32

1 2006/07 Interim numbers & Outlook SFAF Meeting - 15 November 2006 - Bernard HUVÉ CEO

| Date post: | 14-Dec-2015 |

| Category: |

Documents |

| Upload: | haden-westmoreland |

| View: | 213 times |

| Download: | 0 times |

1

2006/07 Interim numbers

& Outlook

SFAF Meeting

- 15 November 2006 -

Bernard HUVÉ CEO

2

SII at a glance

SII is present on the market of technology consulting- Outsourced R&D, engineering and systems integration & telecoms- Presence in France + subsidiary in Poland

A long-lasting company: 27 years of profitable growth (founded on 1 April 1979) 2005/06 sales: €105.7m (+21.6% of organic growth) 2005/06 operating margin: 10.1% Financially sound (IFRS) 31/03/06: Net cash €14.4m; Shareholders’ capital €34.2m

1 800 employees at 31 October 2006 (+23%)- Of which 80% engineers BAC + 5- A strong technical culture and client service

Value creation: 2005 ROCE (after tax) = 35.6%- A flexible organisation, decentralised, reactive- Stringent management on a day-to-day basis

ID card

3

SII’s services

Outsourced R&DR&D Consulting

Studies and implementationProcessing, industrialisation

66%

Systems Integration, Networks & Telecoms

Third partymaintenance

33%

Development consulting

87%

Project management assistance

5%

Other and non IT

8%

SII at a glance

4

Strasbourg

Sophia

Vélizy

Sannois

Lille

9 agences10 offices

Toulouse

Bordeaux

Nantes Tours

Le MansBrest Rennes

Caen

Lyon

MontpellierLa Ciotat

Aix0-100 Lille, Strasbourg, Warsaw

> 100 Aix, Rennes, Nantes Sannois, Sophia, Toulouse, Vélizy

Export 1%

Province63%

Ile de France

36%

Geographical breakdown of sales

Lannion

Niort

National geographical footprint – subsidiary in Poland

SII at a glance

1 subsidiary

5

A loyal clientele with major accounts

Major accounts 95%, SME 2%, Other 3%

20 top clients = 67% of sales- SII’s strategy: quality of service

- SII’s positioning: mixed teams – long and recurrent projects dual expertise: IT and functioning

- Client strategy: listings and discounts on sales, pricing pressure, requests for projects with

earnings commitment

SII at a glance

Amadeus EADS Gemalto Sagem Thales

DCN France Telecom IBM Siemens Thomson

TOP 10 CLIENTS

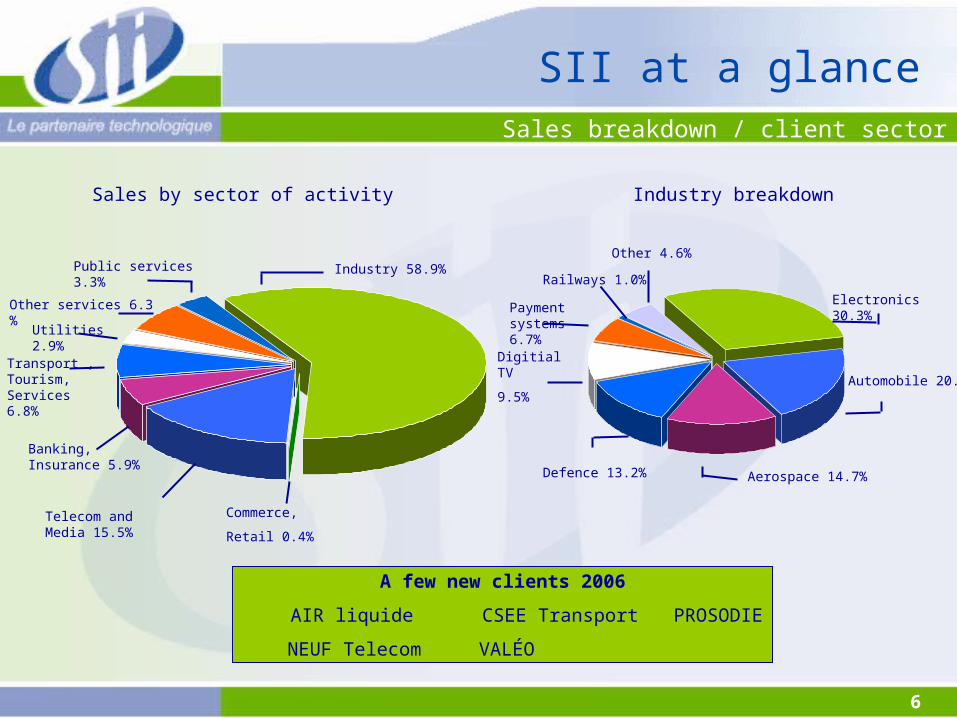

6

Banking, Insurance 5.9%

Sales breakdown / client sector

Industry 58.9%

Telecom and Media 15.5%

Transport , Tourism, Services 6.8%

A few new clients 2006

AIR liquide CSEE Transport PROSODIE

NEUF Telecom VALÉO

SII at a glance

Utilities 2.9%

Other services 6.3 %

Public services 3.3%

Sales by sector of activity Industry breakdown

Electronics 30.3%

Automobile 20.0%

Aerospace 14.7%Defence 13.2%

Digitial TV

9.5%

Payment systems 6.7%

Other 4.6%

Commerce,

Retail 0.4%

Railways 1.0%

7

Gaining strength of fixed-rate services Commitment to achieving earnings rather than supplying means Outsourcing Global contracts vs specific skills

Sales by contract

Changes in contracts

SII at a glance

Technicalassistance

73.3%

Other 7.9%

Fixed rate 18.8%

8

Summary

H1-2006/07

Sustained profitable growth – SII on the stock market

2006/07 Outlook and targets

9

Durable growth drivers- Product innovation, a factor of company competitiveness- Sustained growth in outsourcing (Flexibility / Technological complimentarity)- The taking off of built-in IT

Technology consulting, a buoyant market

Technology consulting€5bn

Outsourced IT R&D, software & ITand technical services

H1-2006/07

Source : Syntec Informatique 17 octobre 2006

Technology consulting outperforms the L&S sector

H1-2006 growth: 8% vs 6.5%

L&S sector(Syntec Informatique structure)

€21bn

10* Source : Syntec Informatique 17 octobre 2006

Return to buoyancy

-5

0

5

10

15

20

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06

GDP L&S Investment

Growth founded on a recovery in IT investment- Projects reappear- Growth mainly driven by volumes and rarely by prices- Durable growth triggers (globalisation, competition, retirement boom)

But a tightening labour market- 65% of companies say they have difficulties in recruiting*- A greater turnover in the IT sector- Salary pressure

H1-2006/07

Growth in %

11

1 company, 9 profit centres - Low indirect rates (10.1%), despite decentralisation- Entrepreneur managers- Reporting in (virtually) real time

A quality approach at the heart of the strategy- One of the first IT services companies to obtain the ISO9001 certificate in 1992- One of very few IT services companies to be certified for 100% of its activity- A very advanced CMMi approach

Attributes of an average-sized player- Decentralisation / Responsibility- Commercial buoyancy- Local services with clients- Huge reactivity

SII outperforms technology consulting

SII +21% in H1-2006/07 vs Technology consulting +8%*

* Source : Syntec Informatique 17 octobre 2006

H1-2006/07

12

41.2

48.4

58.7

H1 2004 H1 2005 H1 2006

SII: Sustained growth

A buoyant first halfQ1 sales €29.61m, +21.3 %Q2 sales €29.13m, +21.3 %

+17.6%

Sales in €m+21.3%

H1-2006/07

13

102 107 108 118 140 173

942 9981059

12101297

1531

0

200

400

600

800

1000

1200

1400

1600

1800

2001 2002 2003 2004 2005 S1 2006

Productive headcount

Indirect

Average headcount

Recruitment trends

HR efforts in line with the strategy- Recent recruitments: 347 engineers (target: +700 engineers in 2006/07)- Huge capacity to recruit: school presence, dedicated in-house teams, enterprise culture,

cooptation- Turnover: 23% - Salary pressure

H1-2006/07

14

0

1

2

3

4

5

6

avr-0

4

juin-

04

août

-04

oct-0

4

déc-

04

févr

-05

avr-0

5

juin-

05

août

-05

oct-0

5

déc-

05

févr

-06

avr-0

6

juin-

06

août

-06

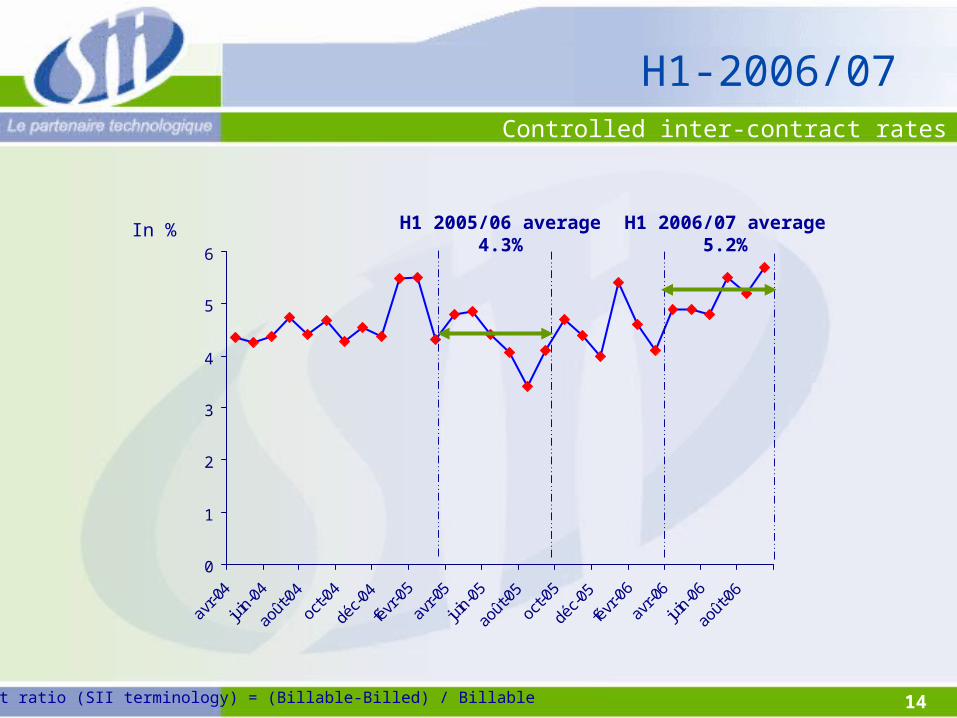

Inter-contract ratio (SII terminology) = (Billable-Billed) / Billable

Controlled inter-contract rates

In %

H1-2006/07

H1 2005/06 average4.3%

H1 2006/07 average5.2%

15

Billable days Q2 Q3 Q4 Q1 Total

2004/05 62 65 64 63 254

2005/06 63 64 63 65 255

2006/07 60 63 63 64 250

An unfavourable first half

A penalising 2006/07 timetable regarding sales- Fewer billable days (250!)- A first half (civil year Q2) with only 60 billable days- A base of comparison focused on SII’s first half

A huge temporary impact on profitability- Employees with 35 days of fixed holiday per year (25+10 fixed flexi days)- A direct impact on profitability (3 / 63 = 4.8% on Q2)- An impact spread over 2006/07 (5 / 255 = 2.2% over the year)

H1-2006/07

16

+ Commercial buoyancy (organic growth = +21%) – Slight increase in the inter-contract rate – Higher average salary > Increase in selling prices– Impact from n° of trading days on sales and above all on profitability

2006/07 Q2 Q3

Sales (€m) 29.61 29.13

2005/06 (in %) +21.3 +21.3

Op. margin (in % of sales) 6.2% 10.2%

Att. net profit (in % of sales) 4.3% 6.6%

Average headcount in quarter 1678 1733

In summary

H1-2006/07

17

Sustained profitable growth

H1-2006/07 numbers

Financial structure

SII shares

18

0.68

47.2

Sales€58.74m +21.3%

In €m

Consumed purchases

PayrollTaxes

4.9

1.7

Provisions

Sustained profitable growth

Other income and expenses

0.61

€4.83m -10.7%

Op. profit

Huge payroll = 80.4% of sales (vs 76.6%)- 4-day delay in billing- Average salary +2.5%

19

C L Ô T U R E A U 31 M A R S

Profit and loss account

Sustained profitable growth

In €m

H1-06/07

IFRS

H1-05/06

IFRS

Sales 58.74 48.43 +21.3

Operating profit 4.83 5.41 -10.7

in % of sales 8.2 11. 2

Financial products 0.11 0.21 -

Tax 1.73 1.94 -

Att. net profit 3.21 3.68 -12.8

in % of sales 5.5 7.7

Average headcount 1704 1346 +26.6

Headcount at end of period 1755 1422 -

20

Cash flow capacity

Change in WCR

Investment

Financing (incl. dividends)

Cash flow

Available cash

H1-2005/06

Cash flow table

Share transfers

In €m

Net cash

3.50

-0.60

-0.30

-1.50

-2.40

-4.10

-1.80

-4.20

H1-2006/07

Sustained profitable growth

4.20

2.00

-0.90

-0.80

0.30

-2.20

-1.00

-0.70

21

Financial structure

In €m

Sustained profitable growth

IFRS30/09/2005

Fixed assets3.4

WCR12.0

Cash16.3

Shareholders’capital

31.1

Fixed assets 0.6

IFRS30/09/2006

Fixed assets5.9

WCR18.9

Cash10.2

Shareholders’ capital

34.5

Fixed assets0.5

22

Shareholders’ structure

Personnel and fund 4.54%

Free float 30.61%

Management 56.42%

Treasury shares 8.43%

3 000 000 shares

SII shares

Source : SII

23

Technology consulting (Akka, Assystem, Alten, Altran, Ausy)

Eurolist (C)Code ISIN : FR0000074122

EuroNext segment NextEconomy / SBF 250 – Small 90

Stock-market performance

SII shares

Source JCF Quant

SII

20

25

30

35

40

45

50

55

T42003

T12004

T22004

T32004

T42004

T12005

T22005

T32005

T42005

T12006

T22006

T32006

T42006

24

2006/07 Outlook

SII strengths

2006/07 targets

SII outlook

Sector outlook

25

Sustained demand

Continued investment in companies- Catching up with underinvestment in the past

- Technological innovation, distribution of in-built electronics

- Renewal of IT systems

- Multiplication of projects (smaller but more frequent)

Growing outsourcing- Retirement boom

- Refocusing on the core business

- Increasingly complex projects

2006/07 Outlook

Today’s challenge: recruitment - Conserve criteria of quality and profitability

- SII: 700 engineers forecast in 2006/07 (half for turnover, half for growth)

26

Margins under pressure

Virtually stable reference prices- Pricing power on the demand side

- Overcapacity of the offering, dumping of small players

- Clients looking for savings

- Indirect pressure from offshoring

Selling price – cost price scissor effect- Pressure on salaries

- Shortfall of certain profiles

Problem of billable days- H2-2006/07 virtually stable in relation to 2005/06 (-1 day)

- 252 days in 2007/08

2006/07 Outlook

Billable days Q2 Q3 Q4 Q1 Total

2005/06 63 64 63 65 255

2006/07 60 63 63 64 250

2007/08 61 64 64 63 252

27

Constantly looking for improvement

SII proactive regarding profitability

Continued rigourous management- Reduced functioning costs- Indirect rates under pressure

Nearshore intervention capacity (Poland)

Growth / profitability arbitrage- Intention to not enter into a deflationary trend…- … which could lead to a refusal of missions

The real challenge: improvement of production processes- The possibility of work packages- The CMMi

2006/07 Outlook

28

The advantages of the CMMi model

Necessity to improve the management of complex projects- Clients require an increasing number of services to commit to earnings

- Additional risks… (exceeding budgets, changes) - …but opportunities to gain margins in certain conditions- Necessary discipline to control projects and optimise teams and expertise

Against this backdrop, quality insurance and CMMi valued processes are solutions adapted to the integration of IT systems.

2006/07 Outlook

Advantages for SII- Traceability, capitalisation and

reproductibility- Better management of employed

resources- Proposals for hybrid contracts- Reduction and control of unknown

Advantages for clients

- Better defined interfaces (quality) - Repeated follow up and deliveries- Platform development (outsourced services for the

supplier)

29

Early implementation of the CMMi model

This valuation backs SII’s level of quality- Process mastered and standardised throughout the company

- Development planned and assessed- Corrective forecasts and actions- Collective capitalisation and valuation (expertise, methods, tools and metrics)

2006/07 Outlook

Certified service sites (at CMMi level) SII Aix-en-Provence (3) Silogic Toulouse (2)

AXLOG engineering (3) SII Sophia Antipolis (2) SQLI Toulouse (2)

Cap Gemini-Paris Accelerated Delivery center (2)

SII Toulouse (2) Steria Midi Pyrénées (2)

SII the most advanced players in this approachAt 4/09/2006 – official list of the SEI relative to valued French IT services companies*

i.e. for SII: 1/2 sites at level 3 and 2/6 sites at level 2 (at 4/09/2006)

SII’s target:

December 2006: Nantes (2) February 2007: Rennes (2)

End-2008: all agencies committed to generating earnings will be at level 3

* Sources: http://seir.sel.cmu.edu/pars/pars_list_iframe.asp

30

2006/07 Outlook

1. Limited risksClients: large accounts, loyalHistorical and technoligical background Persisting quality insurance

2. Basic functional model One company, multiple profit centresDecentralised structure and localised servicesEnterprise culture: Technical and Services

SII’s strengths – Still the same!

3. Sound balance sheetSteady cash generationSatisfactory cash balanceNo financial debt

31

2006/07 Targets

Assumptions regarding the business climate Sustained demand

6-8% of growth according to IT Syntec3 times growth forecast for GDP

Margins under pressure2006 prices = 2005 prices + ε +0% (a little better in 2007?)

SII’s targets* Sales growth of around 20% (€125m-130m) Operating margin down (9-10%) 2,000 salaries at 31 March 2007 (net creation of 350/400 jobs)

Confirmation of targets from May 2006 *

* Réunion SFAF du 17 mai 2006

32

Upcoming meetings

Q3 earnings: 14 February 2007

Full-year earnings and SFAF meeting: 16 May 2007

2006/07 AGM: 20 September 2007