33

1 18. Public Finance

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | madisen-peacock |

| View: | 218 times |

| Download: | 1 times |

1

18. Public Finance

2

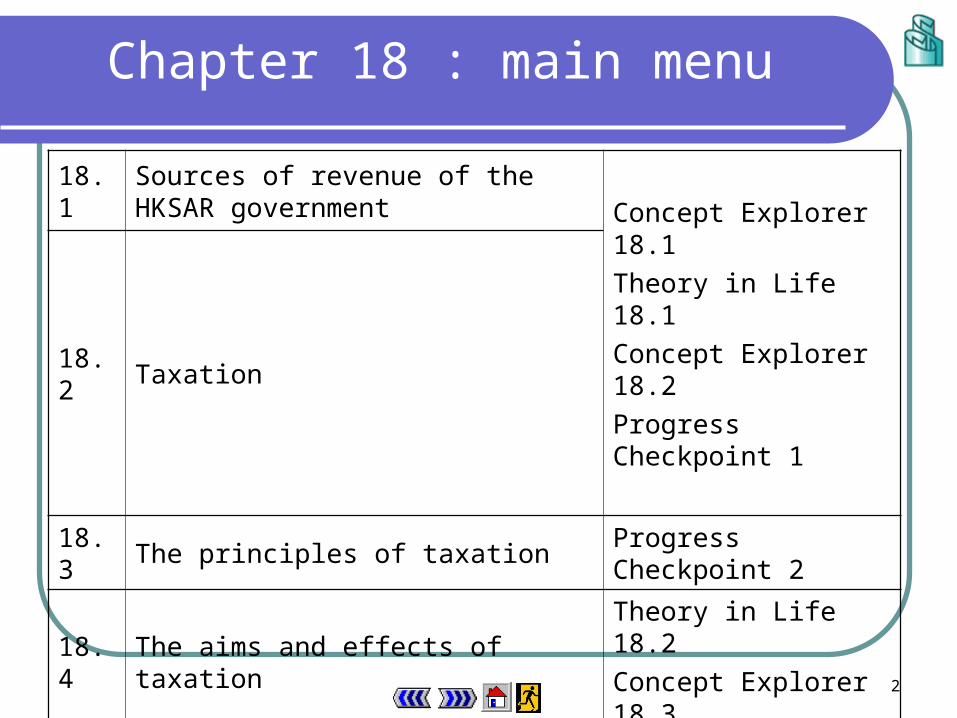

Chapter 18 : main menu

18.1Sources of revenue of the HKSAR government Concept Explorer 18.1

Theory in Life 18.1

Concept Explorer 18.2

Progress Checkpoint 118.2 Taxation

18.3 The principles of taxation Progress Checkpoint 2

18.4 The aims and effects of taxationTheory in Life 18.2

Concept Explorer 18.3

18.5Public expenditure as a proportion of GDP

Progress Checkpoint 418.6 Public expenditure

18.7 Government budget

3

Concept Explorer 18.1

Classifying an ad valorem sales tax Suppose the price of a bottle of wine is $5,000. If

a 60% ad valorem sales tax is imposed, is such tax proportional?

4

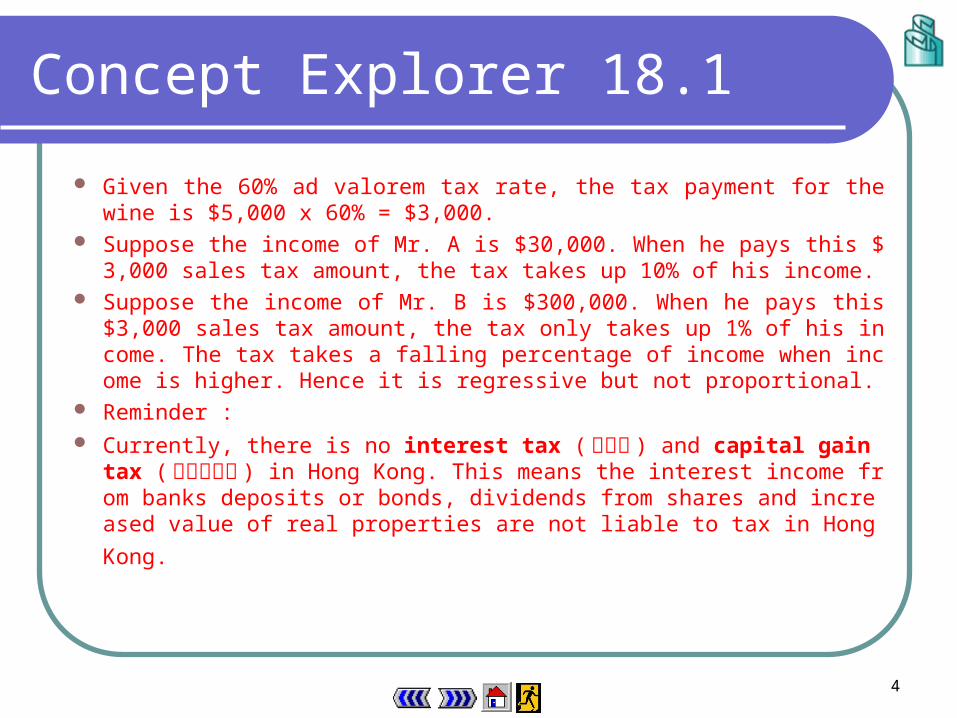

Given the 60% ad valorem tax rate, the tax payment for the wine is $5,000 x 60% = $3,000.

Suppose the income of Mr. A is $30,000. When he pays this $3,000 sales tax amount, the tax takes up 10% of his income.

Suppose the income of Mr. B is $300,000. When he pays this $3,000 sales tax amount, the tax only takes up 1% of his income. The tax takes a falling percentage of income when income is higher. Hence it is regressive but not proportional.

Reminder : Currently, there is no interest tax (利息稅 ) and capital gain tax

(資產增值稅 ) in Hong Kong. This means the interest income from banks deposits or bonds, dividends from shares and increased

value of real properties are not liable to tax in Hong Kong.

Concept Explorer 18.1

5

Theory in Life 18.1

The salaries tax system of Hong Kong Is the Hong Kong salaries tax system progressive or

proportional?

6

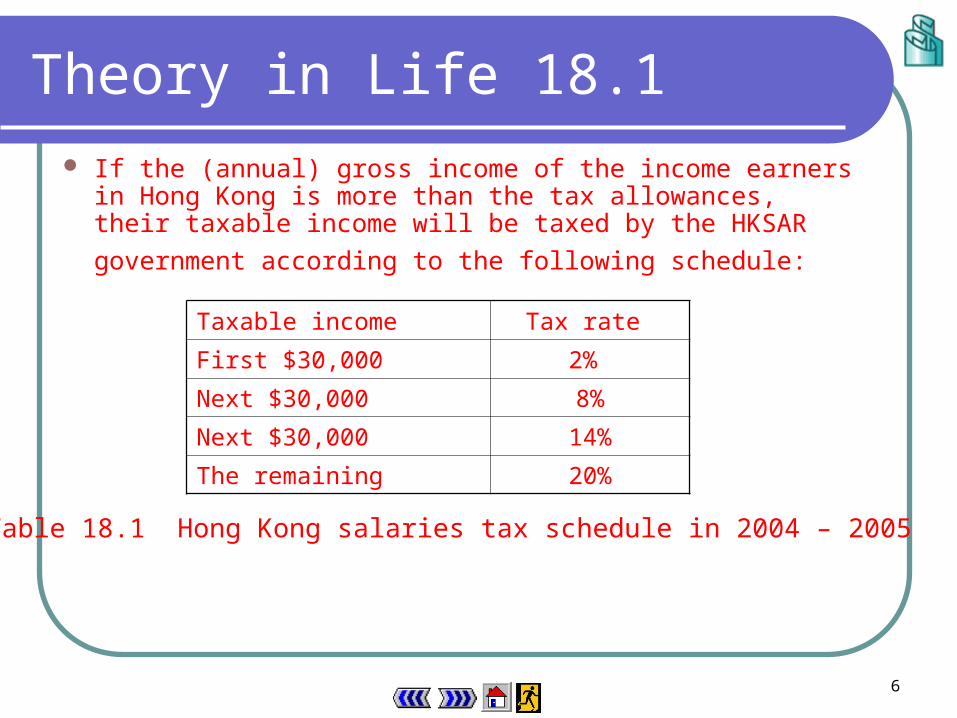

Theory in Life 18.1 If the (annual) gross income of the income earners in Hong

Kong is more than the tax allowances, their taxable income will be taxed by the HKSAR government according to the following

schedule: Taxable income Tax rate

First $30,000 2%

Next $30,000 8%

Next $30,000 14%

The remaining 20%

Table 18.1 Hong Kong salaries tax schedule in 2004 – 2005

7

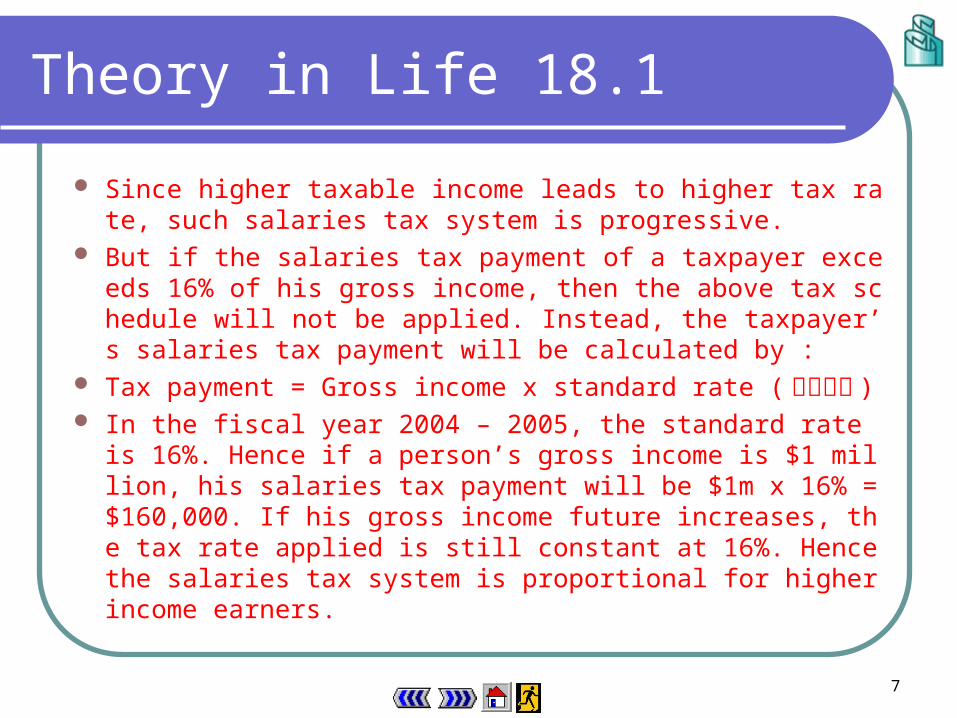

Since higher taxable income leads to higher tax rate, such salaries tax system is progressive.

But if the salaries tax payment of a taxpayer exceeds 16% of his gross income, then the above tax schedule will not be applied. Instead, the taxpayer’s salaries tax payment will be calculated by :

Tax payment = Gross income x standard rate (標準稅率 ) In the fiscal year 2004 – 2005, the standard rate is 16%. Hence if

a person’s gross income is $1 million, his salaries tax payment will be $1m x 16% = $160,000. If his gross income future increases, the tax rate applied is still constant at 16%. Hence the salaries tax system is proportional for higher income earners.

Theory in Life 18.1

8

Theory in Life 18.1

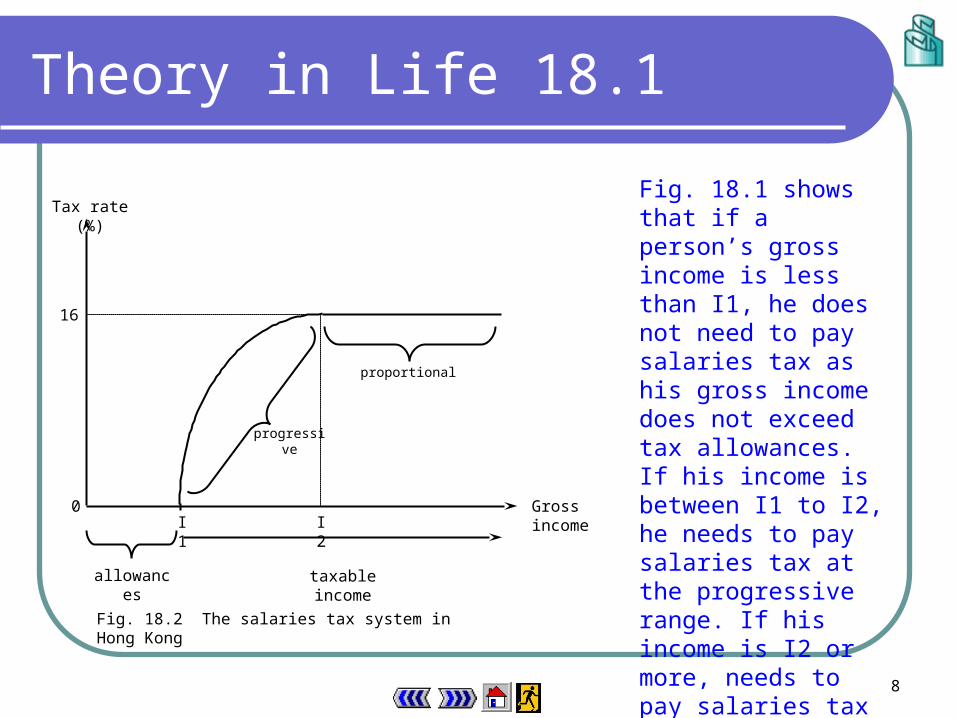

Gross income

taxable incomeallowances

0

Tax rate (%)

16

proportional

progressive

I1 I2

Fig. 18.2 The salaries tax system in Hong Kong

Fig. 18.1 shows that if a person’s gross income is less than I1, he does not need to pay salaries tax as his gross income does not exceed tax allowances. If his income is between I1 to I2, he needs to pay salaries tax at the progressive range. If his income is I2 or more, needs to pay salaries tax at the standard rate of 16%, i.e. the proportional range.

9

Concept Explorer 18.2

Comparing direct taxes and indirect taxes What are the advantages and disadvantages of direct

taxes over indirect taxes?

10

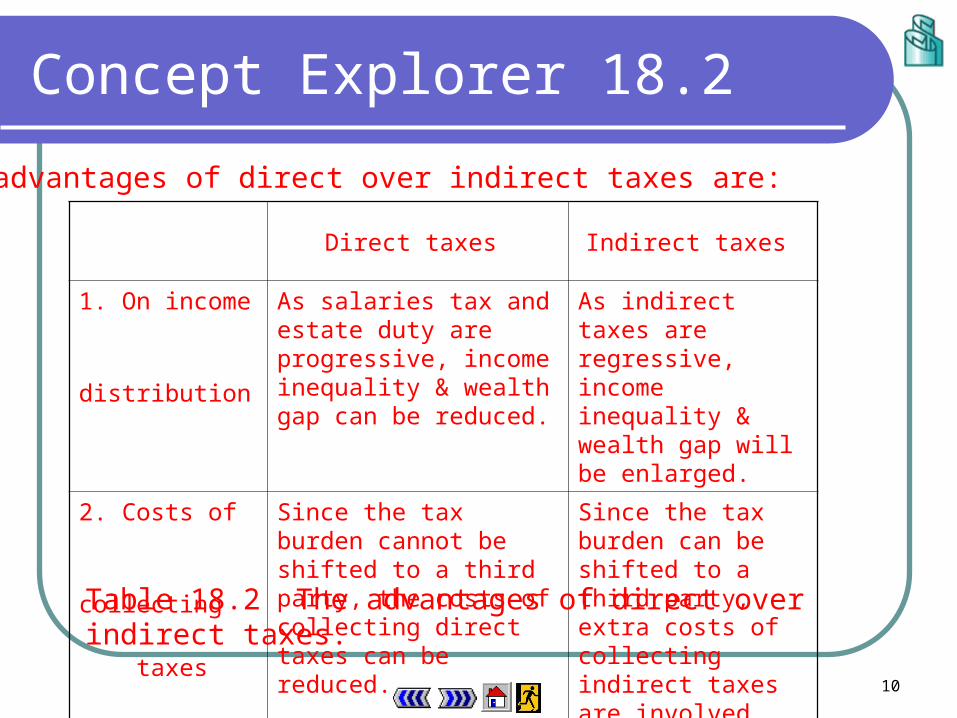

Concept Explorer 18.2

The advantages of direct over indirect taxes are:

Direct taxes Indirect taxes

1. On income

distribution

As salaries tax and estate duty are progressive, income inequality & wealth gap can be reduced.

As indirect taxes are regressive, income inequality & wealth gap will be enlarged.

2. Costs of

collecting

taxes

Since the tax burden cannot be shifted to a third party, the costs of collecting direct taxes can be reduced.

Since the tax burden can be shifted to a third party, extra costs of collecting indirect taxes are involved.

Table 18.2 The advantages of direct over indirect taxes.

11

Concept Explorer 18.2

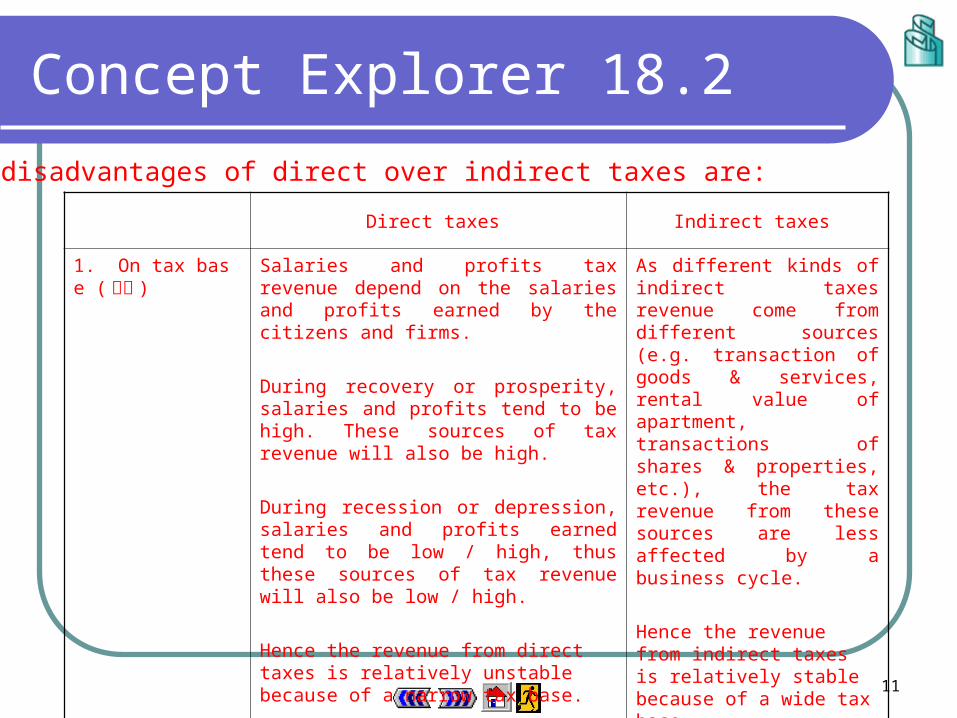

The disadvantages of direct over indirect taxes are:

Direct taxes Indirect taxes

1. On tax base (稅基 )

Salaries and profits tax revenue depend on the salaries and profits earned by the citizens and firms.

During recovery or prosperity, salaries and profits tend to be high. These sources of tax revenue will also be high.

During recession or depression, salaries and profits earned tend to be low / high, thus these sources of tax revenue will also be low / high.

Hence the revenue from direct taxes is relatively unstable because of a narrow tax base.

As different kinds of indirect taxes revenue come from different sources (e.g. transaction of goods & services, rental value of apartment, transactions of shares & properties, etc.), the tax revenue from these sources are less affected by a business cycle.

Hence the revenue from indirect taxes is relatively stable because of a wide tax base.

12

Concept Explorer 18.2

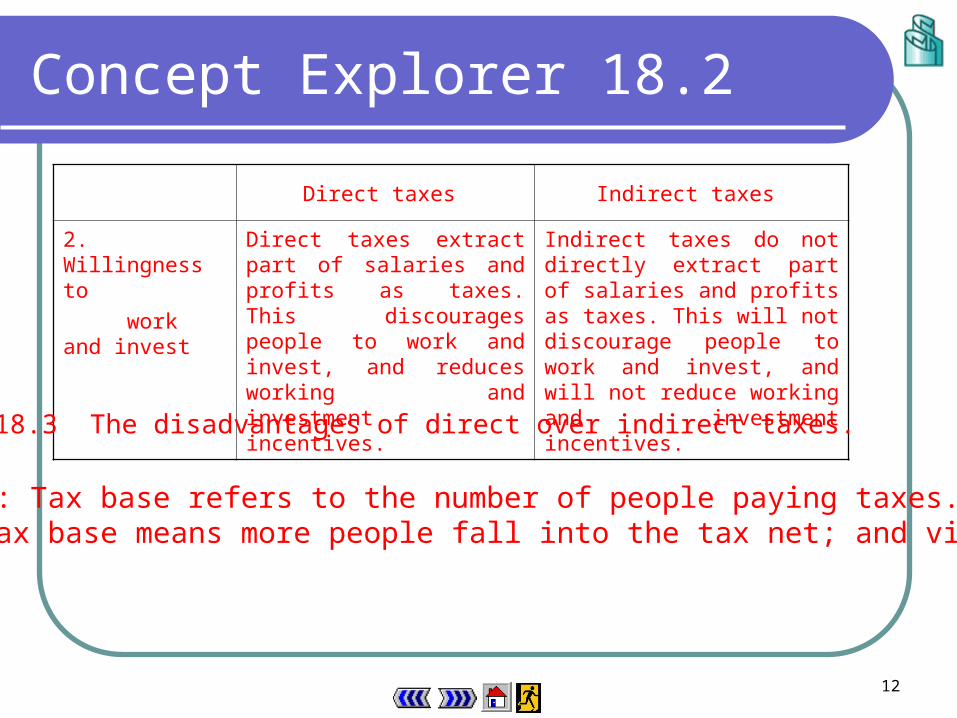

Direct taxes Indirect taxes

2. Willingness to

work and invest

Direct taxes extract part of salaries and profits as taxes. This discourages people to work and invest, and reduces working and investment incentives.

Indirect taxes do not directly extract part of salaries and profits as taxes. This will not discourage people to work and invest, and will not reduce working and investment incentives.

Table 18.3 The disadvantages of direct over indirect taxes.

Reminder : Tax base refers to the number of people paying taxes. A wider tax base means more people fall into the tax net; and vice versa.

13

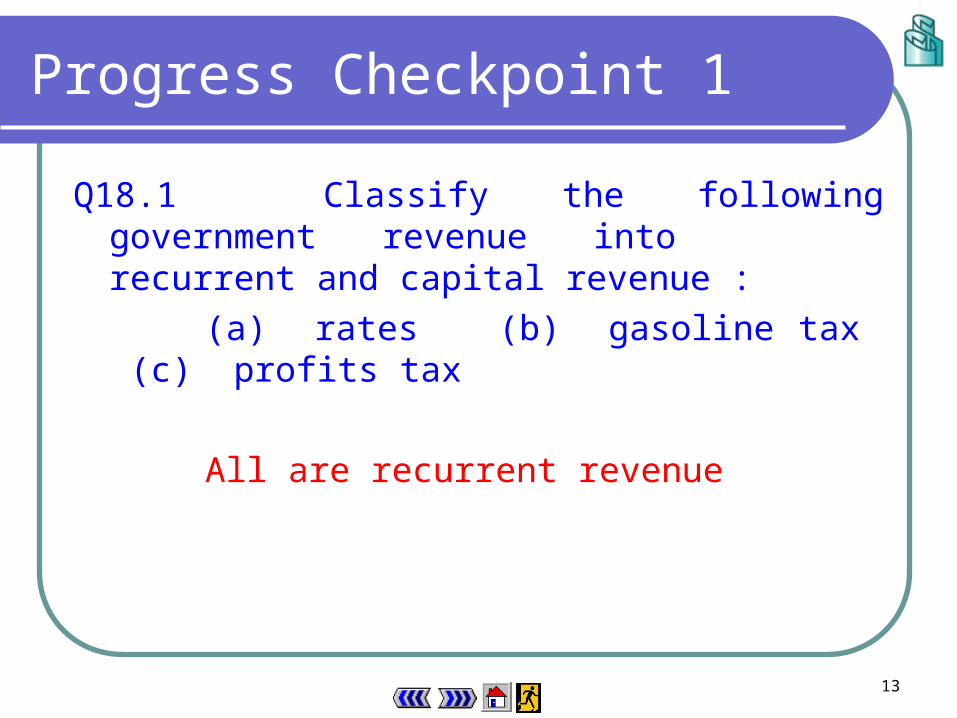

Progress Checkpoint 1

Q18.1 Classify the following government revenue into recurrent and capital revenue :

(a) rates (b) gasoline tax (c) profits tax

All are recurrent revenue

14

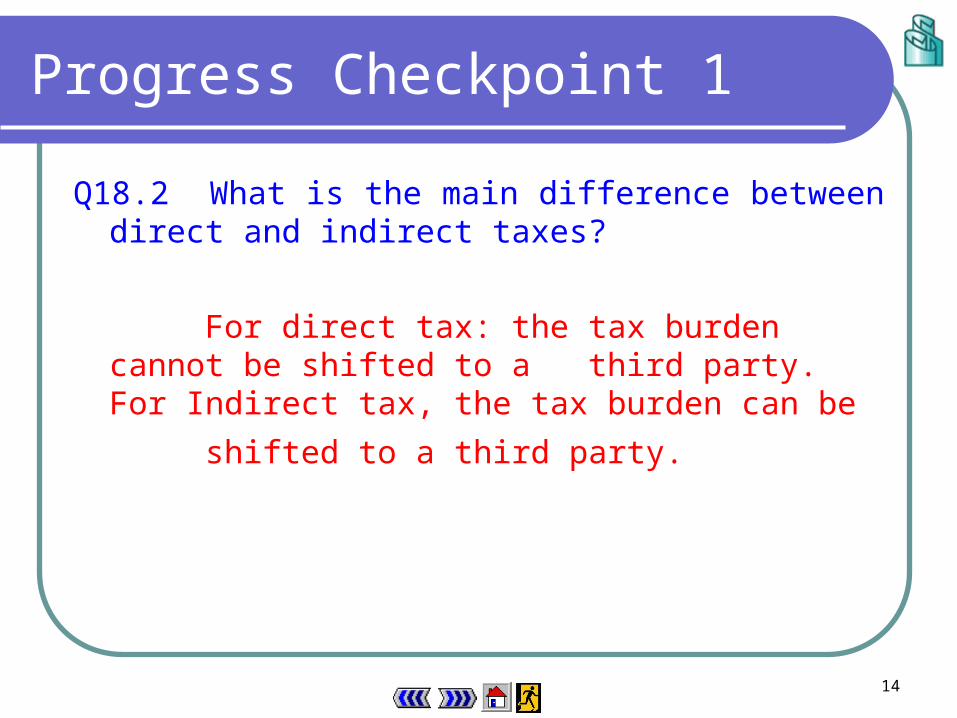

Q18.2 What is the main difference between direct and indirecttaxes?

For direct tax: the tax burden cannot be shifted to a third party. For Indirect tax, the tax burden can be shifted

to a third party.

Progress Checkpoint 1

15

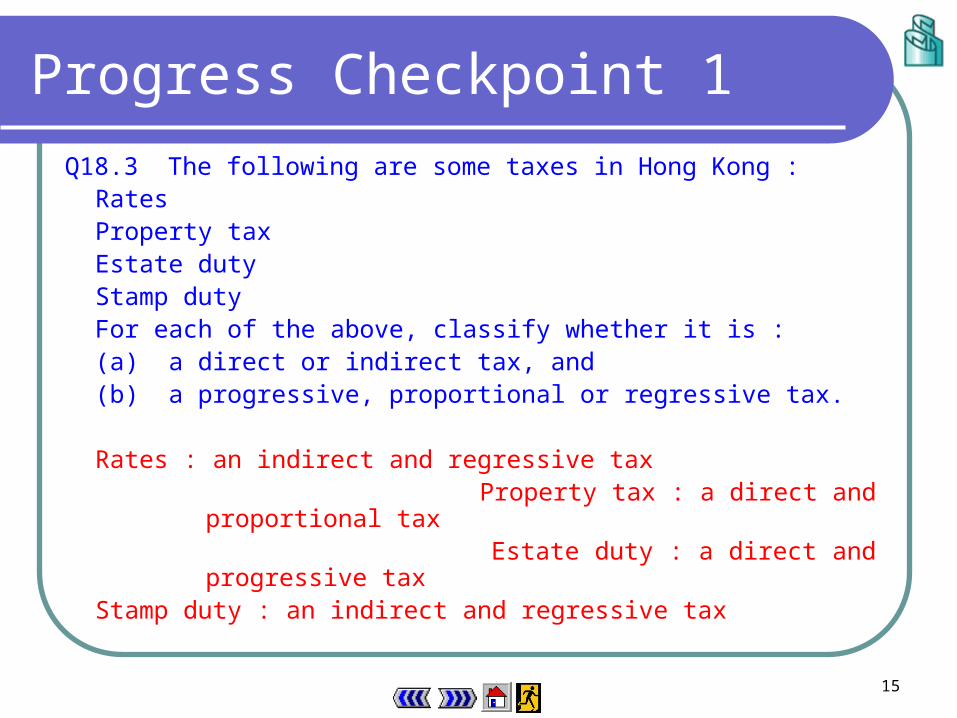

Q18.3 The following are some taxes in Hong Kong :RatesProperty taxEstate dutyStamp dutyFor each of the above, classify whether it is :(a) a direct or indirect tax, and(b) a progressive, proportional or regressive tax.

Rates : an indirect and regressive tax Property tax : a direct and proportional tax Estate duty : a direct and progressive tax

Stamp duty : an indirect and regressive tax

Progress Checkpoint 1

16

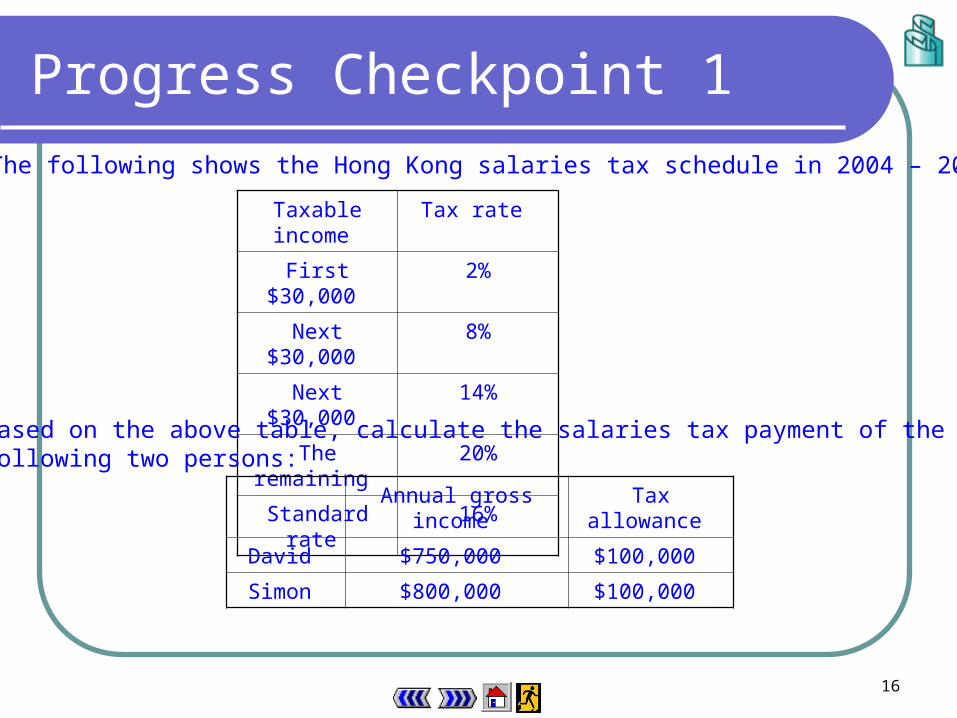

Progress Checkpoint 1Q18.4 The following shows the Hong Kong salaries tax schedule in 2004 – 2005 :

Taxable income Tax rate

First $30,000 2%

Next $30,000 8%

Next $30,000 14%

The remaining 20%

Standard rate 16%

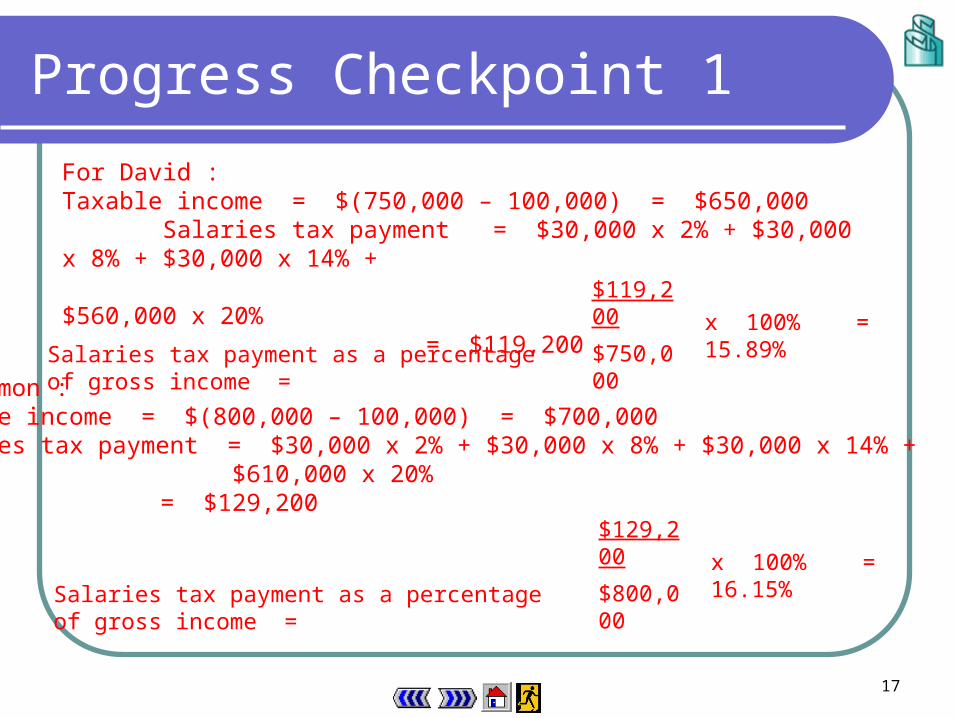

Based on the above table, calculate the salaries tax payment of the following two persons:

Annual gross income Tax allowance

David $750,000 $100,000

Simon $800,000 $100,000

17

Progress Checkpoint 1

For David :Taxable income = $(750,000 – 100,000) = $650,000 Salaries tax payment = $30,000 x 2% + $30,000 x 8% + $30,000 x 14% + $560,000 x 20%

= $119,200

Salaries tax payment as a percentage of gross income =

$119,200

x 100% = 15.89%$750,000

For Simon :Taxable income = $(800,000 – 100,000) = $700,000Salaries tax payment = $30,000 x 2% + $30,000 x 8% + $30,000 x 14% +

$610,000 x 20% = $129,200

Salaries tax payment as a percentage of gross income =

$129,200

x 100% = 16.15%$800,000

18

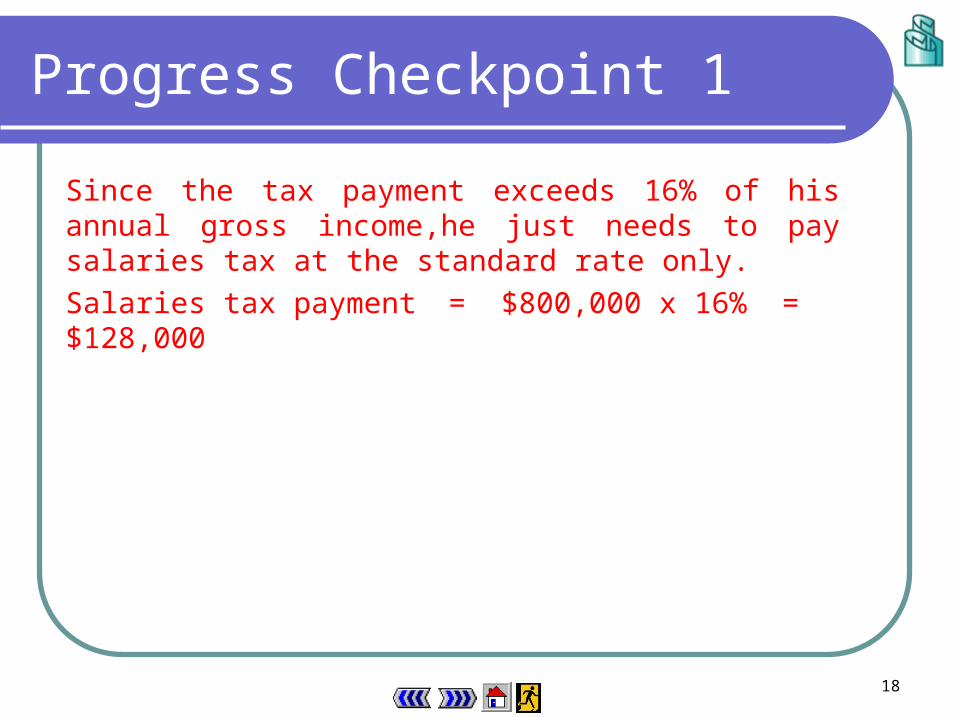

Since the tax payment exceeds 16% of his annual gross income,he just needs to pay salaries tax at the standard rate only.

Salaries tax payment = $800,000 x 16% = $128,000

Progress Checkpoint 1

19

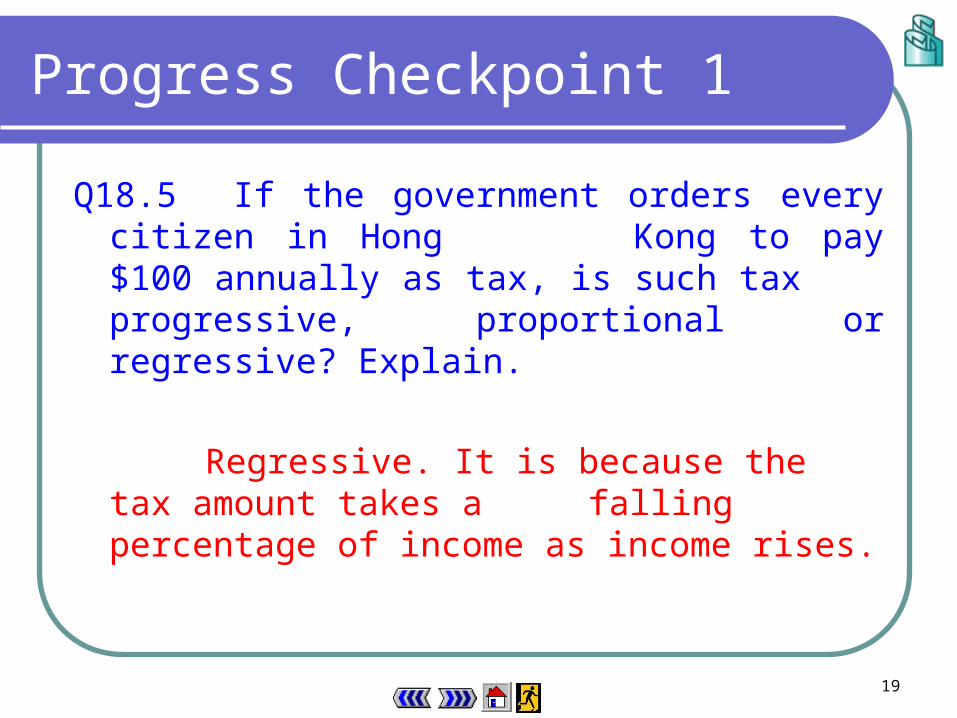

Q18.5 If the government orders every citizen in Hong Kong to pay $100 annually as tax, is such tax

progressive, proportional or regressive? Explain.

Regressive. It is because the tax amount takes a falling percentage of income as income rises.

Progress Checkpoint 1

20

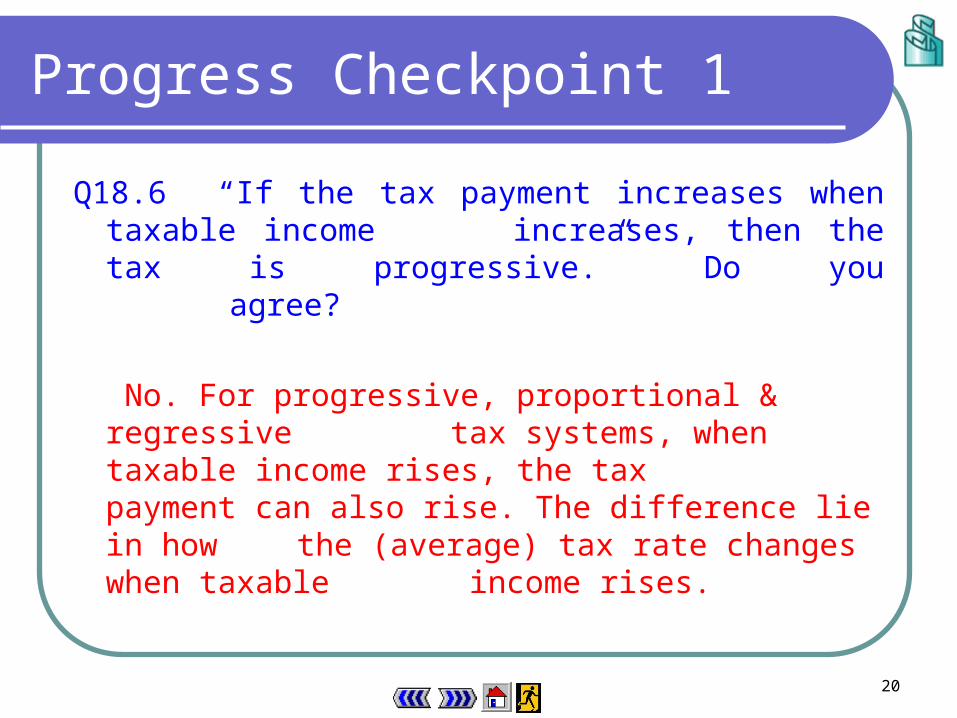

Q18.6 “If the tax payment increases when taxable income increases, then the tax is progressive.” Do you

agree?

No. For progressive, proportional & regressive tax systems, when taxable income rises, the tax payment can also rise. The difference lie in how the (average) tax rate changes when taxable income rises.

Progress Checkpoint 1

21

Q18.7 Suppose Mr. Chan earns HK$200,000 from his investment in Australia. Does he need to pay tax

to the HK SAR government? Which principle of taxation is applied? Explain.

No. This is because the source of receipts is not the Hong Kong economy. This is the source principle of taxation.

Progress Checkpoint 2

22

Theory in Life 18.2

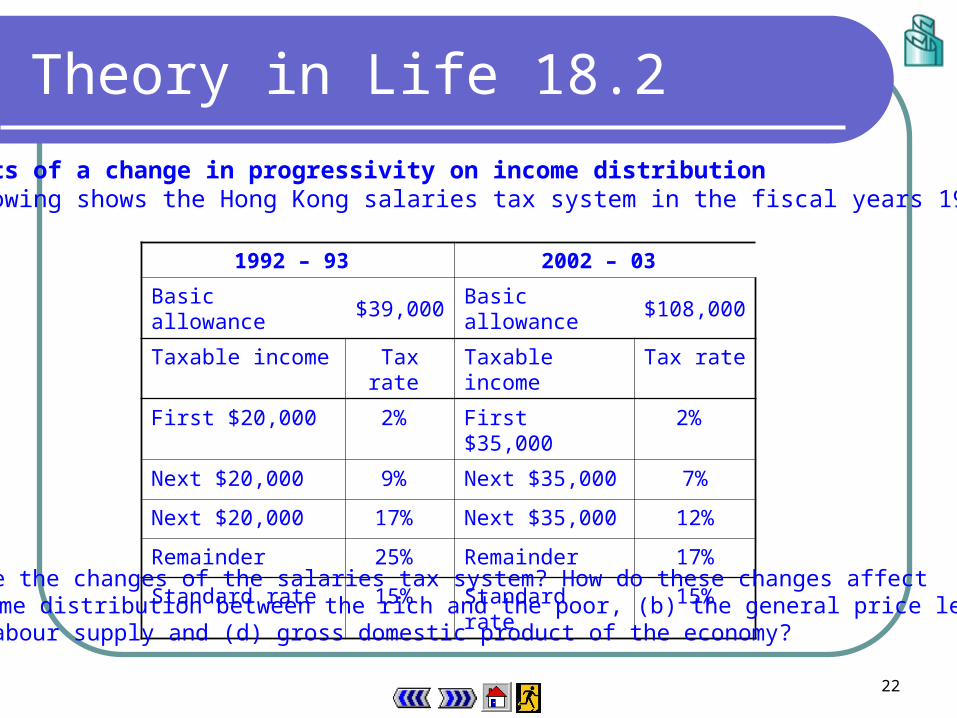

The effects of a change in progressivity on income distribution The following shows the Hong Kong salaries tax system in the fiscal years 1992 – 93 & 2002 – 03:

1992 – 93 2002 – 03

Basic allowance $39,000 Basic allowance $108,000

Taxable income Tax rate Taxable income Tax rate

First $20,000 2% First $35,000 2%

Next $20,000 9% Next $35,000 7%

Next $20,000 17% Next $35,000 12%

Remainder 25% Remainder 17%

Standard rate 15% Standard rate 15%

What are the changes of the salaries tax system? How do these changes affect (a) income distribution between the rich and the poor, (b) the general price level, (c) labour supply and (d) gross domestic product of the economy?

23

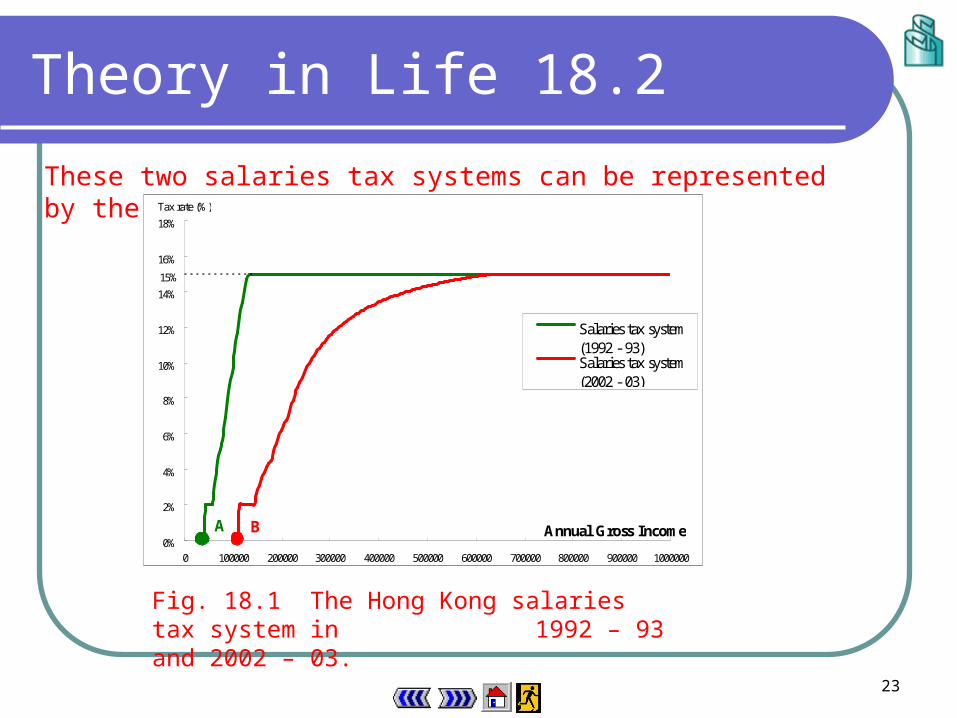

These two salaries tax systems can be represented by the following diagram :

Theory in Life 18.2

15%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0 100000 200000 300000 400000 500000 600000 700000 800000 900000 1000000

Annual Gross Income

Tax rate (%)

Salaries tax system(1992 - 93)Salaries tax system(2002 - 03)Dotted line

A B

Fig. 18.1 The Hong Kong salaries tax system in 1992 – 93 and 2002 – 03.

24

Theory in Life 18.2

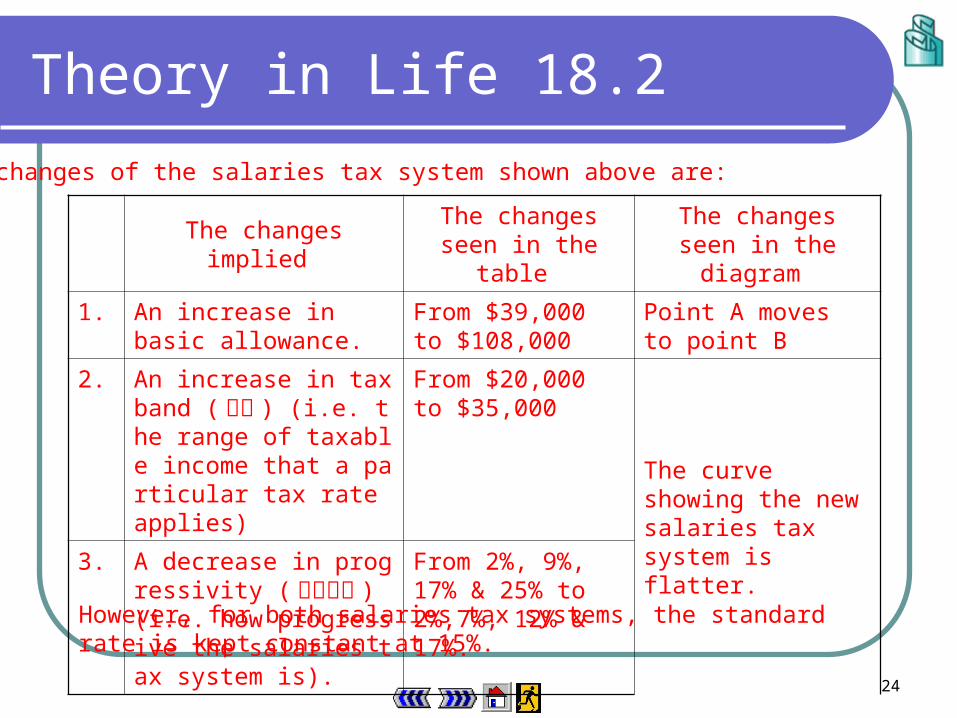

The changes of the salaries tax system shown above are:

The changes implied The changes seen in

the table The changes seen in

the diagram

1. An increase in basic allowance.

From $39,000 to $108,000

Point A moves to point B

2. An increase in tax band (稅階 ) (i.e. the range of taxable income that a particular tax rate applies)

From $20,000 to $35,000

The curve showing the new salaries tax system is flatter. 3. A decrease in progressivit

y (累進程度 ) (i.e. how progressive the salaries tax system is).

From 2%, 9%, 17% & 25% to 2%,7%, 12% & 17%.

However, for both salaries tax systems, the standard rate is kept constant at 15%.

25

(a) The effect on income distributionAs there is an increase in basic allowance, some tax payers whose annual gross income is higher than the original basic allowance but lower than the new one can escape from the tax net. These people usually belong to the low income group.

As there is a decrease in progressivity, some tax payers can pay taxes at tax bands with lower tax rates. Hence they pay less taxes. These people usually belong to the low and middle income groups.

As there is no change in standard rate, some tax payers pay the same amount of taxes. These people usually belong to the high income group.As the low and middle income group get benefits from the changes but not for the high income group, the income distribution is more evenly distributed (i.e. the wealth gap between the rich and the poor is narrower).

Theory in Life 18.2

26

(b)The effect on general price levelSince the low and middle income groups have higher disposable income, their demand for goods and services increase. There will be an upward pressure on the general price level.

(c) The effect on labour supplyWith a decrease in tax rates, the net income from work increases. This increases the working incentive of the low and middle income groups. Their labour supply will increase.

(d)The effect on gross domestic product

As the demand for goods and services increase, GDP tends to increase and unemployment rate decrease. There is an expansionary effect on the economy.

Theory in Life 18.2

27

Concept Explorer 18.3 Taxes and inflation Suppose a government raises taxes in an economy. Is this inflationary or deflati

onary? Is this expansionary or contractionary?

If the government raises direct taxes (e.g. raising the taxes rates for salaries tax, profits tax, etc.), the disposable income of people will decrease.

If the government raises indirect taxes (e.g. sales tax, gasoline tax, hotel accommodation tax, rates), the supply of these goods and services will decrease.

The demand for goods and services will decrease.

As the tax burden can be shifted to consumers, the general price level tends to increase, i.e. it is inflationary.

As aggregate expenditure decreases, the general price level also decreases, i.e. it is deflationary.

28

Quantity0

P ($)S

Q1

P1

D1

Quantity0

P ($)

P1

Q1

D

S1

E1

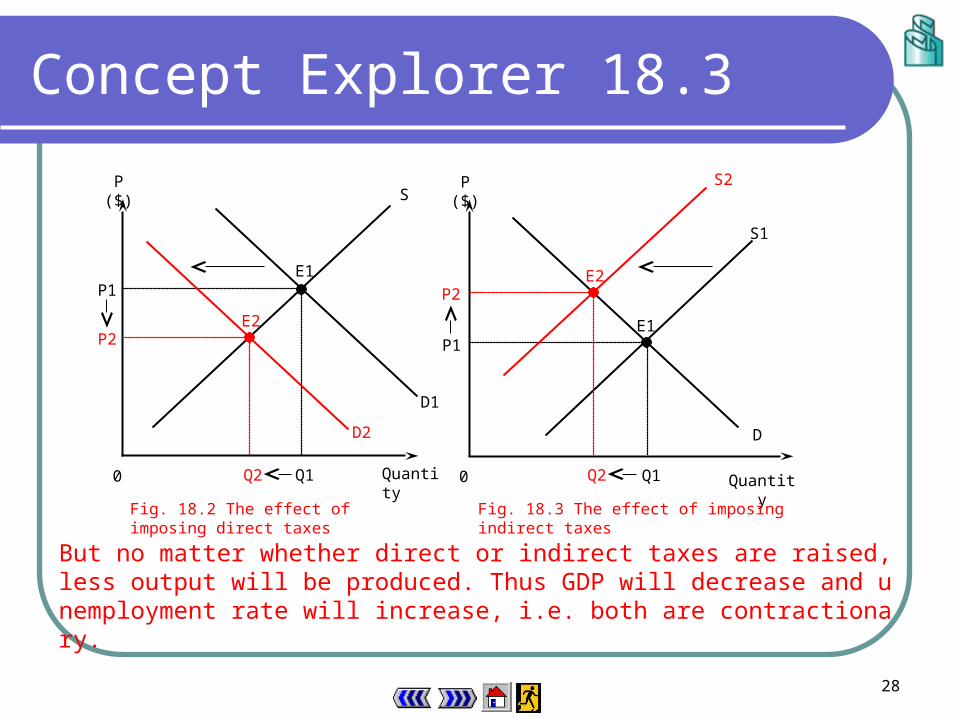

Fig. 18.2 The effect of imposing direct taxes Fig. 18.3 The effect of imposing indirect taxes

E1

D2

P2E2

Q2

E2

Q2

P2

S2

But no matter whether direct or indirect taxes are raised, less output will be produced. Thus GDP will decrease and unemployment rate will increase, i.e. both are contractionary.

Concept Explorer 18.3

29

Progress Checkpoint 3

Q18.8 If the government reduces the salaries and profits tax rates, will the total tax revenue from these two sources necessarily fall? Explain.

No. When profit and salaries tax rates are reduced, this tends to lower salaries and profits tax revenue.

However, with a fall in these rates, people tend to work more and investors invest more. Thus their taxable income and profits will rise. This tends to raise salaries and profits tax revenue. If the effect of a rise in taxable income and profits on tax revenue is greater than that of a fall in tax rates, then the tax revenue will rise.

30

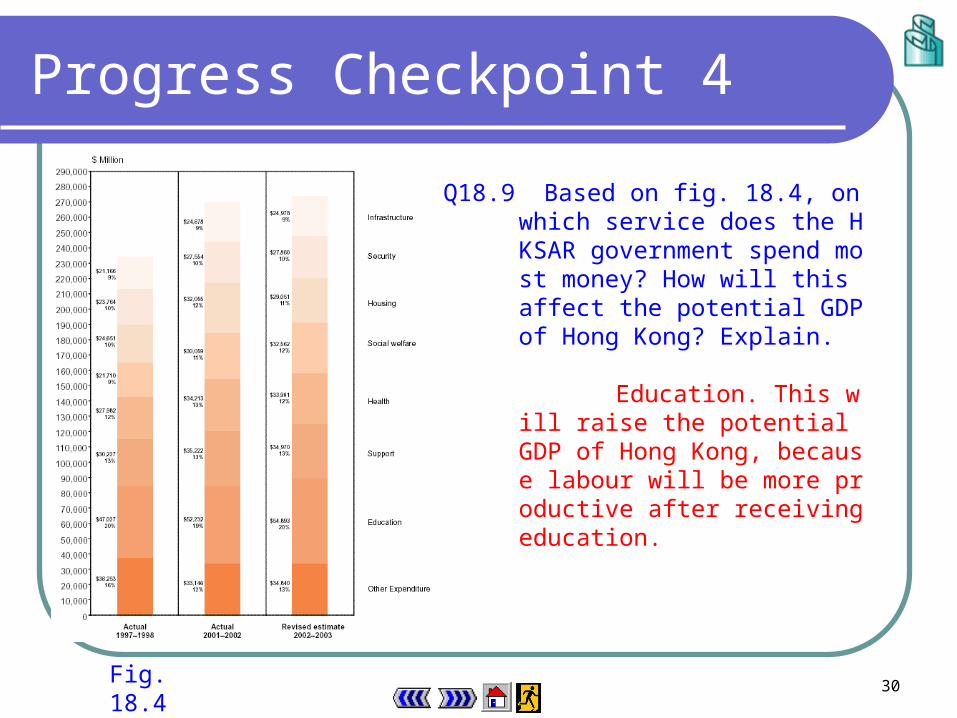

Progress Checkpoint 4

Q18.9 Based on fig. 18.4, on which service does the HKSAR government spend most money? How will this affect the potential GDP of Hong Kong? Explain.

Education. This will raise the potenti

al GDP of Hong Kong, because labour will be more productive after receiving education.

Fig. 18.4

31

Q18.10 Explain how it is possible for the size of the public sector to increase, despite a fall in the amount of public sector expenditure.

The size of the public sector is the ratio of public sector expenditure to GDP. If the fall in GDP is greater than the fall in public sector expenditure, then the size of the public sector may rise.

Progress Checkpoint 4

32

Q18.11 Suppose the estimated expenditure and revenue of a fiscal year are $100 and $80 respectively. What kind of budget is this?

Deficit budget, because the estimated expenditure is greater than the estimated revenue.

Progress Checkpoint 4

33

End of Chapter 18