Valuation of Catastrophe Reinsurance Contract with Considering Equity

Depression-The application of Hybrid CAT Bond Issuing

Chih-Chen Hsu* Juei-Hsiang Chen

Abstract

This study develops a contingent claim framework designed to evaluate

reinsurance contracts of proposed-hybrid catastrophe (CAT) bond to scrutinize

reinsurance companies as to how they reduce default risk and increase reinsurance

contract value by issuing hybrid CAT bonds. Pauline and Henri (2009) proposed the

concept of hybrid instruments. The study alone with this concept to design and to

price a variation of hybrid catastrophe bond that combines CAT bond with a

catastrophe equity put option. Such a bond possesses instrument characteristics of pre-

and post-loss financing that will better provide channels for risk transfer. Results

showed that changes, basis risks, trigger levels, and catastrophe risks inherent in

reinsurance contract and default risk premium value are related to the initial capital

structure of the reinsurance company. Under the premise that instruments are set the

same, even with the consideration of basis risk, the issuing of hybrid CAT bonds is

comparable to that of CAT bonds in that it can further reduce default risk premium

and increase reinsurance contract value.

Keywords: Contingent framework, Hybrid CAT Bond, Reinsurance contract

JEL Classification: C15, C73, G12, G22

Hsu: Assistant Professor of Finance, National Chung Cheng University, Cha-Yi 62100, Taiwan(R.O.C.), Email:

[email protected] . Chen: Mater student of Finance department, National Chung Cheng University, Cha-Yi

62100, Taiwan(R.O.C.), Email: [email protected] . Corresponding author: Chih-Chen Hsu.

2

1. Introduction

Significant losses from catastrophic events in recent years pose a serious threat to

reinsurance companies, resulting in problems of increasing liability and capital

shortage. The cause of such problems is mainly due to the increase in the frequency of

catastrophic events and the mounting losses these events incurred. They lead to

problems of insufficient collection of reinsurance premiums or lack of sufficient risk

aversion by the insurance companies. At this time, reinsurance companies are fully

exposed to this type of catastrophe risk. Therefore, how to reduce reinsurance

company exposure to the impact of this type of catastrophe risk, and how to further

enhance the value of reinsurance contract, will be the subject of this study.

Catastrophic events are low-frequency high-loss by nature, resulting in not only

economic but also human casualties. In recent years, natural catastrophes (hurricanes,

floods, earthquakes, and tsunamis) have been intensely reported by the news media.

Events such as the Indonesian tsunami in 2004, Hurricane Katrina in 2005, and

311-earthquake in Japan in 2011 have all resulted in serious human casualties and

economic losses in their respective countries. Outcomes that accompany a catastrophe

incident are often unknown, and the amount of compensation is uncertain, thus

catastrophe events are difficult to predict.

Traditionally, property insurance companies, in their attempt to avoid

responsibility for huge losses caused by catastrophic events that can lead to a default,

often transfer these catastrophe risks by purchasing reinsurance contracts from

reinsurance companies. According to property and casualty insurance companies, the

actual size of claims may cover all or part of a loss. This type of contract can enable a

property and casualty insurance company, when faced with huge catastrophe loss

claims, to obtain additional capital injections, thereby transfer these catastrophe risks

the property insurance company has to face. The theory, however, from regional or

national perspective, catastrophe events represent systemic risk. The financial impact

of catastrophes can be dispersed by the existing international reinsurance market,

which does not need to issue any catastrophe link securities. Yet, the development of

the market does not follow that, which is expected from Pauline and Henri (2009). In

recent years, a single catastrophic event (earthquake or typhoon) can result in 50 to

100 billion dollars of damage. The amount of catastrophe loss at this level can put a

huge pressure on the underwriting capacity of the entire insurance industry, and poses

a serious threat to the credit risk of many reinsurance companies (Cummins, et al,

2002). Once the catastrophic event has occurred, reinsurance companies must fulfill

compensation obligations under the terms of reinsurance contract, which will

immediately increase their liabilities (Duan and Yu, 2005), causing the likelihood that

3

these reinsurance companies have insufficient capital on hand to withstand a

catastrophic event of such a magnitude. If a certain number of market participants

were to withdraw from the market until after the injection of new capital, then this

type of catastrophe risk can be transferred. Recent reinsurance market research

showed that, due to the limited capacity of international reinsurance market, the needs

of insurance market are no longer being fulfilled (Froot, 1999 and 2001; Harrington

and Niehaus, 2003).

However, catastrophic events represent negative news. In an efficient market,

stocks will instantly reflect the operating conditions of reinsurance companies, and

catastrophic events that cause the loss of equity value of reinsurance companies will

cause their stock price to immediately fall. Studies mentioned in literature that were

done by Sprecher and Pertl (1983), and Davidson, Chandy, and Cross (1987), on the

impact of catastrophe events on stock price of insurance companies, showed that there

is a negative correlation between the value of these companies and the magnitude of

the losses. Reilly and Drzycimski (1973) found that major world events, once they

occur, tend to be reflected in the stock price straight away. Anderson and Cross (1990)

tracked the impact of California earthquake of October 17, 1989 on the stock prices of

the real estate industry and found that the market treats quakes as new information,

which is then reflected in the stock prices of real estate companies located in and

around San Francisco area as negative returns. Reinhold (1995) also found significant

negative price reactions to Hurricane Andrew being reflected in property insurance

company stocks. However, just because a catastrophic event has occurred, it does not

necessarily mean that the effect on insurance company stock prices is negative, and

that the share price of insurance companies must fall. Shelor, Anderson, and Cross

(1992), having monitored market reaction to the stocks of property and casualty

insurance companies after an earthquake, discovered an effect different from the

negative ones experienced by the aforementioned real estate companies. The price

effect on property and casualty insurance industry stocks was actually positive. The

tendency for insurance company stocks to rise following catastrophe events further

points to investors confidence (positive effect) on future demands for insurance

relative to share price decline (negative effect) of insurance company stocks caused

by catastrophic loss. Aiuppa, Carney, and Krueger (1993) also examined the effect of

earthquakes on the value of property insurance company stocks, and found them to be

similarly positive. Various views of others have also been expressed in literature on

whether stocks can really reflect the true equity value of reinsurance companies.

In considering the problem of a lack of sufficient means on the part of

reinsurance, companies to pay for catastrophic claims, both government and market

sectors have proposed various solutions to address the problem. The government part

4

involves the proposed government funded CAT reinsurance program or the issuing of

government CAT bonds, such as CAT bonds issued by the Government of Mexico

(Wolfgang and Brenda, 2010). The market sector part involves the use of financial

innovation to create numerous insurance event-linked products, such as CAT options,

CAT bonds, CAT equity put options, and CAT exchanges. These developments are all

designed to allow reinsurance companies to provide more effective risk transfer

channels.

Insurance event-linked securities are a type of structured product that link

financial claims to an insurance event (Cummins and Philip, 2000). Their most

important function is to transfer catastrophe risk borne by the insurance company to

the capital market. These products have very many types, ranging from CAT bonds,

CAT options, or capital-CAT exchange types. Once catastrophe occurs, the equity

value of reinsurance companies will go down. Past methods of increasing capital

(opening public offering or cash replenishment) were not able to return the capital of

reinsurance companies back to the original level. However, the insurance

event-linked securities can provide even more additional capital-raising channels.

Next, we will introduce CAT bonds, introduce CAT equity put (CatEPut), and

provide a description of hybrid CAT bonds as proposed in this thesis study.

CAT bonds are a kind of insurance-linked security, also known as event-linked

bonds, belonging to pre-loss debt financing. When a specific catastrophe event occurs,

CAT bonds will fulfill the obligation to pay. Although it was only until the late 1990s

before CAT bond market finally took off to a slow start, it has now become a stable

source of underwriting for insurance and reinsurance companies. The CAT bond

market has experienced continued steady growth and has set new records of market

issuing volume in 2005, 2006, and 2007 (Cummins, 2008). CAT bonds carry full

guarantees, which eliminate anxiety over credit risk of CAT bonds. Since correlation

between catastrophe and stock market return rate is low, from risk diversification

point of view, CAT bonds are more admired and respected by investors (Litzenberger,

et al, 1996).

Catastrophe equity put (CatEPut) option is part of equity financing, which refers

to the right to sell equity based on previously agreed strike price. The option buyer

puts up the option money to give consent to purchase, in the event of catastrophe, the

CatEPut offer for the company's equity based on a price agreed in advance. After the

catastrophe, when reinsurance companies are in need of capital injection, CatEPut

allows reinsurance companies to obtain any additional capital injection at an

advantageous price. Therefore, CatEPut option is designed to provide a type of

catastrophe risk transfer channel for reinsurance companies. In addition, any

additional issue of preferred share will dilute existing shareholders' equity value.

5

This study, based on the idea of hybrid CAT bond suggested by Pauline and

Henry (2009), essentially proposed to combine two single type products, namely, CAT

bond and CatEPut option, into a hybrid type product. The design of hybrid CAT bond

type product is aimed to not only transfer catastrophe risk faced by the reinsurance

companies to the capital market, but also provide downside risk protection for the

equity value. It also has a dual natured pre-loss and post-loss financing. The issuing of

hybrid CAT bonds will increase the issuance volume in the market.

The focus of most of the relevant studies in literature was on single product

assessments such as reinsurance contracts, CAT bonds, and CatEPut options, with

additional focus on raising the value of catastrophe reinsurance contracts by

reinsurance companies using CAT bonds (Lee and Yu, 2007). The contribution of this

study are as follows: 1) actually created a hybrid CAT bond from a combination of

CAT bond and CatEPut option; 2) established contingent claims framework to

examine how reinsurance companies were able to lower credit risk and raise the value

of catastrophe reinsurance contracts by issuing hybrid CAT bonds; and 3) discovered

that, relative to CAT bonds, hybrid CAT bonds are positioned to raise reinsurance

contract value to a greater extent. Specifically, we will explore, in the process of

setting up assets, liability, interest rate, and catastrophe loss variations, how insurance

linked securities issuance changed the capital structure of reinsurance companies and

further affected the valuation of insurance contracts. Then, we will make individual

comparisons to discover which insurance-linked security issued by the reinsurance

companies is more favorable. The structure of this study is further explained below.

Part II will describe the process of dynamic in the assets, interest rates, liabilities, and

catastrophe losses of reinsurance companies. Part III will show in detail the profit

functions of reinsurance contracts under different issuance scenarios of reinsurance

companies. Part IV will show the resulting values generated by numerical analysis,

and discuss and compare the values presented. Part V will present the conclusion of

this study.

2. Insurance Company Model Setting

The study adopted the structural approach pioneered by Merton (1974 and 1977)

to value the corporate debt contract, allowing us to link together various concerns

about reinsurance companies such as asset value, debt value, capital structure, default

risk, and financial claims. In addition, the study also followed the structured model

adopted by Cummins (1988), Duan et al (1995), and Duan and Yu (2005), taking into

account the dynamic process of interest rate and liability, and observed how

reinsurance companies were able to transfer catastrophe risks, which they themselves

6

are facing, to the capital market through the issuing of insurance-linked products.

The study considered two kinds of insurance-linked products, CAT bonds, and

hybrid CAT bonds. Here, we first consider the case of CAT bonds issued by

reinsurance companies. Issuing of CAT bonds can transfer catastrophe risk to the

capital market so that the underwriting capacity of reinsurance companies themselves

can be enhanced (Lee and Yu, 2007). CAT bond can be issued through reinsurance

companies, or through special purpose companies (SPC). To focus attention on the

weight of reinsurance contract, the study assumed that CAT bonds are issued through

a SPC, and that the fair price of CAT bonds are also assumed to be consistent with

results obtained by Litzenberger (1996), Lee and Yu (2002), and Vaugirard (2003).

Recent studies found that reinsurance companies, even with capital injections

obtained through the issuing of catastrophe bonds, are not completely able to actually

transfer their own assumed catastrophe risks (Cummins, Lewis, Phillips (2002), Nell

and Richter (2004). Catastrophic events will increase the liability of reinsurance

companies (Duan and Yu, 2005) because, with everything else being equal,

catastrophic events will further reduce the equity value of reinsurance companies. The

study assumes that the market is efficient. That is, the market equity value of a

reinsurance company will fully reflect the fact that catastrophe losses lead to decline

in equity value. To solve the risk of decline in the value of equity, we will consider in

this section the issuing of CatEPuts by reinsurance companies to transfer risk to

capital market. CatEPuts does not need to be issued by SPC, and assumes that the fair

price of CatEPut portion is consistent with the reasonable results obtained by Lin et al

(2009) and Chang et al (2011).

The aforementioned single product type is limited by market size, and the issue

amount is subject to restrictions. To enhance the effectiveness of products, the concept

of hybrid products has emerged to transfer catastrophe risk even further that,

according to the development of financial markets in the past, suggests that the selling

of such complex hybrid products by financial intermediaries is feasible (Pauline and

Henry, 2009). Based on this concept, the study put CAT bond and CatEPut option

together to create a type of hybrid CAT bond. To focus attention on the weight of

reinsurance contract, the study assumes that this type of hybrid CAT bond is issued

through SPC, where the fair price of CAT bonds and CatEPut options are consistent

with those mentioned above.

The capital structure of reinsurance companies and catastrophic loss thresholds

are important factors used to value reinsurance contracts, which fully explains the

dynamic process of reinsurance company assets, liabilities, and catastrophic losses

that corresponds to the changing process of real world probability measure (P) and

risk neutral probability measure (Q).

7

2.1 Asset dynamic process

The study used the traditionally assumed asset dynamic process as being a

logarithmic diffusion process to further incorporate the effect of interest rate on the

value of assets into the model. Since a larger portion of asset investment portfolio of

reinsurance company is usually fixed income assets (interest rate sensitive assets)

(Duan and Yu, 2005; Lee and Yu, 2007), this type of model setting is more apt at

describing the change process of asset value of reinsurance companies.

,t V V t V V t

dV Vdt Vdr VdWµ φ σ= + + (1)

Where,

t

V : Value of asset of reinsurance companies in period t

t

r : Value of risk-free interest rate in period t

,V t

W : Credit risk of reinsurance companies (Wiener process)

V

σ : Credit risk volatility of reinsurance companies

V

φ : Instantaneous interest rate elasticity of assets of reinsurance companies

Among them, credit risk is perpendicular to interest rate risk, where credit risk

represents all risks other than interest rate risk.

2.2 Interest rate dynamic process

The study honors the interest rate dynamic process developed by Duan and Yu

(2005) and Lee and Yu (2007) by assuming that instantaneous interest rate change

process is in line with square root process developed by Cox et al (1985). This type of

configuration will avoid getting Vasicek interest rates to be less than zero.

Instantaneous change process of interest rate under real-world probability measure (P)

is as follows:

( )t t t t

dr k m r dt v r dZ= − + (2)

Where:

k : Mean reversion strength value

m : Long term interest rate average

v : Interest rate volatility

t

Z : Wiener process unrelated to ,V t

W

Since interest rate value is an important factor affecting the value of the assets of

reinsurance companies, in the following we will combine interest rate change process

and asset change process together by substituting Equation (2) into Equation (1). The

asset change process then becomes as follows:

,

( )t V V V t V t t V V t

dV km kr dt v r dZ dWµ φ φ φ σ= + − + + (3)

The standard practice to make evaluation easier is to convert the original

real-world probability measure (P) to risk neutral probability measure (Q). The

8

interest rate change process under risk neutral probability measure (Q) is expressed as

follows:

* * *( )t t t t

dr k m r dt v r dZ= − + (4)

Where:

*

*

*

r

r

r t

t t

k k

kmm

k

rdZ dZ dt

v

λ

λ

λ

= +

=+

= +

Among them, r

λ is market price of interest rate risk, which is set to constant by

Cox et al (1985). *

tZ is the Wiener process under risk neutral probability measure.

The asset change process under risk neutral probability measure (Q) is expressed

as follows:

* *

,t t t V t t t V t V tdV rV dt v r V dZ V dWφ σ= + + (5)

Among them, *

,V tW is the Wiener process unrelated to *

tZ under risk neutral

probability measure (Q).

2.3 Liability dynamic process

With regard to reinsurance company liabilities, they come from not only

catastrophe reinsurance contracts, but also from other types of insurance coverage

liabilities. Any types of liability that have nothing to do with catastrophe reinsurance

contracts will represent future claims of present value, which belong to interest rate

sensitive liabilities, therefore, based on Lee and Yu (2007), the liability change

process of reinsurance companies under real world probability measure (P) is

expressed as follows:

,t L t L t t L t L t

dL L dt L dr L dWµ φ σ= + + (6)

Where:

t

L : Value of liability of reinsurance companies in period t

L

µ : Expected change in liability value

L

φ : Interest rate elasticity of liabilities of reinsurance companies

L

σ Liability value volatility

,L t

W : Wiener process

Such a continuous diffusion process reflects the effect of interest rate change and

the risk of small daily variations. Since small daily variation ,L t

W is part of the

homogeneous change in capital market, the study assumes that it is a no risk premium.

The result from the interest rate change process under risk neutral probability measure

(Q) in Equation (4) is carried into Equation (6). Substituting t

Z with *

tZ to obtain

interest rate change process under risk neutral probability measure (Q), which can be

9

expressed as follows:

* *

,t t t L t t t L t L tdL r L dt v r L dZ L dWφ σ= + + (7)

2.4 Catastrophe losses processes

The study follows the traditional insurance established in literature (see Bowers,

et al (1986)) that uses compound Poisson process to express change in total

catastrophe losses. That is, using a series of loss jumps to describe the process of

catastrophe losses. The catastrophe loss change process in catastrophe reinsurance

contract underwriting standard in period t can be expressed in the follow change

process:

( )

1

N t

t t

j

C c=

= ∑

(8)

To estimate the impact of basis risk on catastrophe reinsurance contract, we

additionally listed the change process of composite index of catastrophe losses, which

is expressed as follows:

( )

, ,

1

N t

index t index t

j

C c=

= ∑ (9)

Where, { }0

( )t

N t≥

represents the number of changes in catastrophes occurred in

each period. The study assumes that such a change process is driven by the Poisson

process with frequency λ . t

c represents the actual amount of loss in jth

catastrophic

loss event underwritten by catastrophe reinsurance contract in a specific period; ,index t

c

represents the amount of composite index of losses. In terms of the amount of actual

losses (t

c ) and the amount of composite index of losses (,index t

c ), the number of

catastrophic occurrence for each time is 1,2,..., ( )j N t= , the study assumes that

catastrophic events are independent of each other, identical to each other, and obey the

variable nature of lognormal distribution, and that the amount of actual losses (t

c ) and

the amount of composite index of losses (,index t

c ) are unrelated to the number of

catastrophic events occurred. Logarithmic mean and variance are represented by the

symbol c

µ (index

µ ) and c

σ (index

σ ), respectively. In addition, assume that each time the

number of catastrophe occurrences is at 1,2,..., ( )j N t= , the correlation between the

logarithm of the amount of actual losses (t

c ) and the amount of composite index of

losses (,index t

c ) is equal to c

ρ .

For the purpose of calculation, the study followed the practice of Merton (1976)

by assuming that the overall economy will only be affected by regional catastrophic

events, so the change process number { }0

( )t

N t≥

and catastrophe loss amounts t

c and

,index tc

in a catastrophic event are risk-free premiums. Therefore, the change process of

loss in Equation (8) and (9) will not alter the original distribution characteristics as a

result of converting real world probability measure (P) to risk neutral probability

10

measure (Q) (Lee and Yu, 2007).

3. Valuation of Catastrophe Reinsurance Contracts

Once the change processes of assets, liabilities, and losses under risk neutral

probability measure (Q) are known, the payoff functions in a wide range of

circumstances under risk neutral measure (Q) can be discounted to measure the value

of reinsurance contract. The study first had to list out basic payoff functions of those

reinsurance companies that did not issue insurance event linked securities. Then, the

study had to extend the analysis to include the valuation of reinsurance contracts that

are affected when different insurance linked products (CAT bonds and hybrid Cat

bonds) are issued.

3.1 Non-issuance situations

The study first had to analyze the profit function of reinsurance contracts in

situations when reinsurance companies have not issued any insurance linked securities.

A non-issuance scenario is viewed as the most basic situation and is easily understood,

and its profit functions can be extended to a variety of complex situations, such as

reinsurance companies issuing CAT bonds and hybrid Cat bonds.

3.1.1 No default risk

The type of reinsurance contract used in this study is excess of loss policy. When

the total amount of loss insured exceeds the minimum contract trigger value A of the

original insurance company due to catastrophe, the reinsurance company must then

pay compensation to the original insurance company as stipulated in the contract, with

upper trigger loss limit M. When taking into account no risk of contract breach by

reinsurance companies, the payoff function of the catastrophe reinsurance contract is

expressed as follows:

,

,

0 ,

T

T T T

M A C M

P C A M C A

otherwise

− >

= − > >

(10)

T

P : Payoff function of reinsurance contract at maturity.

T

C : Aggregate catastrophe losses insured by the insurance company at maturity.

M : Cap level

A : Attachment point

3.1.2 Default risk

When reinsurance companies cannot manage to fulfill claims obligations

11

stipulated in the provisions of catastrophe reinsurance contracts, there is the risk of

default. The payoff function of reinsurance contracts under default risk at time of

contract maturity is expressed in Equation (11). Where, the asset and liability values

of reinsurance companies are represented by T

V andT

L , respectively, upon maturity of

reinsurance contract. We learned, through default risk considerations, that profit

function of this kind of catastrophe reinsurance contracts is based on end-period

financial position ratio analysis of reinsurance companies. This study assumes that

reinsurance contract liabilities underwritten by reinsurance companies have the same

priority claims as other types of insurance liabilities. When reinsurance companies

default because they cannot fulfill claims obligations, these liabilities will be shared

equally among the remaining asset values of the reinsurance companies on a pro rata

basis. As the profit function shows, default risk will reduce the expected cash inflows

of insurance companies and further contribute to the decline in the value of

reinsurance contracts.

,

,

,

( ) ,

( ) ,

0 ,

T T T

T T T T T

T

d T T T T

T

T T

T T T T

T T

M A if C M and V L M A

C A if M C A and V L C A

M A VP if C M and V L M A

L M A

C A Vif M C A and V L C A

L C A

othe

− ≥ ≥ + −

− ≥ ≥ ≥ + −

−= ≥ < + −

+ −

−≥ ≥ < + −

+ −

rwise

(11)

3.2 Issuance of catastrophe bonds

Reinsurance Companies can issue catastrophe bonds to increase their own

underwriting capacity to provide more insurance programs or increase the scope of

protection. These types of CAT bond-based contingent payments are used to pay

liabilities claims. Therefore, in this type of situations, the size of the reinsurance

contract value not only determines the financial positioning of reinsurance companies,

but also determines the correlation between the size of the CAT bond-based

contingent payments and the composite index of catastrophe losses.

In this section, we will consider the situation of reinsurance companies providing

reinsurance contract protections while issuing CAT bonds. In research for our thesis

paper, it is assumed that the CAT bonds are zero-coupon bonds that do not require to

pay any coupon when bond contract period is still in effect. From CAT bond investor

point of view, the payoff function of CAT bonds upon maturity is expressed as

follows:

*

, *

,

,

CAT CAT

CAT T

CAT CAT

F if C KP

rp F if C K

≤=

× > (12)

12

Where:

CAT

F : Denomination of CAT bond

*

C : Could be T

C or,Index T

C , depending on what is stated in the CAT bond

contract.

rp : Ratio between catastrophe loss trigger level and the required

repayment of principal when the level is triggered, with 0 1rp≤ <

When the cumulative catastrophe losses reach the catastrophe bond stipulated

trigger level (CAT

K ), reinsurance companies can obtain capital injections (CAT

δ ) from

CAT bonds as expressed below:

*

,( )CAT CAT CAT TC F Pδ = − (13)

Payoff function Re,dCAT T

P of the reinsurance contract upon maturity is expressed

as follows:

CATRe,

, ( )

, ( )

( )( ), ( )

( )( )

T T CAT T

T T T CAT T T

T CAT

d T T T CAT T

T

T T CAT

M A if C M and V L M A

C A if M C A and V L C A

M A VP if C M and V L M A

L M A

C A V

L

δ

δ

δδ

δ

− > + > + −

− > > + > + −

− += > + < + −

+ −

− +, ( )

0 ,

T T CAT T T

T T

if M C A and V L C AC A

otherwise

δ

> > + < + −+ −

(14)

3.2.1 Basis risk

When compensation claims that catastrophe linked products are based on are

actual catastrophe losses (T

C ), that is, when *( ) ( )

TC Cδ δ= , then from the perspective of

reinsurance companies, basis risk does not exist. However, if the claims are based on

composite index of catastrophe losses (,index T

C ) rather than actual catastrophe losses,

that is, when *

,( ) ( )Index T

C Cδ δ= , then basis risk does exist. When basis risk exists, the

size of reinsurance company's actual underwriting losses and that of composite index

of catastrophe losses will not be in agreement. At such a time, the capital that CAT

bonds should be injected with will not be the same as the actual capital injection. Such

a situation will increase the default risk of reinsurance companies, thereby reducing

their debt repayment ability. Therefore, basis risk is also a risk factor affecting

reinsurance contract value.

3.3 Issuance of hybrid CAT bonds

The study actually combined CAT bonds and CatEPut options into hybrid CAT

bonds. Reinsurance companies can use the issuance of hybrid CAT bonds to solve the

problem of insufficient capital at the time when CAT bonds are issued. However,

13

reinsurance company issued CAT bonds still cannot completely transfer the

underwritten catastrophe risk to the capital market (Cummins, Lewis, and Phillips,

2002; Nell and Richer, 2004). The study proposed instead that reinsurance company

issue hybrid CAT bonds to solve the problem of insufficient capital injections. Based

on product design, hybrid CAT bonds possess more post-loss financing characteristics

than CAT bonds, providing reinsurance companies with more capital injections and

underwriting capabilities.

Next is the description of payoff function during the issuing of hybrid CAT

bonds. Hybrid CAT bonds consist of two products, CAT bonds and CatEPut options,

and therefore have payoff function (Hybrid

δ ) that is sum total of payoff functions of

CAT bonds (CAT

δ ) and CatEPut (CatEPuts

δ ). The payoff function of these products is

expressed as follows:

CAT bond portion of the payoff function:

From the point of view of CAT bond investors, the payoff function of matured

CAT bonds is as follows:

*

, *

,

,

CAT Hybrid

CAT T

CAT Hybrid

F if C KP

rp F if C K

≤=

× >

(15)

Where:

Hybrid

K : Trigger level of hybrid CAT bonds

Capital injections (CAT

δ ) obtained by reinsurance companies is as follows:

*

,( )CAT CAT CAT TC F Pδ = −

CatEPut option portion of the payoff function:

This article assumes that the market is efficient. That is, equity value of

reinsurance companies in the market will fully reflect the actual equity value of

reinsurance companies upon maturity. At such time, the equity value of reinsurance

companies in the market is expressed as follows:

Equity value (T

E ) = Asset value (T

V ) - Liability value (non-CAT + CAT

reinsurance contracts;T

L )

Under the assumption of market efficiency, the equity value of reinsurance

companies in the market can reflect the true equity value of reinsurance companies, so

catastrophic events will increase the value of liability that further reduces equity value.

Therefore, downside risk protection of equity value is critically important.

Reinsurance companies also use CatEPuts to increase post catastrophe capital

injections to protect downside risk of equity value, thereby transferring catastrophe

risk to capital market. The payoff function of CatEPuts upon maturity is expressed as

14

follows:

*,

0 ,

CatEPuts T CatEPuts T T Hybrid

CatEPuts

E E if E E and C K

if otherwiseδ

− > >=

(16)

Where:

CatEPuts

δ : Capital injection of CatEPut option in the hybrid CAT bond

CatEPuts

E : Strike price of CatEPut option in the hybrid CAT bond

Hybrid

K : Trigger level of hybrid Cat bonds

Payoff function of matured hybrid CAT bonds is expressed as follows:

Hybrid CAT CatEPuts

δ δ δ= + (17)

Where:

Hybrid

δ : Payoff function of hybrid CAT bonds

CAT

δ : Payoff function of CAT bond in the hybrid CAT bond

CatEPuts

δ : Payoff function of CatEPut option in the hybrid CAT bond

Payoff function of reinsurance contracts upon maturity is expressed as follows:

Re,

, ( )

, ( )

( )( ), ( )

T T Hybrid T

T T T Hybrid T T

T Hybrid

dHybrid T T T Hybrid T

T

M A if C M and V L M A

C A if M C A and V L C A

M A VP if C M and V L M

D M A

δ

δ

δδ

− > + > + −

− > > + > + −

− += > + < + −

+ −

( )( ), ( )

0 ,

T T Hybrid

T T Hybrid T T

T T

A

C A Vif M C A and V L C A

D C A

otherwise

δδ

− + > > + < + −

+ −

(18)

Therefore, the value of insurance contracts is not only related to initial capital

position of reinsurance companies, but is also related to the size of capital injections

of hybrid CAT bond

3.4 Rate on line (ROL)

Based on the payoff function of reinsurance contracts under various

circumstances , as well as on the dynamic processes of assets, liabilities, and interest

rates described in the previous section, ROL (fair pricing premium rate) is expressed

as follows:

0

0

1r

Sr dSQ

TROL E e POM A

− ∫= × × −

(19)

ROL is the proportion of each dollar of loss recoverable by the reinsurance

contract. 0

QE represents expected value of product issue date under risk neutral

probability measure (Q). , Re, Re,, , ,

T T d T dCAT T dHybrid TPO P P P P= represents payoff function of

reinsurance contact at maturity under various circumstances discussed above. The

15

structure analyzed in the study has now been explained in detail. The study does not

expect to find any closed form solution under these complex circumstances. Thus, in

the next section we will use numerical analysis to estimate the value of reinsurance

contracts.

4. Numerical Analysis

This section will use Monte Carlo simulation method to estimate ROL for

reinsurance contracts under various circumstances. The simulations are run based on a

weekly basis with 20,000 paths. Table 1 shows a list of basic parameter values that

can be regarded as baseline values for Monte Carlo simulation. First, simulation

results obtained under non-issuance situation are served as baseline values, which are

then compared with cases where various insurance linked products are issued. This

will obtain the level of impact of various factors associated with reinsurance

companies, such as initial capital position, catastrophe frequency, standard deviation,

CAT bonds, and hybrid CAT bonds issuance, on ROL of reinsurance contracts when

these factors change.

[Insert Table 1]

The study considered setting the initial financial position ratio for the reinsurance

companies to 1.1, 1.2, 1.3, 1.4, and 1.5. The initial liability (0L ) is set at 100. The

period underwritten by the reinsurance contract is one year, and the minimum trigger

level and the maximum upper limit level is set to 20 and 100, respectively. Next, the

study introduced the product contract portion of the insurance event-linked products.

In the CAT bond portion, the effective maturity period of CAT bond contracts is set to

one year. When cumulative catastrophe losses exceed CAT bond trigger level (CAT

K ),

the portion of principal needed to be repaid to CAT bondholders, ( rp ), is set to be 0.5.

The CAT bond issuing denomination is set to 10. That is, the ratio of issuance

denomination to initial liability of reinsurance companies is 0.1. In addition, CAT

bond contract trigger level (CAT

K ) is set to 80,100, or 120, respectively. Next, the

trigger level (CatEPuts

K ) of CatEPut part is set to 80,100, or 120, respectively. The

intrinsic value (CatEPuts

E ) is set to 10, which is a European style multiple

trigger-condition option. The hybrid CAT bonds are created from CAT bonds and

CatEPut options, with effective maturity period for the hybrid CAT bond set to one

year and trigger level (Hybrid

K ) set to 80, 100, or 120, respectively. The part on CAT

bonds and CatEPut options is the same as those discussed previously. The above is the

part on products setting.

Next is the discussion on other parameter settings. The correlation (VD

ρ ) between

dynamics process of assets and liabilities of reinsurance companies is set to 0.2, initial

16

interest rate (0

r ) is set to 5%, long-term average interest rate ( m ) is also set to 5%,

strength of interest rate mean reversion ( k ) is set to 0.2 and interest rate volatility ( v )

is set to 10 %, and the market price of interest rate risk (r

λ ) is set to be -0.01. The

values of these parameters are all set to the same as those used in literature. To reflect

the number of times catastrophes occur each year, the frequency of occurrence of

catastrophic events ( λ ) is set to annual occurrence of 0.5, 1, and 2 times, respectively.

The study also assumes that the parameters for actual catastrophe losses and

composite catastrophe losses are the same. The logarithmic average of actual

catastrophe losses and composite catastrophe losses ( ,C index

µ µ ) is set to ( 2, 2 ), and that

the value of logarithmic standard deviation ( ,C index

σ σ ) is set to 0.5, 1, and 2,

respectively. Attention of the study will also be focused on the relationship between

actual catastrophe losses and composite catastrophe losses.

4.1 Default risk

The study first describes the value of the contract by considering default and

no-default risks in various cases of catastrophe frequencies and standard deviation of

losses, then analyzed various cases of issuance of insurance linked products. In cases

of no-default risk, the soundness of the initial financial position will not affect the

value of the contract. In cases of default risk, the size of financial position ratio will

affect the value of the reinsurance contract. The difference in the value of contract

between the two cases is called default risk premium. Next, we will list the simulation

results in Table 2.

[Inset Table 2]

The result is consistent with the expected results. Compared to reinsurance

contracts with default risk factors taken into consideration, the value of reinsurance

contracts with no-default risk considerations is larger. The higher the initial capital

ratio of reinsurance companies is, the lower the risk of default; the value of

reinsurance contract value will also be higher. In addition, the observed default risk

premium will increase with the increase in standard deviation of catastrophe

frequency. For example, when the initial capital ratio of reinsurance was 1.3 and

standard deviation of loss was 2, and when frequency of catastrophe occurrence

increased from 0.5 to 1 and 2, the default risk premium went up from 156.5 basis

points to 312.9 and 623.9 basis points in value. Default risk premium increases as

reinsurance companies' degree of financial leverage, frequency of catastrophe

occurrences, and catastrophe loss volatility increase. Since the consideration of

catastrophic risk will lead to the increase of default risk premium, catastrophe risk is

an important factor in reinsurance contract evaluation. For example, in the situation

when standard deviation of catastrophe frequency is 2, and when the initial financial

17

ratio of reinsurance companies decreased from 1.5 to 1.1, the default risk premium

rose from 329 basis points to 963.3 basis points in value, a total increase of 634.3

basis points. In that case, when standard deviation of catastrophe frequency dropped

to 1, the amount of increase in default risk premium fell to 75.4 basis points in value.

In addition, when catastrophe risk is low (low catastrophe frequency and low

catastrophe loss standard deviation), the default risk premium becomes insignificant.

For example, when standard deviation of catastrophe frequency is 0.5, the range of

default risk premium is from 0 to 1.3 basis points in value.

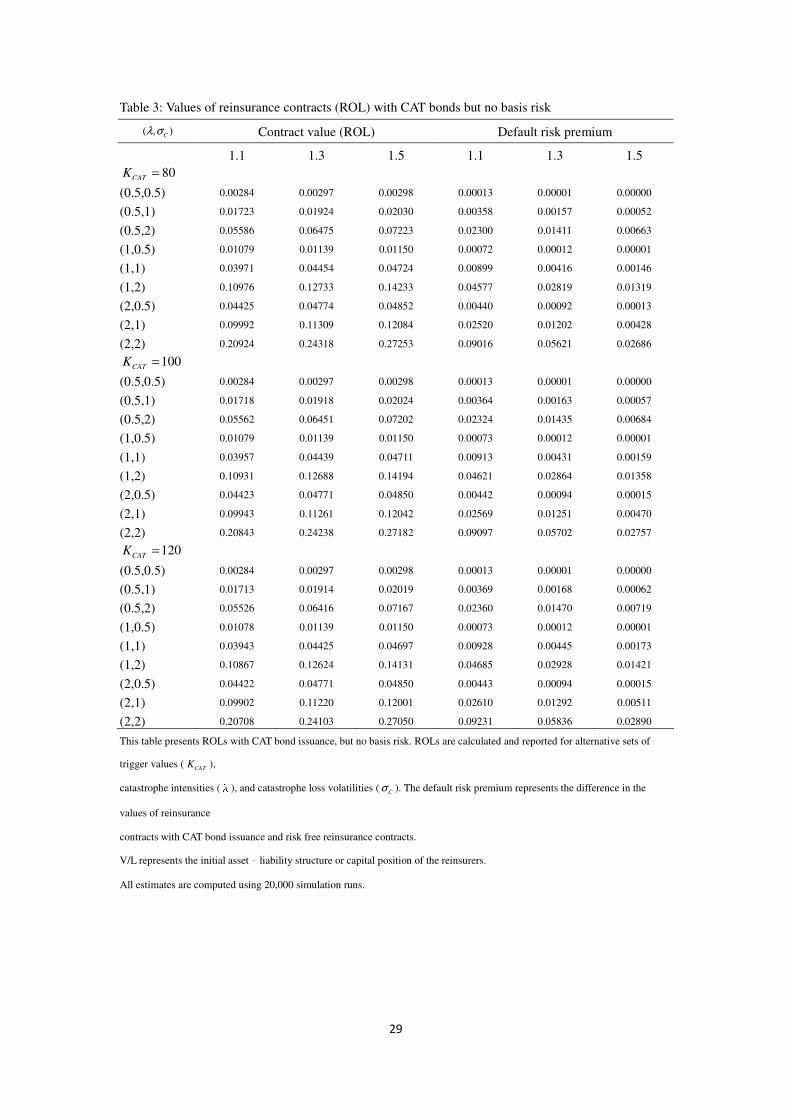

4.2 Issuance of catastrophe bonds

Table 3 shows how reinsurance companies use the issuing of CAT bonds to

facilitate the transfer of catastrophic risk, reduce default risk of reinsurance companies,

and raise the value of reinsurance contracts. The study set the ratio of CAT bond

denomination to total liability is set to be 0.1, and set this type of CAT bonds to no

basis risk. The trigger level (CAT

K ) was set to 80,100, and 120, respectively. Result of

the simulation is shown in Table 3.

[Insert Table 3]

Next, we compared the reinsurance contract values listed in Table 2 and 3. We

observe that no matter what the capital position, trigger level, catastrophe frequency,

and standard deviation are at the beginning, reinsurance companies can use the

issuance of CAT bonds to reduce default risk premium and increase the value of the

reinsurance contracts. Here we should notice that default risk premium and value of

reinsurance contract would reduce and increase, respectively, following the decrease

in trigger level. That is because when the value of trigger level is higher, the

probability of total amount of catastrophe losses reaching trigger level is lower, which

also reduces the ability of reinsurance companies to pay catastrophe claims. In cases

of high catastrophe frequency, high standard deviation, and low initial capital position,

the impact of CAT bonds on the raising of reinsurance contract value is even more

significant. For example, in the situation with standard deviation of catastrophe

frequency equals to 2 and initial capital position equals to 1.1, when the trigger levels

are 80 and 120, respectively, the issuance of CAT bonds can add 61.7 and 40.2 basis

points, respectively, to the reinsurance contract value (or subtract from default risk

premium).

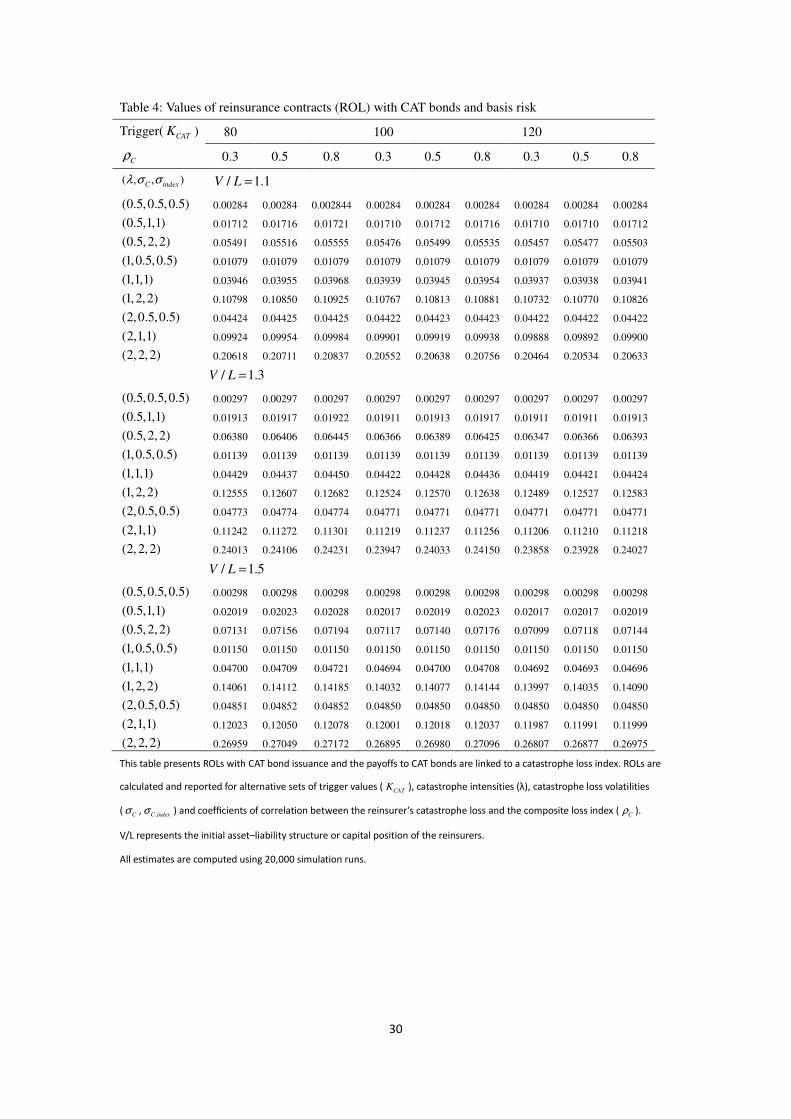

4.2.1 Basis risk

When the size of the capital injected by CAT bonds is based on composite index

rather than actual underwriting losses, basis risk exists in CAT bonds. Table 4 shows

how basis risk affects reinsurance contract value when reinsurance companies issue

18

CAT bonds. Table 5 shows the corresponding default risk premium under the same

condition.

[Insert Table 4]

[Inset Table 5]

Table 4 shows that when correlation between catastrophe losses underwritten by

reinsurance companies and composite index of losses is low, the level of basis risk

faced by reinsurance companies is high. When correlation coefficient is equal to 1,

basis risk does not exist. This means that reinsurance contract value is the same as

those listed in Table 3 under the same condition. The difference between reinsurance

contract value with other different correlations and those with correlation of 1 can be

viewed as a basis risk premium. Under correlation of 0.3, 0.5, or 0.8, we can see that

basis risk lowers reinsurance contract value and raises default risk premium. The

degree of decline in value increases with the increase in basis risk, catastrophe

frequency, and standard deviation. For example, when catastrophe frequency is equal

to 2, the standard deviation of both actual losses and composite index of losses of

reinsurance companies equal to 2, trigger level equals to 80, and initial capital

position equals to 1.1. With correlation dropping from 0.8 to 0.5, the reinsurance

contract decreased (default risk premium will rise) by 12.6 basis points in value. As

correlation continued to drop from 0.5 to 0.3, reinsurance contract continued to

decrease (default risk premium will continue to rise) by 9.3 basis points in value. It

should be noted that basis risk premium decreases with the increase in trigger level

and initial financial position, but increases with the increase in catastrophe frequency

and standard deviation of losses. Although basis risk premium is significant, but

compared to the issuance of CAT bonds, its effect on increasing the value of

reinsurance contract is less significant.

[Insert Figure 1]

Figure 1 shows, under the condition when catastrophe frequency is 2, standard

deviation of both actual and composite index is 2, trigger level is 80, and initial

capital position is 1.1, how the value of insurance contract and basis risk (loss

correlation coefficient) are related to catastrophe liability structure ratio (CAT bond

issuing denominations and total liabilities of reinsurance companies). Figure 1 shows

that reinsurance contract value increases with the increase in proportion of catastrophe

liability structure, which also explains how a higher proportion of CAT bond liability

structure improves the ability of reinsurance companies paying catastrophe claims,

and thus increases the value of reinsurance contracts. Figure 1 also shows that when

CAT bonds are issued with very large denominations, the effect of basis risk becomes

much intense, with increasing basis risk premium following the proportional increase

in catastrophic liability structure. When the proportion of CAT liability structure is

19

lowered, basis risk premium with varying correlation is almost non-existent.

4.3 Issuance of hybrid CAT bonds

Next, we explore the situation of reinsurance companies issuing hybrid CAT

bonds. Although issuance of CAT bonds can transfer catastrophe risks faced by the

reinsurance companies to the capital market, it is not enough to handle all the

catastrophe risks when standard deviation of catastrophe frequency is high. The study

proposes that reinsurance companies issue hybrid CAT bonds to further solve the

problem with insufficient capital created by catastrophe risks.

[Insert Table 6]

Table 6 shows the increase in underwriting ability of reinsurance companies

themselves after they had issued hybrid CAT bonds, which further increase the value

of catastrophe reinsurance contracts. The hybrid CAT bonds proposed in this study is

a combination of CAT bonds and CatEPuts that also assumes that there is no need to

further consider the default risk of this types of insurance linked products. The study

assumes that catastrophe loss trigger level referenced by the CAT bonds and CatEPuts

in hybrid CAT bond products is the same. The trigger level settings for hybrid CAT

bond contract (Hybrid

K ) are 80,100, and 120, respectively. For the CAT bond part, the

ratio of CAT bond denomination to initial liability of reinsurance companies is set to

0.1. For the CatEPuts part, the option is set to a common European style multiple

trigger-condition option, with exercise equity value of 10. The resulting reinsurance

contract value after the simulation is shown in Table 6. Next, we compared the

reinsurance contract value in Table 2 and 6. We observed that, regardless of the

situation with initial capital position, trigger level, catastrophe frequency, and

standard deviation, reinsurance companies could reduce the risk of default and

increase the value of reinsurance contracts by issuing hybrid CAT bonds. It should be

noted that default risk premium and reinsurance contract value will decrease and

increase, respectively, following the drop in trigger level. This is also because that the

higher the trigger level, the lower the probability that the total amount of catastrophe

losses will reach the trigger level. This reduces the ability of reinsurance companies to

pay catastrophe claims. Under conditions of high catastrophe frequency, high standard

deviation of losses, and low initial capital position, the impact of hybrid CAT bond on

the increase of reinsurance contract value is even more significant. For example, when

standard deviation of catastrophe frequency equals to 2, initial capital position equals

to 1.1, and trigger levels equal to 80 and 120, respectively, the issuance of hybrid CAT

bonds can add 185.5 and 120.8 basis points to reinsurance contract value (or subtract

from default risk premium), respectively.

20

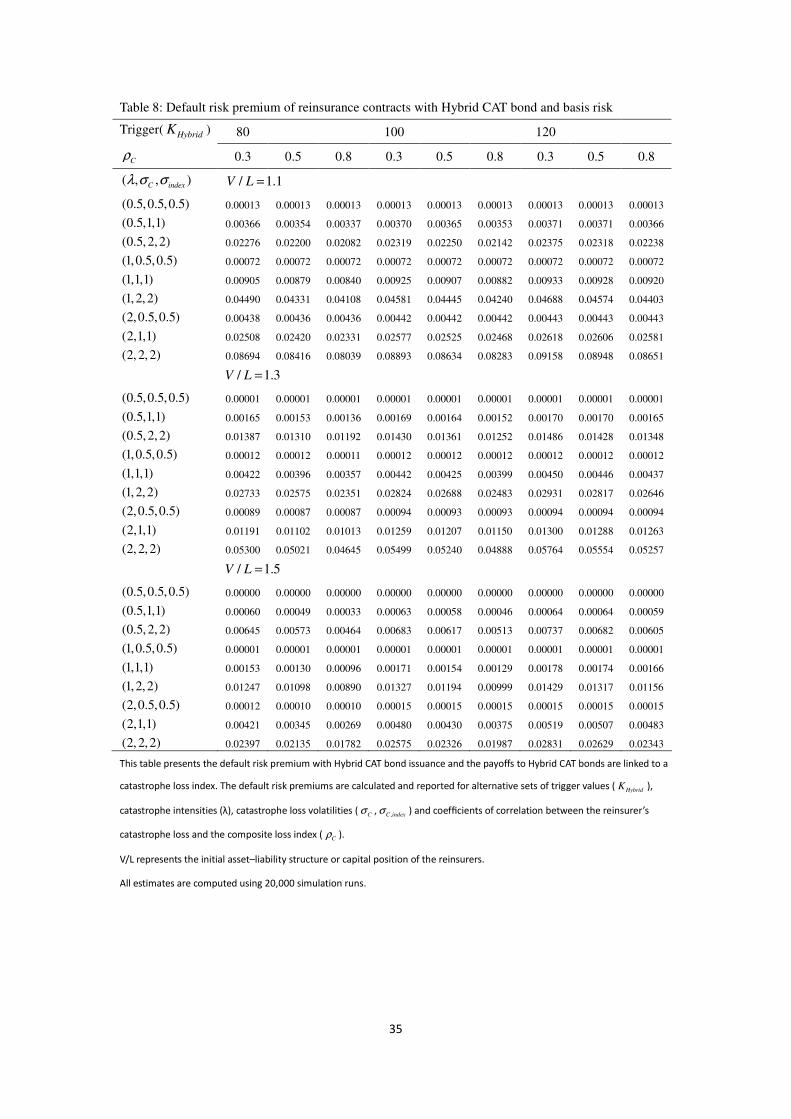

4.3.1 Basis risk

When the amount of capital injection from hybrid CAT bonds is based on

composite catastrophe index rather than actual losses, then basis risk exists. Table 7

shows how basis risks affect the value of reinsurance contracts in the situation of

reinsurance companies issuing hybrid CAT bonds. Table 8 shows the corresponding

default risk premium under the same situation.

[Insert Table 7]

[Insert Table 8]

Table 7 shows that when the correlation between catastrophe losses underwritten

by reinsurance companies and composite index of losses is low, reinsurance

companies face higher basis risk. When the correlation coefficient is 1, basis risk does

not exist, and the reinsurance contract values are the same as those shown in Table 6

under the same condition. The standard deviation between reinsurance contract value

with other different correlations and those with correlation of 1 is viewed as the basis

risk premium. Under correlation of 0.3, 0.5, or 0.8, we observe that basis risks

reduced reinsurance contract value and increased default risk premium. The level of

decline in value increased following the increase in basis risk, catastrophe frequency,

and standard deviation of losses. For example, with catastrophe frequency equals to 2,

standard deviations of actual loss and composite index of reinsurance companies are

both equal to 2, trigger level equals 80, and initial capital position equals 1.1, when

correlation dropped from 0.8 to 0.5, the reinsurance contract subtracted (default risk

premium added) 37.6 basis points in value. As correlation continued to decline from

0.5 to 0.3, the reinsurance contract continued to loss (or default risk premium gained)

27.9 basis points in value. It should be noted that basis risk premium reduces with the

increase in trigger level and initial financial position, but increases with the increase

in standard deviation of catastrophe frequency. Although basis risk premium is

significant, compared to issuance of hybrid CAT bond, the impact on increasing the

value of reinsurance contracts is less significant.

Next, we made comparisons to see whether hybrid CAT bonds are still better at

raising the value of reinsurance contracts when basis risk is considered. First,

comparison between reinsurance contract values in Table 4 and 7 showed that hybrid

CAT bonds could raise the value of reinsurance contracts even more than CAT bonds.

The difference between the value of hybrid CAT bond reinsurance contracts and that

of CAT bond reinsurance contracts under other different correlations can be attributed

to the effect of hybrid CAT bonds. We were able to observe the result of basis risk in

reducing the effect of hybrid CAT bonds. The degree of decline in effect increases as

basis risk increases. For example, when catastrophe frequency was 2, standard

deviations of actual and composite index of losses of reinsurance companies were

21

both 2, trigger level was 80, initial capital position ratio was 1.1, and when correlation

dropped from 0.8 to 0.5, the value of hybrid CAT effect drops by 25 basis points.

When correlation continues to drop from 0.5 to 0.3, the value of hybrid CAT bonds

effect will also continue to drop by 18.6 basis points. We also observed that the

impact of hybrid CAT bonds reduces with the increase in trigger level and initial

financial position, but increases with the increase in standard deviation of catastrophe

frequency. Based on the above analysis, we learn that despite the consideration of

basis risk, hybrid CAT bonds are more able to enhance the value of reinsurance

contracts than CAT bonds.

4.4 Issuance comparison in terms of percentage increase in ROL

Table 9 shows the comparison of percentage increase in the value of reinsurance

contracts because of issuance of CAT bonds and hybrid CAT bonds under various

catastrophe frequency and standard deviation conditions. First, in defining the rate of

increase in issuance value, the numerator is defined as the increase in value of

reinsurance contracts because of issuance of CAT bonds or hybrid CAT bonds, the

denominator is defined as no default risk reinsurance contract value under specific

catastrophic conditions, and is expressed as follows:

[Insert Table 9]

Rate of increase in issuance value = increase in issuance value /no default risk ROL

For example, when standard deviation of catastrophe frequency is 2 and value of

reinsurance contract with no default risk is 0.29939, the issuance value of CAT bonds

with trigger level of 80 will increase by 61.7 basis points and the rate of increase with

CAT bond issuing is 0.00617/0.29939 = 2.06%. Table 9 shows that when standard

deviation of catastrophe frequency is 0.5, regardless of what security is issued, there is

no real effect on raising the value of reinsurance contracts. In other catastrophic

circumstances, regardless of CAT bonds or hybrid CAT bonds, when standard

deviation of catastrophe frequency becomes greater, the rise in the rate of increase of

reinsurance contract value also becomes greater. It means that when catastrophic

impact is more serious, the catastrophe-linked securities issued by reinsurance

companies can more rapidly raise the value of reinsurance contracts. In other words,

the effect of issuing these securities to increase the value of reinsurance contracts will

lead to the rise of rate of increase with growing severity of catastrophic events. For

example, when standard deviation of catastrophe frequency is 2, trigger level is 80,

and initial capital structure is 1.1, and when the rate of increase in catastrophe

frequency rises from 0.5 to 2, then the rate of increase in issuance value of CAT bonds

will rise from 1.96% to 2.06% and the rate of increase in the value of hybrid CAT

bonds will rise from 5.89% to 6.2%. When initial capital position are high, the rate of

22

increase in the issuance value will drop. For example, when the standard deviation of

catastrophe frequency is 2 and trigger level is 80, and when initial capital ratio

increases from 1.1 to 1.5, the rate of increase in issuance value of CAT bonds will

drop from 2.06% to 2.02% and the rate of increase in the issuance value of hybrid

CAT bonds will drop from 6.20% to 5.81%. When trigger levels become higher, the

rate of increase in the issuance value will decline. For example, when the standard

deviation of catastrophe frequency is 2 and opening capital ratio is 1.1, the rate of

increase in issuance value of CAT bonds will decline from 2.06% to 1.34% and the

rate of increase in issuance value of hybrid CAT bonds will decline from 6.20% to

4.03%.

Hybrid CAT bonds are made up of CAT bonds and CatEPuts, thus the effect of

hybrid CAT bonds on raising the value of reinsurance contracts is stronger than CAT

bonds. For example, when standard deviation of catastrophe frequency is 2, trigger

level is 80, and initial capital ratio is 1.1, the rate of increase in issuance value of

hybrid CAT bonds (6.20%) is larger than that of CAT bonds (2.06%). The difference

in the rate of increase in issuance value of both bonds is the CatEPut effect. The above

analysis shows that the issuance of hybrid CAT bonds is better in raising the rate of

increase in the value of reinsurance contracts than CAT bonds.

5. Conclusion

The hybrid CAT bonds proposed in this study can provide an effective solution to

address problems arising from insufficient valuation of catastrophe reinsurance

contracts faced by reinsurance companies and insufficient hedging made by these

reinsurance companies during catastrophic events. The study developed a reinsurance

contract valuation model designed to measure default risk, basis risk, catastrophe risk,

and interest rate risk that can also monitor as to how reinsurance companies raise the

value of reinsurance contracts by way of issuance of CAT bonds or hybrid CAT bonds.

In addition, the study adopted the concept of hybrid products proposed by Pauline and

Henri (2009) to create a type of hybrid CAT bonds composed of CAT bonds and

CatEPuts. The results showed that default risk premium has a significant value in

most cases involving catastrophic risk, and should not be ignored when evaluating

reinsurance contracts. The results also showed that the issuance of CAT bond and

hybrid CAT bond products could reduce default risk premium and increase the value

of the reinsurance contracts. Under condition of high catastrophe frequency, high

catastrophe losses, low capital position, and low trigger levels, the issuance of CAT

bonds and hybrid CAT bonds have a significant effect on raising the value of

reinsurance contracts. Basis risk will increase default risk premium and reduce the

23

value of reinsurance contract. The effect of basis risk will decrease with the increase

in reinsurance companies' initial capital structure ratios and trigger levels, but will

increase with the increase in catastrophe frequency and standard deviation of losses.

However, after considering all the factors, regardless of whether the issuance is CAT

bonds or hybrid CAT bonds, the impact on reinsurance contract is greater than that

from basis risk. In other words, even with potential basis risk, CAT bond or hybrid

CAT bond issuance are still able to reduce the default risk of reinsurance companies

and thus increase the value of reinsurance contracts.

The study assumes a completely efficient stock market truly reflects the equity

value of reinsurance companies. We found that, similar to designs of CAT bond

products, hybrid CAT bond combination product design is more able at reducing

default risk premiums than CAT bond single product design, thereby increasing the

value of reinsurance contracts even further. The reason is that combination type

products could attract additional capital injections as opposed to single type products.

This type of insurance-linked product design not only can increase the issuance

volume in risk capital market (Pauline and Henri, 2009), but the issuance of hybrid

CAT bond products can mitigate catastrophe risk faced by reinsurance companies

despite the existence of basis risk, as the study found.

24

Reference

Aiuppa, Thomas A., Robert J. Carney, and Thomas M. Krueger, 1993, " An Examination of Insurance

Stock Prices Following the 1989 Loma Prieta Earthquake ", Journal of Insurance Issues and Practices,

16: 1-14.

Barrieu, P. and H. Louberg (2009). "Hybrid Cat Bonds." Journal of Risk & Insurance 76(3): 547-578.

Bowers, N.L., Gerber, J.H.U., J.C., Jones, D.A., Nesbitt, C.J., 1986. Actuarial Mathematics. Society of

Actuaries, Itasca, Ill.

Chang, C., Chang, J.S., Krinsky, I., 1989. " On the derivation of reinsurance Premiums. " Insurance:

Mathematics and Economics 8(2), 137-144.

Chang, C., Chang, J.S., Yu, M,-T., 1996. " Pricing catastrophe insurance futurescall spreads: A

randomized operational time approach." Journal of Risk and Insurance 63, 599-617.

Chia-Chien, C., L. Shih-Kuei, et al. (2011). "Valuation of Catastrophe EquityPuts With

Markov-Modulated Poisson Processes." Journal of Risk & Insurance 78(2): 447-473.

Cox, S. H., J. R. Fairchild, et al. (2004). "Valuation of structured risk management products." Insurance:

Mathematics & Economics 34(2): 259.

Croson, D. C., Kunreuther, H. C., 2000. Customizing indemnity contracts and indexed cat bonds for

natural hazard risks. Journal of Risk and Insurance Finance 1, 24-41.

Cox, J., Ingersoll, J., Ross, S., 1985. " The term structure of interest rates." Econometrica 53, 385-407.

Cox, S.H., Pederson, H.W., 2000. Catastrophe risk bonds. North American Actuarial Journal 4, 56-82.

Cox, S. H., Schwebach, R.G., 1992. Insurance futures and hedging insurance price risk. Journal of Risk

and Insurance 59, 628-644.

Cummins, J. D. (2008). "CAT Bonds and Other Risk-Linked Securities: State of the Market and Recent

Developments." Risk Management & Insurance Review 11(1): 23-47.

Cummins, J. D. and M. A. Weiss (2009). "Convergence of Insurance and Financial Markets: Hybrid

and Securitized Risk-Transfer Solutions." Journal of Risk & Insurance 76(3): 493-545.

Cummins, J. D., 1988. Risk-based premiums for insurance guaranty funds. Journal of Finance 43,

593-607.

Cummins, J. D., Doherty, N.,Lo, A., 2002. Can insurers pay for the “big one”? Measuring the capacity

of insurance market to respond to catastrophe losses. Journal of Banking and Finance 26, 557-583.

Cummins, J. D Lalonde, D., Phillips, R.D., 2004. The basis risk of catastrophic-loss index securities.

Journal of Financial Economics 71, 77-111.

Cummins, J.D., Lewis, C.M., Phillips, R.D., 1999. Pricing excess of loss reinsurance contracts against

catastrophic loss. In: Froot, K. (Ed.), The Financial of Catastrophe Risk. The University of Chicago

Press, Chicago.

Cummins, J.D., Geman, H., 1995. Pricing catastrophe futures and call spreads: An arbitrage approach.

Journal of Fixed Income (March), 46-57.

Davidson, Wallace N. III, P. R. Chandy, and Mark Cross, 1987, Large Losses Risk Management and

Stock Returns in the Airline Industry, Journal of Risk and Insurance, 54: 163-172.

25

Duan, J.-C., Moreau, A., Sealey, C.W., 1995. Deposit insurance and bank interest rate risk: Pricing and

regulatory implications. Journal of Banking and Finance 19, 1091-1108.

Duan, J., Simonato, J, 1999. Estimating and testing exponential-affine term structure models by

Kalman filter. Review of Quantitative Finance and Accounting 13, 111-135.

Duan, J. C., Yu, M.-T., 2005. Fair insurance guaranty premia in the presence of risk- based capital

regulations, stochastic interest rate and catastrophe risk. Journal of banking and Finance 29(10),

2435-2454.

Finken, S. and C. Laux (2009). "Catastrophe Bonds and Reinsurance: The Competitive Effect of

Information-Insensitive Triggers." Journal of Risk & Insurance 76(3): 579-605.

Froot, K.A. (Ed.), 1999. The Financing of Catastrophe risk. University of Chicago Press, Chicago.

Froot, K.A., 2001. The market for Catastrophe risk: A clinical examination. Journal of Financial

Economics 60 (2), 529-571.

Harrington, S.E., Niehaus, G., 1999. Basis risk with PCS catastrophe insurance derivative contracts.

Journal of Risk and Insurance 66, 49-82.

Harrington, S.E., Niehaus, G., 2003. Capital, corporate income taxes, and catastrophe insurance.

Journal of Financial Intermediation 12 (4), 365-389.

Härdle, W. K. and B. L. Cabrera (2010). "Calibrating CAT Bonds for Mexican Earthquakes." Journal

of Risk & Insurance 77(3): 625-650.

Jaimungal, S. and T. Wang (2006). "Catastrophe options with stochastic interest rates and compound

Poisson losses." Insurance: Mathematics & Economics 38(3): 469-483.

Lee, J.-P. and M.-T. Yu (2002). "PRICING DEFAULT-RISKY CAT BONDS WITH MORAL

HAZARD AND BASIS RISK." Journal of Risk & Insurance 69(1): 25-44.

Lee, J.-P. and M.-T. Yu (2007). "Valuation of catastrophe reinsurance with catastrophe bonds."

Insurance: Mathematics & Economics 41(2): 264-278.

Lewis, C.M., Murdock, K.C., 1996. The role of government contracts in discretionary reinsurance

market for natural disasters. Journal of Risk and Insurance 63, 567-597.

Lin, S.-K., C.-C. Chang, et al. (2009). "The valuation of contingent capital with catastrophe risks."

Insurance: Mathematics & Economics 45(1): 65-73.

Litzenberger, R.H., Beaglehole, D.R., Reynolds, C.E., 1996. Assessing catastrophe reinsurance-linked

securities as a new asset class. Journal of Portfolio Management 76-86 (special case).

Louberge, H., Kellezi, E., Gilli, M., 1999. Using catastrophe-linked securities to diversify insurance

risk: A financial analysis of CAT bonds. Journal of Insurance Issues 22, 125-146.

Merton, R., 1974. On the pricing of corporate debt: The risk structure of interest rates. Journal of

Finance 29 (2), 449-470.

Merton, R., 1976. Option pricing when underlying stock returns are discontinuous. Journal of Financial

Economies 3, 125-144.

Merton, R., 1977. An analytic derivation of the cost of deposit insurance and loan guarantee. Journal of

Banking and Finance 1,3-11.

26

Naik, V., Lee, M., 1990. General equilibrium pricing of options on the market portfolio with

discontinuous returns. Review of Financial Studies 3 (4), 493-521.

Niehaus, G. (2002). "The allocation of catastrophe risk." Journal of Banking & Finance 26(2/3): 585.

Pielke Jr., R.A., Landsea, C.W., 1989. Normalized hurricane damages in the United States: 1925-95.

Weather and Forecasting 13, 621-631.

Reilly, Frank K. and Eugene F. Drzycimski, 1973, Tests of Stock Market Efficiency Following Major

World Events, Journal of Business Research, 1:57-72.

Shelor, Roger M., Dwight C. Anderson, and Mark L. Cross, 1990, The Impact of the California

Earthquake on Real Estate Firms' Stock Value, Journal of Real Estate Research, 5: 335-340.

Shelor, Roger M., Dwight C. Anderson, and Mark L. Cross, 1992, Gaining from Loss:

Property-Liability Insurer Stock Values in the Aftermath of the 1989 California Earthquake, Journal of

Risk and Insurance, 5: 476-488.

Sprecher, C. Ronald and Mars A. Pertl, 1983, Large Losses, Risk Management and Stock Prices,

Journal of Risk and Insurance, 50: 107-117.

Vasicek, O.A., 1977. An equilibrium characterization of term structure. Journal of Financial Economics

5, 177-188.

Vaugirard, V.E., 2003. Pricing catastrophe bonds by an arbitrage approach. Quaterly Review of

Economics and Finance 43 (1), 119-132.

27

Table 1:

Parameters definitions and base values

Asset parameters Values

V

Vµ

Vφ

Vσ

,V tW

Reinsurer’s assets

Drift due to credit risk

Interest rate elasticity of asset

Volatility of credit risk

Wiener process for credit shock

0 0 1.1, 1.3, 1.5V L =

Irrelevant

-7, 0

5%

Interest rate parameters

r

κ

m

ν

rλ

,r tW

Initial instantaneous interest rate

Magnitude of mean-reverting force

Long-run mean of interest rate

Volatility of interest rate

Market price of interest rate risk

Wiener process for interest rate shock

5%

0.2

5%

10%

-0.01

Liability parameters

L

Lµ

Lφ

Lσ

,L tW

Reinsurer’s liabilities

Drift due to credit risk

Interest rate elasticity of liability

Volatility of credit risk

Wiener process for credit risk

100 不相關

-7, 0

0.05

Catastrophe loss parameters

λ

Cµ

,Index Cµ

Cσ

,Index Cσ

Cρ

( )N t

Catastrophe intensity

Mean of the logarithm of CAT losses for the insurer

Mean of the logarithm of CAT losses for the composite loss index

Standard deviation of the logarithm of CAT losses for the insurer

Standard deviation of the logarithm of CAT losses for the composite loss index

Correlation coefficient of the logarithm of CAT losses of the reinsurer and the

composite index

Poisson process for the occurrence of catastrophes

0.5,1,2

2

2

0.5 , 1 , 1.5

0.5 , 1, 1.5

0.3, 0.5, 0.8, 1

Other parameters

M

A

CATK

HybridK

CatEPutsE

rp

Cap level of loss paid by a reinsurance contract

Attachment level of a reinsurance contract

Trigger level in the CAT bond

Trigger level in the Hybrid CAT bond

Exercise price in the Hybrid CAT bond

The ratio of principal needed to be paid if debt forgiveness is triggered

100

20

80, 100, 120

80, 100, 120

10

0.5

28

Table 2: Values of reinsurance contracts (ROL) without issuing

( λ 、 Cσ ) Default-free ROL Default-risky ROL Default-risky premium

1.1 1.3 1.5 1.1 1.3 1.5

(0.5,0.5) 0.00298 0.00284 0.00297 0.00298 0.00013 0.00001 0.00000

(0.5,1) 0.02081 0.01709 0.01910 0.02016 0.00372 0.00171 0.00065

(0.5,2) 0.07886 0.05431 0.06320 0.07072 0.02455 0.01565 0.00814

(1,0.5) 0.01151 0.01079 0.01139 0.01150 0.00072 0.00012 0.00001

(1,1) 0.04870 0.03936 0.04418 0.04690 0.00934 0.00452 0.00180

(1,2) 0.15552 0.10666 0.12423 0.13932 0.04886 0.03129 0.01620

(2,0.5) 0.04865 0.04422 0.04771 0.04850 0.00443 0.00094 0.00015

(2,1) 0.12512 0.09885 0.11203 0.11983 0.02627 0.01309 0.00529

(2,2) 0.29939 0.20306 0.23700 0.26649 0.09633 0.06239 0.03290

This table presents the ROLs for alternative sets of catastrophe intensities (λ) and catastrophe loss volatilities ( Cσ ) for default

free and default risky reinsurance contracts. The difference of their values are the default risk premiums.

V/L represents the initial asset–liability structure or capital position of the reinsurers.

All estimates are computed using 20,000 simulation runs.

29

Table 3: Values of reinsurance contracts (ROL) with CAT bonds but no basis risk

( , )C

λ σ Contract value (ROL) Default risk premium

1.1 1.3 1.5 1.1 1.3 1.5

80CAT

K =

(0.5,0.5) 0.00284 0.00297 0.00298 0.00013 0.00001 0.00000

(0.5,1) 0.01723 0.01924 0.02030 0.00358 0.00157 0.00052

(0.5,2) 0.05586 0.06475 0.07223 0.02300 0.01411 0.00663

(1,0.5) 0.01079 0.01139 0.01150 0.00072 0.00012 0.00001

(1,1) 0.03971 0.04454 0.04724 0.00899 0.00416 0.00146

(1,2) 0.10976 0.12733 0.14233 0.04577 0.02819 0.01319

(2,0.5) 0.04425 0.04774 0.04852 0.00440 0.00092 0.00013

(2,1) 0.09992 0.11309 0.12084 0.02520 0.01202 0.00428

(2,2) 0.20924 0.24318 0.27253 0.09016 0.05621 0.02686

100CAT

K =

(0.5,0.5) 0.00284 0.00297 0.00298 0.00013 0.00001 0.00000

(0.5,1) 0.01718 0.01918 0.02024 0.00364 0.00163 0.00057

(0.5,2) 0.05562 0.06451 0.07202 0.02324 0.01435 0.00684

(1,0.5) 0.01079 0.01139 0.01150 0.00073 0.00012 0.00001

(1,1) 0.03957 0.04439 0.04711 0.00913 0.00431 0.00159

(1,2) 0.10931 0.12688 0.14194 0.04621 0.02864 0.01358

(2,0.5) 0.04423 0.04771 0.04850 0.00442 0.00094 0.00015

(2,1) 0.09943 0.11261 0.12042 0.02569 0.01251 0.00470

(2,2) 0.20843 0.24238 0.27182 0.09097 0.05702 0.02757

120CAT

K =

(0.5,0.5) 0.00284 0.00297 0.00298 0.00013 0.00001 0.00000

(0.5,1) 0.01713 0.01914 0.02019 0.00369 0.00168 0.00062

(0.5,2) 0.05526 0.06416 0.07167 0.02360 0.01470 0.00719

(1,0.5) 0.01078 0.01139 0.01150 0.00073 0.00012 0.00001

(1,1) 0.03943 0.04425 0.04697 0.00928 0.00445 0.00173

(1,2) 0.10867 0.12624 0.14131 0.04685 0.02928 0.01421

(2,0.5) 0.04422 0.04771 0.04850 0.00443 0.00094 0.00015

(2,1) 0.09902 0.11220 0.12001 0.02610 0.01292 0.00511

(2,2) 0.20708 0.24103 0.27050 0.09231 0.05836 0.02890

This table presents ROLs with CAT bond issuance, but no basis risk. ROLs are calculated and reported for alternative sets of

trigger values ( CATK ),

catastrophe intensities (λ), and catastrophe loss volatilities ( Cσ ). The default risk premium represents the difference in the

values of reinsurance

contracts with CAT bond issuance and risk free reinsurance contracts.

V/L represents the initial asset–liability structure or capital position of the reinsurers.

All estimates are computed using 20,000 simulation runs.

30

Table 4: Values of reinsurance contracts (ROL) with CAT bonds and basis risk

Trigger( CATK ) 80 100 120

Cρ 0.3 0.5 0.8 0.3 0.5 0.8 0.3 0.5 0.8

( , , )C indexλ σ σ / 1.1V L =

(0.5,0.5,0.5) 0.00284 0.00284 0.002844 0.00284 0.00284 0.00284 0.00284 0.00284 0.00284

(0.5,1,1) 0.01712 0.01716 0.01721 0.01710 0.01712 0.01716 0.01710 0.01710 0.01712

(0.5,2,2) 0.05491 0.05516 0.05555 0.05476 0.05499 0.05535 0.05457 0.05477 0.05503

(1,0.5,0.5) 0.01079 0.01079 0.01079 0.01079 0.01079 0.01079 0.01079 0.01079 0.01079

(1,1,1) 0.03946 0.03955 0.03968 0.03939 0.03945 0.03954 0.03937 0.03938 0.03941

(1,2,2) 0.10798 0.10850 0.10925 0.10767 0.10813 0.10881 0.10732 0.10770 0.10826

(2,0.5,0.5) 0.04424 0.04425 0.04425 0.04422 0.04423 0.04423 0.04422 0.04422 0.04422

(2,1,1) 0.09924 0.09954 0.09984 0.09901 0.09919 0.09938 0.09888 0.09892 0.09900

(2, 2,2) 0.20618 0.20711 0.20837 0.20552 0.20638 0.20756 0.20464 0.20534 0.20633

/ 1.3V L =

(0.5,0.5,0.5) 0.00297 0.00297 0.00297 0.00297 0.00297 0.00297 0.00297 0.00297 0.00297

(0.5,1,1) 0.01913 0.01917 0.01922 0.01911 0.01913 0.01917 0.01911 0.01911 0.01913

(0.5,2,2) 0.06380 0.06406 0.06445 0.06366 0.06389 0.06425 0.06347 0.06366 0.06393

(1,0.5,0.5) 0.01139 0.01139 0.01139 0.01139 0.01139 0.01139 0.01139 0.01139 0.01139

(1,1,1) 0.04429 0.04437 0.04450 0.04422 0.04428 0.04436 0.04419 0.04421 0.04424

(1,2,2) 0.12555 0.12607 0.12682 0.12524 0.12570 0.12638 0.12489 0.12527 0.12583