�� Flexible budgets and variances help managers Flexible budgets and variances help managers gain insights into why the actual results differ gain insights into why the actual results differ from the planned performance.from the planned performance.

�� This chapter focuses on the difference of static This chapter focuses on the difference of static and flexible budgets and how budgets and flexible budgets and how budgets ––specifically flexible budgets specifically flexible budgets –– can be used to can be used to evaluate feedback on variances and aid evaluate feedback on variances and aid managers in their control function.managers in their control function.

11 Describe the difference between a static Describe the difference between a static budget and a flexible budgetbudget and a flexible budget

22 Illustrate how a flexible budget can be Illustrate how a flexible budget can be developed and calculate flexibledeveloped and calculate flexible--budget and budget and salessales--volume variancesvolume variances

33 Interpret the price and efficiency variancesInterpret the price and efficiency variancesfor directfor direct--cost input categoriescost input categories

4.4. Explain why purchasingExplain why purchasing––performance performance measures should focus on more factors than measures should focus on more factors than just price variances for inputsjust price variances for inputs

5.5. Describe benchmarking and how it can be Describe benchmarking and how it can be used by managers in variance analysisused by managers in variance analysis

Static and Flexible BudgetsStatic and Flexible Budgets

�� A static budget is a budget prepared forA static budget is a budget prepared foronly one level of activity.only one level of activity.

�� It is based on the level of output plannedIt is based on the level of output plannedat the start of the budget period.at the start of the budget period.

�� The master budget is an example of aThe master budget is an example of astatic budget.static budget.

Static and Flexible Budgets Static and Flexible Budgets (Continued)(Continued)

�� A flexible budget is developed using budgeted A flexible budget is developed using budgeted revenues or cost amounts based on the level of revenues or cost amounts based on the level of output actually achieved in the budget period.output actually achieved in the budget period.

�� A key difference between a A key difference between a flexible budgetflexible budgetand a and a static budget static budget is the use of the actual is the use of the actual output level in the flexible budget.output level in the flexible budget.

�� Budgeted selling price is Budgeted selling price is €€155 per suit.155 per suit.�� Fixed manufacturing costs are expected to be Fixed manufacturing costs are expected to be

€€286,000 within a relevant range between 286,000 within a relevant range between 9,000 and 13,500 suits.9,000 and 13,500 suits.

�� Variable and fixed Variable and fixed period costs period costs are ignored in are ignored in this example.this example.

�� The static budget for the year 2000 is based on The static budget for the year 2000 is based on selling 13,000 suits.selling 13,000 suits.

�� What is the staticWhat is the static--budget operating profit?budget operating profit?

�� Assume that LSY produced and sold 10,000 suitsAssume that LSY produced and sold 10,000 suitsat at €€160 each with actual variable costs of 160 each with actual variable costs of €€120 per 120 per suit and fixed manufacturing costs of suit and fixed manufacturing costs of €€300,000.300,000.

�� A staticA static--budget variance is the difference budget variance is the difference between an actual result and a budgeted between an actual result and a budgeted amount in the static budget.amount in the static budget.

�� Level 0 analysis compares actual operating Level 0 analysis compares actual operating profit with budgeted operating profit.profit with budgeted operating profit.

�� Level 1 analysis provides more detailed Level 1 analysis provides more detailed information on the operating profitinformation on the operating profitstaticstatic--budget variance.budget variance.

�� A favourable variance is a variance that A favourable variance is a variance that increases operating profit relative to the increases operating profit relative to the budgeted amount.budgeted amount.

�� An unfavourable variance is a variance that An unfavourable variance is a variance that decreases operating profit relative to the decreases operating profit relative to the budgeted amount.budgeted amount.

�� A favourable variance for revenue items A favourable variance for revenue items means that actual revenues exceededmeans that actual revenues exceededbudgeted revenues.budgeted revenues.

�� A favourable variance for cost items means A favourable variance for cost items means that actual costs were less than budgeted costs.that actual costs were less than budgeted costs.

Steps in Developing Steps in Developing Flexible BudgetsFlexible Budgets

�� Step 1Step 1: Determine budgeted selling price, : Determine budgeted selling price, budgeted variable cost per unit and budgeted variable cost per unit and budgeted fixed cost.budgeted fixed cost.

�� The budgeted selling price is The budgeted selling price is €€155, the 155, the budgeted variable cost is budgeted variable cost is €€115 per suit and 115 per suit and the budgeted fixed cost is the budgeted fixed cost is €€286,000.286,000.

�� Step 2Step 2: Determine the actual quantity of : Determine the actual quantity of output.output.

�� 10,000 suits were produced and sold in the 10,000 suits were produced and sold in the year 2000.year 2000.

�� Step 3Step 3: Determine the flexible budget for : Determine the flexible budget for revenues based on budgeted selling revenues based on budgeted selling price and actual quantity of output. price and actual quantity of output.

�� Step 4Step 4: Determine the flexible budget for : Determine the flexible budget for costs based on budgeted variable costs costs based on budgeted variable costs per output unit, actual quantity of per output unit, actual quantity of output and the budgeted fixed costs.output and the budgeted fixed costs.

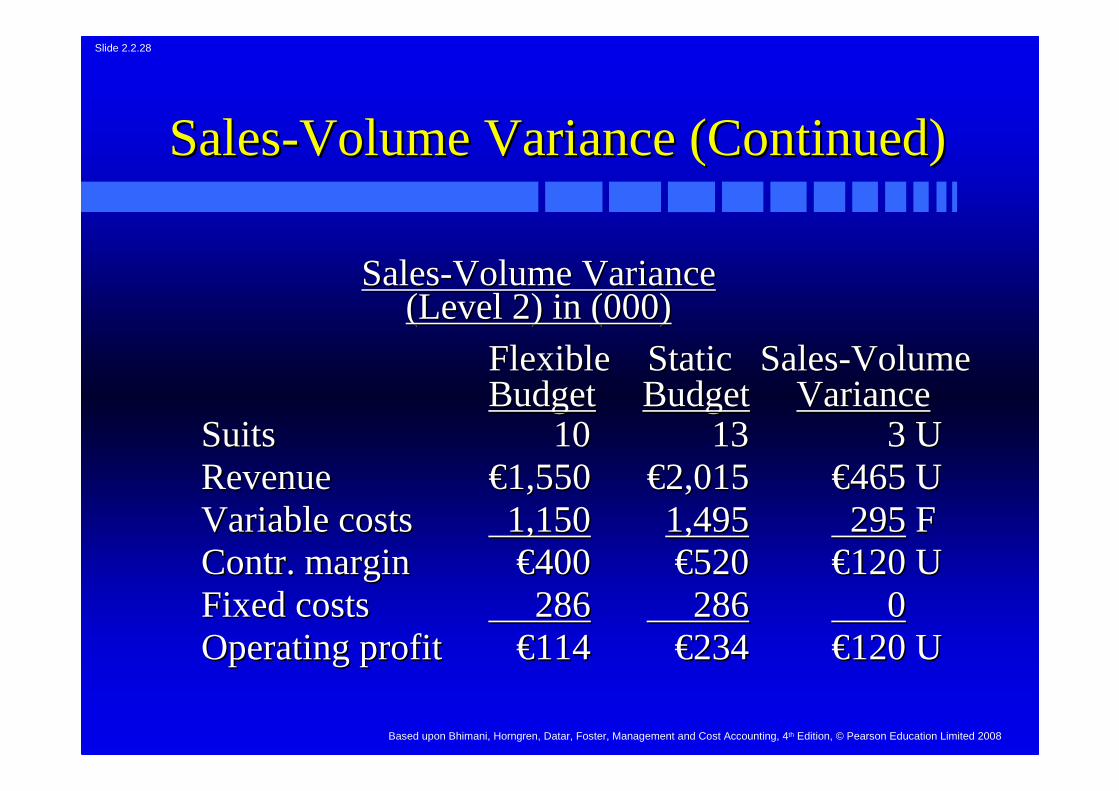

�� Level 2 analysis provides information on the Level 2 analysis provides information on the two components of the statictwo components of the static--budget variance.budget variance.

�� The flexibleThe flexible--budget variance arises because budget variance arises because the actual selling price, variable costs per the actual selling price, variable costs per unit, quantities and fixed costs differ fromunit, quantities and fixed costs differ fromthe budgeted amount.the budgeted amount.

�� Actual Budgeted Actual Budgeted Amount Amount AmountAmount

�� The flexibleThe flexible--budget variance pertaining to budget variance pertaining to revenues is often called a revenues is often called a sellingselling--price price variancevariance because it arises solely from because it arises solely from differences between the actual selling price differences between the actual selling price and the budgeted selling price.and the budgeted selling price.

�� The salesThe sales--volume variance is the difference volume variance is the difference between the the static budget for the number between the the static budget for the number of units expected to be sold and the flexible of units expected to be sold and the flexible budget for the number of units that were budget for the number of units that were actually sold. actually sold.

�� The only difference between the static The only difference between the static budget and the flexible budget is the output budget and the flexible budget is the output level upon which the budget is based.level upon which the budget is based.

Price and Efficiency VariancesPrice and Efficiency Variances

�� Level 3 analysis separates the flexibleLevel 3 analysis separates the flexible--budget budget variance into price and efficiency variances.variance into price and efficiency variances.

�� The following relates to LSY:The following relates to LSY:

�� Direct materials purchased and used: Direct materials purchased and used: 42,500 square metres42,500 square metres

�� Actual price paid per metres: Actual price paid per metres: €€15.9515.95

Price and Efficiency Variances Price and Efficiency Variances (Continued)(Continued)

�� Actual direct manufacturing labourActual direct manufacturing labour--hours: hours: 21,50021,500

�� Actual price paid per hour: Actual price paid per hour: €€12.9012.90�� What is the actual cost of direct materials?What is the actual cost of direct materials?�� 42,500 42,500 ×× €€15.95 15.95 == €€677,875677,875�� What is the actual cost of directWhat is the actual cost of direct

�� A price variance is the difference between the A price variance is the difference between the actual price and the budgeted price of inputs actual price and the budgeted price of inputs multiplied by the actual quantity of inputs.multiplied by the actual quantity of inputs.

–– InputInput--price varianceprice variance

–– Rate varianceRate variance

�� Price variance Price variance == (Actual price of inputs (Actual price of inputs –– Budgeted price of inputs) Budgeted price of inputs) ×× ActualActualquantity of inputs.quantity of inputs.

Actual QuantityActual Quantity Actual QuantityActual Quantityof Inputs atof Inputs at of Inputs atof Inputs atActual Price Actual Price Budgeted PriceBudgeted Price

Actual QuantityActual Quantity Actual QuantityActual Quantityof Inputs atof Inputs at of Inputs atof Inputs atActual PriceActual Price Budgeted PriceBudgeted Price

�� What is the journal entry when the materials What is the journal entry when the materials price variance is isolated at the time of price variance is isolated at the time of purchase?purchase?

�� Materials Control Materials Control 690,625 690,625 Direct Materials Price VarianceDirect Materials Price Variance12,750 12,750 Accounts Payable ControlAccounts Payable Control 677,875 677,875

To record direct materials purchased.To record direct materials purchased.

�� What may be some of the possible causes What may be some of the possible causes for LSYfor LSY’’ s favourable price variances?s favourable price variances?

–– LSYLSY’’ s purchasing manager negotiated more s purchasing manager negotiated more skilfully than was planned.skilfully than was planned.

–– Labour prices were set without careful Labour prices were set without careful analysis of the market.analysis of the market.

�� The efficiency variance is the difference The efficiency variance is the difference between the actual and budgeted quantity of between the actual and budgeted quantity of inputs used multiplied by the budgeted price inputs used multiplied by the budgeted price of input.of input.

�� Efficiency variance Efficiency variance == (Actual quantity of (Actual quantity of inputs used inputs used –– Budgeted quantity of inputs Budgeted quantity of inputs allowed for actual output) allowed for actual output) ×× Budgeted price Budgeted price of inputs.of inputs.

�� What is the journal entry to record materials What is the journal entry to record materials used?used?

�� WorkWork--inin--Progress ControlProgress Control 650,000 650,000 Direct Materials Efficiency Direct Materials Efficiency VarianceVariance 40,625 40,625 Materials Control Materials Control 690,625 690,625

To record direct materials used.To record direct materials used.

�� What may be some of the causes for LSYWhat may be some of the causes for LSY’’ s s unfavourable efficiency variances?unfavourable efficiency variances?

–– LSYLSY’’ s purchasing manager received lower s purchasing manager received lower quality of materials.quality of materials.

Price and Efficiency VariancesPrice and Efficiency Variances

�� What is the journal entry for direct manufacturing What is the journal entry for direct manufacturing labour?labour?

�� WorkWork--inin--Progress ControlProgress Control 260,000 260,000 Direct Manufacturing Labour Direct Manufacturing Labour Efficiency VarianceEfficiency Variance 19,500 19,500

Direct Manufacturing Direct Manufacturing Labour Price Variance Labour Price Variance 2,150 2,150 Wages PayableWages Payable 277,350 277,350

To record liability for direct manufacturing labour.To record liability for direct manufacturing labour.

Price and Efficiency Variances Price and Efficiency Variances (Continued)(Continued)

�� What is the flexibleWhat is the flexible--budget variance for direct budget variance for direct materials?materials?

�� MaterialsMaterials--price variance price variance €€12,750 F +12,750 F +MaterialsMaterials--efficiency variance efficiency variance €€40,625 U 40,625 U ==€€27,875 U27,875 U

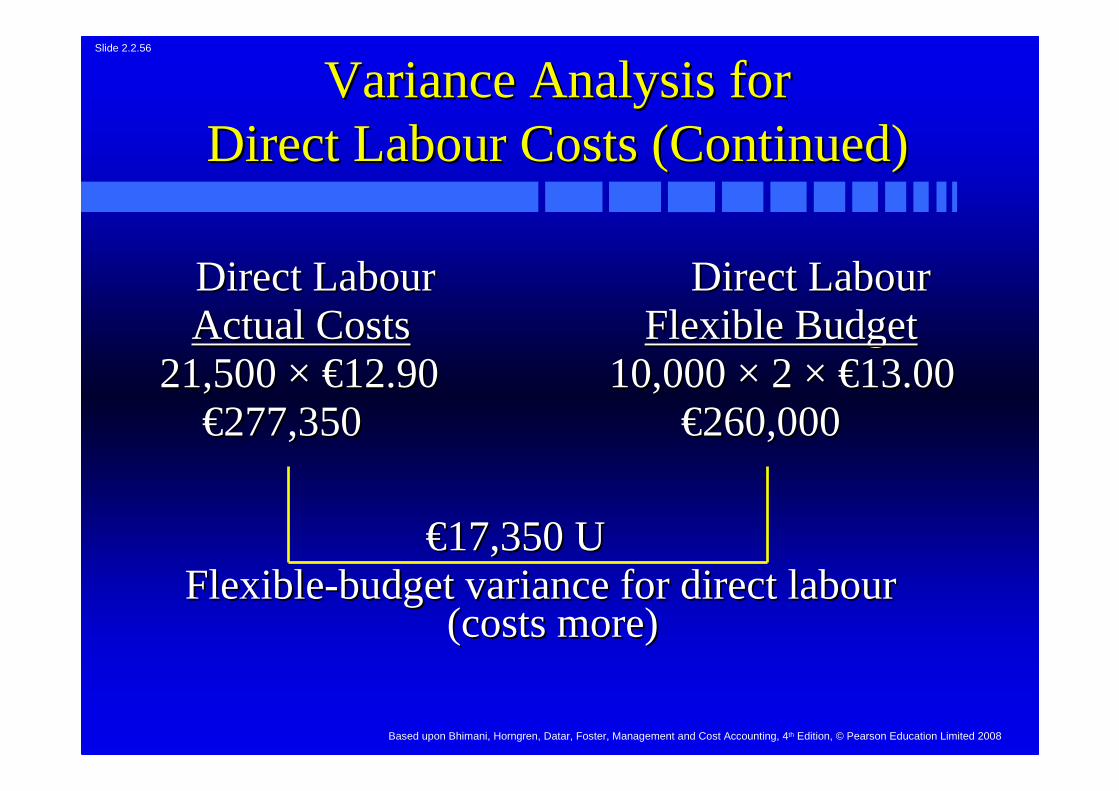

�� What is the flexibleWhat is the flexible--budget variance for direct budget variance for direct manufacturing labour?manufacturing labour?

�� LabourLabour--price variance price variance €€2,150 F + Labour2,150 F + Labour--efficiency efficiency variance variance €€19,500 U 19,500 U == €€17,350 U17,350 U

�� EffectivenessEffectiveness is the degree to which a is the degree to which a predetermined objective or target is met.predetermined objective or target is met.

�� EfficiencyEfficiency is the relative amount of inputs is the relative amount of inputs used to achieve a given level of output.used to achieve a given level of output.

�� Variances should not solely be used to Variances should not solely be used to evaluate performance.evaluate performance.

�� If any single performance measure, such as a If any single performance measure, such as a labour efficiency variance, receives excessive labour efficiency variance, receives excessive emphasis, managers tend to make decisions emphasis, managers tend to make decisions that maximise their own reported performance that maximise their own reported performance in terms of that single performance measure.in terms of that single performance measure.

Multiple Causes of VariancesMultiple Causes of Variances

�� Often the causes of variances are interrelated.Often the causes of variances are interrelated.

�� A favourable price variance might be due to A favourable price variance might be due to lower quality materials.lower quality materials.

�� It is best to always consider possible It is best to always consider possible interdependencies among variances and to not interdependencies among variances and to not interpret variances in isolation of each other.interpret variances in isolation of each other.

When to Investigate VariancesWhen to Investigate Variances

�� When should variances be investigated?When should variances be investigated?�� Frequently, managers base their answer on Frequently, managers base their answer on

subjective judgements.subjective judgements.�� For critical items, a small variable may For critical items, a small variable may

prompt followprompt follow--up.up.�� For other items, a minimum monetary For other items, a minimum monetary

variance or a certain percentage of variance variance or a certain percentage of variance from budget may prompt an investigation.from budget may prompt an investigation.

Benchmarking refers to the continuous process Benchmarking refers to the continuous process of measuring products, services and activities of measuring products, services and activities against the best levels of performance.against the best levels of performance.

�� The best levels of performance are often found The best levels of performance are often found in competing organisations or in other in competing organisations or in other organisations having similar processes.organisations having similar processes.

�� Companies should ensure that the benchmark Companies should ensure that the benchmark numbers are comparable.numbers are comparable.

Benchmarking facilitates companies using Benchmarking facilitates companies using the best levels of performance within their the best levels of performance within their organisation, in competitor organisations organisation, in competitor organisations or at other nonor at other non--competitor organisations to competitor organisations to gauge the performance of their own gauge the performance of their own managers.managers.