32

1 German Manzano UNICA – IPCVA IFFA 07-05-2007 Argentine Beef Industry Argentine Beef Industry Vision and Vision and perspectives perspectives

| Date post: | 26-Dec-2015 |

| Category: |

Documents |

| Upload: | abigayle-francis |

| View: | 215 times |

| Download: | 0 times |

1

German ManzanoUNICA – IPCVAIFFA 07-05-2007

Argentine Beef Industry Argentine Beef Industry Vision and perspectives Vision and perspectives

2

Topics

• Global Beef Production and Trade• Future Opportunities and challenges

3

Global Beef Trade

4

Brazil2004 1,63

2005 1,87

2006 (prov.) 1,87

Australia2004 1,39

2005 1,41

2006 (prov.) 1,42India

2004 0,50

2005 0,63

2006 (prov.) 0,75

New Zealand2004 0,61

2005 0,59

2006 (prov.) 0,54Argentina2004 0,62

2005 0,75

2006 (prov.) 0,56

Canada2004 0,56

2005 0,55

2006 (prov.) 0,46

Uruguay2004 0,40

2005 0,48

2006 (prov.) 0,52

USA2004 0,21

2005 0,32

2006 (prov.) 0,52

World beef exporters

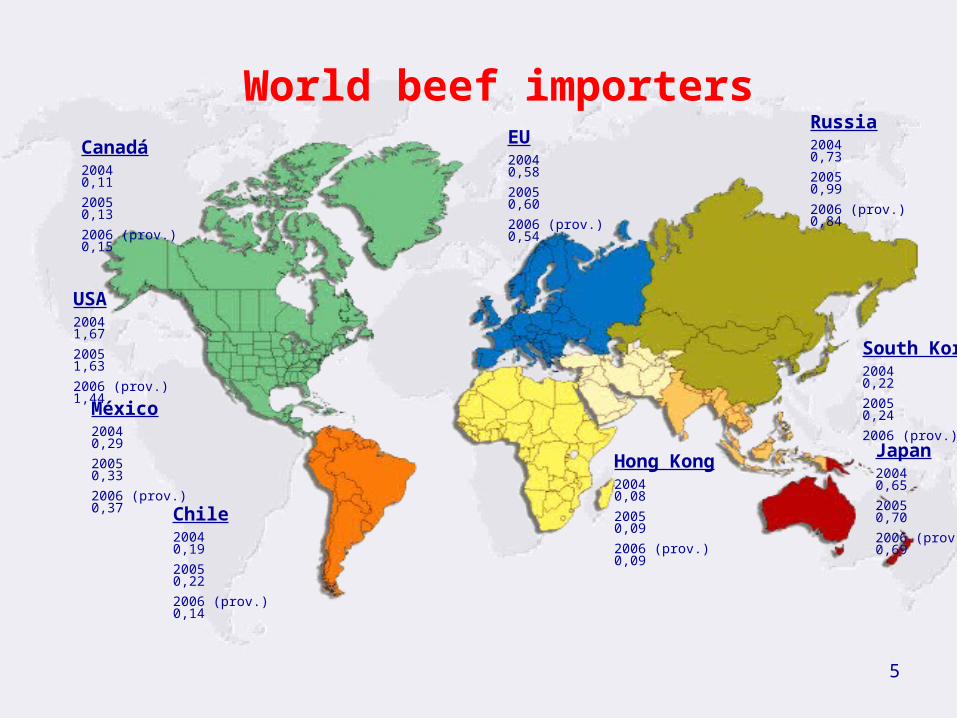

5

Russia2004 0,73

2005 0,99

2006 (prov.) 0,84

Japan2004 0,65

2005 0,70

2006 (prov.) 0,69

EU2004 0,58

2005 0,60

2006 (prov.) 0,54

USA2004 1,67

2005 1,63

2006 (prov.) 1,44

Chile2004 0,19

2005 0,22

2006 (prov.) 0,14

Hong Kong2004 0,08

2005 0,09

2006 (prov.) 0,09

México2004 0,29

2005 0,33

2006 (prov.) 0,37

South Korea2004 0,22

2005 0,24

2006 (prov.) 0,19

Canadá2004 0,11

2005 0,13

2006 (prov.) 0,15

World beef importers

6

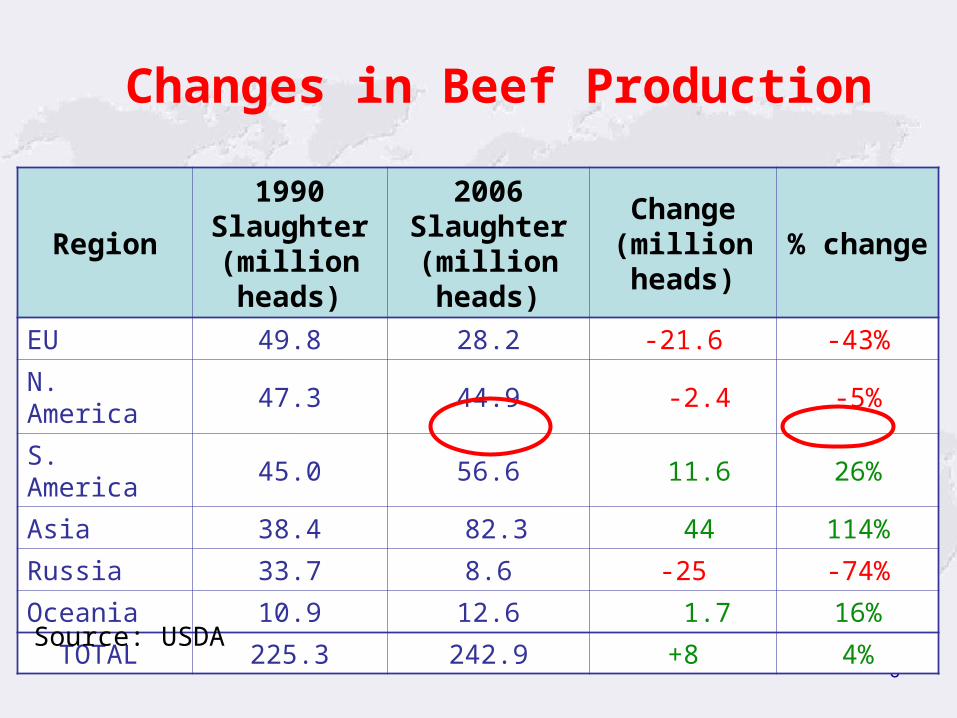

Changes in Beef Production

Region

1990 Slaughter (million heads)

2006 Slaughter (million heads)

Change (million heads)

% change

EU 49.8 28.2 -21.6 -43%

N. America 47.3 44.9 -2.4 -5%

S. America 45.0 56.6 11.6 26%

Asia 38.4 82.3 44 114%

Russia 33.7 8.6 -25 -74%

Oceania 10.9 12.6 1.7 16%

TOTAL 225.3 242.9 +8 4%

Source: USDA

7

Mercosur facts

Facts Brazil Argentina Uruguay Paraguay

Cattle (million hd) 204 55 12 10

Slaughter (million hd) 38 13 3 2

Production (mill tons) 8,800 3,000 0.650 0.330

Consumption (kgs pc) 33 62 26 25

Exports (million tons) 1,900 0.600 0.500 0.200

Total slaughterhouses 1400 480 26 30

National habilitation 750 260 26 12

Export habilitation 480 90 22 6

Steer prices (usdkg) 0.83 0.76 0.98 0.81

Source: own estimates

8

Global Beef Trade Top 10

9

2006 World Beef Production – Top 10Rank Country Total Production

million MT (CWE)

1 U.S. 11.9

2 Brazil 8.85

3 EU-25 7.88

4 China 7.5

5 Argentina 3.1

6 India 2.37

7 Mexico 2.17

8 Australia 2.15

9 Russia 1.46

10 Canada 1.37Source: USDA

10

2006 World Beef Consumption – Top 10

Ranking Country Total Consumption million tons (CWE)

1 U.S. 12.8

2 EU-25 8.22

3 China 7.4

4 Brazil 6.9

5 Argentina 2.6

6 Mexico 2.5

7 Russia 2.3

8 India 1.6

9 Japan 1.2

10 Canada 1.0

Source: USDA

11

2006 World Beef Exports – Top 10Rank Country Exports 000 MT

1 Brazil 1,903

2 Australia 1,140

3 U.S. 656

4 Argentina 600

5 Uruguay 500

6 India 485

7 New Zealand 412

8 Canada 370

9 Paraguay 202

10 Nicaragua 52

Source: USDA estimates

12

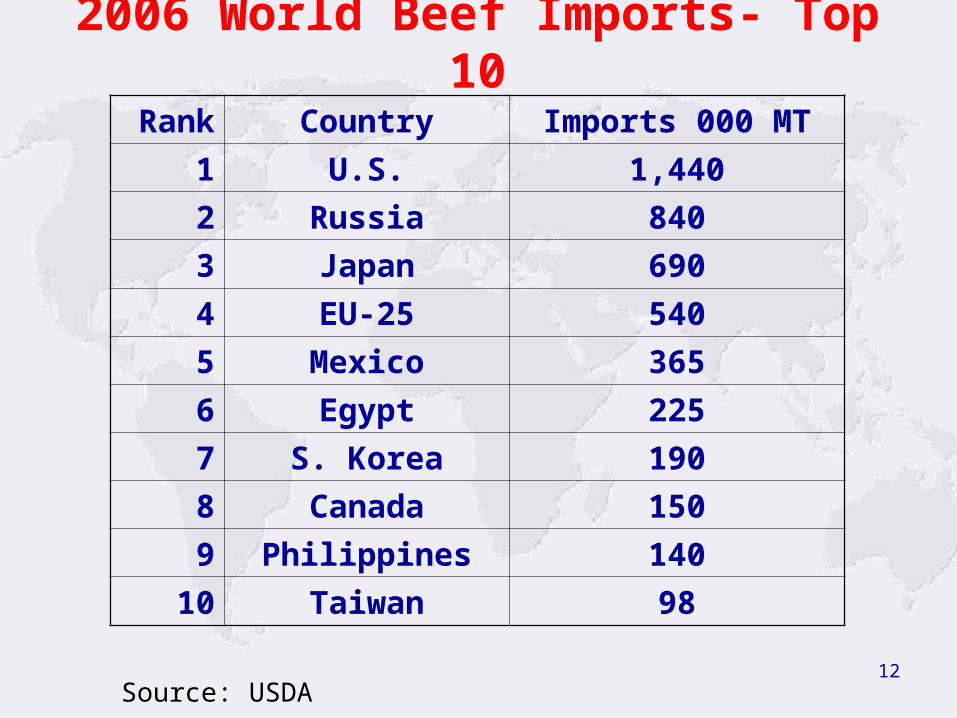

2006 World Beef Imports- Top 10

Rank Country Imports 000 MT

1 U.S. 1,440

2 Russia 840

3 Japan 690

4 EU-25 540

5 Mexico 365

6 Egypt 225

7 S. Korea 190

8 Canada 150

9 Philippines 140

10 Taiwan 98

Source: USDA

13

Beef Trends Projections

14

World Beef Trends

• Increasing costs of production• Growing focus on attributes of end

product• Consumer driven production and focus

on niche marketing• Small but growing demand for natural

and organic beef• Focus on food safety and animal

disease prevention

15

Mercosur potential growth

Facts BrazilArgentin

aUruguay Paraguay

Cattle (million hd) 204 55 12 10

Slaughter (million hd) 38 13 3 2

Production (mill tons) 8,800 3,000 0.650 0.330

Consumption (kgs pc) 33 62 26 25

Exports (million tons) 1,900 0.600 0.500 0.200

Total slaughterhouses 1400 480 26 30

National habilitation 750 260 26 12

Export habilitation 480 90 22 6

Steer prices (usd/kg) 0.83 0.76 0.98 0.81

Source: own estimates

16

World Population GrowthWorld Population Growth

0

1

2

3

4

5

6

7

'50 '55 '60 '65 '70 '75 '80 '85 '90 '95 '00

Billion

0123456789

10

'05 '10 '15 '20 '25 '30 '35 '40 '45 '50

Billion

HistoricalHistorical

Projected

Double 1980 by 2050

17

Red Meat Consumption – FAO Estimates

Source: OECD/FAO

0

50

100

150

200

250

mill

ion

me

tric

to

ns

2006 est 2014 est 2030 est

PorkLambBeef

+14%

+28%

% change from 2006

An increase of over 25 million mtons by 2014

18

Growth Trend Projections Beef Production

0

2000

4000

6000

8000

10000

12000

14000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

00

0 M

T

U.S.

Brazil

China

EU-25

India

Argentina

Australia

Canada

Mexico

N. Zealand

Source: OECD/FAO

19

Growth Trend Projections

Beef Consumption

0

2000

4000

6000

8000

10000

12000

14000

'00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15

00

0 M

T

U.S.

China

Brazil

EU-25

India

Russia

Argentina

Mexico

Japan

Source: OECD/USMEF

20

Growth Trend Projections Beef exports

0

500

1,000

1,500

2,000

2,50020

05

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

Brazil

Australia

New Zealand

United States

Argentina

Canada

Source: USDA; thousand MT (CWE)

21

Growth Trend ProjectionsBeef Imports

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2005

2007

2009

2011

2013

2015

United States

Russia

Japan

EU-25

Mexico

Egypt

South Korea

Canada

Source: USDA; thousand MT (CWE)

22

Foods market trends

Product Level Organoleptic Time Price %

Delicatessen high optimun no no 5-10 medium natural light Standard medium flavour-colour short yes 60-70 taste

Commodities low nutritician no much 20-30

23

Consumers driver’s

• Consumer trust• Brands• Sophisticated markets• Ethical brands• Natural and organic production and standards• Food safety• Nutritional value • Industry image

24

Future opportunities and challenges

25

High-priority subjects

• Installed capacity advantage

• Product development

• Add value and shell life

• By-products advantage

• Quality

• Food safety

• Logistic

26

Installed capacity advantage

• Coordination (Contracts of supplying)

• Informal slaughter elimination

• Internal export-market integration

• Increase capacity of debonning

• Concentration (Integration)

• Increase slaughtering weight

27

Add value and shell life

• Capacity of cold and maturation of beef carcass

• Portion control and special packing (supermarkets, hotels, etc)

• News packing materials (fresh pack)

• Cooked beef

• Commercial sterilization

• Cured and smoked products

28

By-products advantage

• Edible products (offals)

• Industrial use (tallow, blood, leather and bones)

• Opoterapics (glands)

• Pet foods

• Risk material (marrow, brains)

29

Quality

• Cattle and cuts evaluation systems

• Desensitizing methods

• Tenderness process

• Quality audits to correct defects

• Uniform and consistence quality

30

Food safety

• Control of microorganisms

• Conservation at low temperatures

• Alternatives in vacuum packaging

• Microbiological criteria of food safety

• Standardized Norms (SSOP, BMP, HACCP, QUACP, ISO)

31

Logistic

• Cattle trazability

• Product identification

• Animal wellfare in the cattle transport

• Beef cuts transport

• Efluent treatment

32

Thanks!