8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 1/160

TOUGH TIMES DON’T LAST...

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 2/160

TOUGH

COMPANIES DO!

2 0 1 1 - 2 0 1 2

A N N U A L R E P O R T

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 3/160

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 4/160

Corporate Governance. 48Remuneration Committee Report. 60

Audit Committee Report. 61

Risk Management. 63

CONTENTSMANAGEMENT REPORTS

MANAGEMENT DISCUSSION AND ANALYSIS

CORPORATE GOVERNANCE

Financial Highlights. 06 Chairman’s Review. 08

Managing Director’s Review. 14

Board of Directors. 22

Executive Committee. 25

Management Team. 25

Our People. 30Financial Review. 36

Financial Calendar. 45

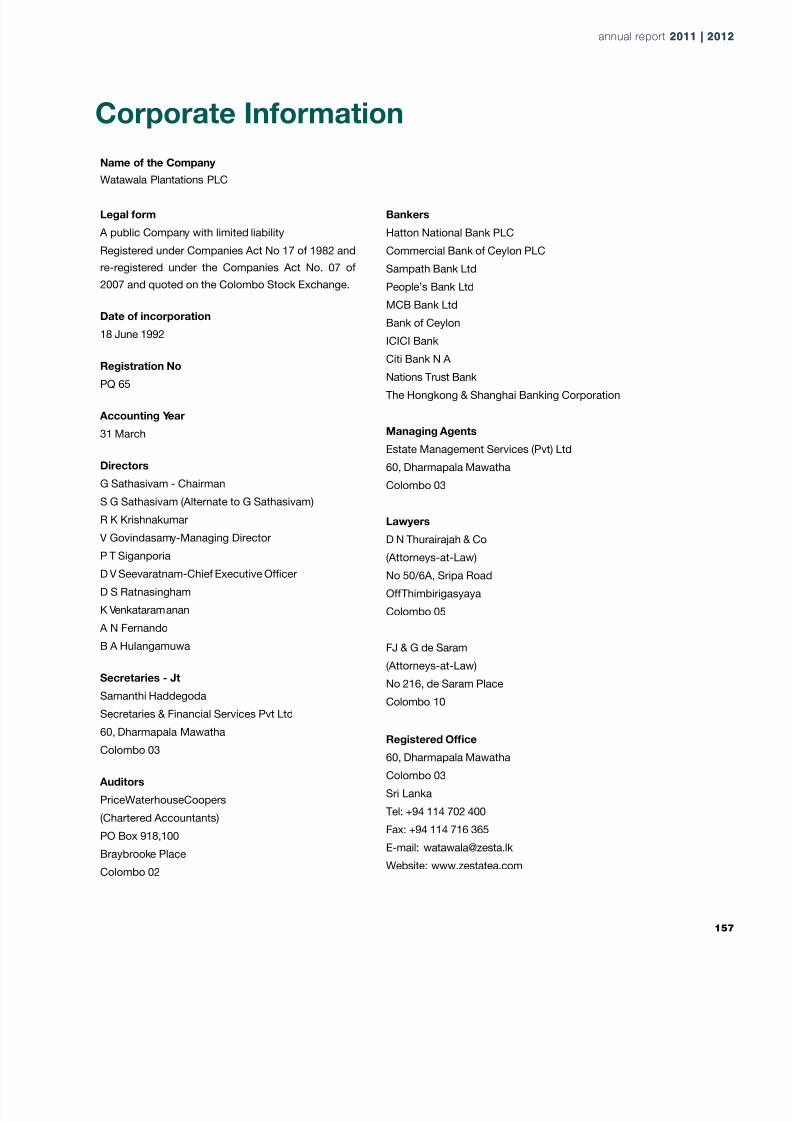

Watawala Plantations PLC

2

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 5/160

Value Added Statement. 142Sources and Utilisation of Income. 143

Estate Hectarage Statement. 144

Crops & Yields. 145

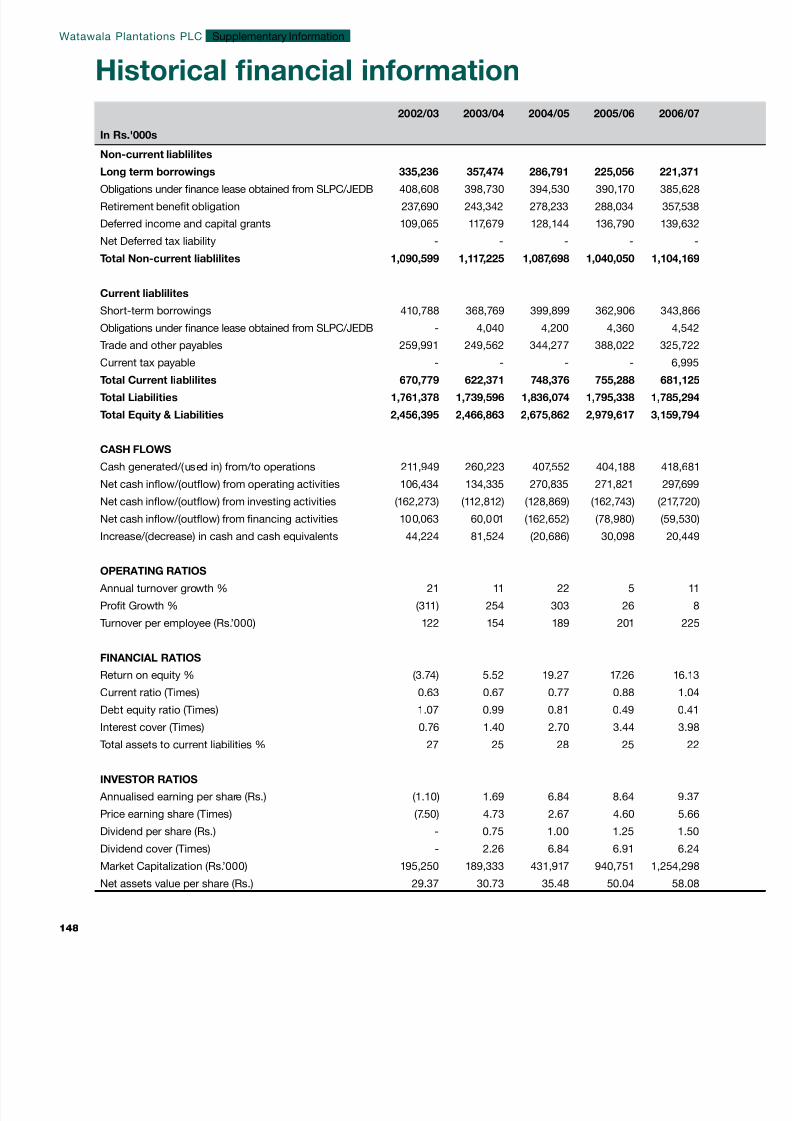

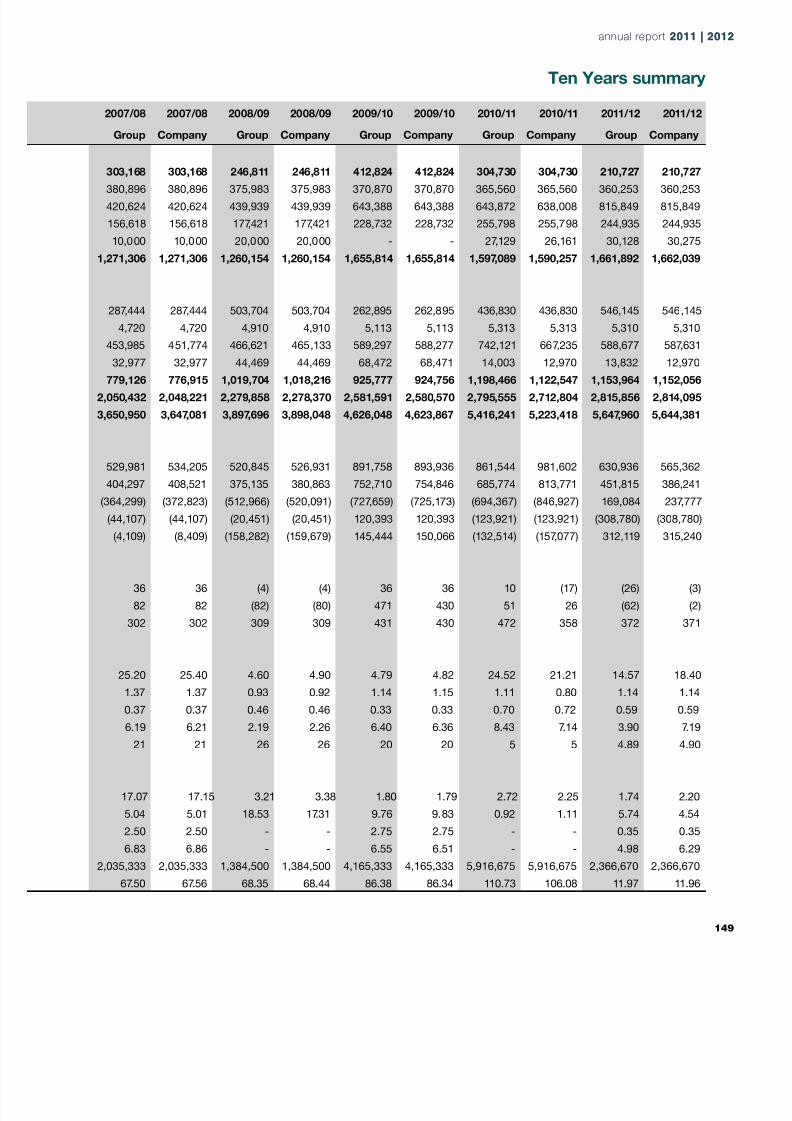

Historical Financial Information 10- Years

summary. 146

SUSTAINABILITY REPORT

FINANCIAL INFORMATION

SUPPLEMENTARY INFORMATION

Sustainability Report. 70GRI Content Index. 90

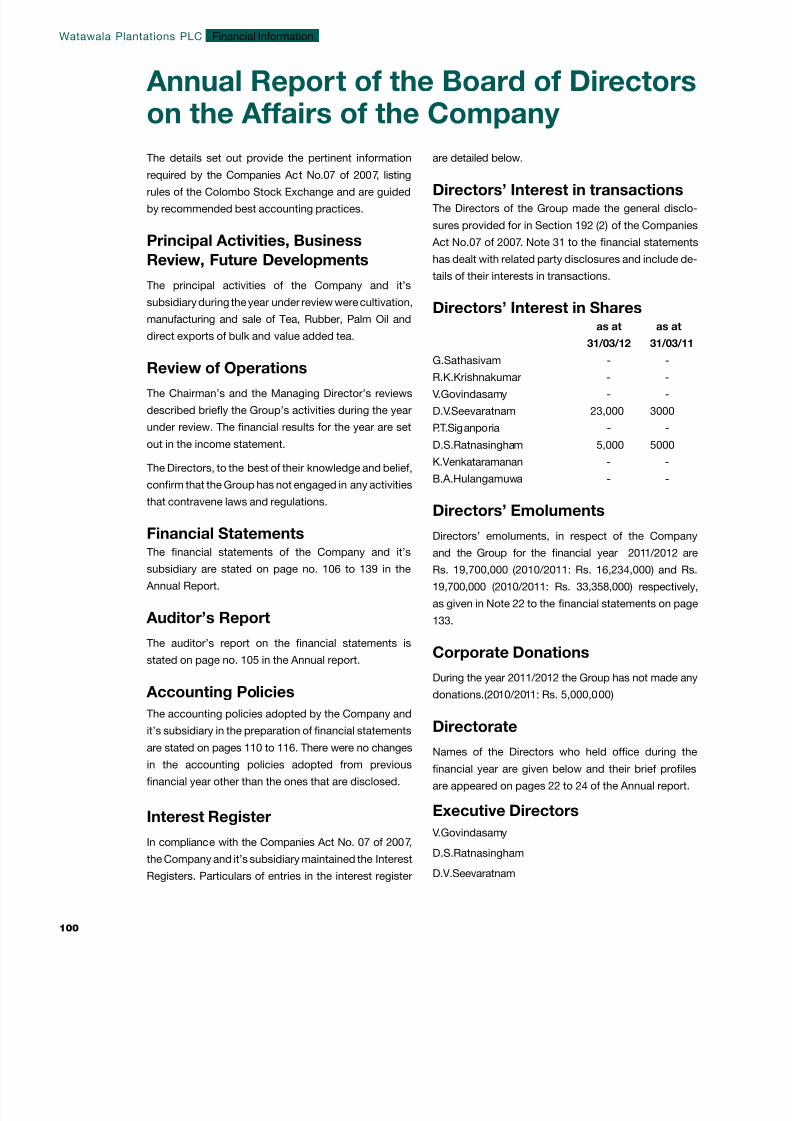

Annual Report of the Board of Directors on the Affairs of the Company. 100

Managing Director’s and Chief Financial

Ofcer’s Responsibility Statement. 103

Statement of Directors’ Responsibility. 104

Report of the Auditors. 105

Balance Sheet. 106Income Statement. 107

Statement of Changes in Equity. 108

Cash Flow Statement. 109

Accounting Policies & Notes to the

Financial Statements. 110

Shareholders’ & Investors’ Information. 150Glossary. 152

Notice of Meeting. 154

Form of Proxy. 155

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 6/160

IMPROVING

INFRASTRUCTURE

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 7/160

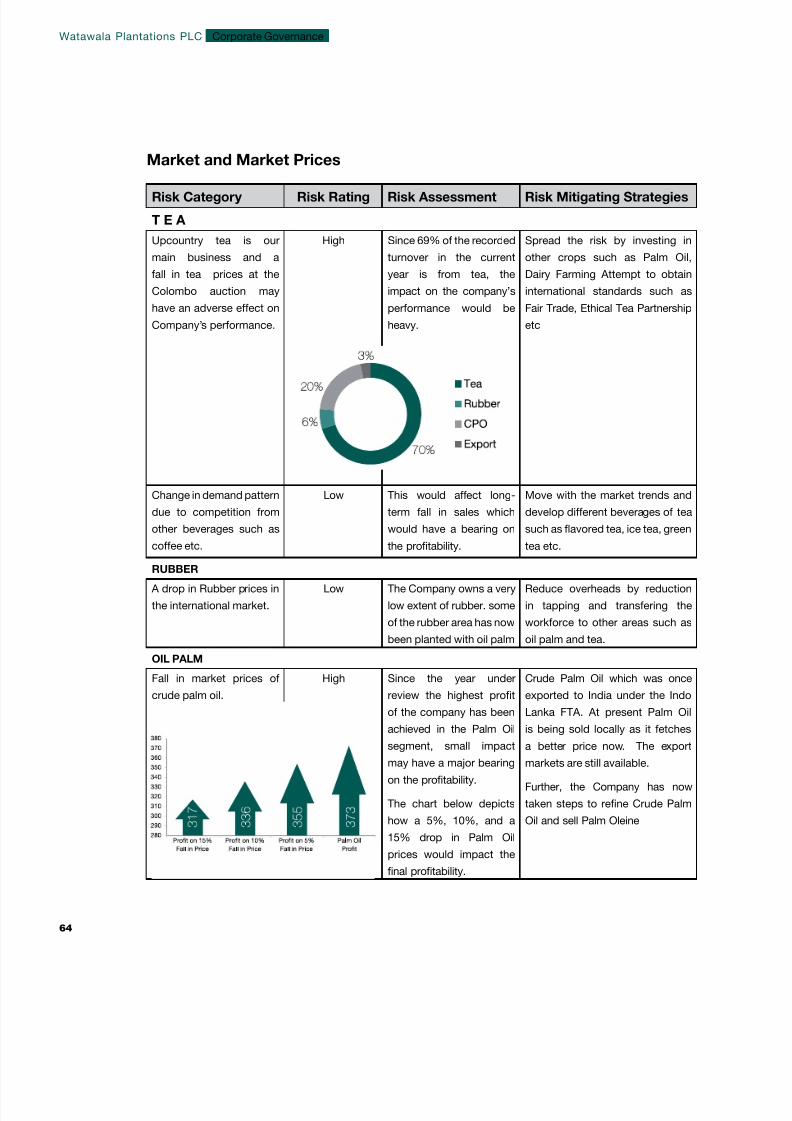

Financial Highlights - Year at a Glance

Chairman’s Review

Group Managing Director’s Review

Board of Directors

Group Executive Committee

Management Team

MANAGEMENT

REPORTS

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 8/160

FinancialHighlights 2011/12

In Rs. Millions 2011/2012 2010/2011 YoY - %

OperationsRevenue 4,532 4,664 -2.8%

Gross Prot 246 683 -63.9%

Operating Prot 610 612 -0.2%

Prot before Tax 525 527 -0.3%

Net Prot for the year 521 532 -2.2%

EBITDA 493 900 -45.2%

Balance SheetNon Current Assets 4,337 4,327 0.2%

Current Assets 1,308 896 46.9%

Equity 2,830 2,511 12.7%

Non Current Liabilities 1,662 1,590 4.5%

Current Liabilities 1,153 1,122 2.8%

Per Share dataEarning per Share (Rs.) 2.20 2.25 -2.2%

Dividend per Share (Rs.) 0.35 0.85 -58.8%

Dividend Cover (Times) 6.29 6.43 -2.2%

Shareholders’ InterestStated Capital 310 310 0.0%

Shareholders’ Funds 2,830 2,511 12.7%

Shareholders’ Funds per Share (Rs) 11.96 10.61 12.7%

Return on Shareholders’ Funds (%) 18% 21% -13.2%

LeverageInterest cost 85 85 -

Interest Cover (Times) 7.1 7.2 -1%

Non Current Borrowings 211 305 -31%

Current Borrowings 546 437 25%

Borrowings as a % of Equity 27% 30% -9%

The Sri Lankan plantation

sector is paramount

to the economy with a

contribution of 18% to the

national export revenue.

However in 2011 the

major commercial crops

tea, rubber and coconut

showed a sluggish

performance. The tea

industry was under severe

pressure due to European

crisis and Middle East

political conicts. The

future of Ceylon tea

comes with the challenge

of productivity and facing

competition that will likely

to be imposed by China,

Kenya and north east Indiawith low cost production.

We at Watawala

plantations have set

our vision on taking a

path which no other

would have walked in

and contemporaneously

looking forward to

re-shape the future of the

company grasping fruitful

opportunities lying ahead

to remain as the best

plantation company while

diversifying and building

up on our key strengths

‘people’ and ultimately

safe guarding the planet.

Future Trends

Segmental Revenue

Management ReportsWatawala Plantations PLC

6

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 9/160

Company ata glance 2011/12

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 10/160

Chairman’s Review

Global Economy

The world economy faced several signicant challenges during the year, due to

higher oil prices, a down turn in the Euro zone and an escalation of the geo political

tensions in the Middle East.

As per IMF’s latest estimates, world output is likely to grow by 3.25% in 2012compared to a 3.8% growth in 2011, whilst output in the Euro area is forecast to

decline by 0.5% in 2012 compared with a 1.6% increase in 2011. The strains felt by

the Euro economies began to intensify in the last quarter of 2011 and the area is

forecasted to be in mild recession in 2012, thus indicating that the demand from one

of Sri Lanka’s key export destinations would continue to remain inhibited. Economic

activity in the United States is seen as improving although factors such as a high

rate of unemployment and other downside risks indicate that recovery remains

fragile.

The economic meltdown is mostly forecasted to affect the Euro Zone but would

have signicant impact on developing nations due to their dependence on trade

and capital and credit inows from the Euro. According to IMF data, Asian regional

growth has already started to slow due to weaker export demand and 2012 is likely

to be a difcult year , although domestic factors such as tighter macroeconomic

policy stances have also played a role, especially in India and China. Asia is one of

the world’s most trade-dependent regions, exporting everything from commodities

such as metals and rice to sophisticated electronic products and cars; and external

demand will hence play a crucial role in determining Asia’s performance as a whole.

Domestic Economy

Sri Lanka’s economy sustained its post war growth momentum, surpassing last

year’s record high to grow by 8.3% in 2011. This was amidst several political andeconomic challenges on the world stage. Low interest rates and low ination-at

4.9% during the year also provided a growth facilitating environment. Per Capita

income increased to US Dollars 2,836 from previous year’s 2,400, whilst a further

decline in the unemployment rate, to reach the lowest level of 4.3% was another

positive indicator.

The downturn in Euro economies, higher energy prices, and the geo political

turbulence in the Middle Eastern region adversely impacted Sri Lanka during the

year, whilst an escalation in energy prices and a surge in imports placed signicant

strain on Sri Lanka’s Balance of Payments.

Your Company’s outlook on the potential of the Oil Palm

crop is buoyant. The crop’s productivity vis a vis other compet- ing cooking oils, such as Coconut, Corn and Soya Bean, is

signicantly higher. Furthermore, harvesting is considerably

less labour intensive compared to...

Management ReportsWatawala Plantations PLC

8

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 11/160

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 12/160

World oil prices are expected to remain high in 2012

and hence likely to continue to strain Sri Lanka’s

Balance of Payments. Estimate for Sri Lanka’s GDP

growth in 2012 has been revised downward to 7.2%

from an earlier projected 8%. The possibility of a

spread of global geo political hostilities is also a factor

which could impact Sri Lanka’s exports in 2012-2013.

Ination is projected to remain in single digit levels this

year despite the expected rise in commodity, fuel and

energy prices and the impact of the rupee depreciation

in 2012.

The Rupee depreciated at a sharper than expected rate

during the rst three months of 2012 resulting in marketvolatilities and adversely impacting importers. Although

the near term impact has been one of market volatility

and uncertainty, we are of the view that these recent

adjustment measures adopted by the government to

address the widening current account decit and the

decline in external reserves such as the tightening of

monetary and credit policy, and abolishment of the

rupee trading band to allow the exchange rate to adjust

more exibly should place the economy on a more

sustainable track in the medium to long term.

Sri Lanka’s agricultural sector grew marginally by 1.5%

in 2011 compared with a growth of 7% in 2010. This

was due to severe crop damage resulting in adverse

weather conditions during the rst half of the year;

but the sector made a remarkable recovery during the

second half of the year. The Tea sub sector declined

marginally whilst Rubber and Coconut both expanded

during the year.

In the External Sector, the growth of Exports which was

at 22.7 % was far outpaced by the growth of Imports

which was at 50.7% leading to an unprecedented risein the Trade Decit in 2011.

Sri Lanka’s high growth level has taken the country to a

higher growth trajectory and placed it amongst “Middle

Income” countries. As rightly suggested by the

Central Bank, improving demand for exports through

diversication of markets and products, strengthening

foreign inows and Foreign Direct Investments (FDIs)

through appropriate policies and a macroeconomic

environment, and improving labour productivity and

addressing structural rigidities in the labour market

would play a key role in overcoming some of the

challenges that Sri Lanka faces in maintaining its

high growth. Moreover, curtailing fuel expenses by

promoting energy efcient production technologies,

increasing the use of renewable energy sources and

energy conservation are other factors which are crucial

to sustaining the level of high growth.

Tea

Several economic, social and ecological factors

pose many challenges to hinder the growth andsustainability of the tea industry worldwide today.

However, a recognition of the critical need and

urgency to address these issues seem alarmingly low.

Amongst the issues that challenge the industry is one

of over supply as demand has failed to keep pace

with production increases. World production over the

last three decades has doubled. It is also noteworthy

that almost 56 percent of all tea produced worldwide is

consumed locally.

Global tea production reached 3,447.57 Mn. Kgs. in

2011 . While tea is produced in more than 35 countries,

only a handful - China, India, Sri Lanka and Kenya -

account for almost three-quarters of production. China

and India are today the world’s top tea producing as

well as consuming nations and as noted by the United

Nations Food and Agriculture Organisation (FAO), with

tea consumption in these two countries rising by 5.6%,

the global tea industry is being driven by these two

giants. China heads the list of producers contributing

33% of world production with an annual production of

1.4 million tonnes whilst India is expected to produce

around 1.1 Mn. Tonnes in 2011/12.

Sri Lanka’s tea production in 2011 fell by 0.19% to 328.37

Mn. Kgs. from 329 Mn. kgs. in 2010. Sri Lanka now

occupies fourth place in terms of production volumes

but remains the second largest exporter with Kenya

being the rst. However, Sri Lanka’s importance in the

world tea trade has declined considerably since 1970,

with share of world trade dropping from 40% in 1970 to

Management ReportsWatawala Plantations PLC

10

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 13/160

27.9% in 2000 and to 21.6% in 2011. Furthermore, its

production volume increase of 7.5% in the last 11 year

period is far below those of its competitors in Asia and

Africa which stand at 21% in India and 60% in Kenya.

The continuing downturn in the Euro economies

will continue to inhibit demand for tea imports into

the region. The turbulence in the Middle East could

continue impact demand for Sri Lanka’s Low Grown

teas in particular. In addition, FAO’s projections that

British, who are the world’s largest consumer of tea

per capita would reduce their consumption by 15%

compared with 15 years ago also exacerbates the

threat of reduced demand in the world for tea.

Rubber

Asia continued to be the world’s largest supplier of

natural rubber in 2011 with its share increasing to 93%

out of a total world production of 10.9 Mn. Tonnes in

2011. Indonesia, Thailand and Malayasia continued

to hold the top three producer slots respectively

accounting for 69% of total world production.

According to the February 2012 Report of the Association

of Natural Rubber Producing Countries’, the NaturalRubber market benetted from seasonal shortages of

supply and a marginal fall in the commodity’s stock in

China, and a rise in prices is being further supported

by the rise in crude oil prices, the depreciation of

Japanese Yen and an appreciation of the currencies of

some of the natural rubber exporting countries . Thus,

the current environment of short supply with expected

increase in demand augures well for natural rubber

prices in the year ahead.

Oil Palm According to Global Industry Analysts, world trade in

Palm Oil has seen a sharp increase over the last two

decades and the world market for Palm Oil is expected

to increase to 100 Mn. Tonnes by 2015. World production

volumes have been on the rise over the past few years as

a result of increases in extent of land cultivated, as well

as higher yields resulting from increased investments

in research and development. Moreover, the countries

which are at present the highest consumers of Palm Oil

such as India and China are not its key producers and

hence largely dependent on imports.

Your company’s outlook on the potential of the Oil

Palm crop is buoyant. The crop’s productivity vis a vis

other competing cooking oils, such as Coconut, Corn

and Soya Bean, is signicantly higher. Furthermore,

harvesting is considerably less labour intensive

compared to Tea and Rubber. These supply side factors

combined with an increasing demand for the product’s

value as a cooking oil, and as a raw material input in

soaps, detergents, cosmetics and pharmaceuticals as

well as a source for biofuel, underscore the viabilityand the immense potential for expansion of this crop

stream. Around 80% of the global palm oil output

at present is used by the food sector, but its use in

the above non food areas is increasing and would

contribute to a higher demand and prices worldwide in

the next few years.

Our Performance

Your Company’s Prots After Tax declined by 2.17% to

Rs. 520 Mn. compared with Rs. 532 Mn. in the previous

year and this was mainly due to a downturn in the tea

sector. Protability of the rubber and oil palm sectors

however, helped to more than offset the loss in the tea

sub sector.

Tea

The Tea sector made a loss Rs. 500 Mn compared

to a loss of 25 Mn. the previous year, and this was a

result of certain demand as well as supply side factors.

Protability reduced due to a lower National Sales

Average, and a 27% wage increase that came into

effect on 1st April 2011 which signicantly impacted

costs of production (COP).

Rubber

The rubber sector recorded a prot of Rs. 60 Mn

compared with a signicant prot of Rs. 139 Mn.

achieved during the previous year. This decline in prots

was mainly due to a fall in the National Sales Average

(NSA), by around 10% over the previous year; a decline

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 14/160

in output, as well an increase in COP due to a wage

increase.

Oil Palm

The Oil Palm sector achieved excellent results during

the year and was the largest contributor to the sector,

with the highest ever after tax prot of Rs. 373 Mn.,

compared to Rs. 195 Mn. in 2010/11. A 28% increase

in crop output as a result of improved agricultural

practices, an increase in the extent cultivated and

a higher NSA, were factors which contributed to this

sharp increase in prots.

Issues and Strategies

The tea sector accounts for 70% of your Company’s

revenue and its rich asset base abounds with potential,

for your Company, the sector and the economy.

However a multitude of issues currently burden the

competitiveness of the industry and challenge the

sustainability of the industry for all its stakeholders.

Most signicant amongst them has been an increased

costs of production. This has mainly been due to the

successive wage increases mandated by the government

over the past seven years which have followed a

regressive model. The wage increase in 2011 resulted

in a Rs. 220Mn. increase on the Gratuity provision by

the company and increased costs of production by

Rs.100Mn. and was particularly regressive as it

contained no productivity component. We hope that a

model for wage increases that incorporates productivity

mind and has the sustainability of the industry in mind

will replace the current biennial ad hoc ones. A long

term strategy formulated with the involvement of all

stakeholders and mediated by the government is now

paramount and urgent.

Another factor that hinders the growth of the tea sector

is a reduction in the supply of labour at levels of middle

management as well as at a level of crop plucking.

The number of tea workers per family living on an

estate has reduced from 2.6% to 1.9% , and of a one

million population who live on estates only 400,000 are

engaged in estate employment. A difculty in attracting

the best managerial talent also challenges the industry.

A shortage of labour is also a factor which hinders

growth of the rubber sector, and the social disparity vis

a vis other sectors has been found to be a factor that

has made this sector relatively less attractive.

Another that the Plantations sector as a whole faces

is the vulnerability to world market conditions that is

characteristic of primary commodities. Business cycles

in major importing countries, developments in the

markets of competing products such as for exampleSoya Bean oil in the case of Oil Palm and Synthetic

rubber vis a vis Natural Rubber; and exogenous factors

such as wars and climatic changes impact commodity

markets.

Whilst we highlight the need for collective action to

address some of these issues and look at innovative

ways to address some of the exogenous factors, we

will also continue to develop strategies and invest in

measures that improve the efciency of production

factors such as land and labour which are within our

control. This year the Oil Palm crop became the main

stay of your company - the pioneers of this crop in Sri

Lanka. Crop diversication has proven to be a valuable

measure for regional plantation companies to improve

protability when exogenous factors have impacted

protability of the traditional crops. Thus, it is also

important that the government encourages practices

such crop diversication; and where traditional crops

cannot be cultivated- diversication into areas such as

forestry cultivation in order to maximize plantation land

productivity and facilitate sustainability.

Management ReportsWatawala Plantations PLC

12

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 15/160

Acknowledgement

I wish to express my sincere appreciation to our

Shareholders, the Managing Agents and Employees of

Watawala Plantations PLC, for their loyalty and utmost

co-operation.

I also wish to express my gratitude to our Buyers, our

Brokers and Suppliers for their unstinted support and

to my colleagues on the Board for their able guidance

and direction.

G. Sathasivam

Chairman

17/05/2012

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 16/160

The Plantation Sector in Sri Lanka

The Plantation sector, albeit reducing in signicance

over the past three decades, still remains an important

sector in Sri Lanka’s socio-economic fabric, contributing

3.4% to the country’s GDP. Tea was Sri Lanka’s largest

export until it was replaced by garments in 1986,

and as early as 1950, plantation crops accounted

for about 70% of the country’s agricultural output,

declining to 51% in 1986 and to 25% by the late 80’s.

The importance and the potential of the sector in Sri

Lanka is also underscored by the large asset base of

both land and human, for which the Plantation sector

is the custodian. The total land extent utilized by this

sector in 2011 was in the region of 800,000 hectares,

whilst the number of direct and indirect employment

opportunities generated stands at about 1.5 million.

These reect the potential of the sector to be a key

contributor to achieving some of Sri Lanka’s key

economic objectives such as food security, employment

generation, environmental conservation and bridging of

the geographic disparities in income distribution in

the country. Thus, despite the down turn during the

year, your company remains buoyant on the potential

of its plantations, and because of the expertise and the

experience that the company possesses.

Sri Lanka’s Plantation sector faced a challenging year

due to a downturn in tea . Adverse weather conditions

during the rst half of the year resulted in a decline in

crop output whilst a 27% wage increase during the

year impacted costs of production. The impact of these

supply side factors were exacerbated by a reduced

demand from some of Sri Lanka’s key export markets

the Middle East, due to political turmoil in the region;

and the Euro zone due to an economic downturn that

intensied during the latter half of the year.

Company Performance

Your Company achieved a Prot After Tax of Rs. 520 Mn.

during the year which was a decline of 2.17%,compared with a Prot After Tax of Rs. 532 Mn. the

previous year. The prot made during the year includes

the net income of Rs. 387 Mn. earned on the disposal

of the fully owned subsidiary, Watawala Marketing

Ltd. The balance of Rs. 133 Mn. is the prots from the

company’s normal operations. The protability of the

Rubber and Oil Palm sectors helped to more than offset

the loss in the Tea sub sector, and Oil Palm became

the main stay of your Company during the year under

review.

Tea

Your Company’s tea crop production of 9.4 kg. mn

during the year reduced marginally by 4.4 % over the

previous year. The key contributor to this was the

reduction in the intake of bought leaf. Our own leaf

production increased by a marginal 0.34% despite a

climatic change that led to a prolonged drought during

the early part of the year; worker agitation for higher

Managing Director’s Review

...in the land extent as well as an increase in land/crop productivity. An output of2,858 Ha. by your company amounted to a productivity level in the region of 3,156

Kgs. of Oil per Ha; And this was a very commendable achievement surpassing last year’s

yield by 32.2%

30%Palm oil prod:

Management ReportsWatawala Plantations PLC

14

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 17/160

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 18/160

wages and the lagged impact of the work disruption that

took place in mid and late 2011. Tea land productivity

remained almost constant with a yield of 1,345 Kg. per

Ha being the highest reported in the last seven years.

The Net Sales Average (NSA) received by the Company

also declined by 6.8 % in the reporting period, and

this was despite your company’s continuing focus on

quality.

The company continued to invest in best practices,

advanced scientic methodologies and technology

to boost protability in the tea sector. Some of the

measures include, soil management practices such as

recycling of pruning and other farm waste for compost,

company and eld specic fertilizer programmes,

“Shear Harvesting” and partial mechanized pruning.

Most of these are measures which will yield benets

with a time lag of two to three years, and hence reect

the long term perspective we adopt, and the focus on

investing in the sustainability of our business.

The Waltrim tea factory, your Company’s show piece

and one of the most modern tea factories in the country,

continued to perform exceptionally well. The most

salient feature during the year was the improvement itachieved in performance rankings- to 4th position, from

13th position the previous season. Securing 88 Top

Prices at the Colombo auctions, during the reporting

period, reected the uniqueness of Waltrim’s quality

assurance practices.

Your company’s majority of the estates in the Hatton/

Watawala region were placed within the top 10

rankings in the Western/ Medium Grown tea category.

Kenilworth secured the 5th position in overall rankings

and the highest average in John Keells catalogue,

Carolina secured 3rd highest average, whilst Strathdon

was ranked the 5th highest in the same catalogue.

Additionally, Kenilworth secured the highest number

of top prices of 98 in the Medium Grown category,

Carolina and Strathdon achieved the 2nd highest and

the 3rd highest number of top prices of, 25 and 20

respectively, in the same category.

Rubber

Despite the industry’s impressive progress over the last

few years, the Sri Lankan rubber industry, continues

to be challenged by a multitude of issues. A decline

in the extent cultivated, low land productivity, high

costs of production, a shortage of labour; low labour

productivity due to factors such as the age of workers;inadequacy of resources; wide social disparity vis a

vis other industries, and factors beyond our control

such as erratic weather patterns. Some of the above

mentioned issues adversely impacted your Company’s

as well, and made it difcult for us to sustain the

positive trend recorded elsewhere in the country. Your

Company’s Crop production, decreased by 4%, to

reach 0.64 mn. kg compared to a crop of 0.67 mn. kg.

recorded in the previous period. This amounted to an

decrease of 26,049 kg in terms of volume.

The land productivity improved during the year with

the company reporting a yield of 705 Kg per Ha., 9.3%

above last year’s yield but still below the yields of other

regional plantation companies. This productivity level

was achieved despite the fact that a signicant extent of

rubber trees are due for uprooting in the next few years.

The company also lost over 4,000 rubber trees during

the mini cyclone during the 3rd quarter of the nancial

year. The extent of unproductive rubber uprooted this

year amounted to around 185 Ha. Recognising the

need for substantial improvements to land and crop

productivity your company is making a concerted

effort to address this issue, such as via the adoption

of site specic agricultural technologies that would

ensure consistent and enhanced output despite erratic

weather patterns that have an increasing tendency to

disrupt eld agricultural practices. The NSA received

by your company during the year was on par with

domestic and international prices, but below what the

company achieved during the previous year. However,

9.3%Yield

Management ReportsWatawala Plantations PLC

16

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 19/160

skillful handling of processing and manufacturing

technologies by the company, enabled the prices to

remain remunerative to its natural rubber business.

The short-term outlook for the natural rubber

market has been weakened by signicant economic

uncertainty and risks regards the United States and

Euro economies, however the long term outlook is one

of protability for the business.

Oil Palm

Palm Oil - seen as a humble source of edible oil, and

heavily criticized for being unhealthy and un-t for

human consumption merely a few years ago has

transformed markets and its image at a pace few

would’ve foreseen, and is today substantiated to be

one of the most nutritious edible oils in the world.

Furthermore, Palm oil is also the least expensive in the

vegetable oil market whilst its value also extends beyond

the use as a cooking oil, as one of the few sources of

Bio-diesel – a renewable substitute for Petroleum driven

diesel. This is in addition to the demand for Palm Oil as

a raw material for soaps, detergents, Pharmaceuticals

and Nutraceutical products.

During the year under review, your Company’s Palm

oil production rose signicantly by 30% to 6.5 Mn

Kgs of CPO from 5 Mn. Kg in the previous year. This

is attributable to an increase in the land extent as wellas an increase in land/crop productivity. An output of

2,858 Ha. by your Company amounted to a productivity

level in the region of 3,156 Kg. of Oil per Ha; and this

was a very commendable achievement surpassing last

year’s yield by 32.2%. We intend further enhancing

productivity to 3,500kg/ha, in the near future.

The company also achieved a commendable NSA,

which saw an increase of 2.81% over the previous

year’s. The infusion of innovative and effective

agricultural and processing technologies, acquired

from global pioneers in the oil palm business, would

strengthen our operations and yield dividends in the

years to come. Your company who pioneered the oil

palm processing facility in Sri Lanka, looks to build on

its current market leadership position and to expand the

crop to harness the vast potential in the industry. WPL

also envisages playing an active role in supporting the

ambitious plans of the Ministry of Plantation Industries,

to expand Sri Lanka’s land extend under Oil Palm from

its current levels of 6,000 ha. to 25,000 ha.

Capital Investments

During the year under review, the Company implemented

a modernization programme of its Nakiyadeniya Palm

Oil Renery with a total investment of Rs 20.3 Mn. and

new machinery for the Renery constituted Rs. 17.8 Mn.

of that investment. The quality of the output from the

renery has improved since, enabling the marketing of

a better quality product.

Tea-Hatton/ Watawala

The company made two investments during the year to

increase the manufacturing capacities at two of its tea

factories. One was an investment of Rs 62.3 Mn in the

Carolina Tea Factory to increase production from 16,000

kg to 24,000 kgs of green leaf per day. The other was

an investment of approx 17.8 Mn in the Company’s

Dickoya estate, to increase the capacity from 15,000kg

to about 20,000Kg of green leaf. The company’s capital

investments during the year amounted to Rs. 573 Mn.

and this includes re planting, factory modernization,

buildings and vehicles amongst others. A more detailed

report on capital investment will appear elsewhere in

this report.

Accolades

We are pleased to have been honored for the best

presented accounts in South Asia, in the Agriculture

Sector, by the South Asian Federation of Accountants

(SAFA) in the year 2010, at a function held in Dhaka.

this was a very commendable

achievement surpassing last year’s yield by 32.2%. We intend further

enhancing productivity to 3,500kg/ha, in the near future.

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 20/160

SAFA is an organization founded by the Institutes of

Chartered Accountants in India, Pakistan, Sri Lanka,

Bangladesh and Nepal and a few other accounting

bodies.

WPL also won the Gold Award for the 4th successiveyear for the Best Annual Report in the Plantation

sector category awarded by the Institute of Chartered

Accountants of Sri Lanka.

Lonach Dairy Farm

The dairy business, launched on Lonach Estate, as

part of the Group’s diversication strategy now has a

herd strength of 150 animals, and the milk production

capacity stands at 1,100 liters per day.

The cattle waste from the farm, continued to provideraw material for the manufacture of compost, a very

valuable source of fertiliser material, to re-develop the

degraded soil and to partially replace the chemical

fertilisers used on our plantations.

A Bio Gas generation system that is able to generate

140 units of electricity per day, and produce organic

slurry at a rate of 20,000liters per day, developed on the

farm are now being used by your Company’s estates.

Subsidiaries

The Board of Directors at an Extra Ordinary General

Meeting held on the 29th of February 2012 obtained

the approval of shareholders to divest its subsidiary

Watawala Marketing Ltd. The decision was taken as

a measure to address the difcult period that the

company underwent during the year, as a result of the

downturn in the tea sector. Rising interest costs and

the negative margins in the tea sector did not permit

the company to secure additional borrowings. The

Directors now intend using the funds raised from this

transaction to develop the company’s core business of

Tea and Palm Oil. A decision made by the Directors to

fund the gratuity provision has already resulted in an

unencumbered deposit of Rs. 46 Mn.

Energy Management

The escalation of world oil prices in the year under

review has further emphasized the need for energy

conservation and made more urgent the search for

alternate sources of energy.

It is also a key focus area for us as we see our costs

of production increasing due to higher energy prices.

The company has identied the opportunity to reduce

its energy costs by twenty percent via the adoption

of certain systems and substitute sources of energy.

Some of these initiatives carried out during the year

include the conversion of all fossil fuel powered tea

dryers to rewood ones; and the launch of an initiative

to replace rewood with the environmentally friendly

briquettes made out of refuse tea which is now being

implemented in the Lindula factories. An initiative

planned for next year include the implementation of the

ISO 50001 standards on energy management .

Issues and future Strategies

Rising costs of input, combined with rising costs of

labour due to ad hoc wage increases that have failed

to consider the nancial viability of the industry, remain

issues of critical concern to all stakeholders of the

industry.

These factors, when combined with price volatility

and market uctuations which are characteristic of

all primary commodities; pose signicant challenges

to the plantations business. Your company will look at

innovative ways in which it can reduce the vulnerability

of these primary commodities to global market

conditions. The year was one in which your Company’s

diversication helped it to benet from a “boom” in the

Oil Palm sector to offset the cyclical “bust” in Tea and

achieve a considerable prot.

The effects of climate change is making harvests

The year was one in which your

Company’s diversication helped it to

benet from a “boom” in the Oil Palm

sector to offset the cyclical “bust” in Tea

and achieve a considerable prot.

Management ReportsWatawala Plantations PLC

18

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 21/160

less predictable than ever and hence, developing

technologies to offset some of the harvest losses that

result from these erratic weather patterns would also

be a priority for WPL.

Your company will continue to expand its business

using the wealth of expertise and experience it

possesses. We would seek avenues to increase

protability via diversication both concentric as well

as conglomerate diversication; whilst investing in

harnessing the potential of our asset rich core business

of plantations.

Sustainable Growth

Sustainable Development, albeit a concept much

heard of , is an essential value that enlightens us that a

business cannot sustain its success in isolation and of

the need for a business entity to integrate its economic

objectives with those of the environment and society at

large. For instance, at your Company the development

of higher yielding crops is intertwined with measures to

sustain the environment. The Company’s sustainability

framework continues to cover Productivity and

Innovation, Care of the environment, Investing in

People and Returning to the community. Our initiatives

thus carried out during the year, for the upliftment of

communities and the environment, are presented

comprehensively in this report under the section on

Sustainability, which I am happy to note is presented

this year, in accordance with the prescribed framework

of the Global Reporting Initiatives (GRI) and reports on

our social, environmental and economic performance

using to the GRI indicators.

Commitment to quality, employee health and safety,

environmental responsibility and care, and ethical

behavior in all our dealings will continue to be priorities

and a part of your company’s ethos. The international

certications we have obtained and will continue

to seek for our many processes and locations are a

reection of our commitment to these values. These

certications are an outcome of stringent audits and

evaluations by globally reputed independent third

parties, and are hence endorsements that benet all

stakeholders of our company.

The certications obtained by Watawala Plantations

are as follows, Fair Trade certication by seven of our

tea gardens, The Ethical Tea Partnership certication

of twelve tea factories, and the Food Safety standardcertication - ISO 22000 by seven of our tea factories.

HACCP certication which is another on Food safety

has been obtained by seven of our factories; whilst

CQUi Certication has been obtained by Kenilworth

factory.

Appreciation

I would like to express my sincere appreciation to

the corporate and estate management teams, and

to all our Associates for their hard work, dedication

and commitment without which your company could

not have thrived during a challenging year. I would

also like to express my gratitude to the Board of

Directors for the condence placed in me and for

their unstinted guidance and support and to our

shareholders, customers, business associates and all

other stakeholders for their inspiration, and support.

V Govindasamy

Managing Director

17/05/2012

The Company’s sustainability framework

continues to cover Productivity and

Innovation, Care of the environment,

Investing in People and Returning to the

community.

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 22/160

L a n d m a r k

sEstate Management Services

(Pvt) Ltd took over the

management following an offer

for sale.

96

New dawning with a payoff to years

of consecutive losses

97

98Successfully overcame the economic

downturn whichwhich adversely affected

Asian region

Created new benchmark

blending traditions with

technology

9900

Recorded highest ever turnover of

Rs. 1.86 bn and highest ever tea

production of 12 mn kg.

Poor attendance, low productivity and

limited agricultural activity affected the

financial results

01/02

02/03 Won Taiki Akimoto 5S award

which is globally renowned as a

technique for setting benchmark

quality standards

Reached a turnover of Rs. the first time in

03/0

92

Birth of WPL on 18 June 1992 under

Companies Act No. 17 of 1982

following the government decision toprivatize the management of 22 RPCs

Strategic joint venture with Tata

Tea Ltd of India

93/95

Repeated losses on cards20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 23/160

04/05Collaboration with Tata Tetly in

the UK to spread the art of pure

Ceylon tea across the globe

Tea sourcing and supply chain to Tata Tea

and Tetley Group. Awarded the Silver at the Annual Reportcompetition held by the ICASL.

05/06

06/07First Runner -up in the best annual

reports awards competition held by

ICASL 2005/06

07/08 Achieved Business Super brand

status

Diversified in to Dairy Farming

Gold award for the best annual report in the plantation sector by ICASL

Recognized as an autho rized supplier to the ‘Ethical Tea Partnership’

08/09

09/10Gold award for the best annual report

in the plantation sector by ICASL for

the second time

Gold Award for Business Excellence in

the Agriculture and Plantations Sector

10/11Gold Award for the Annual

Report of the Plantation Sector

2009/10 by ICASL third time

in a row

Won National Quality Merit

Award, by Sri Lanka Standard

Institute in the medium scale

manufacturing company

11/12Won the Gold Award for the Be

Presented Accounts for 2010 in

Agriculture sector by South Asia

Federation of Accountants (SAF

held in Dhaka, Bangladesh

Bagged the Gold award for Ann

report in plantation sector 2010

by CA Sri Lanka for the 4th

consecutive year

Won National level awards pres

by National Agro Business Coun

Ceylon Chamber of Industries

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 24/160

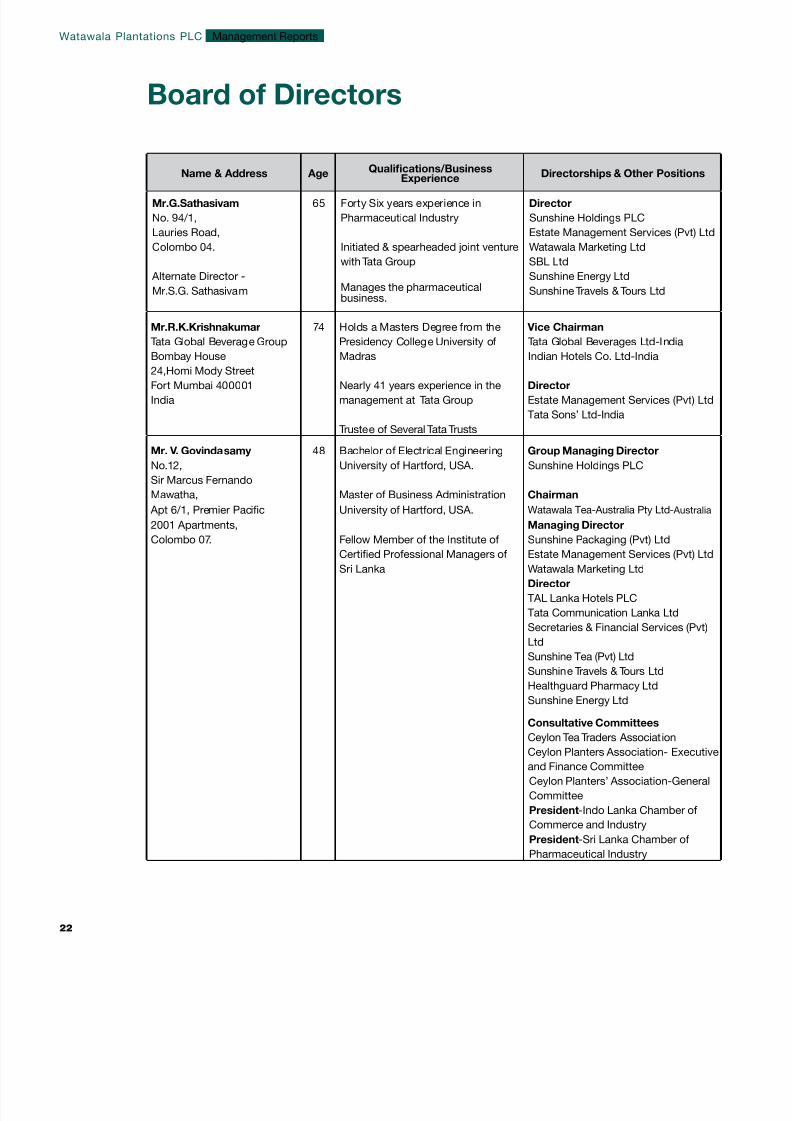

Name & Address Age Qualications/BusinessExperience Directorships & Other Positions

Mr.G.Sathasivam 65 Forty Six years experience in Director

No. 94/1, Pharmaceutical Industry Sunshine Holdings PLC

Lauries Road, Estate Management Services (Pvt) Ltd

Colombo 04. Initiated & spearheaded joint venture Watawala Marketing Ltd

with Tata Group SBL Ltd

Alternate Director -Manages the pharmaceuticalbusiness.

Sunshine Energy Ltd

Mr.S.G. Sathasivam Sunshine Travels & Tours Ltd

Mr.R.K.Krishnakumar 74 Holds a Masters Degree from the Vice Chairman

Tata Global Beverage Group Presidency College University of Tata Global Beverages Ltd-India

Bombay House Madras Indian Hotels Co. Ltd-India

24,Homi Mody StreetFort Mumbai 400001 Nearly 41 years experience in the Director

India management at Tata Group Estate Management Services (Pvt) Ltd

Tata Sons’ Ltd-India

Trustee of Several Tata Trusts

Mr. V. Govindasamy 48 Bachelor of Electrical Engineering Group Managing Director

No.12, University of Hartford, USA. Sunshine Holdings PLC

Sir Marcus Fernando

Mawatha, Master of Business Administration Chairman

Apt 6/1, Premier Pacic University of Hartford, USA. Watawala Tea-Australia Pty Ltd- Australia

2001 Apartments, Managing Director

Colombo 07. Fellow Member of the Institute of Sunshine Packaging (Pvt) Ltd

Certied Professional Managers of Estate Management Services (Pvt) LtdSri Lanka Watawala Marketing Ltd

Director

TAL Lanka Hotels PLC

Tata Communication Lanka Ltd

Secretaries & Financial Services (Pvt)

Ltd

Sunshine Tea (Pvt) Ltd

Sunshine Travels & Tours Ltd

Healthguard Pharmacy Ltd

Sunshine Energy Ltd

Consultative Committees

Ceylon Tea Traders AssociationCeylon Planters Association- Executive

and Finance Committee

Ceylon Planters’ Association-General

Committee

President-Indo Lanka Chamber of

Commerce and Industry

President-Sri Lanka Chamber of

Pharmaceutical Industry

Board of Directors

Management ReportsWatawala Plantations PLC

22

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 25/160

Name & Address Age Qualications/BusinessExperience Directorships & Other Positions

Mr.P.T.Siganporia 61 Holds a Bachelors Degree from Chairman

Tata Global Beverage Loyola College-Madras Mount Everest Mineral Water Ltd-India

Group

1,Bishop Lefroy Road Holds a Postgraduate Diploma in Managing Director

Kolkata- 700020 Business Marketing from XLRI- Tata Global Beverages Ltd-India

India Jamshedpur

Director

Tetly GB Limited-India

Estate Management Services (Pvt) Ltd

Watawala Marketing Ltd

Tata Coffee Ltd-India

Dr.D.V.Seevaratnam 64 Doctor of Science (Honoris Causa) Director

No11, Wayamba University -Sri Lanka Tea Research Board of Sri Lanka

Sangamitta Avenue, Plantation Human Development Trust

off Dharmapala Mawatha, Fellow member of Australian

Mt.Lavinia. Institute of Management Chairman

Ceylon Planters Provident Society

Fellow member of National Institute Consultative Committee on Estates

of Plantation Management and Advisory (Tea Research Institute)

Over 36 years of experience in Member of the Board of Governors

Plantations Sector - National Institute of Plantation

Management- Coconut Research Institute

Member

Standing Committee on Agriculture,

Veterinary,Medicine & Animal Sciences

Sciences of the University Grant

Commission

Consultative Committee on Research

(Tea Research Institute)

CARE International Advisory Board

A Representative of the Medical Wants

Committee

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 26/160

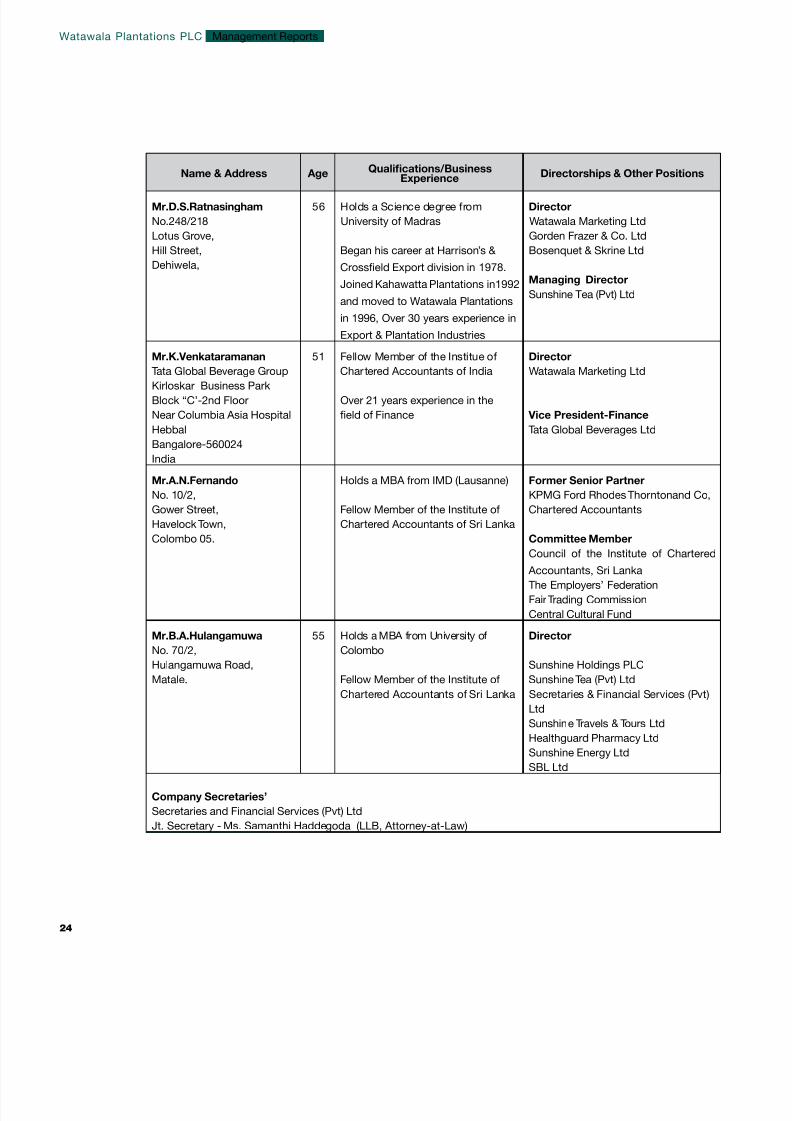

Name & Address Age Qualications/BusinessExperience Directorships & Other Positions

Mr.D.S.Ratnasingham 56 Holds a Science degree from Director

No.248/218 University of Madras Watawala Marketing Ltd

Lotus Grove, Gorden Frazer & Co. Ltd

Hill Street, Began his career at Harrison’s &

Crosseld Export division in 1978.

Joined Kahawatta Plantations in1992

and moved to Watawala Plantations

in 1996, Over 30 years experience in

Export & Plantation Industries

Bosenquet & Skrine Ltd

Dehiwela,

Managing Director

Sunshine Tea (Pvt) Ltd

Mr.K.Venkataramanan 51 Fellow Member of the Institue of Director

Tata Global Beverage Group Chartered Accountants of India Watawala Marketing LtdKirloskar Business Park

Block “C’-2nd Floor Over 21 years experience in the

Near Columbia Asia Hospital eld of Finance Vice President-Finance

Hebbal Tata Global Beverages Ltd

Bangalore-560024

India

Mr.A.N.Fernando Holds a MBA from IMD (Lausanne) Former Senior Partner

No. 10/2, KPMG Ford Rhodes Thorntonand Co,

Gower Street, Fellow Member of the Institute of Chartered Accountants

Havelock Town, Chartered Accountants of Sri Lanka

Colombo 05. Committee Member

Council of the Institute of Chartered Accountants, Sri Lanka

The Employers’ Federation

Fair Trading Commission

Central Cultural Fund

Mr.B.A.Hulangamuwa 55 Holds a MBA from University of Director

No. 70/2, Colombo

Hulangamuwa Road, Sunshine Holdings PLC

Matale. Fellow Member of the Institute of Sunshine Tea (Pvt) Ltd

Chartered Accountants of Sri Lanka Secretaries & Financial Services (Pvt)

Ltd

Sunshine Travels & Tours Ltd

Healthguard Pharmacy LtdSunshine Energy Ltd

SBL Ltd

Company Secretaries’

Secretaries and Financial Services (Pvt) Ltd

Jt. Secretary - Ms. Samanthi Haddegoda (LLB, Attorney-at-Law)

Management ReportsWatawala Plantations PLC

24

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 27/160

V Govindasamy - Managing Director (Page 22)

D V Seevaratnam - Director/CEO (Page 23)

D S Ratnasingham - Director (Page 24)

Lalith Cooray - Chief Financial Ofcer

A Fellow of the Institute of Chartered Accountants of Sr i Lanka

and a Fellow of the Institute of Certied Management Accountants

Sri Lanka. Counts almost 30 years of post qualifying experience

in Sri Lanka and overseas.

Ronnie Almeida - General Manager - Plantations

A Fellow Member of the National Institute of Plantation

Management with a Diploma in Plantation Management and

counts over 41 years experience in the industry. Served as the Asian representative in the Standards Committee of the Fairtrade

Labeling Organization of Germany.

Binesh Pananwala - Deputy General Manager, Plantations

Counts 20 years of experience in planting, joined JEDB and

continued with WPPLC, holds a MBA from Manipal ( Sikkim)

University.

Yajith de Silva - General Manager – South

Counts 31 years experience in the plantation sector, holds a

Degree in Plantation Management from Wayamba University of

Sri Lanka and a Diploma on Human Rights and Peace studiesfrom the Colombo University. Former regional Director of the

PHDT.

Ajantha Nugawela - General Manager - HR & Administration

Ajantha counts over 21 years of experience in Management and

Human Resources/ Administration both in Sri Lanka and overseas

and holds an MBA from the University of Delaware, USA. He

also has a Degree in Textile Technology from the University of

Moratuwa with many years of experience in the apparel industry.

B V Sinthaka Ruwan - Deputy General Manager - Finance

Sinthaka joined as the Finance Manager in 2008. He holds aBSc Special Degree in Finance and an Associate Member of the

Institute of Chartered Accountants of Sri Lanka. He has over 12

years of experience in a vide spectrum of organizations.

N. Vige Bede Johnpillai - General Manager – Marketing

Has over 39 years of experience in the Tea Plantations in Sri

Lanka working on plantations in the Uva and Western Regions.

Viji also served overseas as free-lance consultant to Gtz.

Management Team

Corporate Management Team

Rexy R Perera Manager – Internal Audit

Ms. Badra Jayadeva Manager – Exports & Sales

Gamini Wanasekara Manager – Purchasing

Estate Management Team

Watawala Region

Kenilworth Dinesh A S J Perera - Actg. Senior Manag

Carolina Alex C Samuel - Group Manager

Wigton K D Prasanjith Wetthewe - Manager

Lonach A Jayaram - Manager

Shannon Shameera Rathnayake - Manager

Hatton Region

Vellai Oya Madura H Medagamage - Actg. Senior Manag

Dickoya Gershon P Thevathason - Actg. Senior Manag

Abbotsleigh Robin Winter - Senior Manager

Strathdon P Udeni Wanigatunge - Senior Manager

Lindula Region

Henfold Chaminda Oliver - Manager(Resigned w.e.f 28/04/2012)

Waltrim M S A Akber - Senior Manager

Tangakelle Kapila Sumanarathne - Manager

Agrakande Channa D Ikiriwatte - Manager

Ouvahkelle Harsha P T Hulangamuwa - Manager

Lippakelle A P Premachandra - Actg. Manager

Udugama Region

Nakiyadeniya Rubber N P Chamika Naranapitiya - Actg.Senior Manage

Nakiyadeniya Oil Palm Ruwan Gunaratne - Actg. Manager

Talangaha Dhanushka Daswatte - Manager

Homadola Gamini N Ratnayake - Senior Manager

Palm Oil Mill H Milton Wijepala - General Manager

Prole of theExecutive Committee

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 28/160

Dr D V SeevaratnamDirector/CEO

V Govindasamy Managing Director

D S RatnasinghamDirector

Lalith Cooray Chief Financial Ofcer

Executive Committee

Management ReportsWatawala Plantations PLC

26

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 29/160

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 30/160

MANUFACTURINGBRIQUETTES OUT OF

REFUSE TEAPROTECTING THE ENVIRONMENT BY REDUCING THE FELLING OF TREES

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 31/160

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 32/160

Our People

Our people’s competencies of talent and

dedication have been a mainstay in our success

and have helped to make Watawala Plantations

one of the best Plantation Companies in Sri

Lanka. We always believe in creating a better

future for our employees. We value each one of

them and we make every effort to engage with

them. Those on our plantations referred to ascoolies during the colonial era are now being

treated as Associates. These Associates are the

reason for what we are today and one of our

main objectives is to uplift the quality of their

lives by catering to their needs.

Associates with the CEO on the International Women’s Day 2011 In Colombo

Our people are our key asset. We make good people brilliant

and brilliant people even better.

Conducting training programs on areas such

as Leadership is one of the integral parts in

developing our employees’ competencies. Such

programs are conducted in association with

many local and foreign NGO’s such as Care

Foundation, Berendina and WUSC. We make

sure that we create action plans after surveying

the feedback of every employee followed by thetraining. And through our climate surveys, we

respond meaningfully and efciently, work to

create an environment where our employees feel

valued and condent.

Watawala Plantations PLC

30

Management Discussion & Analysis

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 33/160

Knowledge Inventory

To survive in this volatile industry, having adequate

paper qualications is a must. We have clearly dened

the career path of the executives starting from the

trainee level to Chief Executive Level. Our company

strongly persuades and encourages our team to follow

professional courses. Reimbursement of course fees

in full on successful completion of these courses

embarked upon is introduced as a motivating factor.

Knowledge Inventory - 2011/2012

2011/2012 2010/2011 2009/2010 2008/2009 2007/2008

Senior Management 8 17 10 10 10

Head Ofce Executives 26 27 54 69 55

Estate Managers & Executives 63 93 54 53 53

Head Ofce Staff and other Ofcers 21 37 88 79 86

Estate Staff and other ofcers 632 698 668 655 654

Sub Total 750 872 874 866 858

Associates 11,418 11,744 12,167 12,357 13,403

Total Employees 12,168 12,616 13,041 13,223 14,261

Turnover per Employee Rs.’000’ 372.74 488.13 430.31 309.25 302.48

Prot per Employee Rs.‘000’ 33.91 32.48 32.48 6.04 28.36

Assets per Employee Rs.’000’ 464.17 354.56 354.56 291.84 256.01

Human Resources

Staff Strength

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 34/160

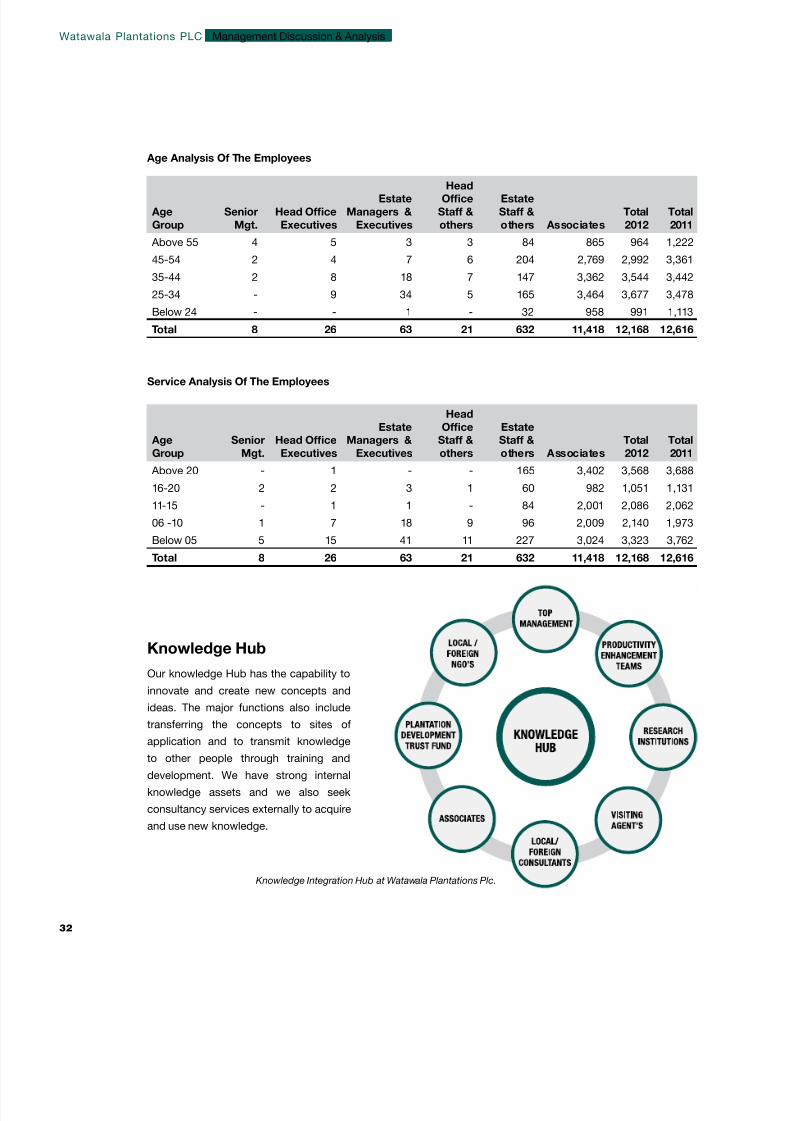

Age Analysis Of The Employees

Service Analysis Of The Employees

Age

Group

Senior

Mgt.

Head Ofce

Executives

Estate

Managers &

Executives

HeadOfce

Staff &

others

Estate

Staff &

others Associates

Total

2012

Total

2011

Above 55 4 5 3 3 84 865 964 1,222

45-54 2 4 7 6 204 2,769 2,992 3,361

35-44 2 8 18 7 147 3,362 3,544 3,442

25-34 - 9 34 5 165 3,464 3,677 3,478

Below 24 - - 1 - 32 958 991 1,113

Total 8 26 63 21 632 11,418 12,168 12,616

Age

Group

Senior

Mgt.

Head Ofce

Executives

Estate

Managers &

Executives

Head

Ofce

Staff &

others

Estate

Staff &

others Associates

Total

2012

Total

2011

Above 20 - 1 - - 165 3,402 3,568 3,688

16-20 2 2 3 1 60 982 1,051 1,131

11-15 - 1 1 - 84 2,001 2,086 2,062

06 -10 1 7 18 9 96 2,009 2,140 1,973

Below 05 5 15 41 11 227 3,024 3,323 3,762

Total 8 26 63 21 632 11,418 12,168 12,616

Knowledge Hub

Our knowledge Hub has the capability to

innovate and create new concepts and

ideas. The major functions also include

transferring the concepts to sites of

application and to transmit knowledge

to other people through training and

development. We have strong internal

knowledge assets and we also seek

consultancy services externally to acquire

and use new knowledge.

Knowledge Integration Hub at Watawala Plantations Plc.

Watawala Plantations PLC

32

Management Discussion & Analysis

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 35/160

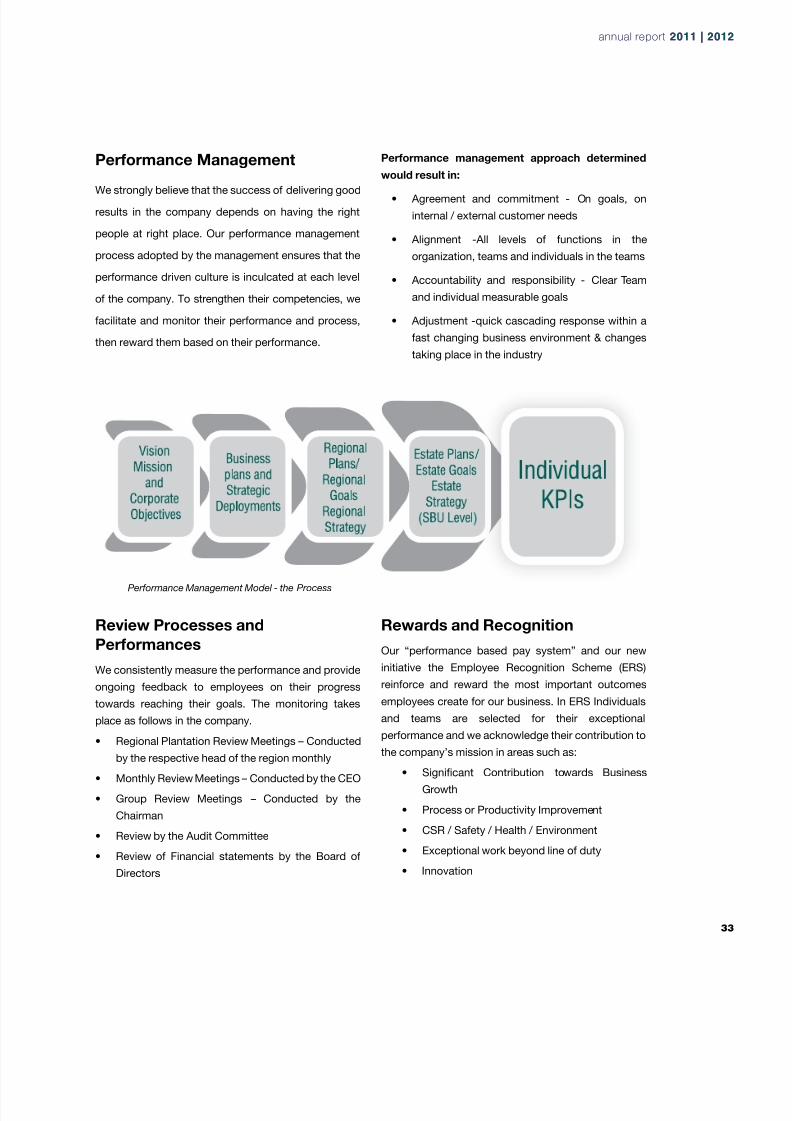

Performance Management

We strongly believe that the success of delivering good

results in the company depends on having the right

people at right place. Our performance management

process adopted by the management ensures that the

performance driven culture is inculcated at each level

of the company. To strengthen their competencies, we

facilitate and monitor their performance and process,

then reward them based on their performance.

Performance management approach determined

would result in:

• Agreement and commitment - On goals, on

internal / external customer needs

• Alignment -All levels of functions in the

organization, teams and individuals in the teams

• Accountability and responsibility - Clear Team

and individual measurable goals

• Adjustment -quick cascading response within a

fast changing business environment & changes

taking place in the industry

Performance Management Model - the Process

Review Processes and

Performances

We consistently measure the performance and provide

ongoing feedback to employees on their progress

towards reaching their goals. The monitoring takes

place as follows in the company.

• Regional Plantation Review Meetings – Conducted

by the respective head of the region monthly

• Monthly Review Meetings – Conducted by the CEO

• Group Review Meetings – Conducted by the

Chairman

• Review by the Audit Committee

• Review of Financial statements by the Board of

Directors

Rewards and Recognition

Our “performance based pay system” and our new

initiative the Employee Recognition Scheme (ERS)

reinforce and reward the most important outcomes

employees create for our business. In ERS Individuals

and teams are selected for their exceptional

performance and we acknowledge their contribution tothe company’s mission in areas such as:

• Signicant Contribution towards Business

Growth

• Process or Productivity Improvement

• CSR / Safety / Health / Environment

• Exceptional work beyond line of duty

• Innovation

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 36/160

Industrial Relations

Our company’s practices enhance the capacity of

workers and management to improve communication

and labor relations in the plantation sector. One suchproject is in collaboration with World University Service

of Canada (WUSC) which brings together workers and

management to discuss ongoing issues and understand

the interdependency between increased productivity

and improved working conditions. The project has

assisted estate management, estate staff, trade union

leaders, and workers to increase their knowledge on

• Labor Law

• Non-Violent Communication and Negotiation

• Positive Thinking

• Stress Management

• Team Building

Our practices are also adapted to the conventions

and recommendations of ILO (International Labor

Organization) and are also in line with the Labor

Standards of Sri Lanka that can be outlined as social

security, industrial safety etc.Our Harvesting Associate Krishnaveni (1st From Right) at

the Association for Women’s Rights In Development (AWID)

Conference In Istanbul, Turkey In April 2012

Gender Equality

We raise awareness on the importance of gender

equality and address key issues in collaboration with

male and female estate residents, workers, staff, andmanagement. The project with WUSC aims to recognize

women’s contribution to the plantation sector by

encouraging leadership of women in decision-making

roles, promoting women’s participation and reducing

Watawala Plantations PLC

34

Management Discussion & Analysis

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 37/160

gender based violence.The main areas of focus include:

• Assisting Neighborhood Women’s Groups

(NWGs) as support system for Women

• Addressing gender based Violence

• Supporting Alcohol Harm Reduction

• Improving Women’s Health

The key goal of this is to support women to take up

leadership positions on the estate based community

and organizations.

Employer-Employee Relationship

The Community Development Forum (CDF) is yet

another of our innovations in the empowerment of

our associates. These we have established in 3 of our

estates and due to its success we are in the process

of extending this initiative in a further 3 of our estates.

Through the CDF the Management and Associates

meet at monthly intervals and put their heads together

to solve day today issues that occur in the estate.

Unlike in the otherwise considered conventional way

of problem solving, here each and every person is

given an opportunity to take part in the process of

solving matters by which they take pride not only by

contributing for decision making, but also are being

given due recognition. Apart from that there are a few

other benets that the community enjoys as a result

of being able to attract the operations and services of

government and other service providers, transparency

of welfare activities on the estate, channeling all the

welfare and operations by NGOs if any through the

CDF so that overlapping of activities would not occur,

discussion of productivity parameters, estate village

integration and training on various aspects.

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 38/160

Financial Review

Global outlook

The world economy showed aftershock symptoms

of 2008 global economic crisis with the Euro zone

calamity which hindered the nancial health of member

countries. The never ending Middle East uprisings

culminated with the Libyan and Syrian power conicts

as well as the economic sanctions posed on Iran fuelled

the amassing uncertainty. Furthermore environmental

catastrophes all around the globe such as earthquakes

and Tsunami waves which devastated a part of Japan.

All these and more, made the outlook for businesses

further challenging and ambiguous during the year

under consideration.

Sri Lankan economy

The nancial year started with loosened monetary and

scal policy decisions which facilitated funding at lower

cost for constructions and other capital investments.

With brighter post war prospects the government

inaugurated massive development projects on

infrastructure network to anchor the upcoming

business ventures.

The foreign direct investments to the country showed

positive momentum with major ventures into tourism

and service sector. Throughout the year the country

has been able to maintain economic growth at 8.3% on

average to be considered as a top economic gainer in

the region by Wall Street Journal. However towards the

second half with widened gap in BOP the government

allowed free oat of Rupee which resulted in hiking

local ination and cost of production. The prime lending

rates pushed to double digits followed by the high

demand for borrowings during the rst 2 quarters. The

high demand and inadequate production of energy has

been pressing the country towards an energy crisis. The

invention of sustainable energy source has become the

need of the hour for the survival of Sri Lankan economy.

The Company had a tough year with the biennial wage increase mandated for estate associates

coupled with a falling Net Sales Average of tea. Driven by the demonstrated resilience to strive

towards success the company managed to sail through the rough sea with tight cost controls and...

Agro sector

The Agro sector had mixed results during the year

following the Euro zone and Gulf crises and changes in

world climatic conditions. However towards the second

half with rupee depreciation the export of agro produce

showed positive momentum.

During the year the shareholders equity

aggregates up to 50% of the total asset base of

the company.

%

Watawala Plantations PLC

36

Management Discussion & Analysis

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 39/160

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 40/160

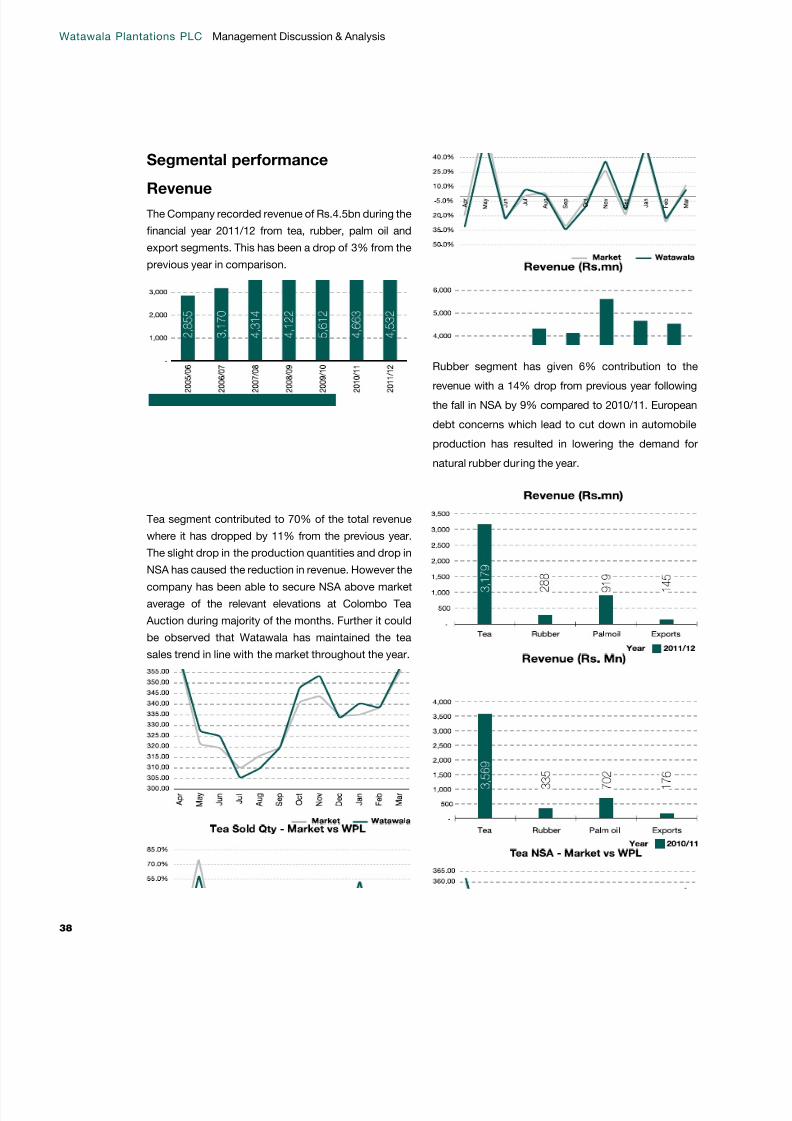

Segmental performance

Revenue

The Company recorded revenue of Rs.4.5bn during the

nancial year 2011/12 from tea, rubber, palm oil and

export segments. This has been a drop of 3% from the

previous year in comparison.

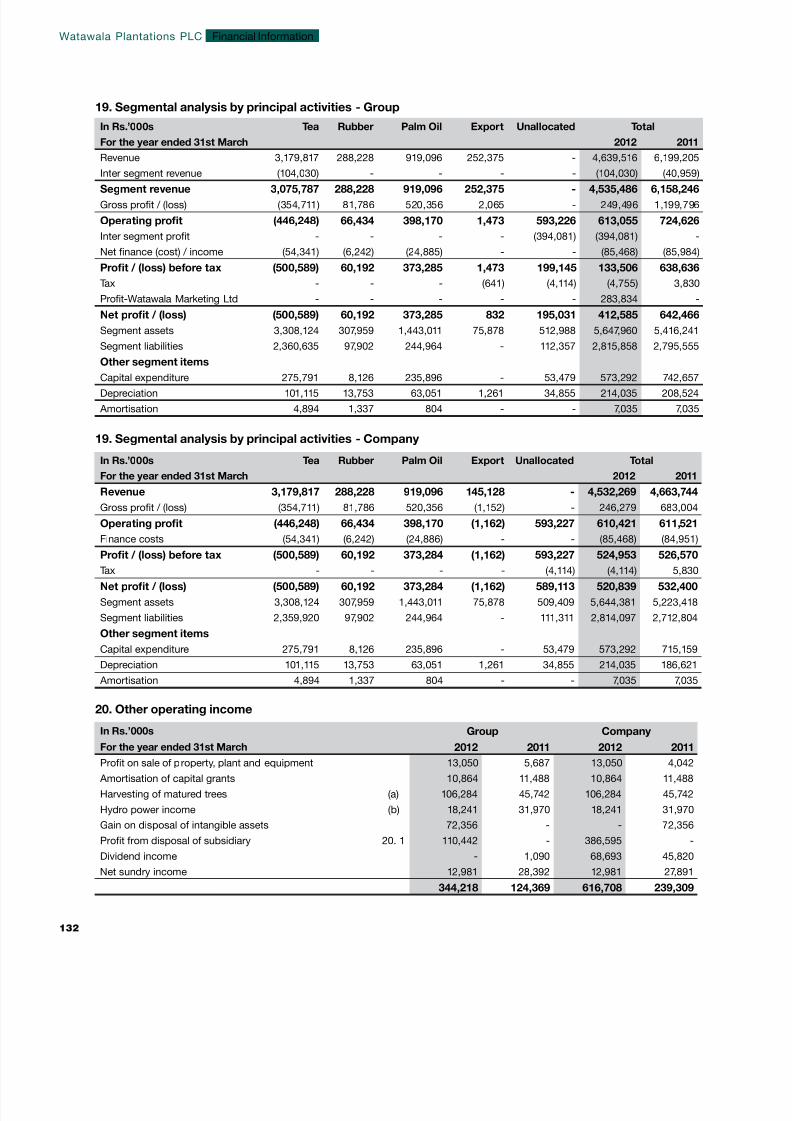

Tea segment contributed to 70% of the total revenue

where it has dropped by 11% from the previous year.

The slight drop in the production quantities and drop inNSA has caused the reduction in revenue. However the

company has been able to secure NSA above market

average of the relevant elevations at Colombo Tea

Auction during majority of the months. Further it could

be observed that Watawala has maintained the tea

sales trend in line with the market throughout the year.

Rubber segment has given 6% contribution to therevenue with a 14% drop from previous year following

the fall in NSA by 9% compared to 2010/11. European

debt concerns which lead to cut down in automobile

production has resulted in lowering the demand for

natural rubber during the year.

Watawala Plantations PLC

38

Management Discussion & Analysis

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 41/160

Palm Oil segment boosted its contribution with 20.2%

slice of revenue which is an increase of 31% from last

year being the only segment with a positive movement

from 2010/11. Increase in production by 28% with

better agricultural practices, improved processing

facilities at Nakiadeniya Mill and better prices achieved

has caused this positive outcome.

Protability

The Company completed a year with mixed results

following heavy cost and squeezed margins. The wage

increase had been the headline for the year in theplantation sector which had a net impact of 27% over

the pay in previous year.

On a quarterly basis the revenue and protability

showed an analogous trend except for Quarter 4, and

only Q3 and Q4 showing positive net results.

Prot before tax (PBT)

Tea segment ended up with a loss of Rs.501mn as a

consequence of additional cost tied to the wage hike.

This has been 20 times increase in the loss from the

previous year which recorded loss of Rs.25mn.

Rubber segment recorded a prot before tax of Rs.60mn

which has been a drop of 57% from the previous year.

This was as a result of lower prices in the market and

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 42/160

the drop in rubber exposure during the year with more

emphasis given on palm oil segment.

Palm oil segment being the premier gainer of the year

was able to achieve Rs.373mn prot before tax. This

was an increase of 90% from the prior year. Extending

the palm oil cultivation land , better agricultural

practices and improved mill facilities followed by better

prices in the market tr iggered the improved protability.

Palm oil has contributed 71% of the total prots made

by the Company during the year.

Export segment had a sluggish outlook throughout theyear with adverse impact posed due to the crisis in

Euro zone and uncertainty in gulf region. The segment

showed a drop of almost 100% in protability with a

marginal loss reported during the year.

Return on equity (ROE)

The Group generated a return on equity of 15% for the

nancial year which has been 10% drop from the prior

year. Decline in the prots and increase in total equity

impelled the dip in ROE.

Return on assets (ROA)

The Group has been able to generate a return of 7%

using the total asset base during the nancial year. This

has been a drop of 4% compared to the previous year

due to lower protability.

Earnings per share (EPS)During the nancial year the Group has generated

Rs.1.74 prot for each unit of shares. (Total Ordinary

shares: 236.67mn). This has been a drop of 36%

compared to the previous year.

Moreover the cash generated from operations per

share was Rs.2.67 for the year where the same has

been Rs.3.64 in 2010/11.

Price earnings ratio (PER)

The nancial year ended 31/03/2012 recorded a PER of

5.74 for Watawala share. During the previous year this

has been 9.21. The year closed with a market price of

Rs.10 per share of the company traded on Colombo

Stocks Exchange. (Rs.24.50 as at 31/03/2011)

Watawala Plantations PLC

40

Management Discussion & Analysis

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 43/160

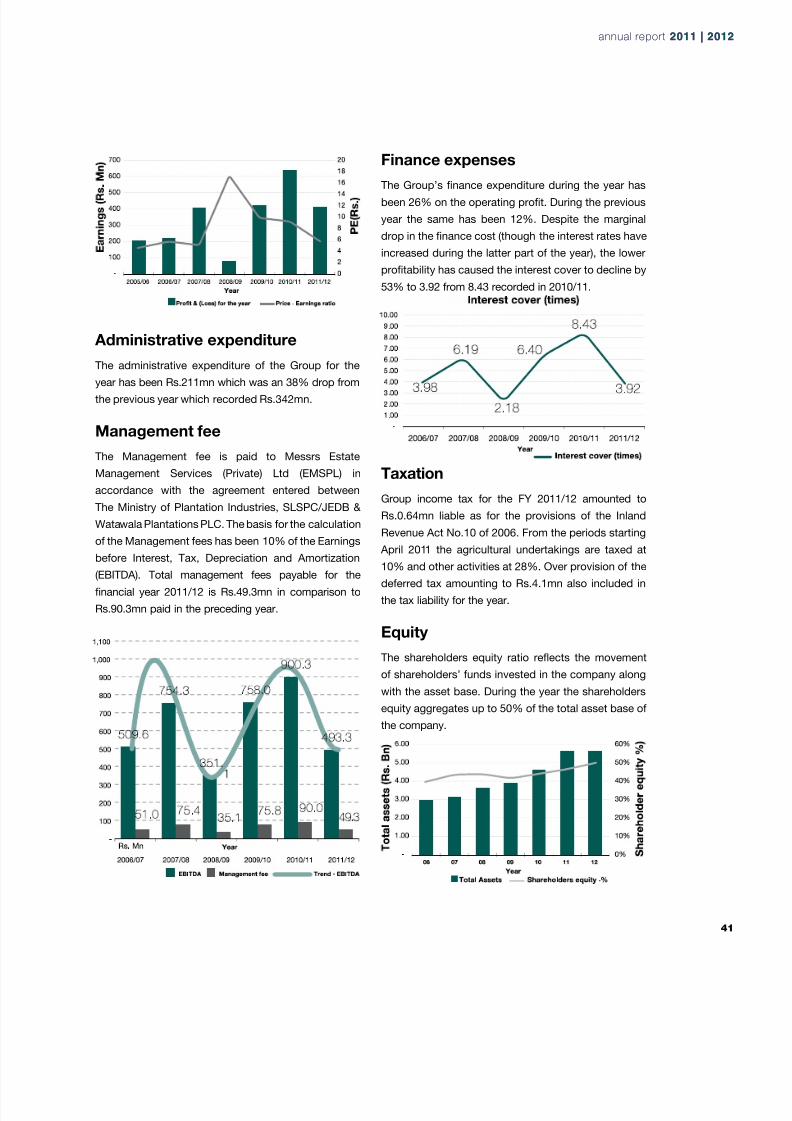

Administrative expenditure

The administrative expenditure of the Group for theyear has been Rs.211mn which was an 38% drop from

the previous year which recorded Rs.342mn.

Management fee

The Management fee is paid to Messrs Estate

Management Services (Private) Ltd (EMSPL) in

accordance with the agreement entered between

The Ministry of Plantation Industries, SLSPC/JEDB &

Watawala Plantations PLC. The basis for the calculation

of the Management fees has been 10% of the Earnings

before Interest, Tax, Depreciation and Amortization

(EBITDA). Total management fees payable for the

nancial year 2011/12 is Rs.49.3mn in comparison to

Rs.90.3mn paid in the preceding year.

Finance expenses

The Group’s nance expenditure during the year has

been 26% on the operating prot. During the previous

year the same has been 12%. Despite the marginal

drop in the nance cost (though the interest rates have

increased during the latter part of the year), the lower

protability has caused the interest cover to decline by

53% to 3.92 from 8.43 recorded in 2010/11.

Taxation

Group income tax for the FY 2011/12 amounted to

Rs.0.64mn liable as for the provisions of the Inland

Revenue Act No.10 of 2006. From the periods starting

April 2011 the agricultural undertakings are taxed at10% and other activities at 28%. Over provision of the

deferred tax amounting to Rs.4.1mn also included in

the tax liability for the year.

Equity

The shareholders equity ratio reects the movement

of shareholders’ funds invested in the company along

with the asset base. During the year the shareholders

equity aggregates up to 50% of the total asset base of

the company.

annual report 2011 | 20annual report 2011 | 20

8/14/2019 Watawala Plantations 2011.2012.pdf

http://slidepdf.com/reader/full/watawala-plantations-20112012pdf 44/160

Market value added (MVA)

MVA is an indication of the value addition ability of a

Company to the shareholders’ funds invested. MVA is

arrived at by subtracting the shareholder funds from

the market value of shares. During the nancial year

2011/12 the market value addition has deteriorated by

Rs.465mn following the drop in market price of share

to Rs.10 from Rs.24.5 recorded the year before. This

has been 114% drop in MVA from Rs.3.3bn recorded

in 2010/11.

Enterprise value (EV)

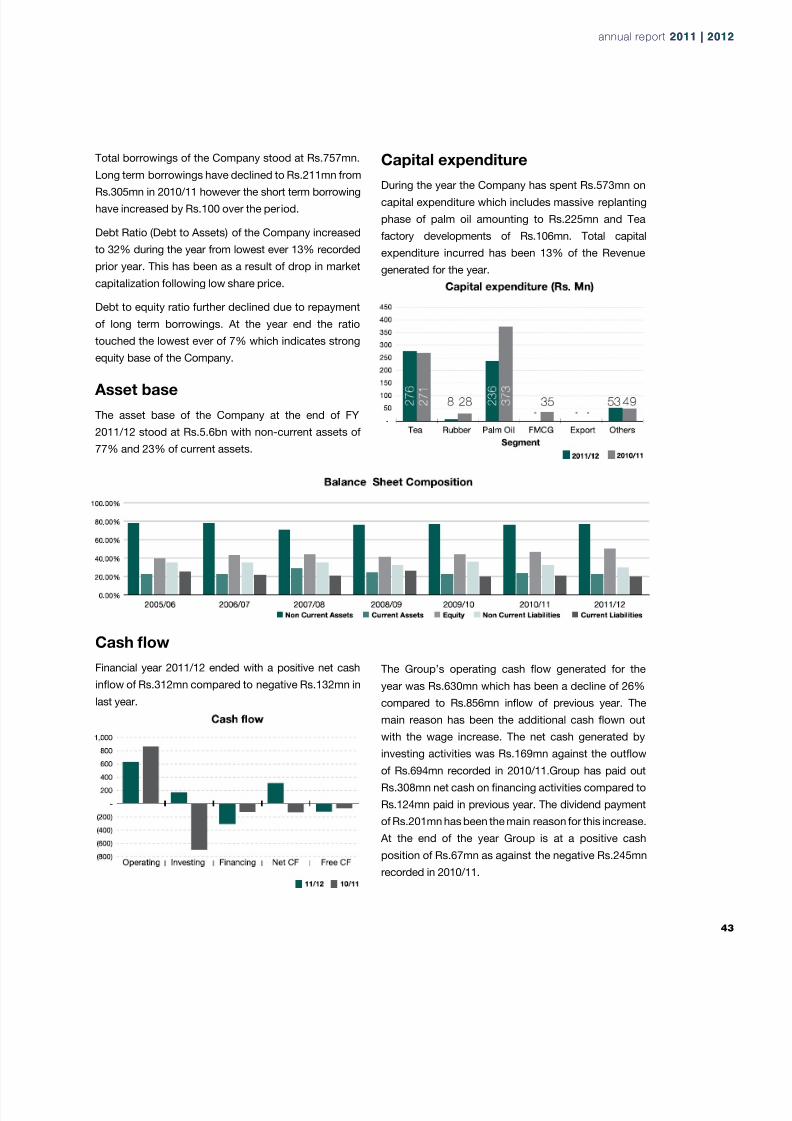

Enterprise value is considered as potential takeover

price of company hence it is derived from the market

capitalization. During the year EV of the company has

dropped substantially to Rs.3.05bn from Rs.6.6bn

recorded in 2010/11. This was as a consequence of

drop in market price of a share by 59%.

Enterprise multiple (EM)

Enterprise Multiple is arrived at by dividing the