29

1 Daniel Felsenstein Eyal Ashbel Simultaneous Modeling of Developer Behavior and Land Prices in UrbanSim UrbanSim European Users Group meeting, ETH Zurich, 17-18 th March 2008

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 215 times |

| Download: | 0 times |

1

Daniel Felsenstein

Eyal Ashbel

Simultaneous Modeling of Developer Behavior and Land Prices in UrbanSim

Simultaneous Modeling of Developer Behavior and Land Prices in UrbanSim

UrbanSim European Users Group meeting, ETH Zurich, 17-18th March 2008

2

The Motivation

The Motivation

• In UrbanSim, interdependence between developer behavior and land prices is noted.

• Interdependence between dev.behav/land prices and h’hold and job location choice, is also noted.

• However, in the model developer behavior and land prices are modeled independently.

• In practice, the two occur simultaneously

3

Motivation cont.

Motivation cont.

• UrbanSim models assumes prices are exogenous to interaction between buyers and sellers (their individual transactions are too small to affect aggregate prices).

• But much urban economics points to endogeneity issue: developer behavior depends on land prices and land prices depend on developer behavior

• Issue of endogeneity means dealing with:

– Correct identification of models (error structures)

– Instrumentation

– Dynamics

4

Motivation cont 2.

Motivation cont 2.

• Dynamics in current land price model: cross-section simulation of end-of-the-year-prices based on updated cell characteristics (from developer model, h’hold and jobs location choices and transport model).

• These land prices then influence h’holds, jobs, developer behavior in next year: back-door endogeneity?

• Prices also fixed by expectations of price (rational expectations world)

5

TheoryTheory

Relative PriceRelative Price QuantityQuantity

itB

A

it

it

P

P L

LA

B

A

P

P

L

LA

AB

D

S' (π+1= π)

S'' (π+1> π)

6

SupplySupply

itite1ititiit UλZγπβπασ

itititit VXπd

Z, X = vectors of variables that cause supply/demand curves to shift

general price is sum of parcel prices.

n

1iitittit w;θ

itit d

(–)

(+)DemandDemand

Equilibrium

Equilibrium

7

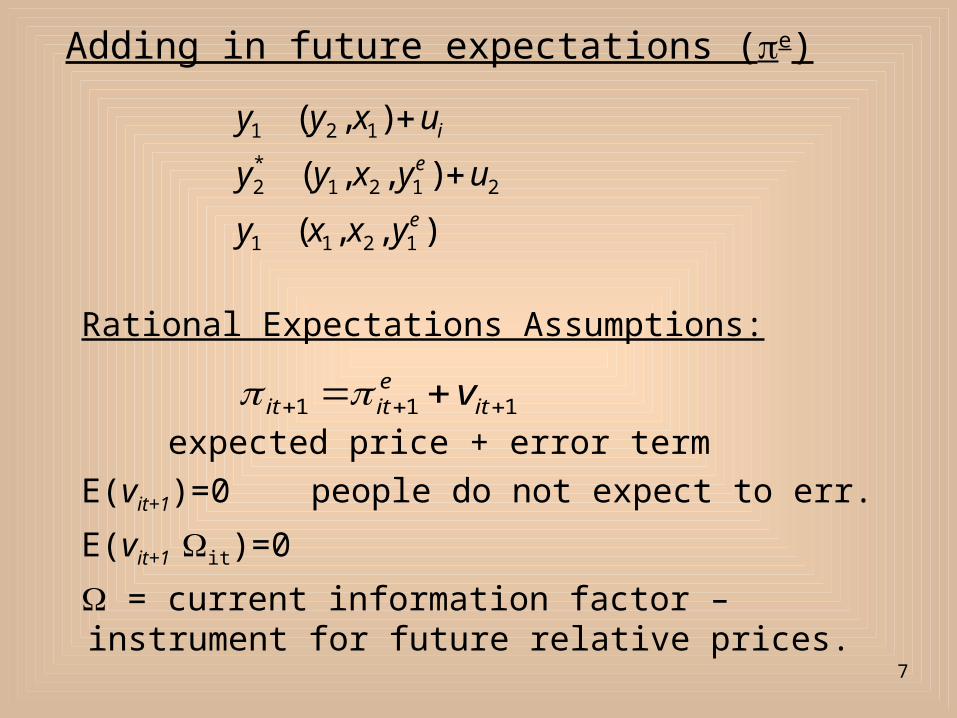

Rational Expectations Assumptions:

expected price + error termE(vit+1)=0 people do not expect to err.

E(vit+1 it)=0

= current information factor – instrument for future relative prices.

Adding in future expectations (e)

),,(

),,(

),(

1211

2121*2

121

e

e

i

yxxy

uyxyy

uxyy

111 iteitit v

8

Adding time factor to future expectations:

yt=xt+[yt+1-vt+1]+ut E(vt+1,ut)=0

=xt+yt+1+ut- vt+1 E(yet+1)<0

IV: yt+1 , xt , vt+1

1te

1t1t

te

1ttt

vyy

uyxy

9

Estimation StrategyEstimation Strategy

Maddala (1983): simultaneous equationsUse probit two-stage least squares (P2SLS)CDSIMEQ routine (STATA Journal 2003)

111

*211 uyy X

22212*2 uyy X

Land price model (OLS)

Developer model (probit)

10

1. Simultaneous equations

2. y*2 is not observed,

rewrite (1) and (2) as

3. Estimate reduced form

4. Extract predicted values

5. Plug-in fitted values and adjust covariance matrix

)2(

)1(

22212*2

111*211

uyy

uyy

X

X

)4(

)3(

2

22

2

21

2

2**2

111**

2211

u

yy

uyy

X

X

)6(

)5(

222**

2

1111

vy

vy

X

X

)8(ˆˆ

)7(ˆˆ

2**

2

11

X

X

y

y

)10(ˆ

)9(ˆ

22212**

2

111**

211

uyy

uyy

X

X

11

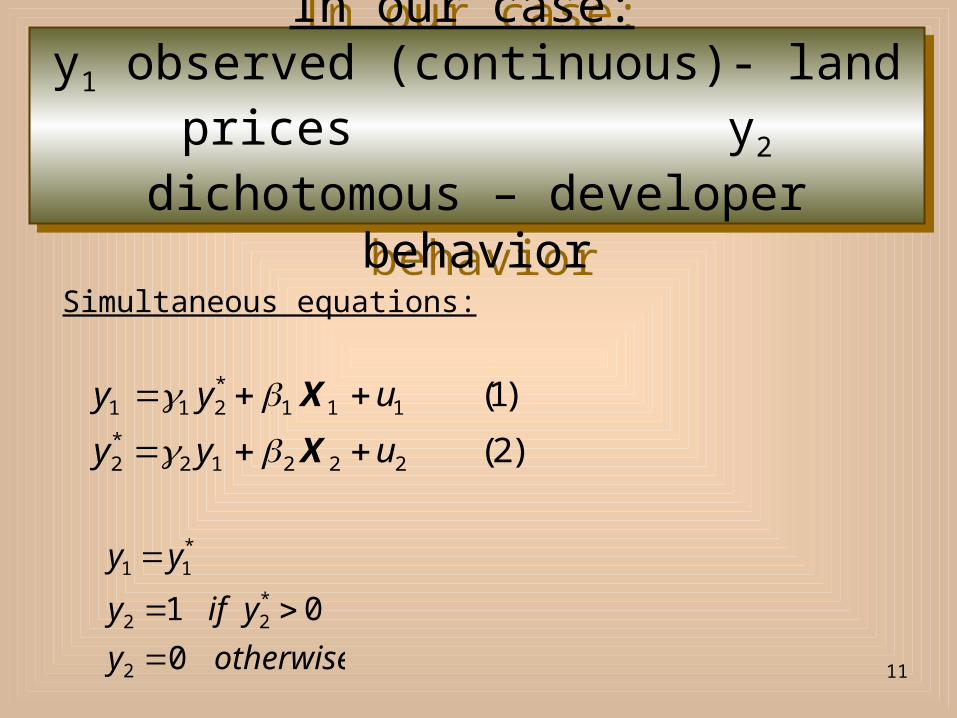

In our case: y1 observed (continuous)- land prices y2 dichotomous –

developer behavior

In our case: y1 observed (continuous)- land prices y2 dichotomous –

developer behavior

otherwisey

yify

yy

0

01

2

*22

*11

)2(

)1(

22212*2

111*211

uyy

uyy

X

X

Simultaneous equations:

12

As is not observed (ie only observed as a dichotomous variable), equations (1) and (2) are re-written:

*2y

)4(

)3(

2

22

2

21

2

2**2

111**

2211

u

yy

uyy

X

X

This has implications for standard errors that will need to be corrected later on.

13

Stage 1: (estimated by OLS and probit): models fitted using all exogenous variables. Predicted values obtained.

)6(

)5(

222**

2

1111

vy

vy

X

X

)8(ˆˆ

)7(ˆˆ

2**

2

11

X

X

y

y

From these reduced-form estimates, predicted values from each model are obtained for use in Stage 2.

Two-stage Estimation Two-stage Estimation

X= matrix of all exogenous variables

Π1’Π2,= vectors of parameters to be estimated

14

Two-stage Estimation cont.

Two-stage Estimation cont.

Stage 2: (estimated by OLS and probit): original endogenous variables in (3) and (4) are replaced by their fitted values from (7) and (8).

1**

2 ˆ,ˆ yy

Finally, need correction for standard errors (adjustment of the variance- covariance matrix) as models based on

and not on the appropriate

)10(ˆ

)9(ˆ

22212**

2

111**

211

uyy

uyy

X

X

1**

2 , yy

15

Estimated Results - Example

Estimated Results - Example

Land PricesDeveloper Behavior 2 -(-1), Residential – no

further developmentConstant 12.43**

Developer Behavior 0.541*

Travel time CBD -0.00253**

Percent water -0.00710 **

ln resid. units walking dist -0.0808**

ln resid. units 0.104**

ln distance highway 0.0468**

ln commercial sq. ft. 0.0199**

Mixed Use 1.477**

Residential -2.377 **

Constant 4.113*

ln land prices -0.1300Access to arterial hwy. -0.5499*

Recent transitions to resid. (walking dist) -0.58853Recent transitions to same type (walking dist) -1.4915**

Percent mixed use (walking dist) 0.5465*

Percent same type cells (walking dist)0.01518*

ln resid. units -0.8261**

-2log likelihood -N 2,919R2 0.73LR X2 -

-57.634238

-

214.5(p<0.000)

16

Tel Aviv Metropolitan Area

Tel Aviv Metropolitan Area

• 1,683 sq km. • Three million

inhabitants.• One million employees• 49 % National GNP.• 60 local authorities

(city governments)

17

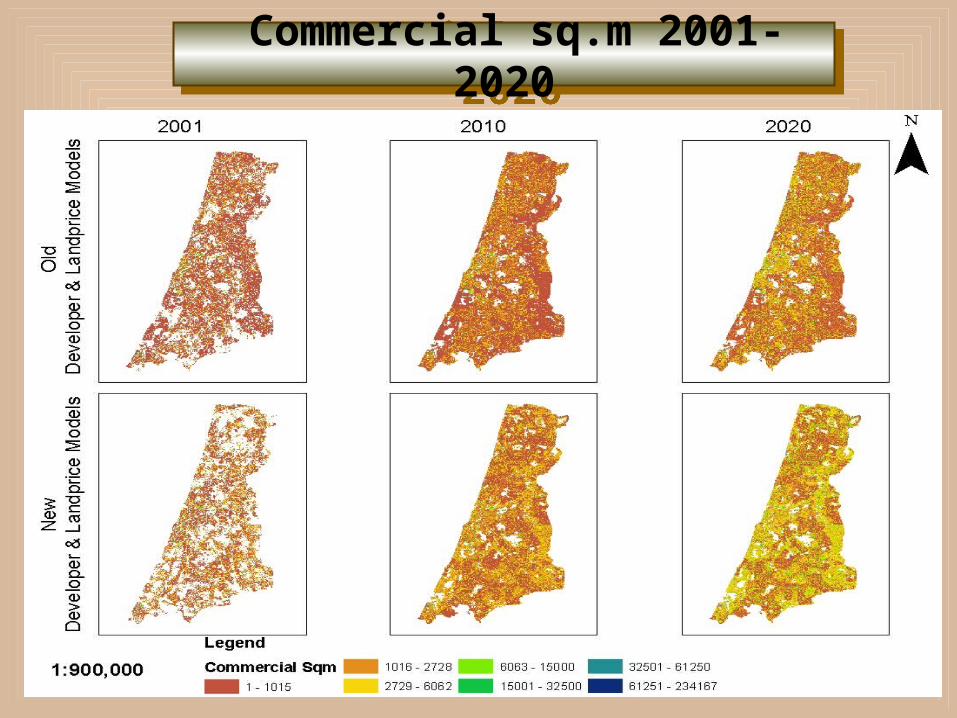

Commercial sq.m 2001-2020

Commercial sq.m 2001-2020

18

Non- residential land values, 2001-2020

Non- residential land values, 2001-2020

19

Non-residentialNon-residential

• Non-resid sq m: development starts later but reaches more extreme values

• Similar trends to individual model estimation. Accentuated suburban non-residential development

• Simultaneous estimation makes for more extreme values in non- resid land prices. Less smooth price gradient

20

Density – persons per grid cell, 2001-2020

Density – persons per grid cell, 2001-2020

21

Residential Land Values, 2001-2020

Residential Land Values, 2001-2020

22

ResidentialResidential

• Simultaneous estimation predicts more population deconcentration.

• Residential land values are estimated to be higher in suburban locations than in CBD (using simultaneous estimation)

• Individual estimation gives opposite picture: higher residential prices closer to CBD

23

Local Authorities within the Metro Area

Local Authorities within the Metro Area

24

City Name Delta 2001 Delta 2010 Delta 2020 Delta 2001 Delta 2010 Delta 2020Ra'anana 17% 0% 1% 4% 1% 5%Petah Tikva -3% 11% -2% 1% 1% 2%Netanya 5% 2% -4% 1% 2% 1%Rehovot 0% 9% 2% 1% -1% 2%Rishon Leziyon -6% 17% 2% 1% 0% 1%Ashdod 2% 8% 10% 3% 1% 2%Tel Aviv 5% 5% 1% 2% 3% 1%

Average Income Households

Delta=(new-old)/new

Households Data

25

Grid Cells Data

City Name Delta 2001 Delta 2010 Delta 2020Ra'anana -22% -4% 0%Petah Tikva 21% 28% 30%Netanya 3% 15% 17%Rehovot 27% 27% 27%Rishon Leziyon 20% 31% 34%Ashdod 24% 34% 40%Tel Aviv 8% 14% 13%

Commercial Sqm

26

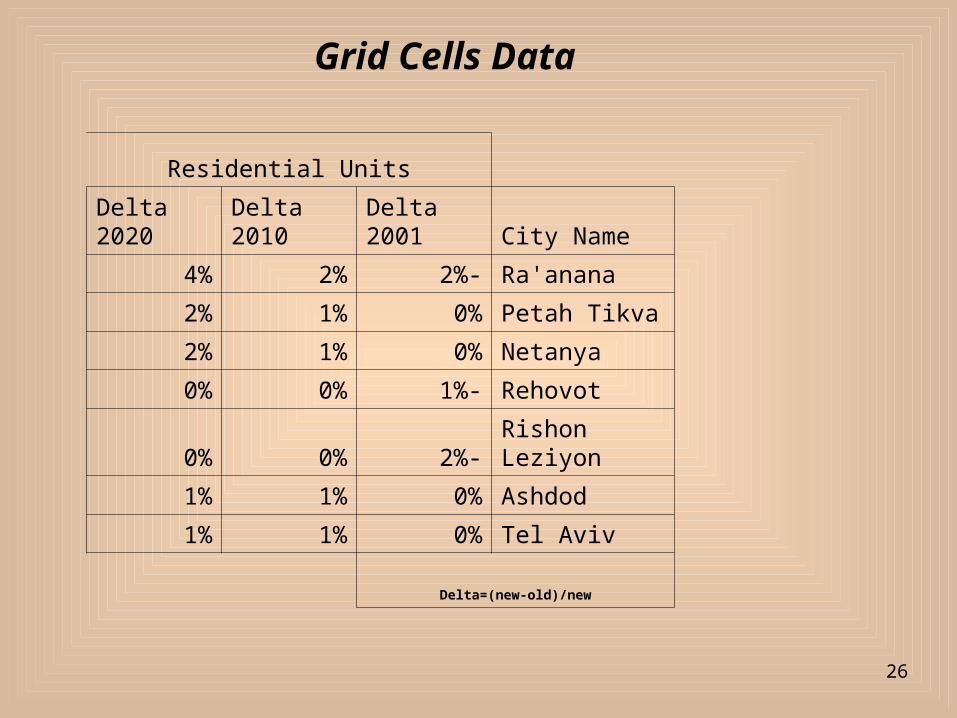

Grid Cells Data

Residential Units

City NameDelta 2001

Delta 2010

Delta 2020

Ra'anana-2%2%4%Petah Tikva0%1%2%Netanya0%1%2%Rehovot-1%0%0%Rishon Leziyon-2%0%0%Ashdod0%1%1%Tel Aviv0%1%1%

Delta=(new-old)/new

27

Grid Cells Data

Fraction Residential

City NameDelta 2001

Delta 2010

Delta 2020

Ra'anana-30%5%5%Petah Tikva-10%5%5%Netanya-7%2%2%Rehovot-20%-2%-2%Rishon Leziyon-23%-1%-2%Ashdod-9%-3%-4%Tel Aviv0%1%1%

Delta=(new-old)/new

28

Results for Individual Local Authorities

Results for Individual Local Authorities

• Results tend to stabilize over the longer term (2020)

• Households data: simultaneous estimation generally yields higher outcomes (positive deltas) than individual estimation.

• Changes in attributes of cells: estimates of changes in non-residential cells (units, area) much more volatile than for residential cells. Confirms results relating to land values.

• Southern local authorities estimated gains much more in non-residential units than in residential (implications for fiscal independence).

29

ConclusionsConclusions

• Avoiding endogeneity in price fixing= the easy way out?

• Explicit treatment of prices in UrbanSim- can this be improved? (Prices respond at the end of the year to grid cell characteristics of location, balance of supply an demand at each location)

• Price expectations need to be included (need credible instrument)

• Is this more suited to UrbanSim4?