Search ExperienceSujata HalarnkarFall 2008LIBR-282-05

For the mid-term project, I reviewed the sports nutrition industry in the United States to identify current trends, major manufacturers, and distributors. For the final project, I decided to explore India’s market and its potential for distributing US sports nutrition products. In this report, I have included some background information on India, reviewed current consumer trends, and identified key information necessary to explore distribution of health products possibilities. I have also included a number of Indian manufacturers of health products.

Search Strategy

From the experience of the mid-term project, I decided to begin my search with Yahoo! Finance and Google.com. Mainly, I looked for statistics and news article on the topic. A narrow topic made it difficult to find resources. India is an emerging market in sports nutrition industry and not much literature is available on the topic. Many new health product companies are being founded and slowly information about them is coming up on the Internet. I also explored Factiva.com. However, as previously experienced I found more or less the similar results. Obviously, it is easier and quicker to search and narrow down resources in the paid databases.

I started my search with basic search terms and developed search terms from them. I noted down new and interesting search terms from news articles and reports. I found the Indian market complex and difficult to analyze. Cultural and social factors influence the Indian consumer market in many ways. Local survey or interview of consumers would have provided a better insight on the market.

Surprisingly, I found sufficient information on the Indian manufacturers and distributors of health related products. Initially, I wanted to focus on whey protein market. However, whey protein products are slowly gaining popularity in India and I could not find sufficient information on the topic.

Finally, I tried to use the latest articles for this research to find current market and consumer trends. Textbooks especially Carr’s Super Searchers were useful reference tools in this search.

Listed below are my search results along with keywords I used for this search.

Keywords used

whey protein market in Indiawhey protein consumer market in Indiamarket trend whey protein Indiawhey protein and Indiasports nutrition and indiasports nutrition and indiaindian sports nutrition industry and consumer trends

india and demographicindia and whey protein and market trendsconsumer market and india and health nutrition trends

Challenges:

Difficulty in narrowing down resourcesSports Nutrition industry is huge and too many categories of products to coverMany good new sources but difficult to find free market reportsDifficulty in finding free research or news articles on the topic

Yahoo!

Search term: whey protein market in india

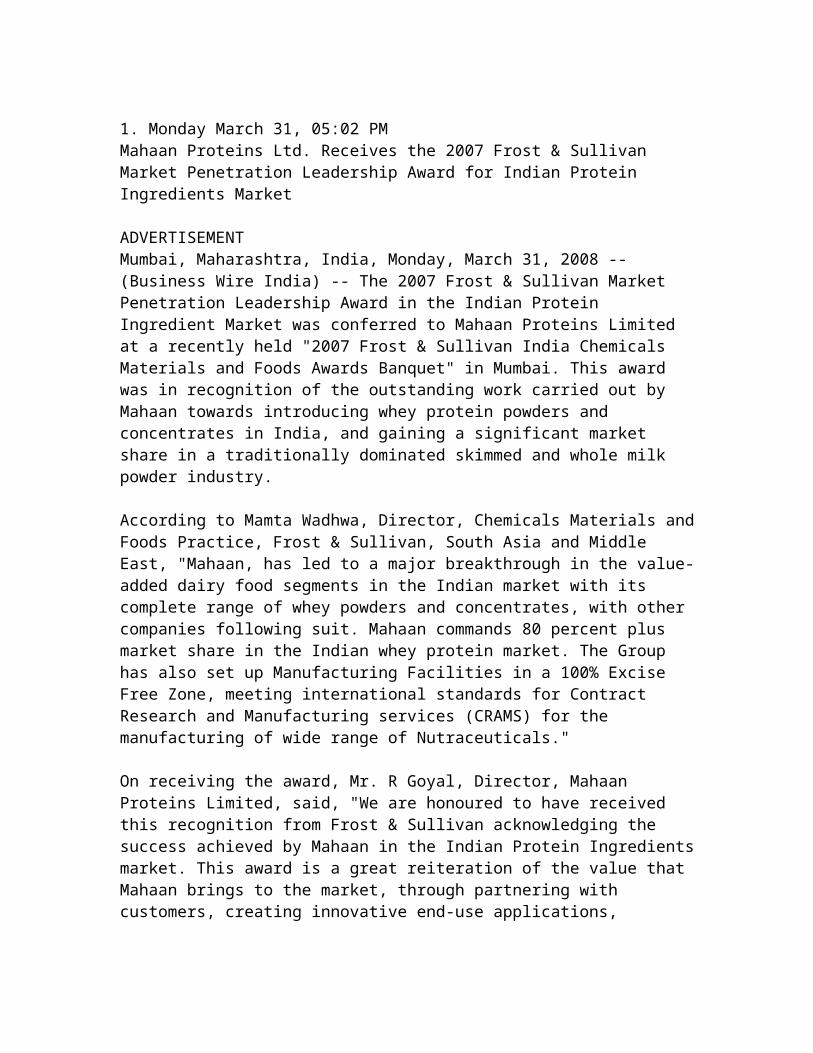

1. Monday March 31, 05:02 PMMahaan Proteins Ltd. Receives the 2007 Frost & Sullivan Market Penetration Leadership Award for Indian Protein Ingredients Market

ADVERTISEMENTMumbai, Maharashtra, India, Monday, March 31, 2008 -- (Business Wire India) -- The 2007 Frost & Sullivan Market Penetration Leadership Award in the Indian Protein Ingredient Market was conferred to Mahaan Proteins Limited at a recently held "2007 Frost & Sullivan India Chemicals Materials and Foods Awards Banquet" in Mumbai. This award was in recognition of the outstanding work carried out by Mahaan towards introducing whey protein powders and concentrates in India, and gaining a significant market share in a traditionally dominated skimmed and whole milk powder industry.

According to Mamta Wadhwa, Director, Chemicals Materials and Foods Practice, Frost & Sullivan, South Asia and Middle East, "Mahaan, has led to a major breakthrough in the value-added dairy food segments in the Indian market with its complete range of whey powders and concentrates, with other companies following suit. Mahaan commands 80 percent plus market share in the Indian whey protein market. The Group has also set up Manufacturing Facilities in a 100% Excise Free Zone, meeting international standards for Contract Research and Manufacturing services (CRAMS) for the manufacturing of wide range of Nutraceuticals."

On receiving the award, Mr. R Goyal, Director, Mahaan Proteins Limited, said, "We are honoured to have received this recognition from Frost & Sullivan acknowledging the success achieved by Mahaan in the Indian Protein Ingredients market. This award is a great reiteration of the value that Mahaan brings to the market, through partnering with customers, creating innovative end-use applications, technological developments, new product applications and research studies."

The recipient of this award is evaluated on specific pre-defined criteria which include market share gain, increase in sales, and brand awareness efforts within the industry. This is accomplished through interviews with market participants, end-user studies, and extensive secondary research.

In addition to the above methodology, there are specific criteria used to determine final competitor rankings within the industry. These include competitive pricing strategies, strong sales force strategy, ability to establish brand awareness through promotional activities and advertising, strategic alliances that expand customer base and finally product innovation which also includes developing new technologies.

The protein ingredients market globally has seen accelerated growth owing to its functionalities like emulsifying, water binding, viscosity enhancing, foaming properties apart from its usual nutritional profile. The Indian Protein Ingredients Market is broadly classified into -Soya protein, Whey protein and Wheat Gluten. Frost & Sullivan's comprehensive analysis indicates that the total market for Indian protein ingredients was valued at INR 279.2 million representing market volumes of 1650 MT in the year 2006. The soya protein market contributes 72.0 percent of the total revenues generated, the whey protein market contributes 23.0 percent and the wheat gluten market contributes only 5.0 percent of the total revenues. The estimated growth rate was 5.6 percent per annum in the year 2006.

The soya and whey proteins would witness good growth in nutritional and functional applications across various end use segments including pharma formulations, tube feeding formulas, infant formulas, functional beverages and fortified foodstuffs.

About Frost and Sullivan:

Frost & Sullivan, the Growth Consulting Company, partners with clients to accelerate their growth. The company's Growth Partnership Services, Growth Consulting and Career Best Practices empower clients to create a growth focused culture that generates, evaluates and implements effective growth strategies. Frost & Sullivan employs over 45 years of experience in partnering with Global 1000 companies, emerging businesses and the investment community from more than 30 offices on six continents. For more information about Frost & Sullivan's Growth Partnerships, visit http://www.frost.com.

About Mahaan

Mahaan Proteins Ltd. is the only composite dairy ingredient plant in India that manufactures edible casein, pharmaceutical and edible grade lactose, whey protein concentrate 70% and pure ghee.

Mahaan Proteins Ltd. has been set up with foreign technical collaboration and has specialized in manufacturing dairy ingredients and is currently developing caseinates and functional WPCs.It has also added a brand new facility for spray drying specialized instantly soluble powders for its buyers engaged in the nutraceuctical industry.

http://www.mahaanfoods.com/mahaangroup.html

Media contact detailsCONTACT:

Frost & SullivanCorporate Communications - South AsiaRemi Chatterjee+91 22 4001 3419fax: +91 22 2832 [email protected] Communications - South Asia & Middle EastNimisha Iyer+91 22 4001 3404fax: +91 22 2832 [email protected]

CONTACT:

Frost & SullivanCorporate Communications - South AsiaRemi Chatterjee+91 22 4001 3419fax: +91 22 2832 [email protected] Communications - South Asia & Middle EastNimisha Iyer+91 22 4001 3404fax: +91 22 2832 [email protected]

2.

Dixon HEALTHCARE PVT. LTD. offers a wide range of health products full of nutritional and vital compositions for healthy and productive life....

About UsA healthy and well balanced diet is the essence of living in an age where people are moving ahead at a jet speed. It has become very much imperative to include vital nutrients in daily diet in order to remain healthy and energetic. As a leading brand in the concerned market, Dixon HEALTHCARE PVT. LTD. has taken the initiatives to provide you with all these vital ingredients which are a part of healthy living. We are an acclaimed manufacturer and exporter of a variety of Health Drinks, Protein Supplements,

Energy Drinks, Food Supplements for Diabetics, Whey Protein Concentrates, Multi-Vitamin Powder, etc. All these products contain high level of protein, vitamins and various amino acids. The food supplements are prepared in a way that they are suitable even for the people suffering from Diabetes.

Since we are in a field where health is the main area of concern, we cross check to be sure that all our products are the best and safe in terms of quality. The rates of these products are within the budgets of middle class people. We ascertain that the related orders are always delivered on time, thereby leading to complete customer satisfaction. Being committed to keep our customers in the pink of health, Dixon HEALTHCARE PVT. LTD. gives keen attention to their feedback and suggestions, trying to incorporate the same and improve the quality of our products. The popularity of our products has given us a brand goodwill in the market with the result that we export them all across the globe.

Our VisionWith a vision to be the market leader in our arena, we, at Dixon HEALTHCARE PVT. LTD., work diligently to increase our productivity and efficiency. We are now planning to import quality raw materials from so as overseas markets to reduce the cost of our products and broaden our international prospects. Our company is solely aimed at delivering new and quality products to our customers to strengthen our image in the domestic as well as global market.

Product RangeSince its establishment in 2000, Dixon HEALTHCARE PVT. LTD. has taken the initiative to produce a wide range of products for the benefit of its customers. We are a reputed manufacturer and exporter of the following products:

* Health Drinks * Protein Supplements * Energy Drinks * Food Supplements for Diabetics * Whey Protein Concentrates * Multi-Vitamin Powder * Protein Supplement Syrup * Nutritional Supplement Capsules * Fiberplus Powder * Pro-Nut Granules.

Quality AssuranceQuality at Dixon HEALTHCARE PVT. LTD. is of paramount importance. All our products go through stringent quality checking mechanism. We have a team of quality supervisors who sincerely check the quality and ensure that only safe and flawless quality health drinks, food supplements and other related products are manufactured. Our testing laboratories are equipped with the latest testing machines where each product is tested for quality and efficiency. The whole procedure is in complete accordance with the

international standards, and this is the reason why our valued clients have always opted for our products time and again.

InfrastructureThe state of the art infrastructure is another USP of Dixon HEALTHCARE PVT. LTD. which provides us an additional edge over other competitors in the market. We have installed the latest machines at our unit to run our production process which is handled by a well managed workforce exhibiting utmost efficiency and sincerity. The employed professionals include scientists, pharmacists, and people from the field of bio-technology; who are experts in the field of protein chemistry and ensure that correct amount of ingredients are mixed in the preparation of the products. All the machines are operated in a clean and hygienic environment in order to prevent any kind of contamination in the products.

The products are packed efficiently along with the manufacturing and expiry dates being clearly mentioned on the labels so as to avoid any confusion. Our Research and Development department is lashed with all the modern equipments needed to test any new product. It has developed various kinds of research programmes to make improvisation in the service standards.

Energy Drink Nutritional Supplement Capsules Protein Supplement Syrup Whey Protein Concentrate Viprex Syrup Health Drink Multi-Vitamin Powder Pro-Nut Granules Fiberplus Powder Food Supplement for DiabeticsContact Details

DIXON HEALTHCARE PVT. LTD.Plot No.- 89, Dhovali Village, Taluka-Vasai,Thane - 401207, Maharashtra, IndiaPhone:91-250-6452995

Send Mail Key PersonnelMs. Ranjana Kolge (Director)Mobile:+919820303499Translate In : View in English View in Spanish View in French View in German View in Italian View in Chinese (Simplified) View in Japanese View in Korean View in Arabic View in Portuguese

3. Sterling Rasayan Ltd.

The activities of the company have expanded significantly over the last five years to a point where over 250 items are regularly traded on an ex-stock basis. Most of the business activities of Sterling Rasayan now consist of locally sourced products to be distributed to the ever growing customer base. Products were initially sourced from India,

however, expansion of product range over the past few years has increased in number of products coming from overseas markets specially from Europe,East Europe, U.S.A, Australia & China. Today Sterling Rasayan are India's leading Indenting / Sourcing Agents for Imports & Exports.

We have a back-up of more than 50 Large Reputed Manufacturers in India & can offer you these products at most competitive rates.

Home |Services| Imports | Exports | Objectives | Contact UsSterling Rasayan (P) LtdSterling House, 27 Old Rajinder Nagar MarketNew Delhi - 110060, INDIA

Ph : +911125734286 Fax : +91112574428Mobile : +919811038104, [email protected]

Yahoo!

Search term: whey protein consumer market in india

Similar results as “whey protein market in india”

Yahoo!

Search term: market trend whey protein india

1. http://www.usdec.org/files/PressReleases/2007%20%23s%20release%20(for %20dairy%20processor%20media)%200208%20-%20FINAL.pdf

Factiva.comSearch term: sports nutrition and india1. http://global.factiva.com/9lqW0VRwuX1Vy8wElyjuGlQnuO5rd42YIqe8DUknG7ucAXG553GSEh6I2PX_2Fm4YWIs2gzZn4hyDWjQ92m6Ae2eiMJcK4JfX0NNlkCNI4ePI_2BgSdvAiEdvKWVZ5_2BL3QjoQScTnQRyctb8ATvA7z6CIB6RnhafCZJmPffT94rGCBWmUL35mDyrl97sI5n1_2FxRB_7C2.mp3Listen to Article

Nutritionals in India242 words1 August 2008MarketResearch.com

EnglishCopyright 2008 MarketResearch.com, All Rights Reserved.

Published By: Euromonitor International

Euromonitor International's Nutritionals in India market report offers a comprehensive guide to the size and shape of the health and wellness nutritional market at a national level. It provides the latest retail sales data (2002-2007), allowing you to identify the sectors driving growth. It identifies the leading companies, the leading brands and offers strategic analysis of key factors influencing the market - be they new product developments, packaging innovations, economic/lifestyle influences, distribution or pricing issues. Forecasts to 2012 illustrate how the market is set to change.Product coverage: Herbal/traditional products; Slimming products; Sports nutrition; Vitamins and dietary supplements

Data coverage: market sizes (historic and forecasts), company shares, brand shares and distribution data.

Why buy this report?

Get a detailed picture of the health and wellness nutritional industry;

Pinpoint growth sectors and identify factors driving change;

Understand the competitive environment, the market's major players and leading brands;

Use five-year forecasts to assess how the market is predicted to develop.

Euromonitor International has over 30 years experience of publishing market research reports, business reference books and online information systems. With offices in London, Chicago, Singapore, Shanghai, Vilnius, Dubai and Cape Town and a network of over 600 analysts worldwide, Euromonitor International has a unique capability to develop reliable information resources to help drive informed strategic planning

To Purchase Report:

http://www.marketresearch.com/feed/factiva/display.asp?productid=2016684

Vendor: Euromonitor International

Document MRKRE00020081124e481000uc

More Like This

Search term: whey protein and India

1. PLETHICO LAUNCHES A LOW FAT WHEY PROTEIN SUPPLEMENT (the product has 65 percent proteins without saturated fat and is free from cholesterol)Modern Food Processing. Oct 31, 2008; pg 10129 words31 October 2008Indian Business InsightEnglishCopyright (c) 2008 Informatics (India) Ltd.

Plethico Pharmaceuticals Ltd has launched Coach's Formula (CF), a low fat whey protein supplement in India. The product has 65 percent proteins without saturated fat and is free from cholesterol. CF is recommended for people who undertake a fitness regimen and for athletes. It has been developed with inputs from international fitness instructors, nutritionists and experts from the field of sports. The protein formula contains all essential vitamins and minerals and helps in regeneration and recuperation of damaged muscle tissue. The low fat supplement increases the physical stamina, leading to better performance of sports persons.

851670|ABSTRACT|BIMONTHLY

Document WIBI000020081126e4av00077

2. Get a Deep Insight into the World Sports and Fitness Nutrition Market6682 words1 October 200807:19Marketwire (English)EnglishCopyright 2008 Marketwire All Rights Reserved.

LONDON, UNITED KINGDOM--(Marketwire - Oct. 1, 2008) - Reportlinker.com announces that a new market research report related to the Health food industry is available in its catalogue.

World Sports and Fitness Nutrition Market

http://www.reportlinker.com/p092492/World-Sports-and-Fitness-Nutrition--Market.html

This report analyzes the worldwide markets for Sports and Fitness Nutrition in Millions of US$. The specific product segments analyzed are Foods and Drinks (Sports/Energy Bars, Sports/Energy Drinks, & Powders to Mix), and Supplements

(Amino Acids/Derivatives, Herbal Products, Prohormones, Vitamins/Minerals, & Others). The report provides separate comprehensive analytics for the US, Canada, Japan, Europe, Asia-Pacific, Latin America, and Rest of World. Annual forecasts are provided for the period of 2001 through 2015. A ten-year historic analysis is also provided for these markets with annual market analytics. The report profiles 293 companies including many key and niche players worldwide such as Abbott Nutrition, Experimental & Applied Sciences Inc., AST Sports Science, Bodyonics Ltd, Body Wise International Inc., Champion Nutrition, Clif Bar Inc, Coca-Cola Co, Dr Pepper Snapple Group, Inc., Dymatize Enterprises, Inc., GlaxoSmithKline Plc., Hansen Natural Corporation, Kraft Foods Inc., Laboratoires Physcience, Maximuscle Ltd., MuscleTech Research and Development Inc., NBTY Inc, Nestle SA, Nestle Nutrition, Nestle Waters, Optimum Nutrition Inc., Otsuka Pharmaceutical Co., Ltd., PepsiCo Inc., The Quaker Oats Company, Red Bull GmbH, Seven Seas Ltd., Slim-Fast Foods Company, Schiff Nutrition International, Inc., and Yakult Honsha Co., Ltd. Market data and analytics are derived from primary and secondary research. Company profiles are mostly extracted from URL research and reported select online sources.

SPORTS AND FITNESS NUTRITION MCP-1089 A GLOBAL STRATEGIC BUSINESS REPORT

Factiva.comSearch terms: whey protein and emerging markets1. http://global.factiva.com/9lqW0VRwuX1Vy8wElyjuGlQnuO5rd42YIqe8DUknG7ucAXG553GSEh6I2PX_2Fm4YWIs2gzZn4hyD2LpTnCxwZUMB27Tysdp_2FdyzYvhKsdcl0onVWy0FYUw3ToTm3QRffkHczxN2oK6BwisfiQ4ajeBachwENoPSlz_2BmgKdpWIb0dT0xl_2FBEpXFN_2F98MaNcucn_7C2.mp3Listen to Article

NewsThe just-food interview - Peder Tuborgh, Arla Foods.just-food.com1217 words25 November 2008Just-FoodEnglish© 2008 Aroq Limited. All rights reserved

Dairy has proved one of the food industry's more colourful sectors in recent years with volatile prices, rising production costs and the emergence of buoyant emerging markets keeping processors on their toes. Arla Foods, Europe's second-largest dairy group, has set out its stall for international growth in this ever-evolving landscape. In

this month's just-food interview, Dean Best spoke with Arla CEO Peder Tuborgh to find out more about Arla's ambitions.

While the global dairy sector remains in a state of flux, one of the industry's heavyweights, Arla Foods, is looking to flex its muscles.

The only certainty in the dairy market at the moment is uncertainty. Following last year's record dairy prices, a combination of increased supply and lower consumer demand has hit prices in 2008. According to food industry analysts Rabobank, prices are expect to bounce back some time in 2009 as global demand recovers and dairy consumption in the world's emerging markets continues to grow.

However, the roller-coaster nature of dairy prices only serves to illustrate the volatility in the sector. Combine that with the spectre of increased production costs and the challenges for those that operate in the dairy sector are plain to see. Some dairy processors, like the Dutch giants Campina and Friesland Foods, have looked to join together to combat that volatility and industry watchers believes further consolidation in the sector is on the cards.

Arla, the Danish-Swedish co-operative, is not standing still. Last month, the company, Europe's second-largest dairy group, unveiled a five-year global strategy for the business. A focus on fewer markets, including those where dairy consumption has been buoyant, including China, and greater investment in product innovation are among the initiatives Arla believes will strengthen the business and improve returns for its farmer-members.

The company plans to double its investment in product innovation, while consolidating its brands into three "strong, global brands" – Castello, Lurpak and a new namesake brand. Arla is also looking to double its worldwide sales of whey protein.

For Arla CEO Peder Tuborgh the programme is vital. The 45-year-old joined Arla in 2000 in the wake of the company's merger with fellow dairy group MD Foods, where he had worked since 1987.

In almost a decade at Arla, Tuborgh has seen a great deal of milestones, not least the 2003 merger of its UK business with Express Dairies. However, Tuborgh, who has been in charge of Arla since 2005, believes the five-year plan unveiled last month is a watershed moment in the company's history.

“It is the most ambitious strategy, and also one of the most visionary strategies,” Tuborgh tells just-food. “We are now ready to look at all solutions that will strengthen the company for the benefit of our owners. We are ready to shift our current focus on brands and markets, open doors to new owners, and invest more in less brands and markets.”

The maker of brands including Castello cheese, Lurpak butter and Cravendale milk sells into around 100 markets worldwide but Tuborgh believes the time is right for Arla to take stock of its global presence and divert resources to key markets. “The main reason for our new and redefined focus on our international markets is a realisation that we get more out of our investments by focusing those investments on fewer markets,” Tuborgh says.

Arla has earmarked three so-called “seed” markets for particular attention. Russia, where Arla has a fledgling cheese and butter venture, the US, where the company has a growing cheese business and China, where the group runs a venture with local dairy group Mengniu, have been identified as key to the company's international growth.

“Any future Arla investments internationally will be focused on these three markets – that way we can benefit more from the investments,” Tuborgh says. “We cannot be everything to everyone on all markets and this new strategy seeks to maximise our impact by prioritising and categorising our world map. Arla is present on approximately 100 markets worldwide, so the need to create a sharper overall focus has been evident.”

One of the company's immediate areas of focus is likely to be China, where its venture was one of the dairy businesses caught up in the recent melamine-in-milk contamination scandal. Arla's Chinese partner Mengniu was named as one of the dairies at the centre of the melamine outbreak, which saw at least four babies die and thousands become ill after consuming milk powder contaminated with the industrial chemical melamine. The scandal rocked China's buoyant dairy sector, which has enjoyed rising milk consumption and attracted growing interest from multinational investors. The worry is just how China's growing love for dairy will be affected by the scandal. Tuborgh, however, is cautiously optimistic about the future of one of the markets central to Arla's international ambitions.

“Regaining consumer confidence is without doubt the absolute number one priority for us in China right now. And we believe it will happen – our expectations are to return to normal sales levels by the end of 2009,” Tuborgh insists. “Our advantage is that we offer products which have been through an extensive testing for melamine, which means we can offer the consumers products that are safe to consume. That being said, the development of the market in China has been set back by the unfortunate incidents this year. Over the long term, we do not doubt that dairy production has great prospects in China in the future.”

Tuborgh also sees opportunities closer to home. Under Arla's review, Germany and Poland have joined the company's “core” markets of Finland, Denmark, Sweden and the UK. Tuborgh keeps his cards close to his chest but the signs are that Arla will take an active role in the widely-expected consolidation in the European dairy sector.

“Although we cannot mention any specific names of potential partners at this point, we can say that Arla is currently searching the market for potential partners with

whom we can either set up some sort of collaboration with regard to local production and distribution or possibly buy other companies,” Tuborgh reveals. “Arla expects to play an active role in the consolidation of the dairy sector in Northern Europe in the next five years. At this point, we cannot get more specific about the nature of possible alliances, but we have identified both Germany and Poland as two new core markets for our business.”

Milk production is set to rise “significantly”, Tuborgh says, and he sees it as vital that Arla is ready to pounce should opportunities for acquisitions or alliances arise.

“We foresee a significant increase in milk production across this Northern European region, and our response to this must be to take part in that actively through consolidation. Growth is essential to success on the international dairy market today, and Arla simply cannot sit back and watch passively as new opportunities present themselves,” Tuborgh insists.

More to come...

This article was originally published on just-food.com on 25 November 2008. For authoritative and timely food business information visit http://www.just-food.com.

Document JUFOO00020081125e4bp000e1

More Like This

Top of pageUI 31.14.0 - Wednesday, November 19, 2008 3:07:14 PM

Google.com

Search terms:

http://www.usdec.org/files/ExportProfile/ExportProfile1105.pdf 1. search term: indian sports nutrition industry and consumer trends

http://www.drinks-business-review.com/researchindustry.asp?startpoint=i^CPG^Consumer4755&ParentTitle=Consumer+Insights

Browse ResearchThe very latest research reports from industry experts...Browse by Industry > Consumer InsightsConsumer SegmentationConsumer Need States

Consumer OccasionsConsumer Trends

Convenience ProductsHealthy ProductsIndulgence ProductsRESEARCH LISTINGThe Aging of BRIC populations30 Apr 2007New Developments in Global Consumer Trends16 Apr 2007The Burgeoning Middle Classes in Brazil, Russia, India and China (BRIC)13 Apr 2007Meeting Beauty and Wellness Needs Through Cosmeceuticals: Solving specific beauty and personal care problems for premium consumers4 Apr 2007Natural Personal Care Consumers: Unlocking Future Potential5 Mar 2007Functional Food & Drink Consumption Trends7 Feb 2007Understanding New Personal Care Behaviors & Occasions29 Dec 2006Tomorrow's Private Label Consumers29 Dec 2006Changing Cooking Behaviors & Attitudes: Beyond Convenience21 Dec 2006Changing Attitudes to Home Hygiene: From House-Proud To Carefree Consumers18 Dec 2006Reinvigorating On-Trade Sales 200714 Dec 2006Targeting Profitable Consumer Trends In Brazil, Russia, India and China14 Dec 2006Masstige & Super-Premium Consumers: Attitudes & Buying Habits7 Dec 2006Marketing To Kids: How To Be Effective And Responsible5 Dec 2006Capitalizing on Natural & Fresh Food & Drink Trends29 Sep 2006How To Exploit New Wellness Trends in Food: resolving the conflict between healthy desires and unhealthy lifestyles29 Sep 2006Trading Up Opportunities in Male Grooming: how to profit by going beyond the 'metrosexual' myth28 Sep 2006Capitalizing On New Breakfast, Lunch & Dinner Consumption Patterns25 Sep 2006

Trends in Novel Versus Traditional Food Flavors: How to benefit from growing desires for intensity and comfort20 Sep 2006Profiting From New Trends in Mid-lifers' Lives18 Sep 2006Keeping Young Adults Loyal in Alcoholic Drinks6 Sep 2006Profiting from Changing Snacking and Beverage Occasions16 Aug 2006How To Attract New Sports Nutrition Consumers: using mainstream health trends to pitch professional-style products8 Aug 2006Seeking Beauty Through Nutrition1 Aug 2006Best Practice In Marketing To Female Consumers3 Jul 2006How To Exploit New Wellness Trends in Drinks12 Jun 2006Targeting Untapped Opportunities In Seniors' Alcoholic Drinking Behaviors18 May 2006Escaping The Discount Trap In Off-Trade Alcoholic Drinks31 Mar 2006Wellness Trends in Personal Care: How To Profit From The Health & Beauty Crossover17 Mar 2006New Opportunities In Out-of Home Food and Drinks Consumption1 Mar 2006How to Resist the Private Label Threat in 200626 Dec 2005Profiting From Consumers' Desires For Healthy Indulgences26 Dec 2005Building & Profiting From Consumers' Trust21 Dec 2005Seniors' Personal Care Behaviors and Occasions21 Dec 2005Attracting New On-Trade Alcoholic Drinks Consumers in 200621 Dec 2005Overweight Consumers and the Future of Food and Drinks21 Dec 2005New Trends In Snacking & Drinking On-The-Go20 Dec 2005Capturing 50-plus Year Olds' Spending in 200615 Nov 2005The Impact of Changing Family Lifestyles on Consumer Packaged Goods25 Oct 2005High Quality Snack & Beverage Consumers

12 Oct 2005The Future of Eating Meals On-The-Go26 Sep 2005Insights into Tomorrow's Cosmeceutical Consumers6 Sep 2005New Insights into Viral and Word of Mouth Marketing in Consumer Packaged Goods29 Aug 2005Insights Into Tomorrow's Ethnic Food & Drink Consumers25 Aug 2005Insights into Tomorrow's Over 25s Alcoholic Drinks Consumers22 Aug 2005Personal & Oral Care On-The-Go3 Aug 2005Evolution of Global Consumer Trends4 Jul 2005The Future of Mealtimes14 Jun 2005Developing Products With A Price Premium26 May 2005Empty Nesters and Consumer Packaged Goods25 May 2005Next 50 reports

Click here to find out more!

2. New Developments in Global Consumer TrendsFURTHER INFORMATIONProduct Type: ReportPublished: 16 Apr 2007Available Format(s): PDFTable of contentsProduct BrochurePublished by: DatamonitorPrice: $7995

IntroductionThis report based on a vast array of primary and secondary research provides a comprehensive snapshot of global consumer behavior. Structured around Datamonitor's well-established mega-trends framework, it offers added clarity, new detailed insight, future trend predictions and intuitive recommendations for marketing and product development.

Scope

* Detailed insight and analysis covering each of the 10 mega-trends with a separate Action Points chapter outlining product development opportunities * Extensive primary research profiling how the consumer attitudes and behaviors influencing the mega-trends have evolved and will continue to evolve * All new trend prediction and implications sections offering futuristic perspectives on every major trend shaping global consumption patterns * Showcases the latest best-practice, "on-trend" product and marketing innovation offering a wealth of creative ideas to guide future innovation

HighlightsIndustry executives surveyed globally believe that health is the most important mega-trend influencing their business today. Changes in consumer values and behavior have been profound; 76% of European and US citizens overall are "conscious of health and wellness issues on a daily basis". Going forward, the trend will only increase in significance.

Consumer preferences are often counter-intuitive leading to a scenario of trends and counter trends. On one level, shoppers are more experimental and value customized choice. But 'choice paralysis' means consumers are simplifying shopping by downsizing the subset of brands in their 'consideration set' of product choices.

Ethical consumerism will continue to migrate away from a small minority of consumers towards the mainstream. Consumers will increasingly expect brands to show they are responsible in the public domain whether contributing to the local community, divulging the means of sourcing, or offering a responsible consumer buying choice.

Why you should buy this report

* Increase the likelihood of being "on-trend" by learning how the mega-trends have affected behaviors and how they are likely to evolve. * Access a wealth of market, behavioral and attitudinal time-series data that can be used to guide your future marketing plans. * Save time and gain maximal insight by using this 'one-stop-shop' resource which offers a clear and up-to-date framework for understanding consumers.

3. The Burgeoning Middle Classes in Brazil, Russia, India and China (BRIC)FURTHER INFORMATIONProduct Type: BriefPublished: 13 Apr 2007Available Format(s): PDFTable of contentsProduct BrochurePublished by: DatamonitorPrice: $1695

IntroductionAll of the BRIC markets have great potential for overcoming their past economic underperformance and establishing the most stabilizing of forces a prosperous middle class. This group in each country is growing at varying rates but the future direction is clear: the middle class will both broaden and deepen providing a solid base for the development of a strong consumer packaged goods industry.

Scope

* In-depth quantitative data covering historical and forecast demographic trends in Brazil, Russia, India and China. * Covers population size and growth overall, by age and gender, and incidence of key age-related health conditions. * Qualitative analysis of these key population trends. * Actionable recommendations for producers and marketers seeking to leverage opportunities within those markets.

HighlightsSince the late 1990s, Russia's economy has benefited from the twin factors of economic structural reforms and high global commodity prices of oil. These have boosted consumer confidence as individuals are more confident of their current situation and their ability to plan their future expenditure, especially in the middle class.

India's overall GDP is reasonably strong but this is mainly due to the vast population of the country. On a per capita basis it lags behind the other BRIC countries. In 2005 the par capita GDP of China was almost double that of India with Brazil and Russia some distance ahead.

Home ownership in Brazil is higher than in the US and is growing steadily, whereas in all other BRIC countries the rate of occupant ownership is in decline. The average home price in Brazil is the highest in all of the BRIC countries but the gap is being closed by China which should almost reach parity by 2010.

Why you should buy this report

* Gain access to detailed data and forecasts to inform your decision-making * Understand the economic trends and shifting consumer motivations in the BRIC countries * Improve your marketing by following best-practice guidelines enabling more effective targeting with on-trend products and relevant communications

If you would like more details on this research report, fill in your details below and one of our

4. The Aging of BRIC populationsFURTHER INFORMATIONProduct Type: BriefPublished: 30 Apr 2007Available Format(s): PDFTable of contentsProduct BrochurePublished by: DatamonitorPrice: $1695

IntroductionMarkets such as Brazil, China, India and Russia (BRIC) should be seen within the context of a transitional period, moving in the direction of developed markets and experiencing a marked aging of their populations in coming years. This will emphasize the need to respond to a reshaping of consumer demand to accommodate the differing needs of an older populace.

Scope

* In-depth quantitative data covering historical and forecast demographic trends in Brazil, Russia, India and China. * Covers population size and growth overall, by age and gender, and incidence of key age-related health conditions. * Qualitative analysis of these key population trends. * Actionable recommendations for producers and marketers seeking to leverage opportunities within those markets.

HighlightsA divide exists between Western markets and those of the less developed world, where the demographic center of gravity tends to be skewed towards youth. However, Brazil, China, India and Russia should be seen within a transitional context, driven by their economic growth and varying degrees of proximity to the Western consumer model.

Adoption of branding, marketing or strategies that fit with the historical value placed on seniors in certain countries and cultures, particularly China and India, offers a smart way to leverage market position in the context of aging populations. Extended families and a deep-seated societal respect for older citizens remain important factors.

Brand loyalty is decreasing across all age groups. This has been a general trend in developed markets for the past few decades that the BRIC countries are set to emulate. A shift towards higher average ages means that a change in marketers' priorities and message away from a focus on younger consumers is necessary to retain competitiveness.

Why you should buy this report

* Gain access to detailed data and forecasts to inform your decision-making * Understand the population trends and shifting consumer motivations in the BRIC countries * Improve your marketing by following best-practice guidelines enabling more effective targeting with on-trend products and relevant communications

5. New Developments in GlobalConsumer TrendsThe definitive trend guide to modern consumerlifestyles and behavior

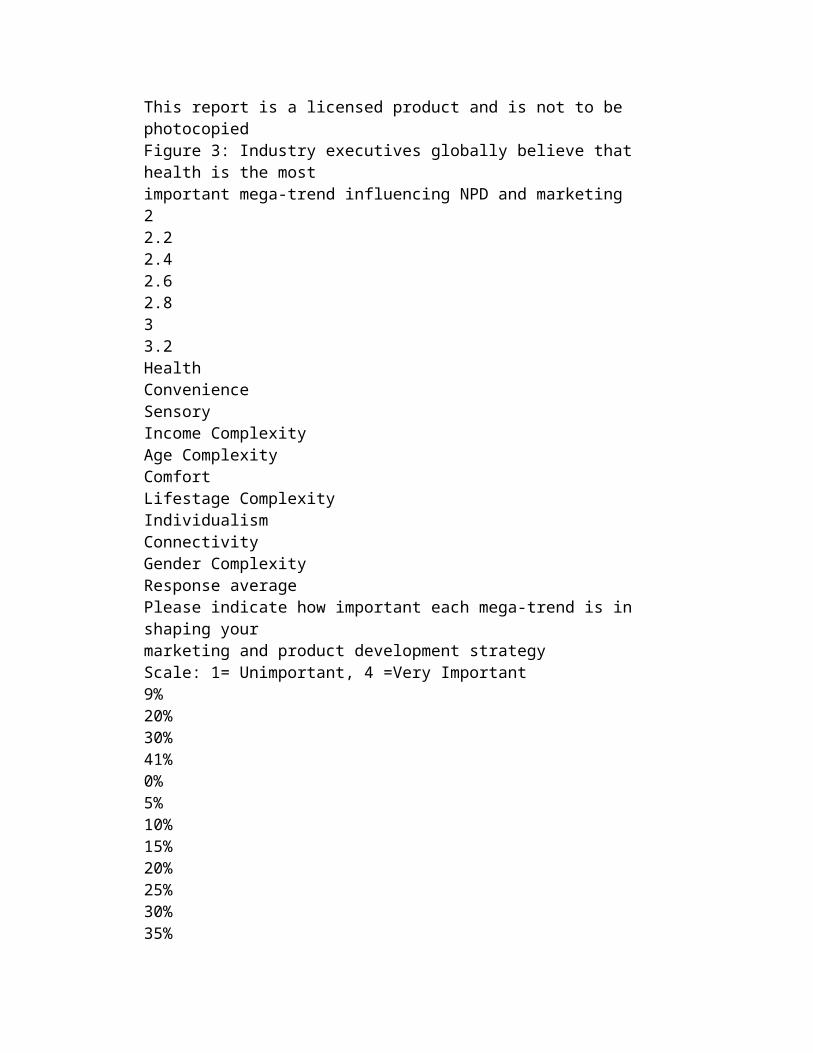

IntroductionThis report – based on a vast array of primary and secondary research –provides a comprehensive snapshot of global consumer behavior. Structuredaround Datamonitor’s well-established mega-trends framework, it offers addedclarity, new detailed insight, future trend predictions and intuitiverecommendations for marketing and product development.Over the next ten years there will be continual developments with regard to the mega-trendsbecause trend cycles are emerging more rapidly as a result of technology, accelerated socialdiffusion, instantaneous communication and a growing willingness to accept or inability toescape new ideas. Only by understanding these new interpretations of the mega-trends cancompanies remain “on-trend” in the long-term and actually save time by gaining a broad clearperspective of the macro-factors influencing sales today.Key findings and highlights• Industry executives surveyed globally believe that health is the most important mega-trendinfluencing their business today. Changes in consumer values and behavior have beenprofound; 76 per cent of European and US citizens overall are "conscious of health andwellness issues on a daily basis". Going forward, the trend will only increase in significance.• Consumer preferences are often counter-intuitive leading to a scenario of trends and

counter trends. On one level, shoppers are more experimental and value customizedchoice. But 'choice paralysis' means consumers are simplifying shopping by downsizing thesubset of brands in their 'consideration set' of product choices.• Ethical consumerism will continue to migrate away from a small minority of consumerstowards the mainstream. Consumers will increasingly expect brands to show they areresponsible in the public domain whether contributing to the local community, divulging themeans of sourcing, or offering a responsible consumer buying choice.Reasons to buy• Increase the likelihood of being "on-trend" by learning how the mega-trends have affectedbehaviors and how they are likely to evolve• Access a wealth of market, behavioral and attitudinal time-series data that can be used toguide your future marketing plans• Save time and gain maximum insight by using this 'one-stop-shop' resource which offers aclear and up-to-date framework for understanding consumerswww.datamonitor.com/consumerSample pages from the reportThe Future DecodedNew Developments in Global Consumer Trends DMCM2468© Datamonitor (Published 04/2007) Page 35This report is a licensed product and is not to be photocopiedFigure 3: Industry executives globally believe that health is the mostimportant mega-trend influencing NPD and marketing22.22.42.62.833.2HealthConvenienceSensoryIncome ComplexityAge ComplexityComfortLifestage ComplexityIndividualismConnectivityGender ComplexityResponse average

Please indicate how important each mega-trend is in shaping yourmarketing and product development strategyScale: 1= Unimportant, 4 =Very Important9%20%30%41%0%5%10%15%20%25%30%35%40%45%Unimportant Somewhat important Important Very important% of industry respondentsPlease indicate how important each mega-trend is in shaping yourmarketing and product development strategy: HealthSource: Datamonitor Global Industry Opinion Survey, 2006 D A T A M O N I T O RThe Future DecodedNew Developments in Global Consumer Trends DMCM2468© Datamonitor (Published 04/2007) Page 151This report is a licensed product and is not to be photocopiedFigure 65: Compact living is often necessary among singlesSource: Datamonitor analysis D A T A M O N I T O RFigure 66: Compact living is accentuated by the negative correlationbetween property size and the average number of people perdwellingAustraliaBrazilChinaFranceGermanyIndiaIndonesia IranItalyMexicoPolandKoreaRussiaSaudi ArabiaSouth AfricaSpain

ThailandUkraineUKUnited States40901401902402 3 4 5 6 7Average number of people per dwelling, 2005Average size of dwelling (square meters), 2005CAGRAverageCAGRAverageSource: Datamonitor analysis D A T A M O N I T O RThe Future DecodedNew Developments in Global Consumer Trends DMCM2468© Datamonitor (Published 04/2007) Page 167This report is a licensed product and is not to be photocopiedThe authenticity trend is, in part, rooted in the desire for qualityAn increasingly affluent consumer base is becoming more educated about the qualityand variety of consumer goods available, making them more critical of the quality ofgoods on retailers’ shelves. Consequently, there is a growing consumer perceptionthat mass-market food, drinks and personal care products, typically purchased inchain retailers, are bland and lacking hedonic benefits. Therefore, being perceived as“the real thing” or “genuine” is increasingly important. Figure 73 summarizes thesocial and consumer dynamics driving the authenticity trend.Figure 73: The search for authenticity reflects consumers’ active pursuitfor higher quality experiences from consumption‘Authenticity’ is a concept built on 6 coreattributes relating to hedonic benefits andheritage‘Authenticity’ is cultural backlashagainst modern world realitiesConsumers are seeking to ‘reconnect with the real’: a desire for a timeoutand a greater interest in the values steeped in tradition• Seeking artisinal, handcrafted specialty products• e.g. growing hand-made, hand-fried, limited edition• Seeking more detailed, regional sensory profiles e.g.• e.g. Catalan wine – not Spanish; Oxacan – not Mexican; Hunan – not Chinese• Seeking origin specific goods• e.g. single origin chocolates and locally sourced ingredients• Choosing heritage brands• e.g. buying into story-based heritage brands

• Expanding connoisseurship• authenticity is also about growing connoisseurial knowledge and preferences• Greater willingness-to-pay (WTP) price premiums• knowing that premiums justify the added nuances in product designSource: Datamonitor analysis D A T A M O N I T O RRequest more sample pages...for FREE!From Europe: tel: +44 20 7675 7202 fax: +44 20 7675 7016 email: [email protected] the US: tel: +1 212 686 7400 fax: +1 646 365 3362 email: [email protected] Asia Pacific: tel: +61 2 8705 6900 fax: +61 2 8705 6901 email: [email protected] Developments in Global Consumer TrendsDMCM2468Daniel Bone, New Developments in Global Consumer Trends“...Factiva.com

Search term: india and demographic

1. India economy: Demographic profile829 words20 August 2008Economist Intelligence Unit - ViewsWireViewsWire18English(C) 2008 The Economist Intelligence Unit Ltd.

COUNTRY BRIEFING

FROM THE ECONOMIST INTELLIGENCE UNIT

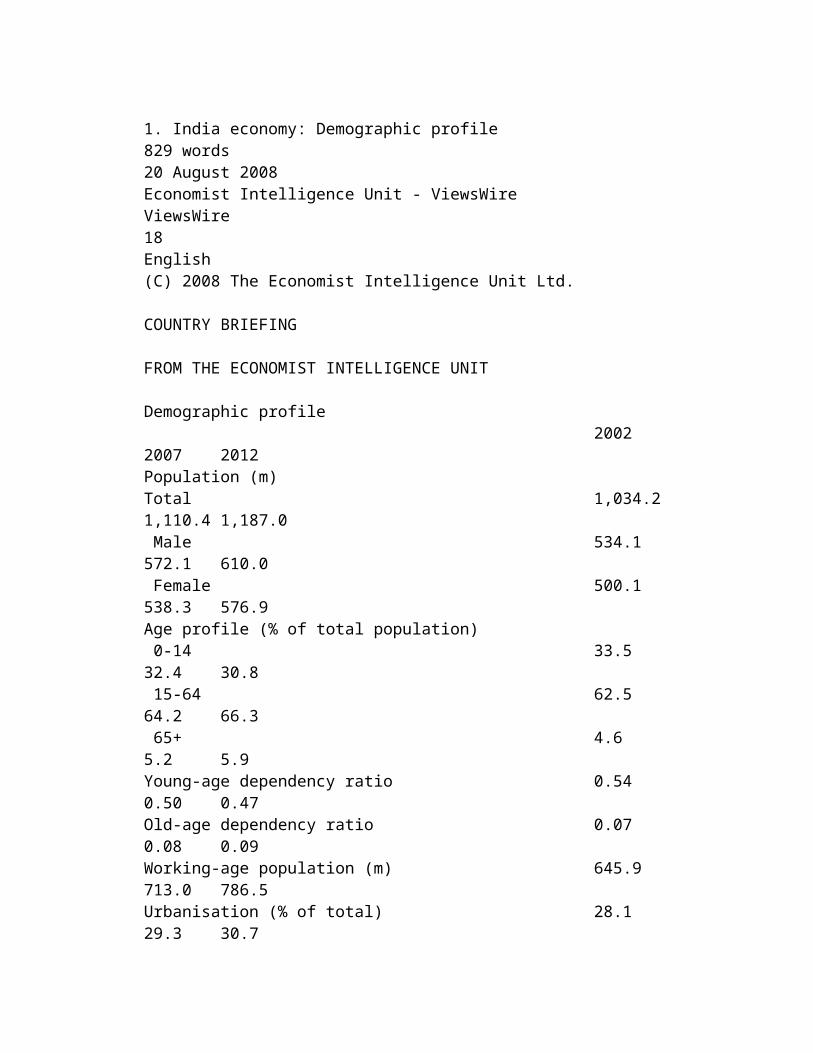

Demographic profile 2002 2007 2012Population (m)Total 1,034.2 1,110.4 1,187.0 Male 534.1 572.1 610.0 Female 500.1 538.3 576.9Age profile (% of total population) 0-14 33.5 32.4 30.8 15-64 62.5 64.2 66.3 65+ 4.6 5.2 5.9Young-age dependency ratio 0.54 0.50 0.47Old-age dependency ratio 0.07 0.08 0.09Working-age population (m) 645.9 713.0 786.5

Urbanisation (% of total) 28.1 29.3 30.7Labour force (m) 470.2 516.4 570.1 Period averages 2003-07 2008-12Population growth (%) 1.4 1.3Working-age population growth (%) 2.0 2.0Labour force growth (%) 1.9 2.0Crude birth rate (per 1,000) 23.6 21.4Crude death rate (per 1,000) 7.0 6.1Infant mortality rate (per 1,000 livebirths) 39.8 28.2Life expectancy at birth (years) Male 65.0 68.0 Female 69.6 73.3 Average 67.2 70.5Sources: International Labour Organisation(ILO), labour force projections; Economist Intelligence Unit estimates andforecasts; national statistics.

India will become the most populous country within the next 30 years

Although the population growth rate is gradually falling, the past failure of family planning policy means that India is expected to overtake China as the world's most populous country in the early 2030s, with a population approaching 1.5bn. Governments have shifted away from sterilisation as the cornerstone of family planning to an emphasis on improving female social and economic welfare. This, coupled with rising living standards, particularly in urban areas, is leading to a fall in the population growth rate. Nonetheless, although strong economic growth is slowing the fertility rate, at 3.1 children per woman, it is one-third above the official target of replacement-level fertility.

The rising population will lead to opportunities and costs. Increased environmental degradation and a growing strain on water and food resources appear inevitable. By 2012 the proportion of the population in the 0-14 age group is expected to fall to around 30%, with potentially beneficial implications for the education system. The proportion of the population over 65 is projected to rise slightly, but in the absence of a national pension system this does not have the worrying implications for pension liabilities that more highly developed countries face.

Better education will be vital if India is to realise its potential

India will, however, enjoy a growing working-age population at a time when other countries (including China) will face increasing dependency ratios. If India can put in place an education system that ensures its working-age population meets global demands, then it will perform well, probably through a combination of production shifting to India, and from Indian workers migrating to meet the needs of other

countries. If its education system fails to adapt, however, a large underemployed population is likely to result in increased social instability.

The gender distribution of India's population is disturbing and has equally important implications for stability. According to the 2001 census, for every 1,000 boys under the age of six, there were only 927 girls. In the worst-affected states, this figure fell below 800. Child mortality rates are higher for girls than boys, and foeticide (aborting a foetus identified as female) is becoming more common as technology enabling elective abortions spreads—despite the fact that these procedures, along with sex-determination tests, are illegal. Historically, countries with severe gender disparities suffer from rising disorder.

Job creation in the rural economy could stem rural-urban migration

Rates of rural underemployment and urban unemployment are high, and India's lack of a well-developed industrial base has hindered employment generation. The government is pinning its hopes on the expansion of the manufacturing sector to increase employment opportunities, but employment growth in the sector will not keep up with the expansion in the labour force. Migration into towns and cities from the countryside is also creating employment stress. India's urban population is expected to rise from just over one-quarter of the total population in the mid-1990s to over one-third by 2010. This will put pressure on the infrastructure of cities, which in most cases is unable to support even current population levels. The supply of transport, water, power and housing in many urban areas is thus likely to be stretched further, and levels of pollution and crime may rise. The need to improve opportunities in rural areas to deter migration and to stimulate the rural economy has been recognised by policymakers, but progress has been slow. The current government has made this its first priority, but achieving quick results will be difficult.

vwvwmain20080820t1405000018; EIU ViewsWire 20 Aug 2008 (T14:05), Part 18 of 43

Document EIUCP00020080822e48k0004r

More Like This

Top of page | Next 100UI 31.14.0 - Wednesday, November 19, 2008 3:07:14 PM

© 2008 Factiva, Inc. All rights reserved. Feedback | W

Yahoo!Search terms: india and whey protein and market trends

Cognis Expands Ops in India02/01/2008

MONHEIM, Germany— Cognis opened a liaison office in Mumbai, India, aiming to strengthen relationships with existing customers and initiate new business opportunities. According to the company, it has seen significant growth in India in the last few years, focusing on supplying specialty chemicals and other ingredients for the wellness and sustainability markets. Cognis already has a strong network of distributors in India covering almost all market segments of its product portfolio.

The liaison office will consolidate Cognis’ activities and expertise in India, while strengthening local ties and analyzing market trends on the ground. It will represent all three of Cognis’ strategic business units—Care Chemicals, Nutrition & Health, and Functional Products. Sales activities will continue to be carried out by local distributors.

Share this article: Email, Slashdot, Digg, Del.icio.us, Yahoo!MyWeb, Windows Live Favorites, FurlRSS Add this article feed to: RSS, My Yahoo, Newsgator, Bloglines

2. Recent Trends in Development of Fermented MilksH. K. Khurana1 and S. K. Kanawjia2*1Science and Technology Entrepreneurs Park, Thapar Institute of Engineering and Technology, Patiala – 147004,Punjab, India, 2Dairy Technology Division, National Dairy Research Institute, Karnal - 132001, Haryana, IndiaAbstract: Ever-growing consumer demand for convenience, combined with a healthy diet and preference for naturalingredients has led to a growth in functional beverage markets. Current trends and changing consumer needs indicate agreat opportunity for innovations and developments in fermented milks. Scientific and clinical evidence is also mountingto corroborate the consumer perception of health from fermented milks. Probiotics, prebiotics, synbiotics and associatedingredients also add an attractive dimension to cultured dairy products. Also, owing to expanding market share and size ofdairy companies, there has been a reduction of clearly structured markets i.e. merging of dairy products and fruit beveragemarkets with introduction of ‘juiceceuticals’ like fruit-yogurt beverages that are typical example of hybrid dairy productsoffering health, flavour and convenience. Another potential growth area for fermented milks includes added-valueproducts such as low calorie, reduced-fat varieties and those fortified with physiologically active ingredients includingfibers, phytosterols, omega-3-fatty acids, whey based ingredients, antioxidant vitamins, isoflavones that provide specific

health benefits beyond basic nutrition. World over efforts have been devoted to develop fermented milks containingcertain nonconventional food sources like soybeans and millets and convert them to more acceptable and palatable formthus producing low cost, nutritious fermented foods especially for developing and underdeveloped nations wheremalnutrition exists. Furthermore, use of biopreservatives and certain innovative technologies like membrane processing,high pressure processing and carbonation lead to milk fermentation under predictable, controllable and precise conditionsto yield hygienic fermented milks of high nutritive value.Keywords: Recent trends, fermented milks, yoghurt, probiotics, health benefits, biopreservatives.

CONSUMPTION PATTERNSAccording to a study by global market analyst Euromonitorinternational global sales of dairy products reached¤211.5 billion [14]. The manufacture of cultured dairyproducts represents the second most important fermentationindustry (after the production of alcoholic drinks) [1]. Adynamic category, fermented dairy drinks were reported togrow at six times the rate of total dairy growth between 1998and 2003 in value terms. Also, probiotic drinking yoghurtwas the fastest growing dairy product sector between 1998and 2003, followed by soy milk, (spoonable) probioticyoghurt, flavoured milk drinks with juice and fermenteddairy drinks [15].The increasing demand from consumers for dairyproducts with 'functional' properties is a key factor drivingvalue sales growth in developed markets. This led to thepromotion of added-value products such as probiotic andother functional yoghurts, reduced-fat and enriched milkproducts and fermented dairy drinks and organic cheese [14].Another important global trend is the increasing demand forconsumer convenience. Present day consumers prefer foodsthat promote good health and prevent disease. Furthermore,these foods must fit into current lifestyles providingconvenience of use, good flavor, and an acceptable pricevalueratio. Such foods constitute current and future waves inthe evolution of the food development cycle [16]. There areseveral principal reasons for the success of fermented dairyproducts, which relate to nutrition and health, versatility andmarketing. Scientific and clinical evidence is also mountingto corroborate the consumer perception of health fromfermented milks [15].The consumption of milk drinks and fermented products

has been recently reviewed by the International DairyFederation, shown briefly in Table 2 [17]. It is quite clearfrom the data that the consumption of fermented milks hasgenerally increased around the globe over a period from2001 to 2004. According to another report by Euromonitor[14] largest fermented dairy market till 2003 was Japan,where the leading brand Yakult is the reference product forthe entire category, having been available in Japan for morethan 50 years. The next most significant markets are SouthKorea and Brazil, followed by a number of WesternEuropean markets including US probiotic drinking yoghurts,booming on the basis of their portability, snack appeal andhealth claims which match those of fermented dairy drinks;offering improvement to digestive health and a boost to theimmune system. In fact, Western Europe has increased inimportance, becoming the second largest region forfermented dairy drinks ahead of Latin America. In 2002Danone’s Actimel, the second largest brand globally, becamethe first fermented dairy drink to be launched in the US [15].In the Indian subcontinent also, fermented milk productssuch as dahi (curd), Lassi (sweetened yoghurt drink likeproduct)/chhach (buttermilk) and shrikhand (drained curdadded with sugar and flavoring) figure prominently inpeople’s diet. The demand for fermented milk products isincreasing and it has been estimated that about 10% of totalmilk produced in India is used for preparation of traditionalfermented milk products. Dahi is an age-old indigenousFig. (1). The Family Tree of Fermented Milk Types [7].fermented milk of India and has managed its popularity inIndian diet despite changing lifestyles and food habits.About 6.9% of total milk produced in India is utilized formaking dahi intended for direct consumption. The volume ofcurd and curd products was reported to be 6.0 million toneswith a market value of 120 billion rupees [10].PRODUCT DEVELOPMENT STRATEGIES AND

CONCLUSION AND FUTURE PERSPECTIVEIt is evident that the market for fermented milks isbooming specially probiotics and those with special addedingredients. Modern consumers are increasingly interested intheir personal health, and expect the food that they eat to behealthy or even capable of preventing illness. Producers andmarketers of cultured milks are making every effort to keepthem growing through product development and packaginginnovations while delivering a ‘good for you’ flavorfulproducts suited for all occasions of gastronomic indulgence.

A major consideration in the continued development andsuccess of ever growing fermented milk market iscommunication. This is linked to other important factorssuch as development of supporting scientific documentation;a health claims strategy and successful presentation.Over the past century, voluminous scientific knowledgehas been well established regarding the technological aspectsof fermented milks, including the physiology of startercultures and related probiotic microflora. However, over thecoming years the possible research areas may include thefollowing aspects:· Special emphasis on research in arena of starters andtheir functionality is required; specially in view ofnatural biodiversity that still exists in food grademicroorganisms as starter cultures are the heart offermented milk industry. It is also very important topreserve this pool for future application. Thus, it isnecessary to have better understanding of enzymicpathways in these starters in order to be able to selectstrains with specific, desired characteristics.· Appropriate international definition(s) of yoghurt andother fermented milks including other probiotic productsare required.· More emphasis is required to get a clear understandingof relationship between food, intestinal bacteria, humanhealth and disease in the field of probiotics along withproperly designed clinical studies to establish the properhealth benefits to humans. Many a times in vitro resultscannot be found in vivo, and observations reported inanimals cannot be translated directly to humans; thereare problems in generalizing the results given types ofmicroorganisms used thus more number of clinicalstudies should be conducted on humans of differentraces in different countries to properly substantiate thehealth benefits to humans in general.· Newer molecular research tools, better process formulationtechnologies for enhanced probiotic stability andfunctionality along with biosafety evaluation ofprobiotics used for human consumption are other majorthrust areas. New product categories, and thus novel andmore difficult raw materials with regard to technologyof probiotics, will certainly be the key research anddevelopment area for future functional food markets.There are now products with complete supplementationoffered as medical foods, as well as healthy products forpeople who have problems obtaining all the nutrients they

need. It is clear from the literature that new kinds offermented milks containing various nutrients are being testedas curatives for specific diseases and are approachingmedical food effectiveness in conventional food format andwill continue to be introduced to the food supply. Theoccurrence of diet-related diseases of deficiency and excess,points to the importance of the development of functionalfoods (science). Functional food science must be viewedworld over beyond the short-term commercial prospects andshould be considered for long-term research anddevelopment.REFERENCES[1] Anon. It’s a tiny world (online). Food Today 2003; 16: 3. EuropeanFood information council online. http://www.eufic.org/gb/food/pag/food16/food163.htm.[2] Beena AK. Healthbenefits of fermented milks. In:

Yahoo!

Search terms: consumer market and india and health nutrition trends

4. Country Case Study: IndiaThe Functional Foods Sector in IndiaIndia’s traditional and regional foods have been documented throughout theages as containing healthy properties, beyond just their nutritional value. Suchhistorically functional foods include herbal extracts, fortified foods, spices,pulses (lentils), and vegetables and fruits.The proven special health properties of functional foods have treatedcommon ailments for centuries. New research is showing that many of thesefoods have preventive properties as well. The Central Food TechnologicalResearch Institute (CFTRI) in Mysore is documenting this history as well asnewer trends in functional foods through its Knowledge Digital Library(Central Food Technological Research Institute 2005). This effort will supporta better understanding of the functional attributes of these foods whileprotecting the intellectual property rights of those who develop new types offoods through R&D.Functional foods R&D in India is rapidly expanding and includes, among otherproducts, nutraceuticals, prebiotics and probiotics, and newer additives, whichare known to prevent certain diseases or other maladies. New research showsthat many of the traditional Indian foods have characteristics of functionalfoods and underscores the fact that the Indians have been consumingfunctional foods for centuries.With this new recognition of functional foods comes new opportunities forproducers to mislabel and overstate the efficacy of their products, requiringthat special attention be paid to the regulatory aspects, particularly as the laws

on functional foods require updating.Functional Food TrendsAs in China, India’s health foods history dates back centuries. Thedevelopments over the last few decades now recognize the value of traditionalmedicines and naturally health-enhancing foods. With its strong tradition ofhealthful eating, India ranks among the top 10 nations in buying functionalfoods (Watson 2006). India’s food industry is generating $6.8 billion in annualrevenue, and this is expected to nearly double in the next five years (Ismail2006).5The government is working to help India become a major force in theinternational functional foods market by updating its intellectual propertylaws and increasing investment in R&D infrastructure (Ismail 2006). Thereis unanimity among major companies, and in government, where bothministers and the substantial state research organizations are behind the ideaof India becoming a major force in the international health foods marketHealth Enhancing Foods19Agricultural and Rural Development20(Shrimpton 2004). In addition, there is little resistance from consumers to buyfunctional foods.In 1950, the Indian government established CFTRI, which has grown to be oneof the world’s largest food research institutes and one that is actively involvedin teaching (Shrimpton 2004). Furthermore, according to sources interviewed,of the more than 200 research institutes and laboratories in India, 25 percentare involved in food research. With such substantial scientific support, theIndian food industry has the possibility to become a significant player in theinternational market supplying high-quality functional foods.According to Dr. S. R. Rao at the Council for Scientific and Industrial Research(CSIR), New Delhi, the thrust of publicly funded research in functional foodshas been on developing fortified foods,6 because this research reflects thegovernment’s concern with malnutrition. According to Dr. Rajesh Kapur,director of the Department of Biotechnology, approximately 60 percent ofchildren below 14 years of age are malnourished (Kapur 2006). Thus, thegovernment has launched the national nutrition mission with the objective ofproviding ready-to-eat precooked food at a low cost and midday meals tostudents at government schools.Dr. S. R. Rao noted that basically there are three countrywide governmentsponsoreddistribution channels for general nutrition-enhancing functionalfoods, namely the following: Public Distribution System (PDS): A system of government-licensed shopswhere grains, sugar, and kerosene oil are subsidized and priced accordingto each family’s monthly entitlement. Midday Meal Scheme: A government-funded program under whichprecooked meals are provided to children at government schoolsthroughout the country (the national nutrition mission referred to above).

Integrated Child Development Services (ICDS) Scheme: A programconceived in 1975 aimed at improving the nutritional and health statusof vulnerable groups (for example, preschool children, pregnant women,and nursing mothers) by providing a package of services includingsupplementary nutrition, preschool education, immunization, healthcheckups, referral services, and nutrition and health education.On consumer behavior, Dr. Kapur said that there is very little awareness offunctional foods among general consumers even though these foods havealways been part of the Indian diet. This opinion is supported by researchanalysts whose report states that awareness of the term “fortified foods”among Indian consumers is low, but there is a high awareness of certainbrands, especially in the case of iodized salt. According to the report, althoughmany people may be eating fortified foods without being aware of it,approximately 30 percent of people in India’s cities regularly consumefortified foods.7 India has been quite progressive in its fortification programsas an early adopter, and often initiator, of many processes.8The government is expected to continue to actively press for the developmentof the functional foods industry. According to a representative of the MinistryHealth Enhancing Foods21of Food Processing Industries, the ministry’s mandate is to develop andpromote the food processing sector, including functional foods, throughoutthe country. It conducts seminars, workshops, and training programs and hasa financing scheme that provides grants-in-aid to the food processingcompanies that want their manufacturing or processing units certified forinternational safety standards, such as Hazard Analysis and Critical ControlPoints (HACCP) and the International Organization of Standardization (ISO).In a speech at Foodworld India 2005, Mr. D. P. Singh, secretary, Ministryof Food Processing Industries, introduced “Vision 2015,” which aims to triplethe size of the food sector in 10 years time by increasing the level of processingof perishable goods from 6 percent to 20 percent, value added products from20 percent to 35 percent, and share in global trade from 1.6 percent to3 percent. Such efforts would require making processed foods affordabledomestically and competitive globally; this effort would include functionalfoods. An investment of approximately US$25.5 billion is envisioned in thenext 10 years.In addition to the substantial government support, the functional foodsindustry is thriving in the private sector. According to the Frost and Sullivanmarketing study, the large food manufacturers understand their consumersin both the mass market and the value added market. With many peoplesuffering from deficiencies of iron, iodine, and vitamin A, the consumer canbuy many fortified foods, such as wheat flour, iodized salt, calcium, andvitamin-enriched jams and soft drinks. To address vitamin Adeficiency, whichis prevalent in much of rural India, food companies have introduced specificproducts at affordable prices. For the middle-class consumer, companies havelaunched such products as low-sodium salt, which is beneficial to patients

with high blood pressure (NutraIngredients.com 2006).Although China is seen as the major competitor, Indian research technology inareas like fermentation processes, plant extraction, and chemical synthesis aremore developed than their Chinese counterparts, and they still benefit fromthe labor cost savings that make outsourcing to India so attractive (Ismail2006). Some people among those involved with functional foods developmentbelieve that Ayurvedic medicine and philosophy, based on knowledgeaccumulated over 4,000 years, offers India several advantages. It is alsorecognized that for these products to be successfully exported, however, theherbs that form their basis must be standardized, or at least their potency mustbe measurable. Traditionally, this is not in accordance with Ayurvedicphilosophy, which recognizes the benefits of variation between growingconditions and individuals. Currently, there is no regulation concerningAyurvedic-based products (Shrimpton 2004).Recognizing the favorable government support combined with the researchfriendlyenvironment and available qualified human resources, European andU.S. multinational firms are already located in India, including Herbalife,DuPont, GlaxoSmith Kline, Akzo Nobel Chemicals, Hindustan Lever, Heinz,Novartis, and Roche. There are also a growing number of Indian companiesthat are working internationally, such as the Associated Capsules Group

Functional Food Constraints and Opportunities in the IndianMarketThe market environment for functional foods in India, while cooperative andrelatively advanced, faces the following constraints and opportunities:Low income of vast majority of the population. For the domestic market toreach its full potential, income levels for the vast majority of the populationwill have to rise. Although disposable income has increased over the yearsand is expected to continue to do so (see the section “Functional FoodTrends”), it is still very low and likely to remain so for many years.Various creative solutions by private industry have been used to overcome theproblem of people having a very small daily disposable income. SomeHealth Enhancing Foods25Box 5. India: Complexity of LicensingAn individual planning to manufacture, distribute, stock, and/or sell food in Delhimust approach the relevant department in the Government of National CapitalTerritory of Delhi to obtain the appropriate licenses. If the process involvesirradiated food, permission is required from the Department of Atomic Energy. Forgenetically modified foods, permission is required from the designated authorityin the Ministry of Environment and Forest.Although a small state like Delhi has only one licensing authority, larger states mayhave several such authorities. For example, the western state of Gujarat, is dividedinto different areas, each with its separate licensing authority. Food units in areaswhere there are no licensing authorities apply to their respective local healthauthorities of the Food and Drug Control Administration, which have offices in

almost all districts.Because each licensing authority has different requirements (and this report cannotlist them all), the following is an example of the procedure for obtaining a licensein Gujarat per Rule 5 of the Gujarat Prevention of Food Adulteration Rules, 1955.The applicant must submit in full detail the following: application form;two photographs of owner or Partners or Director or nominee; block planwith three signed copies with measurements; list of food articles along withapproximate daily production, sales and stock with two signed copies;proof of ownership of place of manufacture or selling; partnership deed ormemorandum of article of the company with complete address of partnersor directors; list of machinery and details of the processing of the food; andcopies of the labels along with brands used.According to sources, approvals or licenses are granted within 30 days and evenless if the company or the brand is considered reputable. However, for companiesthat plan to sell their foods nationwide, they need to obtain a separate license ineach state where they plan to sell. Imported products are required to seek approvalfrom the Ministry of Health.Source: Gujarat Prevention of Food Adulteration Rules 1955; PFA 2005; authors.manufacturers are packaging their goods in single-use packages because thisreduces the cash outlay and may result in more frequent purchases. Forexample, there are a number of supplements sold in the form of single-serveherbal tonics, but they are priced between $0.15 and $0.25 per serving. Evenwith this approach, single-serving prices generally are still out of the reach ofthe poorer consumers for use on a daily basis (Ismail 2006).Another marketing strategy is to sell products in less-processed forms,thereby reducing the cost of the product. For example, in situations inwhich even the single serving is too expensive for low-income consumers,companies sell the supplements in powdered forms, which is not thenormal means of sale. With India’s exceptionally large population, areduced price does not necessarily mean reduced company returns; insteadit could mean significantly more volume by targeting a much larger base(Ismail 2006).Existence of unscrupulous manufacturers. Although the problem is not asdamaging as in China, there are unscrupulous manufacturers that areproducing pirated functional food products and making false claims abouttheir products. Such activities affect the reputation of the industry and can beespecially damaging to companies in the export market. Pirate products areless effective than the genuine product and can cause serious harm and mayeven lead to fatalities. Producers of supplements and Ayurvedic medicines areparticularly vulnerable. At present, GMP in the functional foods industry arevoluntary (Starling 2004).Lack of testing infrastructure to validate manufacturers’ claims. There arelimited laboratories to validate the functional or therapeutic claims of functionalfoods. Many of the current laboratories require additional investment inequipment and infrastructure to meet both the needs and the required testingstandards. According to Ms. Rekha Sinha, executive director, International Life

Sciences Institute, the World Bank has sanctioned a loan of US$44 million toUS$55 million to strengthen the food testing infrastructure needed to validateand certify the packaged foods (Sinha 2006).Lack of physical infrastructure. According to Ms. Sinha, the lack of physicalinfrastructure facilities in the food processing sector as a whole, such as coldchains and good roads that enable the timely supply of raw materials, areother bottlenecks.Lack of flexible regulatory framework for functional foods. As discussed earlier,the food industry is governed by the PFA, a 50-year-old piece of legislation.According to those interviewed, several major bottlenecks are created by thecurrent regulation: The Act has specific definitions for every food preparation permitted to besold in the country and, as such, it does not provide flexibility to the foodmanufacturers to introduce new recipes without violating the law.10 Tocomplicate matters, different laws govern GM foods, drugs, andpharmaceuticals. In all, there are about seven different laws governing thefood sector.Agricultural and Rural Development26 It is difficult for manufacturers to bring out new food preparations in atimely way. There is a process for approving recipes that are not includedin the PFA (mainly functional foods and GM foods), but the appealsprocess is cumbersome and time-consuming, and may take up to two yearsfor approval. In cases in which scientific evidence leads to a need to amendthe standards, the producers can appeal to have the PFA rules amended.Under the PFA, the Central Committee for Food Standards is responsiblefor the final decision regarding PFA rules. Because many of these recipes are classified by their creators as proprietaryfoods, manufacturers are reluctant to share data with the authorities,fearing that this data might eventually be shared with competitors. The process of launching a new food product is cumbersome because thecompany has to go through a time-consuming application process.Some resistance to GM foods. At the present time much opposition to GMfoods has come from the educated elite who fear environmental damage, lossof biodiversity, and foreign control over India’s food supply. For example,Greenpeace campaigners dismissed the “protato,” a GM potato containingapproximately 30 percent more protein, as an advertisement forbiotechnology. “Years were spent in a lab trying to lever protein into potatoes,while cheap, protein-rich pulses grow abundantly all over India,” oneopponent stated. “It makes you wonder what problem the scientists weretrying to solve” (Vidal 2003).Annex 3 documents India’s experience with Golden Rice and the HarvestPlusInitiative, providing background along with some dissenting opinions aboutwhy GM foods are counterproductive in alleviating malnutrition. Many peopleare relatively open-minded regarding GM foods, however, because science isstill seen as a route to prosperity and a better quality of life (Ghosh 2003).