1

ConferenceConference callcall / / WebcastWebcastRESULTS ANNOUCEMENTRESULTS ANNOUCEMENT3rd Quarter 20093rd Quarter 2009(Brazilian Corporate Law)(Brazilian Corporate Law)

Almir Guilherme Almir Guilherme BarbassaBarbassaCFO and Investor Relations OfficerCFO and Investor Relations Officer

NovemberNovember 17th, 200917th, 2009

2

The presentation may contain forecasts about future events. Such forecasts merely reflect the expectations of the Company's management. Such terms as "anticipate", "believe", "expect", "forecast", "intend", "plan", "project", "seek", "should", along with similar or analogous expressions, are used to identify such forecasts. These predictions evidently involve risks and uncertainties, whether foreseen or not by the Company. Therefore, the future results of operations may differ from current expectations, and readers must not base their expectations exclusively on the information presented herein. The Company is not obliged to update the presentation/such forecasts in light of new information or future developments.

The United States Securities and Exchange Commission permits oil and gas companies,

in their filings with the SEC, to disclose only proved reserves that a company has demonstrated by actual production or conclusive formation tests to be

economically and legally producible under existing economic and operating conditions.We use certain terms in this presentation, such as oil and gas resources, that the SEC’s guidelines strictly prohibit us from including in filings with the SEC.

CAUTIONARY STATEMENT FOR US INVESTORS

DISCLAIMER

3

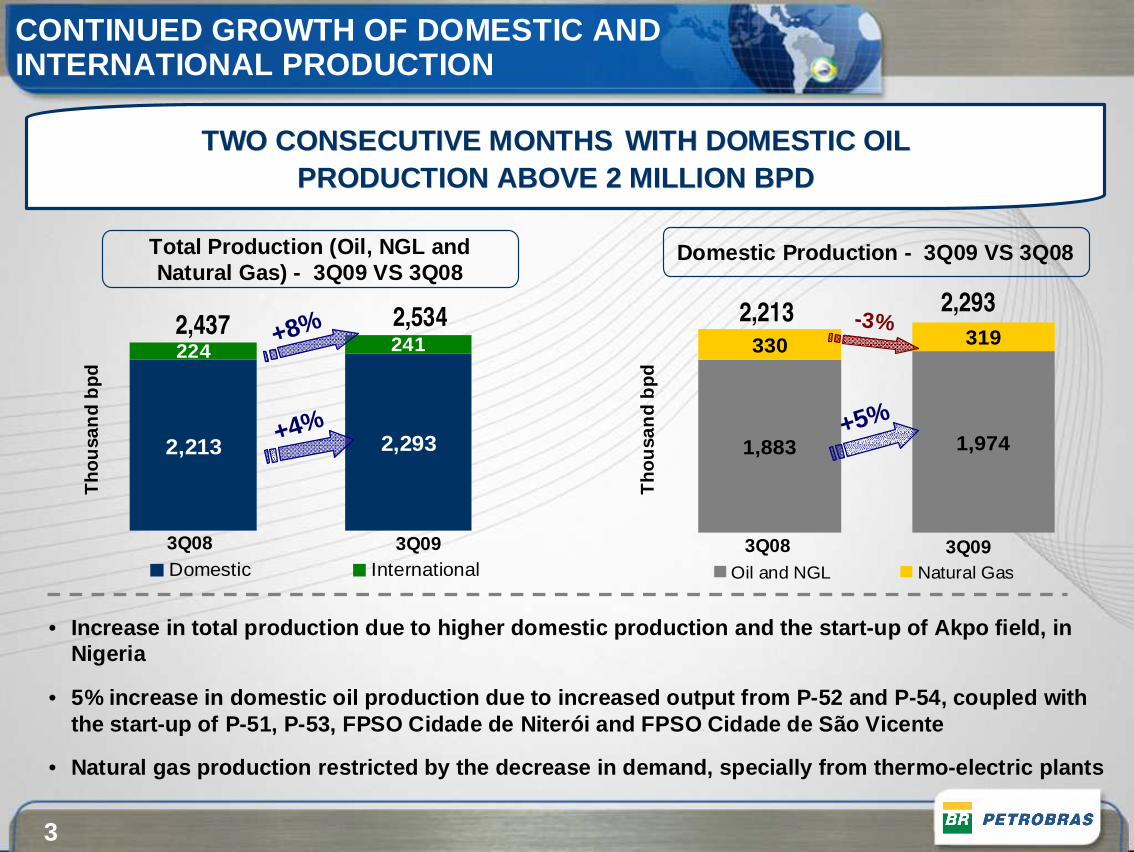

CONTINUED GROWTH OF DOMESTIC AND INTERNATIONAL PRODUCTION

Domestic Production - 3Q09 VS 3Q08

2,213 2,293

224 241

Domestic International

Total Production (Oil, NGL and Natural Gas) - 3Q09 VS 3Q08

2,437

3Q08 3Q09

2,534+8% 2,213 2,293

330 319

1,9741,883

Oil and NGL Natural Gas

+5%

TWO CONSECUTIVE MONTHSTWO CONSECUTIVE MONTHS WITH DOMESTIC OIL WITH DOMESTIC OIL PRODUCTION ABOVE 2 MILLION BPDPRODUCTION ABOVE 2 MILLION BPD

-3%

+4%

Tho

usan

d bp

d

Tho

usan

d bp

d

3Q08 3Q09

• Increase in total production due to higher domestic production and the start-up of Akpo field, in Nigeria

• 5% increase in domestic oil production due to incre ased output from P-52 and P-54, coupled with the start-up of P-51, P-53, FPSO Cidade de Niterói an d FPSO Cidade de São Vicente

• Natural gas production restricted by the decrease i n demand, specially from thermo-electric plants

4

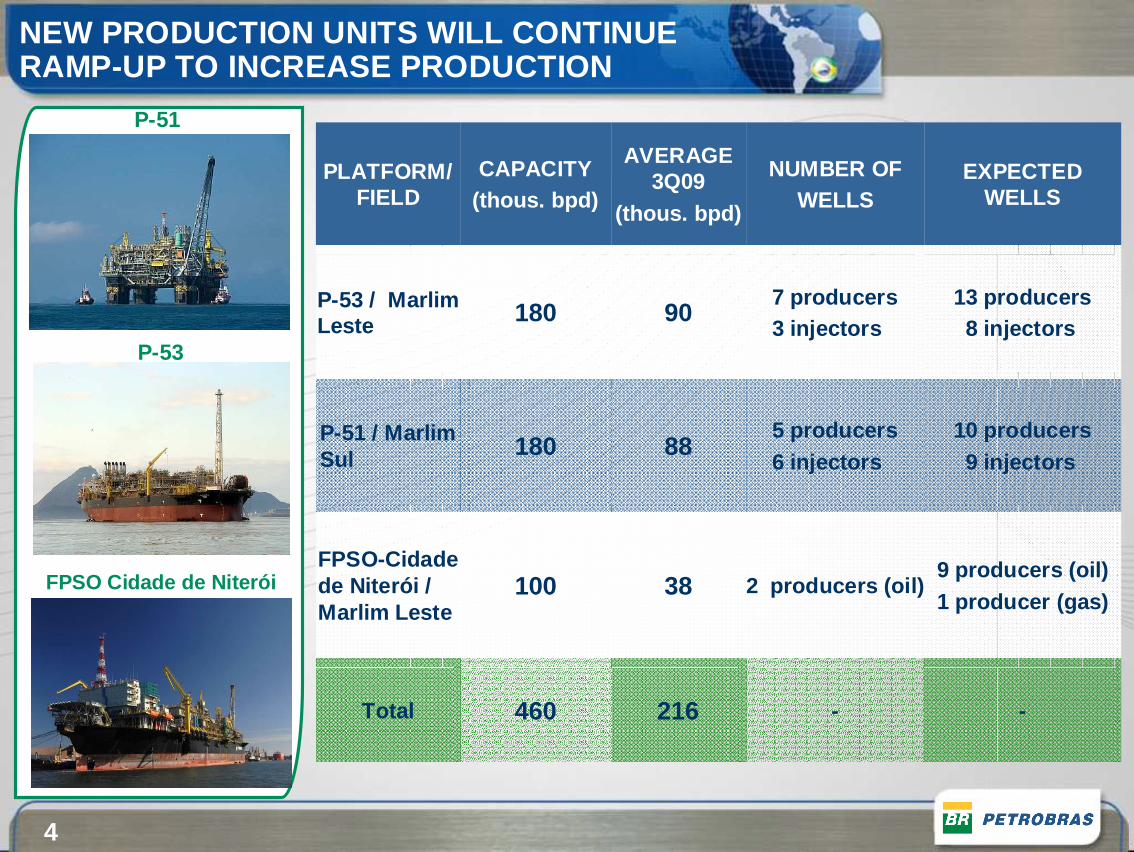

P-51

P-51

PLATFORM/ FIELD

CAPACITY(thous. bpd)

AVERAGE 3Q09

(thous. bpd)

NUMBER OFWELLS

EXPECTED WELLS

P-53 / MarlimLeste 180 90

7 producers3 injectors

13 producers 8 injectors

P-51 / MarlimSul 180 88

5 producers6 injectors

10 producers9 injectors

FPSO-Cidadede Niterói / Marlim Leste

100 38 2 producers (oil)9 producers (oil) 1 producer (gas)

Total 460 216 - -

FPSO Cidade de Niterói

P-53

FPSO Cidade de Niterói

NEW PRODUCTION UNITS WILL CONTINUE RAMP-UP TO INCREASE PRODUCTION

5

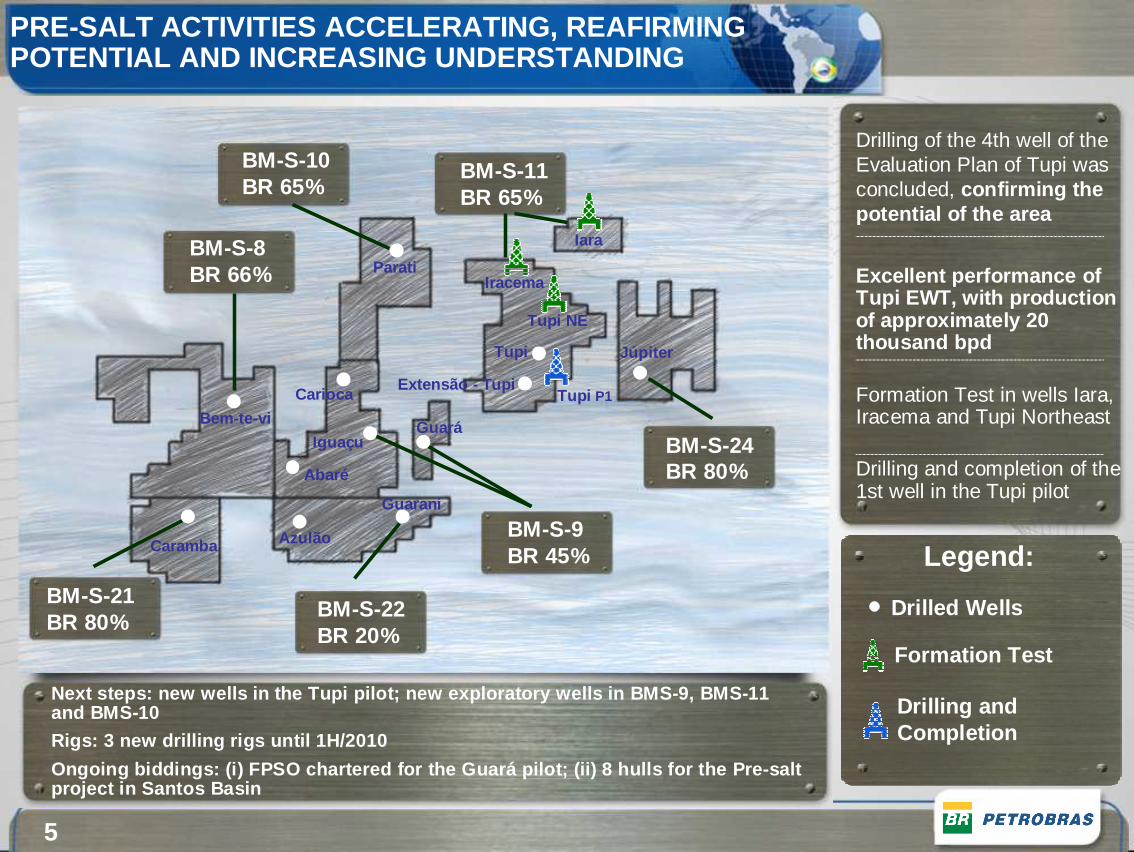

Drilling of the 4th well of the Evaluation Plan of Tupi was concluded, confirming the potential of the area

Excellent performance of Tupi EWT, with production of approximately 20 thousand bpd

Formation Test in wells Iara, Iracema and Tupi Northeast

Drilling and completion of the 1st well in the Tupi pilot

BM-S-10BR 65%

BM-S-11BR 65%

BM-S-24BR 80%

BM-S-9BR 45%

BM-S-22BR 20%

BM-S-21BR 80%

BM-S-8BR 66%

Legend:

Drilled Wells

Formation Test

Drilling and Completion

Parati

Iara

Iracema

Tupi NE

Tupi

Tupi P1Extensão - Tupi

Júpiter

Guará

Carioca

Iguaçu

Abaré

Azulão

Guarani

Caramba

Bem-te-vi

PRE-SALT ACTIVITIES ACCELERATING, REAFIRMING POTENTIAL AND INCREASING UNDERSTANDING

Next steps: new wells in the Tupi pilot; new explora tory wells in BMS-9, BMS-11 and BMS-10

Rigs: 3 new drilling rigs until 1H/2010

Ongoing biddings: (i) FPSO chartered for the Guará p ilot; (ii) 8 hulls for the Pre-salt project in Santos Basin

6

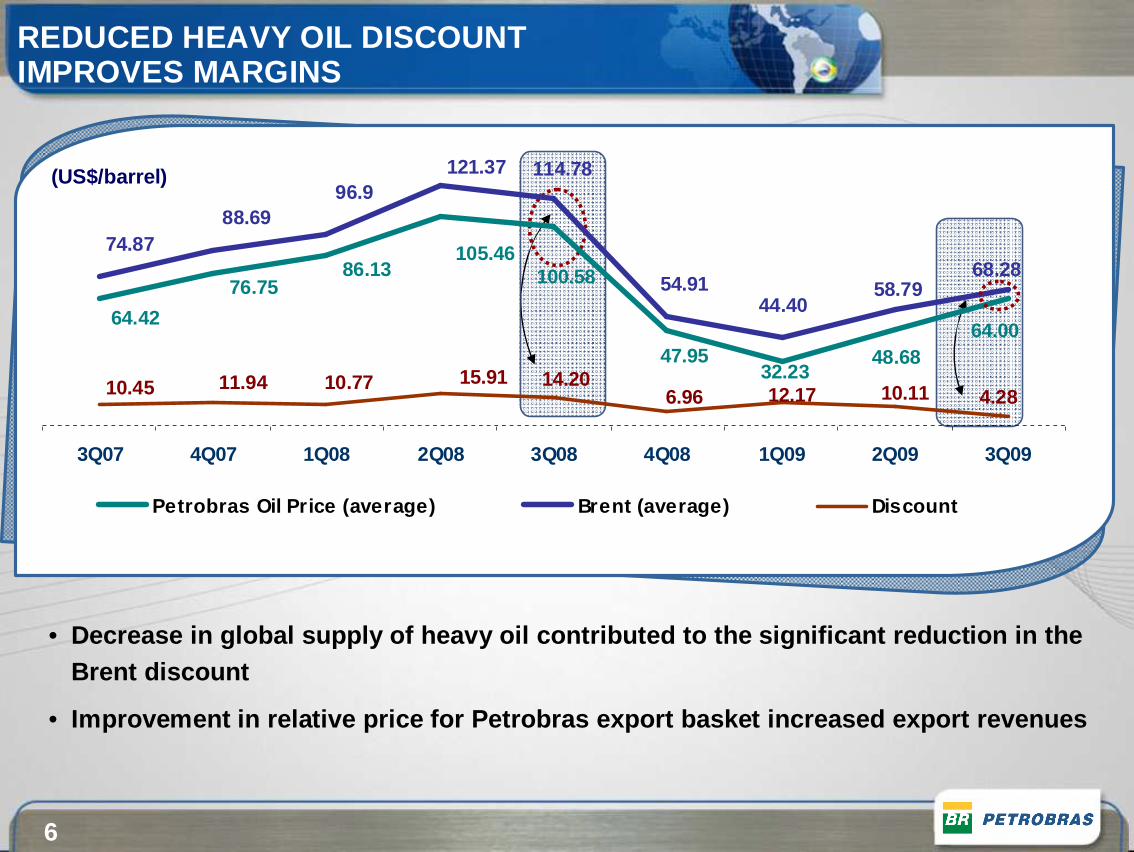

(US$/barrel)

REDUCED HEAVY OIL DISCOUNT IMPROVES MARGINS

32.23

64.42

76.7586.13

105.46100.58

47.95 48.6864.00

44.40

74.8788.69

96.9121.37 114.78

54.91 58.7968.28

4.2810.1112.176.9614.2015.9110.7711.9410.45

3Q07 4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09

Petrobras Oil Price (average) Brent (average) Discount

• Decrease in global supply of heavy oil contributed to the significant reduction in the Brent discount

• Improvement in relative price for Petrobras export basket increased export revenues

7

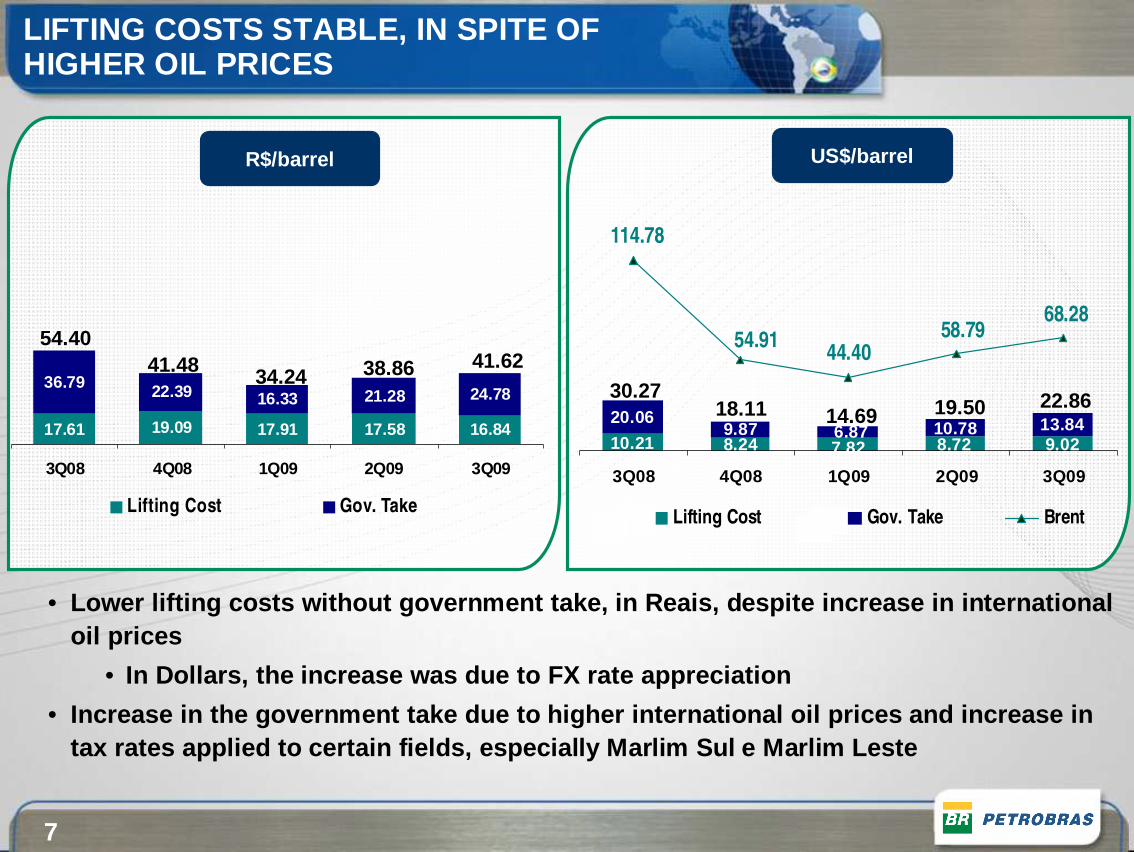

LIFTING COSTS STABLE, IN SPITE OF HIGHER OIL PRICES

17.61 19.09 17.91 17.58 16.84

36.79 22.39 16.33 21.28 24.78

3Q08 4Q08 1Q09 2Q09 3Q09

Lifting Cost Gov. Take

54.4041.48 34.24 38.86 41.62

R$/barrel

• Lower lifting costs without government take, in Rea is, despite increase in international oil prices

• In Dollars, the increase was due to FX rate appreci ation

• Increase in the government take due to higher inter national oil prices and increase in tax rates applied to certain fields, especially Mar lim Sul e Marlim Leste

US$/barrel

10.21 8.24 9.02

20.069.87 13.84

7.82 8.726.87 10.78

58.7968.28

44.4054.91

114.78

3Q08 4Q08 1Q09 2Q09 3Q09

Lifting Cost Gov. Take Brent

30.2718.11 14.69 19.50 22.86

8

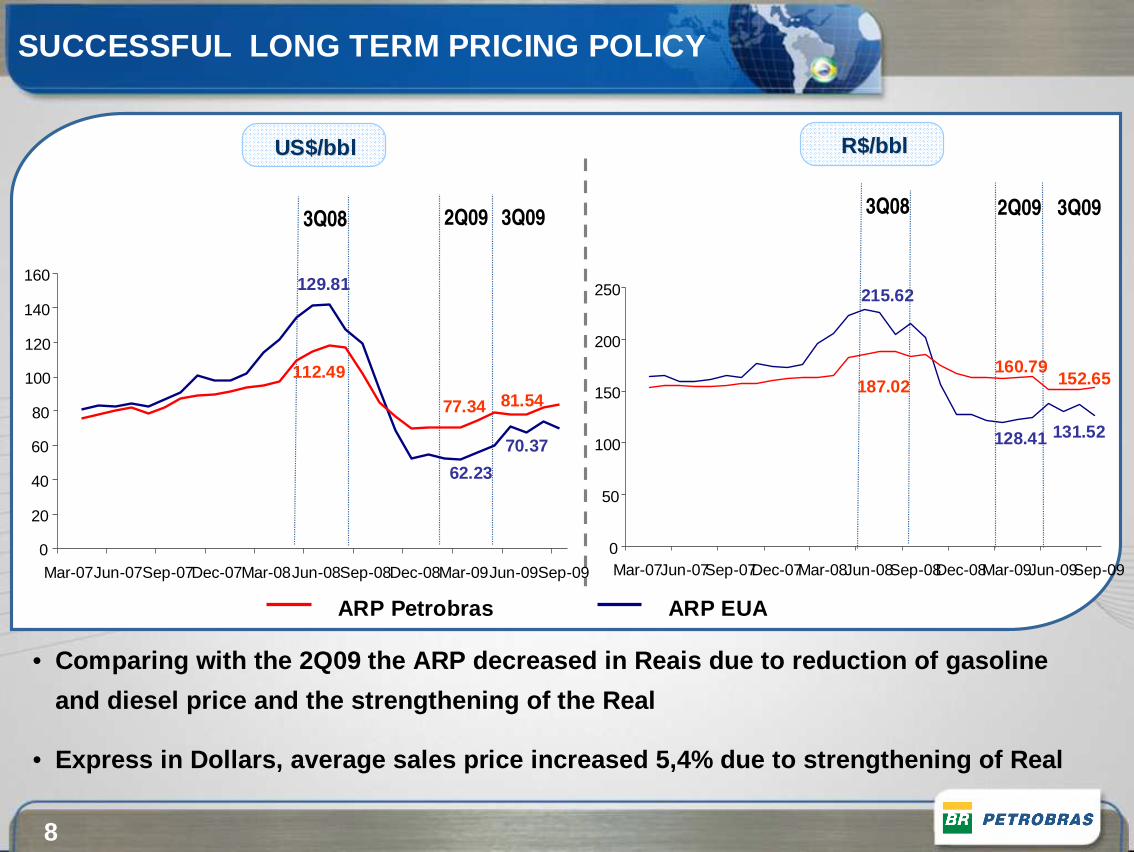

US$/US$/bblbbl R$/R$/bblbbl

ARP Petrobras ARP EUA

• Comparing with the 2Q09 the ARP decreased in Reais d ue to reduction of gasoline

and diesel price and the strengthening of the Real

• Express in Dollars, average sales price increased 5 ,4% due to strengthening of Real

SUCCESSFUL LONG TERM PRICING POLICY

US$/bbl2Q09 3Q093Q08

70.37

81.54

62.23

77.34

129.81

112.49

0

20

40

60

80

100

120

140

160

Mar-07Jun-07Sep-07Dec-07Mar-08Jun-08Sep-08Dec-08Mar-09Jun-09Sep-09

R$/bbl

128.41

160.79152.65

131.52

215.62

187.02

2Q09 3Q093Q08

0

50

100

150

200

250

Mar-07Jun-07Sep-07Dec-07Mar-08Jun-08Sep-08Dec-08Mar-09Jun-09Sep-09

9

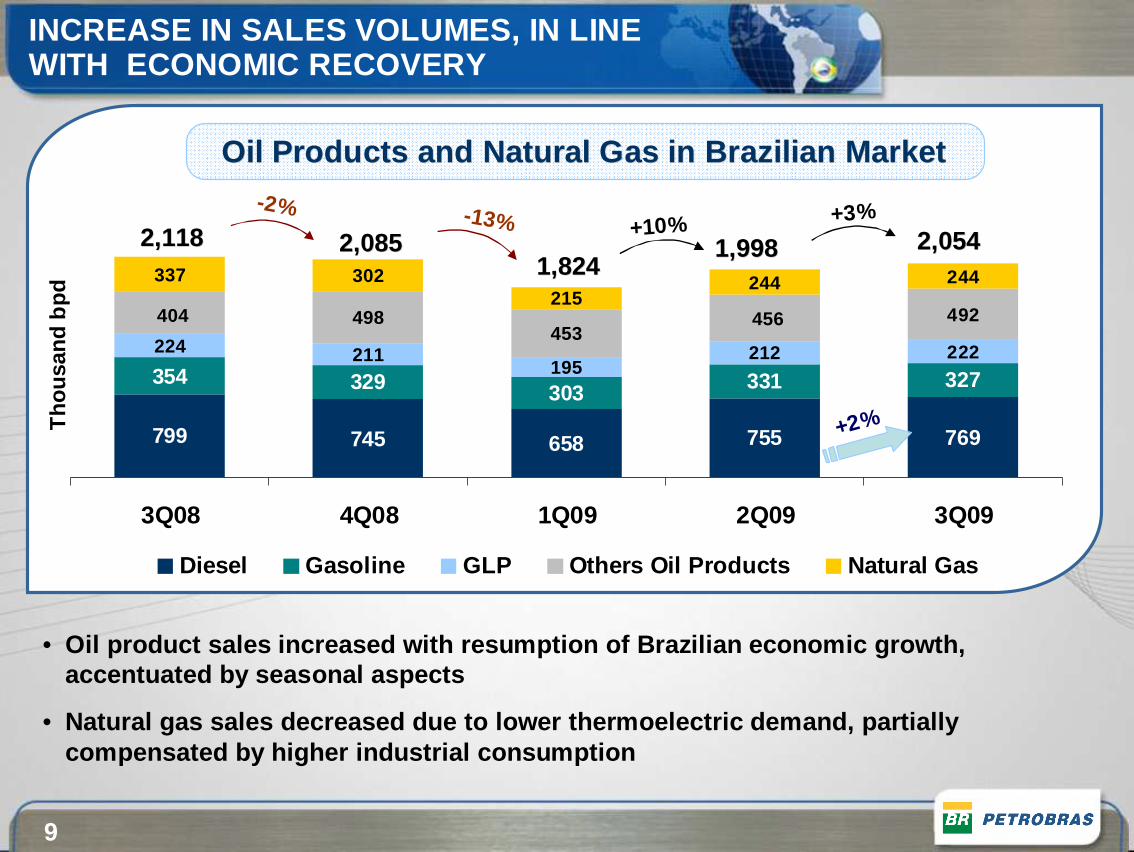

799 745 658 755 769

354 329 303 331 327

224 211195

212 222

337 302215

244 244

492498453

404 456

3Q08 4Q08 1Q09 2Q09 3Q09

Diesel Gasoline GLP Others Oil Products Natural Gas

1,9981,9981,8241,824

2,0542,054

Oil Products and Natural Gas in Brazilian MarketOil Products and Natural Gas in Brazilian Market

Tho

usan

d bp

d

+3%

INCREASE IN SALES VOLUMES, IN LINE WITH ECONOMIC RECOVERY

2,0852,0852,1182,118 +10%

+2%

-2% -13%

• Oil product sales increased with resumption of Braz ilian economic growth, accentuated by seasonal aspects

• Natural gas sales decreased due to lower thermoelec tric demand, partially compensated by higher industrial consumption

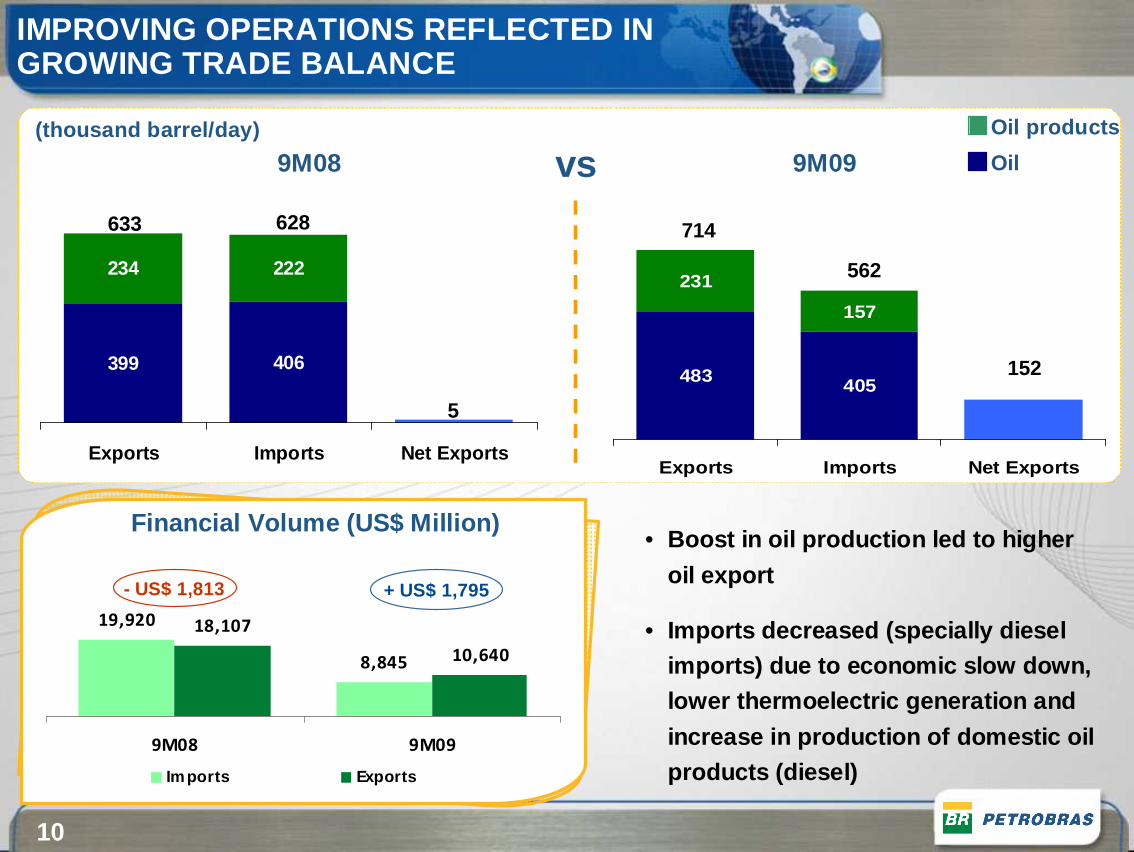

10

9M09

483 405

231

157

Exports Imports Net Exports

9M08

399 406

234 222

Exports Imports Net Exports

628633

5

152

562

714

vs

19,920

8,845

18,107

10,640

9M08 9M09

Imports Exports

+ US$ 1,795- US$ 1,813

IMPROVING OPERATIONS REFLECTED IN GROWING TRADE BALANCE

Oil

Oil products(thousand barrel/day)

Financial Volume (US$ Million)• Boost in oil production led to higher

oil export

• Imports decreased (specially diesel imports) due to economic slow down, lower thermoelectric generation and

increase in production of domestic oil products (diesel)

11

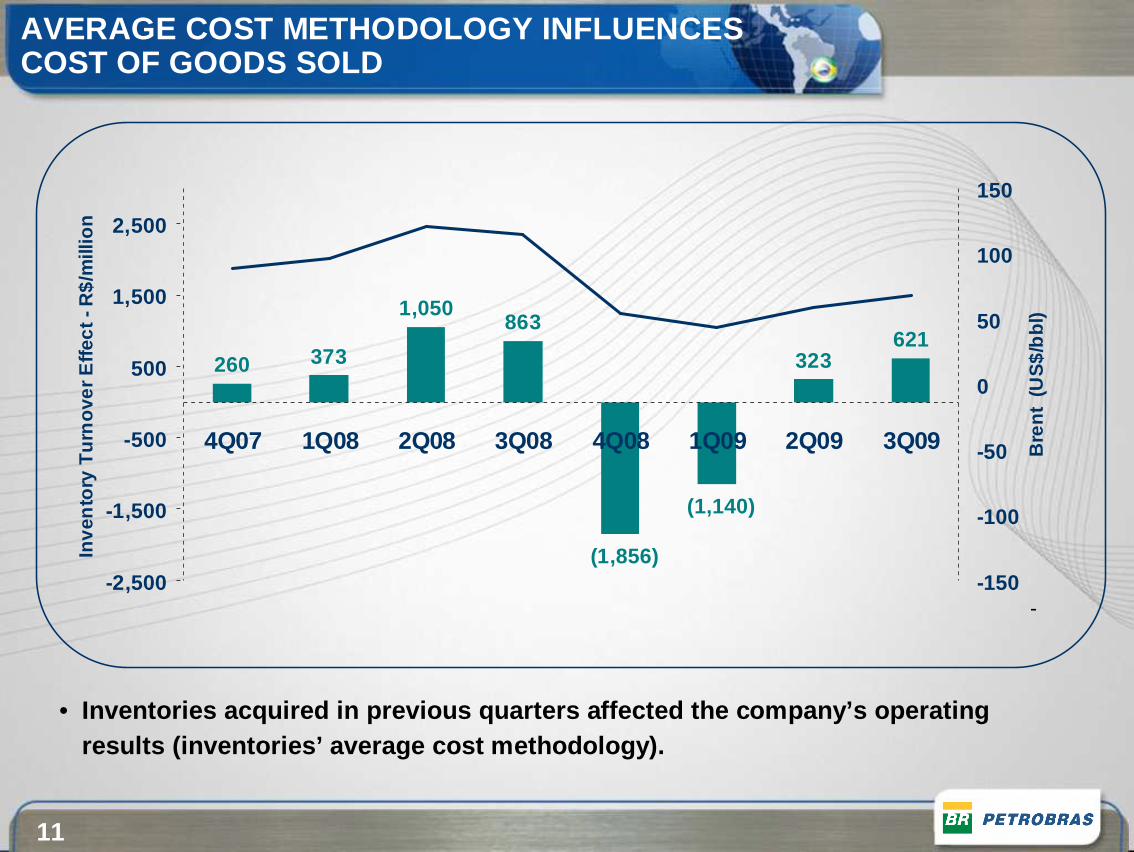

AVERAGE COST METHODOLOGY INFLUENCES COST OF GOODS SOLD

• Inventories acquired in previous quarters affected the company’s operating results (inventories’ average cost methodology).

-

260 373

1,050863

(1,856)

(1,140)

323621

-2,500

-1,500

-500

500

1,500

2,500

4Q07 1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09

Inve

nto

ry T

urn

over

Effe

ct -

R$/

mill

ion

-150

-100

-50

0

50

100

150

Bre

nt (

US

$/b

bl)

12

NET REVENUE NET REVENUE (IN MILLION R$ - 2Q09 VS 3Q09)

2Q09Operating Income

Net Operating Revenue

COGSOperating Expenses

3Q09Operating Income

13,896

3,272 (4,401)

(2,520)

10,247

12,295P.E. MARLIM = 2,048

OPERATING INCOME IMPACTED BY SPECIAL PARTICIPATION PROVISIONING

• Higher oil prices, lower spread between light and h eavy oil and increase in oil products sale generated higher net operating revenu e

• Higher sales volumes and higher import prices led t o increase in COGS

• Decline in operating income is explained by a provi sioning for special participation tax related to Marlim field (R$ 2.05 b illion)

13

NET INCOME NET INCOME (R$ MILLION – 2Q09 VS 3Q09)

7,734 (3,649) 3,168 7,303(836)(63) 949

1,677 Net Monetary Variation

• Better financial result due to lower FX rate apprec iation and net monetary variation from the BNDES loan (R$ 1.7 Billion)

• Counterpart of hedge gains was higher COGS• Taxes Increased due to the higher fiscal benefit fr om interest on equity along with

higher recovery of fiscal credits in exploratory ac tivities abroad in 2Q09

• Reduction in minority interest due to lower FX gain s on SPCs debts

533 Hedge

NET INCOME FLAT, AFTER ADJUSTING FOR FX VARIATIONS

Financial Result

TaxesEquityIncome

OperatingIncome

MinorityInterest

2Q09Net Income

3Q09Net Income

14

2,806(425)

(820)418 (2,419)

7,8068,246

• Reduced spread between light and heavy oil contribu ted to the increase in revenues

• Increase in inventories caused slight reduction in sales volumes

• Increase in COGS due to higher production taxes due to higher oil prices

• Increase in operating expenses due to the extraordi nary provision for Marlim field Government take

EXPLORATION AND PRODUCTION –SOLID OPERATING PERFORMANCE

EXPLORATION & PRODUCTION EXPLORATION & PRODUCTION –– OPERATING INCOMEOPERATING INCOME(R$ MILLION – 2Q09 VS 3Q09)

2Q09 Oper. Income

Price Effect on Revenues

Volume Effecton Revenues

OperationalExpenses

3Q09 Oper. Income

Volume Effecton COGS

Cost Effecton average

COGS

15

DOWNSTREAM DOWNSTREAM –– OPERATING INCOMEOPERATING INCOME(R$ MILLION – 2Q09 VS 3Q09)

(636)

(5,278)2,911

(2,316)

205 2,800

7,914

• Despite reduction in ARP in Reais (2Q09: R$ 160.79; 3Q09: R$ 152.75), increase in the volumes sold, led by economic growth, increa sed revenues

• Higher oil and oil products import costs and reduce d heavy/ light oils spread led to increase in COGS

DOWNSTREAM – INCOME NORMALIZING WITH INCREASES IN INTERNATIONAL PRICES

2Q09 Oper. Income

Price Effect on Revenues

Volume Effecton Revenues

Cost Effecton average

COGS

OperationalExpenses

3Q09 Oper. Income

Volume Effecton COGS

16

INCREASING CONTRIBUTIONS FROM GAS & ENERGY, INTERNATIONAL AND DISTRIBUTION (2Q09 VS 3Q09)

Gas & EnergyGas & Energy

InternationalInternational

Operating Result:2Q09

R$ 576 millionVS.

Operating Result : 2Q09R$ 224 million

VS.

Operating result:2Q09

R$ 466 millionVS.

• 7% increase in sales margins and 9% in volumes supported continued strength for our distribution segment

3Q09R$ 651 million

3Q09R$ 363 million

3Q09R$ 620 million

DistributionDistribution

• Higher volumes sold in non-thermo electric markets

• Decrease in natural gas imports/transfer costs, fol lowing the levels of international reference prices

• Reduction in the energy generation income partially offset by better results from power sales

• Higher realization prices and increase in productio n contributed to higher operating income

• Akpo start-up in Nigeria was main contributor to the trend of increasing production

17

vs

1,5

2,8d

0,10,4

0,4

7,1

1,0

1,1

21%

2%3%

1%

9%

11%

7%

46%

23.2

10.6

4.5

5.5

0.41.5

3.8 1.2

19%

3%

2%

1%

6%

12%

11%

46%

3.7

4.1 15.8

0,5

6.4

2.2

0.30.7

Capex 9M09 - R$ 50.7 billions Capex 9M08 - R$ 34.1 billions

E&P International

0.9

Capex in line with the Company´s opportunities

CONTINUED GROWTH IN CAPEX, CONSISTENT WITH BUSINESS PLAN

G&E Distribution CorporateDoestream SPE Projects under Negociation

18

SUCCESSFUL EFFORTS TO RAISE CAPITAL FROM LONG TERM SOURCES

1.25

0

1.5

2.5

1.5

Brigde Loan Bond issue

Oct-30 (Maturity 2040)Yield: 7.00%

Oct-30 (Maturity 2020) Yield: 5.875%

Jul-09 (Maturity 2019)Yield: 6.875%

Feb-11 (Maturity 2019)Yield: 8.125%

6.5 6.756.75

(US

$ bi

lion)

MarketMarket Capital Bond Capital Bond issuanceissuance

10

13.3

2

2.75

China DevelopmentBank

BNDES

U S Eximbank

Others

(*)

(*) R$ 25 billions converted by FX tax in 07.30.09

OthersOthers LoansLoans++US$ 28.05 US$ 28.05 billionsbillions

In 2009, In 2009, US$ 34.8 US$ 34.8 billionbillion werewere raisedraisedwithwith anan averageaverage lifelife ofof 10.6 10.6 yearsyears

19

LIQUIDITY STRENGTHENED, LEVERAGE WITHIN TARGETS

28%26%

19%

21%18% 19%

21%

28%26%

12%

19%22%21%

25%

21%

18%

23%27%

30/09/2007 31/03/2008 30/09/2008 31/03/2009 30/09/2009

Net Debt/Net Capt.

Short Term Debt/Total Debt

R$ million 09/30/2009 06/30/2009

Short Term Debt 10,639 13,086Long Term Debt 79,588 55,782

Total Debt 90,227 68,868

Cash and Cash Equivalents

30,088 10,072

Short Term Debt 60,139 58,796

Capital Structure 49% 49%

US$ million 09/30/2009 06/30/2009

Total Debt 50,743 35,288

• Increase in liquidity due to the increase in cash a nd decrease in short term debt.

• Net Debt/Net Capitalization stable and within the t arget range (25%-35%)

20

STABLE CASH FLOWS SUPPORT INVESTMENT PLAN

6.386.384.21Average Life of Debt (years)*

1.11**1,000.85Net Debt/ EBITDA

30,08830,08810,776Cash at the end of period

36,987

(9,835)

(12,442)

(50,622)

38,180

15,889

Jan-Sep 2009

25,4413,581Financing

(3,426)(6,187)Dividends

(1,765)(198)Free Cash Flow

(18,446)(34,534)Investment

16,68134,337Operating Cash Flow

10,07213,071Cash at the beginning of period

3Q09Jan-Sep2008

2.08

118.87

1.871.69Average Exchange Rate (R$/US$)

127.68187.62Average Brent (R$/bbl)

R$ million

* End of period** last 12 months

� Higher operating cash flow, despite lower oil price s

� Increasing CAPEX supported by higher borrowings dur ing the year

� New loans improved average life of debt stock

21

For more information:Investor Relations

www.petrobras.com.br/ri+55 21 3224-1510