33

1 CREDICORP November, 2005

| Date post: | 15-Dec-2015 |

| Category: |

Documents |

| Upload: | lee-welles |

| View: | 216 times |

| Download: | 2 times |

1

CREDICORP

November, 2005

2

Agenda

Peruvian Economy

Credicorp Ltd.

Peruvian Financial System

Credicorp’s main subsidiaries

Credicorp’s earnings contributions

Overview

3

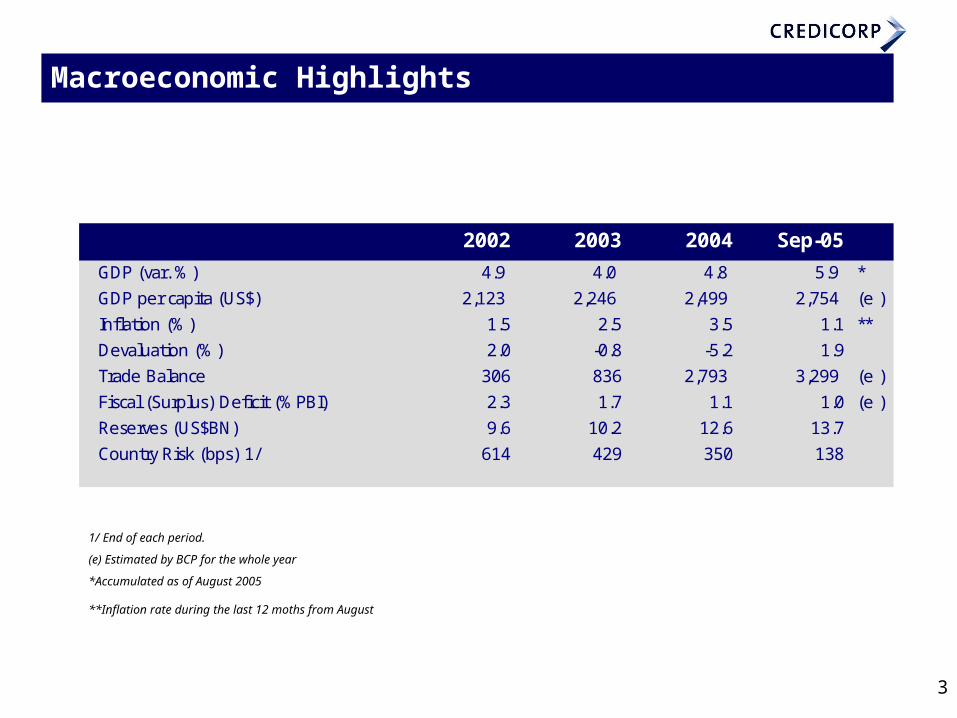

Macroeconomic Highlights

1/ End of each period.

(e) Estimated by BCP for the whole year

*Accumulated as of August 2005

**Inflation rate during the last 12 moths from August

2002 2003 2004 Sep-05

GDP (var. %) 4.9 4.0 4.8 5.9 *

GDP per capita (US$) 2,123 2,246 2,499 2,754 (e )

Inflation (%) 1.5 2.5 3.5 1.1 **

Devaluation (%) 2.0 -0.8 -5.2 1.9

Trade Balance 306 836 2,793 3,299 (e )

Fiscal (Surplus) Deficit (%PBI) 2.3 1.7 1.1 1.0 (e )

Reserves (US$BN) 9.6 10.2 12.6 13.7

Country Risk (bps) 1/ 614 429 350 138

4

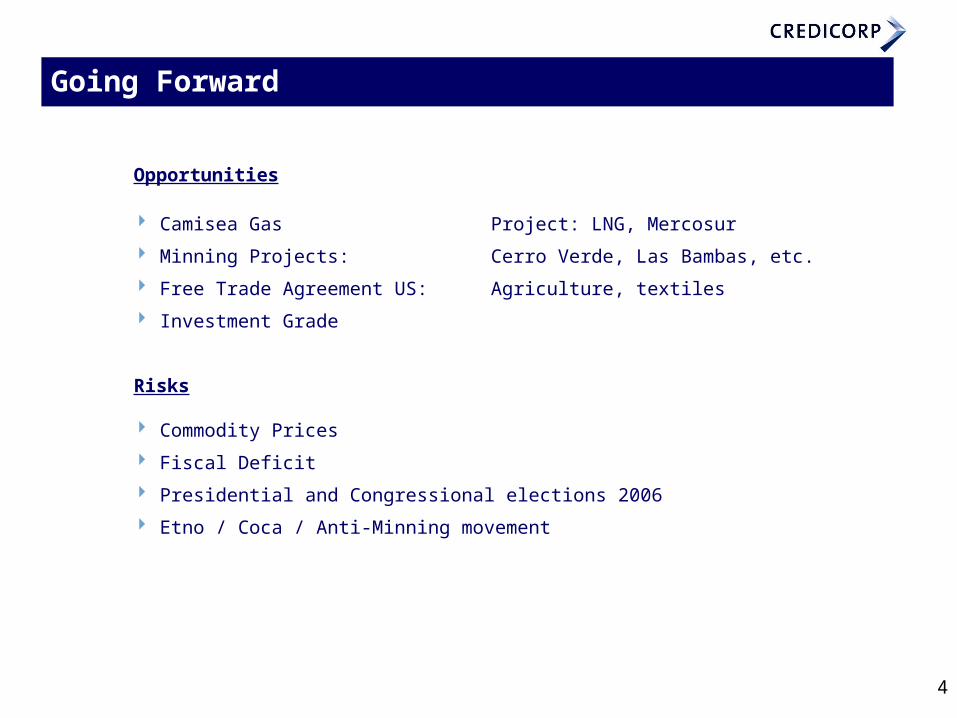

Going Forward

Opportunities

Camisea Gas Project: LNG, Mercosur

Minning Projects: Cerro Verde, Las Bambas, etc.

Free Trade Agreement US: Agriculture, textiles

Investment Grade

Risks

Commodity Prices

Fiscal Deficit

Presidential and Congressional elections 2006

Etno / Coca / Anti-Minning movement

5

Agenda

Peruvian Economy

Credicorp Ltd.

Peruvian Financial System

Credicorp’s main subsidiaries

Credicorp’s earnings contributions

Overview

6

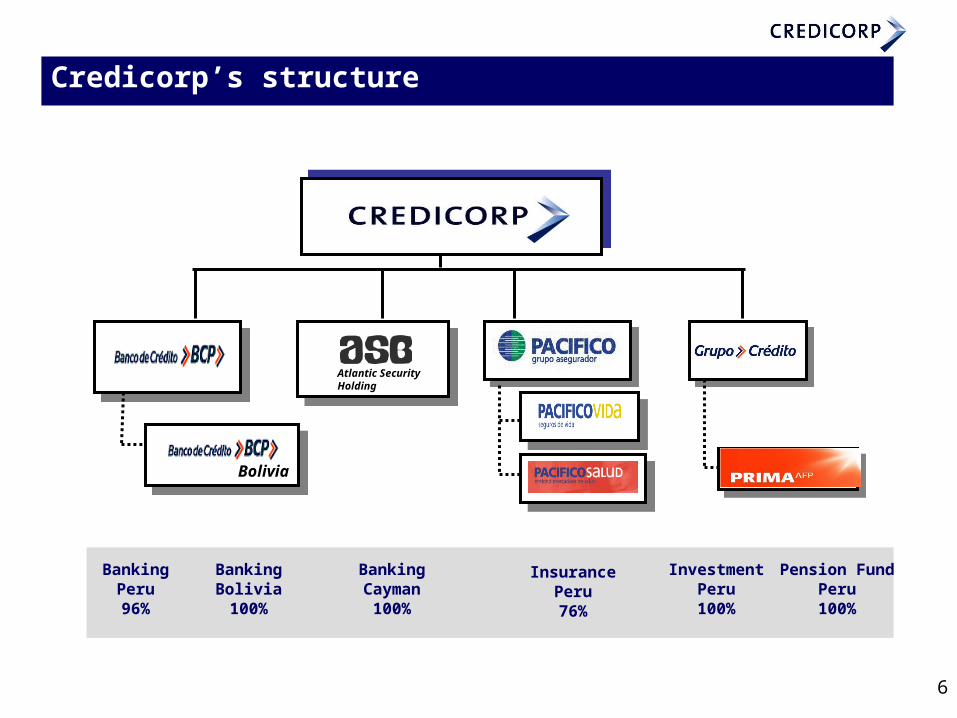

Credicorp’s structure

BoliviaBolivia

BankingPeru96%

BankingBolivia100%

BankingCayman100%

InsurancePeru76%

InvestmentPeru100%

Pension FundPeru100%

Atlantic Security Holding

7

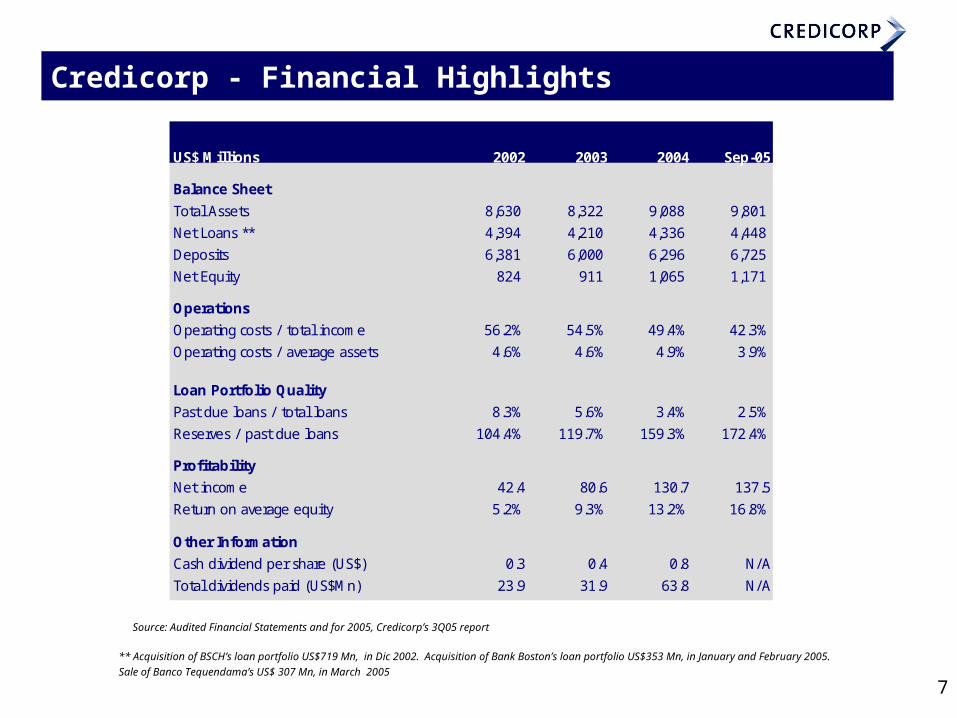

Credicorp - Financial Highlights

US$ Millions 2002 2003 2004 Sep-05

Balance Sheet

Total Assets 8,630 8,322 9,088 9,801

Net Loans ** 4,394 4,210 4,336 4,448

Deposits 6,381 6,000 6,296 6,725

Net Equity 824 911 1,065 1,171

Operations

Operating costs / total income 56.2% 54.5% 49.4% 42.3%

Operating costs / average assets 4.6% 4.6% 4.9% 3.9%

Loan Portfolio Quality

Past due loans / total loans 8.3% 5.6% 3.4% 2.5%

Reserves / past due loans 104.4% 119.7% 159.3% 172.4%

Profitability

Net income 42.4 80.6 130.7 137.5

Return on average equity 5.2% 9.3% 13.2% 16.8%

Other Information

Cash dividend per share (US$) 0.3 0.4 0.8 N/A

Total dividends paid (US$Mn) 23.9 31.9 63.8 N/A

** Acquisition of BSCH’s loan portfolio US$719 Mn, in Dic 2002. Acquisition of Bank Boston’s loan portfolio US$353 Mn, in January and February 2005. Sale of Banco Tequendama’s US$ 307 Mn, in March 2005

Source: Audited Financial Statements and for 2005, Credicorp’s 3Q05 report

8

Agenda

Peruvian Economy

Credicorp Ltd.

Peruvian Financial System

Credicorp’s main subsidiaries

Credicorp’s earnings contributions

Overview

9

2002 2003 2004 Sept05

Loans in dollars (%)Loans in dollars (%) 79.679.6 77.977.9 75.675.6 73.573.5

Deposits in dollars (%)Deposits in dollars (%) 71.571.5 69.569.5 67.167.1 65.965.9

PDL / Loans (%)PDL / Loans (%) 7.67.6 5.85.8 3.73.7 2.72.7

Reserves / PDLs (%)Reserves / PDLs (%) 133.2133.2 141.1141.1 176.4176.4 205.3205.3

ROE (%)ROE (%) 8.48.4 10.910.9 11.311.3 19.519.5

Bank Deposits (US$Bn)Bank Deposits (US$Bn) 13.513.5 13.213.2 14.314.3 16.016.0

Bank Loans (US$Bn)Bank Loans (US$Bn) 10.610.6 10.310.3 10.810.8 11.911.9

Mutul Funds (US$Mn)Mutul Funds (US$Mn) 1,5031,503 2,0072,007 1,7671,767 1,9651,965

Corporate Bonds (US$Mn)Corporate Bonds (US$Mn) 1,1821,182 1,7511,751 2,2932,293 2,3252,325

Peruvian Financial System - Highlights

Source: SBS

10

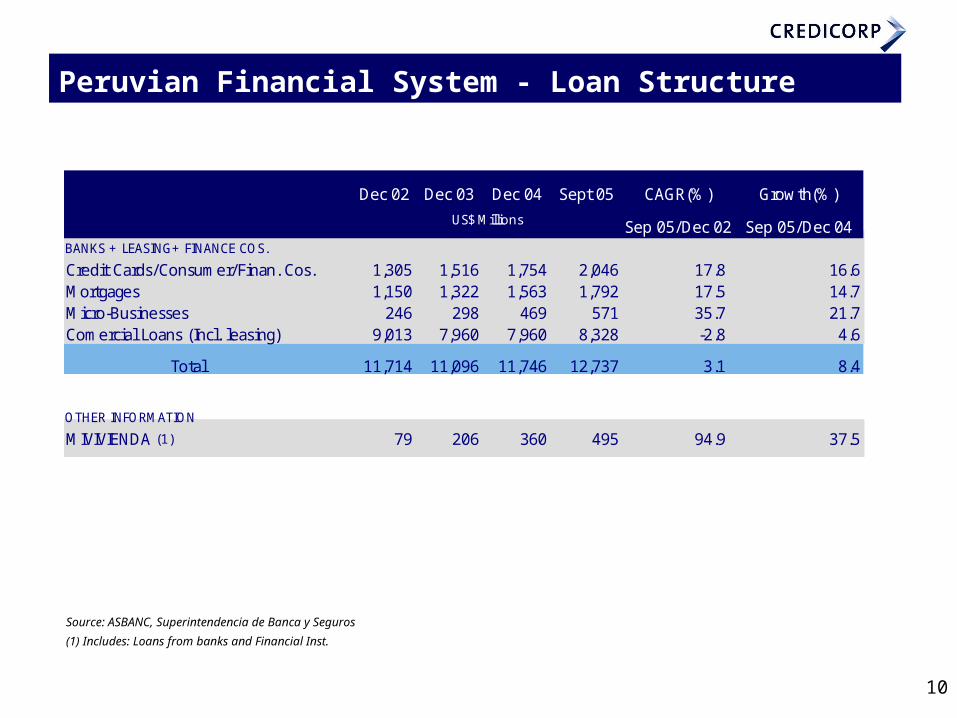

Dec 02 Dec 03 Dec 04 Sept 05 CAGR(%) Growth(%)

Sep 05/Dec 02 Sep 05/Dec 04BANKS + LEASING+ FINANCE COS.

Credit Cards/Consumer/Finan. Cos. 1,305 1,516 1,754 2,046 17.8 16.6Mortgages 1,150 1,322 1,563 1,792 17.5 14.7Micro-Businesses 246 298 469 571 35.7 21.7Comercial Loans (Incl. leasing) 9,013 7,960 7,960 8,328 -2.8 4.6

Total 11,714 11,096 11,746 12,737 3.1 8.4

OTHER INFORMATION

MIVIVIENDA (1) 79 206 360 495 94.9 37.5

US$ Millions

Source: ASBANC, Superintendencia de Banca y Seguros

(1) Includes: Loans from banks and Financial Inst.

Peruvian Financial System - Loan Structure

11

Peruvian Financial System - Market Share (1)

(1) Includes Banks, Finance Institut., Leasing Companies, S&L Regional Institut..

Loan

(%) 2002 2003 2004 Sep-05

BCP 33.6% 31.2% 29.1% 29.0%BBVA 15.2% 16.6% 18.6% 20.2%BWS 17.4% 14.6% 12.8% 12.9%Interbank 7.6% 8.4% 9.0% 8.9%Citibank 4.7% 4.1% 3.4% 4.1%Otros 21.6% 25.1% 27.2% 24.9%

Deposits

(%) 2002 2003 2004 Sep-05

BCP 36.6% 34.1% 31.9% 31.5%BBVA 22.1% 22.4% 24.5% 25.4%BWS 15.5% 15.4% 15.0% 14.7%Interbank 7.4% 8.4% 8.6% 8.4%Citibank 2.8% 2.6% 2.6% 2.6%Otros 15.6% 17.2% 17.3% 17.5%

Source: BCP, SBS Source: BCP, SBS

12

Agenda

Peruvian Economy

Credicorp Ltd.

Peruvian Financial System

Credicorp’s main subsidiaries - BCP Consolidated

- Banco de Credito de Bolivia

- Atlantic Security Holding

- Pacifico Peruano Suiza

- Prima AFP

Credicorp’s earnings contributions

Overview

13

BCP Consolidated : Strategic ApproachBCP Consolidated : Strategic Approach

Market penetration in segments C and D

“Banking made simple”

Transactional Businesses and Services

Highly efficient and profitable distribution network

Excellence in quality service: Leadership

Cost Control, high level of efficiency

14

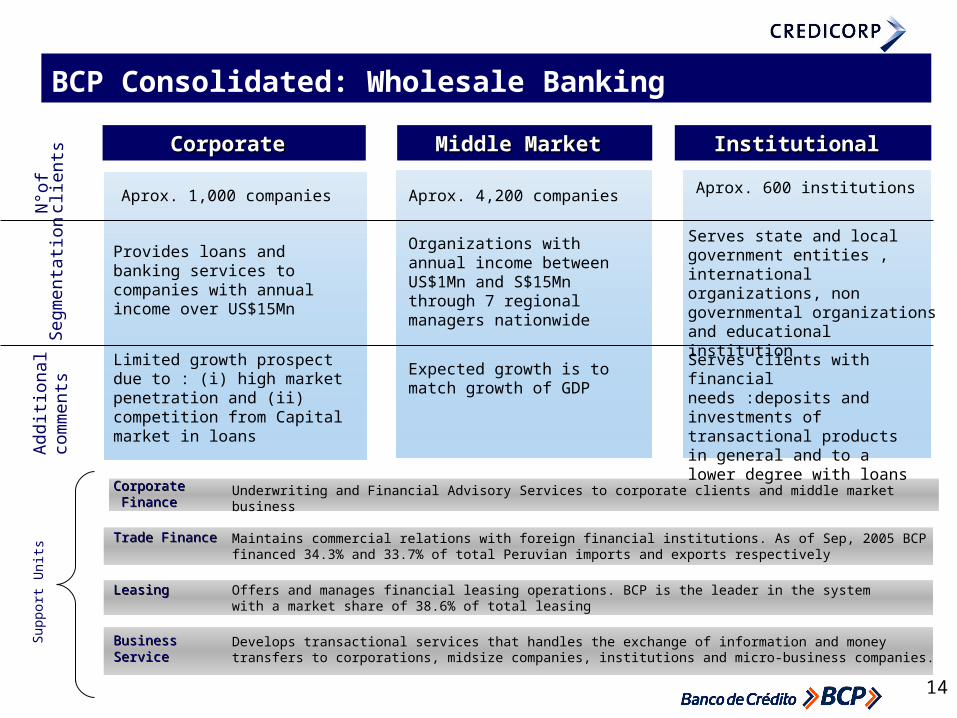

CorporateCorporate Middle Market Middle Market InstitutionalInstitutional

N°o

f cl

ients

Seg

menta

tion

Aprox. 1,000 companies Aprox. 4,200 companies Aprox. 600 institutions

CorporateCorporate Finance Finance

Trade FinanceTrade Finance

LeasingLeasing

Business Business ServiceService

Underwriting and Financial Advisory Services to corporate clients and middle market business

Maintains commercial relations with foreign financial institutions. As of Sep, 2005 BCP financed 34.3% and 33.7% of total Peruvian imports and exports respectively

Offers and manages financial leasing operations. BCP is the leader in the system with a market share of 38.6% of total leasing

Develops transactional services that handles the exchange of information and money transfers to corporations, midsize companies, institutions and micro-business companies.

Provides loans and banking services to companies with annual income over US$15Mn

Organizations with annual income between US$1Mn and S$15Mn through 7 regional managers nationwide

Serves state and local government entities , international organizations, non governmental organizations and educational institution

Limited growth prospect due to : (i) high market penetration and (ii) competition from Capital market in loans

Ad

dit

i onal

com

ments Expected growth is to

match growth of GDP

Serves clients with financial needs :deposits and investments of transactional products in general and to a lower degree with loans

Su

pp

ort

Un

its

BCP Consolidated: Wholesale Banking

15

2000

2500

3000

3500

4000

4500

5000

5500

6000

Mar-03 Jun-03 Set-03 Dec-03 Mar-04 Jun-04 Sep-04 Dic-04 Mar-05 Jun-05 Ago-05

Syst

em L

oan

s (U

S$M

n)

40%

41%

42%

43%

44%

45%

46%

47%

48%

49%

50%

Mar

ket Sh

are

System Loans (US$Mn) Market share

Wholesale Banking Sep-03 Dec-03 Mar-04 Jun-04 Sep-04 Dec-04 Mar-05 Jun-05 Ago-05

Market Share 43.2% 43.5% 43.5% 43.1% 43.4% 42.4% 43.3% 42.3% 45.0%

System Loans 5,274 5,246 5,076 5,515 5,322 5,350 5,684 6,051 5,352

BCP Loans 2,276 2,280 2,208 2,378 2,312 2,269 2,461 2,559 2,406

BCP Consolidated: Market Share Wholesale Banking

16

Consumer Consumer Exclusive Exclusive Small Small Business Business

Micro-Micro-Business Business

N°o

f c

lients

1,653,481 households 54,132 households 8,149 clients 139,004 clients

Segm

enta

tio

n

Offers traditional products to the mass consumer segment

Profitable segment. Generates high volume of business. Segment:US$10 thousand in loans and US$20 thousand in deposits

Serves small and middle market business with annual sales less than US$1Mn

Serves small and micro-business, mostly personal and family businesses, which are offered standard and simple products

CMR / 16.6% Interbank / 13.5% Fincor / 10.3% BBVA / 30.1%BWS / 8.2%Interbank / 6.2%BBVA / 18.5%BWS / 14.5%Interbank / 11.4%Del Trabajo / 10.6%Mi Banco / 11.4%BWS / 5.3%BBVA / 23.2%BWS / 10.3%Interfondos / 15.6%

990Mutual Funds 7.7% 50.7%8.6%

Pyme 210 47.9% 19.8%30.4%

Mortgages 575 21.3%

Mi Vivienda 132 85.9%

% Growth Sep 05 / Sep 04

Loan Vol US$MnProduct

Market share

% Growth Sep 05/Dec

04

Credit Cards 271 19.9% 26.1%9.3%

17.8%

52.1%

Competitors / Mkt shr.

44.1%

27.0%

BCP Consolidated: Retail Banking

Figures as of Sep 2005

17

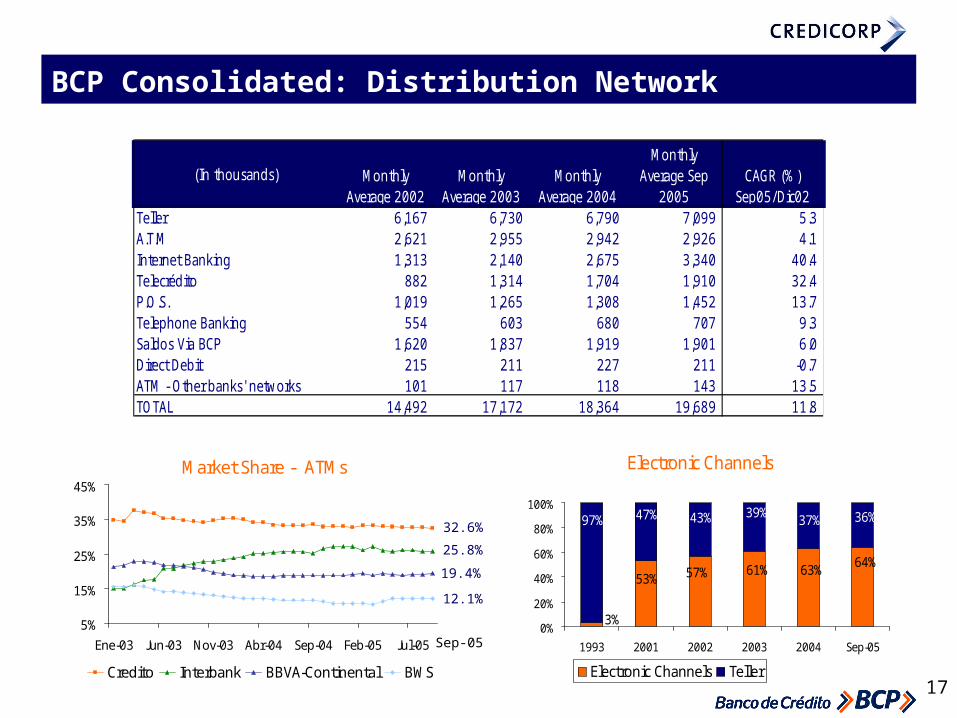

(In thousands) Monthly Average 2002

Monthly Average 2003

Monthly Average 2004

Monthly Average Sep

2005 CAGR (%)

Sep05/Dic02Teller 6,167 6,730 6,790 7,099 5.3 A.T.M 2,621 2,955 2,942 2,926 4.1 Internet Banking 1,313 2,140 2,675 3,340 40.4 Telecrédito 882 1,314 1,704 1,910 32.4 P.O.S. 1,019 1,265 1,308 1,452 13.7 Telephone Banking 554 603 680 707 9.3 Saldos Via BCP 1,620 1,837 1,919 1,901 6.0 Direct Debit 215 211 227 211 -0.7 ATM - Other banks' networks 101 117 118 143 13.5 TOTAL 14,492 17,172 18,364 19,689 11.8

Electronic Channels

64%63%61%57%53%

3%

36%37%97% 47% 43% 39%

0%

20%

40%

60%

80%

100%

1993 2001 2002 2003 2004 Sep-05

Electronic Channels Teller

Market Share - ATMs

5%

15%

25%

35%

45%

Ene-03 Jun-03 Nov-03 Abr-04 Sep-04 Feb-05 Jul-05

Credito Interbank BBVA-Continental BWS

BCP Consolidated: Distribution Network

32.6%

25.8%

19.4%

12.1%

Sep-05

18

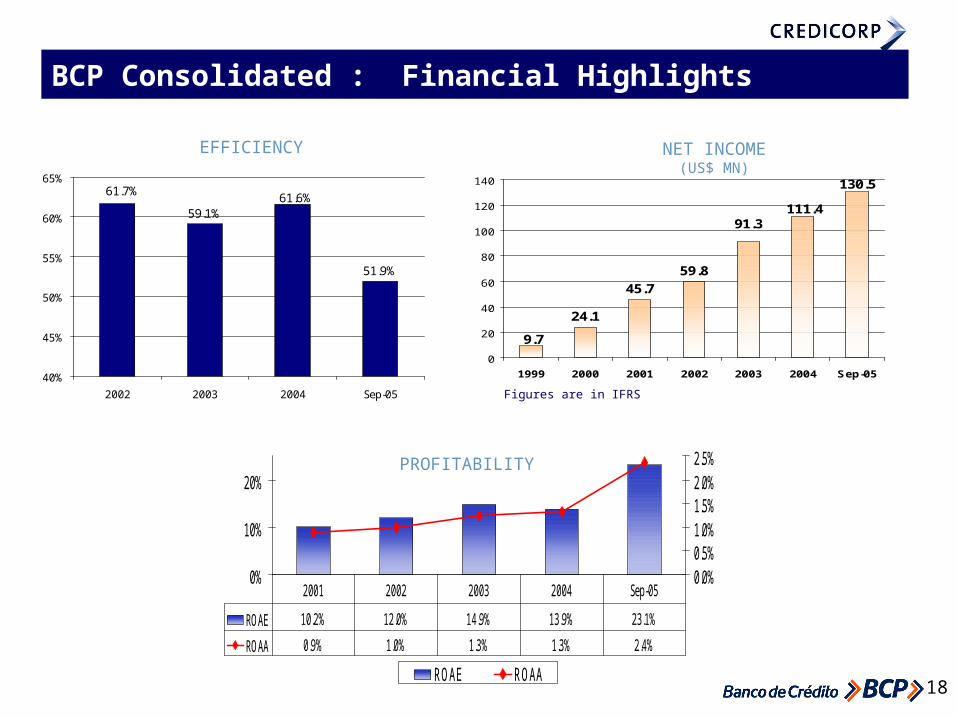

0%

10%

20%

0.0%0.5%1.0%1.5%2.0%2.5%

ROAE ROAA

ROAE 10.2% 12.0% 14.9% 13.9% 23.1%

ROAA 0.9% 1.0% 1.3% 1.3% 2.4%

2001 2002 2003 2004 Sep-05

PROFITABILITY

59.1%

51.9%

61.7% 61.6%

40%

45%

50%

55%

60%

65%

2002 2003 2004 Sep-05

EFFICIENCY

24.1

59.8

9.7

45.7

91.3111.4

130.5

0

20

40

60

80

100

120

140

1999 2000 2001 2002 2003 2004 Sep-05

Figures are in IFRS

NET INCOME(US$ MN)

BCP Consolidated : Financial Highlights

19

Past due Ratio (%) Coverage Ratio (%)

BCP Consolidated : Loan portfolio quality

7.0%

10.0%

13.6%

15.3%17.3%

18.9%

0%

3%

6%

9%

12%

15%

18%

21%

2000 2001 2002 2003 2004 Sep-05

BCP Consolidated

Substandard loans (C+D+E) /Total RiskRatio (%)

8.6

6.1

3.72.6

9.1 8.8

2.7

3.7

5.8

7.6

9.09.8

2000 2001 2002 2003 2004 Sep-05

BCP consolidated

Peruvian BankingSystem

94105 109

125

160

175

133

205

177

141

119

104

2000 2001 2002 2003 2004 Sep-05

20

CTS9%

Demand33%

Time32%

Savings26%

US$ 6,169 Mn

Deposits Loans

Retail36%

Consumer4%

Small Business 10%

Middle Mkt25%

Corporate39%

Credit cards4%

Mortgages18%

US$ 4,479 Mn

Figures as of Sept 2005

BCP Consolidated: Deposits and Loans Structure

21

BCP Peru Dec 02 Dec 03 Dec 04 Sep. 05 % CAGR % Growth

Sep05/Dec02 Sep05/Sep04

Commercial 3,497 2,914 2,762 2,907 -6.5 2.1

Credit cards/Cons. 194 243 271 320 20.0 25.5

Mortgages 347 494 575 707 29.5 29.7

Micro-Businesses 103 141 170 210 29.6 47.9

Total * 4,141 3,792 3,777 4,144 0.0 9.4

BCB 313 310 321 335 2.5 10.9

Total BCP Consol. 4,454 4,102 4,098 4,479 0.2 9.5

US$ Millions

* Acquisition of BSCH’s loan portfolio US$719 Mn, in Dic 2002. Acquisition of Bank Boston’s loan portfolio US$353 Mn, in January and February 2005.

BCP Consolidated: Loans by segment

22

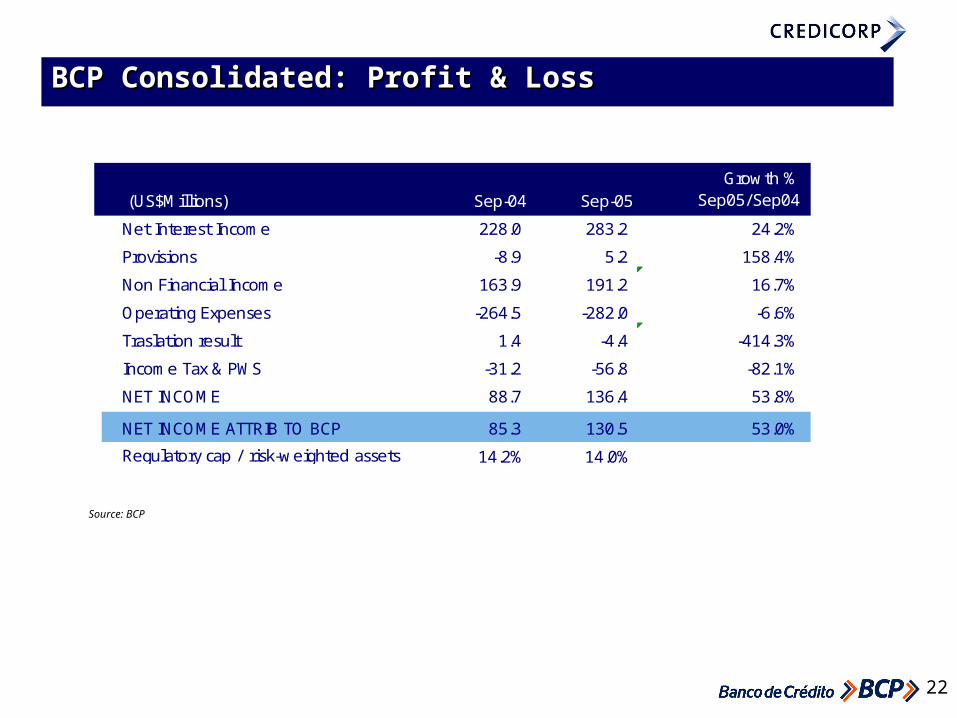

BCP Consolidated: Profit & LossBCP Consolidated: Profit & Loss

(US$Millions) Sep-04 Sep-05Growth %

Sep05/Sep04

Net Interest Income 228.0 283.2 24.2%

Provisions -8.9 5.2 158.4%

Non Financial Income 163.9 191.2 16.7%

Operating Expenses -264.5 -282.0 -6.6%

Traslation result 1.4 -4.4 -414.3%

Income Tax & PWS -31.2 -56.8 -82.1%

NET INCOME 88.7 136.4 53.8%

NET INCOME ATTRIB TO BCP 85.3 130.5 53.0%

Regulatory cap / risk-weighted assets 14.2% 14.0%

Source: BCP

23

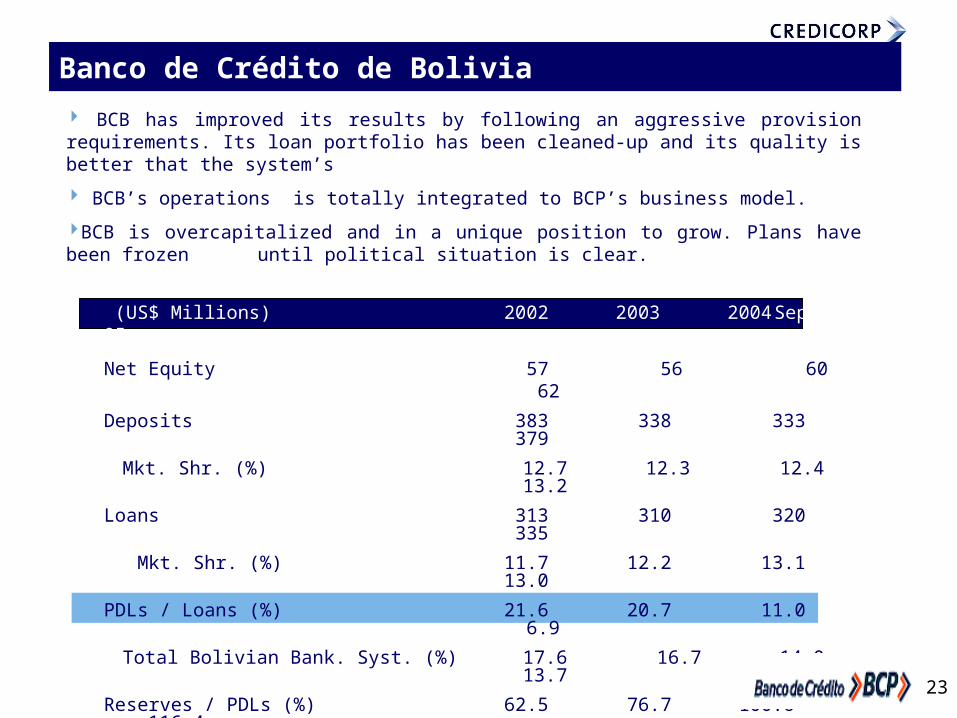

(US$ Millions) 2002 2003 2004 Sep 05

Net Equity 57 56 60 62

Deposits 383 338 333 379

Mkt. Shr. (%) 12.7 12.3 12.4 13.2

Loans 313 310 320 335

Mkt. Shr. (%) 11.7 12.2 13.1 13.0

PDLs / Loans (%) 21.6 20.7 11.0 6.9

Total Bolivian Bank. Syst. (%) 17.6 16.7 14.0 13.7

Reserves / PDLs (%) 62.5 76.7 100.6 116.4

Total Bolivian Banking Syst. (%) 63.7 74.0 84.3 74.7

Net Income 0.0 1.5 4.8 6.5

ROE 0.0% 2.7% 8.4% 14.2%

BCB has improved its results by following an aggressive provision requirements. Its loan portfolio has been cleaned-up and its quality is better that the system’s

BCB’s operations is totally integrated to BCP’s business model.

BCB is overcapitalized and in a unique position to grow. Plans have been frozen until political situation is clear.

BoliviaBanco de Crédito de Bolivia

24

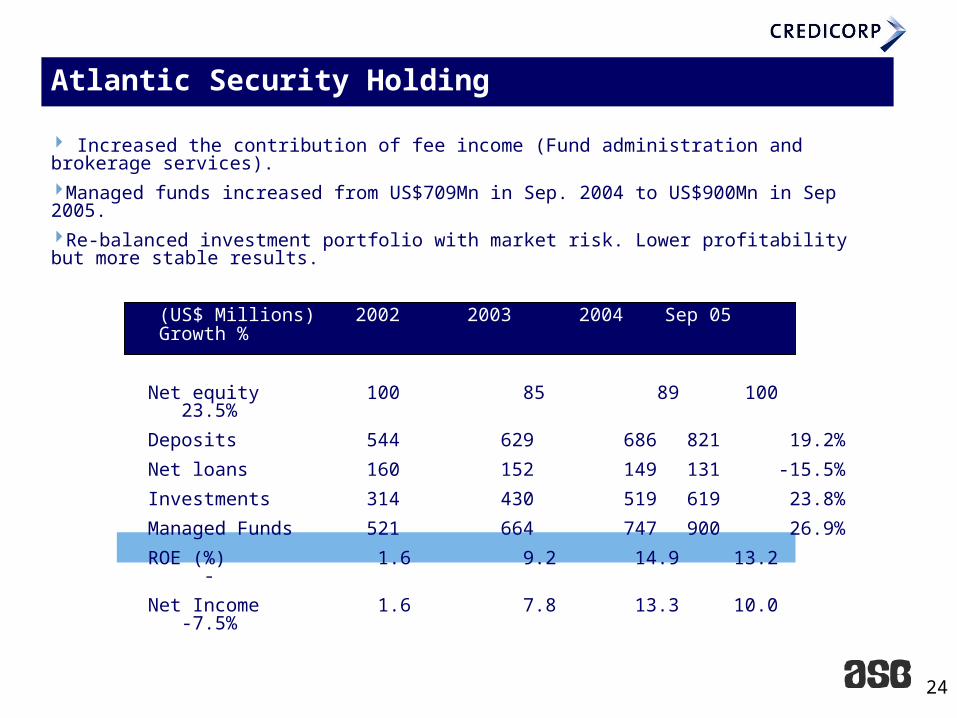

Atlantic Security Holding

(US$ Millions) 2002 2003 2004 Sep 05 Growth %

Sep05/Sep04

Net equity 100 85 89 100 23.5%

Deposits 544 629 686 821 19.2%

Net loans 160 152 149 131 -15.5%

Investments 314 430 519 619 23.8%

Managed Funds 521 664 747 900 26.9%

ROE (%) 1.6 9.2 14.9 13.2 -

Net Income 1.6 7.8 13.3 10.0 -7.5%

Increased the contribution of fee income (Fund administration and brokerage services). Managed funds increased from US$709Mn in Sep. 2004 to US$900Mn in Sep 2005. Re-balanced investment portfolio with market risk. Lower profitability but more stable results.

25

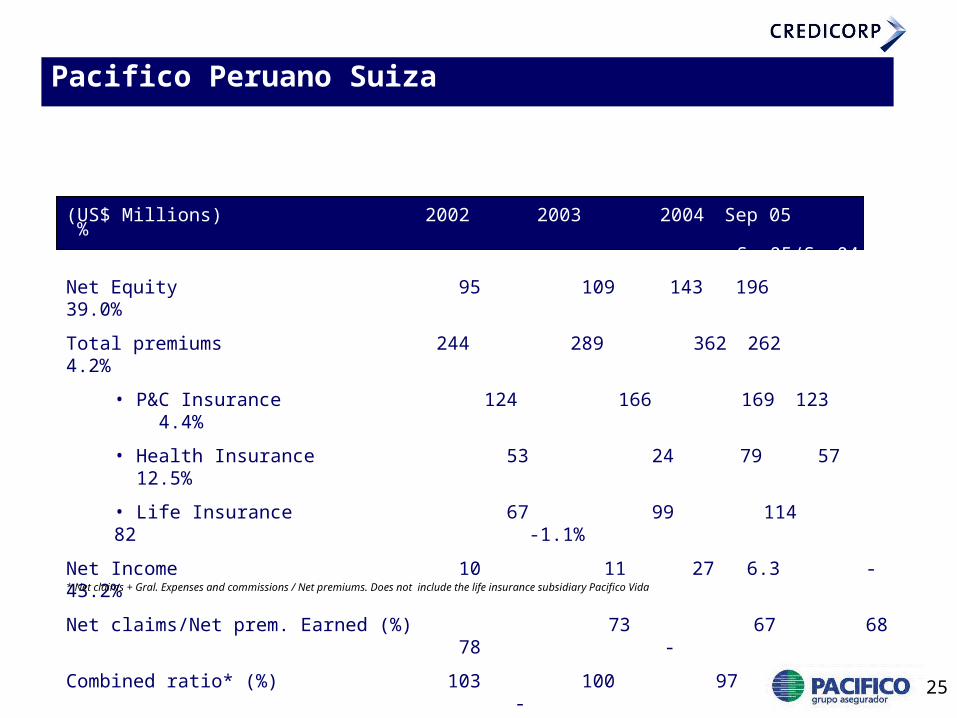

(US$ Millions) 2002 2003 2004 Sep 05 %Sep05/Sep04

Net Equity 95 109 143 196 39.0%

Total premiums 244 289 362 262 4.2%

• P&C Insurance 124 166 169 123 4.4%

• Health Insurance 53 24 79 57 12.5%

• Life Insurance 67 99 114 82 -1.1%

Net Income 10 11 27 6.3 -43.2%

Net claims/Net prem. Earned (%) 73 67 68 78 -

Combined ratio* (%) 103 100 97 102 -

* Net claims + Gral. Expenses and commissions / Net premiums. Does not include the life insurance subsidiary Pacifico Vida

Pacifico Peruano Suiza

26

Higher casualties in the marine hull business during the year. P&C premiums, which represent 47% of total premiums, increased 4.4% from Sept 2004 to

Sept 2005, mainly due to an increase in all of its segments with the exception of premiums in the fire insurance line, which fell 7%.

The annuities line of business is under competitive disadvantage versus other domestic players due to: 1. Our usage of more conservative mortality rate tables than those established by the local

regulators 2. A more conservative fixed income investment policy (minimum rating A).

The health insurance company registered a US$1.5 million provision for reserves during the year as a consequence of recalculating those reserves according to IFRS actuarial practices.

Pacifico Peruano Suiza

27

• Prima AFP has generated higher competition in the Private Pension Fund System.

• Prima’s strategy to introduce low commission rates is based on a low cost and efficient operating structure.

• Its commission rate is 1.5% of workers salary, which is 33% lower than the average commission of the system.

• It started operating in the most relevant cities across the country. Arequipa, Chiclayo, Trujillo and Piura.

• Average net income expected for each year is between US$6 million and US$8 million.

• It is expected to generate US$10 million loss during the year and reach break even in first half of 2007.

• Results reached US$3.5 million loss as of Sep 2005

• The start up capital contributed to Prima is of US$15 million and is expected to

increase by additional US$ 15 million by the end of the year.

Prima AFP

28

Agenda

Peruvian Economy

Credicorp Ltd.

Peruvian Financial System

Credicorp’s main subsidiaries

Credicorp’s earnings contributions

Overview

29

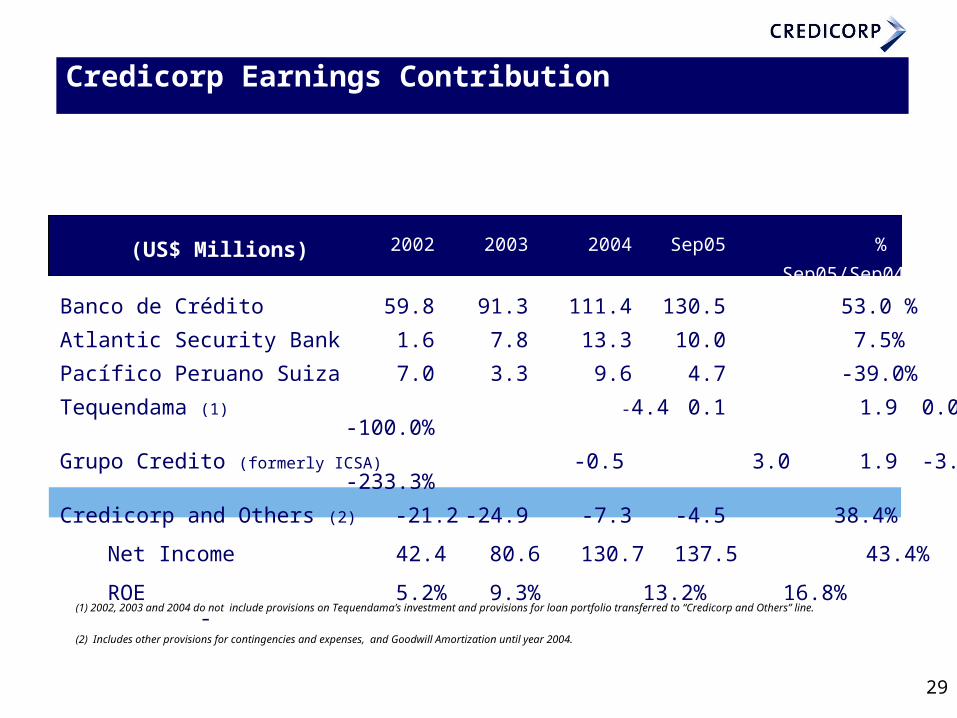

2002 2003 2004 Sep05 %

Sep05/Sep04

Banco de Crédito 59.8 91.3 111.4 130.5 53.0 %

Atlantic Security Bank 1.6 7.8 13.3 10.0 7.5%

Pacífico Peruano Suiza 7.0 3.3 9.6 4.7 -39.0%

Tequendama (1) -4.4 0.1 1.9 0.0 -100.0%

Grupo Credito (formerly ICSA) -0.5 3.0 1.9 -3.1 -233.3%

Credicorp and Others (2) -21.2 -24.9 -7.3 -4.5 38.4%

Net Income 42.4 80.6 130.7 137.5 43.4%

ROE 5.2% 9.3% 13.2% 16.8% -

(US$ Millions)

(1) 2002, 2003 and 2004 do not include provisions on Tequendama’s investment and provisions for loan portfolio transferred to “Credicorp and Others” line.

(2) Includes other provisions for contingencies and expenses, and Goodwill Amortization until year 2004.

Credicorp Earnings Contribution

30

Agenda

Peruvian Economy

Credicorp Ltd.

Peruvian Financial System

Credicorp’s main subsidiaries

Credicorp’s earnings contributions

Overview

31

Credicorp’s results are ahead of our expectations:

Positive trends in banking subsidiaries.

Lower provisioning requirements for BCP’s loan portfolio, higher net interest income and growth of fee income.

Rigid operating cost control in BCP

ASH will continue to concentrate on increasing its fee income related to its wealth management business and maintaining a lower risk profile in its proprietary investment.. Atlantic’s ROE is 13%

BCB’s has improved its results due to lower provisioning requirements PDL and Coverage ratios are better than the system’s. BCB’s ROE reached 14% during the first nine months of the year compared to 6% reached in the same period a year ago.

PPS had a negative impact in the marine hull business due to higher casualties during the first two quarters of the year. Consolidated total premiums increased during the first nine months of the year mainly in P&C business and Health insurance segment.

Prima AFP started its operations in August. With a low cost strategy, the company offers to its customers competitive rates with value added services. Prima’s commission rate is 33% lower than the average of the system. Prima AFP will generate US$10 million loss during the year. Break even will be reached at first half of 2007.

Overview

32

Safe Harbor for forward-looking statements

This material includes “forward-looking statements” within the meaning of Section 21E of the Securities Exchange Act of 1934. All statement other than statements of historical information provided herein are forward-looking and may contain information about financial results, economic conditions, trends and known uncertainties.

The Company cautions readers that actual results could differ materially from those expected by the Company, depending on the outcome of certain factors, including, without limitation: (1) adverse changes in the Peruvian economy with respect to the rates of inflation, economic growth, currency devaluation, and other factors, (2) adverse changes in the Peruvian political situation, including, without limitation, the reversal of market-oriented reforms and economic recovery measures, or the failure of such measures and reforms to achieve their goals, and (3) adverse changes in the markets in which the Company operates, including increased competition, decreased demand for financial services, and other factors. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof.

The Company undertakes no obligation to release publicly the result of any revisions to these forward-looking statements which may be made to reflect events or circumstances after the date hereof, including, without limitation, changes in the Company’s business strategy or planned capital expenditures, or to reflect the occurrence of unanticipated events.

33

CREDICORP

November, 2005