, Snr Mgr: Research & ICT

Statistics for Africa Workshop

Tuesday, 10 February 2009

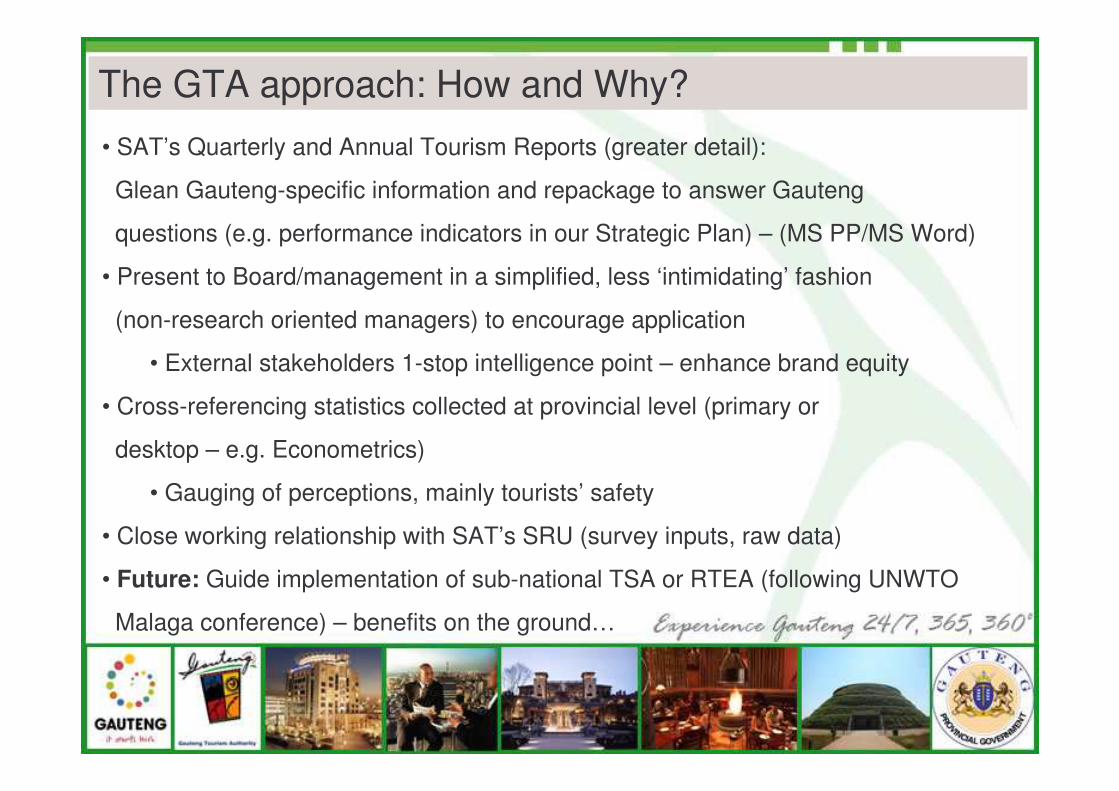

The GTA approach: How and Why?

• SAT’s Quarterly and Annual Tourism Reports (greater detail):

Glean Gauteng-specific information and repackage to answer Gauteng

questions (e.g. performance indicators in our Strategic Plan) – (MS PP/MS Word)

• Present to Board/management in a simplified, less ‘intimidating’ fashion

(non-research oriented managers) to encourage application

• External stakeholders 1-stop intelligence point – enhance brand equity

• Cross-referencing statistics collected at provincial level (primary or

desktop – e.g. Econometrics)

• Gauging of perceptions, mainly tourists’ safety

• Close working relationship with SAT’s SRU (survey inputs, raw data)

• Future: Guide implementation of sub-national TSA or RTEA (following UNWTO

Malaga conference) – benefits on the ground…

Prepared by: GTA Strategic Research Unit

For Senior Management

22 September 2008

An Overview of Inbound TourismA comparative analysis from a Global, National and

Provincial perspective - 2006 and 2007

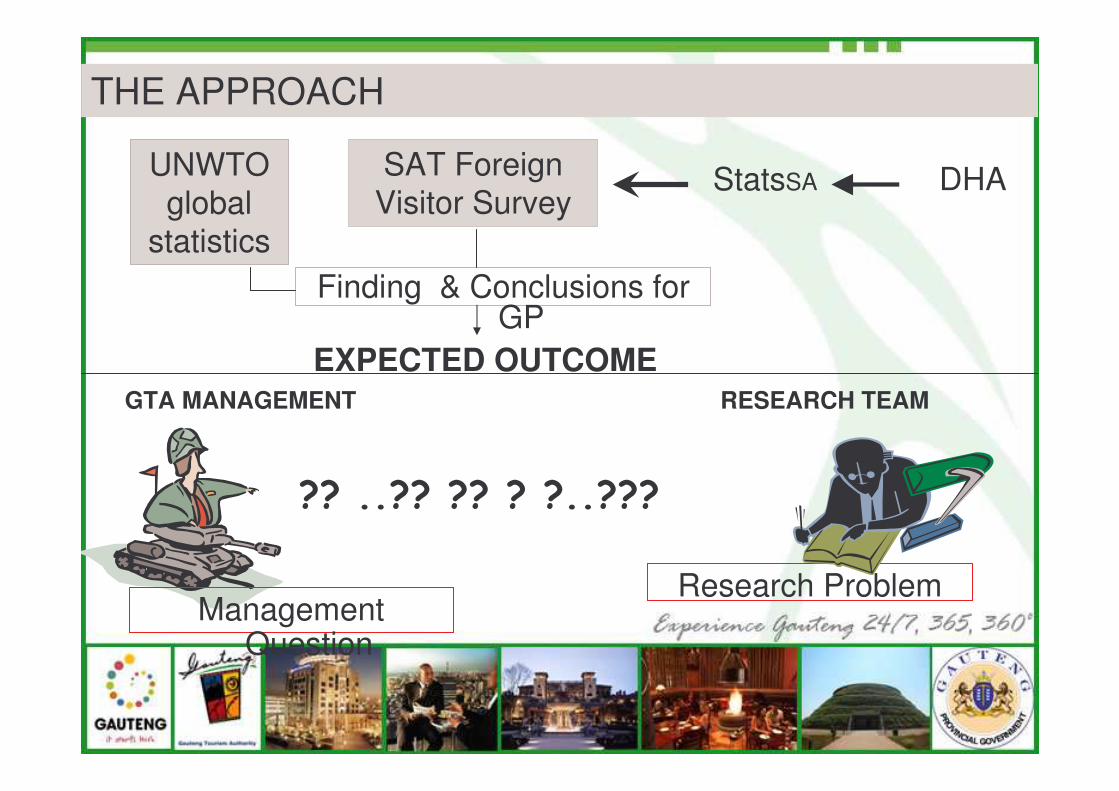

THE APPROACH

Finding & Conclusions for GP

UNWTO global

statistics

SAT Foreign Visitor Survey

DHAStatsSA

Research ProblemManagement

Question

EXPECTED OUTCOMEGTA MANAGEMENT RESEARCH TEAM

�������������������

• Face to face interviews at (OR Tambo International and Cape Town International airport) and land border posts.

• Sampling methodology - stratified probability design and arrivals are used to determine proportions.

• The surveys are conducted over a period of three weeks every month.

• The land survey sampling is day of the week and time randomization.

• The sample size is 26, 400 interviews per year – 1600 Airport and 6000 Land border posts

Methodology

• Global Tourism Statistics

• South African Foreign Tourism Statistics

• Interpretation of Gauteng’s Performance

AGENDA

Overview of World Arrivals 2006 - 2007

16.4%46.441.0Middle East7.5%44.240.9Africa

In millions

6.6%903846World4.2%553461Europe

4.9%168136Americas

10.4%265168Asia & the Pacific

20072006 % Change

Source: 2007 UNWTO barometerTable: GTA Strategic Research Unit

World Travel Trends

•Mature markets remain leading destination in the world growing at 5.1%. •Economic and tourism growth were driven by emerging and developing countries which grew at 7.7%. AEU and Brics(Brazil, Russia, India & China).•World top destinations

1st – France2nd – China3rd – Spain 28th – South Africa (moving up from 29th position in 2006 &32nd in 2005)

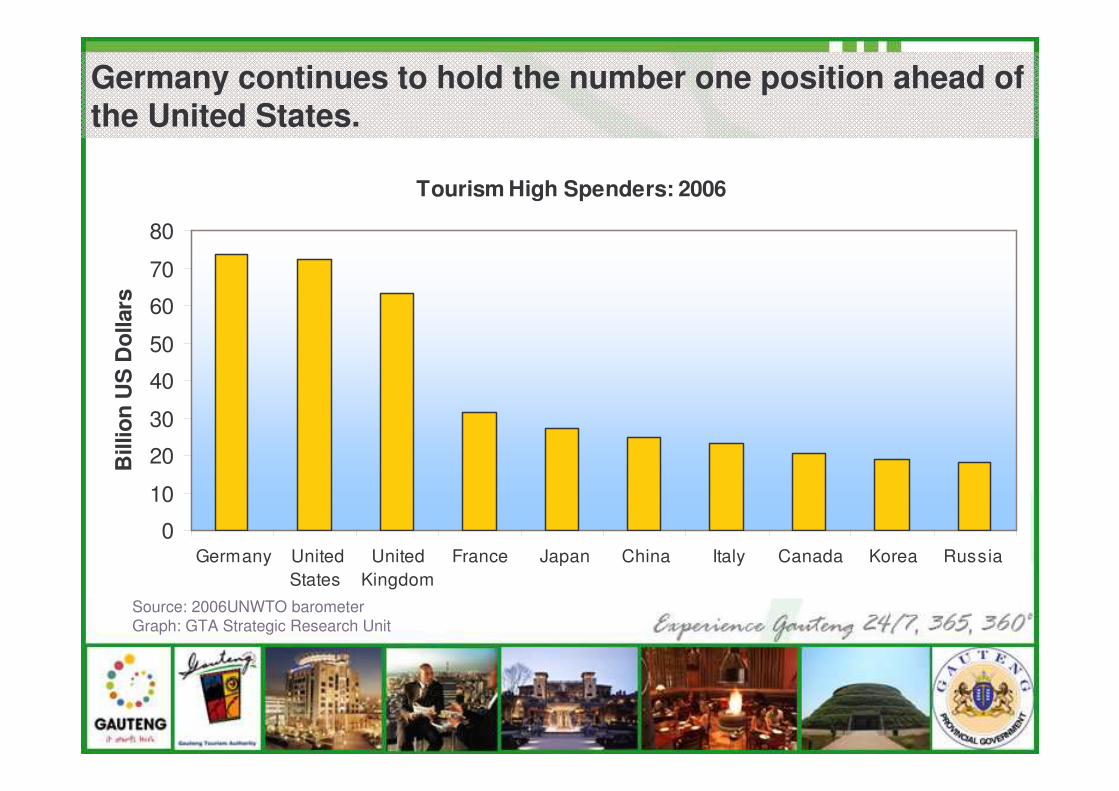

Tourism High Spenders: 2006

0

10

20

30

40

50

60

70

80

Germany UnitedStates

UnitedKingdom

France Japan China Italy Canada Korea Russia

Bill

ion

US

Dol

lars

Germany continues to hold the number one position ahead of the United States.

Source: 2006UNWTO barometerGraph: GTA Strategic Research Unit

World's Top Outbound Travel Markets: 2006 - 2007

-10,00020,00030,00040,00050,00060,00070,00080,00090,000

100,000

Germ

any

UK

USA

China

Canad

a

Italy

Fran

ceNet

herla

nds

Japa

n

India

Brazil

Austra

lia

No

. of

tou

rist

s

2006

2007

Germany, UK and USA remain the top three outbound markets.

Source: 2007 UNWTO barometerGraph: GTA Strategic Research Unit

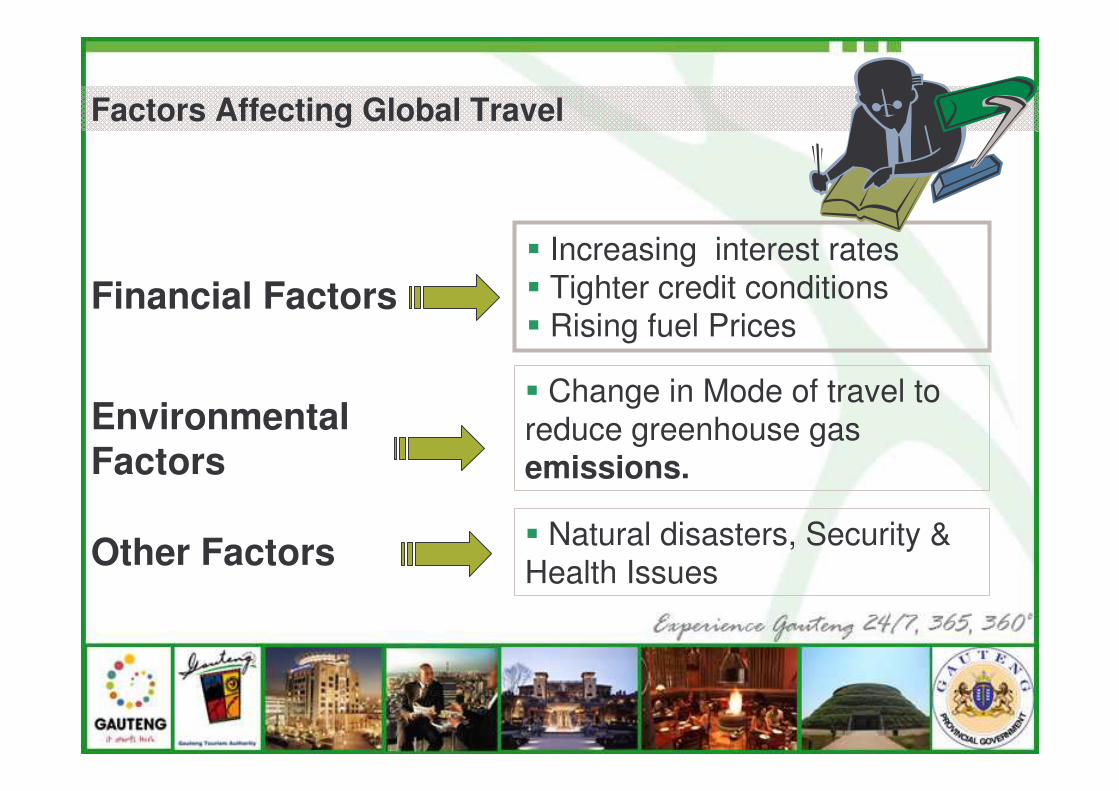

Factors Affecting Global Travel

Financial Factors

Environmental Factors

Other Factors

� Increasing interest rates� Tighter credit conditions� Rising fuel Prices

� Change in Mode of travel to reduce greenhouse gas emissions.

� Natural disasters, Security & Health Issues

• Global Tourism Statistics

• South African Foreign Tourism Statistics

• Interpretation of Gauteng’s Performance

AGENDA

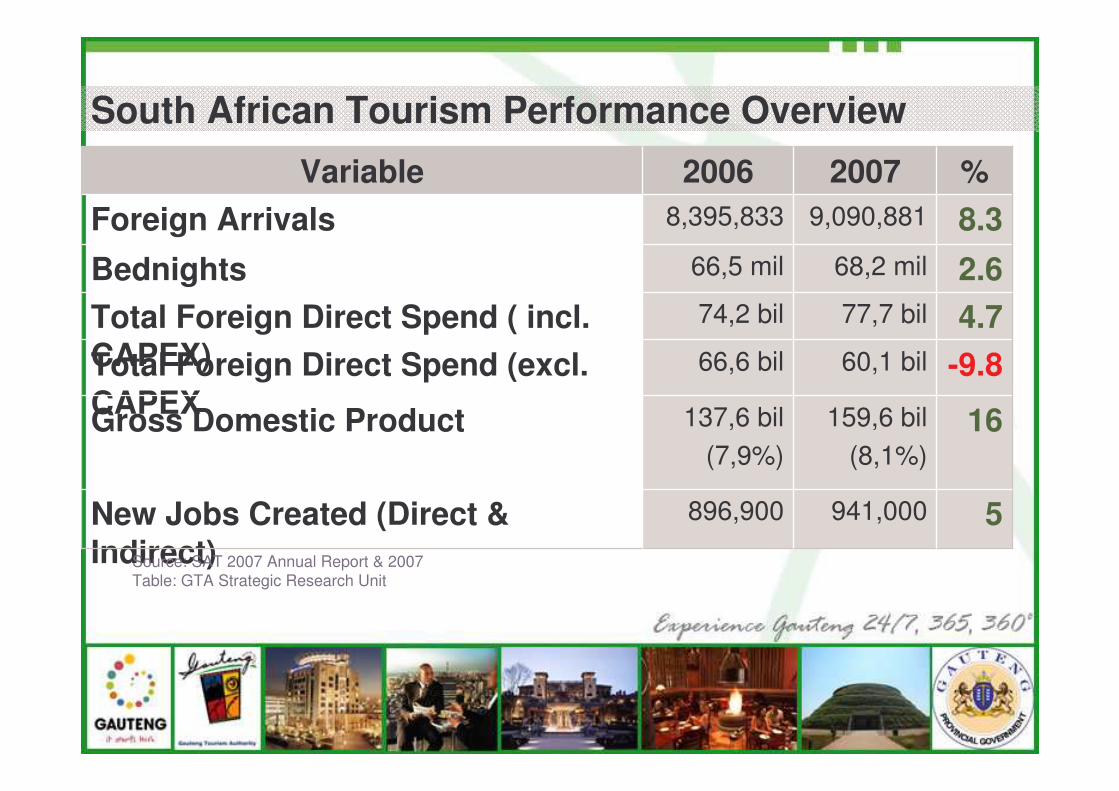

South African Tourism Performance Overview

%

5

16

-9.84.72.68.3

77,7 bil74,2 bilTotal Foreign Direct Spend ( incl. CAPEX)

9,090,8818,395,833Foreign Arrivals68,2 mil66,5 milBednights

159,6 bil(8,1%)

137,6 bil(7,9%)

Gross Domestic Product

941,000896,900New Jobs Created (Direct & Indirect)

60,1 bil66,6 bilTotal Foreign Direct Spend (excl. CAPEX

20072006Variable

Source: SAT 2007 Annual Report & 2007 Table: GTA Strategic Research Unit

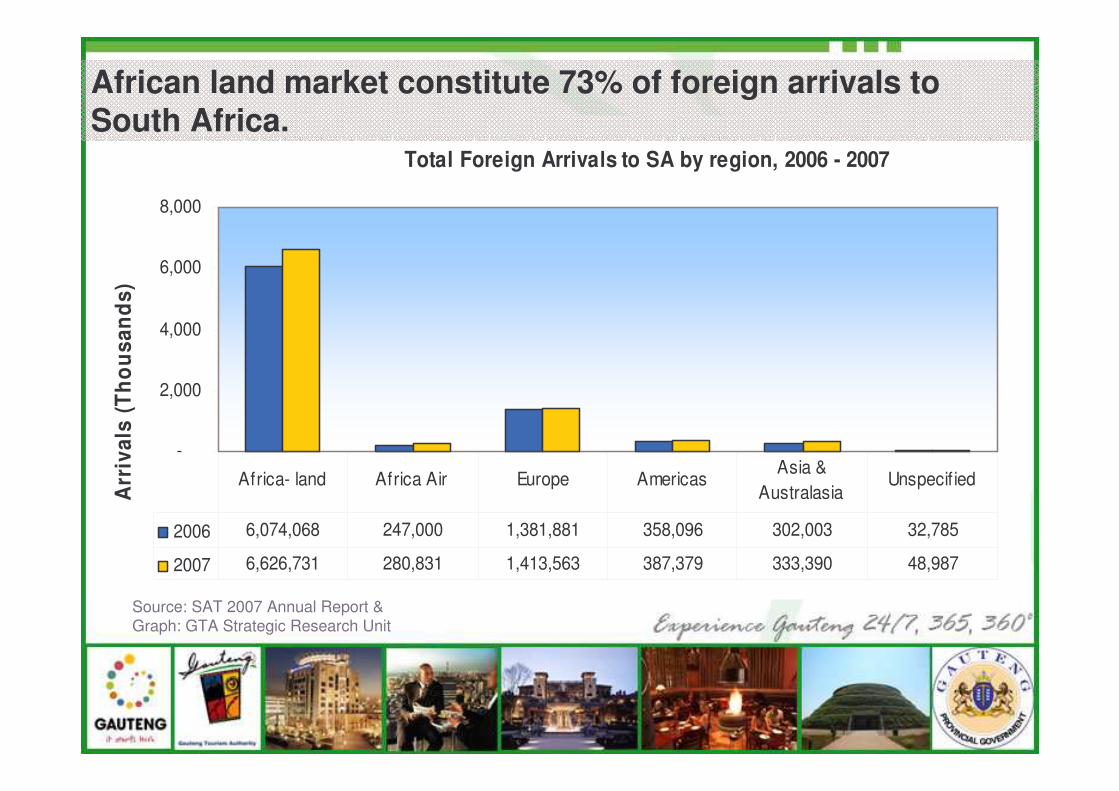

Total Foreign Arrivals to SA by region, 2006 - 2007

-

2,000

4,000

6,000

8,000

Arr

ival

s (T

hous

ands

)

2006 6,074,068 247,000 1,381,881 358,096 302,003 32,785

2007 6,626,731 280,831 1,413,563 387,379 333,390 48,987

Africa- land Africa Air Europe AmericasAsia &

AustralasiaUnspecif ied

African land market constitute 73% of foreign arrivals to South Africa.

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

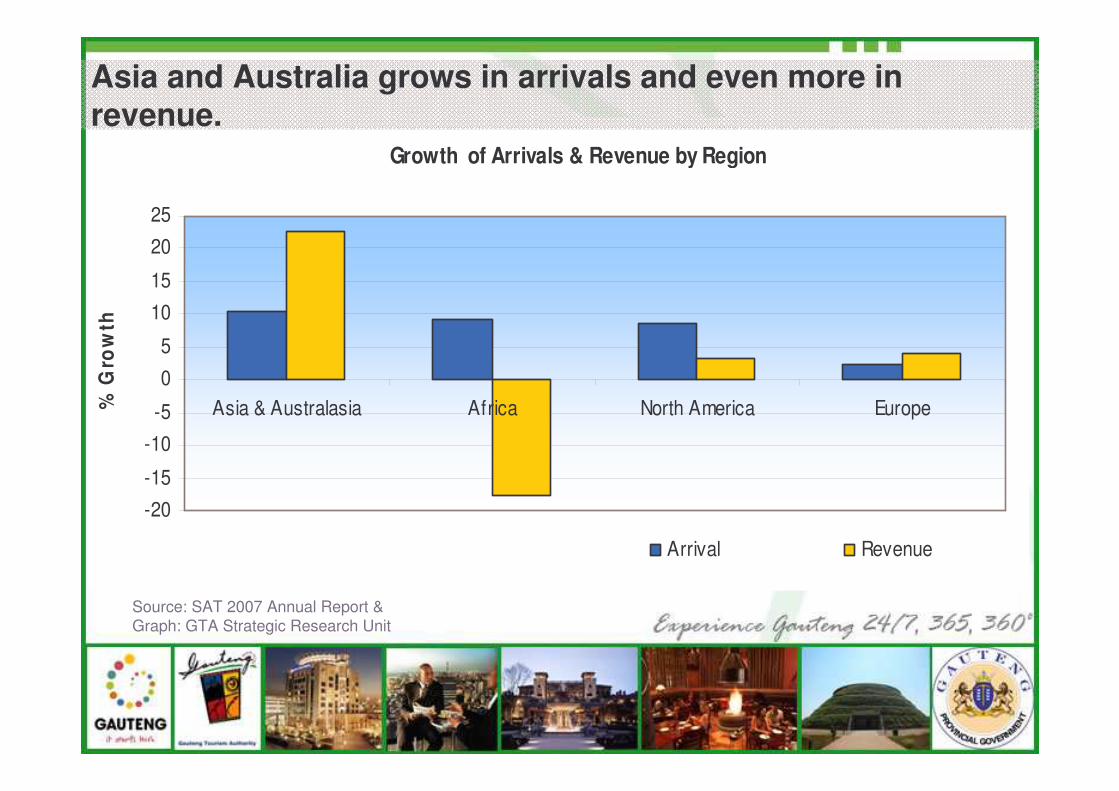

Growth of Arrivals & Revenue by Region

-20-15

-10-5

0

5

1015

2025

Asia & Australasia Africa North America Europe% G

row

th

Arrival Revenue

Asia and Australia grows in arrivals and even more in revenue.

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

Travel Trends in SA

• SA broke a 9 million mark and recorded an 8,3% increase exceeding global average of 6,6%.

• Despite the high growth in volume, revenue generated decreased.

• The greatest decline on spend was on shopping for resale goods (African land markets).

• Expenditure on accommodation decreased by 8.3% ( R 800 mil).

• More nights were spent in B&B’s, self- catering establishments and back-packer hostels while fewer nights were spent in hotels and game lodges.

• Holiday remains the primary purpose of visit 25.3% followed closely by VFR at 24.2%.

• Business tourists increased from 5.8% in 2006 to 7.2% in 2007.

• The average number of provinces visited remained at 1.3.

• Land markets tend to visit one province while air markets visit almost two provinces.

Travel Trends in SA (contd…)

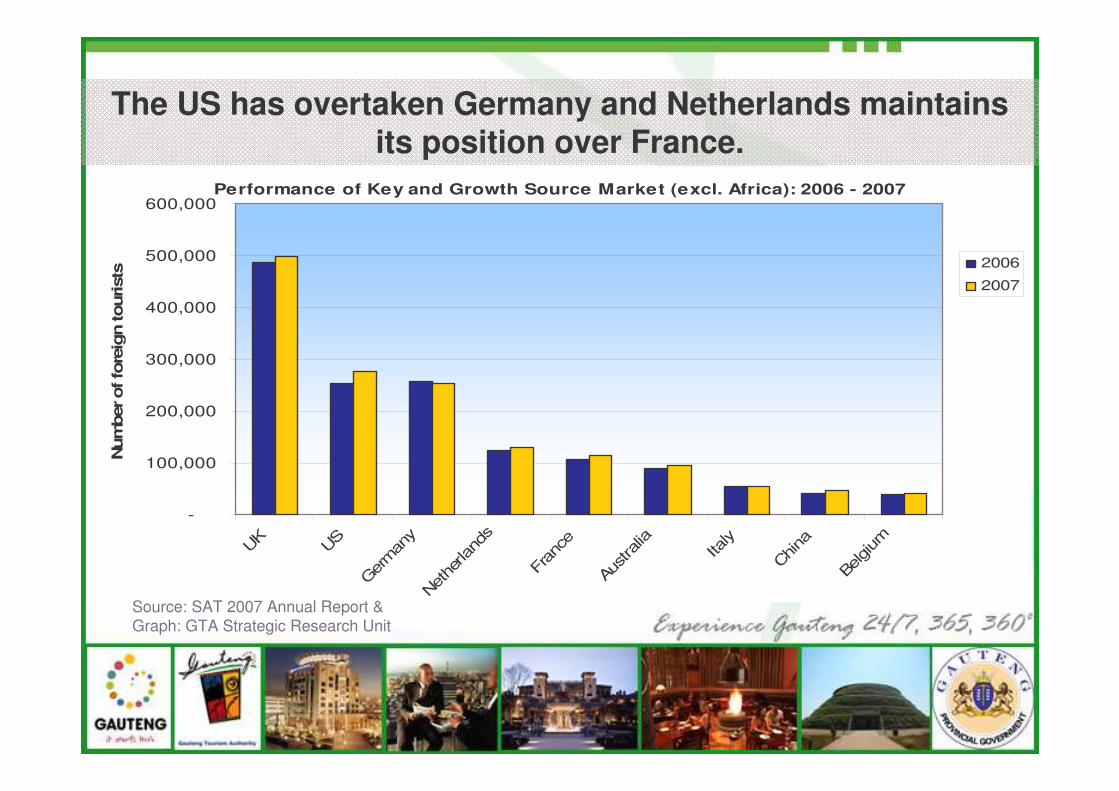

Performance of Key and Growth Source Market (excl. Africa): 2006 - 2007

-

100,000

200,000

300,000

400,000

500,000

600,000

UK US

Germ

any

Nethe

rland

s

Fran

ce

Austr

alia

Italy

China

Belgi

um

Num

ber

of fo

reig

n tourist

s 2006

2007

The US has overtaken Germany and Netherlands maintains its position over France.

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

• Global Tourism Statistics

• South African Foreign Tourism Statistics

• Interpretation of Gauteng’s Performance

AGENDA

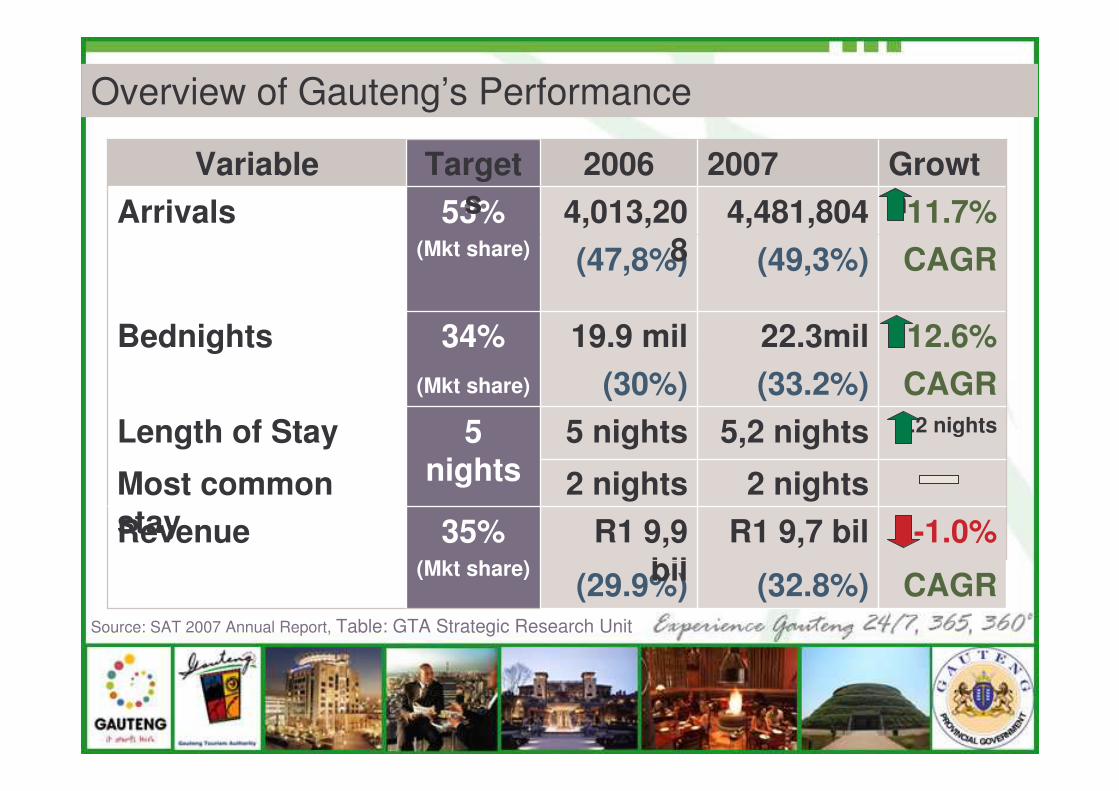

Overview of Gauteng’s Performance

35%(Mkt share)

5 nights

34%(Mkt share)

53% (Mkt share)

Targets

CAGR(32.8%)(29.9%)

CAGR(33.2%)(30%)

-1.0%

.2 nights

12.6%

CAGR11.7%

Growth

(49,3%)(47,8%)4,481,8044,013,20

8Arrivals

22.3mil19.9 milBednights

2 nights2 nightsMost common stay R1 9,7 bilR1 9,9

bilRevenue

5,2 nights5 nightsLength of Stay

20072006Variable

Source: SAT 2007 Annual Report, Table: GTA Strategic Research Unit

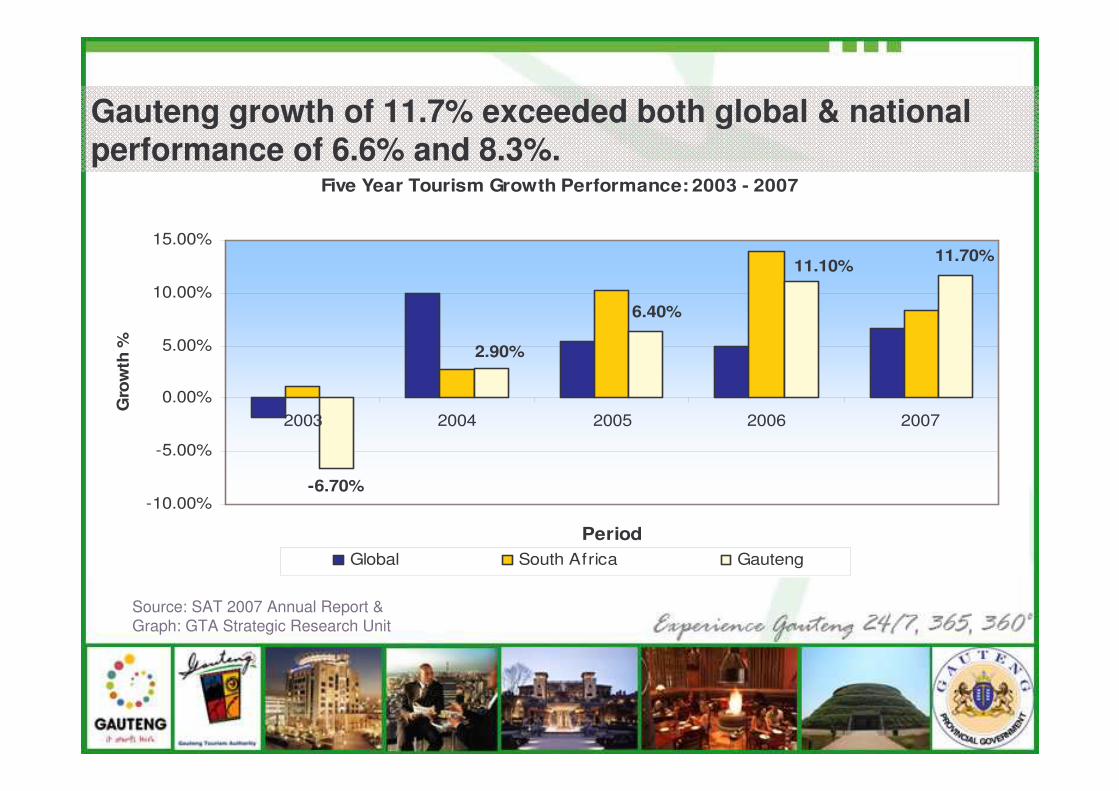

Five Year Tourism Growth Performance: 2003 - 2007

-6.70%

11.10%11.70%

6.40%

2.90%

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

2003 2004 2005 2006 2007

Period

Gro

wth

%

Global South Africa Gauteng

Gauteng growth of 11.7% exceeded both global & national performance of 6.6% and 8.3%.

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

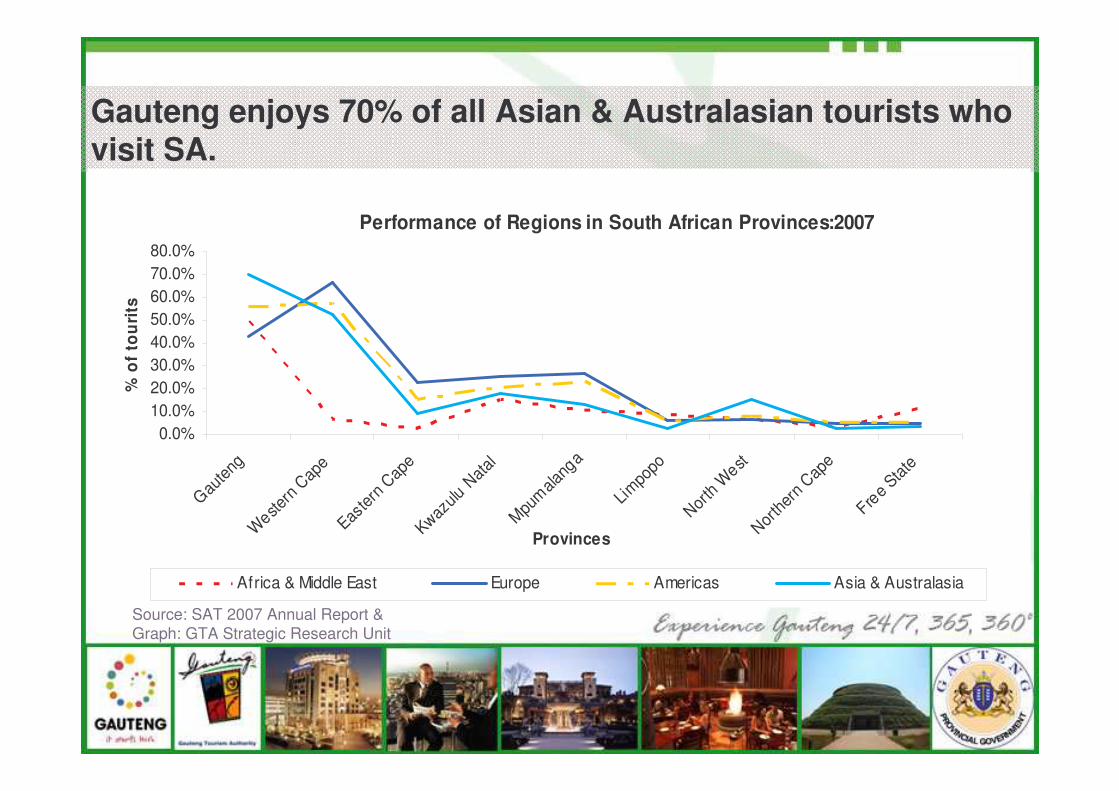

Gauteng enjoys 70% of all Asian & Australasian tourists who visit SA.

Performance of Regions in South African Provinces:2007

0.0%10.0%20.0%30.0%40.0%50.0%60.0%70.0%80.0%

Gauten

g

Western

Cape

Easter

n Cap

e

Kwazulu

Nata

l

Mpumala

nga

Limpo

po

North W

est

Northe

rn Cap

e

Free Stat

e

Provinces

% o

f to

uri

ts

Africa & Middle East Europe Americas Asia & Australasia

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

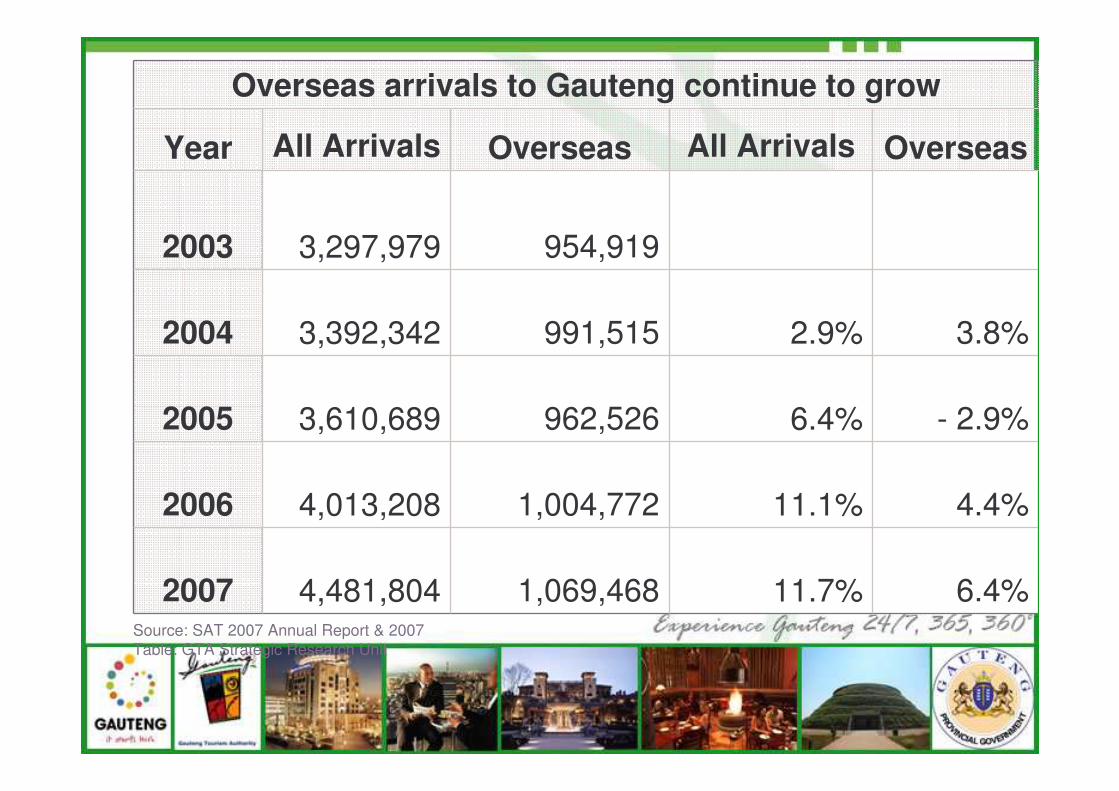

Year

6.4%11.7%1,069,468 4,481,8042007

4.4%11.1%1,004,7724,013,2082006

- 2.9%6.4%962,526 3,610,6892005

3.8%2.9%991,515 3,392,3422004

954,919 3,297,9792003

OverseasAll ArrivalsOverseasAll Arrivals

Overseas arrivals to Gauteng continue to grow

Source: SAT 2007 Annual Report & 2007 Table: GTA Strategic Research Unit

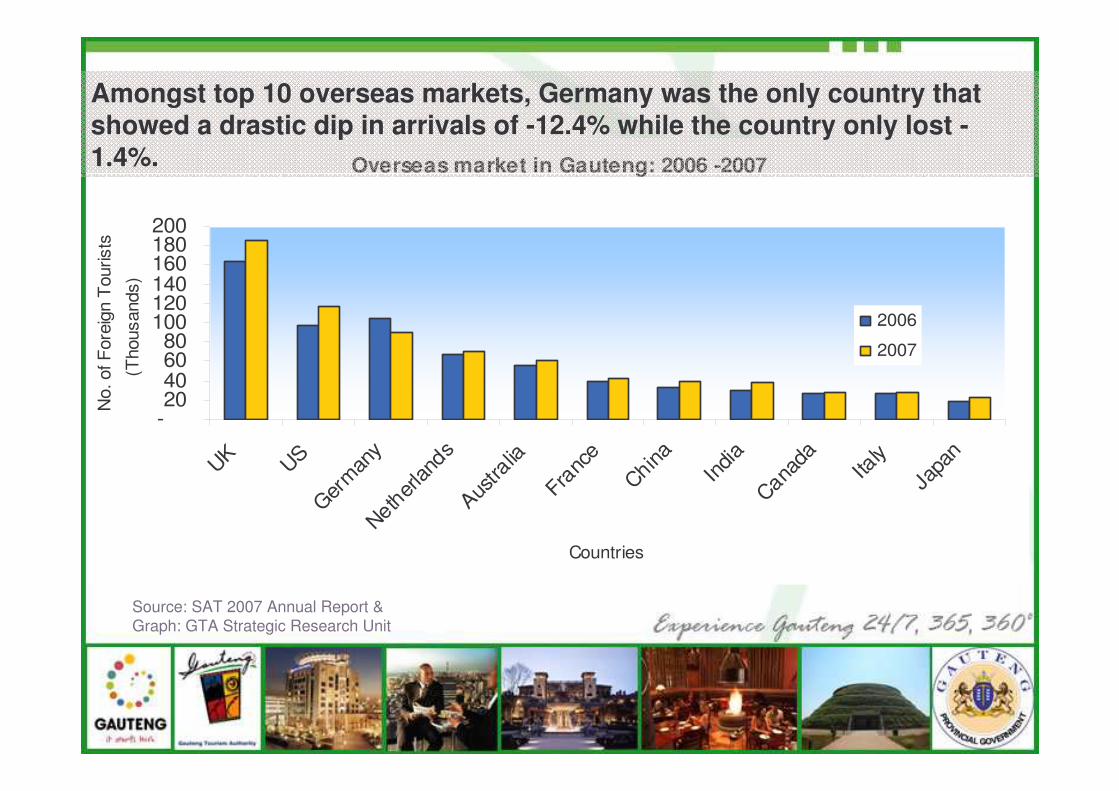

Overseas market in Gauteng: 2006 -2007

-20406080

100120140160180200

UK USGer

many

Netherlan

dsAus

tralia

Franc

e

China

India

Canada

Italy

Japa

n(T

hous

ands

)

Countries

No.

of F

orei

gn T

ouris

ts

2006

2007

Amongst top 10 overseas markets, Germany was the only country that showed a drastic dip in arrivals of -12.4% while the country only lost -1.4%.

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

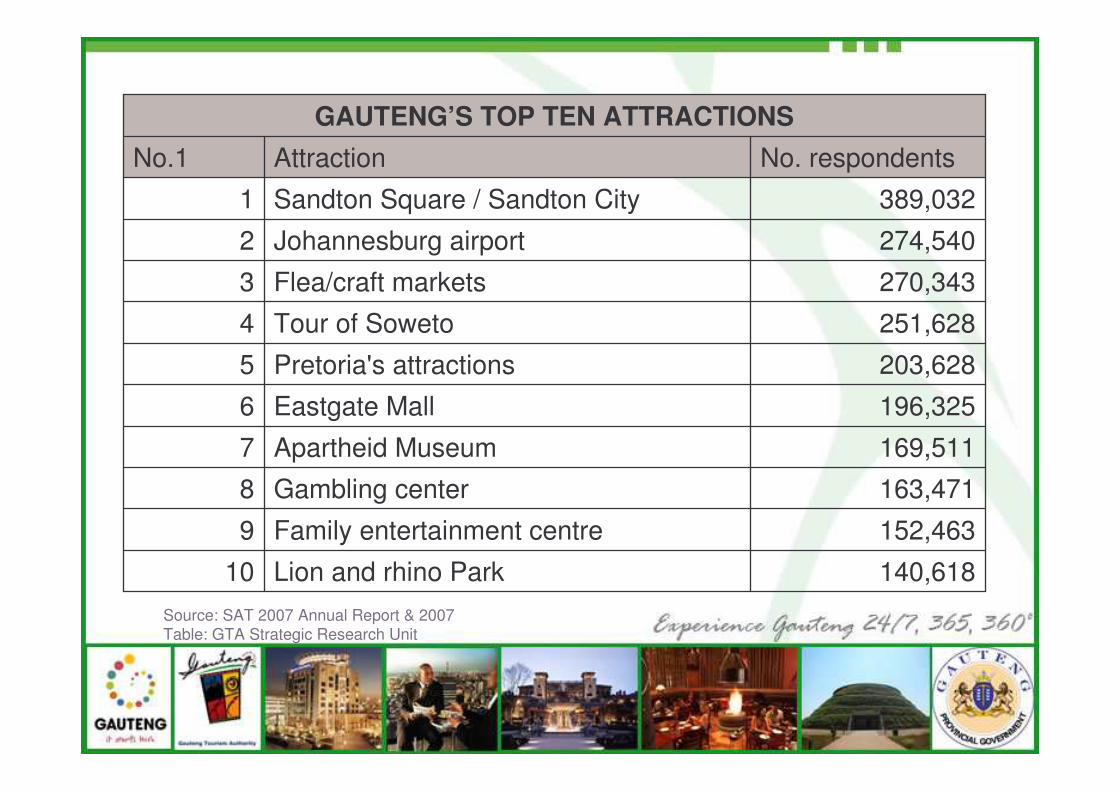

No. respondentsAttractionNo.1

140,618Lion and rhino Park10

152,463Family entertainment centre9

163,471Gambling center8

169,511Apartheid Museum7

196,325Eastgate Mall6

203,628Pretoria's attractions5

251,628Tour of Soweto4

270,343Flea/craft markets3

274,540Johannesburg airport2

389,032Sandton Square / Sandton City1

GAUTENG’S TOP TEN ATTRACTIONS

Source: SAT 2007 Annual Report & 2007 Table: GTA Strategic Research Unit

• Gauteng exceeded both the Global and National growth pace of 6.6% and 8.3%.

• Number of arrivals to GP increased by over 460,000 tourists in 2007.

• 76% of arrivals to Gauteng were Africans.

• Amongst source markets, the highest growth levels (21%) to GP were recorded from China.

• Mozambique as the highest contributor to South Africa’s spend and grew arrivals to Gauteng by 37.2%.

Gauteng’s Tourism Performance

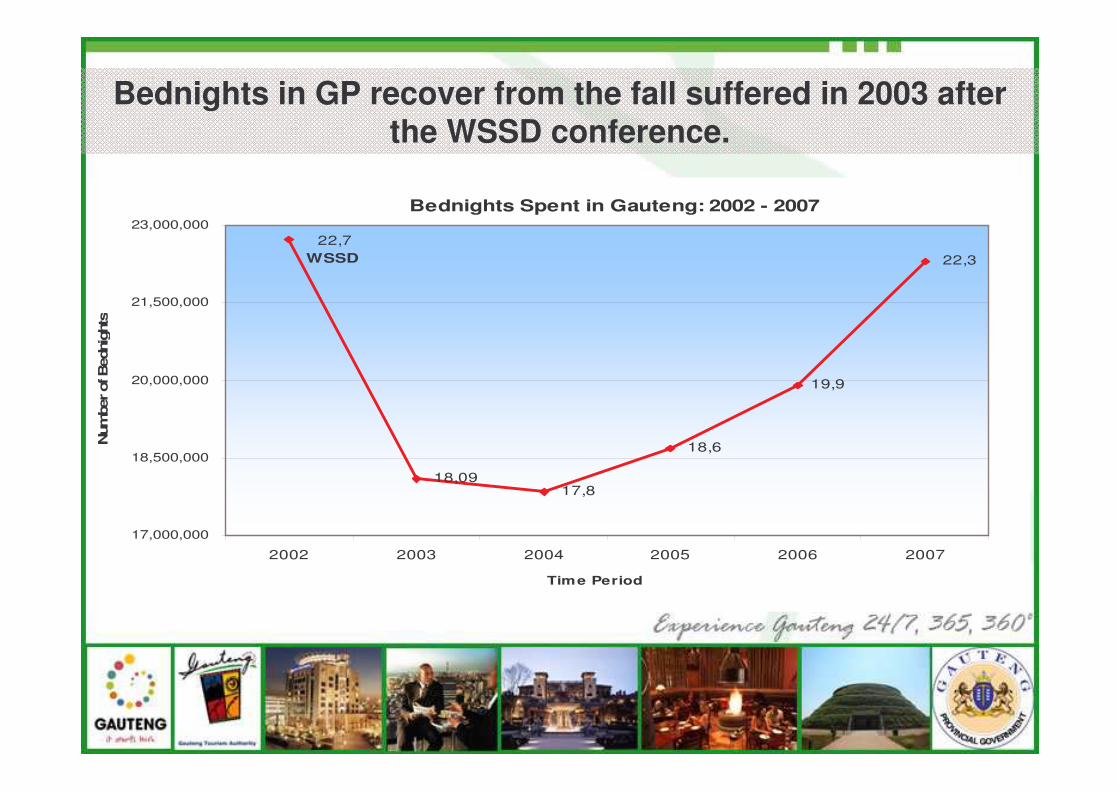

Bednights Spent in Gauteng: 2002 - 2007

22,3

19,9

22,7WSSD

18,09 17,8

18,6

17,000,000

18,500,000

20,000,000

21,500,000

23,000,000

2002 2003 2004 2005 2006 2007

Time Period

Num

ber of

Bed

nigh

tsBednights in GP recover from the fall suffered in 2003 after

the WSSD conference.

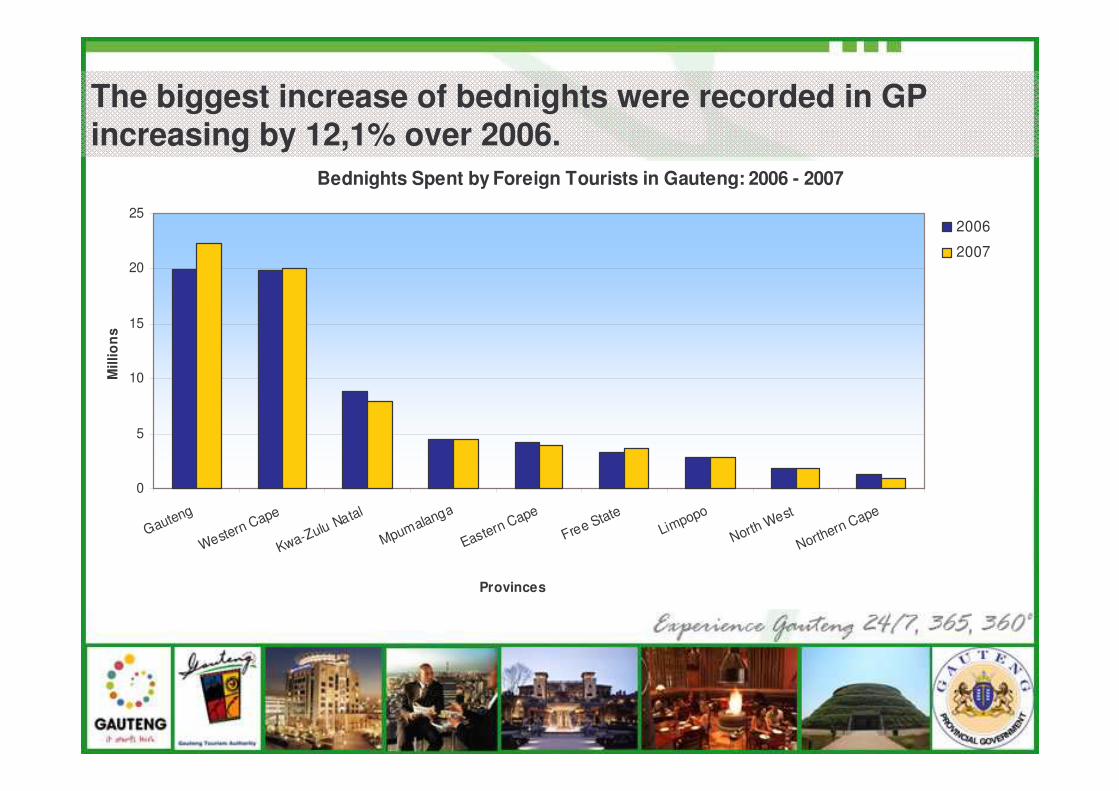

Bednights Spent by Foreign Tourists in Gauteng: 2006 - 2007

0

5

10

15

20

25

Gauteng

Western Cape

Kwa-Zulu Natal

Mpumalanga

Eastern Cape

Free StateLimpopo

North West

Northern Cape

Mill

ion

s

Provinces

2006

2007

The biggest increase of bednights were recorded in GP increasing by 12,1% over 2006.

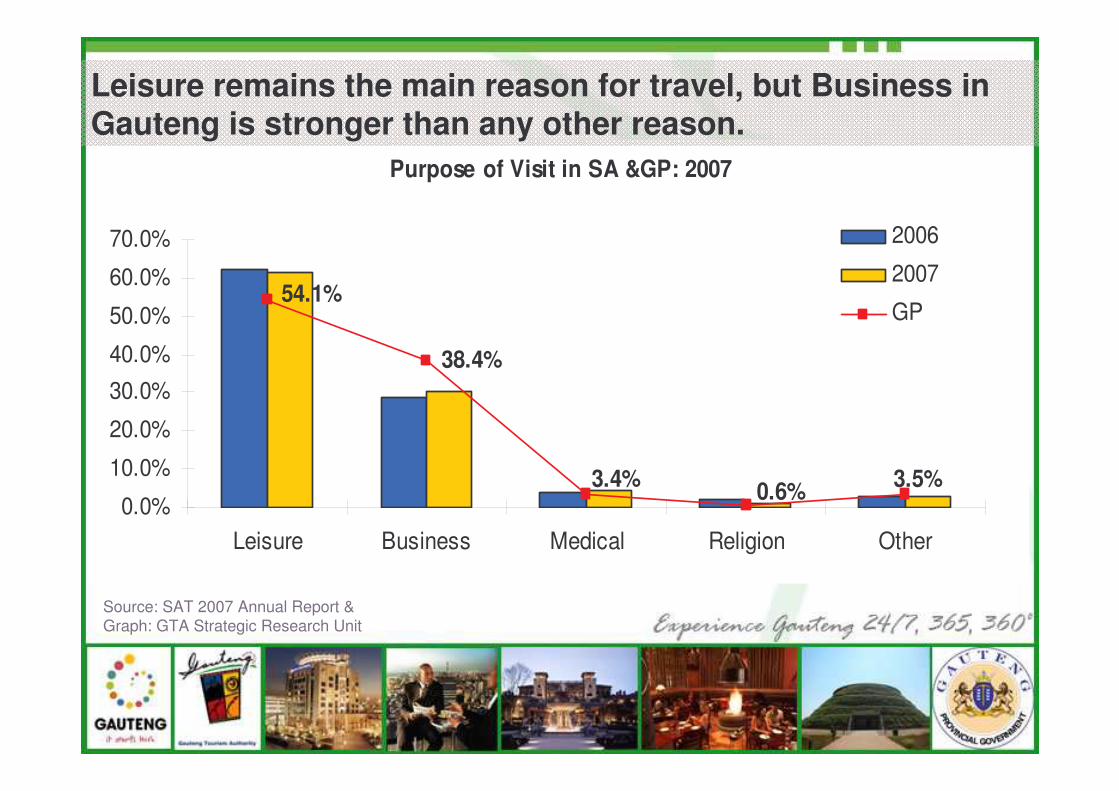

Purpose of Visit in SA &GP: 2007

38.4%

3.4% 0.6% 3.5%

54.1%

0.0%

10.0%

20.0%

30.0%40.0%

50.0%

60.0%

70.0%

Leisure Business Medical Religion Other

2006

2007

GP

Leisure remains the main reason for travel, but Business in Gauteng is stronger than any other reason.

Source: SAT 2007 Annual Report &Graph: GTA Strategic Research Unit

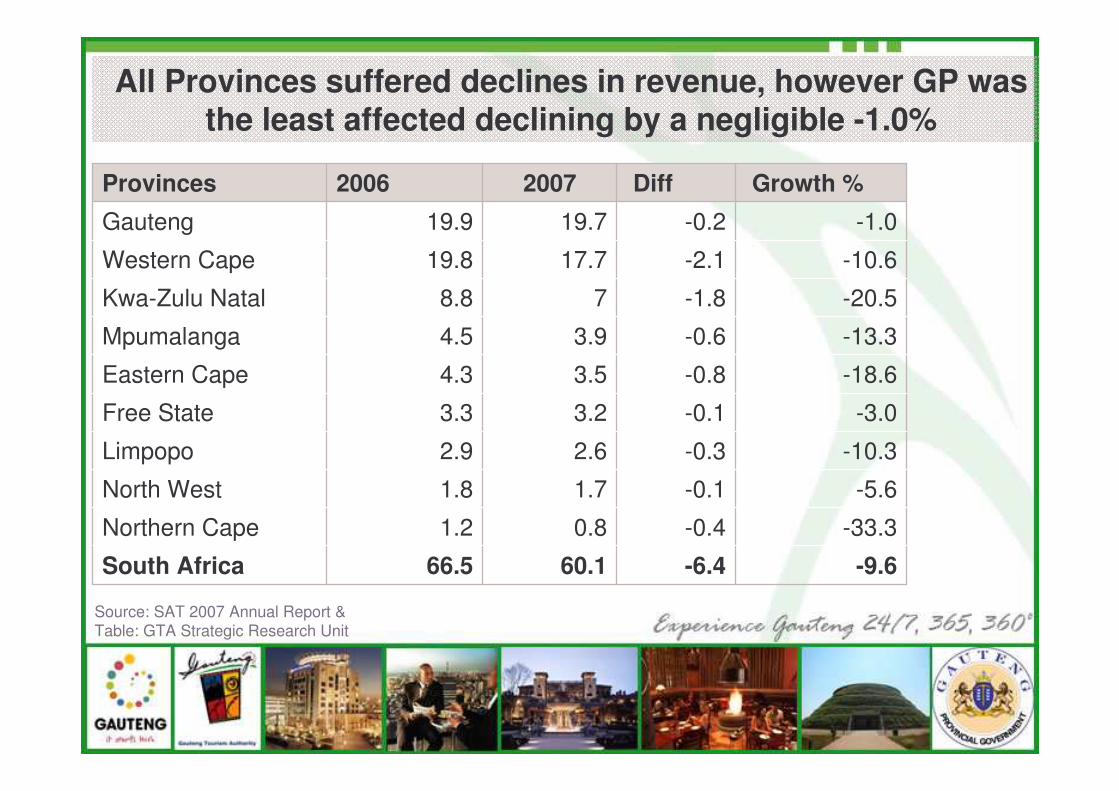

-9.6-6.460.166.5South Africa

-33.3-0.40.81.2Northern Cape

-5.6-0.11.71.8North West

-10.3-0.32.62.9Limpopo

-3.0-0.13.23.3Free State

-18.6-0.83.54.3Eastern Cape

-13.3-0.63.94.5Mpumalanga

-20.5-1.878.8Kwa-Zulu Natal

-10.6-2.117.719.8Western Cape

-1.0-0.219.719.9Gauteng

Growth %Diff20072006Provinces

All Provinces suffered declines in revenue, however GP was the least affected declining by a negligible -1.0%

Source: SAT 2007 Annual Report &Table: GTA Strategic Research Unit

• The gloomy global economy owed to the increasing price of oil and the weakening of the rand against major currencies contributed to the 9.8% decline TFDS (excl. Capex) suffered by the country.

• However, Gauteng experienced a negligible decline of -0.1% in TFDS – a minor blow compared to all other provinces.

• In spite of the decrease in spend, GP’s growth (yoy) in arrivals exceeded both the national and global growth of 6.6% and 8.3%, respectively.

In Conclusion

• We need an elevated interaction with management.• Feedback and/or concrete plans with relevant managers

to implement research recommendations.

Recommendation

Leverage on this interpretation of the results towards to maximizing Return on Investment (ROI).

�������������������

Research Problem

Management Question Identify Problems and Opportunities

THANK YOU!

![INBOUND MARKETING DOES NOT CLOSE DEALS [INBOUND 2014]](https://static.documents.pub/doc/80x56/559419561a28ab650d8b4634/inbound-marketing-does-not-close-deals-inbound-2014.jpg)

![SELLING INBOUND: TRANSFORM YOUR REP'S INBOUND SELLING SKILLS [INBOUND 2014]](https://static.documents.pub/doc/80x56/55d54cf8bb61ebdb228b46ca/selling-inbound-transform-your-reps-inbound-selling-skills-inbound.jpg)