SPE SPE - - ABC ABC - - October, 2009 October, 2009 Singapore Singapore Shanghai Shanghai Houston Houston New York New York London London D D ü ü sseldorf sseldorf Dubai Dubai Howard Rappaport Howard Rappaport Global Business Director Global Business Director Plastics Plastics [email protected][email protected]SPE SPE – – ABC ABC October, 2009 October, 2009 Economy > Energy > Feedstocks & Polymer Markets Economy > Energy > Feedstocks Economy > Energy > Feedstocks & Polymer Markets & Polymer Markets

Transcript

SPE SPE -- ABC ABC -- October, 2009October, 2009SingaporeSingapore ShanghaiShanghai HoustonHouston New YorkNew York LondonLondon DDüüsseldorfsseldorf DubaiDubai

Howard RappaportHoward RappaportGlobal Business Director Global Business Director

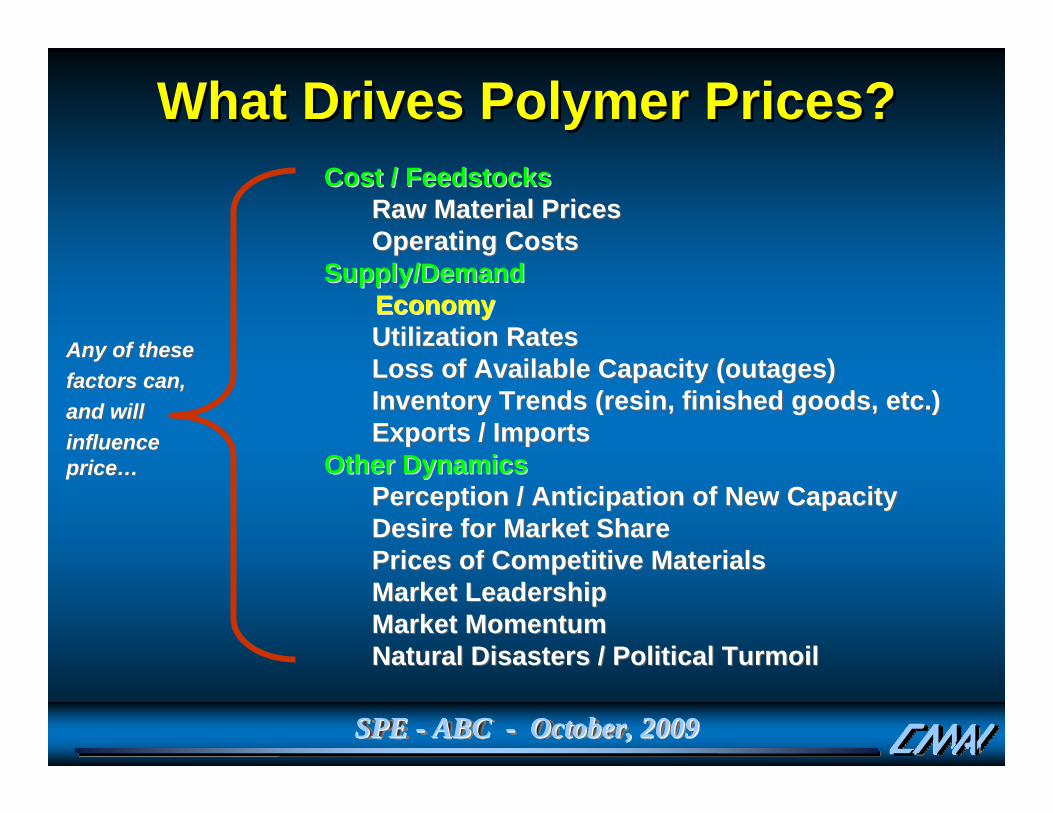

Raw Material PricesRaw Material PricesOperating CostsOperating Costs

Supply/DemandSupply/DemandEconomyEconomyUtilization RatesUtilization RatesLoss of Available Capacity (outages)Loss of Available Capacity (outages)Inventory Trends (resin, finished goods, etc.)Inventory Trends (resin, finished goods, etc.)Exports / Imports Exports / Imports

Other DynamicsOther DynamicsPerception / Anticipation of New CapacityPerception / Anticipation of New CapacityDesire for Market ShareDesire for Market SharePrices of Competitive MaterialsPrices of Competitive MaterialsMarket Leadership Market Leadership Market Momentum Market Momentum Natural Disasters / Political TurmoilNatural Disasters / Political Turmoil

Any of theseAny of thesefactors can,factors can,and willand willinfluence influence priceprice……

SPE SPE -- ABC ABC -- October, 2009October, 2009

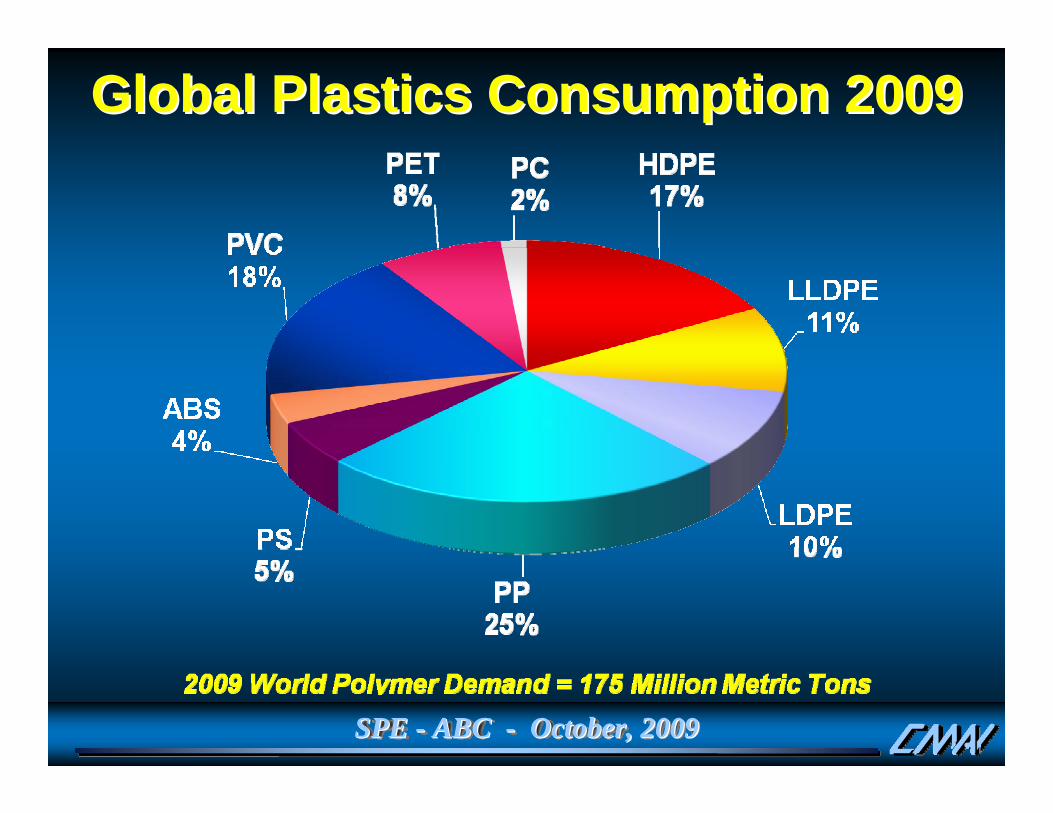

Global Plastics Consumption 2009Global Plastics Consumption 2009

SPE SPE -- ABC ABC -- October, 2009October, 2009

Wood

Aluminum

PET

Glass

PVC

Steel

PS

LL/LDPE

Paper

ABS

HDPE

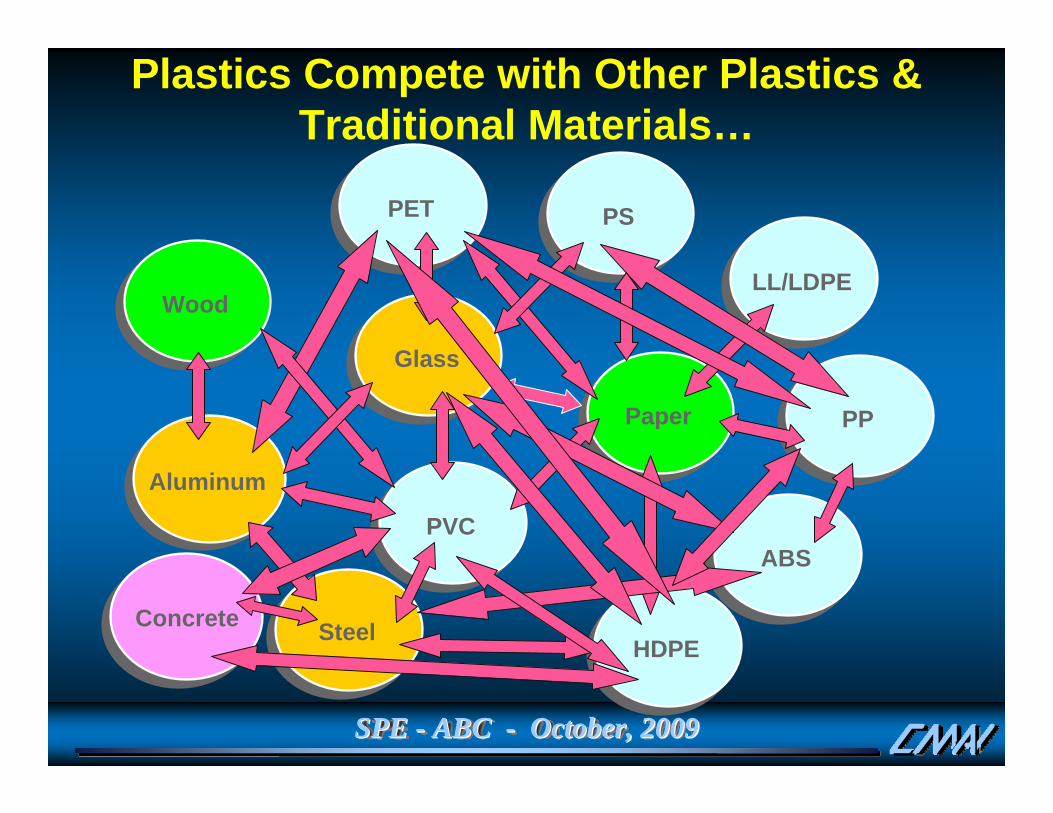

Plastics Compete with Other Plastics & Traditional Materials…

PP

Concrete

SPE SPE -- ABC ABC -- October, 2009October, 2009

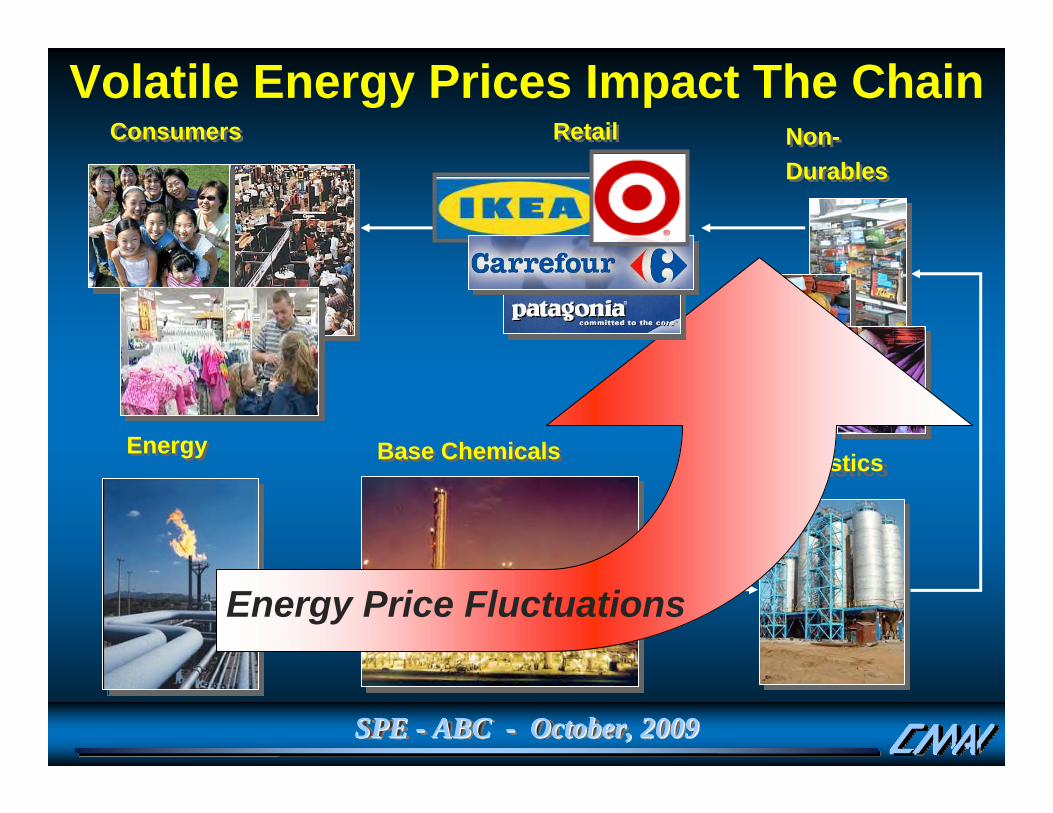

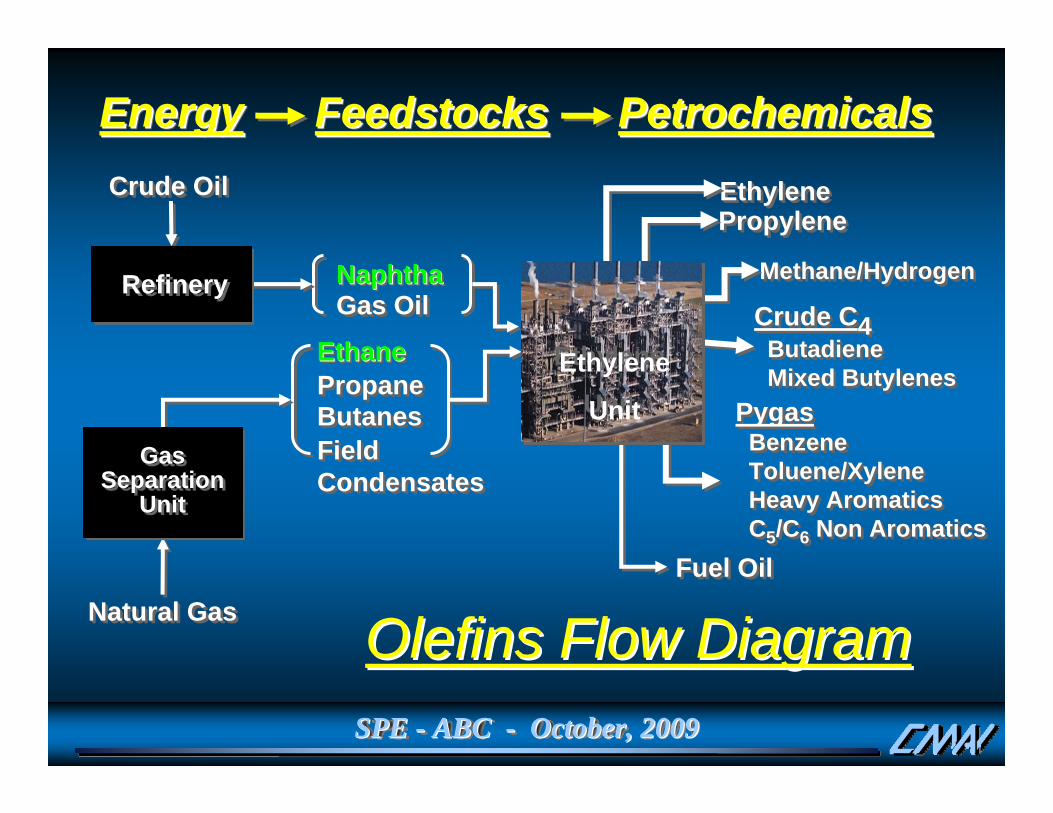

EnergyEnergy Base ChemicalsBase ChemicalsPlasticsPlastics

Volatile Energy Prices Impact The ChainNon-DurablesNon-Durables

ConsumersConsumers RetailRetail

Energy Price Fluctuations

SPE SPE -- ABC ABC -- October, 2009October, 2009

ECONOMYECONOMY& ENERGY& ENERGY

SPE SPE -- ABC ABC -- October, 2009October, 2009

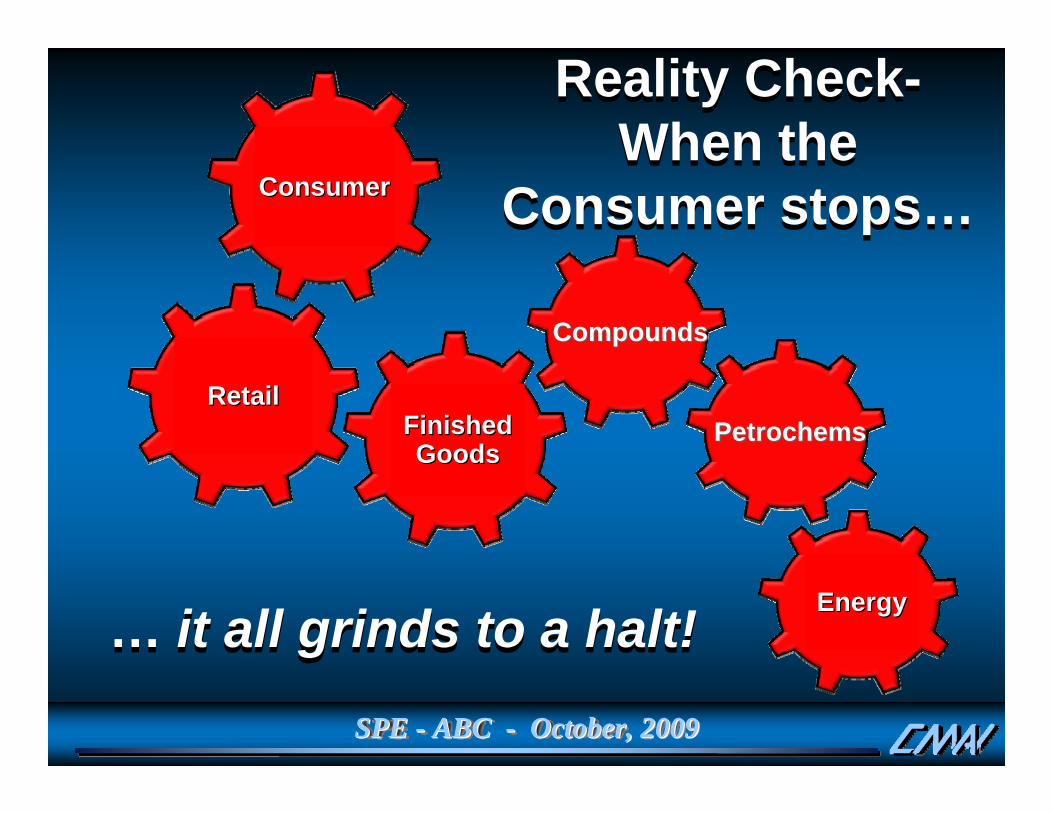

Reality Check-When the

Consumer stops…

Reality Check-When the

Consumer stops…

… it all grinds to a halt!… it all grinds to a halt!

ConsumerConsumer

Retail Retail Finished Finished GoodsGoods

CompoundsCompounds

PetrochemsPetrochems

EnergyEnergy

SPE SPE -- ABC ABC -- October, 2009October, 2009

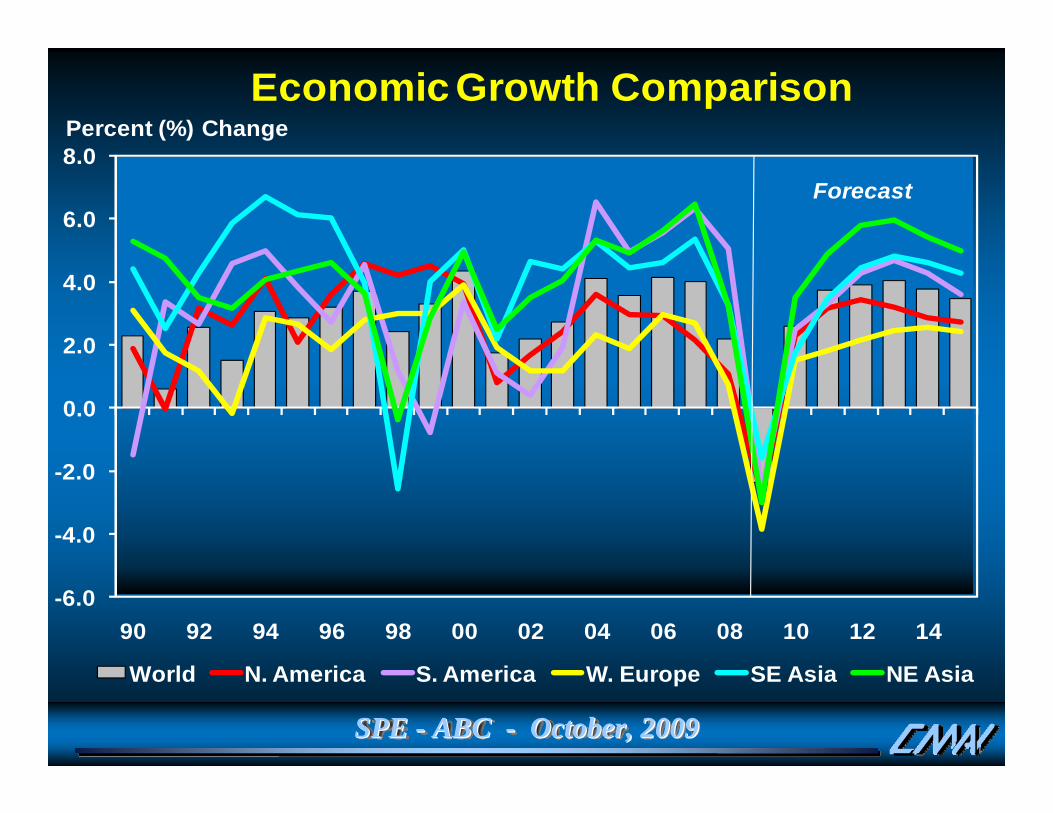

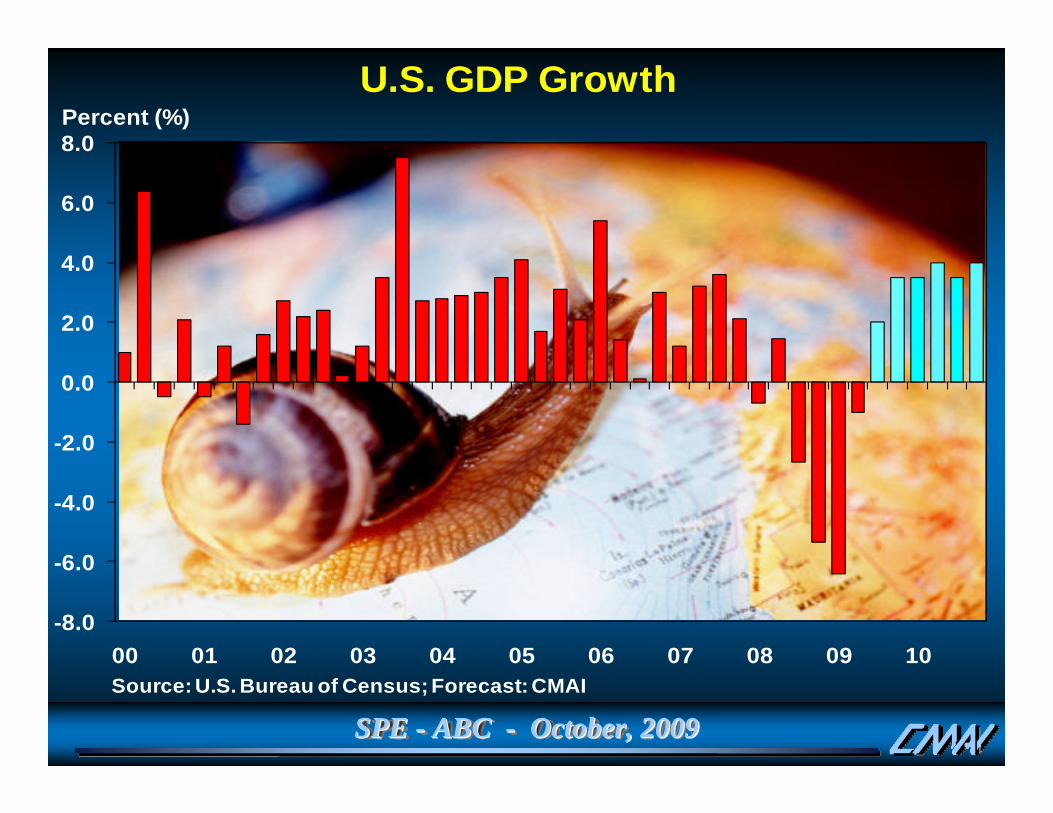

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

8.0

90 92 94 96 98 00 02 04 06 08 10 12 14

Economic Growth Comparison

World N. America S. America W. Europe SE Asia NE Asia

Forecast

Percent (%) Change

SPE SPE -- ABC ABC -- October, 2009October, 2009

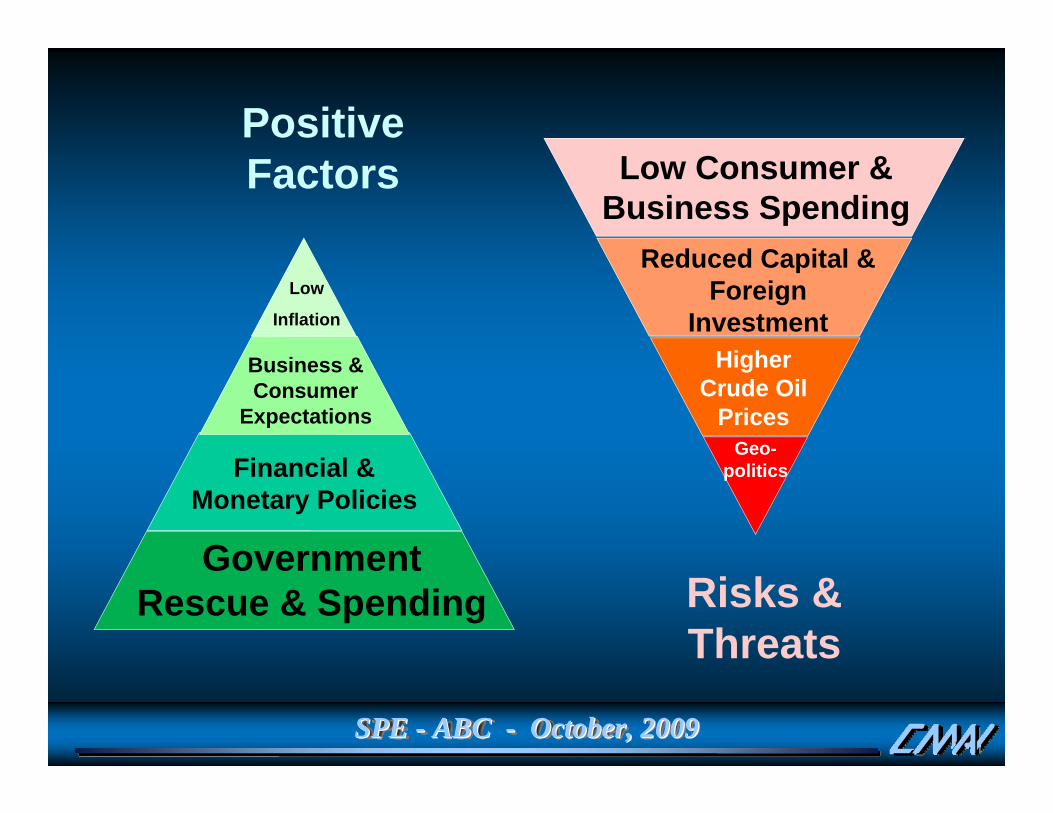

Positive Factors

Risks & Threats

Higher Crude Oil

Prices

Low Consumer & Business Spending

Geo-politics

Reduced Capital & Foreign

Investment

Government Rescue & Spending

Financial & Monetary Policies

Business & Consumer

Expectations

Low

Inflation

SPE SPE -- ABC ABC -- October, 2009October, 2009

-40.0

-30.0

-20.0

-10.0

0.0

10.0

20.0

08 Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 09 Feb Mar Apr May Jun Jul

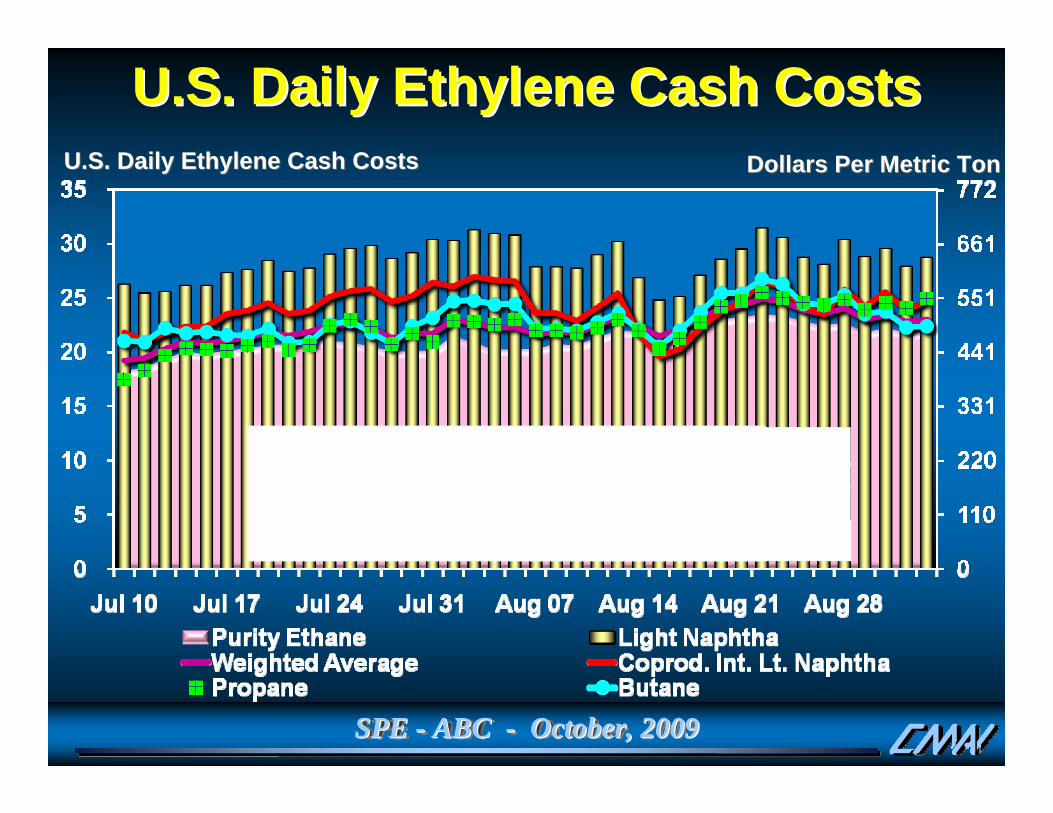

U.S. Daily Ethylene Cash CostsU.S. Daily Ethylene Cash Costs Dollars Per Metric TonDollars Per Metric Ton

U.S. Daily Ethylene Cash CostsU.S. Daily Ethylene Cash Costs

SPE SPE -- ABC ABC -- October, 2009October, 2009

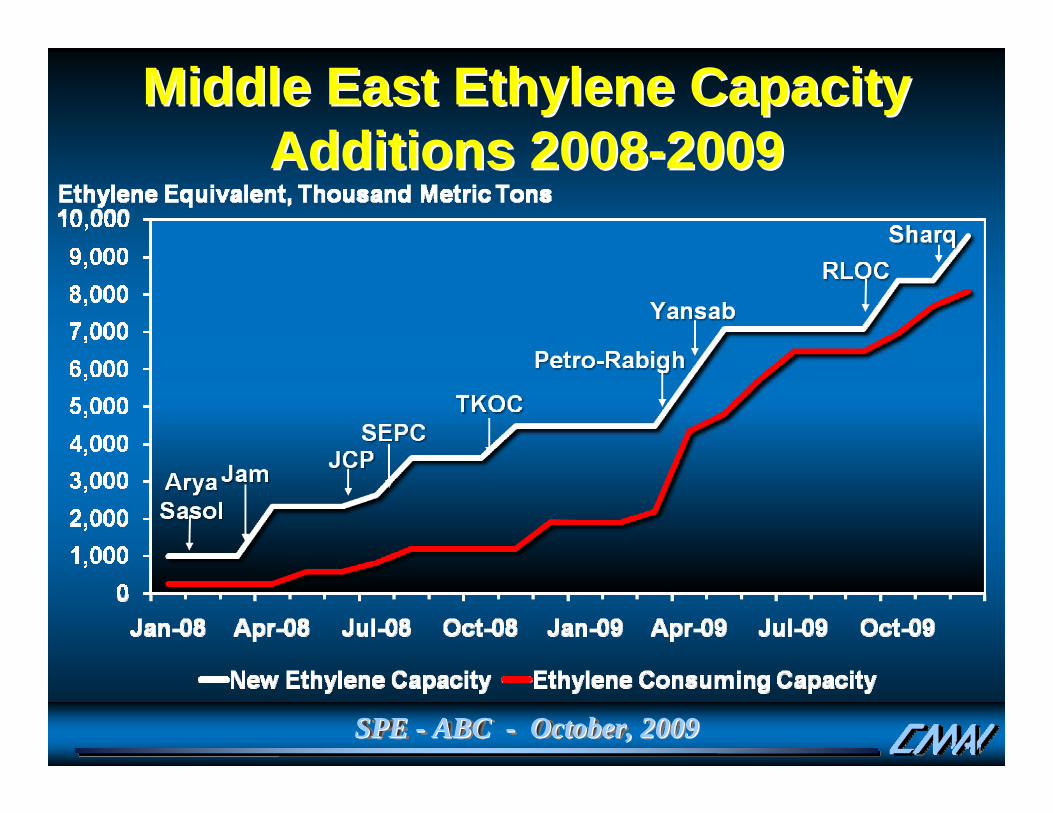

Middle East Ethylene Capacity Middle East Ethylene Capacity Additions 2008Additions 2008--20092009

SPE SPE -- ABC ABC -- October, 2009October, 2009

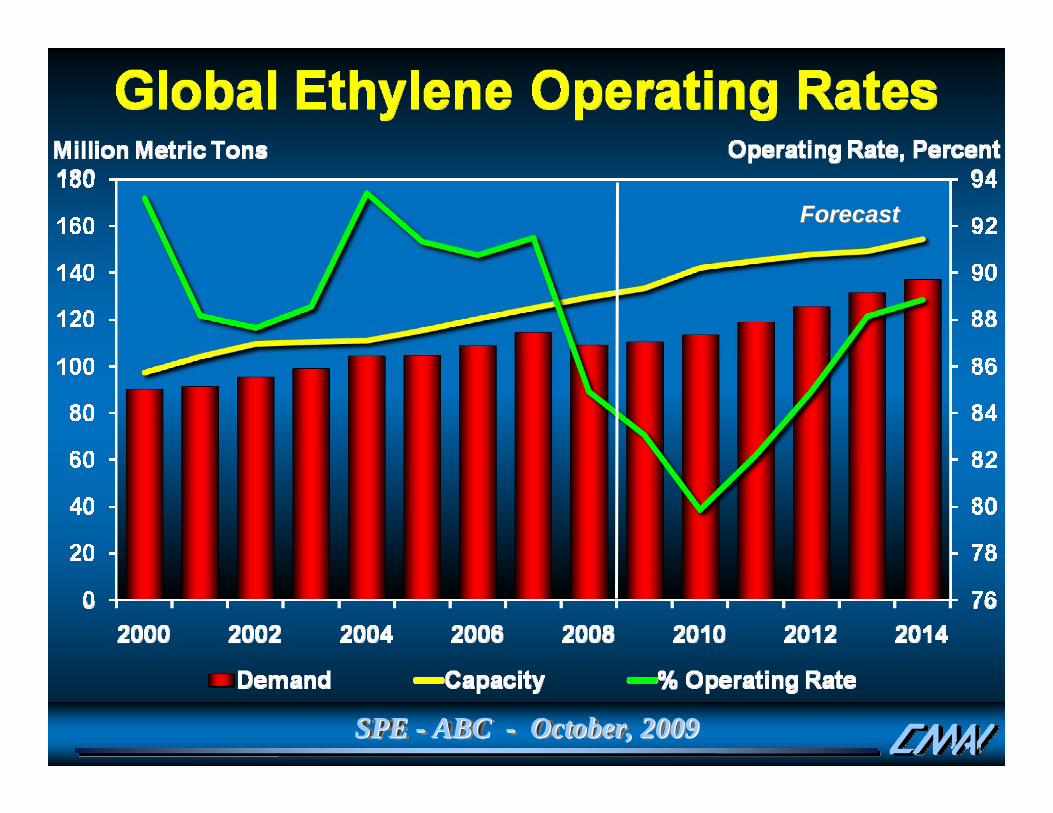

ForecastForecast

SPE SPE -- ABC ABC -- October, 2009October, 2009

U.S. Ethylene ConclusionsU.S. Ethylene ConclusionsOversupply and weak demand result in a long marketOlefins markets clearly in the trough, margins squeezedHeavy feed crackers challenged by crude oil prices vs. natural gasNorth America ethylene derivative exports supported by favorable crude-to-gas ratioSignificant capacity reductions are inevitable

Oversupply and weak demand Oversupply and weak demand result in a long marketresult in a long marketOlefins markets clearly in the Olefins markets clearly in the trough, margins squeezedtrough, margins squeezedHeavy feed crackers challenged Heavy feed crackers challenged by crude oil prices vs. natural by crude oil prices vs. natural gasgasNorth America ethylene North America ethylene derivative exports supported by derivative exports supported by favorable crudefavorable crude--toto--gas ratiogas ratioSignificant capacity reductions Significant capacity reductions are inevitableare inevitable

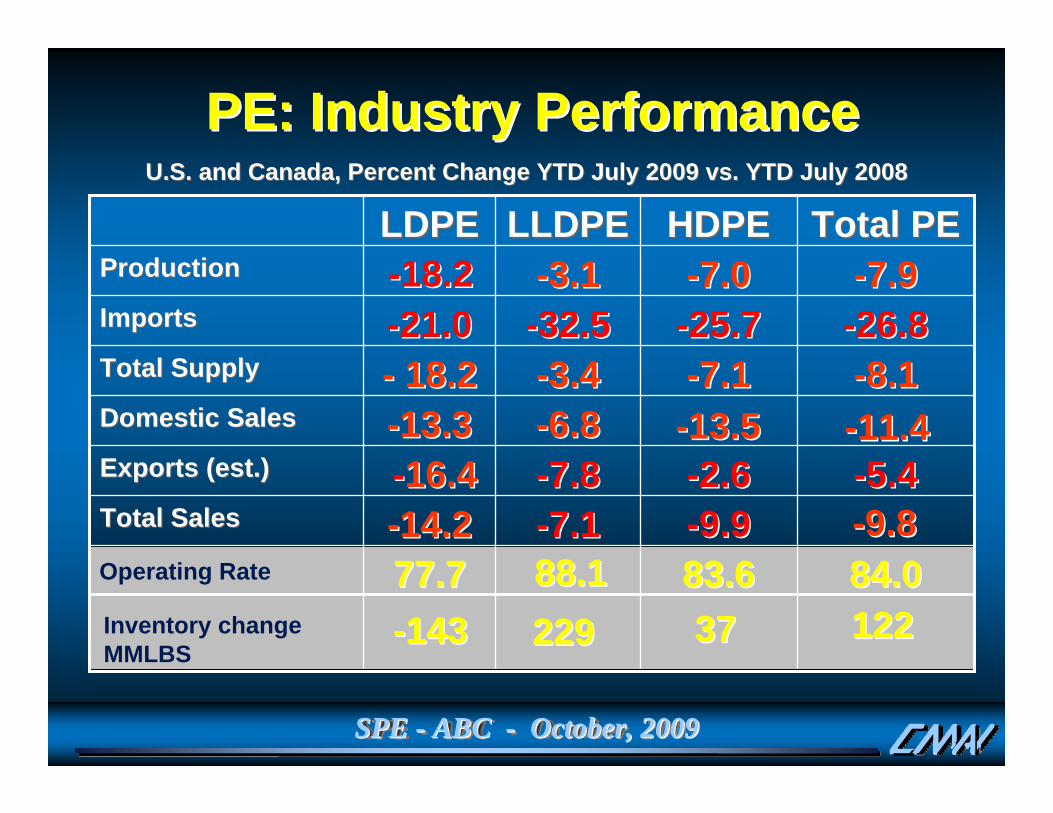

Total PETotal PEHDPEHDPELLDPELLDPELDPELDPEU.S. and Canada, Percent Change YTD July 2009 vs. YTD July 2008U.S. and Canada, Percent Change YTD July 2009 vs. YTD July 2008

--13.513.5 --11.411.4

--9.89.8

PE: Industry PerformancePE: Industry Performance

SPE SPE -- ABC ABC -- October, 2009October, 2009

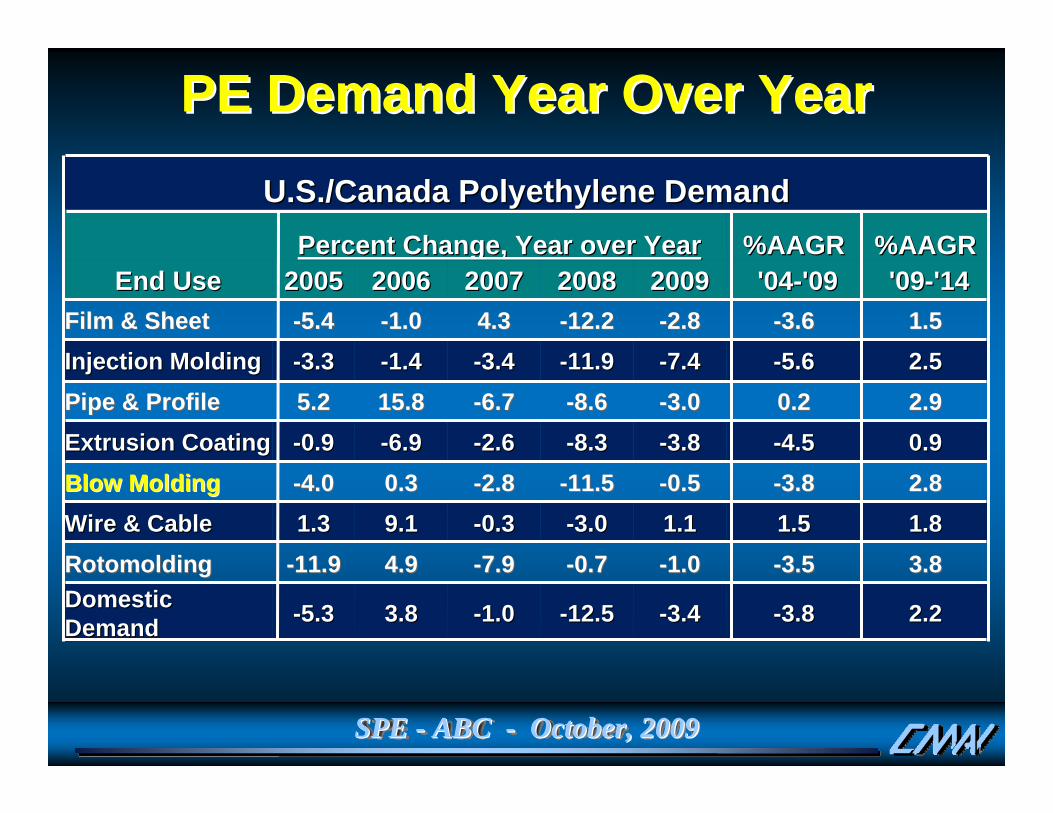

PE Demand Year Over YearPE Demand Year Over YearU.S./Canada Polyethylene DemandU.S./Canada Polyethylene Demand

Percent Change, Year over YearPercent Change, Year over Year %AAGR %AAGR %AAGR%AAGREnd UseEnd Use 20052005 20062006 20072007 20082008 20092009 '04'04--'09'09 '09'09--'14'14

Top Global PE Top Global PE Producers 2013Producers 2013

8,913

8,407

6,748

5,735

5,210

8.47

7.99

6.41

5.45

4.95

TotalTotal 35,01335,013 33.2633.26

Global Producer Market ShareGlobal Producer Market Share

CompanyCapacity

(-000- MT)% Capacity

Dow Chemical

ExxonMobil

LyondellBasell

SABIC

Chevron Phillips

Top Global PE Top Global PE Producers 2008Producers 2008

7,932

7,165

5,313

4,200

3,253

9.91

8.95

6.64

5.25

4.06

TotalTotal 27,86227,862 34.8134.81

Share

SPE SPE -- ABC ABC -- October, 2009October, 2009

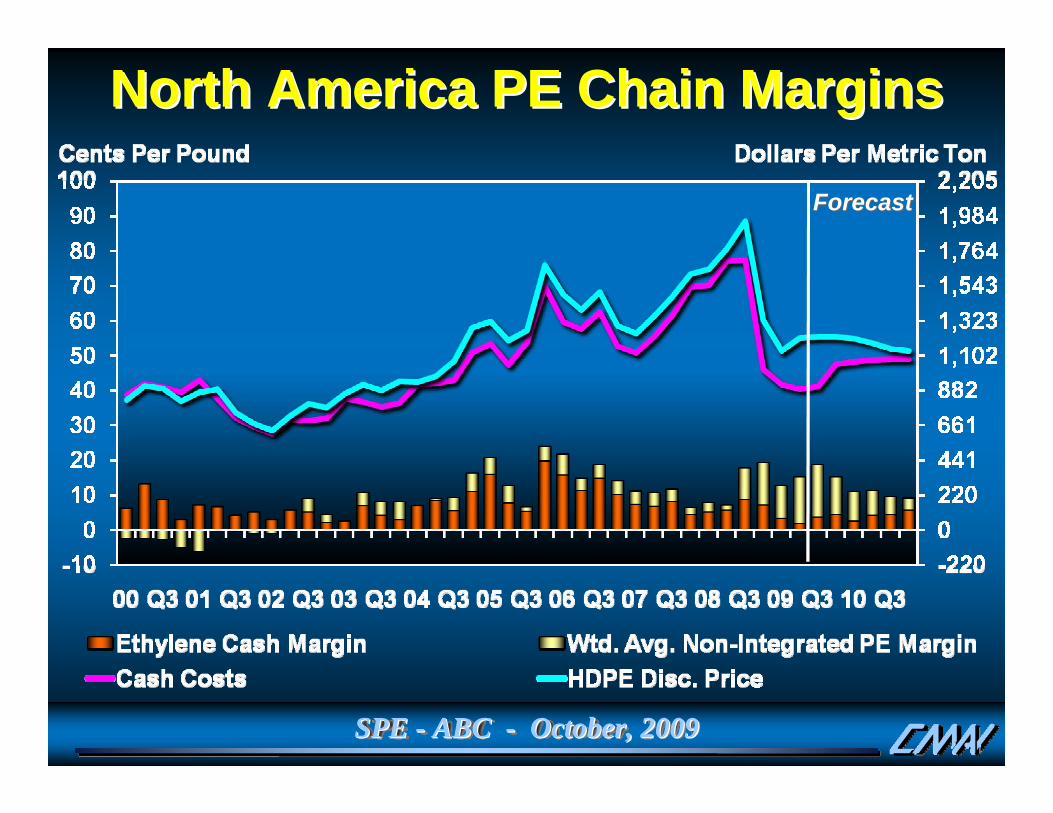

North America PE Chain MarginsNorth America PE Chain Margins

ForecastForecast

SPE SPE -- ABC ABC -- October, 2009October, 2009

PE TakePE Take--AwaysAways•• PE prices less volatile through 2010 than in PE prices less volatile through 2010 than in

recent past.recent past.•• YTD margins stronger than expected due to YTD margins stronger than expected due to

robust exports, capacity shutdowns / turndowns robust exports, capacity shutdowns / turndowns and unusual producer market / production and unusual producer market / production disciplinediscipline

•• NAM PE cost advantage strong vs other regions NAM PE cost advantage strong vs other regions ex. MDEex. MDE

•• Despite delays and shutdowns, unprecedented Despite delays and shutdowns, unprecedented oversupply conditions will drive down operating oversupply conditions will drive down operating rates and margins beginning 4Q 09.rates and margins beginning 4Q 09.

•• The cycle trough is expected from 4Q 09 The cycle trough is expected from 4Q 09 -- 2010, 2010, global recovery evident by 2011global recovery evident by 2011

Propylene & PP Propylene & PP –– Key Points Key Points •• Propylene industry in transition; moving from byPropylene industry in transition; moving from by--product to product to ““own own

productproduct””•• Propylene & PP no longer cheap; must compete based on Propylene & PP no longer cheap; must compete based on

features rather than pricesfeatures rather than prices•• Oversupply expected in the next few years; same issues to be Oversupply expected in the next few years; same issues to be

faced as in the ethylene/PE industryfaced as in the ethylene/PE industry•• However, no region enjoys a marked cost advantage versus However, no region enjoys a marked cost advantage versus

others. Trade to become very competitiveothers. Trade to become very competitive•• Asian imports saved the first half of the year for producers; asAsian imports saved the first half of the year for producers; as

new projects start up in second half of the year, market to movenew projects start up in second half of the year, market to moveto oversupplyto oversupply

•• Prices to be sustained by higher energyPrices to be sustained by higher energy

SPE SPE -- ABC ABC -- October, 2009October, 2009

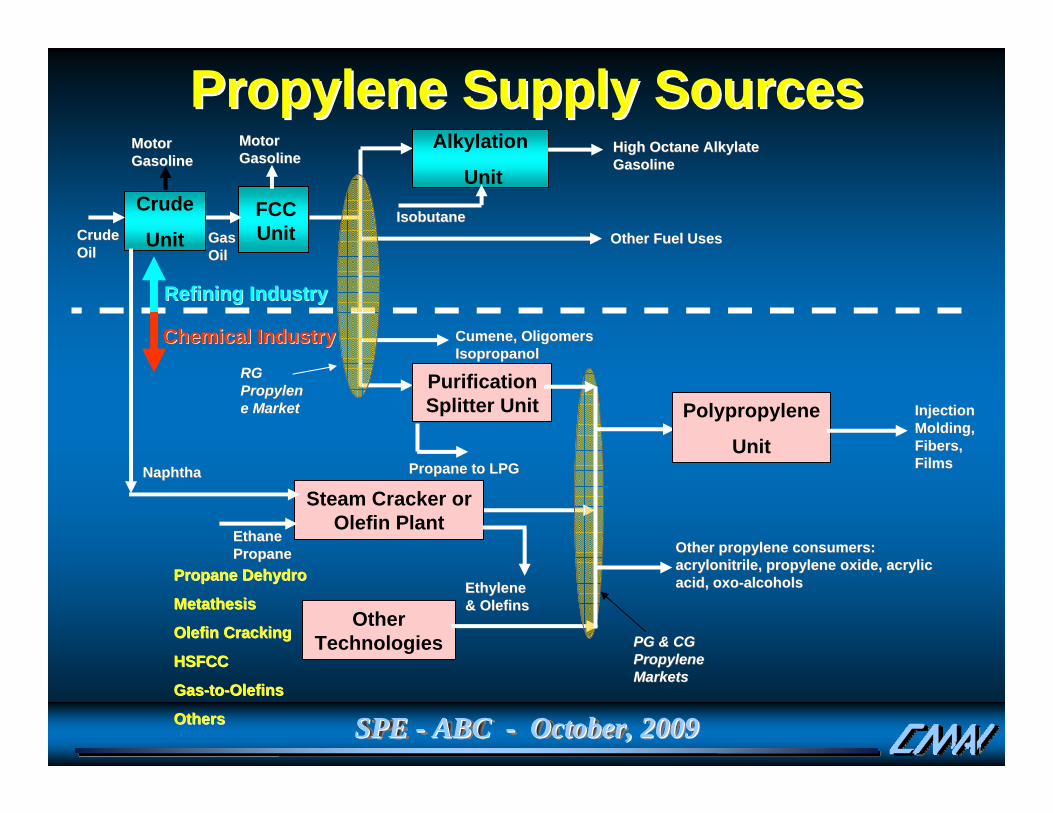

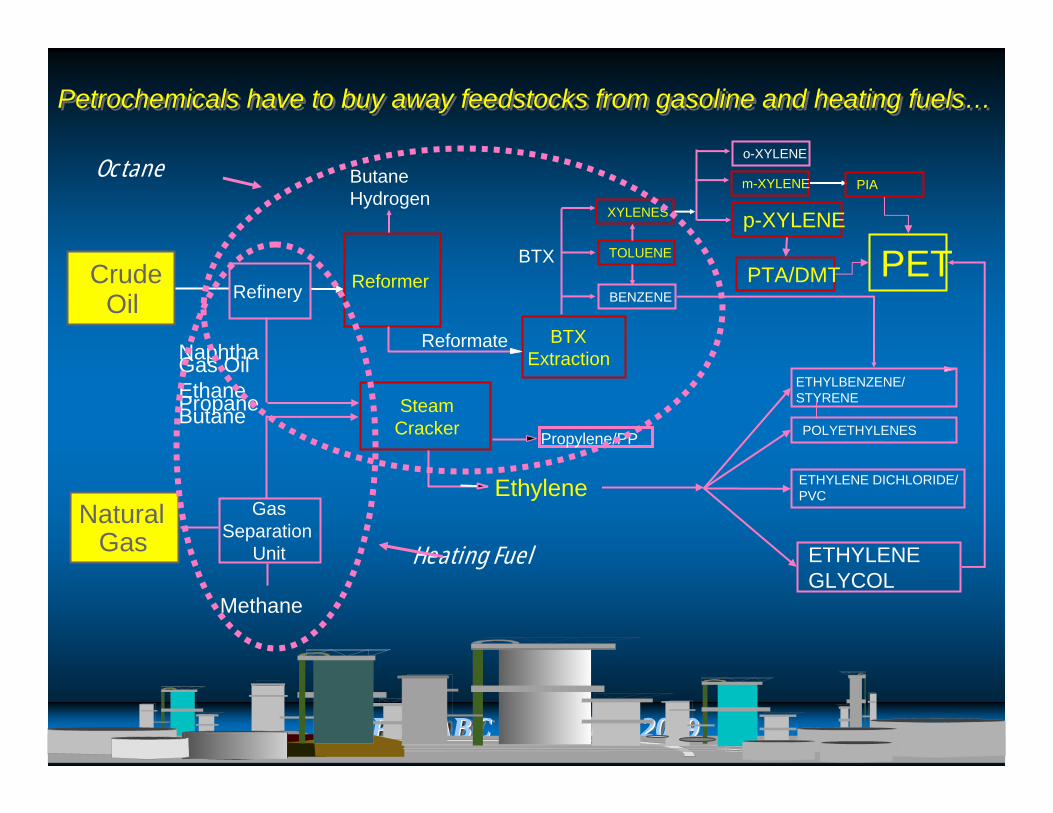

Propylene Supply SourcesPropylene Supply Sources

Other Technologies

Steam Cracker or Olefin Plant

Ethane Ethane PropanePropane Other propylene consumers: Other propylene consumers: