1© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Contents

Executive summary 2

About this report 3

Introduction 4

Entrepreneurial driving forces 5

Entrepreneurs and social responsibility 11

The role of government 15

Conclusion 18

Appendix: Survey results 20

2 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Executive summary

Entrepreneurs are seen as a key driver of the UK’s economic recovery, and new businesses are on the increase. This year alone, over 44,500 start-up businesses had registered by mid-February, according to the government’s StartUp Britain website. But beyond their economic importance as taxpayers and employers, these wealth creators make other positive contributions to society. Yet the UK often has a distinctly ambivalent attitude towards the affl uent individuals who succeed in their business ambitions.

To explore the motivations of Britain’s entrepreneurs, their attitudes to social responsibility and the challenges they face, the Economist Intelligence Unit, on behalf of Lloyds TSB Private Banking, conducted a survey of 300 wealth creators as well as interviews with business owners, academics and government offi cials.

Key fi ndings of the research include:

Entrepreneurs believe they make a positive contribution to societyAlmost three-quarters (70%) of business owners see the role of entrepreneurs as a good thing for society in general. They have become increasingly generous with their time and money. Two-fi fths of respondents now contribute hours of personal or business time to charitable work—up from 32% fi ve years ago.

The proportion giving money to local organisations has also risen, with 86% giving to charity.

Determination and independence drive entrepreneursFreedom to be their own boss is the key motivation for starting a business for 55% of respondents, while almost 40% identify work satisfaction as a major driver. Once in business, almost two-thirds of respondents pinpoint determination as the main source of their success.

Tax and a sluggish economy are the biggest challenges for wealth creatorsAlmost half of respondents (49%) view government policy and tax as the top constraint when creating personal wealth from their businesses, and a similar number (46%) see the economic situation as the main limitation.

More governmental support is needed for wealth creatorsThere is a strong sense (85% of respondents agree) that the government could do much more to encourage and support potential entrepreneurs. And although 45% of respondents believe the government recognises entrepreneurs’ contribution to society, there is less conviction that they are given the practical support they need to provide further social input.

3© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

About this report

In January 2013 the Economist Intelligence Unit, on behalf of Lloyds TSB Private Banking, surveyed 300 UK entrepreneurs to explore their motivations, challenges and attitudes to social responsibility.

In addition, in-depth interviews were conducted with entrepreneurs and experts. Our thanks to the following for their time and insight:

Simon Deakin, assistant director of the Cambridge Centre for Business Research

Jonathan Haward, founder of the property search fi rm, The County Homesearch Company, and the online memorial service, Friends and Relations

Rupert Hodson, co-founder of the online fi nancial services marketing fi rm, Dianomi

Stephen Unwin, founder of the soft drinks fi rm, Cawston Press, and a business coach with the Actioncoach franchise

A spokesperson from the Department for Business, Innovation & Skills

The report was written by Faith Glasgow and edited by Monica Woodley of the Economist Intelligence Unit.

4 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Introduction

It is no secret that the entrepreneurial spirit plays an increasingly signifi cant role in the UK economy. In 2011 Prime Minister David Cameron called for an “enterprise-led” recovery from the fi nancial crisis and its economic fallout, and the fi gures suggest that despite challenging economic conditions, the country’s entrepreneurs remain eager to take the plunge and set up new businesses.

Figures from the Department for Business, Innovation & Skills (BIS) show continuing steady growth in the number of small and medium-sized enterprises (SMEs) in the UK. There were a record 4.8 million SMEs at the start of 2012—up from 4.5 million in 2011, and an increase of almost 40% since 2000 (the earliest point for which comparable data exists). The vast majority (99.2%) of those SMEs were small businesses employing less than 50 people.

Yet their economic contribution is critical. Apart from the potential private wealth generated by the owners themselves,

BIS fi gures show SMEs account for 60% of employment in the private sector and almost half of private-sector turnover.

The government has launched diverse initiatives to attract new entrepreneurs into the business arena, and to nurture existing small businesses. Yet at the same time there is continuing debate about the appropriate use of wealth, and about the social, environmental and fi nancial responsibilities of those who acquire it.

This report explores the motivations driving Britain’s entrepreneurs and the challenges they face. It examines their attitudes to corporate and individual social responsibility, and considers how far such responsibility is embedded in the day-to-day operation of today’s SMEs. Finally, it looks at the extent to which the government is succeeding in its efforts to provide entrepreneurial business ventures with practical support and to inspire new entrepreneurs to join their ranks.

5© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

In line with the government statistics quoted above, this survey highlights the fact that small businesses are the UK’s real economic bedrock: more than four-fi fths (81%) of respondents’ primary businesses have an annual turnover of less than £3m, and indeed 38% turn over less than £150,000 a year.

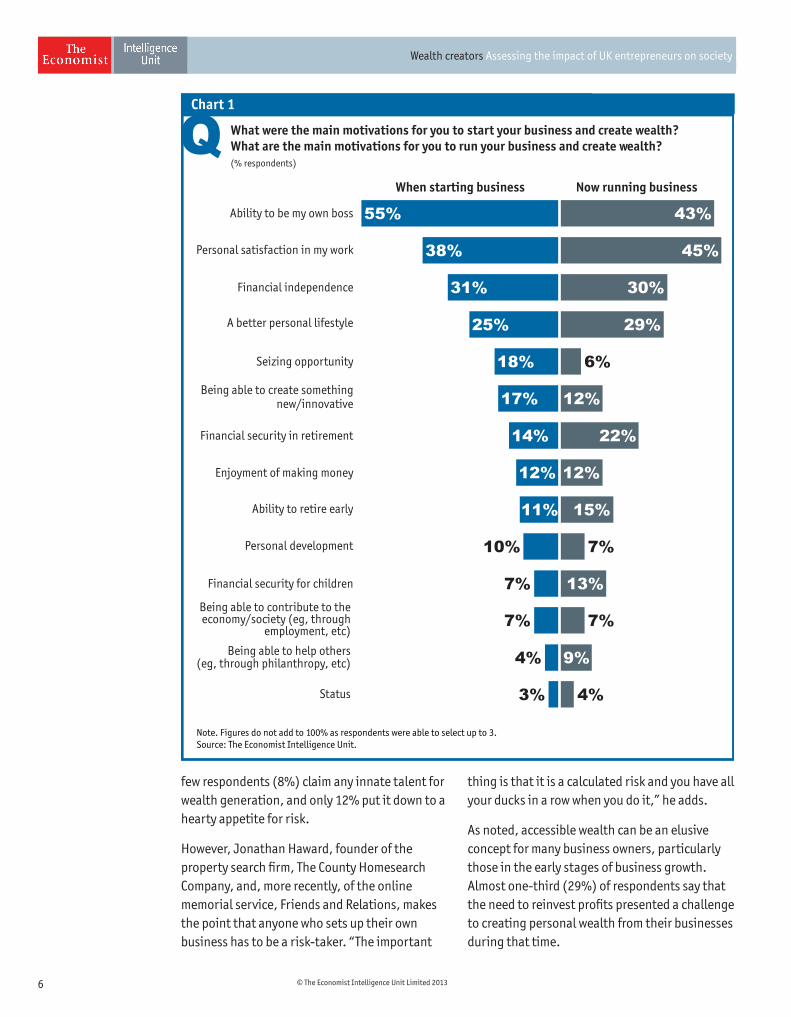

So what motivates entrepreneurs to take the risks associated with setting up and running a business? It is defi nitely not all about making money per se, according to the survey fi ndings.

Ambitious owners of small businesses are likely to plough much of their profi ts back into the business at that stage of development. In fact, wealth is a somewhat elusive concept for many: almost three-fi fths (59%) of respondents have less than £1m in personal investible assets, and only 5% have more than £5m.

When asked to identify up to three motivating factors, 55% of business owners cite independence—the fact that it enables them to be their own boss—while almost two-fi fths (38%) are driven by the personal satisfaction they get from the job. Only 12% of respondents admit to being driven by the sheer enjoyment of making money.

These results strike a chord with our interviewees. “True entrepreneurs are ambitious, restless and looking for new challenges; they’ve always wanted to do their own thing and hate to be constrained,” says Stephen Unwin, founder of the soft drinks fi rm, Cawston Press, and a business coach with the Actioncoach franchise. “But I think that the inclination to break the mould and the desire for success, including fi nancial success, tend to go hand in hand.”

Rupert Hodson is co-founder of Dianomi, which provides online marketing for fi nancial services fi rms. His main motivation for setting up the company was the desire to be his own boss and the fl exibility that goes with it. “Financial security for my family is also increasingly on my mind; you can achieve that in other ways, but this is a more focused and exciting way, and you get a great sense of achievement,” he says.

Motivations may change to some extent once the business is up and running. The desire for personal satisfaction in one’s work becomes stronger, while the novelty of running one’s own show loses some of its appeal. Retirement considerations—fi nancial security and the potential to retire early—also become more pertinent, unsurprisingly.

Mr Unwin makes the interesting point that many entrepreneurs fi nd themselves being business owners by chance, rather than as a result of strategically planning a start-up. “Cawston Press started because I was running a juice fi rm called Copella, which included the Cawston brand, and was offered the chance to buy back the Cawston part of it when the whole fi rm was sold to Tropicana,” he says. “It’s not unusual to end up with a business through such an opportunity or because you inherited it, but it still takes an entrepreneurial mindset to commit to that route.”

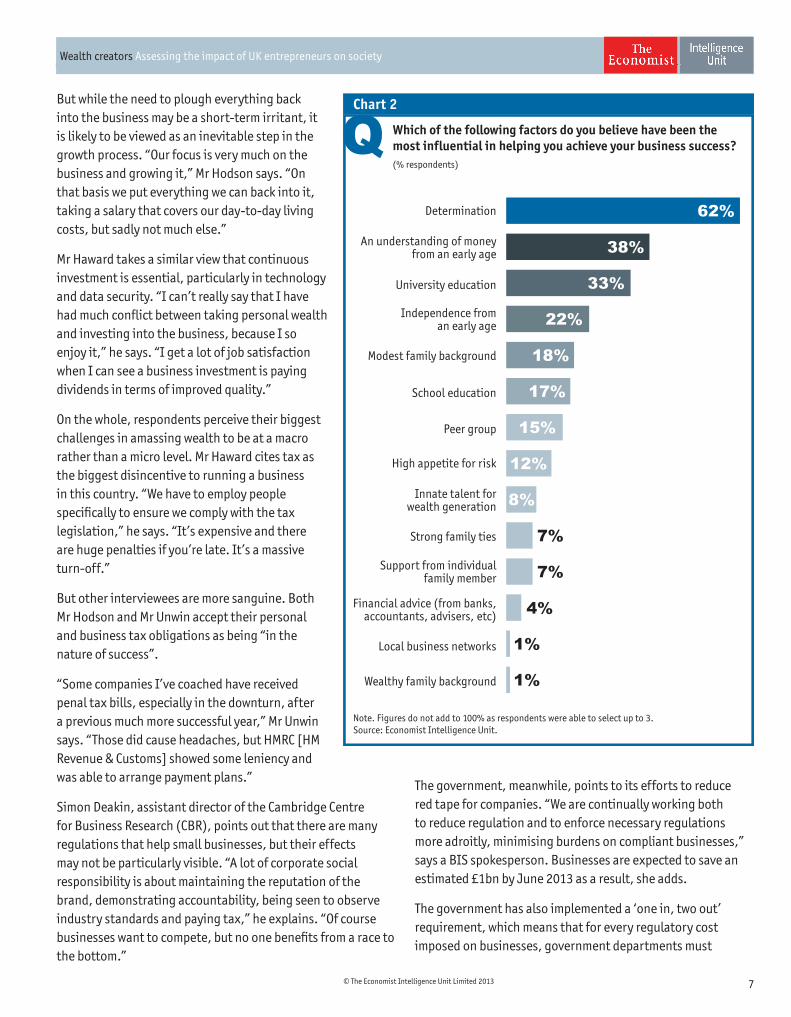

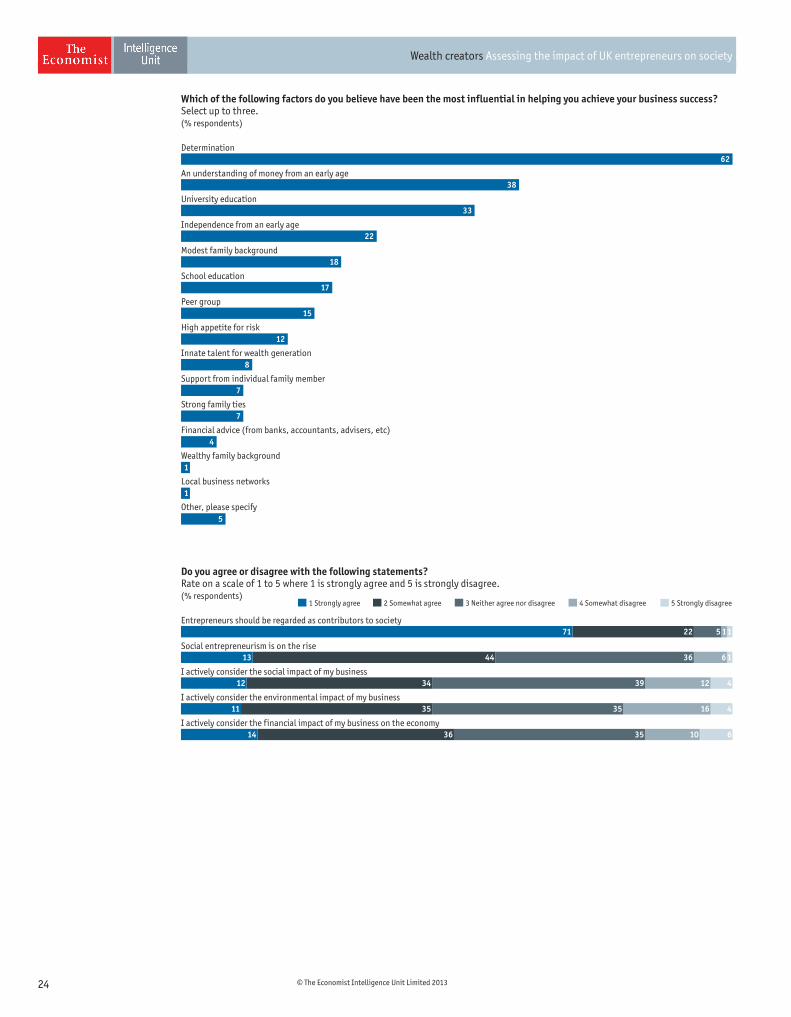

What factors do entrepreneurs consider most infl uential in their success as business owners? Sheer determination to succeed is considered by far the most important element in success, with 62% of respondents citing it. Perhaps surprisingly, bearing in mind the ebullient character of many high-profi le wealth creators,

Entrepreneurial driving forces1True entrepreneurs are ambitious, restless and looking for new challenges; they’ve always wanted to do their own thing and hate to be constrained. I think that the inclination to break the mould and the desire for success, including fi nancial success, tend to go hand in hand.

Stephen Unwin

Founder of Cawston Press,

Business coach with the Actioncoach franchise

6 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

few respondents (8%) claim any innate talent for wealth generation, and only 12% put it down to a hearty appetite for risk.

However, Jonathan Haward, founder of the property search fi rm, The County Homesearch Company, and, more recently, of the online memorial service, Friends and Relations, makes the point that anyone who sets up their own business has to be a risk-taker. “The important

thing is that it is a calculated risk and you have all your ducks in a row when you do it,” he adds.

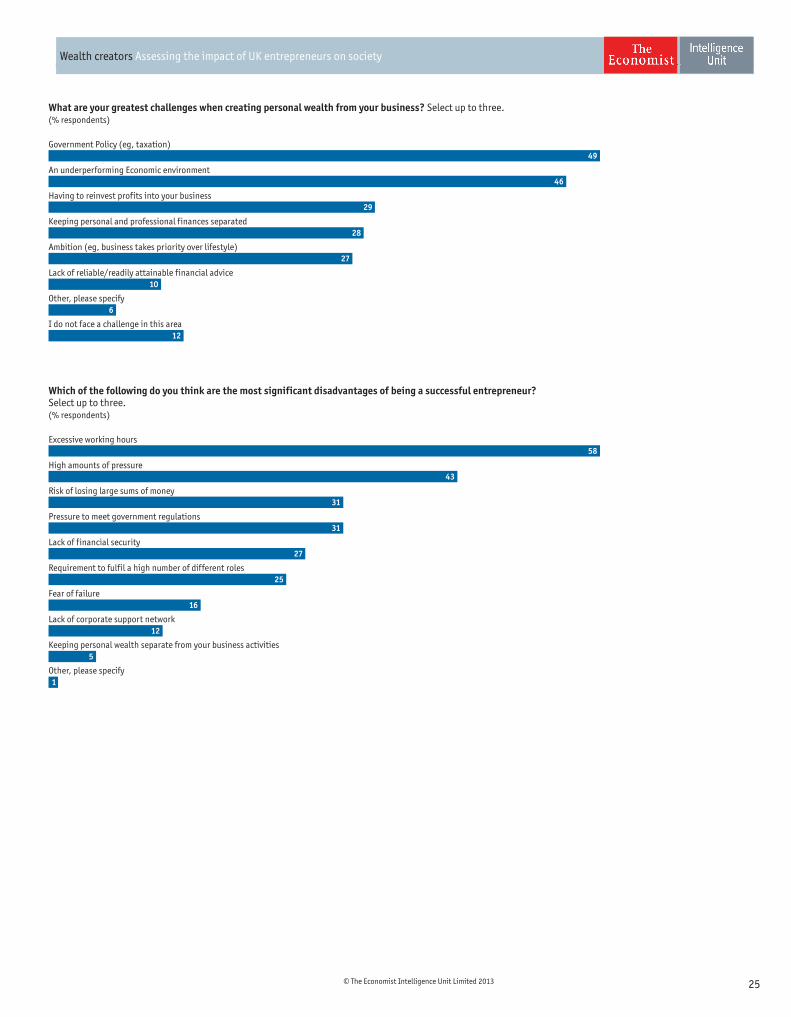

As noted, accessible wealth can be an elusive concept for many business owners, particularly those in the early stages of business growth. Almost one-third (29%) of respondents say that the need to reinvest profi ts presented a challenge to creating personal wealth from their businesses during that time.

Ability to be my own boss

Personal satisfaction in my work

Financial independence

A better personal lifestyle

Seizing opportunity

Being able to create somethingnew/innovative

Financial security in retirement

Enjoyment of making money

Ability to retire early

Personal development

Financial security for children

Being able to contribute to theeconomy/society (eg, through

employment, etc)

Being able to help others(eg, through philanthropy, etc)

Status

Now running businessWhen starting business

What were the main motivations for you to start your business and create wealth?What are the main motivations for you to run your business and create wealth?(% respondents)

Chart 1

Note. Figures do not add to 100% as respondents were able to select up to 3.Source: The Economist Intelligence Unit.

43%

45%

30%

29%

6%

12%

22%

12%

15%

7%

13%

7%

9%

4%

55%

38%

31%

25%

18%

17%

14%

12%

11%

10%

7%

7%

4%

3%

7© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

But while the need to plough everything back into the business may be a short-term irritant, it is likely to be viewed as an inevitable step in the growth process. “Our focus is very much on the business and growing it,” Mr Hodson says. “On that basis we put everything we can back into it, taking a salary that covers our day-to-day living costs, but sadly not much else.”

Mr Haward takes a similar view that continuous investment is essential, particularly in technology and data security. “I can’t really say that I have had much confl ict between taking personal wealth and investing into the business, because I so enjoy it,” he says. “I get a lot of job satisfaction when I can see a business investment is paying dividends in terms of improved quality.”

On the whole, respondents perceive their biggest challenges in amassing wealth to be at a macro rather than a micro level. Mr Haward cites tax as the biggest disincentive to running a business in this country. “We have to employ people specifi cally to ensure we comply with the tax legislation,” he says. “It’s expensive and there are huge penalties if you’re late. It’s a massive turn-off.”

But other interviewees are more sanguine. Both Mr Hodson and Mr Unwin accept their personal and business tax obligations as being “in the nature of success”.

“Some companies I’ve coached have received penal tax bills, especially in the downturn, after a previous much more successful year,” Mr Unwin says. “Those did cause headaches, but HMRC [HM Revenue & Customs] showed some leniency and was able to arrange payment plans.”

Simon Deakin, assistant director of the Cambridge Centre for Business Research (CBR), points out that there are many regulations that help small businesses, but their effects may not be particularly visible. “A lot of corporate social responsibility is about maintaining the reputation of the brand, demonstrating accountability, being seen to observe industry standards and paying tax,” he explains. “Of course businesses want to compete, but no one benefi ts from a race to the bottom.”

The government, meanwhile, points to its efforts to reduce red tape for companies. “We are continually working both to reduce regulation and to enforce necessary regulations more adroitly, minimising burdens on compliant businesses,” says a BIS spokesperson. Businesses are expected to save an estimated £1bn by June 2013 as a result, she adds.

The government has also implemented a ‘one in, two out’ requirement, which means that for every regulatory cost imposed on businesses, government departments must

Chart 2

Which of the following factors do you believe have been themost influential in helping you achieve your business success?(% respondents)

Note. Figures do not add to 100% as respondents were able to select up to 3.Source: Economist Intelligence Unit.

Determination

An understanding of moneyfrom an early age

University education

Independence froman early age

Modest family background

School education

Peer group

High appetite for risk

Innate talent forwealth generation

Strong family ties

Support from individualfamily member

Financial advice (from banks,accountants, advisers, etc)

Local business networks

Wealthy family background

8%

4%

1%

1%

12%

15%

17%

18%

22%

33%

62%

38%

7%

7%

8 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

implement savings worth double that sum. “This is a major culture change that puts Whitehall on the side of business,” the BIS spokesperson claims.

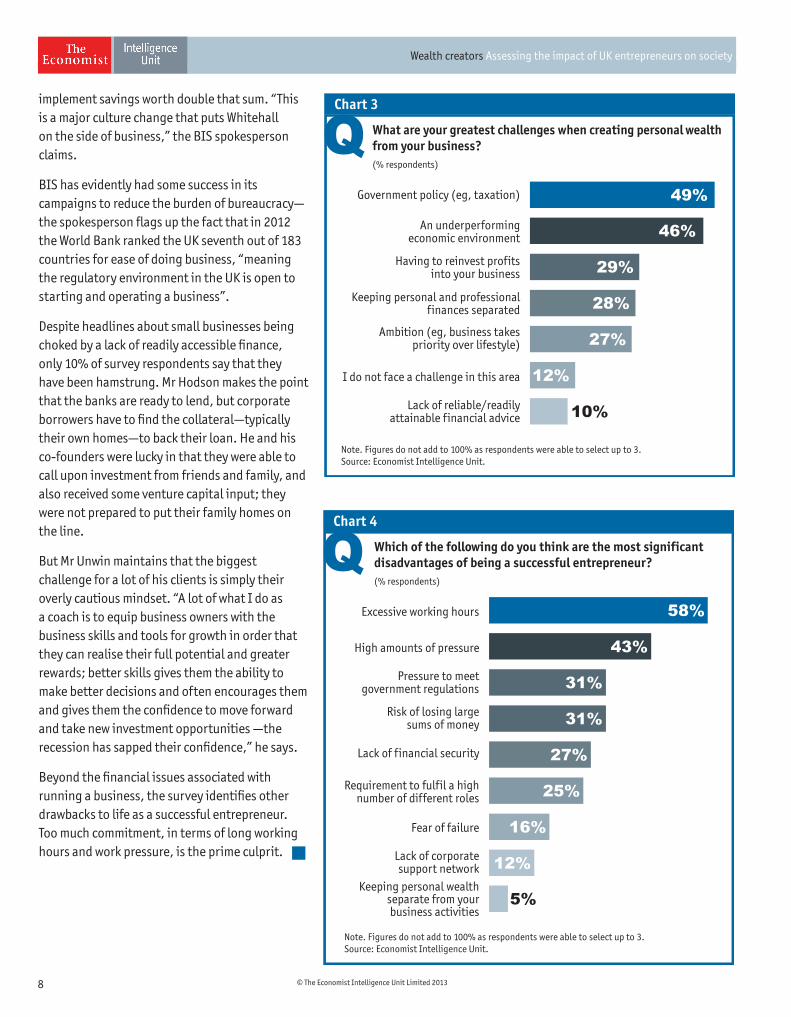

BIS has evidently had some success in its campaigns to reduce the burden of bureaucracy—the spokesperson fl ags up the fact that in 2012 the World Bank ranked the UK seventh out of 183 countries for ease of doing business, “meaning the regulatory environment in the UK is open to starting and operating a business”.

Despite headlines about small businesses being choked by a lack of readily accessible fi nance, only 10% of survey respondents say that they have been hamstrung. Mr Hodson makes the point that the banks are ready to lend, but corporate borrowers have to fi nd the collateral—typically their own homes—to back their loan. He and his co-founders were lucky in that they were able to call upon investment from friends and family, and also received some venture capital input; they were not prepared to put their family homes on the line.

But Mr Unwin maintains that the biggest challenge for a lot of his clients is simply their overly cautious mindset. “A lot of what I do as a coach is to equip business owners with the business skills and tools for growth in order that they can realise their full potential and greater rewards; better skills gives them the ability to make better decisions and often encourages them and gives them the confi dence to move forward and take new investment opportunities —the recession has sapped their confi dence,” he says.

Beyond the fi nancial issues associated with running a business, the survey identifi es other drawbacks to life as a successful entrepreneur. Too much commitment, in terms of long working hours and work pressure, is the prime culprit.

Chart 3

What are your greatest challenges when creating personal wealthfrom your business?(% respondents)

Note. Figures do not add to 100% as respondents were able to select up to 3.Source: Economist Intelligence Unit.

Government policy (eg, taxation)

An underperformingeconomic environment

Having to reinvest profitsinto your business

Keeping personal and professionalfinances separated

Ambition (eg, business takespriority over lifestyle)

I do not face a challenge in this area

Lack of reliable/readilyattainable financial advice 10%

12%

27%

28%

29%

49%

46%

Chart 4

Which of the following do you think are the most significantdisadvantages of being a successful entrepreneur?(% respondents)

High amounts of pressure

Excessive working hours

Pressure to meetgovernment regulations

Risk of losing largesums of money

Lack of financial security

Requirement to fulfil a highnumber of different roles

Fear of failure

Lack of corporatesupport network

Keeping personal wealthseparate from yourbusiness activities

Note. Figures do not add to 100% as respondents were able to select up to 3.Source: Economist Intelligence Unit.

16%

25%

27%

31%

31%

58%

43%

12%

5%

9© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

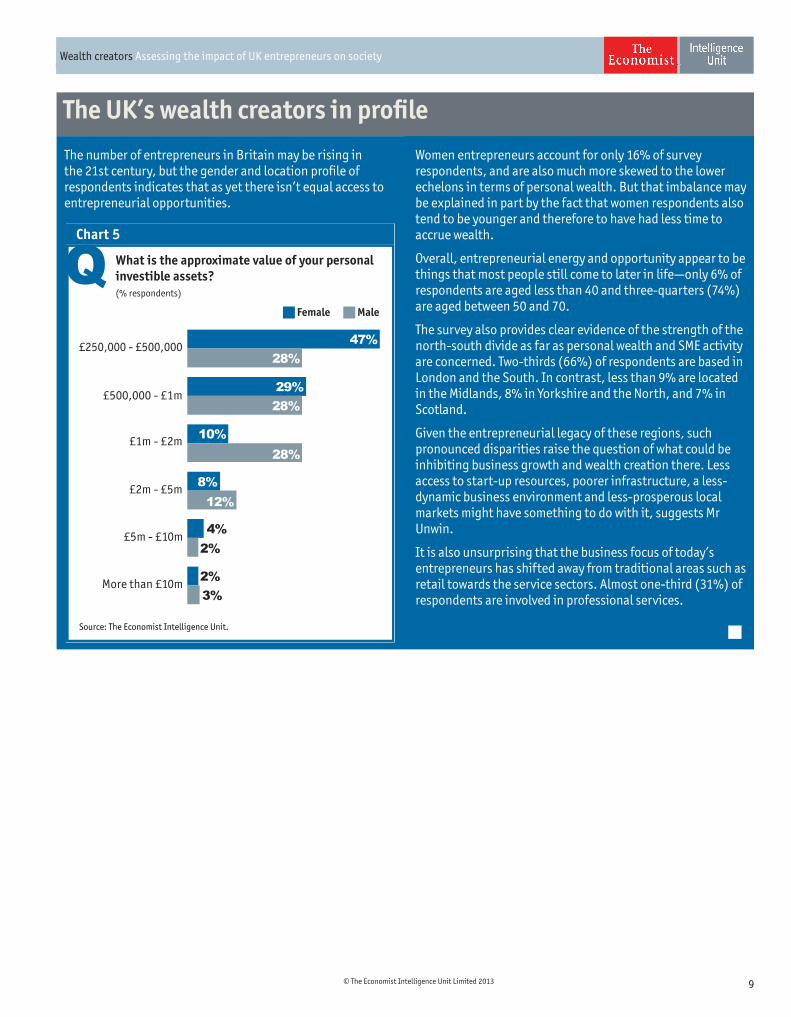

Women entrepreneurs account for only 16% of survey respondents, and are also much more skewed to the lower echelons in terms of personal wealth. But that imbalance may be explained in part by the fact that women respondents also tend to be younger and therefore to have had less time to accrue wealth.

Overall, entrepreneurial energy and opportunity appear to be things that most people still come to later in life—only 6% of respondents are aged less than 40 and three-quarters (74%) are aged between 50 and 70.

The survey also provides clear evidence of the strength of the north-south divide as far as personal wealth and SME activity are concerned. Two-thirds (66%) of respondents are based in London and the South. In contrast, less than 9% are located in the Midlands, 8% in Yorkshire and the North, and 7% in Scotland.

Given the entrepreneurial legacy of these regions, such pronounced disparities raise the question of what could be inhibiting business growth and wealth creation there. Less access to start-up resources, poorer infrastructure, a less-dynamic business environment and less-prosperous local markets might have something to do with it, suggests Mr Unwin.

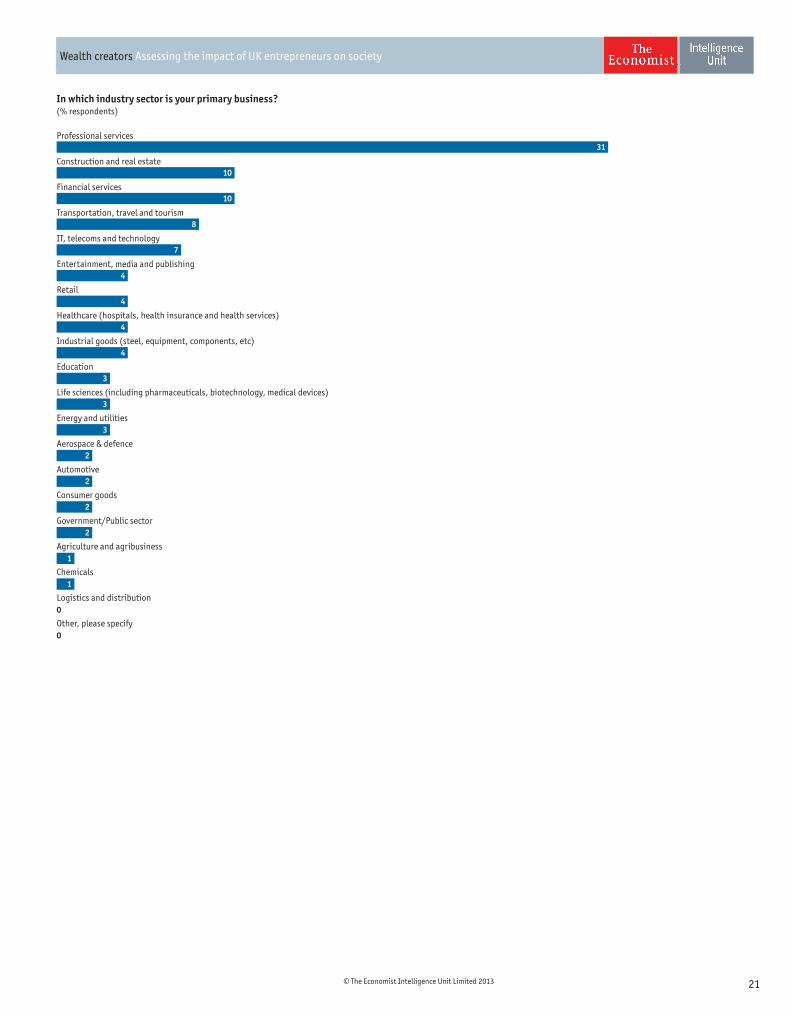

It is also unsurprising that the business focus of today’s entrepreneurs has shifted away from traditional areas such as retail towards the service sectors. Almost one-third (31%) of respondents are involved in professional services.

The number of entrepreneurs in Britain may be rising in the 21st century, but the gender and location profi le of respondents indicates that as yet there isn’t equal access to entrepreneurial opportunities.

The UK’s wealth creators in profi le

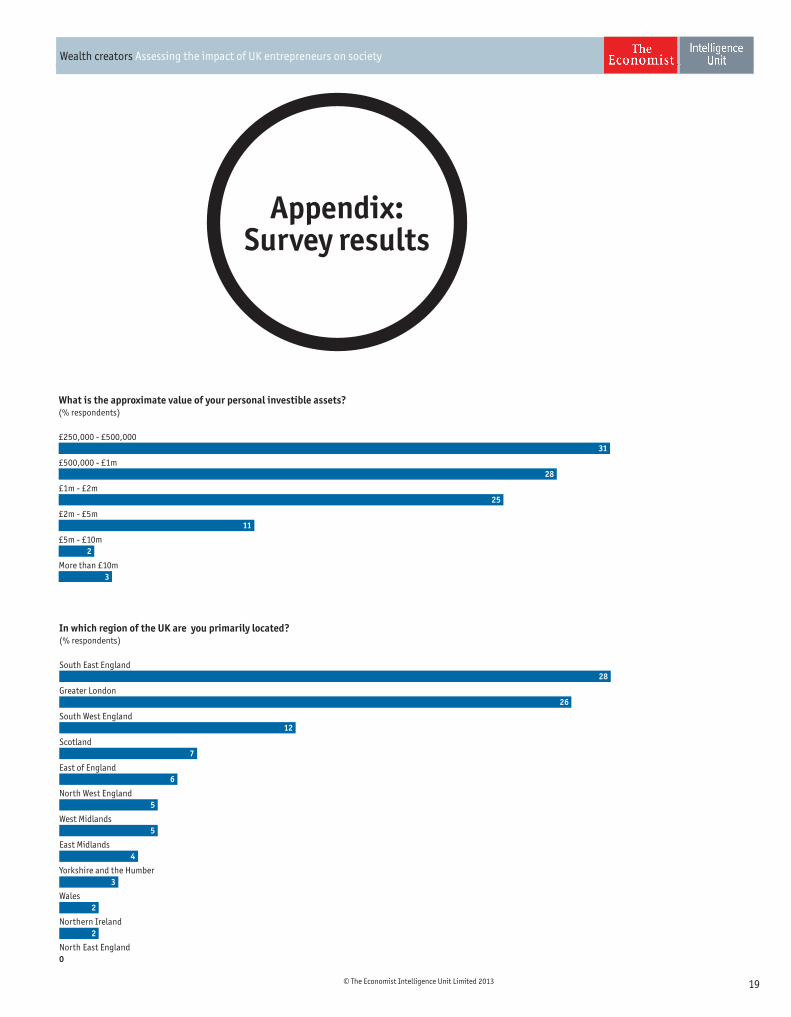

£250,000 - £500,000

£500,000 - £1m

£1m - £2m

£2m - £5m

£5m - £10m

More than £10m

Source: The Economist Intelligence Unit.

MaleFemale

What is the approximate value of your personalinvestible assets? (% respondents)

Chart 5

28%47%

28%29%

28%10%

12%8%

2%4%

2%3%

10 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Business owners have a strong sense that their role is an important one in social terms—93% of respondents believe that entrepreneurs make a positive contribution to society.

This conviction is most pronounced among those with more than £2m in personal investible assets (98%), and also among those who have set up four or more businesses over the course of their career (100%). That may be because they are able to take a longer, less-introspective perspective on the wider impact of their business; less generously, it could also refl ect a tendency towards self-aggrandisement among longer-established entrepreneurs.

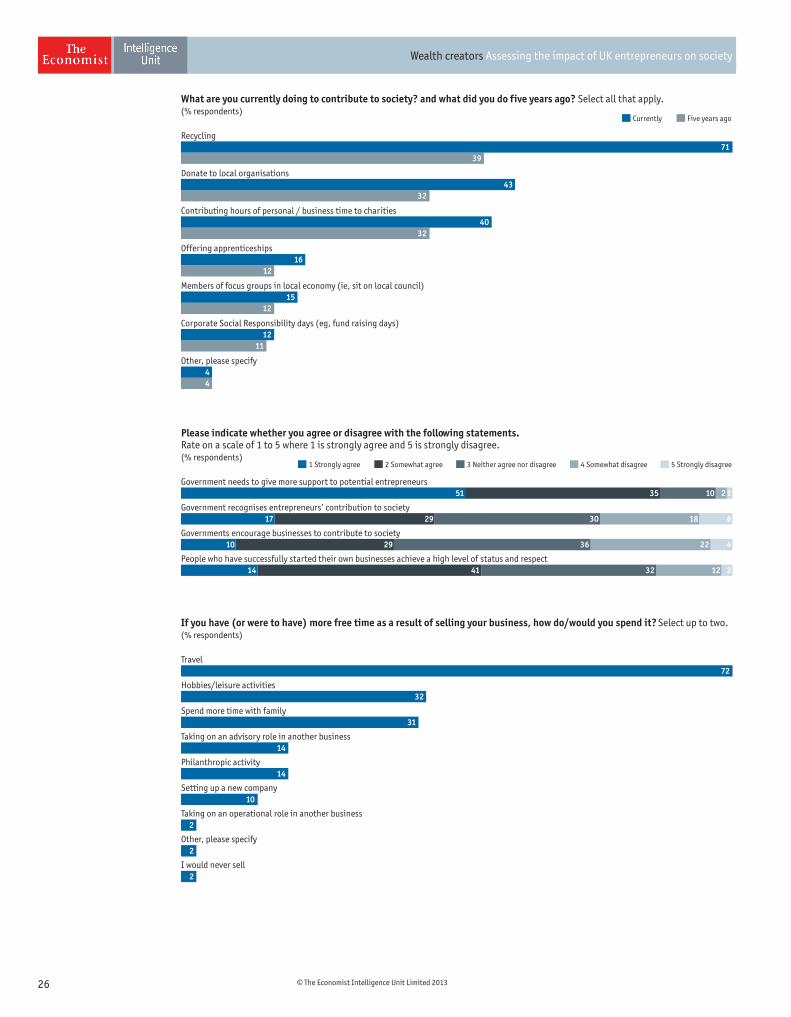

There is also a perception that social problems are increasingly being identifi ed, managed and, in some cases, resolved using entrepreneurial principles. Overall, 57% maintain that social entrepreneurship is on the rise, with women particularly aware of its growing impact (71%).

When it comes to active business engagement with wider issues, respondents are less committed. Less than half (46%) say that they actively consider the social impact of their business, with a similar proportion actively concerned about the environmental impact.

According to the BIS spokesperson, however, it is increasingly the case that businesses do go beyond their minimum statutory obligations in various areas, including social and environmental issues. “This may have a short-term [dampening] effect on profi t, but the motivation for undertaking such activity is rooted in a more long-term, sustainable ambition,” she says.

Entrepreneurs and social responsibility2

Mr Unwin suggests that where sustainable values lead, a profi table business should follow. “A lot of what I do as a coach is to get business owners to recognise their own core values and how important these are to the business and its success,” he says. “For example, if they consider business integrity, environmental awareness and support of their workers are key values of their business, they can proactively communicate that to their customers, and it can provide a competitive advantage, enabling the business to prosper.”

But as Mr Haward observes, in a small business, decisions to do with social and environmental responsibility are likely to be a refl ection of what makes fi nancial and business sense. “We recycle and have a travel policy involving fewer fl ights and more train journeys,” he says. “But although these are green policies, the decisions are partly driven by the bottom line; the two are often linked.” In fact, recycling is the area that has seen the biggest increase among the entrepreneurs surveyed, with 71% currently doing so compared with 39% fi ve years ago.

Entrepreneurs have increased their active social contributions in the past fi ve years in a range of areas, although there is wide variation in levels of activity.

Two-fi fths of respondents contribute their own or their business’s time to local organisations or charitable causes. Time is donated most generously by wealthier individuals (62% of those with more than £2m in personal assets), who may be less personally involved in the day-to-day operation of their companies.

11© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Mr Unwin observes that companies tend to feel some responsibility to support local good causes, and also have a certain self-interest in doing so, particularly if they trade with the local area. “They do it in part to foster a good working relationship with their neighbours,” he says. “But overall, the smaller the company, the less spare money or time there is.”

In contrast, other contributions such as apprenticeships (16%) and business support groups (15%) are less popular. Mr Haward makes the point that community-focused business organisations such as the Round Table do a lot of good work, but membership fees are considered a non-essential in these straitened times.

So what form do these social contributions take in practice? The idea of support for newcomers is an appealing one among interviewees. Mr Unwin, for instance, does not charge for his coaching expertise if clients are young, enthusiastic and keen to get his help with their business, but cannot afford to pay.

Mr Haward, meanwhile, is providing paid work experience for two young people as part of the Unlocking Cornish Potential scheme. “I think we have done the right thing in going through the offi cial work experience channel, but we would have been much better off fi nancially if we had offered unpaid internships,” he says.

For Mr Deakin’s Cambridge community, the involvement of members of business associations and the Chamber of Commerce with the CBR’s research and initiatives has been an important factor. “Once their business is established, a lot of local business people want to be seen to be giving something back, in this case by sharing their time and expertise with the university and other businesses,” he says.

They are likely to raise their own standing in the business community by doing so, but as he observes, “there is not necessarily a confl ict in having some self-interest in following a particular course of apparently altruistic action”.

Chart 6

What are you currently doing to contribute to society? What did you do to contribute tosociety five years ago? (% respondents)

Recycling

Donate to local organisations

Contributing hours of personal /business time to charities

Offering apprenticeships

Members of focus groups in localeconomy (ie, sit on local council)

Corporate Social Responsibility days(eg, fund raising days)

Other

5 years ago

Note. Figures do not add to 100% as respondents were able to select up to 3.Source: The Economist Intelligence Unit.

39%

32%

32%

12%

12%

11%

4%

71%

43%

40%

16%

15%

12%

4%

Now

12 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Again, however, smaller businesses tend to be hard-pushed to contribute in this or other ways because they are short of both ready cash and free time. “If you can make some kind of local contribution where you can see its value, then that’s a rewarding idea, but I’m not able to do that while growing a business and bringing up three kids,” says Mr Hodson.

So are business owners really giving enough back to society? Mr Haward stresses that they already play key roles and should not be automatically expected to do more. “We provide employment, we pay and collect taxes—what more do you want?” he says.

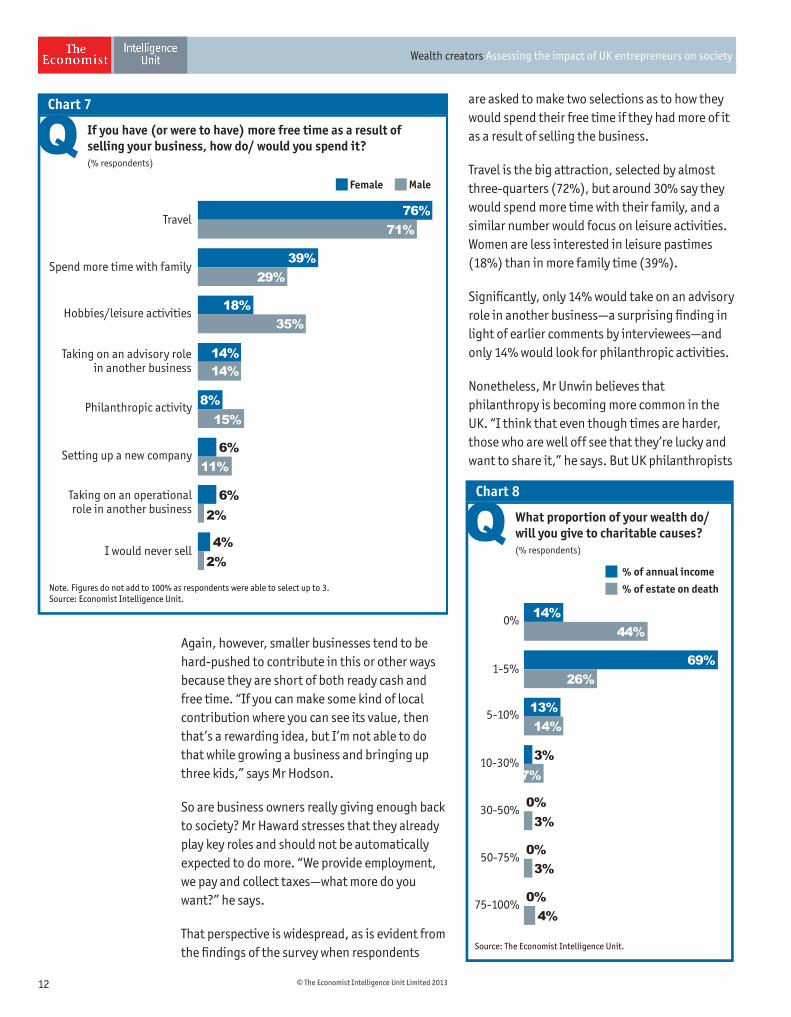

That perspective is widespread, as is evident from the fi ndings of the survey when respondents

are asked to make two selections as to how they would spend their free time if they had more of it as a result of selling the business.

Travel is the big attraction, selected by almost three-quarters (72%), but around 30% say they would spend more time with their family, and a similar number would focus on leisure activities. Women are less interested in leisure pastimes (18%) than in more family time (39%).

Signifi cantly, only 14% would take on an advisory role in another business—a surprising fi nding in light of earlier comments by interviewees—and only 14% would look for philanthropic activities.

Nonetheless, Mr Unwin believes that philanthropy is becoming more common in the UK. “I think that even though times are harder, those who are well off see that they’re lucky and want to share it,” he says. But UK philanthropists

Travel

Spend more time with family

Hobbies/leisure activities

Taking on an advisory rolein another business

Philanthropic activity

Setting up a new company

Taking on an operationalrole in another business

I would never sell

Note. Figures do not add to 100% as respondents were able to select up to 3.Source: Economist Intelligence Unit.

MaleFemale

If you have (or were to have) more free time as a result ofselling your business, how do/ would you spend it?(% respondents)

Chart 7

71%76%

29%39%

35%18%

14%14%

15%8%

6%11%

2%6%

2%4%

Source: The Economist Intelligence Unit.

% of estate on death% of annual income

What proportion of your wealth do/will you give to charitable causes? (% respondents)

Chart 8

26%

0%

1-5%

5-10%

10-30%

30-50%

50-75%

Source: The Economist Intelligence Unit.

44%14%

26%69%

14%13%

7%3%

3%0%

0%3%

75-100%0%4%

13© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

do not have the tax incentives that are in place in the US.

Smaller-scale charitable giving is widespread among entrepreneurs, however. Only 14% of respondents donate nothing to charitable causes (compared with 45% of the population at large in 2011/12), although most (69%) give less than 5% of their annual income. Women are more likely to give a higher proportion, with one-quarter of female respondents donating between 5% and 30% of their income to charity, compared with 15% of males.

In contrast, charitable bequests are much less commonplace—overall, 44% of respondents have made no charitable provision in their will, although a further 40% plan to leave up to 10% of their estate to charity.

the world for a huge range of activities, from gardening for an elderly neighbour or cleaning beaches to donating blood. “It shows there’s a willingness to volunteer time, even though people don’t have much money to spare generally,” says Mr Haward.

Following Mr Haward’s charitable trek to Chile, employees at the County Homesearch Company are also offered a four-week sabbatical after they have worked there for fi ve years, provided they use the time to go on a fund-raising adventure trip.

Although there is a clear sense that SME owners have plenty on their plates simply running and growing their businesses, it is equally clear that many people would like to give something back to the community, whether on an individual or a corporate basis.

Mr Haward, who is based in Truro, Cornwall, was involved in setting up the Jubilee Hour project, whereby companies or individuals pledged an hour doing something charitable or helpful to mark the Queen’s Jubilee year in 2012. More than 2.75 million hours were pledged around

Innovative social contributions

14 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Is there a mismatch between the positive perceptions of the role of wealth creators in society and the extent of formal support provided by the government for entrepreneurs starting out and existing businesses?

The present government has talked a lot about its commitment to an entrepreneur-friendly environment, not least because of the importance of grassroots growth in kick-starting the sluggish economy. “We know that our entrepreneurs drive growth, so we will continue to do everything we can to help unleash and unlock entrepreneurs’ potential,” said business

The role of government3minister Michael Fallon in October 2012. To that end, he cites “the additional tax relief for angel investment, reforms to employment law, investment in business mentoring and further cuts in red tape”.

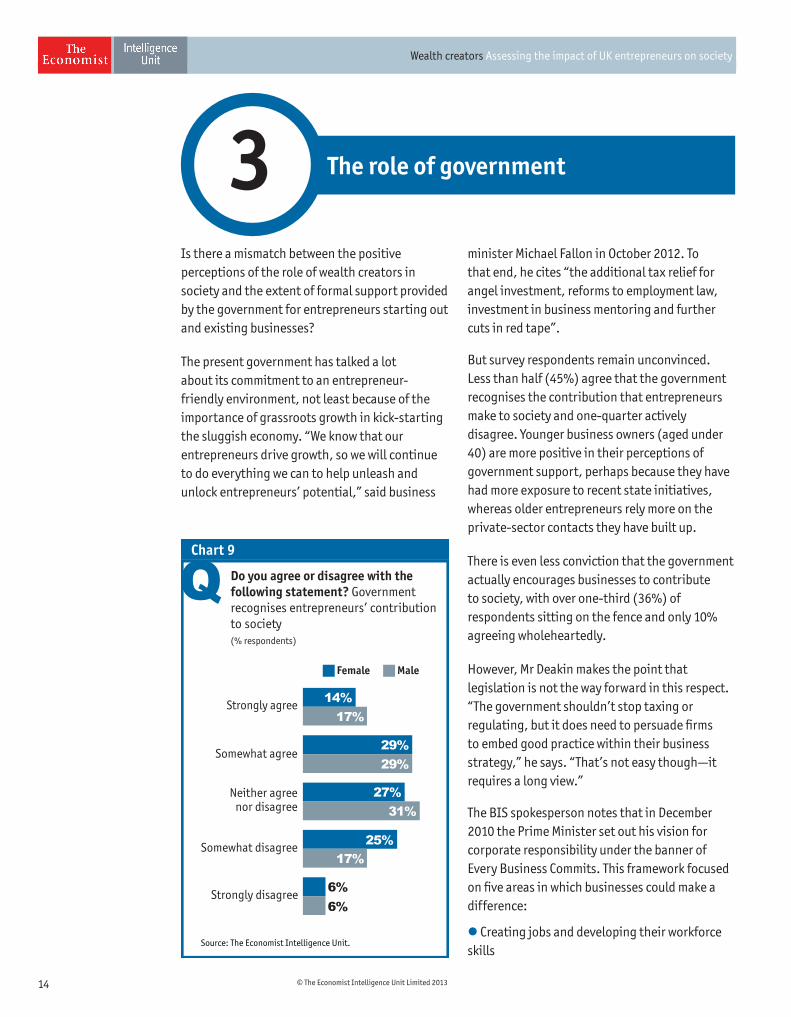

But survey respondents remain unconvinced. Less than half (45%) agree that the government recognises the contribution that entrepreneurs make to society and one-quarter actively disagree. Younger business owners (aged under 40) are more positive in their perceptions of government support, perhaps because they have had more exposure to recent state initiatives, whereas older entrepreneurs rely more on the private-sector contacts they have built up.

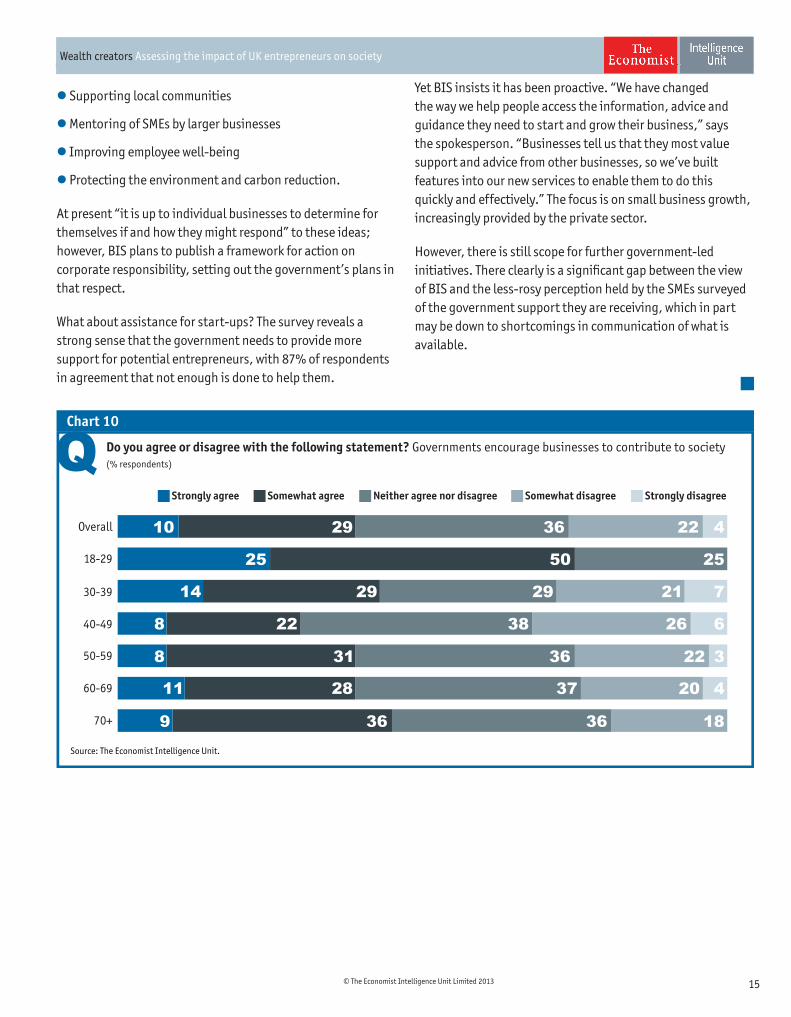

There is even less conviction that the government actually encourages businesses to contribute to society, with over one-third (36%) of respondents sitting on the fence and only 10% agreeing wholeheartedly.

However, Mr Deakin makes the point that legislation is not the way forward in this respect. “The government shouldn’t stop taxing or regulating, but it does need to persuade fi rms to embed good practice within their business strategy,” he says. “That’s not easy though—it requires a long view.”

The BIS spokesperson notes that in December 2010 the Prime Minister set out his vision for corporate responsibility under the banner of Every Business Commits. This framework focused on fi ve areas in which businesses could make a difference:

Creating jobs and developing their workforce skills

Strongly agree

Somewhat agree

Neither agreenor disagree

Somewhat disagree

Strongly disagree

Source: The Economist Intelligence Unit.

MaleFemale

Do you agree or disagree with thefollowing statement? Governmentrecognises entrepreneurs’ contributionto society(% respondents)

Chart 9

17%14%

29%29%

31%27%

17%25%

6%6%

15© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Yet BIS insists it has been proactive. “We have changed the way we help people access the information, advice and guidance they need to start and grow their business,” says the spokesperson. “Businesses tell us that they most value support and advice from other businesses, so we’ve built features into our new services to enable them to do this quickly and effectively.” The focus is on small business growth, increasingly provided by the private sector.

However, there is still scope for further government-led initiatives. There clearly is a signifi cant gap between the view of BIS and the less-rosy perception held by the SMEs surveyed of the government support they are receiving, which in part may be down to shortcomings in communication of what is available.

Supporting local communities

Mentoring of SMEs by larger businesses

Improving employee well-being

Protecting the environment and carbon reduction.

At present “it is up to individual businesses to determine for themselves if and how they might respond” to these ideas; however, BIS plans to publish a framework for action on corporate responsibility, setting out the government’s plans in that respect.

What about assistance for start-ups? The survey reveals a strong sense that the government needs to provide more support for potential entrepreneurs, with 87% of respondents in agreement that not enough is done to help them.

Overall

18-29

30-39

40-49

50-59

60-69

70+

Do you agree or disagree with the following statement? Governments encourage businesses to contribute to society(% respondents)

Chart 10

Source: The Economist Intelligence Unit.

10

25

14

8

8

11

9

29

29

22

31

28

36

36

50

29

38

36

37

36

22

25

21

26

22

20

4

7

6

3

4

18

Strongly disagreeSomewhat disagreeNeither agree nor disagreeSomewhat agreeStrongly agree

16 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Young people aged 18-30 can now apply for a start-up loan; an additional £3m has been added to the fund, taking the total available to £110m (www.startuploans.co.uk).

There are also several fi nance schemes in place, including the Enterprise Finance Guarantee scheme for businesses without the collateral or track record to access bank lending; Enterprise Capital Funds, in the shape of venture capital for new businesses with high growth potential; the Business Finance Partnership, which provides alternative sources of lending; and the Funding for Lending scheme, which is encouraging banks to lend more freely.

Business in You, launched in January 2012, is designed to inspire would-be entrepreneurs and highlight the range of support available (www.businessinyou.bis.gov.uk).

The mentoring portal, www.mentorsme.co.uk, provides a single access point to bring together mentoring organisations and those looking for guidance. Services may be free or paid-for. There are now 27,000 mentors across the UK listed on the portal.

SMEs with potential for rapid growth could apply to www.growthaccelerator.com for additional help from a qualifi ed coach.

Government initiatives to support SMEs

17© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Conclusion

better direct, effective channels of communication between the powers that be and small business communities around the country.

Similarly, the government has work to do in promoting the various ways in which businesses can make valuable and rewarding social contributions beyond providing employment and paying tax. BIS’s forthcoming framework for corporate responsibility should help to clarify best practice, but it will need to think laterally about how best to get the message to companies, and how to help them embed these ideas sustainably in their business over the long term.

The bottom line is that wealth creators remain the bedrock of the UK’s economy, with a crucial role to play both in driving the economic growth that has proved so elusive in recent years, and also in shaping and embedding good business practices in this country; their importance to wider prosperity cannot be overstated.

Crucially, they are running their own businesses because they are happy to embrace the vulnerabilities as well as the opportunities of being their own boss. Indeed, they have pride in their entrepreneurial status and in many cases are keen to share their knowledge and experience with others. If they receive the targeted, innovative support they need from government- and community-based sources, their ranks are likely to swell.

Wealth creators have faced major challenges over the past few diffi cult years, yet there is no sign of the taste for entrepreneurship dwindling in the UK—indeed, it’s quite the reverse, as SME and start-up numbers continue to rise.

As they probably always have been, wealth creators are determined and patient players, prepared to invest and reinvest to realise their business vision. However, they are driven less by the dream of wealth for its own sake than by the independence, fl exibility and job satisfaction they associate with running their own business.

At the same time, they are also increasingly aware of their potential to make broader social contributions in a variety of ways and of the fact that such social and environmental efforts can pay dividends over time in terms of making their business more sustainable and strengthening its public image.

But while such efforts are seen as feasible for thriving, growing businesses, the perception is that they are beyond the means of the smallest enterprises, which simply do not have either the time or means to invest in socially orientated initiatives.

It is evident that this government’s initiatives to nurture enterprise and improve business conditions have not percolated through effectively to SME owners who might benefi t from them. Business owners are still inclined to see much of what the government does in terms of regulation and tax as restrictive and designed to make their lives more diffi cult, suggesting that part of the issue is to do with building

18 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

spillover, has opened up lots of opportunities for small businesses in Cambridge. “With the right government-investment programme, similar high-tech clusters could be nurtured in large cities too,” he says. “Firms can grow their capabilities, but they require an environment that’s resource-rich, which Cambridge is.”

To make technology start-ups easier, Mr Deakin believes that the government should relax the rules regarding employee mobility. “Highly skilled employees cannot move easily between fi rms as things stand,” he says. “They have to take gardening leave, but new businesses really need to be able to recruit industry knowledge and skill.”

Mr Unwin believes that incentives and regulations are in place to support entrepreneurs, but that they need to be encouraged towards a less-negative outlook. He has been asked by a bank to talk to local business owners to help them develop a more positive, entrepreneurial mindset focused on growing their business and learning new skills rather than merely surviving.

The bottom line is that the government needs to promote its various support channels more effectively, perhaps not so much to new businesses, which are likely to be actively exploring such opportunities, but to more established enterprises that could nonetheless benefi t.

Mr Haward would like to see a committee of small business owners set up to report back to government on the real practical problems facing the sector. “The government needs a reality check and this would be fantastic,” he says.

He also suggests a government-backed programme of seminars “where successful people can pass on precisely what’s involved in running a business, talk to budding entrepreneurs and assess their business plans. It would help nurture those with potential and caution those that are likely to bomb—a sort of kindly Dragons’ Den.”

Mr Deakin points out that government investment in high-quality transport and healthcare infrastructure, as well as university

How can entrepreneurs be better supported?

19© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Appendix:Survey results

£250,000 - £500,000

£500,000 - £1m

£1m - £2m

£2m - £5m

£5m - £10m

More than £10m

31

28

25

11

2

3

(% respondents)What is the approximate value of your personal investible assets?

South East England

Greater London

South West England

Scotland

East of England

North West England

West Midlands

East Midlands

Yorkshire and the Humber

Wales

Northern Ireland

North East England

28

26

12

7

6

5

5

4

3

2

2

0

(% respondents)In which region of the UK are� you primarily located?

20 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

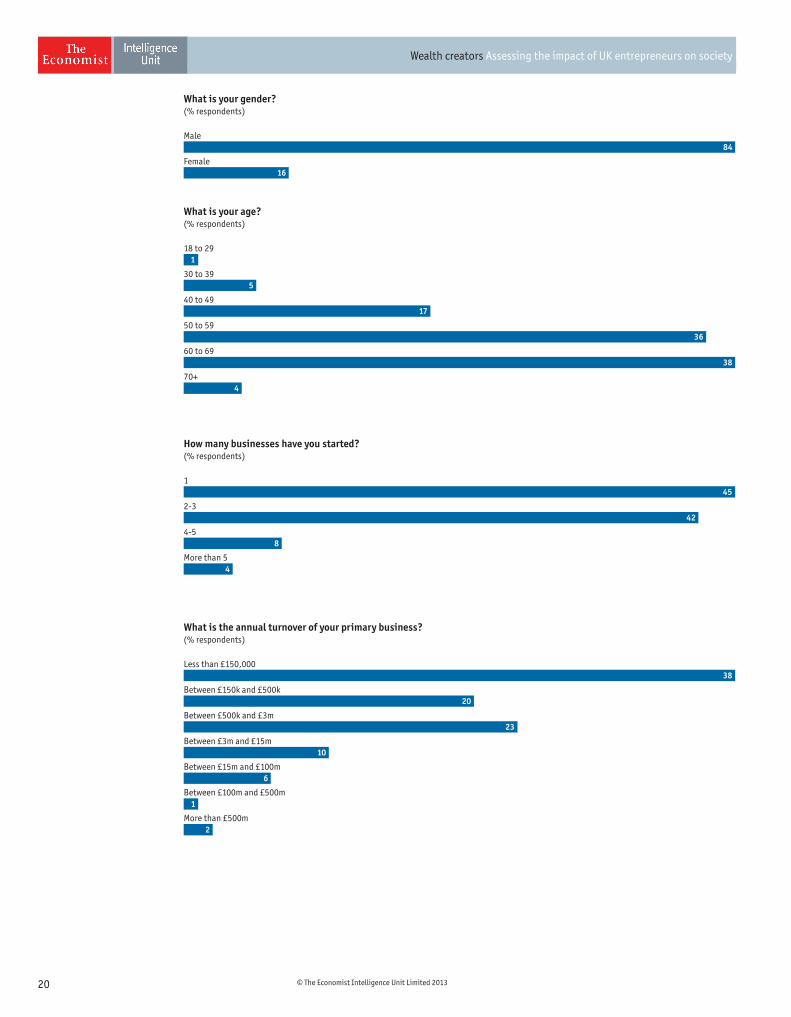

Male

Female

84

16

(% respondents)What is your gender?

18 to 29

30 to 39

40 to 49

50 to 59

60 to 69

70+

1

5

17

36

38

4

(% respondents)What is your age?

1

2-3

4-5

More than 5

45

42

8

4

(% respondents)How many businesses have you started?

Less than £150,000

Between £150k and £500k

Between £500k and £3m

Between £3m and £15m

Between £15m and £100m

Between £100m and £500m

More than £500m

38

20

23

10

6

1

2

(% respondents)What is the annual turnover of your primary business?

21© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Professional services

Construction and real estate

Financial services

Transportation, travel and tourism

IT, telecoms and technology

Entertainment, media and publishing

Retail

Healthcare (hospitals, health insurance and health services)

Industrial goods (steel, equipment, components, etc)

Education

Life sciences (including pharmaceuticals, biotechnology, medical devices)

Energy and utilities

Aerospace & defence

Automotive

Consumer goods

Government/Public sector

Agriculture and agribusiness

Chemicals

Logistics and distribution

Other, please specify

31

10

10

8

7

2

1

1

0

0

4

4

4

4

3

3

3

2

2

2

(% respondents)In which industry sector is your primary business?

22 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

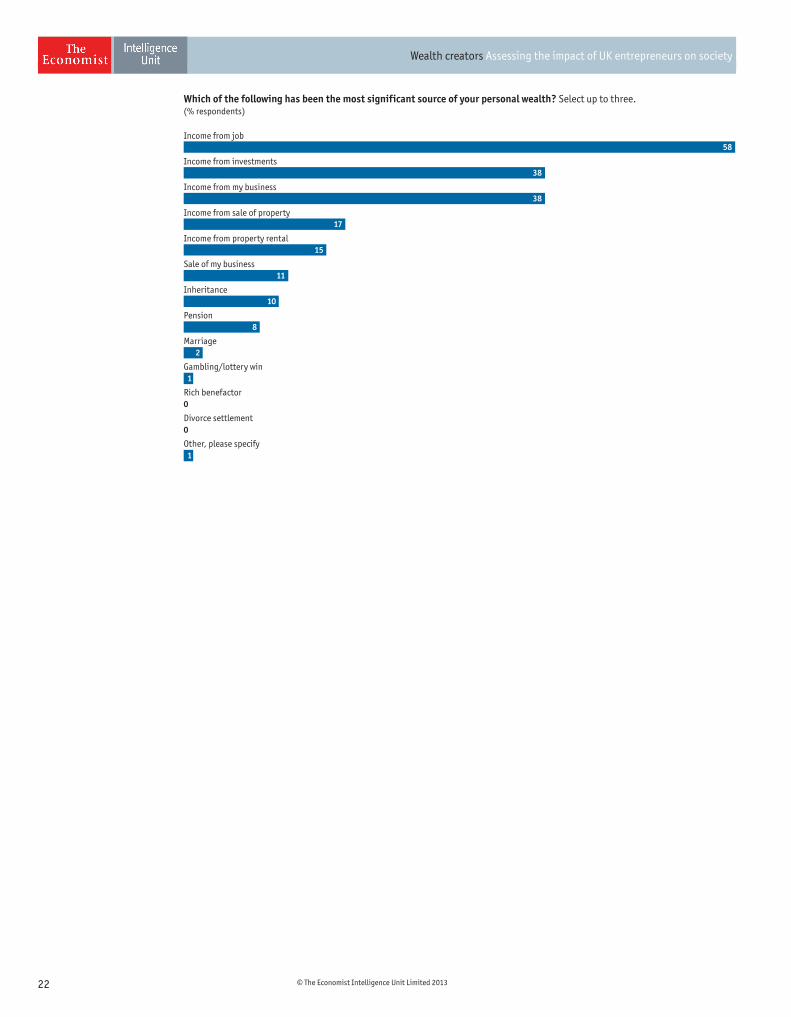

Income from job

Income from investments

Income from my business

Income from sale of property

Income from property rental

Sale of my business

Inheritance

Pension

Marriage

Gambling/lottery win

Rich benefactor

Divorce settlement

Other, please specify

58

38

38

17

15

11

10

8

2

1

0

0

1

(% respondents)Which of the following has been the most significant source of your personal wealth? Select up to three.

23© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

(% respondents)What were the main motivations for you when you were starting your business? and what are they now? Select up to three.

Ability to be my own boss

Personal satisfaction in my work

Financial independence

A better personal lifestyle

Seizing opportunity

Being able to create something new/innovative

Financial security in retirement

Enjoyment of making money

Ability to retire early

Personal development

Financial security for children

Being able to contribute to the economy/society (eg, through employment, etc)

Being able to help others (eg, through philanthropy, etc)

Status

Other, please specify

5543

3845

3130

2529

186

1712

1422

1212

1115

107

713

77

49

34

23

What were the main motivations What are the main motivations now

24 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Determination

An understanding of money from an early age

University education

Independence from an early age

Modest family background

School education

Peer group

High appetite for risk

Innate talent for wealth generation

Support from individual family member

Strong family ties

Financial advice (from banks, accountants, advisers, etc)

Wealthy family background

Local business networks

Other, please specify

62

38

33

22

18

17

15

12

8

7

7

4

1

1

5

(% respondents)

Which of the following factors do you believe have been the most influential in helping you achieve your business success?Select up to three.

1 Strongly agree 2 Somewhat agree 3 Neither agree nor disagree 4 Somewhat disagree 5 Strongly disagree

Entrepreneurs should be regarded as contributors to society

Social entrepreneurism is on the rise

I actively consider the social impact of my business

I actively consider the environmental impact of my business

I actively consider the financial impact of my business on the economy

115

1

2271

364413 6

4

4

12393412

16353511

610353614

(% respondents)

Do you agree or disagree with the following statements?Rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

25© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Government Policy (eg, taxation)

An underperforming Economic environment

Having to reinvest profits into your business

Keeping personal and professional finances separated

Ambition (eg, business takes priority over lifestyle)

Lack of reliable/readily attainable financial advice

Other, please specify

I do not face a challenge in this area

49

46

29

28

27

10

6

12

(% respondents)What are your greatest challenges when creating personal wealth from your business? Select up to three.

Excessive working hours

High amounts of pressure

Risk of losing large sums of money

Pressure to meet government regulations

Lack of financial security

Requirement to fulfil a high number of different roles

Fear of failure

Lack of corporate support network

Keeping personal wealth separate from your business activities

Other, please specify

58

43

31

31

27

25

16

12

5

1

(% respondents)

Which of the following do you think are the most significant disadvantages of being a successful entrepreneur?Select up to three.

26 © The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

Recycling

Donate to local organisations

Contributing hours of personal / business time to charities

Offering apprenticeships

Members of focus groups in local economy (ie, sit on local council)

Corporate Social Responsibility days (eg, fund raising days)

Other, please specify

7139

4332

4032

1612

1512

1211

44

Currently Five years ago(% respondents)What are you currently doing to contribute to society? and what did you do five years ago? Select all that apply.

1 Strongly agree 2 Somewhat agree 3 Neither agree nor disagree 4 Somewhat disagree 5 Strongly disagree

Government needs to give more support to potential entrepreneurs

Government recognises entrepreneurs’ contribution to society

Governments encourage businesses to contribute to society

People who have successfully started their own businesses achieve a high level of status and respect

121035

618

51

302917

422362910

212324114

(% respondents)

Please indicate whether you agree or disagree with the following statements.Rate on a scale of 1 to 5 where 1 is strongly agree and 5 is strongly disagree.

Travel

Hobbies/leisure activities

Spend more time with family

Taking on an advisory role in another business

Philanthropic activity

Setting up a new company

Taking on an operational role in another business

Other, please specify

I would never sell

72

32

31

14

14

10

2

2

2

(% respondents)If you have (or were to have) more free time as a result of selling your business, how do/would you spend it? Select up to two.

27© The Economist Intelligence Unit Limited 2013

Wealth creators Assessing the impact of UK entrepreneurs on society

0%

1-5%

5-10%

10-30%

30-50%

50-75%

75-100%

1444

6926

1314

37

03

03

04

% of income annually % of estate on death(% respondents)What proportion of your wealth do/will you give to charitable causes?

While every effort has been taken to verify the accuracy of this information, neither The Economist Intelligence Unit Ltd. nor the sponsor of this report can accept any responsibility or liability for reliance by any person on this article or any of the information, opinions or conclusions set out in this white paper.This report is sponsored by Lloyds TSB Private Banking Limited. No representation, warranty or undertaking is given or made by Lloyds TSB Private Banking Limited as to the accuracy, reasonableness or completeness of the contents of this report including any opinions or projections expressed in it.

LONDON20 Cabot SquareLondonE14 4QWUnited KingdomTel: (44.20) 7576 8000Fax: (44.20) 7576 8500E-mail: [email protected]

NEW YORK750 Third Avenue5th FloorNew York, NY 10017United StatesTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

HONG KONG6001, Central Plaza18 Harbour RoadWanchai Hong KongTel: (852) 2585 3888Fax: (852) 2802 7638E-mail: [email protected]

GENEVARue de l’Athénée 321206 GenevaSwitzerlandTel: (41) 22 566 2470Fax: (41) 22 346 93 47E-mail: [email protected]