VETERANS BENEF ITS ADMINISTRAT ION NOVEMBER 1 , 2012

VA REGIONAL LOAN CENTER Saint Paul, Minnesota

Construction & Valuation Fee Appraiser Guide

INFORMATION FOR FEE APPRAISERS AND LENDERS’ STAFF APPRAISAL REVIEWERS

Serving - Illinois, Iowa, Kansas, Minnesota, Missouri, Nebraska,

North Dakota, South Dakota, and Wisconsin

i

PREFACE

Introduction:

This Fee Appraisers Handbook is intended to supplement the appraisal requirements and guidelines provided in the Lender’s Handbook, VA Pam 26‐7. Where there are any inconsistencies between this Fee Appraisers Handbook and the Lenders Handbook, the St. Paul VA Regional Loan Center should be contacted for clarifications and the Lenders Handbook will be considered the controlling document. Appraisers must be familiar with Chapters 10 through 13 of this handbook.

The VA Lender’s Handbook is available online at

http://www.warms.vba.va.gov/pam26_7.html In addition, appraisers are encouraged to periodically check the following websites for additional information and program updates as:

http://benefits.va.gov/stpaul/AppraisersHome.asp

http://www.benefits.va.gov/homeloans/new.asp

Statement of VA Expectations:

In addition to quality appraisal reports completed in a timely fashion, the Department of Veterans Affairs expects and requires the highest standards of professional conduct from its Fee Panel members. This includes courtesy, appearance, and customer service. Remember, that in the eyes of the clients (e.g., Veterans, lenders, Realtors, and others),

you represent VA. While we recognize and respect your right to conduct your appraisal business as you see fit, VA has the right and responsibility to ensure that the Loan Guaranty program is administered for the benefit of our Veterans.

Reminders:

If the Veterans Information Portal is not operating, it is acceptable to e‐mail an appraisal to a lender to prevent a delay for a Veteran. Please upload the appraisal when the Portal is back in operation. Appraisals should not be e‐mailed to VA unless specifically requested by VA staff.

ii

When it appears that the appraised value will be below the sales price the appraiser is required to notify the lender, or their POC, and document the URAR as described in detail on page 17. Appraisers are required to have an e‐mail address for communicating with VA Staff and lenders. Please send an e‐mail to [email protected] with any changes in your e‐mail address so we can update our distribution list.

E‐APPRAISAL IS NOW WebLGY:

The e‐appraisal functions have been consolidated into WebLGY (E‐Appraisal is no longer in use). WebLGY is located on the Veterans Information Portal. The Internet address is: http://vip.vba.va.gov. For help with user IDs or passwords, please e‐mail: [email protected]. The Regional

Loan Centers do not have the ability to assist with passwords. When an appraisal is requested online in WebLGY, the appraisal request will be e‐mailed to the assigned appraiser. We strongly recommend that appraisers check WebLGY for new assignments on a daily basis. All VA appraisals will be uploaded in WebLGY, which is located on the Veteran’s Information Portal at http://vip.vba.va.gov. Before uploading an appraisal, appraisers must be sure the .pdf file is named with the VA case number (i.e., 17‐17‐6‐1234567.pdf), not just “1234567.pdf” or a name assigned by appraisal report software.

After an appraisal has been uploaded into WebLGY, any future uploads under the same case number and will “write over” the appraisal that was already uploaded. In order to add pages to an appraisal in WebLGY, the entire report must be uploaded with the additional pages. Technical questions concerning WebLGY will be e‐mailed to [email protected].

iii

Table of Contents PREFACE .............................................................................................................................................. i

Table of Contents ............................................................................................................................... iii Contact Information ……………………………… ........................................................................................... vi

Chapter 1: ........................................................................................................................................... 1 1.1 Timeliness Guidelines .............................................................................................................. 1 1.2 Appraiser Contact Information ................................................................................................ 2 1.3 Appraiser Availability .............................................................................................................. 2 1.4 Media Access .......................................................................................................................... 3 1.5 Phone/Fax Availability ............................................................................................................ 3

Chapter 2: Appraiser Conduct and Allowable Fees .............................................................................. 4 2.0 General Conduct ..................................................................................................................... 4 2.1 Conflicts of Interest ................................................................................................................. 4 2.2 Use of Associate Appraisers ..................................................................................................... 6 2.3 Confidentiality Requirements .................................................................................................. 6 2.4 Fees and Collection Issues ....................................................................................................... 7

2.4.1 Fee Schedule: ........................................................................................................... 7 2.4.2 Mileage Fees: ......................................................................................................... 7 2.4.3 Payment Policy: ...................................................................................................... 8

Chapter 3: VA Quality Control ............................................................................................................. 9 3.1 Desk and Field Reviews of Appraisal Reports .......................................................................... 9 3.2 Quality Control and Standards ................................................................................................. 9

3.2.1 Substantive Error: .......................................................................................................... 9 3.2.2 Non‐Substantive Errors: ............................................................................................... 10

3.3 Complaints ............................................................................................................................ 10 3.4 Summary of Deficiencies and Administrative Action .............................................................. 10

3.4.1 Summary of Deficiencies: ………………………………………………………………….………………………. 10 3.4.2 Administrative Actions: ..................................................................................................... 11 3.5 Disciplinary Due Process ........................................................................................................ 11

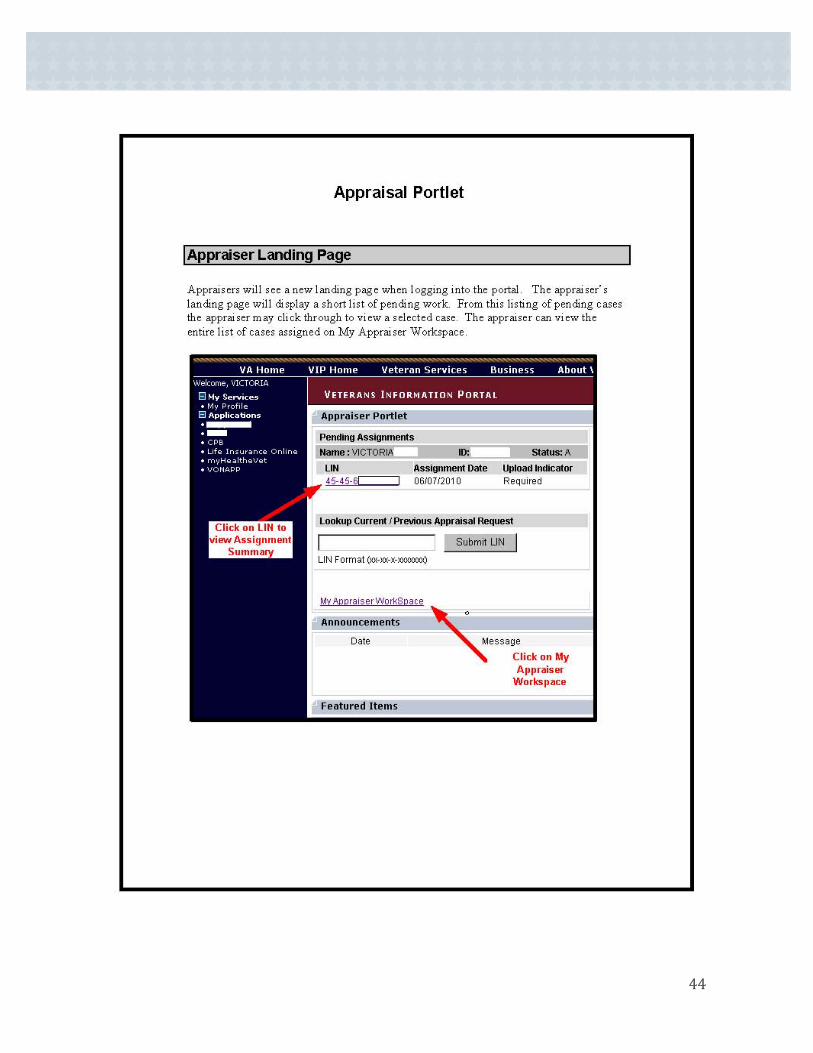

Chapter 4: Veterans Information Portal (VIP) & WebLGY ................................................................... 12 4.1 Registration ........................................................................................................................... 12 4.2 Appraisal Portlet ................................................................................................................... 12 4.3 Assignment Procedures ......................................................................................................... 13 4.4 Creating the PDF Appraisal Report ........................................................................................ 13 4.5 Uploading Appraisal Reports ................................................................................................. 14 4.6 VIP Portal Problems .............................................................................................................. 15

Chapter 5: Communication with LAPP Staff Appraisal Reviewers (SARs) …………………………. 16 5.1 The Role of the LAPP Staff Appraiser Reviewer (SAR) ............................................................ 16 5.2 Contact and Cooperation with the LAPP SAR ......................................................................... 16 5.3 Tidewater Initiative ............................................................................................................... 17 5.4 LAPP Reconsiderations of Value ............................................................................................ 17 5.5 Servicer Appraisal Processing Program Staff Appraiser Reviewer (SAPP SAR) ........................ 17

iv

Chapter 6: VA Appraisal Requirements .............................................................................................. 18 6.1 Properties Not Eligible For VA Guaranty & Appraisal ............................................................. 18 6.2 USPAP ................................................................................................................................... 19 6.3 Scope VA Appraisal Assignments ........................................................................................... 19 6.5 Approaches to Value ............................................................................................................. 22

6.5.1 Sales Comparison Approach: ........................................................................................ 22 6.5.2 Income Approach: ........................................................................................................ 24 6.5.3 Cost Approach: ............................................................................................................. 24 6.6 USPAP Guidance ............................................................................................................. 25

6.7 Market Analysis .................................................................................................................. 255 6.7.1 Market Conditions Addendum ‐ Form 1004MC ............................................................. 26

Inventory Analysis Section ............................................................................................... 27 Median Sale & List Price, DOM, List/Sale Ratio Section .................................................... 27 Overall Trend Section ...................................................................................................... 27 Seller Concessions ........................................................................................................... 27 Foreclosure Sales and Summary/Analysis of Data ............................................................ 28

6.8 Completing the Uniform Residential Appraisal Report (URAR) ............................................... 28

Chapter 7: Minimum Property Requirements (MPR) ......................................................................... 29 7.1 Overview ............................................................................................................................... 29 7.3 Repair Items Requiring Special Attention .............................................................................. 30 7.4 When to Recommend Rejection of a Property ....................................................................... 31 7.5 Reporting MPR Repair Items ................................................................................................. 31 7.6 Certification of Completion of Repairs ................................................................................... 32

Chapter 8: Liquidation Appraisals ...................................................................................................... 33 8.1 Inspection Requirements....................................................................................................... 33

8.1.1 Vacant Properties ......................................................................................................... 33 8.1.2 Occupied Properties ..................................................................................................... 33

8.2 Market Value vs. Distressed/REO Value ................................................................................ 34 8.2.1 Selection of Comparable Sales ...................................................................................... 34 8.2.2 Use of Distressed / REO Sales ....................................................................................... 35

8.4 Liquidation Addendum Information ...................................................................................... 36

Chapter 9: New and Proposed Construction ...................................................................................... 37 9.1 Built Less Than One Year and Never Owner Occupied (New Construction)............................. 37 9.2 Proposed Construction .......................................................................................................... 37

Chapter 10: Other Property Types and Situations …………………………………………………………………….…….399

10.1 Manufactured Housing Classified as Real Estate .................................................................. 39 10.2 Condominiums and PUDS (Planned Unit Developments) ..................................................... 39 10.3 Special Property Problems and Situations ........................................................................... 40

10.3.1 Properties Subject to Flooding .................................................................................... 40 10.3.2 Farm Residences ........................................................................................................ 40 10.3.3 Properties Near Airports ............................................................................................ 41 10.3.4 Partial Release of Loan Security .................................................................................. 42

v

APPENDIX

Appendix 1: Appraisal Portlet .................................................................................................... 433

Appendix 2: VA Circular 26‐11‐21 ............................................................................................... 577

Appendix 3: VA Circular 26‐11‐14 .............................................................................................. 599

Appendix 4: VA Circular 26‐09‐04 ............................................................................................... 623

Appendix 5: VA Circular 26‐09‐03 ............................................................................................... 644

Appendix 6: VA Liquidation Addendum ...................................................................................... 666

vi

Contacts & Addresses

Phone Numbers: (800) 827-0611 ext. 5421 (612) 970-5421 Fax Number: (612) 970-5499

Email: [email protected]

Veterans Information Portal (VIP) address: http://vip.vba.va.gov

St. Paul web site: http://www.vba.va.gov/rostpaul.htm Staff:

St. Paul Construction and Valuation RLC -

Jay R. Buchite, Valuation Officer Ext. 5318 Dave Campbell, Assistant Valuation Officer Ext. 5541 Ryan Nelson, Assistant Valuation Officer Ext. 5560

Review Appraisers – Ext. 5421

Amy Bennett Stephanie Finken Kevin Gallagher Matthew Jensen Kenneth Stewart Jeremy Schillinger Special Adapted Housing Agents –

Anthony Augello Madison, WI 608-293-3579 Gregory Bell Kansas City, MO 816-246-1411 Ext. 1010 Jim Cruce Wichita, KS 316-688-6763 John Eidel North Dakota/NW Min. 612-970-5546 Jennifer Etten Chicago, IL 312-980-4219 Michael Finkeldey St. Louis, MO 314-552-9407 Theresa Hurley Milwaukee, WI 414-727-6063 Andre Logan St. Louis, MO 314-552-9306 Susan Merrick Des Moines, IA 515-362-7364 Christopher Meyer Madison, WI 608-830-6408 Ashley Nantes Scott and Carver County MN 612-970-5542 Michael Ostwald South Dakota/S. MN 612-970-5552 Carol Scribner NW Wisc. &Twin Cities Metro 612-970-5547 Courtney Shereck Des Moines, IA 515-323-7523 Duane Viglicky Lincoln, NE 402-420-4095 Michael Waclawik Kansas City, MO 816-246-1411 Ext. 1011

1

1.1 Timeliness Guidelines

VA appraisers are required to submit all appraisal reports in a timely manner as outlined herein. The time for submission begins the first business day after the appraisal request is made and ends on the date the report is uploaded to the Appraiser Portlet. Any questions regarding timeliness guidelines should be directed to:

Origination Appraisals: The maximum time for origination appraisals is ten (10) business days (excluding North Dakota which is 20 business days). If there are extenuating circumstances, detailed documentation must be included in the appraisal report. The appraiser is also required to make notes in the case in the Appraiser Portlet and notify the requester on the 26‐1805.

Liquidation Appraisals: The maximum time for liquidation appraisals is five (5) business days (ten in North Dakota). If problems arise regarding access to vacant or occupied properties, the appraiser will immediately notify VA by email at [email protected]. Access appraisal delays must be fully documented in the appraisal report.

Appraisers must document the URAR Fannie Mae 1004 in the “Additional Comments” area on page 3 for conventional single family origination appraisals, the “Summary of Sales Comparison Approach” area on page 3 of the Fannie Mae Form 1073 for condominiums, or in the “Additional Comments” area on page 4 of the Fannie Mae Form 1025 for multi‐family reports, as follows:

R (received) = 01/3/11 A (appraised) = 01/7/11 M (mailed/uploaded) = 01/10/11

If the dates indicate more than 10 business days, an explanation for the delay must be included. We recommend that appraisers check WebLGY for new assignments on a daily basis.

If the requester asks you to delay an appraisal assignment for any reason (e.g. seller is on vacation, house not complete to customer preference items, etc.) and this delay would result in

Chapter 1: Timeliness and Availability

2

a normally unacceptable delay, VA must be notified, and the reason for the delay documented in the appraisal report. Entering an appropriate note in the Appraisal Portlet will is an acceptable means of VA notification.

Frequent Timeliness Issues: When the submission of origination and/or liquidation appraisals indicates a pattern of exceeding the delivery requirements indicated above, RLC staff reserve the right to pursue appropriate corrective and/or disciplinary action on a case‐by‐case basis.

1.2 Appraiser Contact Information

Fee Appraisers must respond to all inquiries about when the appraisal will be completed from any party involved with the transaction (Veteran, lender, real estate broker, or builder). VA Fee Appraisers are expected to represent the Department of Veterans Affairs in a manner that reflects professionalism and customer service. All requests for clarifications deserve a prompt, courteous reply. All contact information must be kept up to date in the Appraiser Portlet and with the VA Regional Loan Center. Appraisers must be available and respond to contact from industry partners within a reasonable period of time (24 hours). Lack of contact may result in appraisal reassignments and/or withholding of future assignments.

1.3 Appraiser Availability

Requests for vacation from the assignments and reassignments from current cases will be directed to the VA. Notify the VA of the day that assignments should be stopped and the day that assignments should resume. You must notify VA at least 7 days in advance when you are going on vacation or will otherwise be unavailable for a period of 3 days or more. Email your request to the general C&V mailbox ([email protected]) and include your state(s) of jurisdiction as well as the date you would like assignments withheld and the date of your return. In addition, it is your responsibility to ensure that all current pending assignments are completed and uploaded to the system. If you are unable to complete an appraisal before your departure, be sure to notify VA so that it can be reassigned. In the event of an emergency that would preclude compliance with the 7‐day notification requirement, every effort should be made to inform VA. If this is not possible, VA should be notified as soon as possible and any delay in the submission of appraisal reports should be documented in the file. Notifying VA to request a reassignment is the responsibility of the appraiser, not the lender. VA staff will reassign the case to another appraiser. When an appraisal assignment is canceled by

3

the requester, the appraiser should notify VA by e‐mail or notation in the system with the public option set.

1.4 Media Access

Internet/Email Access: VA Fee Appraisers must have Internet access that is compatible with all VA online applications; also, appraisers must be able to send and receive email.

1.5 Phone/Fax Availability

A fax machine, or access to a fax machine, is required. Any appraiser found to be without a functioning fax machine may have future assignments withheld until such time as fax communication is available.

A telephone answering machine, voicemail, or someone to answer your phone during normal business hours (8:00 AM ‐ 4:30PM, central time zone) Monday through Friday, is also required. If no one is available to answer your phone or respond to emails during a vacation or other period of unavailability, you are required to have a recorded message informing the caller of the date you expect to return.

4

2.0 General Conduct

As a member of the VA fee panel, you are working on behalf of the U.S. Department of Veterans Affairs. Courteous, professional conduct is required at all times. Conduct to the contrary reflects poorly on yourself and VA. It also does a serious disservice to the Veterans we serve.

Appraisers must be prepared to show a photo ID at each site visit. Appraisers should comply with a request from the property owner, tenant or Veteran purchaser present at the site visit. Appraisers are not authorized to speak to any groups or give interviews for publication in an official capacity for VA (for example, lenders’, builders’ and Realtors’ organizations, newspapers or magazines).

2.1 Conflicts of Interest

The ETHICS RULE of USPAP 2012‐13 states that:

If known prior to accepting an assignment, and/or if discovered at any time during the assignment, an appraiser must disclose to the client, and in the subsequent report certification:

any current or prospective interest in the subject property or parties involved; and any services regarding the subject property performed by the appraiser within the three‐

year period immediately preceding acceptance of the assignment, as an appraiser or in

any other capacity.

Comment: Disclosing the fact that the appraiser has previously appraised the property is permitted except in the case when an appraiser has agreed with the client to keep the mere occurrence of a prior assignment confidential. If an appraiser has agreed with a client not to disclose that he or she has appraised a property, the appraiser must decline all subsequent assignments that fall within the three‐year period.

VA Fee Appraisers are held to the above requirements. The following statement of VA policy provides some examples of conflict of interest as well as other guidelines for fee personnel:

Chapter 2: Appraiser Conduct and Allowable Fees

5

It is neither the desire nor the intent of VA to interfere in the private lives of Fee Appraisers or to infringe upon their personal liberties. It is appropriate, however, for VA to require that persons serving as Fee Appraisers do not engage in private pursuits that conflict with their duties on behalf of the VA. Except as may be otherwise expressly authorized by VA regulations, instructions, or directives, VA requires that, as a condition for appointment and retention on rosters of designated or approved Fee Appraisers, any particular individual serving in such capacities shall not engage in any private pursuits where there may or will be:

• Any connection established that might result in a conflict between the private interests of the VA Fee Appraiser and his/her duties and responsibilities to VA and Veterans.

• Any circumstances wherein information obtained from or through a VA assignment to appraise will be used to the detriment of the Government or Veterans. Specifically, the foregoing statements of policy and the standards contained therein are intended to preclude any Fee Appraiser from ‐

• Selling land to a builder or sponsor and then making an appraisal of a dwelling unit purchased by a Veteran with guaranteed, insured, or direct loan.

• Owning an interest in, being employed by, or operating an architectural, engineering or land planning firm which renders services to builders or sponsors and later accepting an assignment from VA to appraise or inspect dwelling units built or to be built by a particular builder or sponsor for whom architectural, engineering, or land planning services have been rendered by the firm in which the Fee Appraiser has employment or an interest.

• Appraising or inspecting dwelling units on VA assignments and later accepting exclusive selling rights for the homes.

• Appraising or inspecting properties for builders or sponsors who are purchasing hazard insurance or title services with respect to those properties from a company in which the Fee Appraiser or Compliance Inspector has an interest.

• Owning an interest in a project developed by a builder and accepting VA appraisal assignments in another area which the same builder owns, is building, or is handling as real estate broker.

• Having an interest in or representing building supply firms and accepting VA assignments on dwelling units built by builders or sponsors who deal extensively with such supply firms.

• Accepting a VA assignment to appraise property if the fee is contingent upon supporting a predetermined conclusion.

The above examples are not all‐inclusive, but they do illustrate some obvious conflicts of interest. The provisions above do allow you to act as sales agent or broker in connection with a

6

particular property. However, if you receive an appraisal request related to VA financing on that property, then you must immediately contact VA and request reassignment of that case to another appraiser.

2.2 Use of Associate Appraisers

Assignments received by VA Fee Appraisers are to be completed by the appraiser assigned. Delegation of appraisal assignments is explicitly prohibited.

The following tasks cannot be delegated and the VA fee panel appraiser must personally perform:

• view the interior and exterior of the subject (except on liquidation cases in which entry is not possible), and the exterior of each comparable

• select and analyze the comparable properties used in the report • make the final value estimate, and • sign the appraisal report as the appraiser.

If the St. Paul RLC finds evidence that any appraiser other than the VA fee panel appraiser assigned has completed a VA appraisal, the appraiser assigned will be removed from the VA fee panel.

However, Fee Appraisers can rely on assistance from associate appraisers or other administrative staff. Except as prohibited above, if the assigned VA fee panel appraiser relied on significant professional assistance in performing the appraisal or in preparing the appraisal report, the name of that individual and the specific tasks he/she performed must be shown in the “reconciliation” section of the appraisal report. An assistant may sign the report on an addendum page, but not the signature page, to document qualifying experience for future licensing/certification purposes.

2.3 Confidentiality Requirements

St. Paul VA fee panel appraisers are bound by the confidentiality provisions of the ethic provisions of USPAP which state:

An appraiser must protect the confidential nature of the appraiser‐client relationship. An appraiser must act in good faith with regard to the legitimate interests of the client in the use of confidential information and in the communication of assignment results. An appraiser must be aware of, and comply with, all confidentiality and privacy laws and regulations applicable in an assignment.

7

An appraiser must not disclose: (1) confidential information; or (2) assignment results to anyone other than:

the client;

persons specifically authorized by the client;

state appraiser regulatory agencies;

third parties as may be authorized by due process of law; or

a duly authorized professional peer review committee except when such disclosure to

a committee would violate applicable law or regulation.

A member of a duly authorized professional peer review committee must not disclose confidential information presented to the committee.

Comment: When all confidential elements of confidential information and assignment results are removed through redaction or the process of aggregation, client authorization is not required for the disclosure of the remaining information, as modified.

2.4 Fees and Collection Issues

2.4.1 Fee Schedule: Fee Appraisers may not charge their VA clients more than the maximum allowable charge issued by the St. Paul VA. These fees fluctuate in accordance with the state of jurisdiction and the type of appraisal performed. VA fees are market driven, and we make every effort to analyze any market changes to conventional appraisal fees and adjust our fee schedule accordingly. Current fee schedules (as of September, 2012) broken down by state and appraisal type are provided in the St. Paul RLC website located at:

http://www.benefits.va.gov/homeloans/docs/stpaul_fee.pdf

2.4.2 Mileage Fees: In certain instances, VA appraisers are authorized to charge fees for

mileage. Current mileage rates can be found at the St. Paul RLC website and are set by GSA. Generally, mileage fees only apply outside of the appraiser’s home county for trips in excess of 75 miles roundtrip. The fee may only be charged on miles beyond the base 75 miles roundtrip. In addition, no mileage fees will be allowed within metropolitan areas as defined below. Appraisers are not required to travel throughout a metropolitan area, but if they choose to work in more than one county in a metropolitan area, no mileage fees can be charged in those counties.

Metropolitan counties in our jurisdiction are defined as follows:

Kansas City: Clay (MO), Jackson (MO), Platte (MO), Johnson (KS), Leavenworth (KS), Wyandotte (KS)

8

Saint Louis: St. Louis (MO), St. Charles (MO), Jefferson (MO), St. Clair (IL), Madison (IL)

Chicago: Cook, Du Page, Lake Minneapolis/ St. Paul: Hennepin, Ramsey, Anoka, Washington, Dakota, Scott Omaha: Douglas, Sarpy Milwaukee: Milwaukee, Waukesha, Racine, Washington and Ozaukee

2.4.3 Payment Policy: Appraisers must make the invoice the first page of the appraisal report package when uploading it into WebLGY. Fee Appraisers should always send a copy of the invoice to the broker and lender.

When a Notice of Value (NOV) is issued or when the requester receives notification from VA that a NOV will not be issued, the requester must send the appraiser his/her fee. An appraiser may not collect fees in advance from a requester unless the appraiser has a letter from VA authorizing advance payment from that requester. VA makes the determination whether the requester will be required to pay the Fee Appraiser in advance. Appraisers are not authorized to collect the fee from the Veteran, seller or anyone other than the requester. In rare cases where the requester is an individual, appraisers can request payment in advance without first contacting the VA. When an invoice has been outstanding for 90 days or more, appraisers may request assistance from our office in writing. Our office will intercede on the appraiser’s behalf. The appraiser must provide the following information:

VA Form 26‐1805

Invoice sent to the requester

Any contact information you might have

A written log of attempts to collect payment

Please e‐mail these items to: [email protected]

After our office has been asked to assist in collecting an unpaid fee, the appraiser must notify our office when the fee is collected.

9

3.1 Desk and Field Reviews of Appraisal Reports

Every appraisal report will be desk‐reviewed by a VA Lender Appraisal Processing (LAPP) Staff Appraiser Reviewer (SAR), by a VA Staff Appraiser, or both to verify that:

• The report was submitted timely

• That the Fee Appraiser’s conclusions of value are consistent, sound, supportable, and

logical

• The report was prepared in accordance with acceptable appraisal as well as specific VA

instructions. In addition, all appraisal reports are subject to field review by VA staff.

3.2 Quality Control and Standards

As previously stated, all appraisal reports are reviewed for both work quality and timeliness. Unacceptable quality or timeliness findings in any appraisal are classified as either Negative Work Quality Findings or Negative Timeliness Findings, or both. All Negative Work Quality Findings are further categorized, according to their significance, into ‘Substantive’ or ‘Non‐Substantive’ findings.

3.2.1 Substantive Error: A Substantive negative work quality finding will generally be assessed where VA has determined that the Fee Appraiser made a serious error of fact or methodology that materially impacts the appraised value or condition of the property. Examples include, but are not limited to:

• Fraudulent reporting (misrepresentation of a material fact in the appraisal)

• Appraising the wrong property

• Failing to require necessary MPR repairs that may result in damage to the Veteran

• Repeating or failing to correct non‐substantive errors after notification by VA

• Continued disregard for VA instructions or requirements after they have been called

to the Appraiser’s attention

• Errors affecting value by more than 5%.

NOTE: While VA is not a USPAP enforcement agency, suspected USPAP violations are subject to reporting to the appropriate State licensing authority for their investigation.

Chapter 3: VA Quality Control

10

3.2.2 Non‐Substantive Errors: A Non‐Substantive finding is generally one in which VA has determined that the Fee Appraiser made a relatively minor error of fact or methodology that did not impact the final value or the reported condition of the property. Examples include, but are not limited to:

• Failing to provide required information on the URAR (e.g., Remaining Economic Life, HOA dues on PUD appraisal)

• Misreporting of distances between subject and comps

• Inconsistency within the URAR (e.g., room count differs from page 1 to page 2)

• Failing to adequately describe reasoning in support of adjustments

• Using time adjustments not supported or documented

• Making insupportable or incorrect adjustments

3.3 Complaints

The VA Regional Office shall consider a lender’s valid report of complaint as a basis for administrative action. Administrative action shall be based upon a thorough VA review of:

The facts and evidence presented in support of the allegation(s)

Full consideration of any response provided by Fee Appraiser

The number of previous cumulative negative findings and/or complaints documented in the Fee Appraiser's performance folder

3.4 Summary of Deficiencies and Administrative Action

Documented negative timeliness or quality findings can form the basis for administrative action by VA against a Fee Appraiser. Additionally, an appraiser who exhibits chronically deficient customer service, as evidenced by documented unprofessional conduct or repeated complaint calls and letters from program participants, may also be subject to administrative action.

3.4.1 Summary of Deficiencies: The following summary of deficiencies is not all inclusive but is intended to supplement the examples given in the preceding section:

• Substantive violation(s) of established VA policies or procedures.

• Substantive negative work quality finding(s) of a nature that would materially or significantly impact the value or condition of the property.

• A series of non‐substantive negative work quality findings, which in the aggregate would establish a pattern of careless or negligent performance.

• Technical incompetence (i.e. appraisal reports which demonstrate insufficient knowledge of industry‐accepted principles, techniques, and practices).

11

• Improper conduct (i.e. conduct or behavior not befitting a professional and/or not in the best interest of VA or of VA program participants).

• Continued disregard for VA requirements after they have been called to the appraiser’s attention.

3.4.2 Administrative Actions: In instances where an appraiser chooses to disregard these guidelines, VA is mandated to take corrective action. VA has discretion to employ a wide variety of administrative actions as circumstances dictate. Some of these include the following:

• Withholding of Appraisal Assignments ‐‐ imposed by the Director of the Regional Office for a period of up to 60 days.

• Suspension ‐‐ imposed by the Department of Veterans Affairs for a minimum period of six months. After the suspension period is completed, the appraiser will automatically receive new assignments.

• Limited Denial of Participation (LDP) ‐‐ imposed by the Director of the Regional Office for a period of one year. After this period, the appraiser will be required to reapply to the VA panel, and if there is a need for additional appraisers, may be reinstated to the panel.

3.5 Disciplinary Due Process

Any Fee Appraiser receiving notification that significant administrative action is being taken, will be afforded the opportunity to appeal the action by requesting a meeting with the Fee Roster Committee at the Regional Loan Center in St. Paul. The Fee Roster Committee consists of the Loan Guaranty Officer, the Assistant Loan Guaranty Officer, and the Valuation Officer. Appellate rights and procedures will be explained in detail within the disciplinary action letter. If, after all due process and appellate procedures have been exercised, the disciplinary action is upheld, that Fee Appraiser is subject to having his or her name, and the reason for the disciplinary action, reported to the state licensing authorities and/or to any professional appraisal organizations of which the appraiser is a member.

12

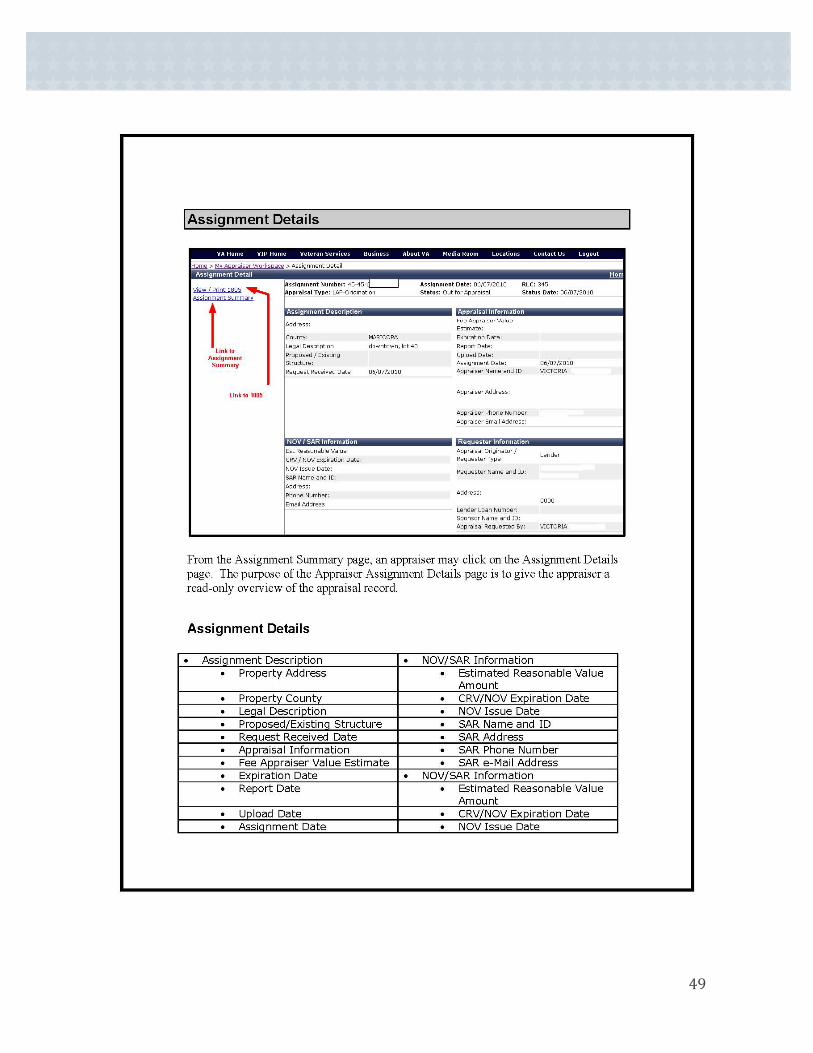

Veteran’s Information Portal Website The Veteran’s Information Portal is a web‐based application that provides links to integral applications pertaining to the VA home loan program. As stated earlier, Fee Appraisers are expected to use this system and its applications to check assignments and update personal information as well as to upload all appraisal assignments. The Veterans Information Portal can be located at:

https://vip.vba.va.gov

4.1 Registration

If you have never used the portal in the past, you will need to register. This is done by clicking on the “register” link at the top of the blue sidebar after accessing the site at the link above. Fill out all required information in the boxes provided, and then select “submit.” You must submit the four digit appraiser I.D. number assigned to you, and you must select St. Paul as your RO (Regional Office). The system will then assign you a password, which you can change at any time. Whenever you try to log in to the portal, you will be asked to provide your user name and password. Remember, your user name will always be your first name (dot) your last name in lower case (e.g. john.doe)

NOTE: If you forget your password, just under the username and password boxes is a lost password link. Please click on the link and follow the instructions. If you are locked out due to too many unsuccessful attempts (usually three (3) unsuccessful attempts), call 1‐800‐827‐0611 ext. 5421 or e‐mail [email protected] for assistance.

4.2 Appraisal Portlet

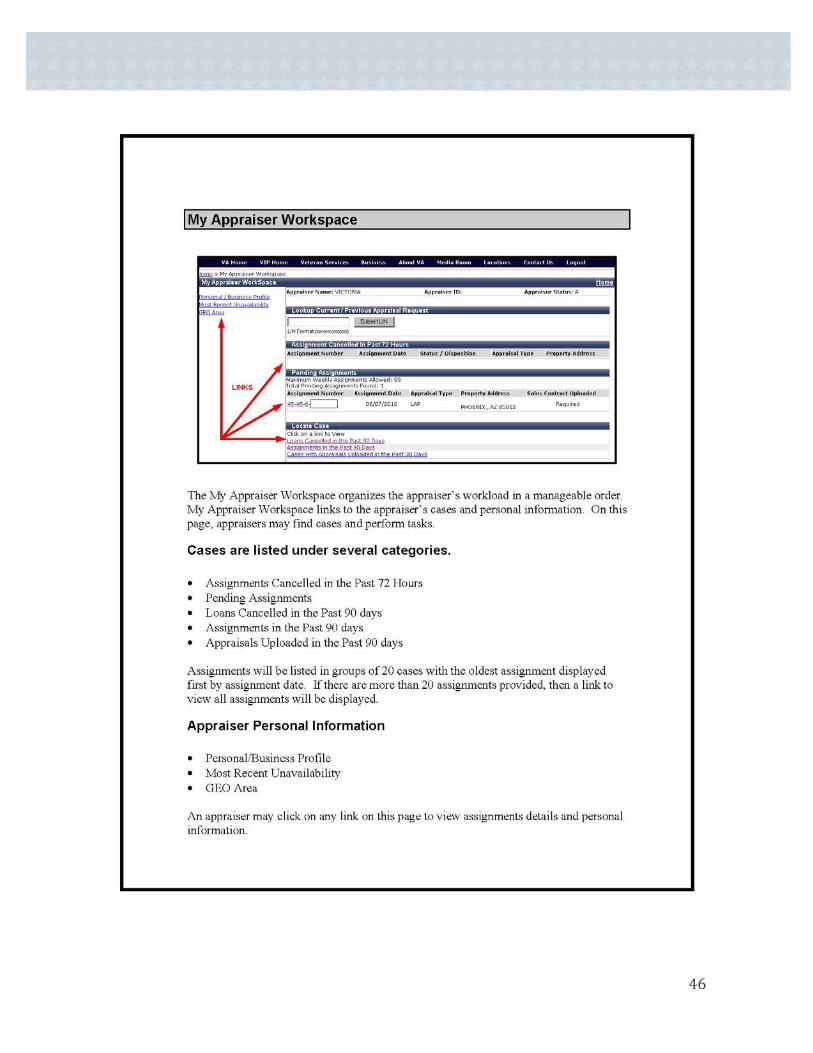

As previously stated, e‐appraisal functions have now been consolidated on the “Appraisal Portlet”. This system allows for the following functions:

• Check pending assignments • Find contact information of the requester • Check your availability status

Chapter 4: Veterans Information Portal (VIP) & WebLGY

13

• View and/or change your personal file (email, address, etc.) • Check your geographical area.

4.3 Assignment Procedures

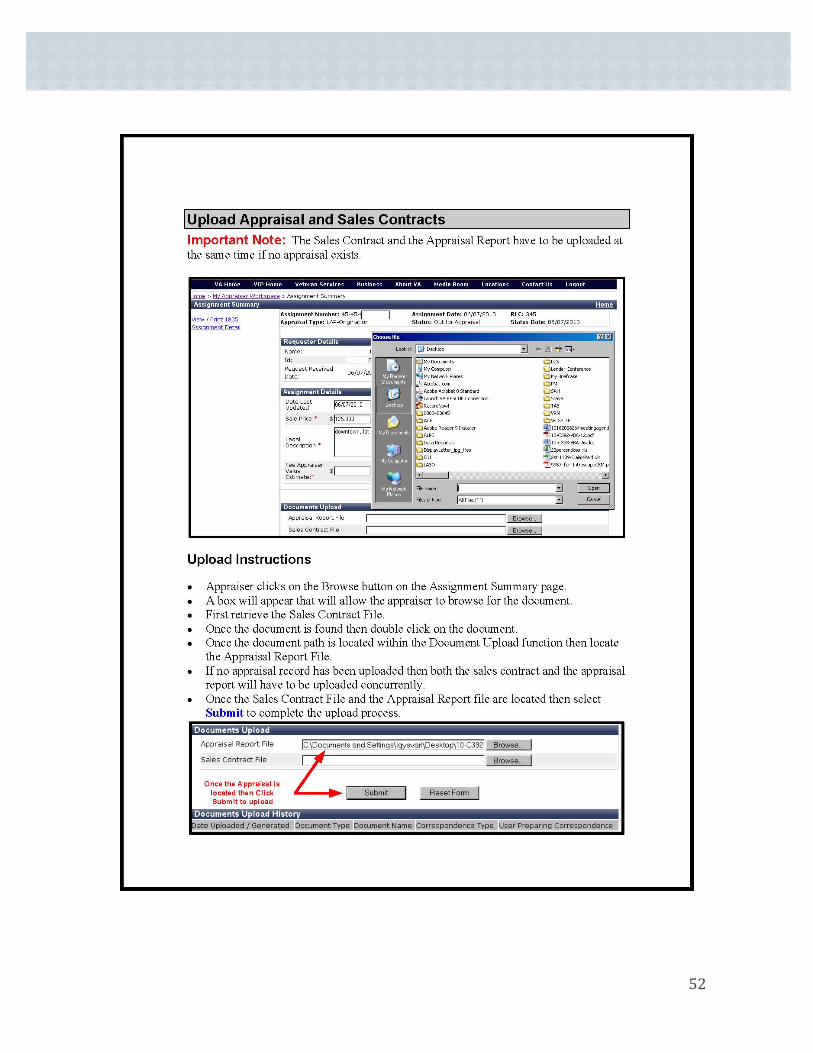

Lenders and other requesters order case numbers and appraisals in WebLGY, a function available in the Veteran’s Information Portal to lenders and VA personnel. The system assigns a Fee Appraiser for each case on a rotational basis according to geographic areas of coverage. All appraisers currently on the VA Fee Panel whose status is “Active and Available” are in the rotation and eligible to receive assignments. When the requester has entered all necessary information on the screen, a fully completed VA Form 26‐1805 (“Request for Determination of Reasonable Value”) is e‐mailed to you. The VA Form 26‐1805 will include the VA case number, along with access information and lender contact information. Appraisers must check their Appraisal Portlet on a regular basis for new assignments to ensure that a request is not missed. The 1805 can be viewed from the Appraisal Portlet and is considered a valid request in the event that an emailed 1805 was not received. If the appraisal is for a purchase transaction, the requester of a VA appraisal must also provide a copy of the agreement of sale and all addendums to the appraiser. The requester can either upload the agreement and additional addendums directly to the VA system, where the appraiser can access them, or e‐mail them to the appraiser. The assigned VA appraiser must analyze the agreement of sale and consider the analysis in establishing the fair market value of the property. Should the requester fail to provide the agreement of sale to the appraiser, the appraiser will, hold the assignment and notify VA and the requester of the delay (see VBA circular 26‐09‐3). Current VA policy holds the appraiser as being responsible for ensuring that the agreement of sale and all addendums are uploaded to the Appraisal Portlet.

4.4 Creating the PDF Appraisal Report

VA requires appraisals to be uploaded to WebLGY as a PDF file. The appraiser has the option of continuing to produce PDF appraisals by any acceptable method previously used for E‐Commerce purposes.

14

An appraisal report can be created as (or converted to) PDF format in three ways:

1) Use an appraisal software package that contains Adobe Acrobat 4.0 (or newer version) or PDF Publisher software to produce a .PDF file. Known supporting software includes:

• a la mode, Inc. (WinTotal 2000)

• Day One (Appraisal Manager)

• Polaroid (ACI/MCS)

• Software for R.E. Professionals (AppraiseIt)

• United Systems (HighPerform)

• Bradford Technologies (Appraiser’s Toolbox)

2) Use Adobe Acrobat 4.0 (or newer version ) or PDF Publisher to IMPORT a file created by another appraisal software package. Most appraisal software packages that do not produce a .PDF (dot PDF) extension will instead produce one of the following file extensions, all of which can be imported:

.GIV .JPEG .TIF

.TIFF .PCX .PNG

.BMP .PICT (for Macintosh PCs)

3) Use Adobe Acrobat 4.0 (or newer version *) or PDF Publisher to SCAN an appraisal report into a VA PDF file template.

• The template can be obtained from VA. • This template is a one‐page .PDF file. • The appraiser inputs the required 14 fields in the template (e.g. property

address, city...) • The Fee Appraiser then scans in the appraisal report (this makes pages 2, 3, 4, 5,

6, etc. of the PDF template file) • The appraiser uploads the .PDF appraisal to E‐Appraisal

4.5 Uploading Appraisal Reports

Please note that ALL appraisal reports must be uploaded to this system, including LAPP appraisals. As stated earlier, it is allowable to email, fax, or mail reports to lenders. However, the report must still be uploaded to the Appraisal Portlet to allow for field and desk review of the appraisal by VA staff. Prior to uploading the appraisal report you must first ensure that the report is in PDF format and is named correctly. All reports should be named starting with the VA case number (dot) pdf. (for example, 35‐35‐6‐0999999.pdf)

15

Please review Appendix 1 for detailed guidance on using the Appraisal Portlet and uploading appraisal reports and real estate contracts.

4.6 VIP Portal Problems

If you are experiencing problems with any applications associated with the VIP Portal, contact the VA technical support email for assistance at [email protected].

16

5.1 The Role of the LAPP Staff Appraiser Reviewer (SAR)

Generally, the LAPP SAR must ensure that:

• the URAR and all required attachments and addendums are complete and correct

• the appraiser's methodology is appropriate and reasonable and that conclusions are consistent with data

• the appraiser has complied with current VA instructions

• the appraiser’s market value is consistent with the current standard definition of market value and VA’s regulatory definition of reasonable value.

5.2 Contact and Cooperation with the LAPP SAR

LAPP SARs are expected to take reasonable steps to resolve problems detected during their appraisal reviews. While branch office staff and authorized agents may contact the Fee Appraiser about the timeliness or status of a particular appraisal, only the LAPP lender’s VA‐authorized Staff Appraisal Reviewer (SAR) may contact the Fee Appraiser to discuss valuation matters. LAPP SARs should contact VA Fee Appraisers directly when any information, or methodology, or conclusion contained in an appraisal report requires clarification, correction, or additional support in order for the SAR to make a prudent decision on the reasonableness of the Fee Appraiser’s market value estimate.

VA Fee Appraisers are expected to be cooperative with lenders and SARs in addressing their concerns regarding the content of appraisal reports or timeliness in the completion of their assignments. SARs are expected to take reasonable steps to mitigate difficulties encountered with an appraiser's report. VA should not be considered a referee between the lender and Fee Appraiser in resolving routine issues.

In any case where the SAR determines that substantive problems with the Fee Appraiser's report are not correctable through reasonable interaction with the appraiser, the lender will forward the original appraisal report to the C&V Section at the St. Paul Regional Loan Center. The lender’s submission will include a written report clearly outlining the difficulties

Chapter 5: Communication with LAPP Staff Appraisal Reviewers (SARs)

17

encountered, with the date and outcome of each contact made with the Fee Appraiser. This will assist VA in monitoring Fee Appraiser performance and determining what, if any, administrative action may be warranted.

NOTE: Any revisions, corrections, or clarifications made by a Fee Appraiser to the appraisal report must be uploaded to the Appraisal Portlet. Any case in which VA determines that relevant appraisal documentation has been withheld, will constitute an unacceptable act and may be considered a basis for administrative action against the lender, the Fee Appraiser, or both.

5.3 Tidewater Initiative

The Tidewater procedure allows an opportunity for a designated “Point of Contact” (POC) (typically the POC shown on the VA Form 1805) to provide market evidence for the appraiser’s consideration prior to establishing the final URAR value. The appraiser initiates the procedure by alerting the contact person that the appraised value appears to come in under the sales price. The appraiser should not discuss the appraisal contents except to explain that the comparable sales located by the appraiser do not adequately support the sales price. The contact person then has two business days to provide additional sales information in support of the sales price. Verification of all closed sales is required (pending sales may be offered, but can only be used as additional support). All attempts to communicate with the designated Point of Contact must be documented in the appraisal report to show the date of the attempt, the party’s name and phone number, and whether or not additional information was provided.

5.4 LAPP Reconsiderations of Value

Specific and detailed instructions for handling LAPP reconsiderations of value are provided in Chapter 13 of the revised Lenders Handbook, Section 13.09. This includes the roles and responsibilities of the LAPP lender, the Fee Appraiser, and VA.

5.5 Servicer Appraisal Processing Program Staff Appraiser Reviewer (SAPP SAR)

An appraisal request designated as a SAPP is a liquidation appraisal where the lender or servicer’s Staff Appraisal Reviewer (SAR) reviews the appraisal. All items in this chapter refer to both the LAPP and SAPP SAR.

18

6.1 Properties Not Eligible For VA Guaranty & Appraisal

Properties in the following situations should not be appraised:

Property is in badly deteriorated condition unless VA agrees that there is reasonable likelihood that it can be repaired to meet VA MPRs.

Proposed construction/under/ new construction in a flood zone with elevation of the lowest floor below the 100 year flood level.

Properties located in a flood zone where flood insurance is not available.

Properties in an area subject to regular flooding (whether or not it’s in a flood zone).

Properties in a Coastal Barrier Resources System (CBRS) area (Appraisers are

responsible for obtaining maps from the U. S. Geological Survey and checking the location of properties).

Proposed/under construction in a Clear Zone or in Airport Noise Zone 3 (unless VA

accepted the project before the Noise Zone 3 contour was changed to include it). Airport Noise Zones are discussed in Chapter 10.

Any part of the residential structure is or is to be located within a transmission line easement for high‐pressure gas, liquid petroleum, or high‐voltage electricity.

Proposed/under/new construction in an area susceptible to geological or soil instability unless the builder has provided evidence that the site is not affected or the problem has been adequately addressed in the engineering design.

Less than fee simple ownership (for example: leasehold, cooperative, ground rental

arrangement) without prior approval of VA Central Office (contact our office for more information).

A condominium that has not yet been approved by the VA.

Nonresidential use exceeding 25% of total floor area or impairing the residential

character of the property. If the appraiser determines that the area exceeds 25%, the appraiser must submit a dimensioned sketch of the subject property showing the nonresidential area and may charge a fee proportional to the amount of work completed. Please call our office if needed for guidance on appraisals of properties with commercial zoning.

Chapter 6: VA Appraisal Requirements

19

6.2 USPAP

Every VA appraisal must meet the Uniform Standards of Professional Appraisal Practice (USPAP) requirements for a complete appraisal, but may be issued as either a self‐contained Appraisal Report or a Summary Appraisal Report. There are potential exceptions:

• VA prior approval is required prior to performing a “restricted” appraisal.

• With the exception of liquidation appraisal updates, VA prior approval is required for any case in which the USPAP departure rule is used.

6.3 Scope VA Appraisal Assignments

VA requires a determination of "reasonable value" or "market value" and not "liquidation or investor value" for all loan origination appraisal assignments. As such, distressed sales and REO sales should not be used as comparable sales unless they truly represent the current market. Sufficient justification for the use of REO sales must be provided in the appraisal report.

The determination of when to use distressed sales is up to the appraiser's judgment. The appraiser must, however, clearly indicate and support why the use of distressed sales was required within the appraisal report. Several tests will be employed and addressed in the report such as:

What is the amount and degree of repairs needed? Will a "typical" buyer consider this property as an alternative to other listings? Will traditional lenders be willing to make a loan on the property in its "as is" condition

without a significant reserve account for repairs? Are REO sales and forced sales the only sales (or the predominant sales) in this market?

These four keys would dictate whether the value sought was "market value" for a typical buyer or "market value" for an investor who is knowledgeable about this type of market and property. For every appraisal where distressed sales are used, the appraiser will estimate, and report, the concentrations of distressed sales within the subject's market; (e.g., Total number of Sales, number of REO Sales, Short Sales, and percentage of total Distressed Sales against the Total number of Sales). Additionally, REO/Short sales used as comparable sales in a report must be justified by the market and explained in the report, and the sales must be verified by a party to the transaction (seller and/or buyer) to ascertain the motives of the parties involved. Reliance on MLS or assessor data is NOT sufficient. For VA loan guaranty purposes, the “reasonable value” of a property is that figure which represents the amount a reputable and qualified appraiser, unaffected by personal interest, bias, or prejudice, would recommend to a prospective purchaser as a proper price or cost in

20

the light of prevailing conditions. VA considers reasonable value and market value to be synonymous. VA’s definition of market value is consistent with that used by Fannie Mae, Freddie Mac and major appraisal organizations.

The VA Fee Panel Appraiser must personally

• View the interior and exterior of the subject (except on liquidation cases in which entry is not possible) and the exterior of each comparable

• Select and analyze the comparable sales

• Make the final value estimate, and

• Sign the appraisal report as the appraiser

The Fee Appraiser is expected to take sufficient time to observe all aspects of the property. The Fee Appraiser must view every room in the interior and all easily accessible spaces such as the attic, crawl space, basement, garage and storage spaces. The Fee Appraiser is expected call for repairs of any VA Minimum Property Requirements (MPR’s) deficiencies noted in the property inspection. The Fee Appraiser is not expected to climb onto the roof. The Fee Appraiser is not expected to perform operational checks of mechanical equipment. However, if the appraiser notices that any equipment appears to be broken, he/she should note the defect in the report. The appraiser should not recommend repairs, which are cosmetic in nature, nice to have, or reflect personal tastes. The appraiser should not require certifications or inspections for roofing, plumbing, heating or air conditioning unless there is a documented reason for such inspections (i.e., less than two years estimated remaining life of the roof or evidence of roof failure). Appraisers must not require inspections for liability protection. The appraiser should require corrective action by licensed personnel if the condition does not appear to be safe, sound or sanitary; or require nothing if the condition appears satisfactory. The Fee Appraiser must provide a specific list of repairs needed for the subject to meet VA’s minimum property requirements in the improvements section on page 1 of the URAR or on an addendum that is referenced in the improvements section on page 1. For example, the appraiser should list “replace broken window in kitchen” instead of saying “kitchen window is broken.” Every VA appraisal report must be reported using one of the following forms as appropriate:

• Uniform Residential Appraisal Report (URAR), Freddie Mac Form 70/Fannie Mae Form 1004, if the property is a single‐family residence, not a manufactured home or a unit in a condominium.

21

• Manufactured Home Appraisal Report, Freddie Mac Form 70B/Fannie Mae Form 1004C, if the property is a single‐family manufactured home.

• Individual Condominium Unit Appraisal Report, Freddie Mac Form 465/Fannie Mae Form 1073, if the property is a condominium unit.

• Small Residential Income Property Appraisal Report, Freddie Mac Form 72/Fannie Mae Form 1025, if the property has two to four living units.

• Exterior‐Only Inspection Residential Appraisal Report, Freddie Mac Form 2055/Fannie Mae Form 2055, for liquidation appraisals (only), when interior access cannot be obtained (see section 13 of this chapter).

• Exterior‐Only Inspection Individual Condominium Appraisal Report Freddie Mac 466/Fannie Mae 1075, for liquidation appraisals (only), when interior access cannot be obtained (see section 13 of this chapter).

• Exterior‐Only Individual Cooperative Interest Appraisal Report, Fannie Mae 2095 for liquidation appraisals (only), when interior access cannot be obtained (see section 13 of this chapter).

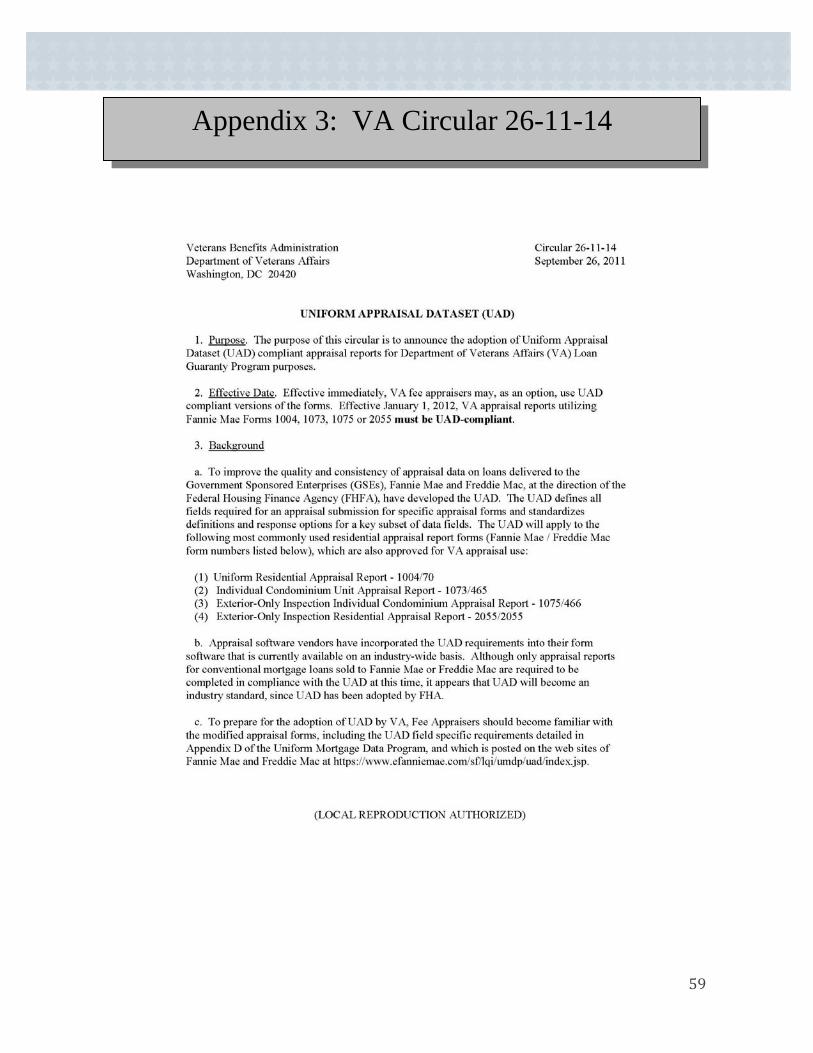

Uniform Appraisal Dataset (UAD) Appraisals: Effective January 1, 2012, VA appraisal reports utilizing Fannie Mae Forms 1004, 1073, 1075 or 2055 must be UAD‐compliant. (See Appendix 3) UAD compliant reports must include an addendum explaining and/or defining the codes used for Quality/Conditions and UAD abbreviations.

Every VA Appraisal report must include:

• Location map clearly showing the location of the subject and each comparable.

• Floor plan sketch showing room layout, exterior dimensions, exterior decks, porches and patios, and square footage calculations (s/f calculations must be on the floor plan or on page 3 of the URAR in cost approach comments)

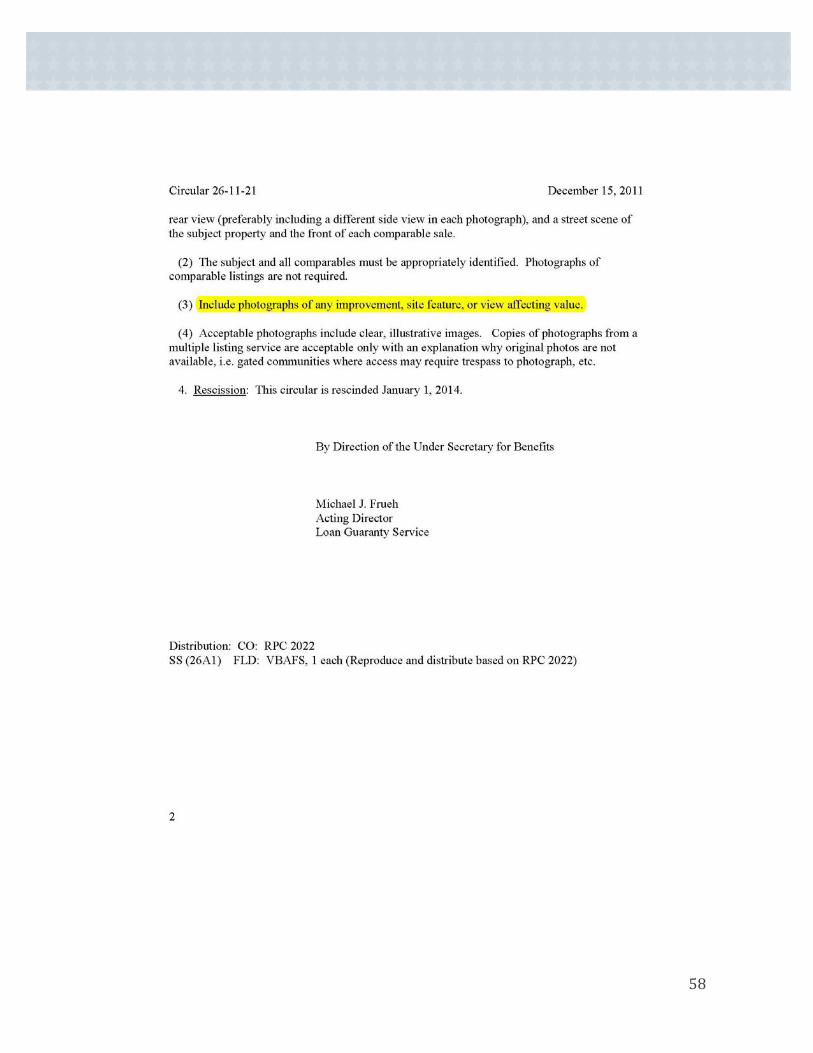

• Photographs (see appendix 2) must include:

a front and rear photo of the subject property

a street scene picture

the kitchen

all bathrooms

main living area

examples of physical deterioration if present

examples of recent updates, such as restoration, remodeling, and renovation, if present

a photo of all comparable sales from the street

22

• Invoice – a copy of the appraisal invoice should be included preceding the report and should be first page when uploading into WebLGY. If applicable, mileage fees will be listed separately on the invoice.

• Any additional appraisal or repair‐related information needed to support the Fee Appraiser’s conclusions.

• Fannie Mae Market Conditions Addendum, Form 1004MC.

• Conform to the provisions of USPAP and VA appraisal requirements.

• A statement regarding the prevalence of sales concessions in the subject’s market area and, if concessions are prevalent, the typical concession seen.

• The following Certification ‐ “I have considered competitive listings and/or contract offerings in performing this appraisal, and any trend indicated by that data is supported by the listing/offering information included in this report.”

• A properly completed Statement of Limiting Conditions and Appraiser’s Certification, Freddie Mac Form 439/Fannie Mae Form 1004B.

• Explanations for all large or unusual adjustments.

• Every proposed construction appraisal must include the following certification;

“I hereby certify that the information contained in (specific identification of all construction exhibits (e.g., Smith Construction Plan Type A, 9 sheets, VA Form 26‐1852, plot plan by Jones, Inc.)) was used to arrive at the estimate of reasonable value noted in this report. __(appraiser’s signature)___”

• The Remaining Economic Life of the subject property.

6.5 Approaches to Value

6.5.1 Sales Comparison Approach:

For most VA appraisals, this approach will be your primary, if not exclusive, indicator of final value. Key points to keep in mind: At least three confirmed closed sales of comparable properties must be utilized. Ideally,

the comparable sales should bracket the subject’s Gross Living Area (GLA) and estimate of value. If the sales do not bracket the value conclusion, a supporting explanation and additional closed sales, pending sales, or listing data are required. If comparable sales are located at excessive distances from the subject or market area boundaries, their use in the Sales Comparison Approach must be justified and explained. Typically a comment should be made if comparable sales are located over one mile from the subject.

23

When the market is declining or increasing, and additional support for a time adjustment if warranted is required. We recommend that you include a fourth comp that can be a pending sale where you have verified the sale price with the selling agent. Selection of Comparable Sales: The appraiser must select the three best, and most recent, comparable sales available and properly adjust the sales price of each one for differences between it and the subject property. The goal is for the VA value estimate to not exceed the price at which similar properties can be purchased in the current market. The appraiser must adequately explain any reliance on sales that are not truly comparable to the subject. In determining what constitutes a truly comparable property, the appraiser often relies on experience and judgment rather then a set of procedures. Following are the Five Keys to Comparability to be considered as a guide when considering a comparable sale:

1. Market Area: Brokers often speak of "location, location, location" as the key to determining a property's value. While this may serve brokers well, an appraiser should view it from a market area perspective that includes much more than its physical location. These would include physical, economic and legal aspects of the area and the subject property. Having the necessary geographic competency is of primary importance since, in many markets, the house around the corner may not have the same characteristics as the subject property. 2. Style: To the extent possible, compare similar or the same style homes. A ranch style home does not have the same utility as a two‐story colonial. A clear

understanding of the demands of market participants is important. This should be accomplished by research and communications with buyers, sellers and brokers on an ongoing basis. Market tastes and standards are constantly changing. 3. Age (Construction Era): Different eras in our country's history brought different construction methods and techniques. In today's construction, many components are "pre‐manufactured" and brought to the site. Most are now engineered truss systems. It has been estimated that in California nearly 90% of all homes were built after 1960. An "old" house then would be one that is 50 or 60 years old. On the east coast however it is not unusual to find a home that is over 200 years old and everything in between.

24

Having a working knowledge of basic home construction is necessary. Having a working knowledge of different methods used in various construction eras is critical in proper analyses. 4. Square Footage or Size: Appraisers often use square footage as a basis for beginning a comparable sale search. This is one feature that tends to lend itself to direct comparison. All things being equal, if all ranches on slabs in a particular market sold in the past six months between $120‐$125 per square foot of GLA (land and building merged) the final value indication of the subject should fall within that range of values. 5. Other Features: This would include features such as basements, porches, decks and others. These features should be relevant features, not merely adjustments for adjustment's sake. A five‐car detached garage may add considerable value, depending on the market. If this is the case, then an appraiser should use at least one comparable with a similar garage, to demonstrate marketability and value. But not all features are important to value. Explanations should be provided if an amenity exists that does not add market value to the subject.

6.5.2 Income Approach:

If the appraisal involves an income‐producing property (more than one living unit), the appraiser will use value estimates developed through the income approach, including the rental comparison grid, and the sales comparison approach in the final reconciliation.

Note that for VA purposes, a Veteran may purchase a dwelling of up to four living units, so long as he or she occupies one of the units. In valuing such properties, consideration must be given to the income‐producing potential of the remaining unit(s).

6.5.3 Cost Approach:

With the exception of a Remaining Economic Life, you are not required to provide the cost approach to value on any existing VA appraisal. However, a properly developed cost approach can provide additional support to the value conclusion of sales comparison approach. This is warranted in rare situations where the comparable sales analysis alone does not provide an adequate indication of value. The cost approach should be considered in all new and proposed construction appraisal assignments as additional support.

25

Similarly, the cost approach should be given serious consideration in appraising residences that are less than 20 years old to provide additional support to the sales comparison analysis.

6.6 USPAP Guidance

USPAP Standards Rule 1‐1 states that – "In developing a real property appraisal, an appraiser must: (a) be aware of, understand, and correctly employ those recognized methods and techniques that are necessary to produce a credible appraisal". USPAP Standards Rule 2‐2b further states that –

"The content of a Summary Appraisal Report must be consistent with the intended use of the appraisal and, at a minimum: (viii) summarize the information analyzed, the appraisal methods and techniques employed, and the reasoning that supports the analysis, opinions, and conclusions; exclusion of the sales comparison approach, cost approach, or income approach must be explained."

While VA does not require the development of an income approach or the cost approach for single family properties unless they are applicable to the appraisal. It is therefore a responsibility of the appraiser, per USPAP, to explain the exclusion of any approached to value not developed. The appraiser cannot simply state that the VA does not require the excluded approach.

6.7 Market Analysis

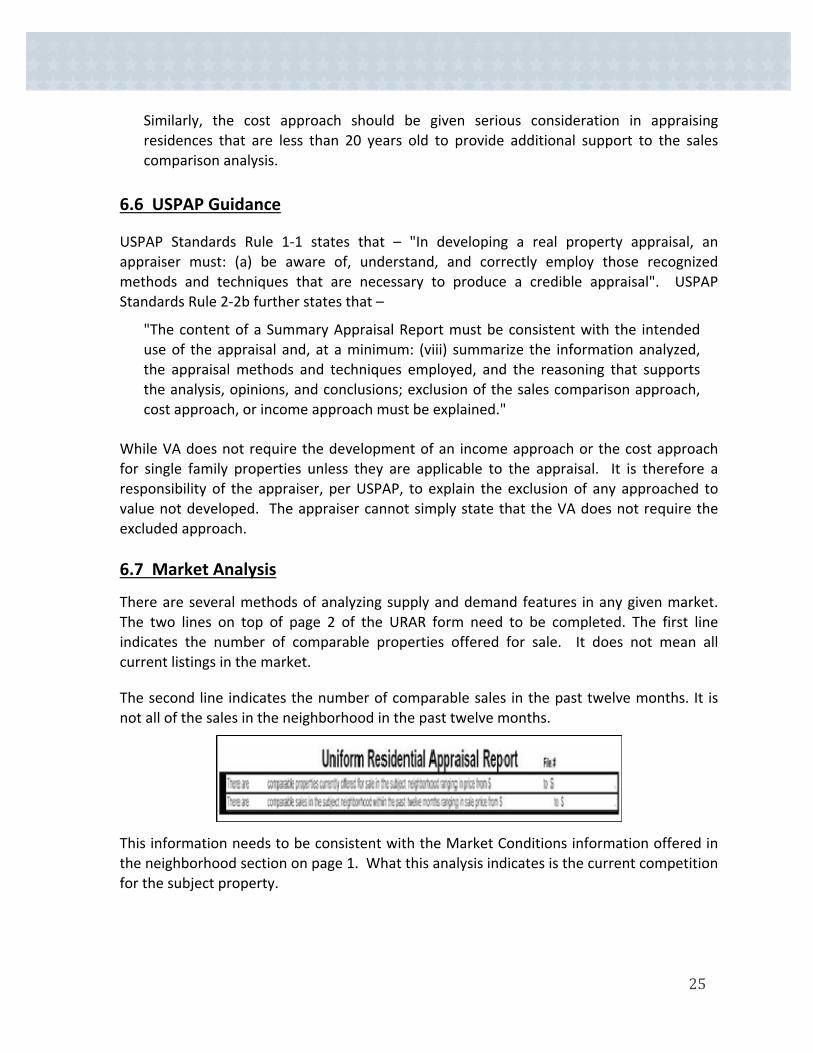

There are several methods of analyzing supply and demand features in any given market. The two lines on top of page 2 of the URAR form need to be completed. The first line indicates the number of comparable properties offered for sale. It does not mean all current listings in the market.

The second line indicates the number of comparable sales in the past twelve months. It is not all of the sales in the neighborhood in the past twelve months.

This information needs to be consistent with the Market Conditions information offered in the neighborhood section on page 1. What this analysis indicates is the current competition for the subject property.

26

6.7.1 Market Conditions Addendum ‐ Form 1004MC: The Form 1004MC is intended to provide the lender with a clear and accurate understanding of the market trends and conditions prevalent in the subject neighborhood. The form provides the appraiser with a structured format to report the data and to more easily identify current market trends and conditions.

VA, and Fannie Mae, recognize that all of the requested data elements for analysis are not equally available in all markets. In some markets it may not be possible to retrieve the total number of comparable active listings from earlier periods. If this is the case, the appraiser must explain the attempt to obtain such information. Also there may be markets in which the data is available in terms of an “average” as opposed to a “median.” In this case, the appraiser needs to note that his or her analysis has been based on an “average” representation of the data. Regardless of whether all requested information is available, the appraiser must provide support for his or her conclusions regarding market trends and conditions.

If there is not enough data to present a meaningful analysis, the appraiser must complete the form with the information he or she has for the defined neighborhood or market; the lack of data may speak to what is occurring in that area. In the absence of MLS data, appraisers are expected to analyze and report on data drawn for their own files to support their conclusions. Simply indicating N/A in all the data entry sections and then stating that there is ‘insufficient data available to produce a meaningful report’ is not acceptable. While data for the subject’s neighborhood may be limited, an analysis of a broader regional market can provide the reader of the report with an acceptable understanding of existing market trends for the subject property. In these cases, the data may not always directly correlate between the 1004MC Form and the conclusions shown on Page 1 of the report. Any differences or discrepancies must be addressed in the report. Regardless of whether all requested information is available, appraisers must provide support for their conclusions regarding market trends and conditions as noted in the Neighborhood Section of the appraisal report. Stating that the conclusions are based on the ‘appraisers knowledge of the local market’ is insufficient to meet this requirement. Here’s a five‐step process that may be helpful when preparing the 1004MC.

• Define the neighborhood boundaries, resisting the temptation to artificially expand them.

• Identify comparable sales and listings within the neighborhood.

• Categorize comparable neighborhood sales and listings by date and complete gridded sections of the form

27

• Determine if sufficient data exists within the neighborhood to enable development of a meaningful market analysis.

• If data is insufficient, develop a broader‐based analysis using data from competing areas and report the analysis in the summary section of the 1004MC or as an addendum.

Inventory Analysis Section

The “Inventory Analysis” section assists the appraiser in analyzing important supply and demand factors in order to reach a conclusion regarding housing trends and market conditions. When completing this section, the appraiser must include the comparable data that reflects the total pool of comparable properties from which a buyer may select a property in order to analyze the sales activity and the local housing supply.

Median Sale & List Price, DOM, List/Sale Ratio Section

The appraiser must analyze additional trends, including the changes in median prices and days on the market (DOM) for both sales and listings as well as a change in list‐to‐sales price ratios.

Overall Trend Section

The “Overall Trend” section is designed to reflect potential positive trends, neutral trends, or negative trends in inventory, median sale and list price, days on market, list‐to‐ sale price ratio, and seller concessions. Seller Concessions

Form 1004MC also provides a section for comments on the prevalence of seller concessions and the trend in seller concessions for the past 12 months. The change in seller concessions within the market provides the lender with additional insight into current market conditions. The appraiser should consider and report on seller‐paid (or third‐party) costs. Seller concessions must be carefully analyzed by the appraiser since excessive concessions often lead to inflated property values.

There are a number of markets across the country where, due to current conditions, there has been an increase in the prevalence of seller concessions. The following excerpt from the Selling Guide, Part XI, Section 406.5 (C) provides guidance for these circumstances:

“The need to make negative dollar adjustments for sales and financing concessions and the amount of the adjustments to the comparable sales are not based on how typical the concessions might be for a segment of the market area; large sales concessions can be relatively typical in a particular segment of the market and still result in sale prices that reflect more than the value of the real estate. Adjustments based on dollar‐for‐dollar deductions that are equal to the

28

cost of the concessions to the seller (as a strict cash equivalency approach would dictate) are not appropriate. We recognize that the effect of the sales concessions on sales prices can vary with the amount of the concessions and differences in various markets. The adjustments must reflect the difference between what the comparable sales actually sold for with the sales concessions and what they would have sold for without the concessions so that the dollar amount of the adjustments will approximate the reaction of the market to the concessions.”

Foreclosure Sales and Summary/Analysis of Data

The presence and extent of foreclosure/REO sales is worthy of comment when analyzing market data and must be reported on the form. The form also allows the appraiser to summarize the data and provide other data analysis or additional information, such as analysis of pending sales, which over time can show a market trend.

6.8 Completing the Uniform Residential Appraisal Report (URAR)

The URAR should be completed fully, in accordance with the following instructions and guidelines. Not all areas of URAR are mentioned below, be sure to complete all items of the URAR; do not leave any item blank. Indicate N/A if not applicable. Do not use phrases such as “in lender’s file” or “see prelim.” The appraisal should contain the VA case number, preferably at the top right corner of all pages on the report. It also must list both the lender and the Department of Veteran Affairs as the lender/client. This can be abbreviated to DVA if needed. The report must be signed and dated. Provide your VA Appraiser number next to your signature. Provide your State Certification or License number in the space indicated. Be sure to include sufficient commentary regarding the sales comparison approach, adjustments made, and anything unusual about the subject or the comparable sales.

29

7.1 OVERVIEW

Require only those repairs needed to make the property conform to VA Minimum Property Requirements (MPR’s). Cosmetic repairs are not required, so consider them in the overall condition rating and valuation of the property. In Existing Construction, the most common MPR repairs are for maintenance needed to prevent "continued deterioration of the improvements", such as deteriorated exterior walls and trim, roof leaks, damp basements, water in crawl space, and exterior painting required due to the effect of the soundness to the subject or if the property was built prior to 1978. Interior painting is typically only required if paint is chipping/flaking and the subject was built prior to 1978. Typical safety items include missing handrails, porch/deck rails and safety bars (for sliding glass doors). Typical sanitary problems include defective septic systems, water in the crawl space and plumbing leaks. A property is ineligible for appraisal (for new VA loan) if you consider the repairs to be so extensive that the property likely cannot be corrected to meet MPR’s. Call us for guidance if necessary; otherwise reject the property and notify the lender. For Specific VA Requirements regarding Basic MPR’s, variations, exemptions, shared facilities and utilities, access related issues, hazards and defective conditions, fuel pipelines, high voltage electric lines, and water supply/sewage disposal requirements, please refer to

the Lender’s Handbook chapter 12.

7.2 WHAT IS EXPECTED OF THE FEE APPRAISER

The Fee Appraiser is expected to take sufficient time to observe all aspects of the property. The Fee Appraiser must view every room in the interior and all easily accessible spaces such as the attic, crawl space (the VA does require all crawl spaces be accessible), basement, garage and storage spaces. The Fee Appraiser is not expected to climb onto the roof. The Fee Appraiser is not expected to perform operational checks of mechanical equipment. However, if the appraiser notices that any equipment is broken, he/she should require that the item be repaired.

Chapter 7: Minimum Property Requirements (MPR)

30

The appraiser should not require certifications or inspections (e.g., roofing, plumbing, heating or air conditioning) for liability protection. The appraiser should require corrective action by licensed personnel if the condition does not appear to be safe, sound or sanitary; or require nothing if the condition appears satisfactory.

7.3 REPAIR ITEMS REQUIRING SPECIAL ATTENTION

The following repair items require special attention ‐

• The roof must provide reasonable future utility, durability and economy of maintenance. The appraiser should make this determination from his/her professional experience. Appraisers should never require a roof inspection unless there is evidence that the roof has failed or the roof has less than a two (2) year estimated remaining economic life.

• If the roof does not appear to have an adequate remaining life, the appraiser should complete the appraisal subject to installation of a new roof by a licensed roofer.

• If a small area of the roof is damaged and the appraiser believes it could be repaired without replacing the entire roof, the appraiser may require that the roof be repaired by a licensed roofer instead of bring replaced.