22

SHALE-ADVANTAGED CHEMICAL INDUSTRY INVESTMENT 9 April 2013 Martha Gilchrist Moore Sr. Director, Policy Analysis and Economics

SHALE-ADVANTAGED CHEMICAL INDUSTRY INVESTMENT

9 April 2013

Martha Gilchrist Moore

Sr. Director, Policy Analysis and Economics

Shale Gas

• Shale gas is possibly the most important

energy development in the past 50

years.

• Shale gas now accounts for 30% of

production.

• Abundant supplies of natural gas liquids

are changing the economics of global

petrochemical production patterns.

• Lower natural gas costs are improving

the competitiveness of not only chemical

producers, but other gas-intensive

manufacturers

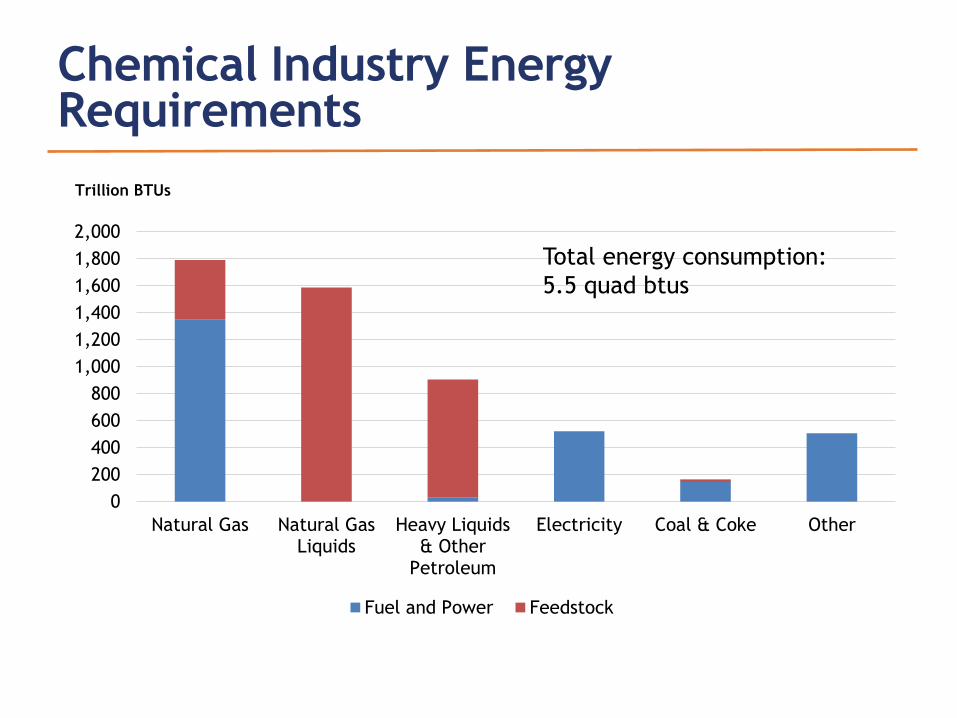

Chemical Industry Energy Requirements

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Natural Gas Natural GasLiquids

Heavy Liquids& Other

Petroleum

Electricity Coal & Coke Other

Fuel and Power Feedstock

Trillion BTUs

Total energy consumption:

5.5 quad btus

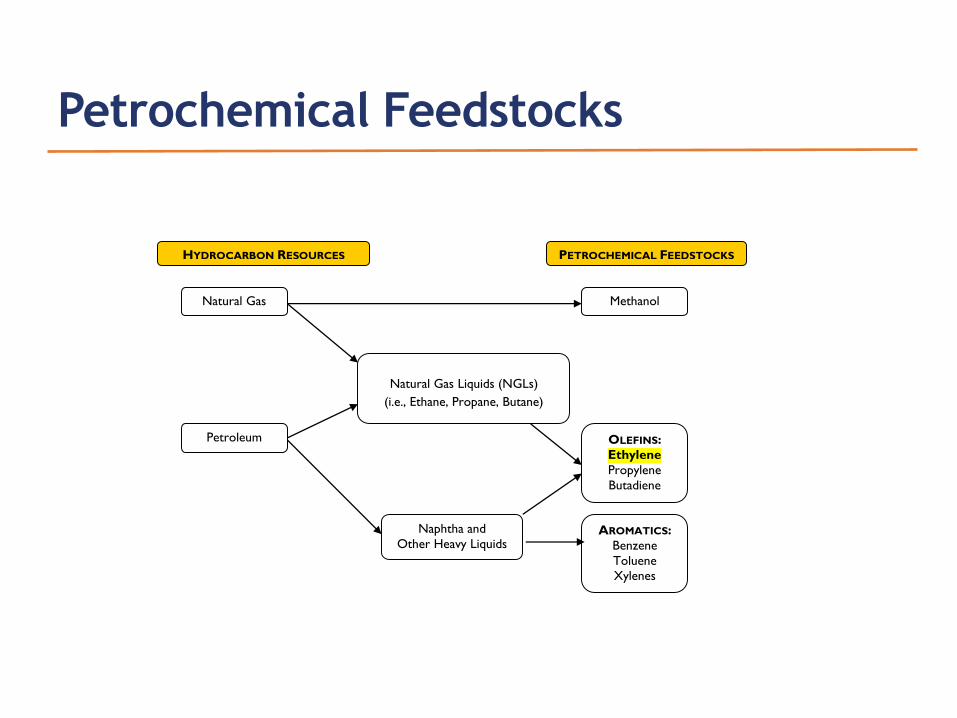

Petrochemical Feedstocks

HYDROCARBON RESOURCES PETROCHEMICAL FEEDSTOCKS

Natural Gas Methanol

Petroleum

Natural Gas Liquids (NGLs)

(i.e., Ethane, Propane, Butane)

OLEFINS:

Ethylene

Propylene

Butadiene

Naphtha and

Other Heavy Liquids AROMATICS:

Benzene

Toluene

Xylenes

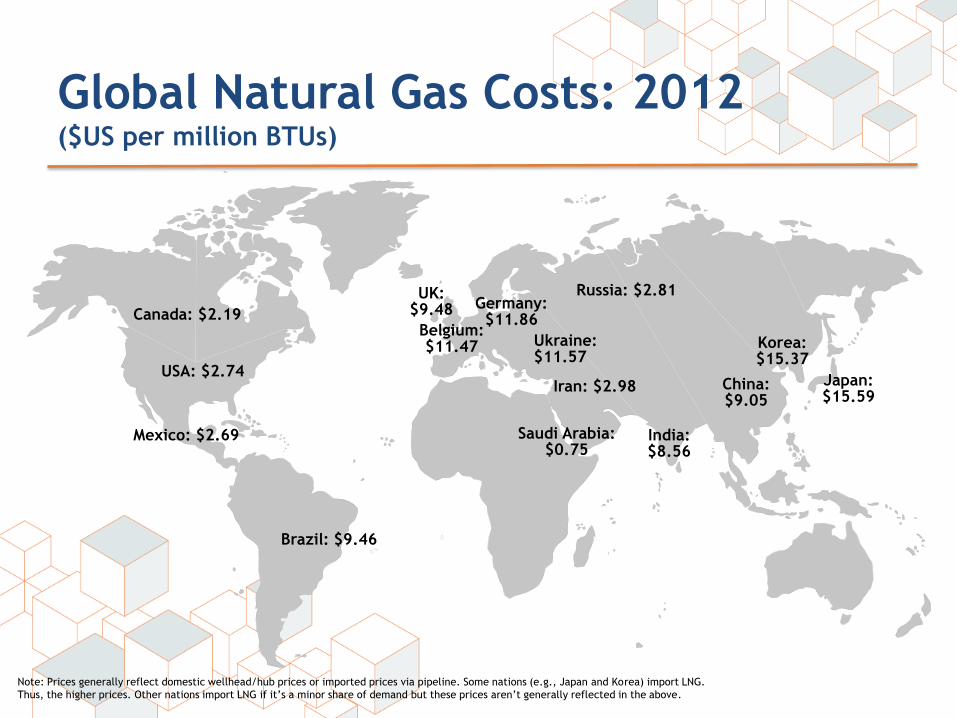

Global Natural Gas Costs: 2012 ($US per million BTUs)

Note: Prices generally reflect domestic wellhead/hub prices or imported prices via pipeline. Some nations (e.g., Japan and Korea) import LNG.

Thus, the higher prices. Other nations import LNG if it’s a minor share of demand but these prices aren’t generally reflected in the above.

USA: $2.74

Mexico: $2.69

Canada: $2.19

Saudi Arabia: $0.75

Iran: $2.98

Brazil: $9.46

Germany: $11.86

China: $9.05

India: $8.56

Korea: $15.37

Japan: $15.59

UK: $9.48

Belgium: $11.47

Russia: $2.81

Ukraine: $11.57

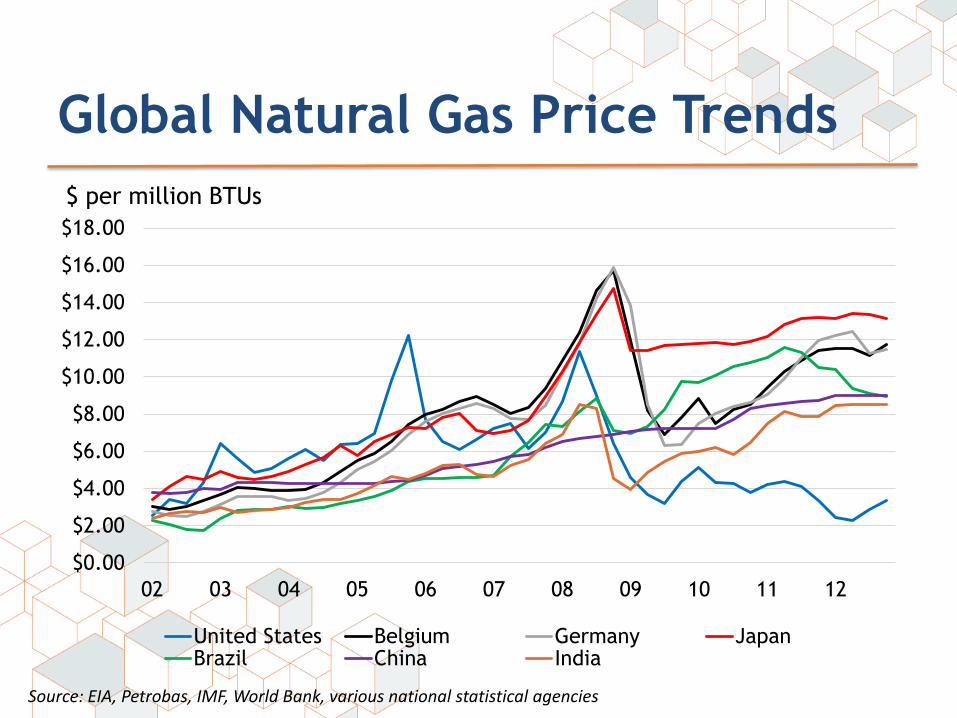

Global Natural Gas Price Trends

$0.00

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$16.00

$18.00

02 03 04 05 06 07 08 09 10 11 12

United States Belgium Germany JapanBrazil China India

Source: EIA, Petrobas, IMF, World Bank, various national statistical agencies

$ per million BTUs

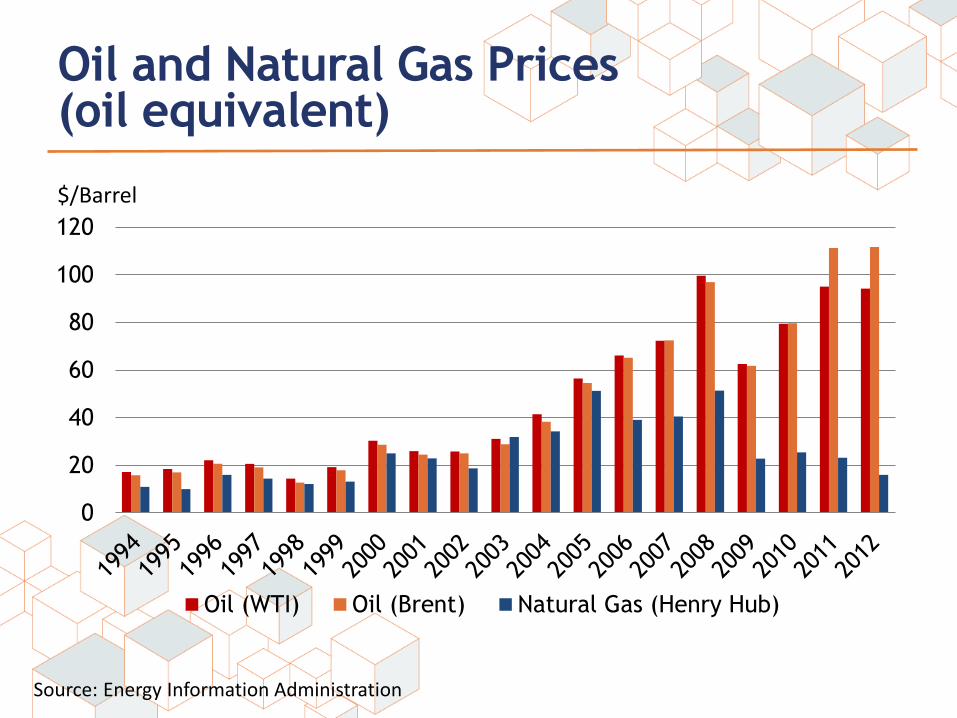

Oil and Natural Gas Prices (oil equivalent)

0

20

40

60

80

100

120

Oil (WTI) Oil (Brent) Natural Gas (Henry Hub)

$/Barrel

Source: Energy Information Administration

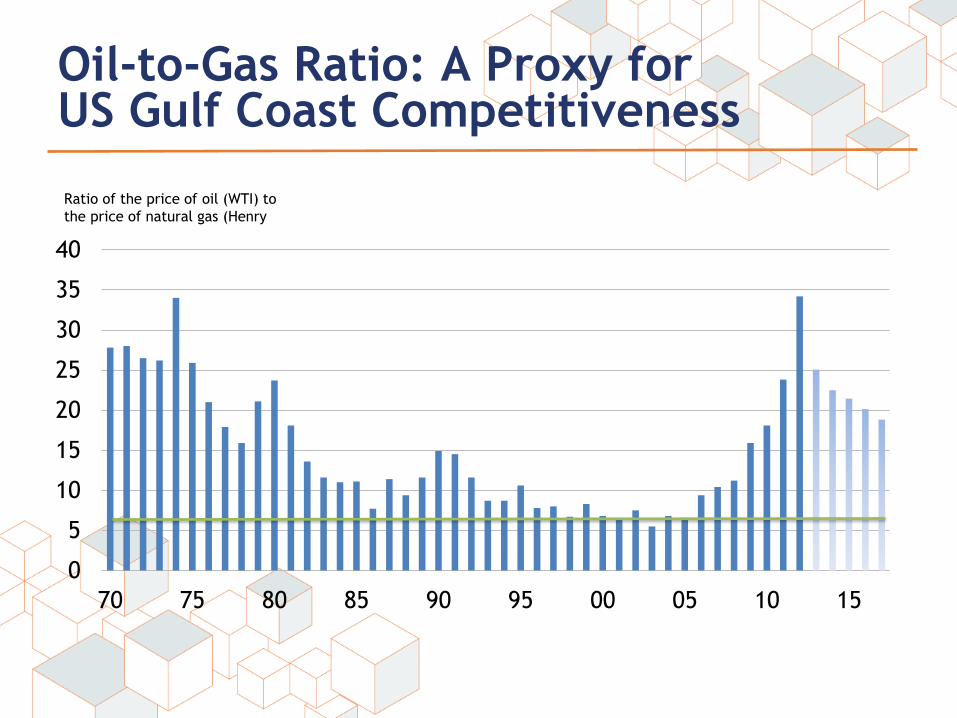

Oil-to-Gas Ratio: A Proxy for US Gulf Coast Competitiveness

0

5

10

15

20

25

30

35

40

70 75 80 85 90 95 00 05 10 15

Ratio of the price of oil (WTI) to

the price of natural gas (Henry

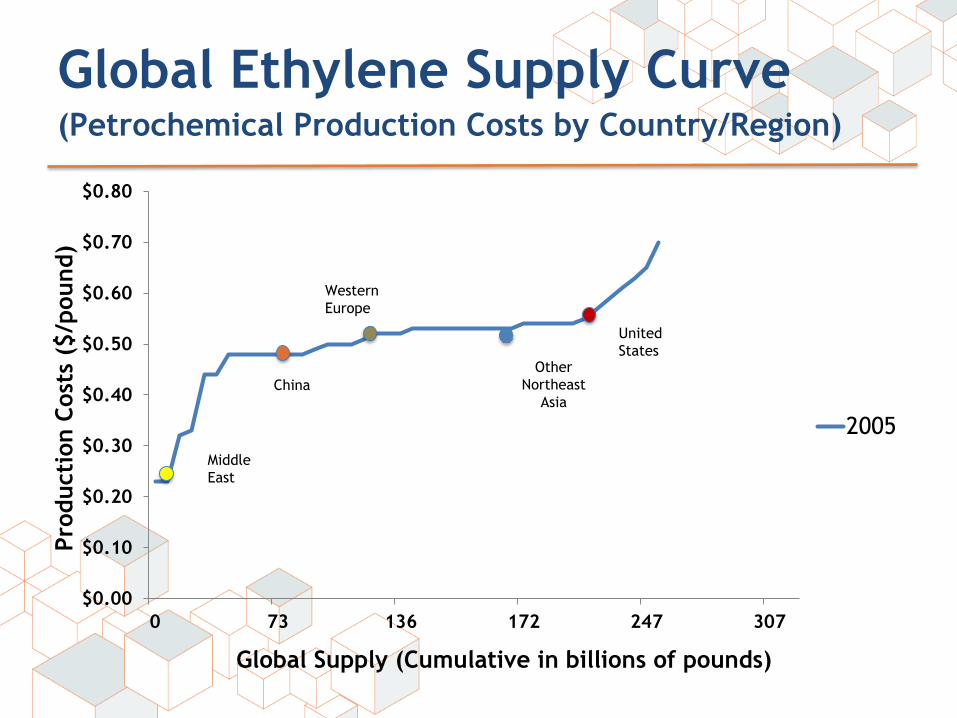

Global Ethylene Supply Curve (Petrochemical Production Costs by Country/Region)

$0.00

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

0 73 136 172 247 307

Pro

ducti

on C

ost

s ($

/pound)

Global Supply (Cumulative in billions of pounds)

2005

Middle

East

United

States

China

Other

Northeast

Asia

Western

Europe

Global Ethylene Supply Curve (Petrochemical Production Costs by Country/Region)

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

0 73 136 172 247 307

Pro

ducti

on C

ost

s ($

/pound)

Global Supply (Cumulative in billions of pounds)

2005

2012Middle

East

Middle East

United

States

United

States

China

Western Europe China

Western

Europe

Other Northeast Asia

Other

Northeast

Asia

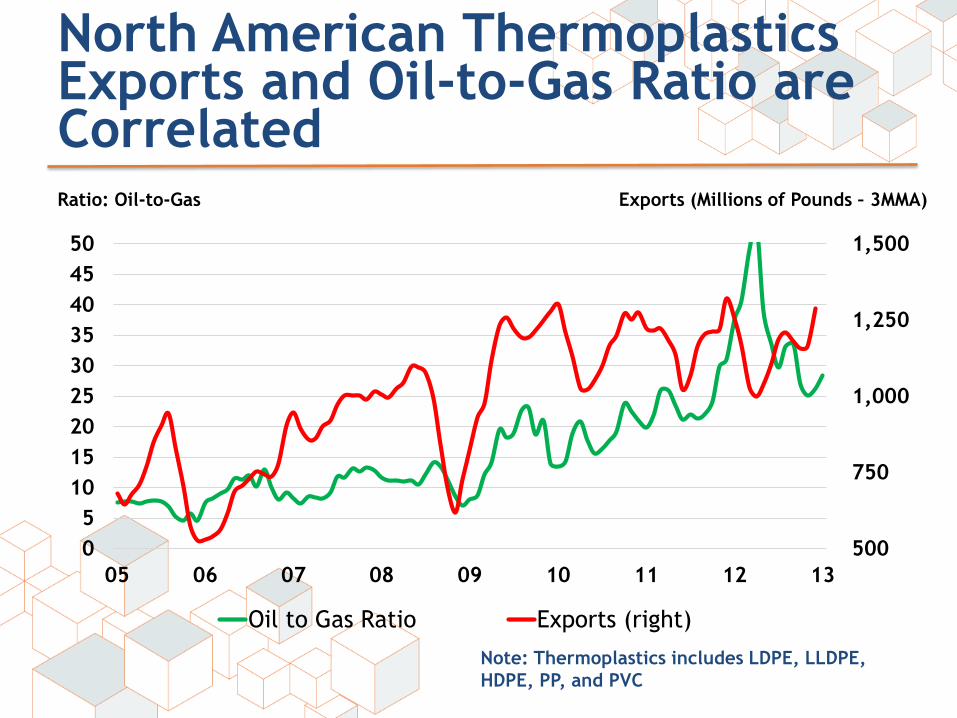

North American Thermoplastics Exports and Oil-to-Gas Ratio are Correlated

500

750

1,000

1,250

1,500

0

5

10

15

20

25

30

35

40

45

50

05 06 07 08 09 10 11 12 13

Oil to Gas Ratio Exports (right)

Ratio: Oil-to-Gas Exports (Millions of Pounds – 3MMA)

Note: Thermoplastics includes LDPE, LLDPE,

HDPE, PP, and PVC

0

5

10

15

20

25

30

35

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 21 22

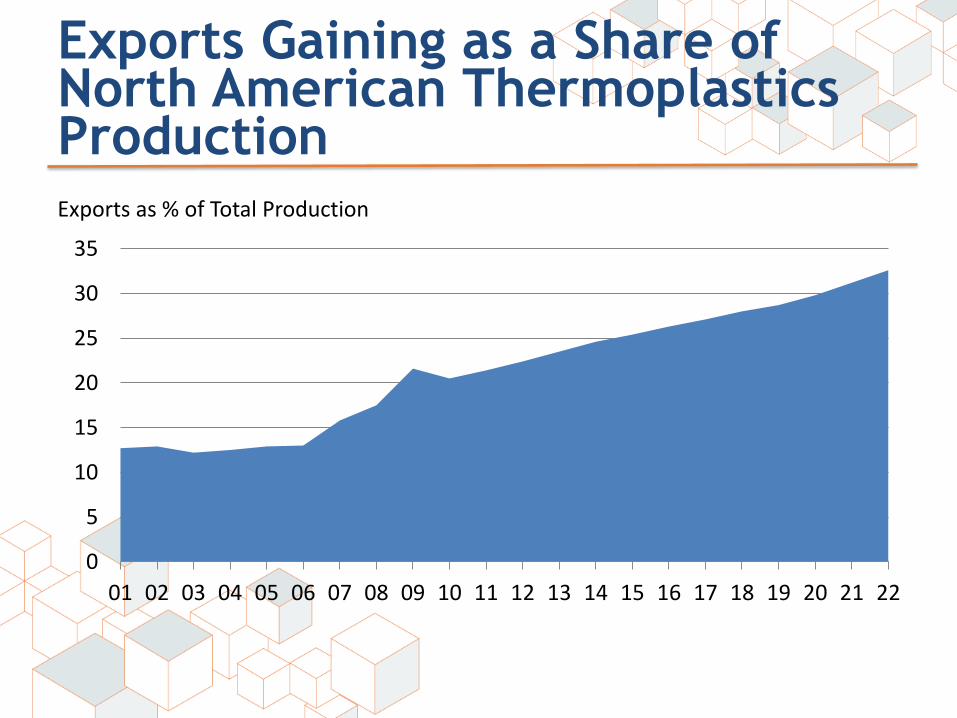

Exports Gaining as a Share of North American Thermoplastics Production Exports as % of Total Production

Petrochemical Competitiveness

Then…

USGC petrochemicals

competitively

disadvantaged

Near top of global cost

curve

Major capacity build in the

Middle East with stranded

ethane from that region

Now…

By 2011, USGC cost

position had improved that

region follows Middle East

Ethane supplies tightening

in Middle East; era of low-

cost feedstocks may be

over - some producing

nations may ride up the

cost curve

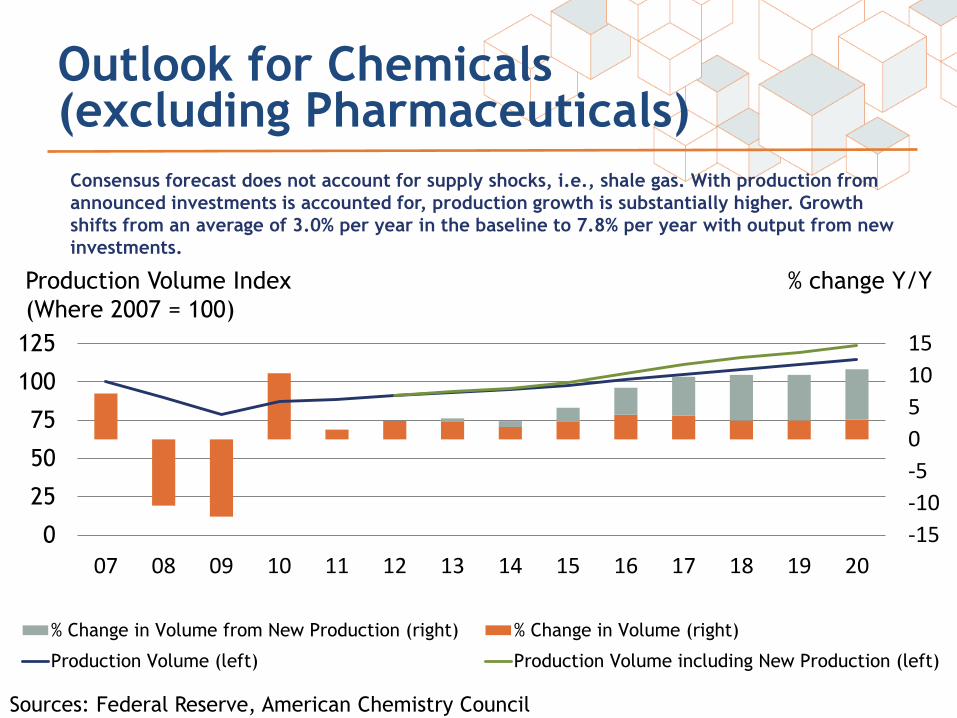

Outlook for Chemicals (excluding Pharmaceuticals)

-15

-10

-5

0

5

10

15

0

25

50

75

100

125

07 08 09 10 11 12 13 14 15 16 17 18 19 20

% Change in Volume from New Production (right) % Change in Volume (right)

Production Volume (left) Production Volume including New Production (left)

Production Volume Index

(Where 2007 = 100)

% change Y/Y

Consensus forecast does not account for supply shocks, i.e., shale gas. With production from

announced investments is accounted for, production growth is substantially higher. Growth

shifts from an average of 3.0% per year in the baseline to 7.8% per year with output from new

investments.

Sources: Federal Reserve, American Chemistry Council

16

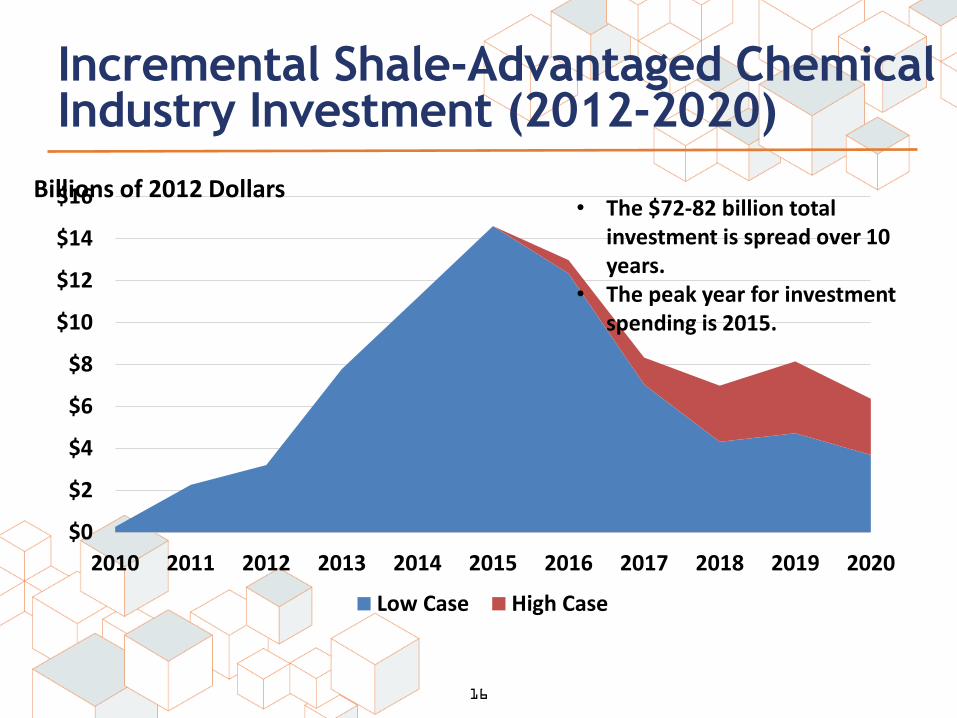

Incremental Shale-Advantaged Chemical Industry Investment (2012-2020)

$0

$2

$4

$6

$8

$10

$12

$14

$16

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Low Case High Case

Billions of 2012 Dollars • The $72-82 billion total

investment is spread over 10 years.

• The peak year for investment spending is 2015.

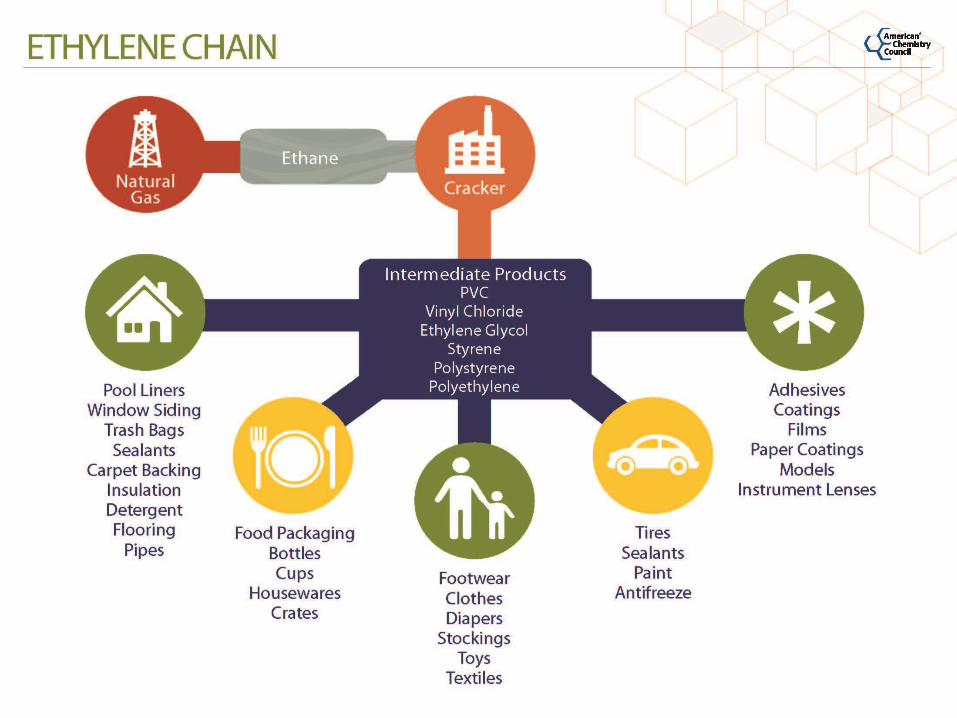

Shale Advantage Driving Capacity Expansion Across Many Products

Ethylene – capacity expected to grow by half

Ethlyene cracker co-products - propylene, butadiene

Derivatives – PE, vinyls, MEG, alpha-olefins, etc.

Co-products – chlor-alkali

Methanol

Nitrogeneous fertilizers – ammonia, urea and derivatives (AN, UAN)

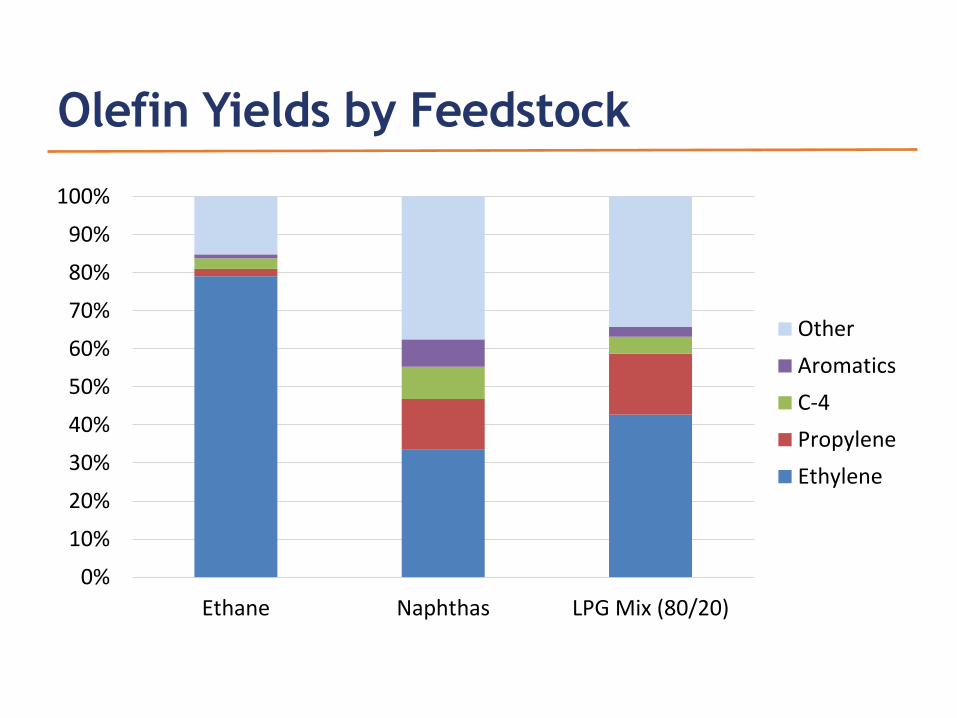

Olefin Yields by Feedstock

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Ethane Naphthas LPG Mix (80/20)

Other

Aromatics

C-4

Propylene

Ethylene

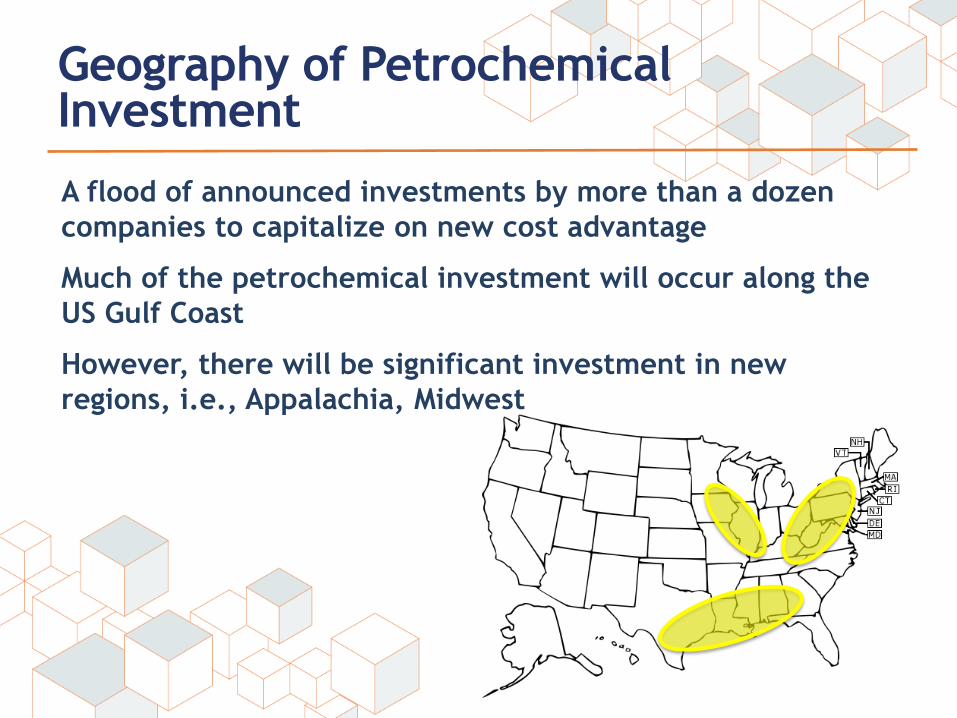

Geography of Petrochemical Investment

A flood of announced investments by more than a dozen

companies to capitalize on new cost advantage

Much of the petrochemical investment will occur along the

US Gulf Coast

However, there will be significant investment in new

regions, i.e., Appalachia, Midwest

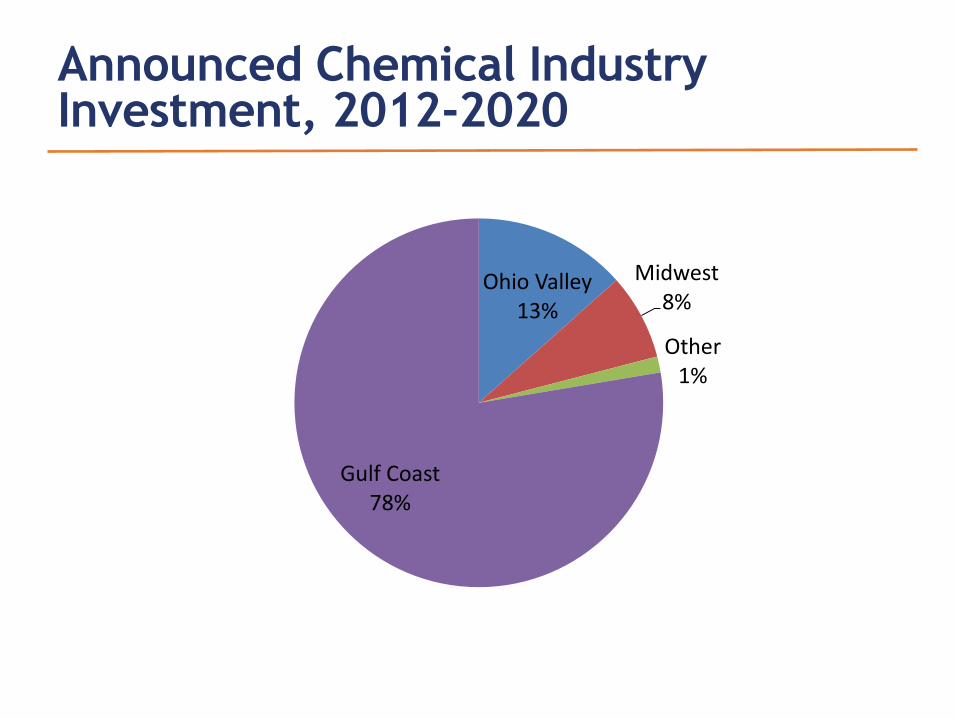

Announced Chemical Industry Investment, 2012-2020

Ohio Valley 13%

Midwest 8%

Other 1%

Gulf Coast 78%

Concluding Remarks

• Shale gas changes everything. Renewed US competitiveness from shale gas is already lifting chemical exports and production and will grow as new capacity comes online.

• Strong investment growth in chemicals already materializing.

• Investments by other customer industries will create additional opportunities.

• Further gains in plastic and chemical exports, employment, and capital spending.

• Challenges: skilled labor, environmental permitting, etc.