AUTOFACTS Global Automotive Outlook

VW Group Strategic Analysis:A Company in Transition

2002 Q1 Quarterly Executive Briefing

2© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

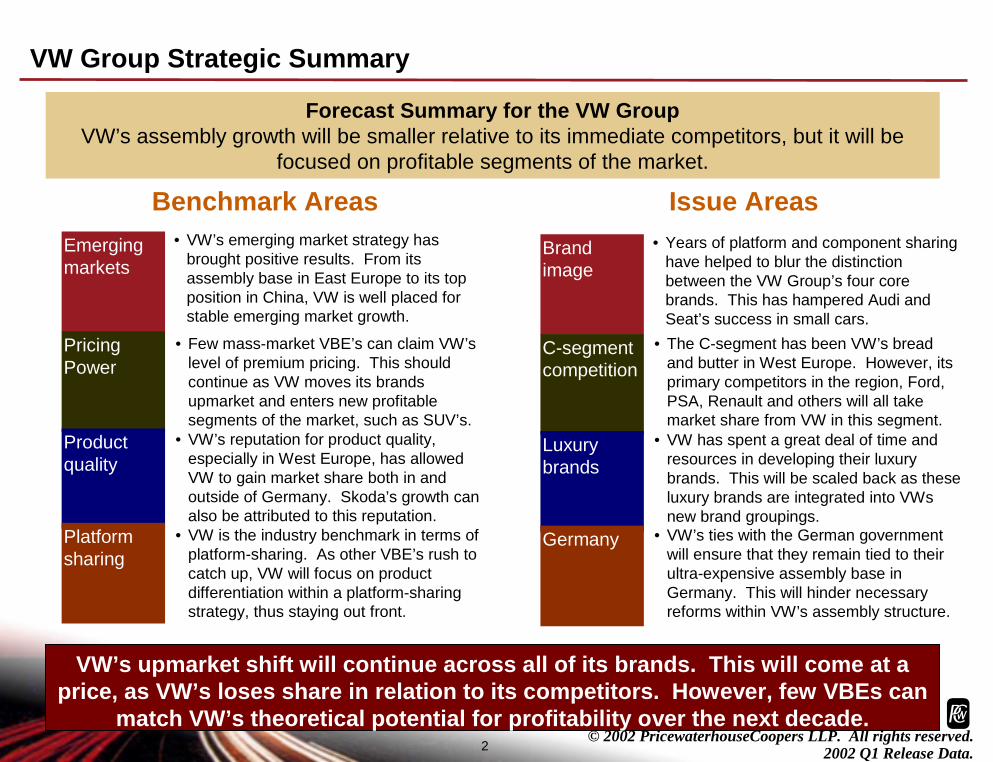

VW Group Strategic Summary

Brand image

C-segment competition

Luxury brands

Germany

Forecast Summary for the VW GroupVW’s assembly growth will be smaller relative to its immediate competitors, but it will be

focused on profitable segments of the market.

• Years of platform and component sharing have helped to blur the distinction between the VW Group’s four core brands. This has hampered Audi and Seat’s success in small cars.

VW’s upmarket shift will continue across all of its brands. This will come at a price, as VW’s loses share in relation to its competitors. However, few VBEs can

match VW’s theoretical potential for profitability over the next decade.

Issue AreasBenchmark AreasEmerging markets

Pricing Power

Product quality

Platform sharing

• VW’s emerging market strategy has brought positive results. From its assembly base in East Europe to its top position in China, VW is well placed for stable emerging market growth.

• The C-segment has been VW’s bread and butter in West Europe. However, its primary competitors in the region, Ford, PSA, Renault and others will all take market share from VW in this segment.

• VW has spent a great deal of time and resources in developing their luxury brands. This will be scaled back as these luxury brands are integrated into VWsnew brand groupings.

• VW’s ties with the German government will ensure that they remain tied to their ultra-expensive assembly base in Germany. This will hinder necessary reforms within VW’s assembly structure.

• Few mass-market VBE’s can claim VW’slevel of premium pricing. This should continue as VW moves its brands upmarket and enters new profitable segments of the market, such as SUV’s.

• VW’s reputation for product quality, especially in West Europe, has allowed VW to gain market share both in and outside of Germany. Skoda’s growth can also be attributed to this reputation.

• VW is the industry benchmark in terms of platform-sharing. As other VBE’s rush to catch up, VW will focus on product differentiation within a platform-sharing strategy, thus staying out front.

3© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

News: VW’s Brand Restructuring

One of the first changes introduced by Chairman-elect Pischetrieder was a drastic reorganisation of VW’s brands into two distinct groupings.

• The “Classic” brand group includes:➤ Volkswagen➤ Skoda➤ Bentley➤ Bugatti

• The “Sporty” brand group includes:➤ Audi➤ Seat➤ Lamborghini

• This reorganisation will allow VW’s brands to better attain the market images they have sought to create for each individual brand

➤ Witness Seat which has been hampered in its quest to become “the Spanish Alfa Romeo” by its close relationship with Volkswagen and Skoda

VW Group Global Competitive Context

5© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW remains committed to achieving profitable sales growth

in North America and West Europe while increasing

assembly in emerging markets.

VW: Global Competitive Context

The VW Group will be the smallest of the G6 by 2009

• VW is looking to steady, profitable growth in emerging markets

• VW is consolidating its leading position in West Europe

➤ all this will help ensure that VW remains one of the most profitable VBEs in the world

VW’s size makes it a potential take-over target of one of the larger VBEs

• The Niedersachsen government (a 20% shareholder in VW) gives VW a degree of security against a take-over bid

➤ However, the European Union is considering legislation to outlaw these types of “poison pills” in the future

• For a VBE looking to strengthen its long-term position in Europe, there is no more attractive target than VW

0

2,00

0

4,00

0

6,00

0

8,00

0

10,0

00

12,0

00

14,0

00

16,0

00Units (000)

BMW Group

Hyundai Group

Honda Group

PSAGroup

VW Group

Renault-Nissan

DCX Group

Toyota Group

Ford Group

GM Group

Global Light Vehicle Assembly

2001 2009

6© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW Group Global Light Vehicle Assembly & Capacity

2

3

4

5

6

7

8

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Uni

ts (m

illio

ns)

60%

65%

70%

75%

80%

85%

90%

Capacity

Assembly

Utilization

VW Group Structural Overview

Excess Capacity

VW will improve their asset utilization through a small-scale rationalization in assembly facilities. What capacity expansion is undertaken will occur in areas

where VW is already operating at near full capacity, such as Central Europe.

Utilization Rate

VW Group Assembly Volume and Share of Global Assembly

0.00

2.00

4.00

6.00

1990

1993

1996

1999

2002

2005

2008

Mill

ions

of U

nits

5%

6%

7%

8%

9%

10%

11%

% S

hare

Assembly

Assembly Share

VW Group: Globalisation Strategy

8© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW Group Globalisation Strategy

West Europe• VW is aggressively gaining market share in West Europe’s main markets outside of

Germany➤ Skoda and Seat are seen as key competitors for brands such as Peugeot, Renault and

Fiat in France, Spain, Italy and the UK

East Europe• VW will finally be tempted by the riskier markets of Russia and Ukraine

➤ Central Europe, however, will remain a key facet of the group’s European assembly plans

North America• VW will continue to seek profitable growth through Audi and VW products such as

the new Tuareg SUVSouth America

• The Seat brand will play an key role in VW’s regional growth strategyAsia-Pacific

• VW will continue to focus on China➤ Their flirtation with India will remain little more than that over the near term.

9© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW Group Share by Region, 1990-2009

Since acquiring Skoda in 1991, VW has focused on East Europe as a centre of assembly for exports to West Europe.

Share of Region Assembly

0%

5%

10%

15%

20%

25%

30%

APEEMEANASAWE

20091990

Volume and Share Change

-500 -250 0 250 500 750 1000

AP

EE

MEA

NA

SA

WE

Units (000)

-0.1 -0.05 0 0.05 0.1 0.15 0.2

Share Points

VolumeChangeShareChange

VW Group: Brand/Partner Strategies

11© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

0

100

200

300

400

500

600

2001 2009

Units

(000

)

0

100

200

300

400

500

600

2001 2009

Units

(000

)

0

1000

2000

3000

4000

5000

2001 2009

Units

(000

)

VW Group Brand Relationship MapIm

age,

Pric

ing

Pow

er

VW VBE

Low-Cost Mass-Market Upscale LuxuryBrand Type:N/A

Skoda

SEAT

VW

Audi

= Primary target market for brand= Secondary target market

• VW has a plethora of upmarket brands in the shape of Bugatti, Bentley and Lamborghini

• All appeal to different market segments

• Having the brands in the stable intended to help VW in its strategy to increase pricing power for each of its mainstream brands

Bugatti/Bentley/

Lamborghini0

100

200

300

400

500

600

700

800

900

2001 2009

Units

(000

) 0

20

2001 2008

Units

(000

)

12© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

Market Competitiveness2001-2008

-8%

-4%

0%

4%

8%

12%

16%

-50% 0% 50% 100% 150%Contribution to Growth

Cha

nge

%

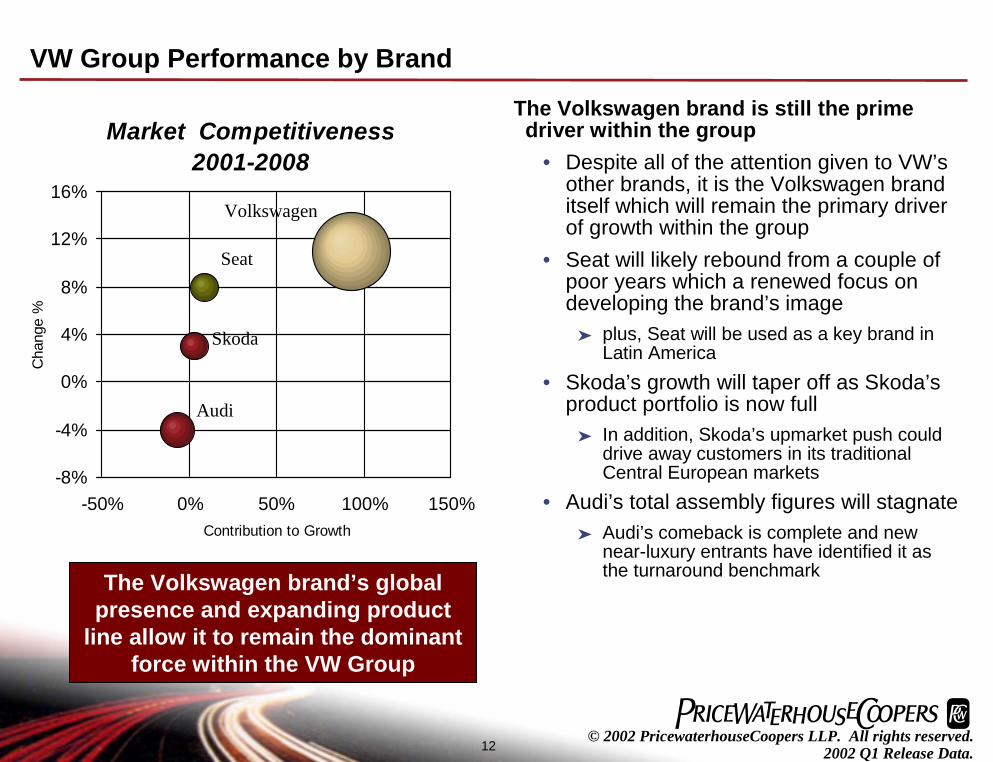

VW Group Performance by Brand

Seat

Volkswagen

Audi

The Volkswagen brand is still the prime driver within the group

• Despite all of the attention given to VW’sother brands, it is the Volkswagen brand itself which will remain the primary driver of growth within the group

• Seat will likely rebound from a couple of poor years which a renewed focus on developing the brand’s image

➤ plus, Seat will be used as a key brand in Latin America

• Skoda’s growth will taper off as Skoda’sproduct portfolio is now full

➤ In addition, Skoda’s upmarket push could drive away customers in its traditional Central European markets

• Audi’s total assembly figures will stagnate➤ Audi’s comeback is complete and new

near-luxury entrants have identified it as the turnaround benchmarkThe Volkswagen brand’s global

presence and expanding product line allow it to remain the dominant

force within the VW Group

Skoda

VW Group: Economies of Scale Strategy

14© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW High Volume Platform Snapshot

GM

DCXPSA

Renault

Toyota

Ford

VW

GM

Honda

DCX

PSARenault

ToyotaFord

VW

• VW is the leading proponent of the high volume platform strategy

• VW has one of the industries most co-ordinatedmultibrandstrategies

• 11 key modules is a well-developed platform strategy by any other name - separation into “Sporty” and “Classic” key tool in argument against cannibalisation and the next stage in VW’s competitive advantage

Honda

HVPs in 2001

0 1,000 2,000 3,000

AO3

B5

A4

Units (000)

HVPs in 2009

0 1000 2000 3000

B5

AO4

A5

Units (000)

AssemblyExcess Capacity

AssemblyExcess Capacity

2001

0

5

10

0% 50% 100%% of Total Capacity

Milli

ons

of U

nits

2009

0

5

10

0% 50% 100%% of Total Capacity

Milli

ons

of U

nits

15© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW Portfolio Performance – High-Volume Platforms

VW’s global strategy of using three main platforms for the majority of their assembly volume will continue. The only deviations will continue to be for niche

products and older models for emerging markets.

High-Volume Platforms, 2009

0

1.5

3

60% 80% 100%Utilization Rate

Mill

ions

of U

nits

of C

apac

ity

High-Volume Platforms, 2009

A5

AO4

B5

6

9

12

4 7 10Number of Nameplates

Num

ber o

f Bod

ysty

le V

aria

nts

EffectivenessFlexibility

A5

AO4

B5

16© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW Use of High-Volume Engine Families -- Competitive State

GM

Honda

BMW

PSA

Renault

ToyotaFord

VW

DCX

GM

Honda

BMW

PSARenault

Toyota

Ford

VW

DCX

VW’s engine strategy is as simplified as its platform strategy: EA111 (82mm bore centre 3- and 4-cylinder gasoline engines), EA827/113 (88mm bore centre 4-, 6- and 8-cylinder gas engines), VR (65mm bore centre 4-, 5-, 6-, 8, 12 and 16-cylinder gas

engines) and the EA086/188 diesel engines

2001 VW’s Use of High-Volume Engine Families

0

5

10

0% 50% 100%Installation Rate

Milli

ons

of U

nits

2009 VBE Use of High-Volume Engine Families

0

5

10

0% 50% 100%Installation Rate

Milli

ons

of U

nits

VW was the early adopter of this

strategyAnother diminishing

structural competitive

advantage for VW

VW Group: Product Strategies

18© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

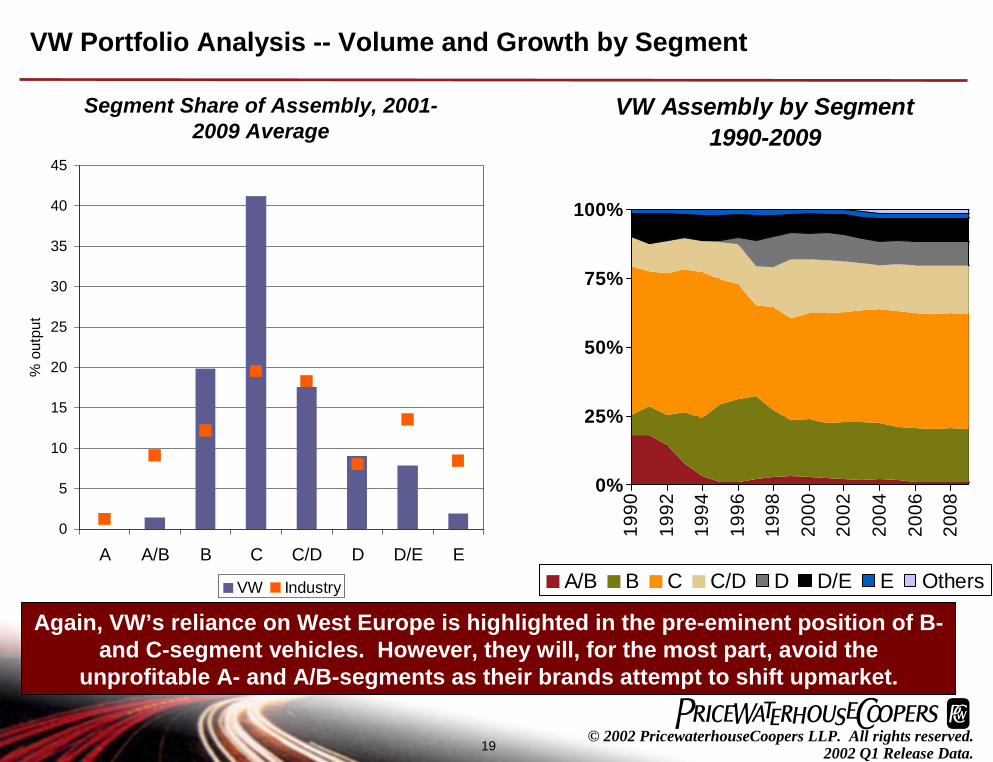

Segment Share of Assembly, 2001-2009 Average

VW Portfolio Analysis -- Volume and Growth by Segment

0

10

20

30

40

50

60

70

80

90

100

Car Van SUV Pickup

% o

utpu

t

VBE Industry

0%

25%

50%

75%

100%

1990 1992 1994 1996 1998 2000

VW Assembly by Segment 1990-2009

Car SUV Van Pickup

VW’s reliance on West Europe is highlighted by their dependence upon car assembly. As VW expands in Asia and the Americas, this will change, albeit slowly,

as seen in Volkswagen’s upcoming SUV.

19© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

Segment Share of Assembly, 2001-2009 Average

VW Portfolio Analysis -- Volume and Growth by Segment

0

5

10

15

20

25

30

35

40

45

A A/B B C C/D D D/E E

% o

utpu

t

VW Industry

0%

25%

50%

75%

100%

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

VW Assembly by Segment 1990-2009

A/B B C C/D D D/E E Others

Again, VW’s reliance on West Europe is highlighted in the pre-eminent position of B-and C-segment vehicles. However, they will, for the most part, avoid the

unprofitable A- and A/B-segments as their brands attempt to shift upmarket.

20© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

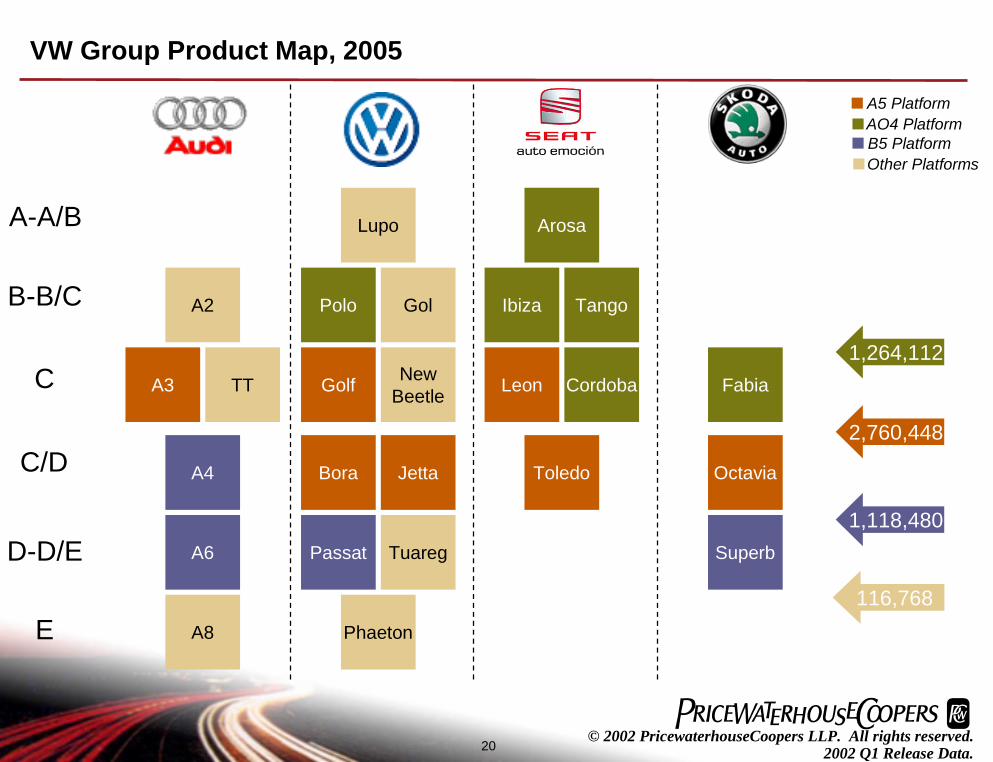

A-A/B

B-B/C

C

Arosa

Fabia

Ibiza

A3

A8

A6D-D/E

E

A2

Leon

Bora

Passat

Phaeton

Toledo Octavia

Superb

AO4 PlatformA5 Platform

Other PlatformsB5 Platform

1,264,112

2,760,448

1,118,480

C/D

VW Group Product Map, 2005

A4

Golf

Tuareg

TT Cordoba

TangoPolo

Jetta

New Beetle

Gol

Lupo

116,768

Lessons Learned: The VW Group’s Emerging Markets Strategy as a Benchmark

22© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW - The Automotive World’s Leader in Utilising Emerging Markets

VW’s use of Mexico as an assembly centre for the affluent North American market emulates their

strategy in East Europe

VW will continue to expand their presence in East Europe, hoping to

lessen their dependence on German labour

Thus far, VW has only set up major “build where you sell” facilities in two emerging markets, China and Brazil. Russia looks to be next.

23© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

VW - The Automotive World’s Leader in Avoiding Recent Troubles in Emerging Markets

VW’s focus on Brazil in South America has helped them to avoid most of the troubles in Argentina in

late 2001

In Asia, VW has avoided the troubles of the past five years by focusing their activities on high-

growth China

In the Middle East and Africa region, VW has focused their efforts on

establishing South Africa as a centre of export assembly to West Europe

VW has avoided the on-again/off-again joint venture negotiations

which most other major VMs have suffered through in Russia. Only

now are they exploring possibilities for a Russian assembly plant

VW has shown foresight and constraint in their emerging markets strategy over the past decade. By focusing on low-risk markets with either a probable market

expansion or a high export potential, VW is well positioned to avoid future shocks.

Key Takeaways

25© 2002 PricewaterhouseCoopers LLP. All rights reserved.

2002 Q1 Release Data.

Key Takeaways

VBE Name Key Success FactorsVBE Name Key

Success Factors• Brand Management

• VW’s reorganisation of their brand structure highlights the precarious situation they face in differentiating their core brands

• Upmarket Push• VW proposes to move not one,

but three core brands upmarket in the coming years

➤ while maintaining Audi’s current position

• Labour Flexibility• VW’s leading shareholder, the

government of Niedersachsen, makes it difficult for VW management to enact necessary assembly reforms

➤ too much of VW’s assembly is tied to the expensive and inflexible German labour market

• Brand Management• VW’s reorganisation of their

brand structure highlights the precarious situation they face in differentiating their core brands

• Upmarket Push• VW proposes to move not one,

but three core brands upmarket in the coming years

➤ while maintaining Audi’s current position

• Labour Flexibility• VW’s leading shareholder, the

government of Niedersachsen, makes it difficult for VW management to enact necessary assembly reforms

➤ too much of VW’s assembly is tied to the expensive and inflexible German labour market

How to Compete with VW

How to Compete with VW

• Brand Image• VW’s brands risk a blurring of

differentiation between them• Exploit the brands in your

portfolio with real weight➤ Before “pseudo” Alfa Romeo

succeeds

• Pricing• Weak at bottom end as Skoda

moves up• Product

• VW slow to react to any developing niches.

• Key Lesson• Despite plethora of “me-too”

VW-like products in West Europe in recent years only one company has really succeeded, that’s Skoda. Recent success stories have been Peugeot and Citroen -simply right price and the right product, with interiors that are functional and utilitarian

• Brand Image• VW’s brands risk a blurring of

differentiation between them• Exploit the brands in your

portfolio with real weight➤ Before “pseudo” Alfa Romeo

succeeds

• Pricing• Weak at bottom end as Skoda

moves up• Product

• VW slow to react to any developing niches.

• Key Lesson• Despite plethora of “me-too”

VW-like products in West Europe in recent years only one company has really succeeded, that’s Skoda. Recent success stories have been Peugeot and Citroen -simply right price and the right product, with interiors that are functional and utilitarian

Key Supplier OpportunitiesKey Supplier Opportunities

• HVPs and Modular Assembly

• VW has been an industry leader in this field

➤ Nearly 80% of VW’svehicles will come off of its three main platforms

• VW’s modular assembly strategy is designed to share eleven components across most products

• Expansion into non-European markets

• VW is counting on significant growth in North America, Brazil and China throughout this decade

➤ VW is exploring sites in Russia, Ukraine, India, US and Mexico

• HVPs and Modular Assembly

• VW has been an industry leader in this field

➤ Nearly 80% of VW’svehicles will come off of its three main platforms

• VW’s modular assembly strategy is designed to share eleven components across most products

• Expansion into non-European markets

• VW is counting on significant growth in North America, Brazil and China throughout this decade

➤ VW is exploring sites in Russia, Ukraine, India, US and Mexico